Three Leading Aesthetic Medicine Companies Go Public in 2019 Amid Scarce High-Quality Assets and Pursuit of Sustainable Growth

In 2019, several star companies in the medical aesthetics industry went public, injecting a strong shot of confidence into the sector.

On May 2, Eastern Time, Beijing So-Young Technology Co., Ltd. (hereinafter referred to as “So-Young”) listed on the NASDAQ. The latest third-quarter financial report shows that as of September 30, 2019, So-Young achieved revenue of RMB 302.4 million, a year-on-year increase of 79.6%, exceeding the high end of its Q3 revenue guidance previously issued in the Q2 earnings report; it realized a net profit of RMB 31.6 million, with Non-GAAP net profit amounting to RMB 40.49 million, compared to a net loss in the same period last year.

On October 25 (U.S. Eastern Time), Pengai Medical Aesthetics International Holdings Group Co., Ltd. (“Pengai”) listed on the Nasdaq Stock Market. Founded in 1997, the Group currently operates 21 medical aesthetic centers, 19 of which are wholly owned or majority-controlled, spanning 15 cities across mainland China, Hong Kong, China, and Singapore.

Peng Ai’s revenues in 2016, 2017, and 2018 were RMB 585 million, RMB 697 million, and RMB 761 million, respectively, with revenue reaching RMB 393 million in the first half of this year. The number of active customers (those who received at least one medical aesthetic service per year) was 108,291, 128,892, and 178,657 in 2016, 2017, and 2018, respectively. In the first half of 2019, Peng Ai Medical performed 147,436 non-surgical and 27,984 surgical medical aesthetic procedures, with average spending per customer of RMB 1,364 and RMB 5,629, respectively.

In November, Beijing time, Bloomage Biotechnology, a leading player in the hyaluronic acid industry, successfully listed on the STAR Market. In the first half of 2019, the company’s raw material business continued to account for the largest share of its core operations, maintaining a steady growth trajectory with a year-on-year increase of 13.78%. Revenues from all major types of raw material products rose compared to the same period last year. Driven by a substantial increase in revenue from injectable modified sodium hyaluronate gel, the medical end-product segment achieved a year-on-year revenue growth of 51.66% from January to June 2019.

From January to June 2019, the functional skincare segment achieved significant growth in operating performance. In addition to the strong performance of its classic single-dose serum products following new brand positioning and the application of new technologies, the “Forbidden City Series” launched at the end of 2018 gained widespread consumer recognition and became a best-selling product line in the first half of 2019. During this period, the series generated cumulative revenue of RMB 40.562 million, driving a year-on-year increase of 122.06% in overall revenue for functional skincare products and contributing to a continuous rise in their share of total revenue.

From the perspective of the entire medical aesthetics industry chain, it is primarily composed of upstream pharmaceutical and medical device manufacturers, midstream medical aesthetic institutions, and downstream environmental factors closely related to industry development, such as O2O intermediary platforms for medical aesthetics and financial services, whileBloomage Biotech, Pengai, and So-Young are positioned in the upstream, midstream, and downstream segments of the industry, respectively., their ability to go public amid the prevailing “capital winter” has brought hope to countless practitioners.

According to Frost & Sullivan estimates, the size of China's medical aesthetics market has maintained a CAGR of 23.6% since reaching RMB 121.7 billion in 2014. The Chinese medical aesthetics market is projected to sustain a compound annual growth rate (CAGR) of 24.4% through 2023. The primary drivers of growth in the medical aesthetics market include increasingly younger consumers willing to increase spending on minimally invasive procedures, as well as a trend toward younger demographics seeking anti-aging treatments.

Furthermore, Frost & Sullivan projects that the growth of the medical aesthetics market will also be driven by rising disposable income among the middle class, increasingly mature medical aesthetic technologies, and growing societal and cultural acceptance of medical aesthetic procedures.

However, the current reality is that the medical aesthetics industry continues to face long-standing pain points and chaotic practices, such as high customer acquisition costs, a disordered physician workforce, and the prevalence of both legitimate and counterfeit institutions and products. Statistics from Frost & Sullivan show that the top five market players hold a combined market share of approximately 7.4%. These private aesthetic clinics include Mylike, Yestar, Aist, Yimeier, and Pengai, indicating persistent opportunities for mergers and acquisitions.

Next, you will learn:

1. How does the capital market view new breakthroughs in the medical aesthetics industry;

2. Why Is It Difficult for Purely Business-Model-Innovative Medical Aesthetics Projects to Alter the Supply-Demand Relationship at This Stage?

3. M&A Wars and Technological Roadmaps among Energy-Based Device Manufacturers and Hyaluronic Acid Producers;

4. Upstream players in the medical aesthetics supply chain, such as Hydrafacial, SkinCeuticals, Bloomage Biotech, and Filorga, have begun to venture into offline clinics or physical entities;

5. Why Are Chain Businesses Inherently Localized, and How Can Leading Enterprises Enhance Coverage Density and Improve Operational Efficiency?

6. As giants like Alibaba Health, Meituan Medical Aesthetics, and JD Health enter the market, how should platforms such as SoYoung, Gengmei, Meibei, and Yuemei respond?

Overall Impression: Scarce Top-Tier Assets, Companies Seek New Growth Curves

Amid the broader slowdown in economic growth, practitioners must adopt a more macroscopic perspective, focusing on developments over the next three to five years. The era of pursuing quick profits by exploiting information asymmetries and preying on consumers’ lack of knowledge is essentially over—a trend that has been particularly pronounced in the medical aesthetics industry this year.

In 2019, as downward pressure on China’s macroeconomic growth intensified further, ordinary consumers significantly curtailed their spending on medical aesthetics, competition in the medical aesthetics market became increasingly fierce, and customer acquisition costs continued to rise.

Pengai, which officially listed on the Nasdaq this year, reported revenues of RMB 585 million, RMB 697 million, and RMB 761 million in 2016, 2017, and 2018, respectively, with revenue reaching RMB 393 million in the first half of this year. Its sales and marketing expenses for 2016–2018 were RMB 231 million, RMB 300 million, and RMB 333 million, respectively, amounting to RMB 165 million in the first half of this year.

Other medical aesthetics companies, such as Yestar, reported revenues of RMB 405 million, RMB 723 million, and RMB 1.037 billion in 2015, 2016, and 2017, respectively, while their sales expenses amounted to RMB 130 million, RMB 254 million, and RMB 305 million. This high cost of sales is difficult to change or break through in the short term.

The medical aesthetics industry boasts relatively high gross profit margins, typically around 60%. However, after deducting the two major expenses of substantial marketing costs and labor costs, net profit margins usually fall below 10%. The phenomenon of high gross profits but low net profits is prevalent in the current medical aesthetics sector. It has become a widespread consensus among medical aesthetics institutions this year to strictly control advertising, personnel, and material costs, thereby ensuring growth in operating profits.

In 2019, the overall performance of the medical aesthetics market fell short of expectations, and the decline in stock prices in the secondary market also transmitted to the primary market. It is expected thatIn 2020, the overall medical aesthetics market will undergo industry reshuffling., the head-concentration effect is intensifying, which may create opportunities for M&A and consolidation.

From a financing perspective, publicly available data show that large-scale funding rounds are few and far between. The capital market remains cautious toward the medical aesthetics sector as a whole, with funds increasingly flowing to leading enterprises that either demonstrate clear high-growth potential or have already validated their business models.

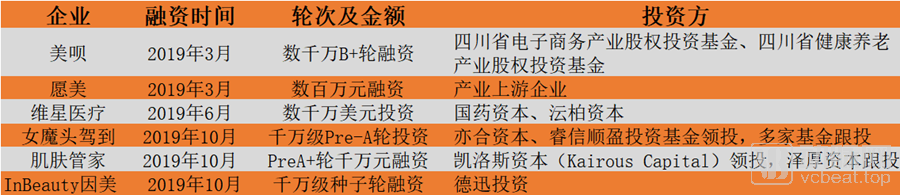

Companies That Publicly Announced Completion of Financing in 2019

Based solely on an assessment of the external financing environment,In 2019, high-quality assets were scarce and remained expensive., inferior assets are relatively cheaper than in previous years, while high-quality assets are scarce, making overall valuations appear to have declined. However, premium targets never lack investors; the listings of So-Young, Pengai Medical, and Bloomage Biotech on NASDAQ or the STAR Market this year serve as clear proof.

Sinopharm Capital, jointly established by China National Pharmaceutical Group and the Sinopharm Capital management team, is a professional private equity investment firm specializing in the healthcare sector. Sinopharm Capital invested in Yanshu Medical Aesthetics in 2017 and co-invested in Singapore’s Weixing Medical Technology in June 2019, demonstrating its continued optimism about the entire medical aesthetics industry.

Wang Wei, Senior Investment Manager at Sinopharm Capital, stated: “The current turbulence in the medical aesthetics industry is a positive development. At present, competition in first- and second-tier cities has become increasingly intense and homogeneous. For instance, in certain new first-tier cities, the growth in supply has far outpaced the increase in medical aesthetics penetration rates, leading to price wars. This market consolidation will facilitate the healthy development of the industry.”

In Wang Wei’s view, the following areas in the medical aesthetics industry may yield new breakthroughs:

First, from the perspective of talent, the industry’s continued improvement will attract an increasing number of high-caliber, highly educated professionals from cross-disciplinary and non-traditional backgrounds. This will create a “catfish effect,” compelling incumbent practitioners to accelerate their professional development, innovation, and competitiveness, thereby ensuring survival of the fittest;

Second, Informatization and Data-Driven OperationsThis will bring new opportunities to the industry. The pursuit of efficient operations to optimize profit margins and address supply-side efficiency issues may give rise to new operational and business models;

Third, the integration of medical aesthetics and life beauty, how to truly integrate clients from lifestyle beauty services and medical aesthetics to build a long-tail service cycle is worthy of close attention.

In a nutshell, a large number of domestic medical aesthetics startups in ChinaAfter achieving a breakthrough in a single area, attempt to lay out the upstream and downstream industrial chains., the sum of all business growth points identified from existing resources and capabilities, seeking newBusiness Growth Curve, specifically manifested asExpand into new products, new customers, or new fields。

We believe that medical aesthetic projects based purely on business model innovation attempt to alter pricing and enhance efficiency by leveraging scale to achieve theoretical economies of scale,Due to the lack of sustained capital for continuous "cash burn," it is difficult to alter the existing supply-demand relationship., validate the business model and establish a profit zone.

The medical aesthetics industry may be truly entering a phase of seeking tangible business growth through innovations in technology, products, and services. Medical aesthetics practitioners are adopting a more pragmatic approach by tapping into lower-tier markets, expanding new products and services to reach new consumer segments, and leveraging digital technologies to enhance service boundaries and efficiency.

Profit-Driven Consolidation and M&A: Oligopolistic Landscape Takes Shape Amid Fierce Competition in Pharmaceuticals and Medical Devices

This year, the upstream pharmaceutical and medical device sectors have witnessed significant changes and consolidation efforts, involving leading industry players.

On June 25, AbbVie announced that it would acquire Allergan at a valuation of $63 billion. This acquisition will become one of the largest mergers in the healthcare industry this year, with the new company owning Humira, AbbVie's global top-selling drug, and Botox, Allergan's flagship product.

On November 19, Baring Private Equity Asia announced that its affiliated private equity fund (BPEA) had agreed to acquire Lumenis from XIO Group, a transaction that valued Lumenis at over $1 billion.

On November 20, an investment fund managed by the U.S. private equity firm Clayton, Dubilier & Rice announced the acquisition of Hologic’s Cynosure medical aesthetics business for a total consideration of $205 million. Financial details of the transaction were not disclosed.

M&A History of Upstream Medical Device Manufacturers

As the supply side, changes in pharmaceuticals and medical devices are closely related to shifts on the demand side.

From the demand side, medical aesthetic services are primarily provided by the following departments: cosmetic surgery, cosmetic dermatology, cosmetic dentistry, and traditional Chinese medicine (TCM) aesthetics. In summary, the changes are mainly reflected in:

First,Procedures or therapies with high technical barriers are seeing stable or rising prices (e.g., breast augmentation, rhinoplasty, and brands of botulinum toxin type A).Procedures or therapies with low technical barriers, such as double eyelid surgery, hyaluronic acid injections, and minimally invasive or non-invasive energy-based devices, are seeing declining prices and intensifying competition, which in turn is pressuring pharmaceuticals and medical devicesFocus on innovative technologies, expand product lines or indications, and maintain market position by deterring potential competitors from entering the market., which constitutes the underlying logic of mergers and acquisitions for pharmaceutical and medical device companies: to conduct bolt-on acquisitions of other technology-driven enterprises or to in-license products.

Second, current aesthetic medicine procedures are more refined, minimally invasive, and personalized.Consumers Place Greater Emphasis on Non-Surgical Aesthetic Procedures, strong demand for anti-aging, skin tightening, lifting, and wrinkle reduction, non-invasive and minimally invasiveNew Optoelectronic Technologies, Adipose Medicine, Hair TransplantationFields such as these have recently emerged as new hotspots, gaining gradual acceptance among mainstream consumers. The customer base is becoming increasingly diverse in age, and non-surgical medical aesthetics has become the largest revenue source for institutions. Energy-based device manufacturers are undergoing a continuous phase of mergers and acquisitions, which will further intensify industry competition. A landscape has already taken shapeAn oligopolistic landscape led by Apax Partners, El.En., XIO, Fosun Pharma, and Hologic。

Specifically, cosmetic surgery primarily includes surgical aesthetic medical services and injectable aesthetic medical services. Surgical aesthetic medical services refer to surgical procedures aimed at altering the appearance of various facial or body parts (such as the eyelids, nose, breasts, and face), typically involving local or general anesthesia, as well as partial or full incisions.

Injectable aesthetic medical services involve injecting substances such as type A botulinum toxin, collagen, poly-L-lactic acid, and hyaluronic acid dermal fillers into targeted areas of the face or body to reshape facial or bodily contours or reduce wrinkles. Compared with surgical aesthetic medical services, injectable aesthetic medical services offer a faster recovery time, lower risk, and cause only minimal trauma to the body without leaving surgical incisions.

Aesthetic dermatology primarily offers energy-based device treatments. By utilizing various forms of energy-based devices, including lasers, radiofrequency instruments, ultrasound devices, intense pulsed light (IPL) systems, and cryolipolysis machines, these treatments achieve aesthetic outcomes such as pigmentation removal, skin brightening and rejuvenation, body contouring and shaping, skin hydration, skin lifting and tightening, hair removal, scar revision, soothing of sensitive skin, mole removal, acne treatment, and female intimate area treatments.

According to Frost & Sullivan data, among the most popular surgical aesthetic medical services (including double eyelid surgery, breast augmentation, thigh liposuction, and rhinoplasty), the average price of breast augmentation increased steadily from 2013 to 2017 and is projected to grow slightly from 2018 to 2022, primarily due to its increasing popularity and relatively high technical requirements.

The approximate average price of rhinoplasty remained relatively stable from 2013 to 2017 and is projected to remain stable from 2018 to 2022. The approximate average prices of double eyelid surgery and thigh liposuction both decreased slightly from 2013 to 2017 and are expected to continue declining from 2018 to 2022, primarily due to intense competition.

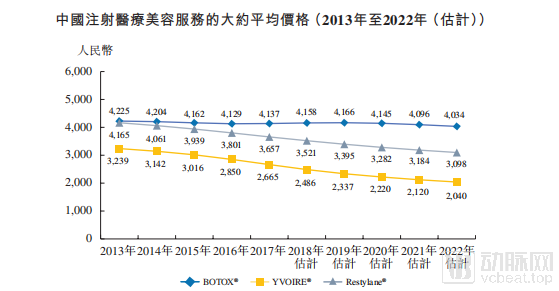

Injectable medical aesthetic services primarily include the administration of type A botulinum toxin and hyaluronic acid. As the only imported brand of type A botulinum toxin approved in China, the approximate average price for Botox injections remained stable from 2013 to 2017. From 2018 to 2022, the approximate average price for Botox injections is expected to remain stable.

Trend in Average Prices for Injectable Medical Aesthetic Services

In terms of hyaluronic acid injections, the approximate average prices for Restylane and YVOIRE fell from RMB 4,165 and RMB 3,239 in 2013 to RMB 3,657 and RMB 2,665 in 2017, respectively, primarily due to intense market competition. The approximate average prices for Restylane and YVOIRE injections are projected to continue declining rapidly from 2018 to 2022, as these two overseas brands face increasingly fierce competition from domestic brands.

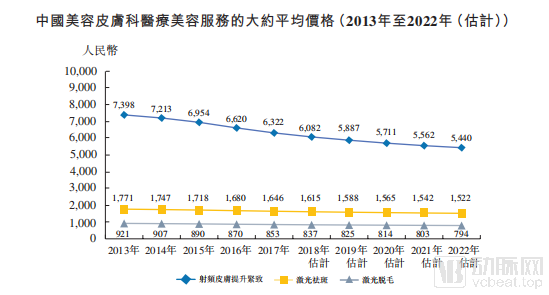

The approximate average prices for radiofrequency skin tightening, laser pigmentation removal, and laser hair removal decreased from RMB 7,398, RMB 1,771, and RMB 921 in 2013 to RMB 6,322, RMB 1,646, and RMB 853 in 2017, respectively, primarily due to intense market competition. Facing competition from beauty centers that also offer energy-based device treatments, the approximate average prices for radiofrequency skin tightening, laser pigmentation removal, and laser hair removal are expected to continue declining during the period from 2018 to 2022.

Trend in Average Prices for Cosmetic Dermatology Services

Thus, it is evident that the pharmaceutical and medical device sectors experiencing significant changes are primarily concentrated in surgical procedures or therapies with low technical barriers, characterized by declining prices and intense competition, especiallyIn the fields of hyaluronic acid injections and minimally invasive or non-invasive energy-based devicesIn terms of market share, the sector is dominated primarily by foreign giants and a select few leading domestic enterprises. Photoelectric aesthetic devices from countries such as the United States, Israel, and Germany, as well as hyaluronic acid products from Sweden, the United States, and South Korea, benefit from an earlier industry start and have established relatively mature industrial chains.

Of course, leading domestic enterprises in China have developed independent R&D capabilities for products at various levels. The quality gap between their products and imported ones is gradually narrowing, market share is steadily increasing, and they are accelerating the substitution of imported products. Notable representative companies include Bloomage Biotech, Haohai Biological Technology, QiZhi Laser, Peninsula Medical, and Ouhua Meike. In some regions, industrial cluster effects have even emerged, such as the hyaluronic acid enterprises in Shandong Province.

Regarding the differences between domestic and foreign products, in terms of specific efficacy, Li Guanhui, a renowned attending physician in dermatological aesthetics, told VCBeat: “In terms of therapeutic efficacy for injectable hyaluronic acid, there is little difference in the underlying technical principles between domestically produced and imported hyaluronic acids. The main distinction lies in whether they are monophasic or biphasic cross-linked, with the key difference being in the manufacturing process, specifically the uniformity of molecular weight.”

Next, we examine industry shifts through the latest strategic moves of three leading companies: Sisram Med, Allergan, and Bloomage Biotech.

Sisram Medical’s flagship products include the Soprano series, primarily used for hair removal; the Harmony series, a versatile multi-application platform approved by the FDA for up to 60 indications; and the Accent series, mainly used for body contouring and skin tightening. All of these belong to the medical aesthetics product line. Additionally, Sisram offers FemiLift, a minimally invasive medical aesthetic device for treating various female health issues. Furthermore, Sisram Medical Technologies provides lifestyle beauty product lines such as Rejuve and Reshape.

Sisram Med will continue to provide modular, high-performance, and cost-effective device systems based on the latest clinical research and cutting-edge technology. Through an analysis of global trends and market opportunities, the company has identified three major “hotspots”—body contouring, skin treatments (particularly skin repair), and women’s health. In line with its “medical + aesthetic” product strategy, Sisram Med will further expand its minimally invasive surgical product portfolio and develop new indications.

In June 2019, Allergan announced that its CoolTone muscle stimulation system had received FDA approval for improving, strengthening, and tightening abdominal muscles. Additionally, CoolTone is indicated for stimulating the buttocks and thighs to aid in muscle contouring. In August, Allergan announced that the marketing application for Juvederm Voluma had been approved by China’s National Medical Products Administration (NMPA) for mid-face filler treatments, filling a gap in this field within China. Previously approved by the U.S. FDA, Juvederm Voluma leverages proprietary Vycross technology, with clinical trial data demonstrating that its lifting and contouring effects last up to two years. It has become the preferred solution for aesthetic consumers and professional physicians in over 100 countries worldwide for restoring mid-facial volume.

Bloomage Biotech’s main business revenue is primarily derived from three product categories: raw materials, medical end-use products, and functional skincare products. As of June 2019, these three categories accounted for 43.05%, 24.91%, and 31.95% of the company’s main business revenue, respectively.

Among these, the primary logic driving the future development of the raw material business is the continuous expansion of application areas for hyaluronic acid. Medical end-products are also increasingly adopting a combination strategy. The existing small-particle variant of Runbaiyan serves as a traffic-driving product, primarily facilitating customer acquisition for the company. Meanwhile, the company has successively launched the Runzhi brand, which contains lidocaine (anesthetic), targeting the mid-to-high-end market. The company now offers a comprehensive portfolio of hyaluronic acid dermal fillers, including monophasic, biphasic, monophasic with lidocaine, and biphasic with lidocaine formulations, to meet the diverse needs of different customer segments. The future approval of botulinum toxin products will further enrich the company’s aesthetic medicine end-product lineup.

Although the skincare business only began to gain momentum in the past two years, it benefits from nearly 20 years of accumulated expertise in raw material technologies and has long served as a supplier to various international cosmetic brands, thereby gaining deep insights into specific consumer needs. Initially launched with only the Biohyalux brand, the company’s skincare portfolio has since expanded into a comprehensive product matrix. Targeting distinct consumer segments and underpinned by proprietary patented technologies, the company continues to introduce new products, such as its recently launched men’s personal care line and maternal-and-infant care products, with hair care solutions planned for future release.

Bloomage Biotech currently organizes its business units by sub-brand, having successively established the Biohyalux Business Unit, Medrepair Business Unit, QuadHA Business Unit, DermaRun Business Unit, and BM Active Business Unit, along with an Innovation Business Unit dedicated to incubating new brands.

In summary, upstream manufacturers benefit from relatively standardized industry regulations and a concentrated industrial landscape, resulting in higher profit margins for leading companies. In the future, they will continue to focus their new product development on two key directions: reducing the "cost" of cosmetic procedures for patients seeking aesthetic enhancement and improving their "aesthetic appeal."Expanding Product Lines and Indications, technological innovation is driving industry development, and most private equity firms areStriving to Identify Exit Channels in 2019, with Strong Momentum for Upstream Integration and M&A。

Strengthening Local Chains by Focusing on High-Net-Worth Clients, with Data Middle Platform Capabilities as a Bottleneck

Midstream end-user institutions represent one of the most closely watched segments within the medical aesthetics industry. Against the backdrop of slower-than-expected IPO progress among leading chain operators, intense competition, challenges in breaking through existing financial models, and low net profit margins, Pengai’s successful listing on NASDAQ as the first to achieve this milestone has sparked explosive attention across the industry.

Overall, the midstream sector is categorized by hospital type into public hospitals and private hospitals. Private hospitals dominate in cosmetic and plastic surgery, while public hospitals focus more on trauma repair.

In terms of market share,Private institutions account for nearly 80% of the total market share., dominating the landscape. Public hospitals have a longer development history and benefited significantly from early policy dividends, such as policies facilitating technology introduction and physician benefits. However, as marketization accelerates on the medical aesthetics service side, private enterprises with stronger competitive awareness and boldness in market development will emerge as leaders capable of resource integration.

In terms of quantity, there are over 10,000 mid-tier medical aesthetic institutions in China, continuing to experience explosive growth at an annual rate of approximately 20%. These institutions are primarily concentrated in economically developed regions such as Beijing, Shanghai, Guangzhou, and Shenzhen, while markets in central and western China are gradually developing. In terms of scale, most institutions are relatively small, resulting in a highly fragmented industry with significant potential for consolidation and improvement. This sector is likely to become a key battleground for competition among various stakeholders. Large medical aesthetic hospitals that have already established branded identities are acquiring and integrating smaller hospitals, forming chain operations—a clearly visible trend.

Throughout its development, Pengai Medical has been committed to expanding its chain network layout. By implementing centralized network management, it has established a three-tier structure comprising large flagship hospitals, medium-sized hospitals, and small satellite clinics. This approach mirrors the expansion strategy adopted by most chain enterprises.

For brick-and-mortar hospitals, the ability to establish a chain network directly determines their ultimate competitiveness. Through chain operations, medical aesthetic hospitals can better compete with small and medium-sized peers in the industry. Regarding the benefits of chaining, Zhou Pengwu, Chairman of Pengai Medical, stated in a previous exclusive interview with VCBeat that competitiveness is mainly reflected in the following aspects:

First, centralized procurement by the group, as a leading medical aesthetics enterprise in China, it can achieve centralized procurement for 20 hospitals in the purchase of hyaluronic acid and botulinum toxin, basically ensuring the lowest procurement price nationwide;

Second, centralized allocation of expert physicians within the group, in medical aesthetic hospitals, physician compensation accounts for a high proportion of the group’s operating costs. Expert physicians are centrally allocated within the group and provide services across multiple hospitals through mechanisms such as multi-site practice, which not only effectively controls medical risks but also ensures fuller utilization of physicians’ workload, thereby spreading out and reducing their fixed costs;

Third, the national brand value continues to rise, which helps enhance consumers' trust and loyalty toward the brand and alleviate their concerns about medical safety.

As an investor in Peng Ai, Chuangrui Investment considers three key factors when selecting medical aesthetic hospitals for investment: compliance, encompassing hospital operations, equity structure, and financial status; growth potential, including revenue growth, sustainable expansion, and listing plans, specifically whether there is a clear path to going public. Its investment logic can be summarized as focusing on scalable and compliant investment opportunities.

It is an indisputable fact that no nationwide chain monopoly has yet emerged. However, by examining the new explorations and significant moves of leading chain institutions, we can gain insights into the development of terminal medical aesthetic institutions over the past year. Large-scale chain medical aesthetic institutions are beginning to expand their boundaries from a “heavy-asset” model to a “light-asset” model:

Beauty United already operates more than 50 medical aesthetic institutions. On November 22, 2019, So-Young and Beauty United Group officially announced the launch of China’s first shared medical aesthetic hospital, Beauty United Second Medical Aesthetic Hospital (hereinafter referred to as “Beauty United Second Hospital”). The hospital aims to integrate online and offline services to better support independently practicing plastic surgeons.

Currently, the existing shared hospital models in China are predominantly centered around ambulatory surgery centers and remain in their nascent stages. The Lige Second Hospital, jointly established by So-Young and United LiGe, marks the first application of this model within the medical aesthetics industry, aiming to pioneer a novel operational pathway. ThroughShared Model, Regis Second Hospital can eliminate various intermediary links between doctors and consumers, such as hospital operating costs and customer acquisition costs, charging doctors only for the use of the operating room based on time.

According to Li Bin, Chairman of United Regal, Regal Second Hospital provides dedicated shared operating rooms and nursing teams but employs no physicians of its own and does not accept direct patient visits. Currently, Regal Second Hospital primarily serves legally compliant, independently practicing physicians and aesthetic medicine doctors employed by small and medium-sized institutions. By sharing equipment, operating rooms, anesthesia teams, and other resources, the hospital enables these professionals to launch their practices with reduced overhead while delivering more comprehensive and high-quality services.

PhiSkin (hereinafter referred to as PhiSkin) is a benchmark brand in the chain of light medical aesthetics industry. Its co-founder Huang Kan revealed to VCBeat: "In 2019, we focused on two main things. The first was to focus more on the experience of high-net-worth customers and differentiated projects. The second was to strengthen our data center capabilities by integrating member data, project data, and operational data into a data middle platform, outputting standardized digital display formats."

In 2020, For Face will continue to focus on the mid-to-high-end demographic in the core CBD areas of first-tier cities, implementing a tiered management system within the same city. “Internally at For Face, this is categorized into First Class, Business Class, and Economy Class. Particularly for the O2O initiatives under the ‘Economy Class’ segment, we are committed to developing highly affordable and easily standardized medical services that can be administered by nurses or technicians. These offerings are more accessible than those of our main brand and support online appointment scheduling, online payment, and online skin analysis. Next year, we will prioritize the development of fully intelligent clinics, potentially operating them under sub-brands and through a franchise model.”

Reporters learned that another leading light medical aesthetics company, Xinghe Medical Aesthetics Technology (hereinafter referred to as “Xinghe”), achieved fourth-quarter revenue twice that of its full-year 2018 performance. Tian Kai, COO of Xinghe, highlighted the following key points:

First, Xinghe has already completed its layout in East China and North China. In the future, it will focus on expanding its business in South China by opening 4–5 new stores, bringing the total number of stores in South China to 6–7 and initially forming a nationwide chain presence.

Second, develop the core system of the intelligent middle platform to integrate all data and assess the aesthetic medicine expertise of both consumers and senior staff; this system is scheduled for a key market launch next year, serving both B-end and C-end customers.

Third, in the second quarter of 2019, Singtel launched a local premium lifestyle services platform—Singtel S.A.Y.—collaborating with merchants, key opinion leaders (KOLs), and users. In 2020, the S.A.Y. platform will be registered as a system to effectively address the challenge of customer acquisition in local lifestyle services.

For Fanxing Light Medical Aesthetics, a standout enterprise, key business developments in 2019 included: first, successfully validating the “Light Medical Aesthetics Single-Store 2.0” operational model, with both existing clinics already achieving profitability at the individual store level; second, preparing to open two additional clinics, which will establish it as the light medical aesthetics brand with the largest chain presence in Shaanxi Province and enable gradual regional coverage.

Liu Tengfei, founder of Fanxing Light Medical Aesthetics, told reporters that from a user perspective, light medical aesthetics has become a new growth driver in the aesthetic medicine market. “The primary demand of light medical aesthetics users is for more refined facial features, which requires long-term, repeated professional services. Therefore, clinics need to be geographically close to users, and chain operations facilitate accessibility. Meanwhile, prices must be affordable. Finally, by leveraging skilled physicians to provide professional services and deliver a positive user experience, we identify our new opportunity.”

Regarding the market for minimally invasive aesthetic medicine, Liu Tengfei believes that internet-based medical aesthetics platforms have enhanced user awareness and improved access to information. Meanwhile, the accelerated iteration of products and technologies is driving greater safety and diversification across categories. These developments are continuously improving supply-demand dynamics and further expanding consumption scenarios for minimally invasive aesthetic procedures. The supply from clinics offering such services is steadily increasing, gradually trending toward large-scale operations.

As a representative of boutique skin care chains, YSPLUS Yan Shi Skin Care Center is currently in discussions with potential franchise partners across more than 10 cities nationwide, and plans to open its third and fourth company-owned stores in Shanghai’s Pudong and Changning districts, respectively, in 2020.

It is worth noting that upstream players in the medical aesthetics supply chain, such as Hydrafacial, Skinceuticals, Bloomage Biotech, and Filorga, have already expanded into offline clinics or physical entities. By leveraging rapidly standardized products and service systems to establish boutique clinics, these companies may emerge as future competitors to chained medical aesthetics clinics. The growth potential for functional skincare products is significant.

China Galaxy Capital is a leading Chinese new-economy investment bank with nearly two decades of history, focusing on the global TMT, consumer, and healthcare sectors. In the medical aesthetics field, China Galaxy Capital has served industry leaders such as United Beauty Group and Huahan Medical Aesthetics. Looking ahead at the medical aesthetics industry, Liu Zeyuan of China Galaxy Capital shared insights with VCBeat on the emerging growth trajectories and variables within the midstream segment of the medical aesthetics value chain, summarizing them as follows:

First, penetrate new lower-tier markets.As competition in the medical aesthetics market of first-tier cities reaches a fever pitch, provincial capitals and second- and third-tier cities have become the next main battlegrounds. The key success factors for victory lie in securing high-quality physician resources, delivering superior customer experiences, and executing effective brand marketing and promotion.

Second, the "He Economy" is experiencing explosive growth.In recent years, medical aesthetic procedures for men have developed rapidly. Services once considered the exclusive domain of women—such as hair transplantation, eye and nose surgery, laser skin rejuvenation, and cosmetic skincare products—have seen increasing penetration rates among men, particularly the younger population. In the future, a wave of medical aesthetic chains focusing on the “he economy” may emerge.

Third, the new business model of “private-label products + offline chain services.”Leading medical aesthetics chain service providers will penetrate and integrate into the upstream product sector by developing and designing their own beauty or functional skincare brands, leveraging the advantages of their proprietary offline chain networks to rapidly capture market share. This strategy aims to enhance end-consumer stickiness while improving overall profitability.

of the medical aesthetics industrySubspecialtyDeveloped as a standalone single-category productSingle-Store Financial ModelThe situation is expected to improve. Initially, these services were spun off from the broader category of non-surgical medical aesthetics; however, this sector is highly competitive, making it difficult to establish a strong brand advantage. In contrast, the hair transplant niche has seen the emergence of large-scale companies such as Biliansheng, Yonghe, and Damai (Kefayuan). Similarly, there are chain brands specializing in fat grafting that boast more favorable financial models. Conversely, conditions like acne, characterized by diverse etiologies and complex treatment modalities, are not well-suited for single-specialty clinics.

We believe that medical aesthetic clinics are an offline business. Returning to the essence of offline business, first,The issue to be addressed is the local layout density., which is also the underlying reason why most medical aesthetics chains are strengthening their regional layouts.

Secondly, it is essential to strengthen internal capabilities to enhance efficiency and reduce costs, primarily by addressing the challenges of “patient acquisition” and “physician engagement.” Whether by bolstering the capabilities of the data middle platform, targeting differentiated user segments, or building a physician-shared medical platform, the strategy relies on service, technology, and products to address the needs of those with the most acute pain points.

Finally, after completing the initial layout of scale, involving the upstream and downstream of the industry, such as clinics developing functional skincare brands to increase customer acquisition scenarios, while functional skincare brands also open offline stores to seek conversion and find new growth curves.

The “medical” nature of healthcare services determines that in the growth path, letIt is difficult for medical aesthetics companies to achieve exponential growth in their business within a short period., cost reduction is difficult; efforts must focus on improving efficiency or expanding the profitable growth zone.

Traffic Giants Enter the Fray: Shortened Decision-Making Pathways and Accelerated Digitalization

On May 2, Eastern Time, SoYoung listed on the Nasdaq. This marked SoYoung’s pinnacle moment and the most prominent milestone for internet-based medical aesthetics platforms.

In the medical aesthetics industry, downstream internet platforms are leading a transformation in customer acquisition models. Given the high degree of marketization and the lengthy consumer decision-making process inherent to this sector, these platforms leverage internet technologies to further increase the penetration rates among institutions, physicians, and users. They address information asymmetry across the multi-sided supply and demand landscape, enhance overall operational capabilities, and serve as an informational bridge between suppliers and consumers. This improves decision-making efficiency and diversifies channels, thereby reducing both customer acquisition and consumption costs.

In the past, medical aesthetics institutions relied heavily on traditional marketing channels. Online customer acquisition was primarily driven by paid search engine rankings. However, this pay-per-click model delivered only one-way, purely promotional content, failing to bridge information asymmetry or earn genuine consumer trust. Consequently, competition among institutions merely continued to drive up marketing costs.

Compared with the comprehensive search engine model, from the perspective of business model innovation, medical aesthetics apps represented by So-Young reorganize supply, organize production or facilitate transactions in a way that increases efficiency and reduces costs. Specifically, they acquire and retain users through high-quality “content pools,” and maximize monetization from the merchant side through intensive services and operations.

As traffic concentrates, platform bargaining power and overall monetization rates will also evolve: in terms of revenue models, this may initially manifest as a gradual increase in commission fees; at a certain stage, the penetration rate of information services will grow rapidly, ultimately enhancing comprehensive monetization capabilities.

Based on its performance in the quarters following its IPO, increasing the penetration rate among medical aesthetics consumers and achieving rapid user growth have become So-Young’s strategic priorities and long-term objectives.

On one hand, So-Young is exploring how to better serve users in the medical aesthetics industry by launching the “Chi Yan Yi Xuan” brand, which targets consumers in China with high-quality medical aesthetics needs, curating the finest medical aesthetics resources and providing one-stop concierge services.

On the other hand, an industry consensus holds that physicians, as the core element of the sector, will increasingly step into the spotlight. In 2019, the number of SoYoung’s “Million-Revenue Physicians” (referring to physicians generating over RMB 1 million in gross merchandise value on the SoYoung platform) increased by 70% year-on-year. These physicians share common traits: strong professional expertise and proficiency in leveraging internet tools to communicate with medical aesthetics consumers. In addition to providing physicians with a suite of operational tools and display platforms online, SoYoung has also begun to close the service loop offline. For example, it jointly invested with Ligear Group, a physician entrepreneurship support platform, to establish Ligear Second Hospital, which has officially commenced operations.

In addition to So-Young, other medical aesthetics apps such as Gengmei, Meibei, and Yuemei are also making various attempts.

In 2019, the Gengmei app focused on intelligentizing medical aesthetics, strengthening its platform, educating the market, deepening market penetration, and upgrading its brand. In 2020, Gengmei will continue to upgrade its AI system, disseminate medical aesthetic content and promote healthy values of beauty, helping users select appropriate doctors and procedures. It will curate meticulous and skilled physicians for users, continuously optimize the platform, rigorously verify the qualifications of doctors and institutions, strictly screen authentic case studies, and comprehensively safeguard user rights and interests.

In 2019, Meibei focused on five key areas: content upgrading, platform strengthening, talent enrichment, market expansion, and brand promotion. For 2020, Meibei’s strategic plans include: first, continuing to deepen its presence in plastic surgery by refining the rigorous selection mechanisms for hospitals, doctors, and consultants; second, expanding into full-category demands by extending services to dermatology and dentistry; third, optimizing AI technology to enhance the depth of artificial intelligence-driven services; fourth, increasing video content production and leveraging micro-variety shows to provide users with engaging, humorous, and in-depth popular science education on medical aesthetics; and fifth, penetrating deeper into the medical aesthetics industry chain by starting from the terminal market, serving users, institutions, and doctors effectively, while gradually expanding upstream to manufacturers and other suppliers to achieve a closed-loop business model that efficiently serves the entire medical aesthetics industry chain.

In recent years, the fierce competition between two leading platforms, So-Young and Gengmei, first drew significant attention to medical aesthetics apps within the industry. Subsequently, tech giants such as Meituan Medical Aesthetics, Tmall, and JD.com entered the market. Leveraging their massive traffic portals and adopting a model that integrates community engagement, user reviews, and e-commerce, they have often made medical aesthetics their fastest-growing segment.

For industry giants, consumer healthcare—a high-growth business segment—continues to maintain strong momentum. Taking the medical aesthetics industry as an example, transactions during this year’s Tmall Double 11 shopping festival surpassed the full-day total of the previous year within just 10 hours and 31 minutes, highlighting its significant potential.

In August this year, Meituan Dianping released its Q2 financial report, mentioning the inaugural Meituan Medical Aesthetics 618 Grand Promotion. Leveraging the momentum of e-commerce marketing trends, medical aesthetics transactions contributed approximately RMB 670 million in gross merchandise value to the platform.

Data from Meituan Medical Aesthetics’ Double 11 campaign showed that online consumer spending increased by more than 320% year-on-year. The top five subcategories in highest demand were skin rejuvenation, wrinkle reduction and face slimming, minimally invasive eye procedures, anti-aging treatments, and skin booster injections. As spending power in the medical aesthetics sector continues to rise, consumer preferences are increasingly shifting toward “non-surgical” or “minimally invasive” aesthetic procedures.

Industry giants are committed to providing users with authentic and safe medical aesthetic services by standardizing and making transparent the information related to institutions, physicians, products, and services. Meanwhile, they aim to connect the upstream and downstream segments of the industry chain, integrate online and offline operations, and collaborate with industry partners to drive the transformation and upgrading of the medical aesthetics sector.

However, the difficulty of standardization remains a persistent bottleneck for the advancement of medical aesthetics platforms. Although various platforms are working to structure their service offerings into Stock Keeping Units (SKUs), aiming to subdivide all procedures in the medical aesthetics industry and break down comprehensive solutions into standardized actions—such as those centered around the eyes, nose, and facial contours—they seek to ensure that both beauty seekers and physicians share a consistent understanding of each procedure. Simultaneously, these platforms aim to commoditize physician services by modularizing doctors’ and experts’ time as much as possible, thereby achieving thorough digitalization.

Regarding the widely discussed view that Alibaba Health and Meituan Medical Aesthetics leverage “high-frequency services to disrupt low-frequency ones,” we believe that while tech giants possess substantial traffic and brand resources, medical aesthetics is inherently a low-frequency business. Moreover, treatment outcomes depend heavily on physicians’ skills and craftsmanship, distinguishing it from the sale of standard “commodities.” In-clinic medical services are difficult to standardize, and the decision-making process is lengthy. Consequently, platforms are unlikely to establish an absolute advantage in targeted user acquisition within a short timeframe.

Conversely, structured databases and community reviews are more critical for patient decision-making. For low-frequency services, optimizing the user experience and advancing the standardization and digital transformation of specialized categories can extend engagement time for both providers and users, thereby more effectively converting infrequent service interactions into positive word-of-mouth.

Refine patient evaluation systems, and expand and enhance the volume and efficiency of the supply side., bridging the gap between the “content” and “service” systems in medical aesthetics remains a long and arduous journey, which will be the key focus of the platform’s efforts in the next phase.

By reviewing the overall landscape of the medical aesthetics industry in 2019, summarizing the current status and growth drivers across the upstream, midstream, and downstream sectors, and assessing the performance of leading enterprises, we have gained a glimpse into just the tip of the iceberg of this entire industry.

China's medical aesthetics industry, overall,There remains substantial room for growth over the next five years., with the primary growth driver stemming from incremental markets in third- and fourth-tier cities. Although competition in the current medical aesthetics industry is intense, opportunities remain for new entrants.

On the one hand, the overall medical aesthetics market still possesses significant room for growth, offering substantial potential for future development by industry participants. On the other hand, the diverse needs of patients necessitate a diversified range of services within the medical aesthetics industry. This diversity makes it difficult for any single entity to dominate the market. Consequently, new entrants must precisely define their positioning within the industry and identify optimal service entry points to secure a competitive advantage in the medical aesthetics market.

References and Related Reading: