New Health Insurance Regulations Spark Influx of Billions in Investment as Sequoia, Tencent Enter the Trillion-Yuan Blue Ocean | 2019 Year-End Review

Innovative Payment: The Wind Is Rising!

Three Companies Announce Financing on the Same Day; One Company Secures Funding Three Times Within a Year, with the Largest Single Round Exceeding RMB 1 Billion, as Giants Including Sequoia China, Alibaba, and Tencent Enter the Fray. The events unfolding in the health insurance sector this year seem to confirm the advent of a new growth frontier.

From RMB 158.718 billion in 2014 to RMB 544.813 billion in 2018, health insurance has drawn significant attention with a compound annual growth rate (CAGR) of over 35% in the past five years.In the first three quarters of this year, the original premium income from health insurance business reached 567.7 billion yuan, a year-on-year increase of 30.90%., exceeding the total premium income for the entire previous year. Based on the projected growth rate,The market size of health insurance is expected to exceed one trillion yuan in 2020.。

In terms of policy, the China Banking and Insurance Regulatory Commission (CBIRC) published the newly revised"Measures for the Administration of Health Insurance", once again affirming and encouraging the development of health insurance.

In the face of a trillion-yuan blue ocean market with such certain prospects, what are the reasons behind the explosive popularity of health insurance? What problems exist in its development? What are the possible future trends? And what potential changes will it bring to the entire industry?

VCBeat has conducted an annual review of developments in the health insurance sector this year, aiming to address these questions.

Four years ago, at a café in Zhongguancun, Beijing, Chen Penghui, a partner at Sequoia Capital China, delivered a presentation at a healthcare industry forum. He stated, “The healthcare sector is arguably one of the few industries most resistant to transformation by the internet. Precisely because it is so difficult to disrupt, there remain many pain points that are not easily uncovered or monetized. This also means that opportunities exist across various healthcare subsectors.”

Over the past few years, among the various subsectors of “Internet + Healthcare,” medical payment has undoubtedly emerged as one of the most deeply addressed pain points. In the arena of internet-based health insurance coverage, innovative payment solutions have proliferated—ranging from the once wildly popular million-yuan medical insurance plans and critical illness fundraising campaigns, to online mutual aid platforms with over 100 million participants, and installment payment options for pharmaceuticals.ZhongAn, Shuidi, Ant Group, Tencent, Sequoia China, and other players are entering the innovative payment sector with new models, new technologies, and capital.

The surge in this sector is not without reason. In recent years, improving the expenditure efficiency of medical insurance funds and implementing cost containment measures have been the direction of the government’s healthcare reforms. During the major State Council institutional restructuring in 2018, the National Healthcare Security Administration (NHSA) was established, with its mission centered on “medical insurance cost containment” and the “coordinated reform of medical care, health insurance, and pharmaceuticals.”

Under this trend,Continuously emphasize the development of commercial medical health insurance to play a supplementary role in healthcare coverage., seems to have become a panacea for reforming the current payment dilemma.

Moreover, in addition to alleviating pressure on the social medical security system, health insurance can also resolve supply-side contradictions. With rising out-of-pocket healthcare expenditures, an aging population, accelerated urbanization, a growing middle-income group, and an expanding population with chronic diseases, the current supply capacity of social security falls far short of meeting the people’s rapidly growing demand for health protection.

Driven by multiple factors, residents’ awareness of controlling medical expenses has grown increasingly strong, and market demand for health insurance has become more robust. Whether viewed from the perspective of the external macroeconomic environment, industry regulatory guidance, or the strategic development goals of leading life insurers, demand for protection-oriented insurance products—represented by health insurance—has been consistently and effectively stimulated, with health insurance premiums maintaining a growth rate that outpaces the industry average.

Since 2018, driven by technological empowerment and policy changes, the health insurance industry has entered a phase of rapid growth. According to data from the China Banking and Insurance Regulatory Commission (CBIRC), the original premium income from health insurance business reached RMB 544.813 billion in 2018, a year-on-year increase of 24.12%. Claims and benefits paid out in the health insurance sector totaled RMB 174.434 billion, representing a year-on-year increase of 34.72%.

This year, the data for health insurance continues to show significant growth. In the first three quarters of 2019, the original premium income from health insurance business reached 567.7 billion yuan, a year-on-year increase of 30.90%.

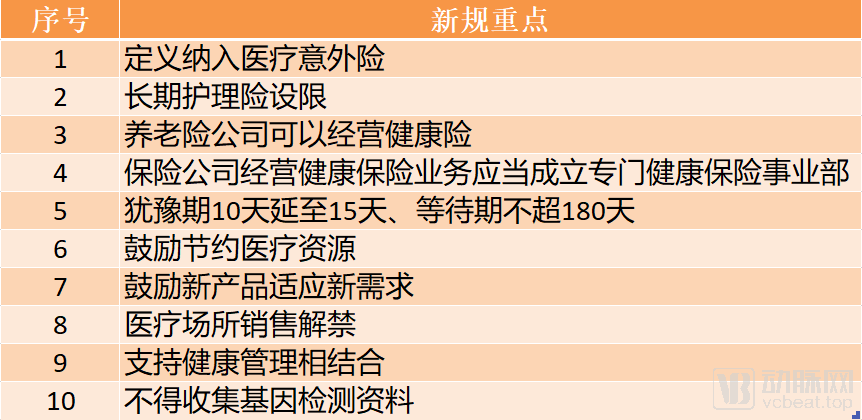

Since 2019, policy support has continued to fuel the growth of the health insurance sector. Information released during the Two Sessions at the beginning of the year highlighted that the Government Work Report explicitly called for “enhancing the risk protection function of the insurance industry.” On November 12, the China Banking and Insurance Regulatory Commission (CBIRC) published the newly revised Administrative Measures for Health Insurance on its official website. This significant policy announcement sent shockwaves through the industry, prompting numerous professionals to share the news link.

Top 10 Key Points of the New Health Insurance Regulations

The newly introduced regulations have once again affirmed the development of health insurance.

In terms of technology, with the application of artificial intelligence, big data, and other technologies, the entire process of health insurance is undergoing innovation. For example, customer acquisition, claims processing, underwriting, risk control, product development, and other links are all experiencing significant changes.

“Policies in recent years have been consistently encouraging the development of health insurance, with a favorable policy trend. The health insurance market is just getting started and will undoubtedly accelerate its growth, experiencing rapid expansion,” said Peng Xuan, Co-CEO of Yuanxin Huibao, in an interview with VCBeat.

“Undoubtedly, China’s healthcare payment system will evolve toward diversification; meanwhile, there is immense potential for both public health insurance and commercial insurance to leverage technology-driven cost containment and efficiency improvements. The trends in this sector are clear, making it highly promising.”Huang Shengxuan, Managing Director at Sunshine Ronghui Capital, said in an interview with VCBeat.

In short, nearly everyone in the industry recognizes the clear market prospects for health insurance and sees its trillion-yuan blue ocean. An increasing number of players are joining the competition in this field.

Capital is undoubtedly the most sensitive indicator of market trends.

On July 8, 2019, three companies—Yuanxin Huibao, Nuohui Medical, and Zhanlue Data—simultaneously announced their financing news on the VCBeat platform. Yuanxin Huibao secured RMB 50 million in Series A funding, led by Sequoia Capital, to provide solutions for insurance companies in areas such as actuarial pricing of products, risk control, and user acquisition. In an interview with VCBeat, Peng Xuan stated that future health insurance would not merely be insurance but would evolve toward health management and comprehensive health services.

Nohui Medical, established last November, secured a Series B financing round led by Legend Star. The company provides health insurance and payment solutions for major diseases, covering medication reimbursement, efficacy guarantees, and medication security. Zhanlue Data raised nearly RMB 100 million in its Series B financing round, led by Lingfeng Capital, to provide enterprise-level big data risk control solutions for insurance companies and intermediaries.

The fact that these three companies secured financing on the same day is not merely a coincidence; capital has been highly active in the health insurance market over the past year.

2019 Health Insurance Sector Financing Overview

Data sources: VCBeat, 36Kr, Tianyancha

Two more companies on this list are worth mentioning.

Duobaoyu, a company founded just two years ago, secured three rounds of financing in 2019. In February of this year, it completed its Series A funding round, led by Bertelsmann Asia Investments (BAI) with participation from ZhenFund. In April, it closed a Series A+ round worth tens of millions of US dollars, led by Lightspeed China Partners, with follow-on investments from existing shareholders BAI and ZhenFund. In September, Duobaoyu announced its latest Series B financing of over RMB 200 million, led by Yunfeng Capital. Duobaoyu’s key business strength lies in providing users with long-term insurance purchasing decision support services through multiple channels, including WeChat Official Accounts, Douyin (TikTok), Xiaohongshu (Little Red Book), Weibo, and Kuaishou. The company has currently obtained an insurance brokerage license.

Waterdrop, now a unicorn company, has also attracted significant attention. Established just over three years ago, Waterdrop secured two rounds of financing this year alone, with each single round exceeding RMB 1 billion, thereby achieving unicorn status. In terms of business operations, Waterdrop Crowdfunding leverages social networks to educate the market on fundraising for critical illnesses; Waterdrop Mutual Aid serves users within this fundraising ecosystem who have protection needs; and a substantial portion of these mutual aid members are expected to convert into customers of Waterdrop Insurance, purchasing insurance products. This three-tier funnel model employed by Waterdrop effectively creates a closed-loop ecosystem.

In terms of capital, dozens of well-known venture capital firms, including Tencent, Sequoia China, Yunfeng Capital, and Legend Star, have entered the health insurance sector across various funding rounds.Based on the investment rounds they entered, as the rounds progress to later stages, additional capital injections may continue in the future.

“The outlook for this sector is relatively clear, with the landscape currently dominated by early- to mid-stage companies. The industry is poised for imminent breakthroughs driven by technology and data. Given the substantial market size and well-defined demand, we anticipate that several companies will achieve significant scale within the next two to three years,” said Huang Shengxuan, Managing Director at Sunshine Ronghui Capital, in an interview with VCBeat. As an investor, he expressed particular optimism about solution integrators capable of connecting customers, data, payment systems, and supply chains, as well as companies that provide incremental value-added services to commercial insurers and social security programs.

Health insurance is one of the lines of business operated by insurance companies. Given the relative complexity of its product features, services, and management, it necessitates a collaborative division of labor among front-office, middle-office, and back-office departments covering development, sales, and service, thereby forming an internal health insurance value chain within the insurer. Meanwhile, as health insurance involves medical services, data, and health management, among other elements, insurers must collaborate with specialized third-party providers across various fields. This has given rise to an industry ecosystem centered on insurance companies, linked by insurance products, and supported by third parties delivering diverse services and support.

Various nodes across the health insurance industry chain are undergoing innovation and upgrading, with a wave of innovative companies emerging from the back end through the mid-end to the front end.

Some Companies in the Sub-sectors of Health Insurance

Data sources: VCBeat, Tianyancha

Based on their current core businesses and their positions within the health insurance industry value chain, this article categorizes health insurance entities into three types: platform/channel providers, health insurance TPAs (Third-Party Administrators), and others. It is worth noting that it is difficult to strictly assign these innovative companies to a single sector, as any company would prefer to brand itself as a “health insurtech company” from a public relations perspective.

Our general definition of health insurance platform/channel companies is: entities that leverage information technology to provide online insurance knowledge, product comparisons, product screening, purchase, and services. Large and medium-sized insurance companies are not included in this category; although they typically operate online “product supermarkets,” their sales channels remain predominantly offline. Even for products purchased online, customer acquisition often relies on traditional channels driving traffic to online platforms.

With the deepening development of the internet and mobile terminals, generational shifts in consumer demographics, and heightened public awareness of insurance, short-term health insurance has seen significant growth through online channels in recent years. Leveraging the traffic characteristics of the internet, many platform-based companies with substantial user traffic have achieved rapid growth in their health insurance businesses.

According to data from the China Banking and Insurance Regulatory Commission (CBIRC), premiums for internet health insurance reached RMB 11.6 billion in the first half of 2019. Zeng Zhuo, Senior Vice President of ZhongAn Insurance, previously predicted that the internet health insurance market would reach a scale of RMB 100 billion within two years. In terms of growth rate, internet health insurance has arguably ushered in a new growth curve for the health insurance market.

As can be seen from the table above, platform-based enterprises are a type favored by capital and often command higher valuations. Internet giants entering the health insurance sector have also largely focused on the track of channel innovation.It is foreseeable that channel innovation will become the most fiercely contested arena among all segments of the health insurance industry.

Third-party administrators in the health insurance sector are commonly referred to as TPAs. Given the rapid evolution of the industry, this article adopts a broad definition of TPA, encompassing not only traditional services such as claims processing, medical expense settlement arrangements, and reimbursement administration, but also emerging business areas including risk control, product development, construction of healthcare service networks, and health management.

This sector holds significant promise and is highly favored by investors.Huang Shengxuan, Managing Director of Sunshine Ronghui Capital, stated, “As the health insurance market continues to expand, TPAs will be the first to reap the benefits.”

In accordance with the recently issued “New Regulations on Health Insurance” by the China Banking and Insurance Regulatory Commission,Health services can account for 20% of health insurance premium income. If the health insurance market reaches a trillion yuan in the future, the market size for health insurance TPA (Third-Party Administrator) could reach 200 billion yuan.

Health insurance sits at the intersection of the insurance and healthcare sectors. As the entire healthcare industry transitions from traditional fee-for-service reimbursement models to service-oriented and managed care models, health insurance Third-Party Administrators (TPAs) have significant room to operate within this nexus. It is foreseeable that large-scale model innovations will emerge in the future.

In the “Others” category, there are diverse business models, such as technology-enabled solutions and big data applications. Taking Ping An HealthCare Technology and Neusoft Wanghai as examples, Ping An HealthCare Technology has cumulatively provided medical insurance and commercial insurance management services to over 200 cities and a population of 800 million; its substantial big data reserves will further empower its business operations. Meanwhile, Neusoft Wanghai has been striving to maintain its competitive advantage in the field of lean hospital information and data services.

In addition, there are Miaojiankang, which focuses on health management; Jianyibao and Shanzhen, which target specific population segments; Medxhealth and Zhongnuo Puhui, whose businesses involve installment payment plans for pharmaceuticals; and Wanhu Liangfang, which operates as a pharmacy benefit manager (PBM).

In recent years, the health insurance sector has also seen a highly significant innovation in scenarios,“The Mutual Aid + Insurance” model has pioneered a key scenario for health insurance sales in the mobile internet era.. In particular, since the beginning of this year, Ant Financial has disclosed that its mutual-aid user base has exceeded 100 million; Shuidi has reported that new monthly premiums for long-term insurance policies on its insurance marketplace have surpassed RMB 100 million; and Tencent’s WeSure, after two years of development, has amassed over 55 million registered users and provided insurance services to more than 25 million users.

Capital-driven marketing, vast demand for health protection, the highly promising county-level market, and efficient, precise policy conversion rates are injecting new vitality into the industry.

In terms of products, homogenization of health insurance offerings has been a major industry challenge. However, this year has seen a surge in innovative products. WeSure (Tencent’s micro-insurance platform), in collaboration with Taikang Online and Medbanks Health, launched “Yao Shen Bao,” which integrates the pharmaceutical supply chain; its model of providing in-kind drug reimbursements is highly worthy of emulation. MiaoBao, the insurance brand under Miao Jiankang, introduced three chronic disease management products leveraging its self-developed health management platform for insured users and an intelligent underwriting system. The concept of future-oriented health management will undoubtedly appear increasingly in the design of health insurance products.

Selected Innovative Health Insurance Products in 2019

As shown in the table above, this year’s health insurance sector is placing greater emphasis on refined operations for segmented populations, with a series of upgrades underway in coverage scope, pricing strategies, risk management, and medical services.

Although the blue-ocean characteristics of the health insurance market are evident, the industry’s development still faces numerous bottlenecks that need to be overcome.

The current Chinese health insurance market is highly concentrated, with 80% of revenue concentrated among the top 8% of companies. The main participants are primarily life and property insurance companies, while specialized health insurance companies remain small in both scale and number.

However, as more and more players enter the health insurance market,The market landscape of health insurance companies is shifting toward diversification, evolving from traditional single insurers to include internet platforms, medical institutions, pharmaceutical groups, health management organizations, medical big data companies, and entities from the real economy.。

Severe product homogenization represents a major bottleneck. Disease insurance and medical insurance dominate the market, while long-term care insurance and disability insurance account for a relatively low share of premiums. Commercial health insurance plays a limited role in supplementing basic medical insurance, and the ratio of actual commercial health insurance claims to total national health expenditure lags significantly behind that of countries with mature insurance markets. There is minimal differentiation among commercial health insurance products offered by various insurers, many of which are sold as bundled riders attached to life insurance policies.

From the perspective of sales channels, health insurance distribution can be categorized into online and offline channels. Traditional channels are dominated by individual agents, with health insurance policies sold through insurance agents accounting for more than 60% of the market share, indicating that strong offline channels hold the majority of the market. However, it is evident that online channels, leveraging their massive traffic, are redefining the sales model of health insurance.

From the perspective of the industry chain, health insurance operations involve multiple segments: “medical care, pharmaceuticals, insurance, and wellness.” Customers directly or indirectly receive financial compensation for health protection from payers; obtain diagnostic, therapeutic, and prescription services from healthcare providers; and access full-cycle health services and health incentives from wellness service providers. Payers and service providers achieve integration in terms of customer bases, data, and systems. Nevertheless, numerous pain points persist across these segments.

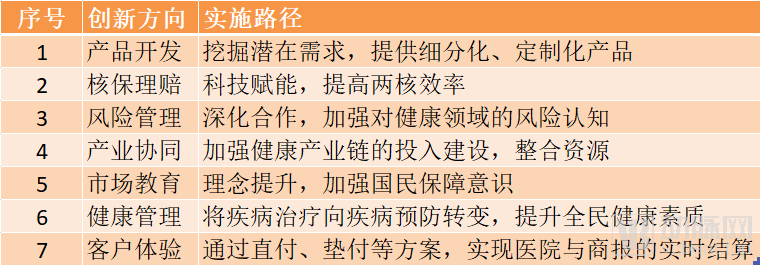

Seven Major Directions for Innovation in Commercial Health Insurance

In the future, the industry can drive innovation in commercial health insurance across multiple dimensions—including product development, core operations of underwriting and claims, risk management, industrial synergy, and active administration of government-commissioned projects. By strengthening the accumulation of foundational risk data, deepening engagement across the health insurance value chain from internal operations to external collaborations, the industry can achieve healthy and sustainable growth.

Regarding health insurance, another issue is that the general public has long had a low level of awareness about the insurance industry. According to data disclosed in the "2018 China Commercial Health Insurance Development Index Report," the current coverage rate of commercial health insurance is less than 10%. It is easy to imagine how large the market will become as insurance awareness increases.

Perhaps, only with the overall rise in national insurance awareness will health insurance truly reach for the stars.