Commercial Health Insurance and Value-Based Healthcare Practices: Domestic and International Insights

As China’s healthcare reform deepens, the upgrade toward a patient-centered and value-oriented healthcare system is profoundly impacting the industry. Commercial health insurance should be guided by value-based healthcare, deeply participating in the “tripartite linkage” of medical care, health insurance, and pharmaceuticals by expanding funding sources, providing insurance coverage, integrating service delivery, and strengthening industrial consolidation, thereby serving as a catalyst for deepening healthcare reform. In the future, commercial health insurance should not only mitigate the risk of medical expenses but also help drive the transformation of the healthcare model from being disease-centered to health-centered.

The white paper “Value-Based Healthcare in China: Promoting Industry Collaboration and Business Model Innovation to Accelerate Healthcare System Transformation,” jointly authored by Fudan University’s Health Finance Research Lab and iShakang, was recently released. The white paper provides an actionable blueprint for the development of value-based healthcare and cross-sector collaboration in China, and explores how payers—including commercial insurers—can facilitate the implementation of value-based healthcare. VCBeat has republished and edited the content of the white paper.

Value-based healthcare focuses on the overall health outcomes of populations, emphasizing the maximization of utility from limited resources. Building on the research by Professor Porter and colleagues, institutions such as the World Economic Forum have conducted related model studies and pilot projects, identifying four key drivers to advance the implementation of value-based healthcare. The transformation of payers is a critical leverage point among these drivers.

Four Key Elements of Value-Based Healthcare

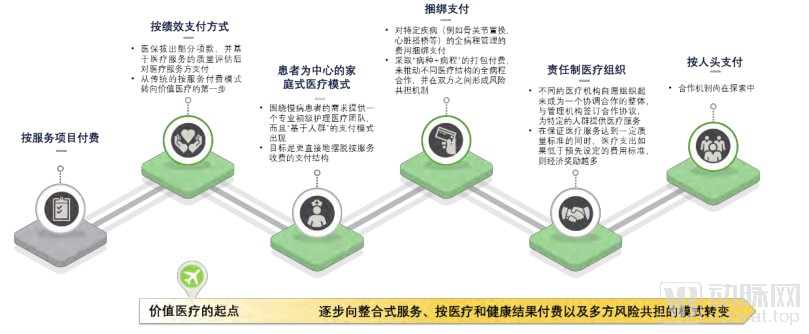

Whether for public health insurance or commercial health insurance payers, traditional coverage has predominantly been based on fee-for-service models. On one hand, poorly designed incentive structures in such models can easily lead to the overutilization of healthcare services and medical resources; on the other hand, adopting crude cost-containment mechanisms can result in under-provision of care and adverse population health outcomes. To address this challenge, the value-based healthcare model requires payers to shift their focus toward the actual value of medical services. This approach drives healthcare providers to transition toward patient-centered, integrated care delivery models, systematically collects and analyzes evidence related to healthcare quality and population health status, and establishes risk-sharing and incentive mechanisms with providers that tie reimbursement to actual clinical effectiveness and population health outcomes.

Major payers in various countries, including public health insurance systems and commercial health insurers, are actively moving in this direction under the guidance of value-based healthcare principles. Among developed nations, the United States has a relatively high proportion of commercial health insurers and has been quite active in exploring and innovating care delivery models. This includes pioneering managed care through the Health Maintenance Organization (HMO) model and, in recent years, actively participating in the promotion of Accountable Care Organizations (ACOs).

Commercial Insurance Companies Take the Lead in Promoting Managed Care

Similar to the development histories of other countries, the U.S. healthcare system has traditionally operated on a fee-for-service model, wherein healthcare providers are reimbursed by payers solely based on the volume of services delivered to patients. Since providers’ income is decoupled from treatment outcomes and service quality, this has led to inconsistent quality of care, as well as profit-driven overutilization and waste. To counterbalance these issues, U.S. commercial insurers pioneered the introduction of managed care concepts and models (including HMOs, PPOs, etc.) in the 1980s and 1990s, which subsequently experienced rapid growth.

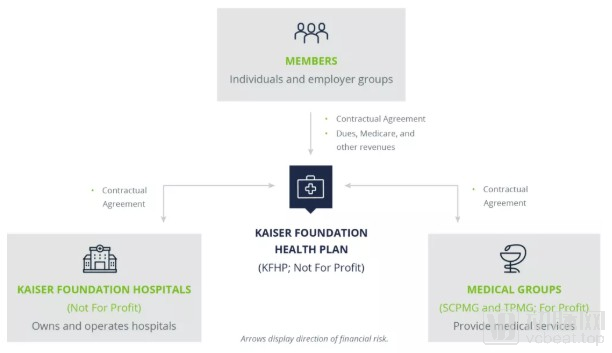

The HMO model adopted by Kaiser Permanente is a paradigm of managed care. It forms a commercial closed loop for healthcare delivery and payment, comprising three independent entities: the Kaiser Foundation Health Plan (KFHP), Kaiser Foundation Hospitals (KFH), and the Permanente Medical Groups. This structure provides exclusive medical and insurance services to enrolled members. The most distinguishing feature of HMO organizations is their emphasis on controlling healthcare costs and utilization, making this model the most effective among various healthcare systems in curbing medical expenditures. Within the Kaiser system, physicians negotiate an annual budget with the insurance arm each year, along with “risk-sharing agreements” tied to population health outcomes and medical spending. This mechanism ensures that both the insurance and physician sides share responsibility for health outcomes and cost containment. The annual budgeting and risk-sharing mechanisms incentivize physicians to consider economic costs, proactively seek the most cost-effective treatment options, and establish an integrated healthcare system with primary care physicians serving as gatekeepers.

Kaiser's HMO Model

The U.S. Government Promotes Value-Based Transformation

To further advance healthcare reform in the United States, the Obama administration signed the Affordable Care Act (ACA) into law in 2010. In addition to promoting universal health coverage for U.S. citizens, the ACA initially outlined the direction for transitioning toward value-based care, introducing a series of healthcare quality assessment standards and payment model reforms, thereby establishing the significant role of value-based payment models. The implementation strategy followed a pathway where the Centers for Medicare & Medicaid Services (CMS), the government agency responsible for administering Medicare and Medicaid, took the lead, with commercial insurers following suit. CMS played a pioneering and benchmarking role in this transition, launching a range of practical value-based care initiatives. Although these initiatives varied in design, they all shared the common goal of gradually shifting from the traditional fragmented, fee-for-service model to an integrated care model characterized by payment based on health outcomes and shared risk among multiple stakeholders.

Value-Based Care Programs in the United States: An Overview and Comparison

Accountable Care Organizations (ACOs) resemble Kaiser’s HMO managed care model. In this model, diverse healthcare providers—including primary care physicians, specialists, and hospitals—voluntarily form a collaborative network and enter into agreements with payers to deliver medical services to a defined population. The aim is to ensure that patients, particularly those with chronic conditions, receive appropriate care at the right time, thereby avoiding medical errors and unnecessary duplicate services. Under this model, provided that healthcare services meet established quality standards, ACOs are eligible for financial incentives if their medical expenditures fall below pre-set cost targets. In other words, while maintaining population health outcomes and clinical effectiveness, the greater the cost savings achieved, the higher the financial rewards received by the ACO. Practical experience with ACOs indicates that, compared with control groups, ACOs have consistently achieved comparable or superior levels of care quality, with a trend of year-over-year improvement. Regarding healthcare spending, ACO initiatives have overall succeeded in reducing costs, with more pronounced effects observed in programs employing risk-sharing mechanisms.

U.S. Commercial Health Insurers’ Participation in the Transition to Value-Based Care

During the Centers for Medicare & Medicaid Services’ (CMS) push toward a value-based care transformation, commercial insurers have actively participated. Taking Accountable Care Organizations (ACOs) as an example, data from Health Affairs Journal indicates that by the third quarter of 2019, approximately 1,600 ACOs across the United States were serving 44 million people. In terms of enrolled population, 60% were covered by commercial insurers, while 40% were enrolled in Medicare or Medicaid. Partly influenced by revisions to healthcare legislation under the new Trump administration, some companies adopted a wait-and-see approach toward ACO development. Nevertheless, the overall direction of value-based care has gained recognition within the healthcare industry; although the expansion of commercial insurance-backed ACOs has been slow, their overall development has remained relatively steady. Beyond policy uncertainty, observers have identified other factors hindering the growth of commercial ACOs, such as the complexity of ACOs as a managed care model, conflicts of interest among stakeholders, challenges in coordinating behavioral patterns, and the lack of relevant quality standards and foundational data. Policy recommendations have focused on promoting multi-party collaboration and sharing best practices, establishing quality standards and data-sharing platforms, and avoiding the pursuit of short-term results by fostering long-term commitment to ACO programs to measure effectiveness and ensure success.

Beyond promoting the development of managed care, commercial insurance companies have also introduced value-based innovative payment models for medical technologies such as pharmaceuticals and medical devices. In the pharmaceutical sector, for example, several U.S. insurers (including UPMC Health Plan and Harvard Pilgrim Health Care) have entered into agreements with AstraZeneca to implement value-based healthcare programs based on pay-for-performance for its anticoagulant Brilinta and diabetes medication exenatide. In the medical device sector, insurers such as UnitedHealthcare and Aetna have collaborated with Medtronic on value-based healthcare programs for insulin pumps, under which Medtronic guarantees clinically meaningful improvements in patient outcomes and shares financial risk with the insurers.

Implications for Us

Although there are significant differences between the Chinese and U.S. healthcare systems, and commercial insurers differ in their positioning and capabilities, the practical experience of U.S. commercial insurance companies in delivering healthcare value can serve as a reference for China.

First, on the basis of having relatively comprehensive basic risk prevention functions, health insurance should further focus on the concept of value-based healthcare, promote the development of managed care health insurance, and optimize the balance between medical expenditures and population health outcomes.

Second, the government and enterprises should actively collaborate to clarify the roles and relationship between public medical insurance and commercial health insurance, provide enterprises with clear policy guidance and support, and jointly promote the transformation of the healthcare system.

Third, the managed care system is relatively complex and requires collaborative efforts from multiple stakeholders, including government and enterprises, to establish foundational platforms such as standards and data infrastructure. Its successful implementation demands a long-term developmental perspective and sustained investment.

Commercial Health Insurance’s Exploration of Value-Based Healthcare

Over the past decade, China’s commercial health insurance sector has experienced rapid development, with its operational philosophy beginning to transcend traditional life insurance thinking. The industry is shifting from a sole focus on risk mitigation through expense reimbursement and financial compensation toward actively exploring a transformation toward value-based healthcare in commercial health insurance. In recent years, critical illness insurance and indemnity-based medical insurance products such as “Million Yuan Medical Insurance” and “Yao Shen Bao” have gained significant market popularity. However, these products offer limited intervention in policyholders’ health risk management and exhibit weak integration with healthcare service providers. Next-generation health insurance should place greater emphasis on integrating with medical services and health management, extending comprehensive health protection and management across the pre-disease, intra-disease, and post-disease stages. Furthermore, it should foster close collaboration with pharmaceutical and medical device companies as well as healthcare institutions to jointly explore new business models and holistic solutions for patient health.

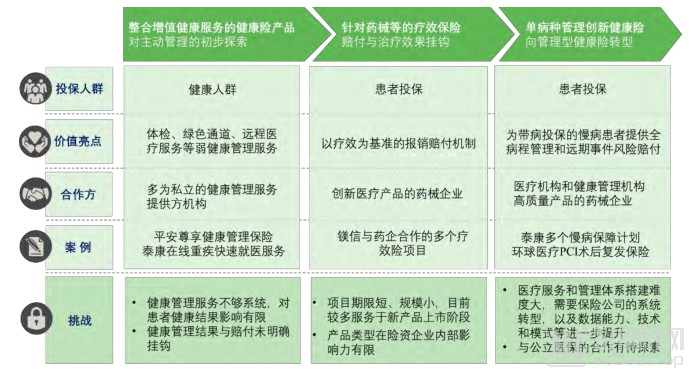

Based on developments in recent years, commercial insurance companies’ explorations in the field of value-based healthcare can be categorized into three models: (1) integrating health management services with medical insurance; (2) outcome-based insurance centered on innovative pharmaceuticals and medical devices; and (3) managed care insurance products represented by single-disease health insurance. The figure below summarizes these explorations by commercial health insurers in value-based healthcare across dimensions such as value proposition, covered populations, and targeted disease areas (Note: Innovative models of indemnity products such as “Million Medical Insurance” and “Yao Shen Bao” are excluded).

Commercial Health Insurance’s Foray into Value-Based Healthcare

Expand population coverage to improve public health levels and resilience against risks

In the first model, insurance companies identify the health needs and insured value of different participant groups and make initial attempts at proactive health management for these populations. However, as it stands, health management currently serves merely as a value-added service, with limited targeting and minimal actual impact on the health status of policyholders. In the long run, the integration of insurance with health and medical services remains a key area for innovation in commercial insurance, offering significant potential for advancement in technology application and business model design.

Case Sharing

As a global reinsurer specializing in health and life reinsurance solutions, Reinsurance Group of America (RGA) is committed to assisting its partners in China in driving the development of the health insurance market. RGA has conducted an in-depth analysis of customer demographics in China’s health insurance market and found that healthy/sub-healthy individuals and the elderly population represent the two ends of the human life cycle. These groups are key target segments for health insurance product innovation, as their health status can be improved and unnecessary medical expenses for individuals and the healthcare system can be controlled through health management and disease intervention. Therefore, RGA has collaborated with partners to design personalized products tailored to these two populations. For instance, targeting the high-risk elderly demographic, RGA partnered in 2019 with Shanzhen, a leading digital health platform with extensive experience in elderly care services, to launch China’s first senior medical insurance policy covering individuals up to age 80.

This insurance product is built upon Shan Zhen’s extensive experience in providing health services to the elderly population across China and its accumulated medical research data. It enables differentiated analysis of disease risks for elderly policyholders, providing technical support for RGA in product design, development, and risk control. Beyond precise big data-driven risk management, another distinctive feature of this insurance product is the integration of full-cycle health services. At the front end, it incorporates an industry-first post-underwriting medical examination risk control model. Instead of mandating pre-policy medical examinations, it adopts an incentive-based “post-examination” approach to tailor coverage scopes and sum-insured amounts according to each elderly policyholder’s actual health needs. The collaboration between RGA and Shan Zhen not only empowers end-to-end innovation in elderly medical insurance products, positioning them as pioneers and game-changers in this sector, but also introduces new paradigms for cooperation between the insurance industry and upstream and downstream players in the health ecosystem. Through this partnership, insurers are gradually transforming from mere payers into health managers.

Innovative Single-Disease Health Insurance Drives the Development of Managed Care in China

Single-disease health insurance, a category within the third model, is an innovative health insurance product that has emerged in recent years. It also represents commercial insurers’ exploratory transition from payment-oriented health insurance to management-oriented health insurance. Similar to other health insurance products, payouts for single-disease insurance are linked to events such as disease progression and recurrence. However, what sets it apart is that its core business focus lies in strengthening disease management for enrolled patients and reducing disease-related risks. Under this model, commercial insurance companies collaborate with multiple stakeholders, including healthcare providers, third-party health management organizations, and pharmaceutical and medical device manufacturers. In selected disease areas—primarily chronic conditions such as hepatitis B and chronic obstructive pulmonary disease (COPD)—they scientifically integrate medical products and service systems, encompassing clinical pathways, system development, data accumulation, patient–provider engagement, and disease management.

Centered on insured patients, providing medical solutions and ensuring their health status to achieve maximum medical value at minimal cost is the essential pursuit of value-based healthcare. From the perspective of project characteristics, the single-disease health insurance model will also become an entry point for cooperation between commercial insurance companies, basic medical insurance schemes, and public healthcare institutions. Taking Taikang Insurance’s pilot liver disease project as an example, commercial insurers collaborate with healthcare providers to conduct long-term tracking of clinical outcomes and full-course data for insured patients, applying efficacy and cost data to improve and innovate frontline clinical medication practices. Through payment mechanisms and technological tools, physicians are incentivized to focus on post-discharge follow-up management and comprehensive monitoring, while specialized follow-up centers are established to deliver patient-centered medical management services. This project is dedicated to promoting the tracking and quantification of patient outcomes and incentivizing cost-effective medical practices, thereby achieving the value-oriented goals of managed care health insurance.

In the article “As the Inflection Point Arrives, Is Commercial Health Insurance Ready?” published by Caijing Magazine, it is proposed that “commercial health insurance should be deeply integrated with medical services. Within the framework of the ‘Three-Medical Linkage’ (coordinated reform of healthcare, health insurance, and pharmaceuticals), commercial health insurance, as an increasingly important payer, not only collaborates with basic medical insurance to monitor and constrain irregular medical practices, but more importantly, achieves deep integration with healthcare providers and the pharmaceutical industry to foster positive interaction. This will drive the transformation of the healthcare model from a disease-centered approach to a health-centered one. This shift is both an intrinsic requirement for the development of commercial health insurance itself and an objective impetus driven by the continuously upgrading healthcare security needs of the Chinese population.”

This aligns with the direction advocated in our white paper, “Value-Based Healthcare in China.” Similar to the value-based healthcare transformation across other sectors of the medical and health industry, the future path for commercial health insurance should center on population health, focusing on improving patients’ clinical outcomes and overall health status. Furthermore, by strengthening health and medical service systems, enhancing data and technological capabilities, and deepening collaboration with basic medical insurance, commercial health insurers can expand their reach to broader populations, thereby promoting sustainable development. We propose the following recommendations:

First, we should actively develop new types of health insurance.

The role positioning of relatively simple indemnity-based insurance is inconsistent with the original intent of developing commercial health insurance. Insurance companies should not merely be recipients of health risk transfers engaged in a zero-sum game with policyholders; rather, they should serve as proactive health risk managers. Developing new types of health insurance oriented toward managing chronic diseases and preventing serious illnesses can effectively reduce economic and social operational costs. Medical insurance shifts the role of insurance companies from efficient risk pooling and payers to active health risk managers, striving to effectively control medical costs while improving the overall health status of the population and enhancing patients’ experience in accessing medical services. This approach aligns more closely with the guidance provided by the Healthy China 2030 initiative and the Action Outline for High-Quality Development of the Health Industry.

Second, deeply integrate with medical services to establish our own health and medical service system.

Forge closer collaborations with diverse healthcare providers to strengthen the medical service components within insurance products. The essence of value-based care lies in linking clinical outcomes of medical services to their costs, thereby achieving optimal therapeutic results within a defined budget. The involvement of commercial insurance plays a significant role in enhancing the affordability of medical technologies. However, since traditional health insurance exerts no intervention or guidance over the efficacy of medical technologies or the quality of services delivered by healthcare institutions, it does not constitute genuine value-based care practice. Currently, many commercial insurers are striving to integrate disease management or health management modules into their product designs, transitioning toward proactive managed-care health insurance. They will continue to intensify these efforts to optimize health outcomes for policyholders while meeting cost-containment objectives, embodying the principle that “the healthier the patients, the healthier the commercial insurance industry.”

Third, public-private partnerships to enhance data capabilities

To effectively manage the health of insured individuals, it is essential to have not only a service delivery system but also comprehensive whole-course patient data. In China, such whole-course patient data is relatively fragmented. While medical insurance agencies and public healthcare institutions hold substantial amounts of data, commercial insurance companies, health management organizations, and digital health enterprises also possess portions of it; however, overall, these data remain largely unstructured and dispersed. On one hand, some commercial insurers are actively building their own whole-course patient data systems based on current data sources. On the other hand, as the government promotes patient-centered chronic disease management systems in the future, commercial insurers should proactively seek participation in the upgrading of local healthcare systems. By collaborating with medical insurance agencies and public healthcare institutions, they can gradually establish scientific clinical pathways and standardized data systems for specific diseases.

Fourth: Explore innovative models of collaboration with the government and medical insurance programs to expand the coverage and enhance the protection level of commercial health insurance products.

Collaboration between commercial insurers and public medical insurance has a long history, evolving from initial assistance with underwriting and claims processing for basic and critical illness insurance, to the opening of personal account funds for purchasing commercial health insurance in certain provinces and cities, and most recently to government-organized group-purchasing supplementary medical insurance programs funded by insured individuals, such as the initiative launched in Zhuhai. Among the various models currently being explored by commercial insurers in the realm of value-based healthcare, single-disease managed care health insurance may emerge as an effective entry point for collaboration with public medical insurance, particularly in the area of chronic diseases that impose a heavy societal burden. Single-disease managed care health insurance not only helps rationalize current medical expenditures for public insurance but also effectively controls long-term risks through scientific early intervention and management, thereby further reducing future medical costs. Meanwhile, the drug formularies and supply chains of commercial insurers meet patients’ needs for payment and services regarding prescription drugs outside the centralized procurement list of public medical insurance, especially in the context of enhanced volume-based procurement markets.

Citation:

1. iSukang, "Value-Based Healthcare in China" White Paper

2. Wang Xinyi, “How HMOs Became Pioneers in Cost Control”

3. Li Hang, “As the Wind Rises, Is Commercial Health Insurance Ready?”

4. Jiang Guanjun, Huang Qinqin, “Outlook on the Development of New Health Insurance Guided by Healthy China 2030”