FTC2019 | Haitong Securities' He Wenbin: Current Landscape and Unmet Needs in Cardiovascular Innovative Devices

Recently, the FTC 2019 Inaugural China Forum on Frontier Technologies in Cardiac Surgery, hosted by the Cardiac Surgery Professional Committee of the China Medical Education Association and the Cardiovascular Surgery Technology and Engineering Branch of the China Medical Biotechnology Association, co-organized by Da Yisheng Bingqipu, and undertaken by VCBeat, was held in Beijing.

Image source: Live photo streaming from the conference venue

The conference invited numerous experts and scholars to share their insights. Among them, He Wenbin, formerly a cardiovascular physician at Beijing Anzhen Hospital and currently a Senior Analyst at Haitong Securities, provided an in-depth analysis of his inaugural comprehensive report on innovative medical devices. VCBeat (WeChat ID: vcbeat) has compiled the transcript of his presentation on “Development Trends in Cardiovascular Device Innovation” for our readers.

1. Capital Markets Boost Medical Device Innovation

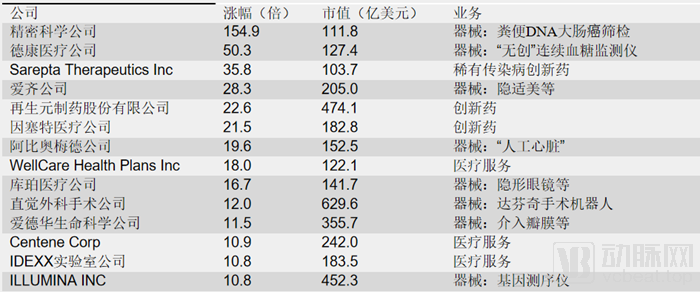

From the perspective of capital markets, U.S. stocks have seen a surge of high-performing medical device companies, warranting significant attention to innovation in China’s medical device sector. Over the past decade (January 1, 2009, to March 5, 2019), the U.S. stock market produced 14 pharmaceutical and healthcare stocks that achieved tenfold returns (with market capitalizations exceeding $10 billion). Among these, eight were innovative medical device companies, including star performers such as Intuitive Surgical (da Vinci Surgical Robot), Illumina (gene sequencers), DexCom (non-invasive continuous glucose monitors), and Align Technology (Invisalign). The remaining six comprised three innovative drug companies and three healthcare service providers.

From a business perspective, among the eight medical device companies, those specializing in cardiovascular and molecular diagnostics are the most numerous. Two focus primarily on innovative cardiovascular devices (Edwards Lifesciences, Abiomed), while two specialize in molecular diagnostics (Exact Sciences Corporation, Illumina Inc.), all operating in sectors characterized by substantial market potential and vigorous innovation.

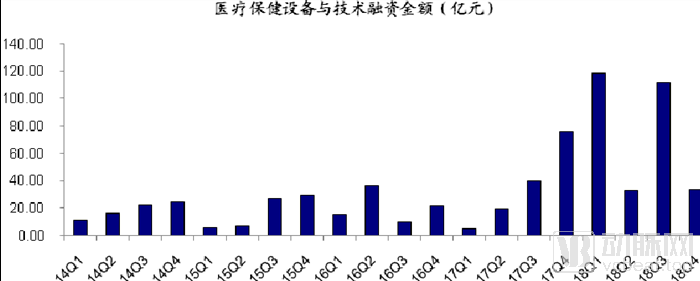

We compiled statistics on financing in the healthcare equipment and technology sector from the Wind PE/VC database, with total funding reaching RMB 29.605 billion in 2018, setting a new historical high.

2. Policy Environment

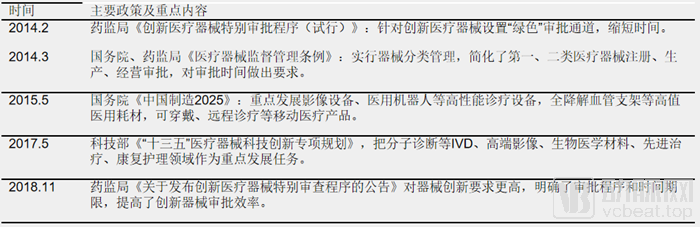

From a policy perspective, multiple initiatives have encouraged innovation, leading to a year-on-year increase in the number of approved medical devices. 2014 marked the first year of the second round of regulatory reforms in the medical device sector. This period saw the completion of the revision to the Regulations on the Supervision and Administration of Medical Devices, the overarching legislation for the industry that had been under review for many years. Additionally, four departmental rules were issued sequentially, becoming the most significant documents influencing industry development throughout the year. The new Regulations explicitly state that the state encourages research and innovation in medical devices, promotes the adoption and application of new technologies, and drives the development of the medical device industry. Furthermore, the Regulations introduced a series of specific institutional designs aimed at optimizing evaluation and approval processes, reducing corporate burdens, and fostering innovation. These measures have provided a strong legal basis and policy foundation for promoting the growth of the medical device industry and supporting enterprises in scaling up and strengthening their market position.

In 2014, the National Medical Products Administration (NMPA) also nearly simultaneously issued the “Special Examination Procedures for Innovative Medical Devices (Trial),” which established a “green channel” for the approval of innovative medical devices, shortened review timelines, and revolutionized the era of innovative medical device approvals. In November 2018, the NMPA officially released the “Announcement on Issuing the Special Examination Procedures for Innovative Medical Devices,” which raised higher requirements for device innovation based on the previous version, while clarifying the approval procedures and timeframes, thereby improving the efficiency of innovative device approvals.

Furthermore, the “Made in China 2025” initiative and the “13th Five-Year Plan for Scientific and Technological Innovation in Medical Devices,” issued by the State Council and the Ministry of Science and Technology, respectively, have also identified innovative medical devices as a key area of development, thereby further encouraging innovation in the medical device sector.

3. Approval Environment

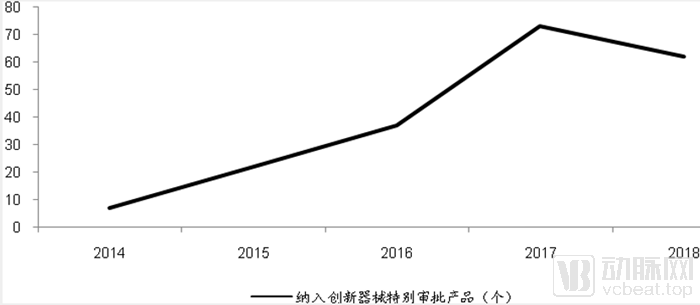

Since the launch of the Special Approval Procedure for Innovative Medical Devices in 2014, a total of 218 products had been included in this program as of February 28, 2019. The period from 2017 to 2018 witnessed explosive growth, with 73 and 62 products respectively admitted into the special approval process. In the first two months of 2019 alone, 17 products were already included, a figure significantly exceeding that of the same period in 2017–2018.

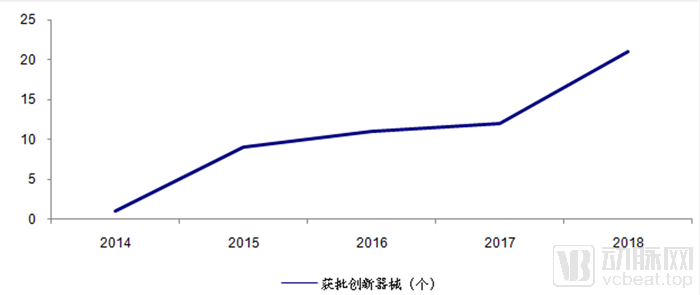

The number of approved innovative medical devices has been gradually increasing. As of February 28, 2019, a total of 57 innovative medical devices had received approval. Notably, 2018 witnessed explosive growth, with 21 innovative products approved, while three additional innovative medical devices were approved in the first two months of 2019. Since 2017, products included in the Special Approval Procedure for Innovative Medical Devices have seen a surge in numbers, laying a solid foundation for the wave of approvals observed after 2018. We believe that China has officially entered the era of innovative medical devices.

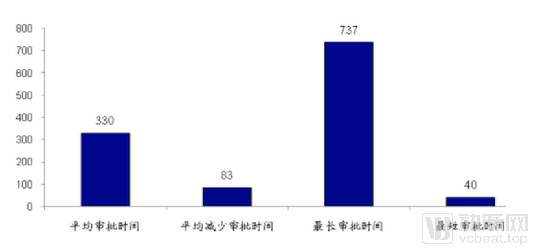

The average approval time for innovative medical devices is 330 days. We analyzed 22 approved innovative medical devices and found that the average approval time was approximately 330 days. The shortest approval time was 40 days for porous tantalum bone graft substitute, while the longest was 737 days for the miR-92a detection kit (fluorescent RT-PCR method). According to statistics from the China Food and Drug Administration (CFDA), the average approval time for innovative priority products was reduced by 83 days compared to other ordinary Class III first-time registration products, further shortening the time from research and development to market launch for innovative products.

4. Talent Issues

Over Two Decades of Talent Accumulation Lay the Foundation for Medical Device InnovationChina’s innovation in medical devices is inseparable from more than twenty years of accumulation in technical and managerial talent. This journey ranges from BioCapital, founded by Academician Cheng Jing, and early returnees from the United States such as Mr. Chang Zhaohua and Mr. Wang Jian, who established MicroPort Scientific Corporation and BGI Genomics, to recent returnees like Mr. Zhang Ji and Mr. Zheng Limou, who founded Jiecheng Medical and Amoy Diagnostics, as well as ventures born from collaborations between technology and capital, such as Venus Medtech and Xianjian Technology. Talent remains the cornerstone of innovation.

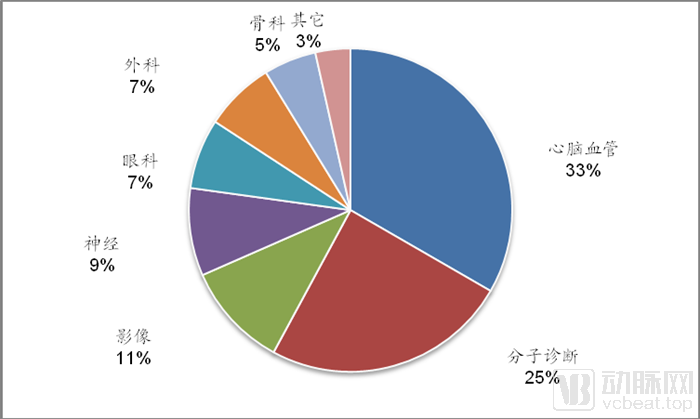

We analyzed 57 approved innovative medical devices (as of February 28, 2019), among which 19 were cardiovascular and cerebrovascular devices, accounting for 33%; molecular diagnostics and imaging devices numbered 14 and 6, respectively, accounting for 25% and 11%. Other fields included neurology, ophthalmology, surgery, and orthopedics.

1. Cardiac Intervention

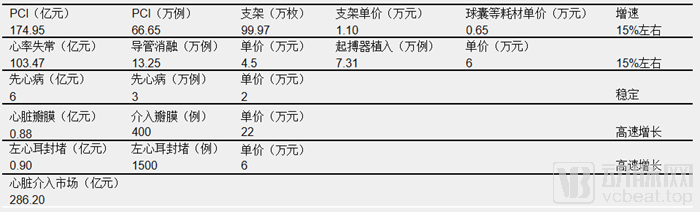

Among cardiovascular and cerebrovascular interventions, cardiac interventional procedures mainly include percutaneous coronary intervention (PCI), arrhythmia management, congenital heart disease, heart valve interventions, and left atrial appendage closure. We estimate that the national market size for cardiac interventions in China was approximately RMB 28.62 billion in 2016, representing a year-on-year growth of around 15%. Of this, the market sizes for PCI and arrhythmia were approximately RMB 17.5 billion and RMB 10.3 billion, respectively. Although the market size for interventional valves and left atrial appendage closure devices was less than RMB 100 million, it is in a stage of rapid growth with significant potential.

2. Transcatheter Heart Valves

We believe that transcatheter heart valves are undoubtedly a hot area in cardiovascular academia and investment, with the global market for transcatheter heart valves exceeding $30 billion. Taking TAVR as an example, the domestic market size for transcatheter aortic valves was only 280 million yuan in 2018, while the global market had already reached $3.75 billion. We estimate that the domestic TAVR market has a potential of 24 billion yuan, projected to reach 14.7 billion yuan (terminal) by 2030, with CABG accounting for nearly 40%. The industry leader Edwards' stock price has increased tenfold over the past decade, with its market capitalization reaching $38.4 billion.

Transcatheter heart valves are not merely an innovation; they represent an era. On one hand, among the four cardiac valves, only transcatheter aortic valve replacement (TAVR) has reached a relatively mature stage of development. The markets for mitral, tricuspid, and pulmonary valve replacement or repair, which offer significantly larger market potential, remain largely untapped. On the other hand, disruptive innovations often give rise to new industry leaders and high-performing stocks. Just as pacemakers propelled Medtronic to a market capitalization in the hundreds of billions of dollars, and the da Vinci Surgical System drove Intuitive Surgical’s stock price up by more than 200-fold, similar opportunities exist here. Generally, medical devices have longer life cycles than pharmaceuticals and are less susceptible to patent cliffs. Product iterations also help maintain pricing power more effectively. Early entrants can leverage their technological and channel advantages to continuously consolidate their industry position, actively expand related product portfolios, and grow stronger, ultimately emerging as the leading enterprises in the TAVR era.

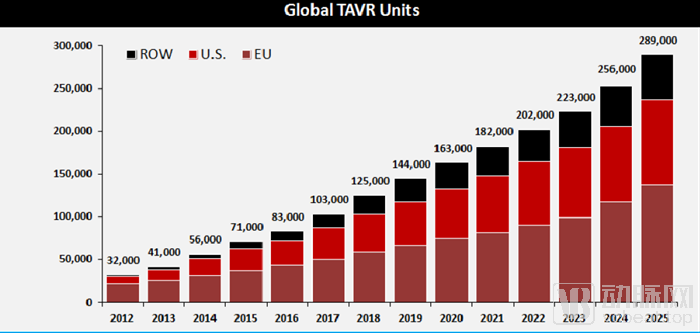

According to estimates from the TVT CHICAGO conference, approximately 125,000 TAVR procedures were performed globally in 2018. With an estimated average unit price of around $30,000, the global TAVR market size reached approximately $3.75 billion in 2018. By 2025, the number of TAVR procedures worldwide is projected to reach 289,000. Assuming an average unit price of $20,000–$30,000, the TAVR market size is expected to be around $7 billion. Driven by global population aging and the development of the Chinese market, we estimate the ultimate market potential for TAVR to reach $10–15 billion. Furthermore, when considering transcatheter repair/replacement of the mitral, tricuspid, and pulmonary valves, we estimate the total addressable market for transcatheter heart valve therapies to exceed $30 billion.

Development of Valve Therapy

1. TAVR Indications Are Gradually Expanding to Include Patients with Low-Gradient Severe Aortic Stenosis

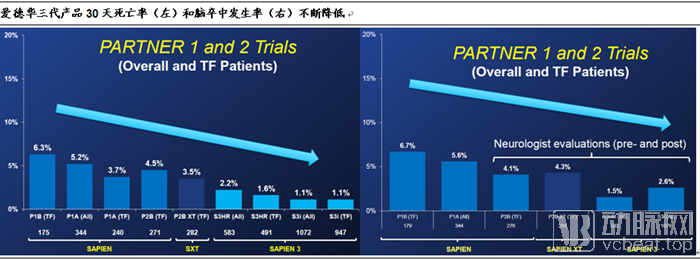

TAVR shone at the ACC 2019 conference held earlier this year, where the 1-year results of the PARTNER 3 trial and the 2-year results of the EVOLUT trial were presented. PARTNER 3 demonstrated that TAVR (SAPIEN 3) significantly outperformed surgical aortic valve replacement (SAVR) in primary endpoints at 12 months post-procedure among low-risk patients with severe aortic stenosis. The EVOLUT trial showed that TAVR (78% Evolut R and 22% Evolut PRO) achieved primary endpoints comparable to SAVR at 24 months post-procedure in low-risk patients with severe aortic stenosis; however, TAVR patients exhibited superior hemodynamic parameters at 12 months.

PARTNER 3 used the balloon-expandable valve (SAPIEN 3) as the transcatheter intervention arm compared with the surgical group, while the EVOLUT study used second- and third-generation self-expanding transcatheter valves (Evolut R in 78% and Evolut PRO in 22%) compared with the surgical group; both trials enrolled more than 1,000 patients. The PARTNER 3 results showed that the incidence of the primary composite endpoint (death, stroke, or rehospitalization) was significantly lower in the TAVR group than in the surgical group (8.5% vs. 15.1%). The 2-year results of the EVOLUT study showed that the incidence of the primary composite endpoint (death or disabling stroke) was 5.3% in the TAVR group and 6.7% in the SAVR group (P > 0.999). Although the primary outcomes were comparable, hemodynamic parameters were superior in the TAVR group compared with the SAVR group. It should be noted that only 22% of patients in this trial received Medtronic’s third-generation transcatheter aortic valve, Evolut PRO.

Following product iterations and validation through clinical trials, TAVR has been proven to achieve superior outcomes compared to traditional surgical replacement with mechanical or bioprosthetic valves in an increasing number of patients. In 2014, TAVR was included for the first time in the ACC/AHA guidelines for patients with severe aortic stenosis who were inoperable or at high surgical risk. In the same year, Edwards’ second-generation transcatheter aortic valve, SAPIEN XT, entered the U.S. market, while its third-generation product, SAPIEN 3, was launched in Europe. The latest indications for TAVR have expanded to include patients with low-risk severe aortic stenosis.

2. Transcatheter Heart Valves Poised to Replicate PCI’s Replacement of Coronary Artery Bypass Grafting

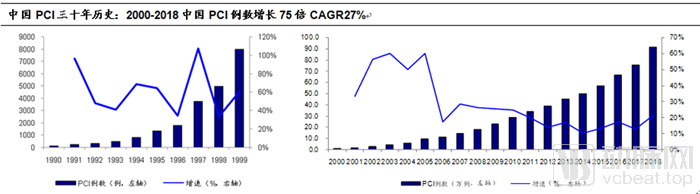

According to Academician Gao Runlin’s article, “Current Status and Prospects of Percutaneous Coronary Intervention in China,” the first percutaneous coronary intervention (PCI) procedure in China was performed in 1984. After 2000, PCI in China entered a period of rapid development. By 2001, a total of 16,345 PCI procedures had been completed nationwide, with a success rate of 97%. The number of coronary interventions performed that year exceeded the cumulative total of the previous 15 years, and the number of hospitals offering coronary intervention services increased to more than 200. According to data from the 22nd National Congress of Interventional Cardiology (CCIF 2019), as reported on the International Circulation website, China performed 915,000 PCI procedures in 2018, representing a 775-fold increase compared with 2000, with a compound annual growth rate (CAGR) of 27.2%. We estimate that more than 2,000 hospitals across China are currently capable of performing PCI.

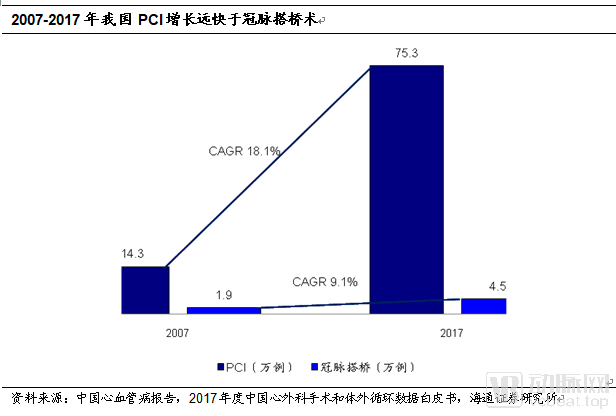

In 2007, China performed a total of 143,000 percutaneous coronary interventions (PCIs), with 18,000–20,000 coronary artery bypass grafting (CABG) procedures during the same period. In 2017, the number of PCIs performed nationwide reached 753,000. According to the 2017 White Paper on Cardiac Surgery and Cardiopulmonary Bypass Data in China, there were 45,000 CABG procedures during the same year. The growth rate of PCI has been significantly faster than that of CABG, and the development of minimally invasive surgeries has driven rapid market expansion.

In China, since Academician Ge Junbo successfully performed the first domestic case of transcatheter aortic valve replacement (TAVR) in 2010, the number of TAVR procedures exceeded 150 in 2014. We estimate that approximately 1,000 TAVR procedures were completed nationwide in 2018. Although TAVR is still in its early stages in China, it is experiencing rapid growth, and we believe it has the potential to replicate the trajectory by which percutaneous coronary intervention (PCI) replaced and surpassed coronary artery bypass grafting (CABG). According to the latest reports, the cumulative number of TAVR cases in China has reached 3,000.

3. Survey on the Prevalence of Aortic Valve Disease Shows Regurgitation Is More Common Than Stenosis

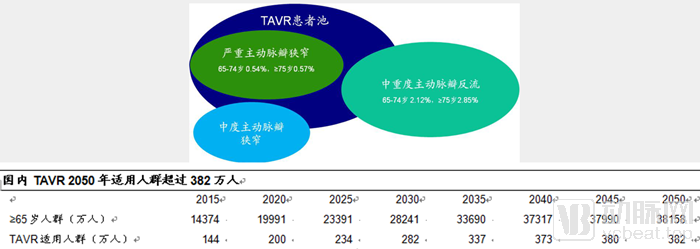

According to the Chinese Expert Consensus on Transcatheter Aortic Valve Replacement, the incidence of aortic stenosis in Western countries is approximately 2.0% among individuals aged ≥65 years and approximately 4.0% among those aged ≥85 years. Authoritative epidemiological data on valvular heart disease are currently lacking in China. We believe there are significant differences in the prevalence of valvular diseases between Eastern and Western populations; the prevalence of aortic stenosis is higher in European and American populations than in East Asian populations, whereas the prevalence of aortic regurgitation in China may be higher than that of aortic stenosis.

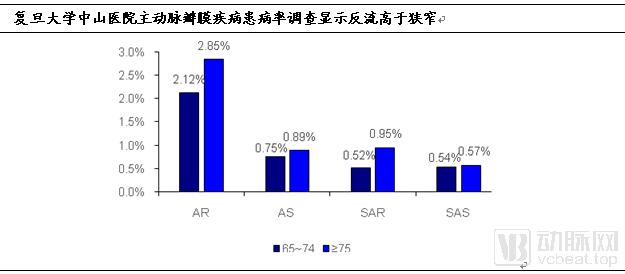

According to a statistical analysis of the echocardiography database of patients at Zhongshan Hospital, Fudan University, from 2005 to 2013, the detection rates of moderate or severe aortic regurgitation (AR) among patients aged 65–74 years (49,995 cases) and ≥75 years (34,671 cases) were 2.12% and 2.85%, respectively; the detection rates of moderate or severe aortic stenosis (AS) were 0.75% and 0.89%, respectively. The detection rates of severe aortic regurgitation (SAR) and severe aortic stenosis (SAS) in the two groups were 0.52% vs. 0.95% and 0.54% vs. 0.57%, respectively. These findings indicate that elderly Chinese individuals are more prone to aortic regurgitation than aortic stenosis in the context of degenerative aortic valve disease.

1. The target population for TAVR in China includes patients with aortic stenosis combined with partial regurgitation.

According to the Chinese Expert Consensus on Transcatheter Aortic Valve Replacement (TAVR), TAVR is currently primarily used to treat severe aortic stenosis (SAS) and may in the future be partially applied to treat aortic regurgitation (AR). The prevalence of severe aortic stenosis among patients aged 65–74 years and those aged ≥75 years is 0.54% and 0.57%, respectively. The prevalence of moderate-to-severe aortic regurgitation among patients aged 65–74 years and those aged ≥75 years is 2.12% and 2.85%, respectively. We believe that TAVR will be practically applied in the future to patients with severe aortic stenosis, selected cases of severe aortic stenosis, and selected cases of moderate-to-severe aortic regurgitation. Taking into account both severe aortic stenosis and regurgitation, we estimate that the applicability rate of TAVR in the population aged 65 years and older is 1%.

According to the National Bureau of Statistics and the report “Trends in Population Aging and Projections of the Elderly Population in China, 2015–2050,” the number of people aged 65 and above in China will reach 382 million by 2050. Assuming a 1% applicability rate, we estimate that the domestic population eligible for TAVR will be 3.82 million.

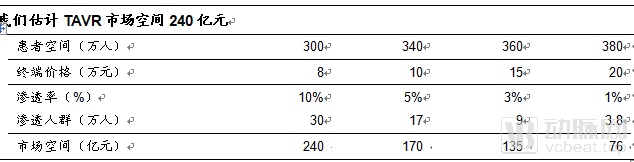

2. TAVR Market Size: RMB 24 Billion

Currently, the price of transcatheter aortic valve replacement (TAVR) systems in China is approximately RMB 250,000. We consider this price relatively high and the technical complexity substantial. We estimate that TAVR procedures are currently performed in only slightly over 100 hospitals. We believe that as the technology becomes more widely adopted and the number of experienced physicians increases, pricing will become a key determinant of TAVR penetration rates. Furthermore, with future improvements in TAVR valve design and increasingly effective treatment outcomes for aortic regurgitation, the market potential for TAVR is expected to expand further.

We assume an end-user price of RMB 200,000, with minimal reimbursement from basic medical insurance, leading to an estimated penetration rate of approximately 1%, equivalent to 38,000 patients treated and corresponding to a terminal market size of RMB 7.6 billion. Assuming the end-user price drops to RMB 80,000 with partial reimbursement from basic medical insurance, we estimate the penetration rate will rise to 10%. With 300,000 TAVR procedures performed annually and considering that some patients have already undergone surgery, we estimate the patient pool will decrease to 3 million, resulting in a market size of RMB 24 billion. We believe that transcatheter aortic valve replacement (TAVR) systems will gradually decline in price, penetration rates will steadily increase, and next-generation products will be progressively launched. As newer products are relatively more expensive than older ones, prices are unlikely to experience a cliff-like drop. Based on comprehensive analysis, we estimate the domestic TAVR terminal market size to reach RMB 24 billion.

3. TAVR Landscape: Four Domestic Competitors Within Three Years

Currently, Hangzhou Venus MedTech’s interventional artificial heart valve system, VenusA-Valve, and Suzhou JieCheng Medical’s interventional biological heart valve, J-Valve, have both received market approval in 2017 through the special review channel for innovative medical devices. Edwards Lifesciences’ SAPIEN valve was withdrawn from review, and clinical trials for its latest-generation transcatheter aortic valve system, Sapien 3, only commenced in early 2018. MicroPort’s VitaFlow was approved in July 2019. Medtronic has also withdrawn its application, while Peijia Medical’s transcatheter aortic valve system, TaurusOne, is currently in clinical trials. We estimate that the future TAVR market in China will be dominated by domestically produced products, with competition among four Chinese manufacturers within the next three years.

1. VenusA-Valve from Venus MedTech Demonstrates Favorable 5-Year Outcomes Following TAVR

At the 2019 China Interventional Cardiology Conference, Academician Gao Runlin presented the five-year follow-up results of a prospective, multicenter, observational study on the safety and efficacy of the VenusA-Valve in treating severe aortic stenosis. The study commenced in September 2012, with the first implantation performed on September 12, 2012, involving five centers across China. A total of 101 patients were enrolled, all aged >70 years, with NYHA functional class I or higher, an expected life expectancy >12 months, and degenerative aortic valve stenosis (including native aortic valves and severely dysfunctional surgical aortic bioprostheses). Eligibility criteria included echocardiographic measurements showing a mean transvalvular pressure gradient ≥40 mmHg, or a peak aortic jet velocity ≥4.0 m/s, or an aortic valve area <0.8 cm² (or an indexed aortic valve area <0.5 cm²/m²). Patients were followed up at 30 days, 6 months, 12 months, and annually from 2 to 5 years post-TAVR. The primary endpoint of the study was all-cause mortality or major stroke within 12 months after the procedure.

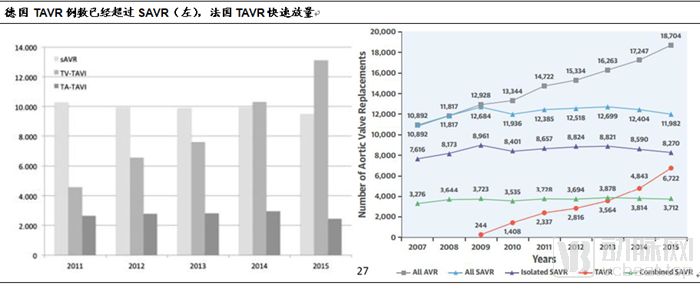

2. Rapid Volume Growth of TAVR in Germany and France

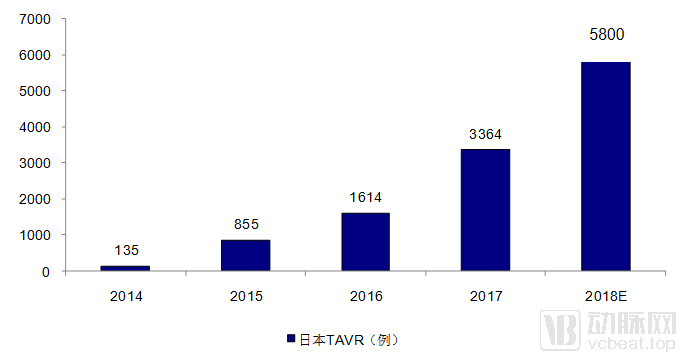

3. Rapid Uptake of TAVR in Japan

In 2007, with the launch of Edwards’ SAPIEN and Medtronic’s CoreValve in Europe, the era of TAVR officially began. Various manufacturers have subsequently introduced multiple products, with Edwards and Medtronic capturing the majority of the market. Edwards has launched three generations of balloon-expandable valves: SAPIEN, SAPIEN XT, and SAPIEN 3. Medtronic has also introduced three generations of self-expanding valves: CoreValve, Evolut R, and Evolut PRO. The latter two feature recapturability, allowing for repositioning to improve fault tolerance and positioning accuracy.

Major complications of TAVR include conduction block (requiring pacemaker implantation), paravalvular leak, stroke, and bleeding. With improvements in TAVR devices and increased operator proficiency, the 30-day postoperative mortality and stroke rates have continued to decline. For the Edwards SAPIEN 3 valve, the 30-day postoperative mortality and stroke rates can be reduced to 1.1% and 1.5%, respectively.

According to JACC 2017 statistics, the current 30-day mortality rate after new-generation TAVR valve implantation is 1.0–3.6%, the incidence of major stroke is 0.5–3.2%, major vascular complications (such as bleeding) are 3.8–7.2%, the permanent pacemaker implantation rate is 5.3–35.5%, and moderate-to-severe paravalvular leak is 0.6–5.7%.

Currently, representative next-generation TAVR products worldwide include Edwards’ SAPIEN 3 and CENTERA, Medtronic’s Evolut PRO, ACCURATE Neo from Symetis (acquired by Boston Scientific), and Boston Scientific’s Lotus Edge. These newer-generation devices have made significant improvements in preventing paravalvular leak, enabling retrievability, and miniaturizing delivery system profiles. They are supported by substantial clinical data, and some valves already feature a degree of automatic positioning capability.

We believe that the future development of TAVR valves will primarily focus on retrievability, double-skirt design (to reduce paravalvular leak), appropriate valve length, miniaturization of delivery system size, pre-loading, and extended durability of biomaterials, with the aim of simplifying procedures, enhancing positioning precision, and improving postoperative safety.

1. The Potential of TMVR in Treating Patients with Secondary Mitral Regurgitation

Another clinical study presented at ACC 2019, COAPT, brought significant hope to transcatheter mitral valve repair (TMVR). Abbott’s MitraClip is currently the most commonly used device-based intervention for minimally invasive treatment of mitral regurgitation. European and American guidelines recommend MitraClip for patients with primary mitral regurgitation who are at high surgical risk or have contraindications to surgery; however, its efficacy in secondary mitral regurgitation remains unclear.

According to the article “Transcatheter Mitral-Valve Repair in Patients with Heart Failure” published in The New England Journal of Medicine, the COAPT trial enrolled a total of 614 patients with heart failure and moderate-to-severe (grade 3+ and 4+) secondary mitral regurgitation, who were randomly assigned to either the standard heart failure medication group (312 patients) or the MitraClip plus standard therapy group.

Standard Heart Failure Medication Group (302 cases). Follow-up was conducted every six months postoperatively, with a planned follow-up duration of five years. The results of this two-year follow-up indicated that, compared to the standard heart failure medication group, patients in the MitraClip plus medication group had a significantly reduced risk of death and heart failure hospitalization (67.9% vs. 45.7%), demonstrating the potential of transcatheter mitral valve repair (TMVR) in treating patients with secondary mitral regurgitation.

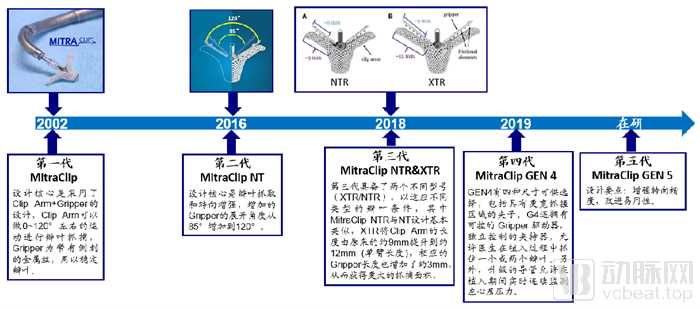

2. Abbott's MitraClip is a milestone product in the field of TMVR

In the field of mitral valve therapy, Abbott’s MitraClip is a landmark product. It is currently the only commercially available transcatheter mitral valve intervention product widely used worldwide. The first-generation MitraClip was launched in 2002; its anterior leaflet-capturing component, the Clip Arm, could move through 120 degrees, and the Gripper, designed to stabilize the leaflets, utilized barbed wires. Building on the first generation, MitraClip has continued to optimize leaflet stabilization and grasping as well as delivery system design. In the second generation, the Gripper opening angle increased from 85 to 120 degrees. The third generation introduced two size options, with the XTR model featuring both Clip Arm and Gripper lengths extended by 3 mm, thereby achieving a larger grasping area. The fourth generation received FDA approval in July 2019. The GEN4 system offers four size options and features a controllable Gripper driver; the independently controlled Grippers allow physicians to grasp one or both leaflets during implantation.

MitraClip has also achieved significant commercial success. After receiving CE certification in 2008, its sales volume grew rapidly. By March 2019, more than 80,000 patients had undergone MitraClip implantation. Based on a unit price of $30,000, we estimate that approximately 17,000 MitraClip devices were sold in 2018, generating $520 million in revenue for Abbott Laboratories.

3. Hanyu Medical and Dejin Medical Are Rapidly Advancing Their TMVR Development

Although MitraClip therapy has been widely implemented worldwide, particularly in developed countries, its application in China started relatively late. The first procedure in China was performed by Academician Ge Junbo in 2012. The high cost of the MitraClip device is a significant barrier to its routine use in China, as multiple clips are sometimes required for a single treatment.

Domestically produced transcatheter mitral valve repair devices have emerged as a powerful force. TiYu Medical’s ValveClamp and DeJin Medical’s MitralStitch have advanced rapidly, having completed 12 and 10 first-in-man (FIM) studies, respectively. Unlike the MitraClip system, which accesses the left atrium via a transvenous approach through the right atrium and transseptal puncture before reaching the left ventricle, both ValveClamp and MitralStitch utilize a transapical approach. This pathway is shorter and more direct, allowing for easier device control and simplified procedural execution. On July 5, 2019, the first patient was enrolled in the China National Medical Products Administration (NMPA) pivotal clinical study of the MitralStitch mitral valve repair system at Fuwai Hospital, Chinese Academy of Medical Sciences. The procedure was performed by Professor Pan Xiangbin’s team. The patient achieved favorable outcomes, and the procedure time was exceptionally short, with less than five minutes elapsed from device introduction to completion of implantation.

Both ValveClamp and MitraClip are edge-to-edge repair devices. The advantages of ValveClamp include: 1) A smaller delivery system profile (ValveClamp: 14–16 Fr; MitraClip: 24 Fr); 2) A larger grasping range and broader indications. MitraClip relies on the downward swinging and compression of its upper arm against the lower arm to achieve grasping, whereas ValveClamp accomplishes this through the overall translational approximation of the upper tube toward the lower tube. Consequently, ValveClamp offers a larger space for leaflet capture. Due to the relatively limited grasping space of MitraClip, its indications require a mitral valve prolapse gap of <10 mm, whereas ValveClamp has no such requirement; 3) Simpler operation and shorter procedure time. The average catheter manipulation time for ValveClamp is 18.5 ± 8.5 minutes, significantly shorter than the 157 ± 81 minutes required for MitraClip.

Dejin Medical’s MitralStitch has pioneered a new frontier in transcatheter mitral valve repair. As China’s first minimally invasive interventional device for mitral valve repair, it is also the world’s first transcatheter system capable of simultaneously performing artificial chordae tendineae implantation and edge-to-edge repair. This “one-stop” artificial chordae repair approach holds significant clinical value for patients with both degenerative mitral regurgitation (DMR) and functional mitral regurgitation (FMR). It is particularly suitable for complex MR cases, allowing for personalized treatment plans by combining targeted artificial chordae implantation with edge-to-edge repair.

The LuX-Valve, a transcatheter interventional tricuspid valve jointly developed by Professor Xu Zhiyun’s Innovation Team at Changhai Hospital of Naval Medical University and Jian Shi Biotechnology, has achieved a technological breakthrough in China for the interventional treatment of severe tricuspid regurgitation. This novel product completely departs from previous design concepts that relied on radial support force, innovatively applying ventricular septal anchoring technology and anterior leaflet central holding technology for fixation. Due to the absence of significant radial support force on the native tricuspid annulus, the position of the stent valve can be adjusted based on real-time ultrasound monitoring after initial deployment and commencement of opening and closing functions. Final fixation and delivery system withdrawal are performed only after confirming the absence of paravalvular leakage, thereby significantly improving procedural outcomes. The procedure is convenient to perform, does not require pacing during surgery, and can be conducted without contrast agents in patients with renal insufficiency. It is currently the world’s first product of its kind based on this new concept. Since September 2018, a total of 15 subjects with severe tricuspid regurgitation have been enrolled, demonstrating favorable clinical outcomes.

Heart failure has become one of the leading causes of death from cardiovascular disease. Statistics from the American Heart Association in 2013 showed that approximately 19% of all deaths were attributed to heart failure. According to the Report on Cardiovascular Diseases in China 2017, there are 4.5 million patients with heart failure in China, and treatment currently relies primarily on pharmacological therapy. The definitive treatment for end-stage heart failure is surgical heart transplantation; however, due to a severe shortage of donors relative to the number of patients requiring transplantation, a large number of patients die during the prolonged waiting period. The rapid development of ventricular assist devices (VADs), or artificial hearts, in recent years has provided new approaches to prolonging survival in patients with heart failure, thereby increasing opportunities for heart transplantation or directly sustaining life. The evolution of artificial hearts has progressed from early pulsatile-flow devices that mimicked natural cardiac function to the currently predominant continuous-flow artificial hearts. Among continuous-flow artificial hearts, classifications based on bearing technology include mechanical contact bearings, hydrodynamic suspension, and full magnetic levitation.

In the 1960s, artificial hearts were first used in clinical practice. According to the Seventh INTERMACS Annual Report: 15,000 Patients and Counting, more than 2,500 artificial hearts were implanted in the United States in 2014, with an overall one-year survival rate of 80% and a two-year survival rate exceeding 70%. Thoratec is the oldest and most representative company in the global artificial heart field. Its pulsatile-flow artificial heart, HeartMate I, was approved by the FDA in 2003 for permanent replacement therapy, offering new options for patients with heart failure. However, it still had drawbacks such as large size and poor durability, and its therapeutic efficacy was inferior to heart transplantation. The second-generation continuous-flow artificial heart, HeartMate II, was approved for market launch in 2010, improving size and durability, but blood compatibility issues were not fundamentally resolved. The third-generation HeartMate III was approved by the FDA in 2017, and we believe it holds promise for significantly addressing blood compatibility concerns. In 2015, Thoratec’s artificial heart sales reached $478 million, with a net profit of $50.4 million. Currently, 90% of patients choose Thoratec’s HeartMate II, while the remaining patients mostly opt for HeartWare’s HVAD. Other companies, such as SynCardia and Carmat, also have their own artificial heart products.

China’s artificial heart R&D is gaining momentum. Currently, the following products have entered the Special Approval Procedure for Innovative Medical Devices: Chongqing Yongrenxin Medical’s implantable left ventricular assist device (LVAD), Suzhou Tongxin Medical’s ventricular assist device, Changzhi Jiuan Artificial Heart Technology’s ventricular assist system (implantable axial-flow blood pump), and Aerospace Taixin Technology’s implantable magnetic-levitation ventricular assist device. Notably, Suzhou Tongxin Medical’s latest-generation fully magnetically levitated artificial heart, CH-VAD, achieved a 100% success rate in six goat experiments conducted in China and eight bovine experiments conducted in the United States. In collaboration with Academician Hu Shengshou’s team, three procedures were completed at Fuwai Hospital under humanitarian exemption approval. All patients survived postoperatively in good health; one underwent heart transplantation six months later, while another had the ventricular assist device removed after five months due to recovery of cardiac function. The CH-VAD product is currently undergoing clinical trials. Based on publicly available parameters, CH-VAD demonstrates strong competitiveness compared with HeartMate II and HVAD.

Currently, the price of a set of artificial heart in the United States is around $100,000. In China, there are currently over 4.5 million patients with heart failure, and in 2016, there were a total of 2,149 registered cases of heart transplants in mainland China, which is greatly limited by the availability of donor hearts. If the annual use of artificial hearts reaches 5,000 cases in the future, with a unit price of about $100,000, it would represent a market worth more than 3 billion yuan. Considering technological advancements and further penetration, the market potential would be even greater.

Patients with acute myocardial infarction or cardiogenic shock, as well as those requiring high-risk percutaneous coronary intervention (PCI), need short-term cardiac function support to buy time for further treatment or recovery. Compared with artificial hearts or ventricular assist devices, heart pumps are used for a shorter period, generally 5-7 days, and involve less invasive implantation.

In the field of cardiac pumps, Abiomed’s Impella product line has few rivals. The Impella series works by placing an axial-flow pump within the patient’s heart chamber, directing blood through a cannula into the ascending aorta to maintain systemic perfusion, including coronary blood flow. The Impella product received CE marking from the European Union in 2001. In 2008, the U.S. Food and Drug Administration (FDA) approved the Impella series for use in patients undergoing percutaneous coronary intervention (PCI). To date, the widely used Impella products mainly include the Impella 2.5, 5.0, CP, and RP models. The Impella cardiac pump system has been included as a recommended therapeutic option in seven different clinical guidelines.

Compared with traditional manual intervention methods for cardiac function, such as ECMO/CPS and IABP (intra-aortic balloon pump), Impella has unique advantages. In terms of safety, the Impella device requires vascular access at only a single site without the need for cardiac puncture. Furthermore, its mechanical circulatory support relies on active hemodynamics rather than inotropic agents, thereby significantly reducing the incidence of complications and mortality. Additionally, the use of Impella does not require heart rate synchronization, greatly simplifying procedural complexity. According to a report in the Journal of the American College of Cardiology, there is no significant difference in procedure time between first-time users and experienced operators of Impella, with an average procedural time of less than 10 minutes.

The average selling price of the Impella product series is approximately $23,000 per unit. Driven by its overwhelmingly superior products, Abiomed has reported strong financial performance. In fiscal year 2018, the company’s total revenue reached $594 million, a 33% year-over-year increase, with a gross margin of 83%. Sales of the Impella product series amounted to $571 million, representing a 35% year-over-year growth. As of March 5, Abiomed’s market capitalization stood at $15.25 billion, marking a 19.6-fold increase over the past decade. New technologies are continuously being integrated into the Impella product line, including optical sensors and smart device interoperability. The new generation of the Impella CP heart pump, equipped with optical sensors, has received CE certification, demonstrating significantly improved accuracy in real-time positioning. In late January 2019, the Impella Connect system also obtained EU CE certification. Currently, there are no comparable competing products in the Chinese domestic market that can rival the Impella product line. However, given the Impella product’s remarkable performance over the past decade, domestically produced heart pump series hold substantial promise for future development.

Note: All materials and images in this article are sourced from the speakers' PowerPoint presentations.