China's Innovative Drug Sector Sees Listing Boom and Seven Major Domestic Drugs Approved in 2019, Marking a Return to Steady Growth

In 2019, the total volume of investment and financing in China’s innovative drug sector declined. Amid a broader cooling of the investment and financing environment, even innovative drugs—the hottest segment within the healthcare industry—were not spared.

In 2018, domestically produced innovative drugs in China experienced a surge, and this momentum continued into 2019. However, in terms of investment and financing, as capital inflows tightened, investors began to take a more rational approach to the innovative drug sector in 2019, squeezing out the hype-driven bubble that had formed in 2018.

VCBeat Reviews Data and Analyzes the Environment to Summarize Five Key Points in the Innovative Drug Sector for 2019:

1. Investment and financing activities have declined somewhat compared with 2018, but remain on the stable growth trajectory observed during 2015–2017;

2. Multiple landmark products received approval, achieving a breakthrough from zero for Chinese-made innovative drugs going global and marking their entry into the international market;

3. Production of large-molecule biosimilars has commenced, with key products achieving domestic manufacturing;

4. The successful implementation of the "vacating the cage to change the bird" strategy in medical insurance has led to the large-scale inclusion of new and specialized drugs in the coverage;

5. The opening of the STAR Market, the surge in popularity of Hong Kong stocks, and the large-scale listing of innovative drug companies.

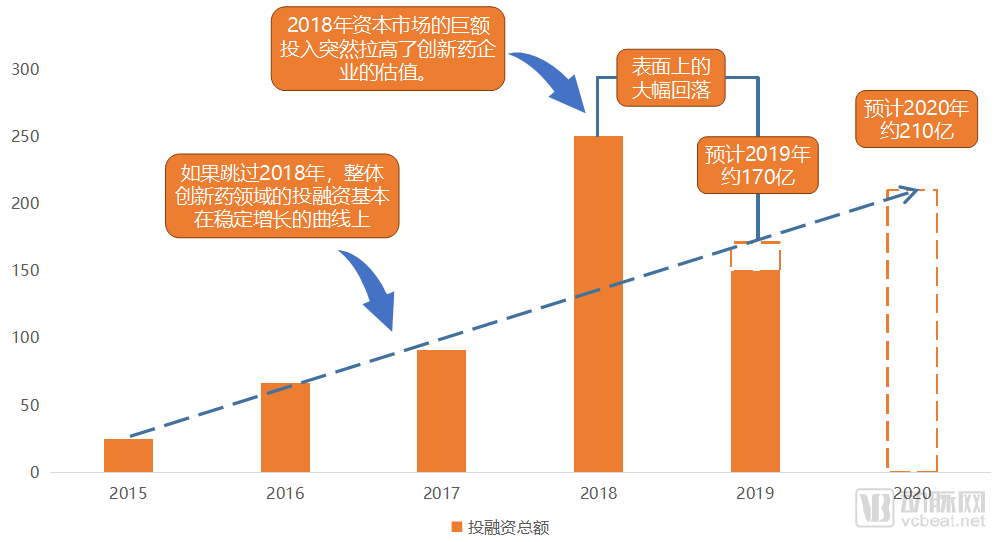

Total Investment and Financing in the Innovative Drug Sector

This year, there has been widespread discussion about the cooling of investment in innovative drugs. Indeed, according to data from the VCBeat knowledge base, as of November 15, total financing for innovative drug ventures amounted to less than RMB 15 billion, compared with 2018. Full-year investment and financing are projected to decline by 32%, from RMB 25 billion in 2018 to RMB 17 billion.

However, if we exclude 2018 from consideration, the period spanning 2015–2017 and 2019 shows that financing and investment in innovative drugs actually followed a relatively steady upward trajectory. Therefore, rather than characterizing 2019 as a year of cooling investment in innovative drugs, it is more accurate to say that investment in 2018 was excessively overheated, making it unsustainable for 2019 to maintain the same level as the corresponding period in 2018.

We project that total investment and financing for the full year of 2019 will reach RMB 17 billion. In the following year, 2020, investment and financing in China’s innovative drug sector is expected to continue growing compared with 2019, with full-year totals projected at RMB 20–21 billion.

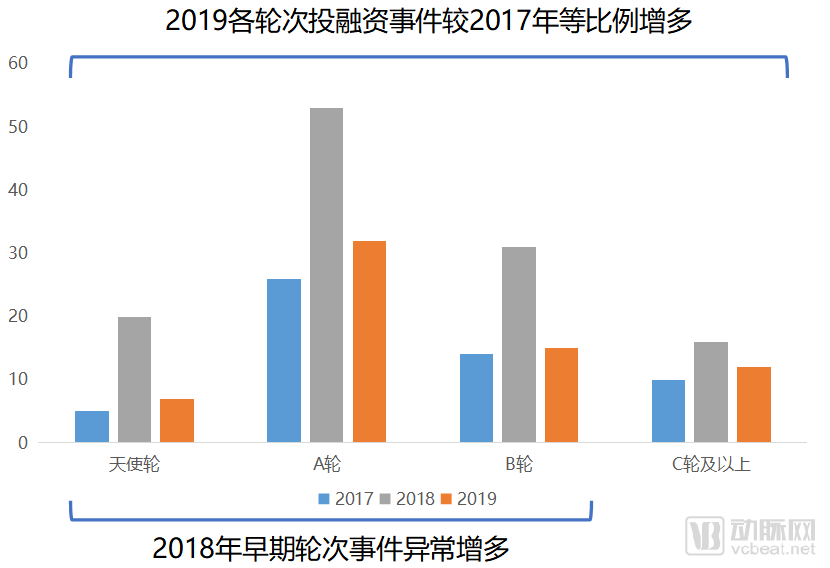

Distribution of Investment and Financing Rounds in the Innovative Drug Sector

From the perspective of investment and financing structure, it is evident that the distribution of funding rounds in 2019 more closely resembled that of 2017, whereas 2018 saw a significant shift toward earlier-stage rounds. As the investment climate cooled in 2019, the distribution of funding rounds returned to a normal pattern. This indicates that the innovative drug sector has become a stably operating niche market.

Key Factors Influencing Changes in Investment and Financing in the Innovative Drug Sector Over the Past Two Years

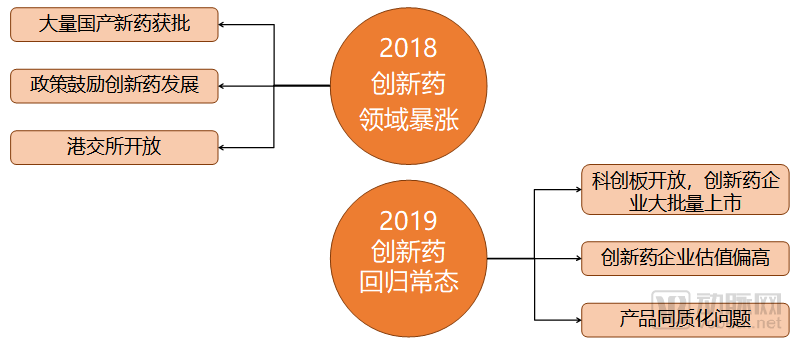

For most industries, the 2019 capital winter may have been a devastating snowstorm, but for the innovative drug sector, it was more akin to a beneficial remedy. Adjusted by multiple unfavorable factors, the innovative drug field ended the irrationality of 2018 and set sail once again in 2019.

In 2019, the funding shortage in the venture capital sector prompted investors to reassess their investment and financing decisions in the innovative drug field with greater restraint, rather than making large-scale investments as they did in 2018. Driven by the momentum of 2018, the innovative drug sector indeed saw significant bubble formation; however, many investors we engaged with indicated that although a bubble existed, it had largely been deflated by the market conditions in 2019. Thus, while complaining about the high valuations of innovative drug companies, investors remained willing to channel capital into the sector.

Product homogenization is arguably the most significant challenge currently facing the innovative drug sector, with PD-1 monoclonal antibodies being the most typical example. The four domestically produced PD-1 monoclonal antibodies that had submitted New Drug Applications (NDA) have all been approved. However, according to our previous statistics, nearly 20 different PD-1 monoclonal antibodies are still in clinical development. Unless these products in clinical stages can demonstrate significant differences in efficacy compared to previously approved agents, they will struggle to gain a foothold in the market.

Domestically Developed Innovative Drugs Approved in 2019

Compared with 2018, domestically produced innovative drugs in 2019 failed to maintain the explosive growth seen in 2018. Nevertheless, each product still demonstrated high intrinsic value.

Following the 2018 market launches of Junshi Biosciences’ Tuoyi and Innovent Biologics’ Tyvyt, Hengrui Medicine’s and BeiGene’s PD-1 monoclonal antibodies were also approved in 2019. With this, all four domestically produced PD-1 monoclonal antibody products that had submitted New Drug Applications (NDAs) have now been launched, marking the formal entry of competition into the phase of indication expansion.

Six PD-1 Monoclonal Antibodies Approved in China

In terms of indication expansion, Keytruda has taken the lead, with three new lung cancer-related indications approved in 2019. Moreover, Keytruda’s global sales for the first three quarters of 2019 had already reached $7.973 billion, virtually securing annual sales exceeding $10 billion and potentially surpassing lenalidomide to become the second best-selling drug worldwide.

In the recently announced list of drugs included in the national medical insurance negotiations, the status of PD-1 monoclonal antibodies has undergone a major reversal. It was widely expected that at least two domestic brands would voluntarily reduce prices to gain inclusion in the national medical insurance coverage; however, ultimately, only Innovent Biologics’ sintilimab successfully passed the negotiation. The original price of sintilimab was RMB 7,838 per 100 mg, with an annual treatment cost of approximately RMB 167,000 after accounting for patient assistance programs. With its inclusion in the national medical insurance, the annual treatment cost for sintilimab has dropped to around RMB 100,000, representing a further 40% reduction compared to the patient assistance program pricing.

With the approval of all first-tier PD-1 monoclonal antibodies, opportunities for other domestic developers appear increasingly slim. Companies with products nearing market launch may still find openings through new indications or combination therapies, while those in preclinical or early clinical stages will struggle to gain a foothold. It is hoped that this “bandwagon” approach to R&D will serve as a lesson for Chinese innovative drug companies, encouraging them to pursue truly distinctive innovation opportunities.

The other four domestically developed innovative drugs approved in 2019 each have their unique characteristics. Hansoh Pharmaceutical achieved two major milestones this year: first, losenatide and Eli Lilly’s dulaglutide were successively approved, joining the previously approved exenatide microspheres as long-acting GLP-1 receptor agonists, forming a tripartite competitive landscape; by year-end, flumatinib was also approved for marketing, with Phase III clinical trial results demonstrating superiority over imatinib (Gleevec). Benvitimod, as China’s first approved dermatological “First-in-Class” new drug, has seen numerous patients share their treatment outcomes online, with the majority reporting significant therapeutic efficacy.

Compared with several other drugs, GV-971, which was approved at the end of the year, has sparked significant controversy. According to the experimental results disclosed for GV-971, data based on the ADAS-cog12 scale showed a difference of 2.54 points in the relative change between the treatment group and the placebo group after 36 months of therapy. Regardless of whether there are issues with the data curves presented in the trial results, from the perspective of the ADAS-cog12 scale alone—with a total score of 70 or 75 points—an improvement of 2.54 points indicates that the drug’s efficacy is minimal. Consequently, the approval of this drug by the Center for Drug Evaluation (CDE) has generated substantial debate. However, given the current situation, we can only hope that GV-971 will demonstrate superior efficacy in post-marketing use compared to its performance in clinical trials.

In addition to its domestic approval, Zanubrutinib achieved a historic breakthrough this year by becoming the first Chinese-developed innovative drug to gain regulatory approval overseas. During the approval process, Zanubrutinib set several precedents, such as being the first to rely primarily on domestic clinical trial data as a key basis for approval and marking the first time that U.S. FDA inspectors conducted on-site evaluations at clinical trial sites in China. With this milestone, Zanubrutinib has officially propelled Chinese innovative drugs into the global arena.

Key Policies in the Innovative Drug Sector in 2019

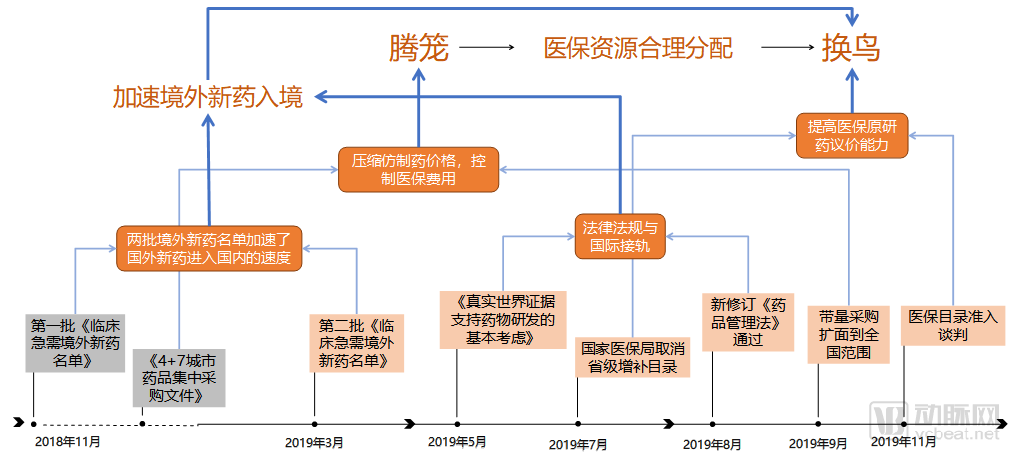

A major development has finally come to fruition in recent days. The national medical insurance reimbursement negotiations, originally scheduled for November 11–13, were extended to the 15th. This round of negotiations included an unprecedented 150 therapeutic categories. Ultimately, 70 new drugs successfully gained inclusion, and 27 existing drugs secured contract renewals. Following volume-based procurement and large-scale reimbursement negotiations, China’s “cage-swapping” strategy—replacing older treatments with innovative ones—has reached a milestone and demonstrated significant effectiveness.

The National Reimbursement Drug List (NRDL) access negotiations, initiated in 2017, have now been conducted for three years. The drugs subject to the current round of negotiations include not only a large number of new and specialty medicines approved before 2018 that were previously excluded from NRDL coverage, but also the renewal of contracts for drugs successfully included through the 2017 negotiations. For certain drugs in this round of negotiations, the enhanced bargaining power of the National Healthcare Security Administration (NHSA) has already become evident following the abolition of provincial-level drug catalogs.

The most notable example is the blockbuster drug Humira (adalimumab). In 2018, adalimumab was priced at approximately RMB 7,600 per pre-filled syringe. In 2019, its price was reduced by 60% across various provinces and municipalities in China as it was included in local medical insurance reimbursement lists, with a uniform winning bid price of RMB 3,160 per syringe. In the latest national medical insurance negotiation, the price of adalimumab dropped further to RMB 1,290 per syringe, making it nearly the lowest globally.

However, the National Healthcare Security Administration’s negotiations on PD-1 monoclonal antibodies did not achieve significant success. Among the four drugs, only Innovent Biologics’ sintilimab was included in the final list. This outcome may be attributed to sintilimab having the fewest new indications currently under application with the Center for Drug Evaluation (CDE).

This year marks the first round of negotiations following the abolition of local medical insurance catalogs. Neither the national medical insurance authorities nor innovative pharmaceutical companies have yet been able to accurately assess their respective bargaining power in this new environment, leading to frequent disagreements and an inability to reach consensus. Drugs that fail to pass these negotiations will have another opportunity during the next round of medical insurance access negotiations at the end of 2020. After a year of observation, both parties are expected to have a clearer understanding of their relative negotiating positions, ultimately enabling more drugs to be included in the National Reimbursement Drug List at prices acceptable to both sides.

In terms of expanding medical insurance coverage, from the pilot launch of the centralized drug procurement program in late 2018 to its nationwide rollout in September 2019, traditional generic drug manufacturers have gradually realized that the business model they once relied on for survival has vanished, replaced by a dilemma. Joining the national medical insurance list means razor-thin profits, while staying out means no market access. Standing at a crossroads of fate, these generic drug companies are looking around but cannot see a clear direction for the future.

Regardless of how these companies develop, the National Healthcare Security Administration (NHSA) has achieved a modest objective with this policy. The inflated prices of generic drugs have been significantly reduced, freeing up space within the medical insurance budget to accommodate new therapies. However, upon surveying the landscape, the NHSA found few suitable candidates to fill this newly available capacity. Consequently, encouraging the entry of urgently needed overseas innovative drugs into the domestic market has become the quickest way to populate this space. Many enterprises had been making solid progress in generic drug development, but the sudden release of the list of overseas new drugs caught them off guard, disrupting their strategic plans.

Following a series of initiatives in 2019, the strategy of “phasing out low-value products to make room for high-value innovations” has begun to yield results. In the future, more funds saved from generic drugs will be allocated to innovative medicines, thereby addressing medication needs for a greater number of patients.

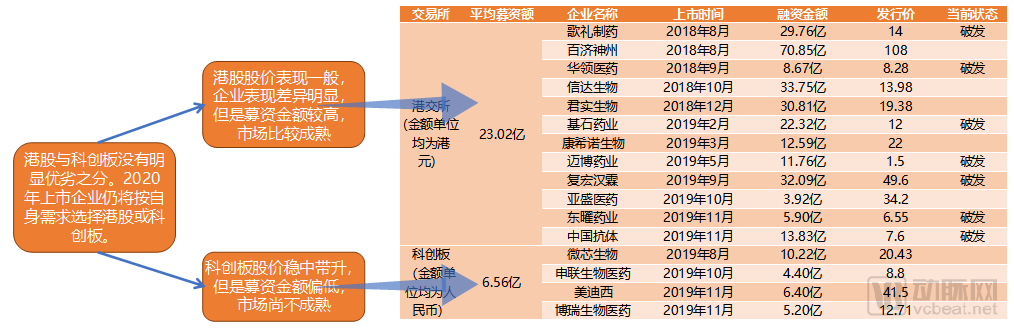

Innovative drug companies listed on the STAR Market and the Hong Kong Stock Exchange in the past two years (including one CRO and one API manufacturer)

In April 2018, the Hong Kong Stock Exchange (HKEX) opened its doors to pre-revenue biotechnology companies, sparking a wave of IPOs. Companies that would otherwise have continued to navigate the primary market for several years swiftly adjusted their strategies to list in Hong Kong. Starting with Ascletis Pharma’s listing on August 1, 2018, five unprofitable biopharmaceutical companies were listed on the HKEX by the end of 2018, underscoring the market’s strong appeal. Consequently, in November 2018, the China Securities Regulatory Commission (CSRC) announced the establishment of the STAR Market on the Shanghai Stock Exchange, fully opening China’s secondary market to innovative drugs.

Thus, in 2019, the successive openings of the Hong Kong stock market and the STAR Market successfully kept domestic enterprises within China. Eleven innovative drug companies made their mark on China’s secondary capital markets in rapid succession.

Among the companies queued for listing on the STAR Market are Lead Pharma, Bio-Thera Solutions, and several others. Meanwhile, firms that secured substantial financing in the past two years, such as Harbour Biomed and InnoCare Pharma, have yet to announce their IPO plans, while InnoCare has just submitted its prospectus to the Hong Kong Stock Exchange. This wave of IPO enthusiasm in 2019 is highly likely to continue into 2020.

Amidst the boom, listed innovative drug companies have experienced both triumphs and setbacks. Among the 12 companies listed on the Hong Kong Stock Exchange, seven saw their share prices fall below the IPO price. The remaining five are: Junshi Biosciences and Innovent Biologics, the twin stars of domestic PD-1 inhibitors; BeiGene, which has launched its self-developed new drugs in the U.S. market; CanSino Biologics, a leader in innovative vaccines; and Ascentage Pharma, the first small-molecule novel drug company to go public.

It is evident that the Hong Kong stock market has adopted a stringent stance toward innovative drug companies still in the R&D phase. Companies endorsed by the Hong Kong market demonstrate strong market appeal on paper, while those with uncertain prospects—even China Biologics, a local Hong Kong firm—have not escaped the fate of trading below their IPO price.

In contrast to the Hong Kong stock market, mainland Chinese investors are in a state of widespread jubilation. Four innovative drug stocks on the STAR Market, including CRO firm Medicilon and API manufacturer Borui Pharmaceutical, have performed well, with Chipscreen Biosciences surging 511% on its first day of trading. Mainland investors have warmly welcomed innovative drug companies, suggesting that both capital markets and enterprises are highly satisfied. However, how long the STAR Market’s momentum will last, and whether the sharp surge reflects another instance of market “irrationality,” remains to be seen as the market self-corrects.

On the other hand, companies listed on the STAR Market generally raise relatively small amounts of capital. Chipscreen Biosciences, which raised the largest amount, only just exceeded RMB 1 billion. Compared with the Hong Kong stock market, where the average fundraising amount exceeds HKD 2 billion, the Shanghai Stock Exchange tends to assign more conservative valuations to companies. This is why we witnessed the remarkable moment when Chipscreen Biosciences’ share price surged fivefold on its trading debut. However, impressive as this was, the fundraising capacity of the STAR Market is indeed somewhat inadequate for large innovative pharmaceutical companies whose products are in the final sprint phase and require substantial financial support.

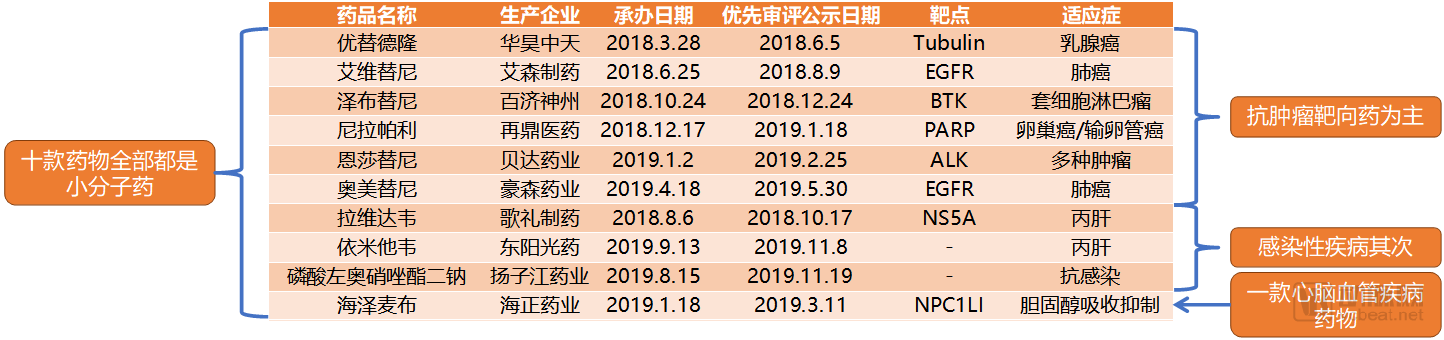

Top 10 Domestic Innovative Drugs Expected to Gain Approval in China in 2020

Following the market launch of more than a dozen domestically produced innovative drugs in 2018–2019, the number of such drugs remaining in the priority review queue has been steadily decreasing. Among the ten domestically produced innovative drugs identified from the priority review list that are expected to be launched in 2020, all are small-molecule drugs. Meanwhile, domestically produced large-molecule innovative drugs have temporarily quieted down after the completion of all New Drug Applications (NDAs) for PD-1 monoclonal antibodies.

Small-molecule targeted drugs still primarily follow a fast-follower innovation strategy in target selection, such as the third-generation EGFR inhibitors almonertinib and osimertinib; flumatinib, a drug in the same class as imatinib; and the ALK inhibitor ensartinib. Among these, zanubrutinib stands out for its high value; following its FDA approval, domestic approval in China is expected to be imminent.

In recent years, the global surge in antibody drugs has pushed small-molecule targeted therapies into a brief downturn. However, as time has passed, challenges associated with large-molecule drugs—such as high difficulty in original research and development, long development cycles, and substantial costs—have begun to emerge. In contrast, after several years of consolidation, small-molecule drugs have maintained stable output efficiency.

Biologic Biosimilar Products of Major Antibody Drugs Submitted for Market Approval

However, large-molecule drugs will not fade into obscurity in 2020. The approval of two biosimilars in succession in 2019 ushered in an era of domestic production for key antibody drug products. Multiple companies are currently submitting New Drug Applications (NDAs) for biosimilars targeting several major therapeutic areas. Coupled with the pressure from national medical insurance reimbursement policies to reduce drug prices, biosimilars are well-positioned to meet this demand. We anticipate that the biosimilar sector may experience explosive growth in 2020.

Compared with innovative drugs, biosimilars have relatively clear development goals, shorter R&D cycles, stable market sizes, and higher launch efficiency, enabling faster capital recovery. Due to the high barriers associated with large-molecule drugs, biosimilars are less likely to face the intense competition from numerous me-too products that is common among generic small-molecule drugs. Moreover, developing biosimilars helps teams accumulate R&D experience, laying the groundwork for innovative drug development. Therefore, the strategies of “imitation before innovation” and “driving innovation through imitation” have become widely accepted industry norms in the field of antibody drug development, representing a relatively smooth path for corporate growth in the current domestic environment.

During the national medical insurance reimbursement negotiations at the end of 2019, adalimumab was successfully included in the reimbursement list, while trastuzumab and bevacizumab successfully renewed their contracts. Biosimilars of these originator drugs are treated similarly to generic drugs during the medical insurance access process; they can be included in the reimbursement scope through straightforward discussions on payment standards with the medical insurance authorities, and their indications are fully consistent with those of the originator products.

Nearly all leading domestic antibody drug companies have included some biosimilar pipelines. Even international pharmaceutical giants (such as Pfizer) are engaged in biosimilar development. Based on the products that have already submitted NDA applications, Henlius and Innovent Biologics both have multiple products at the forefront of the queue, and they are likely to reap significant rewards next year.

1. Investment and financing conditions have continued to improve compared with 2019, but are unlikely to exceed the levels of the same period in 2018;

In 2019, overall investment and financing in innovative drugs returned to a normal growth trajectory, with the distribution pattern remaining largely stable. Therefore, it is projected that the innovative drug sector will continue to grow along this previous trajectory in 2020, with total investment and financing expected to reach RMB 20–21 billion.

2. The return of domestically developed innovative drugs to small molecules has driven up interest in the small-molecule drug sector;

According to our statistics, domestic innovative drugs still in the priority review queue are almost exclusively small-molecule drugs. The top ten domestic innovative drugs we listed as potentially launching in 2020 are all small-molecule agents. Therefore, it is foreseeable that small-molecule innovative drugs will constitute the mainstay of approvals in 2020, thereby driving up interest in the small-molecule drug sector.

3. Macromolecule biosimilars will experience explosive growth, with most key products achieving domestic production;

With the opening of the floodgates for large-molecule biosimilars in 2019, more biosimilars are expected to gain approval in 2020. Following the approval of the first biosimilar products for rituximab and adalimumab, biosimilars for other key agents are likely to be gradually approved throughout 2020. An increasing number of innovative drugs are entering the domestic production pipeline.

4. The “vacating the cage to change the bird” strategy in medical insurance continues to advance, with more innovative drugs being included in the national reimbursement list;

Volume-based procurement was expanded nationwide in September 2019, making the further expansion of this policy a key focus for the National Healthcare Security Administration (NHSA) in 2020. Meanwhile, the large-scale national reimbursement drug list (NRDL) access negotiations organized at the end of 2019 covered a substantial number of drugs approved by the end of 2018. Such negotiations are likely to become an annual occurrence, thereby accelerating the inclusion of innovative drugs into the NRDL.

5. Listed companies choose between the STAR Market and the Hong Kong stock market based on their own needs, with the STAR Market gradually maturing in its development.

Amid the lack of significant improvement in China-U.S. trade frictions, the domestic market will remain the top choice for companies preparing to go public. The Hong Kong stock market and the STAR Market each have their own advantages in terms of listing requirements; it is expected that companies will continue to make choices based on their specific needs in 2020. As a hot sector in 2019, the STAR Market will gradually enter a phase of stable development in 2020 after the initial listing frenzy subsides.