Domestic Microfluidics Technology Finds Early Success in IVD Sector as Four Companies Secure Hundreds of Millions in Funding and File IPO Prospectuses

The advent of microfluidics technology represents researchers' ultimate pursuit of automation and maximized efficiency.

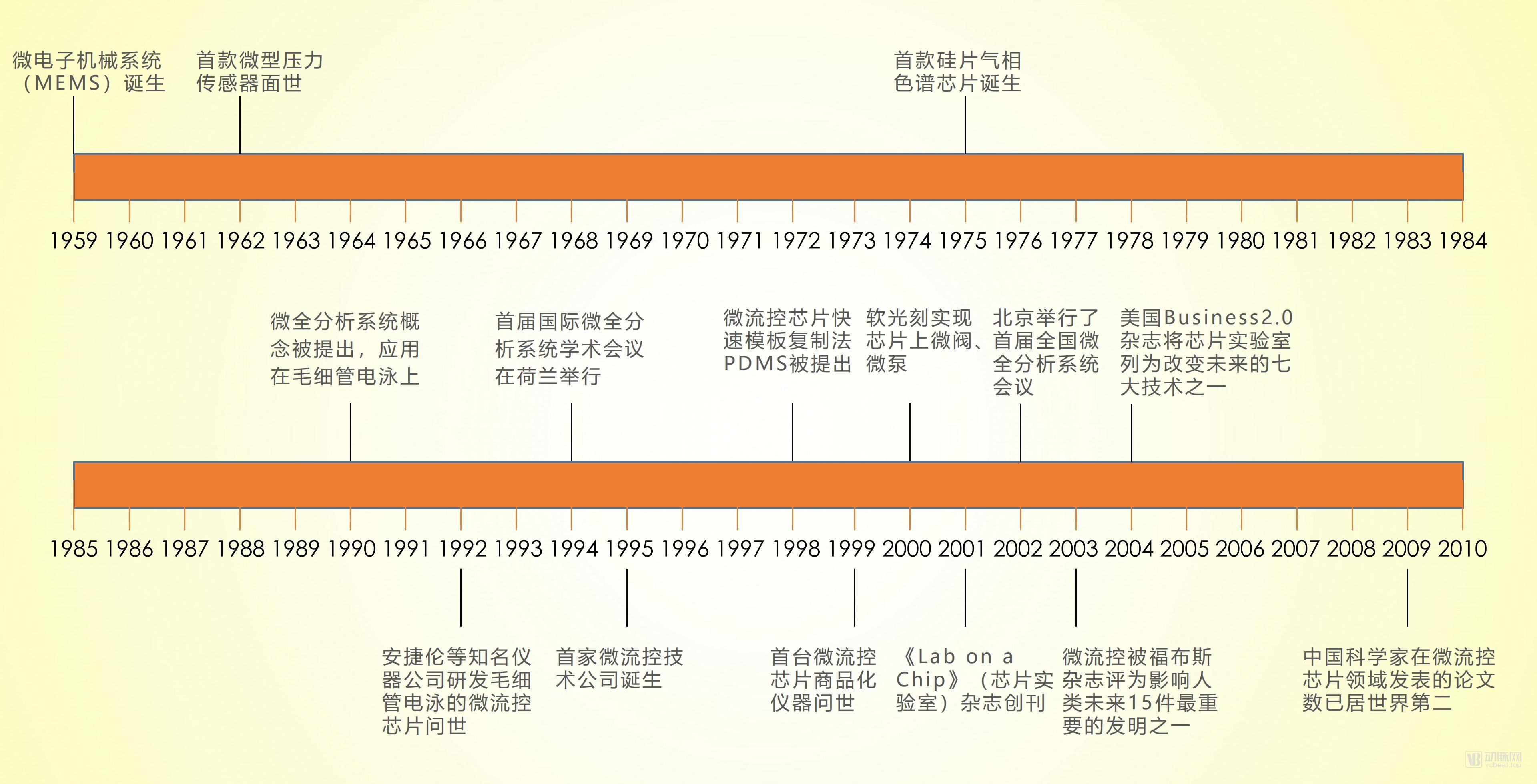

In the late 1950s, Professor Richard Feynman, a U.S. Nobel Laureate in Physics, foresaw that future manufacturing technologies would evolve along a path from macro to micro scales. In 1959, he miniaturized an experimental mechanical system using semiconductor materials, thereby creating the world’s first micro-electro-mechanical system (MEMS), which laid the foundation for the emergence of future microfluidic technologies.

From the perspective of the definition of microfluidics, the true emergence of microfluidic technology occurred in 1990. Manz and Widmer from the Swiss company Ciba-Geigy applied MEMS technology to achieve electrophoretic separation on a miniature chip—a process that had previously required capillary tubes—thereby proposing the concept of the Micro-Total Analytical System (μ-TAS), which is now commonly known as the microfluidic chip.

When Manz and Widmer first attempted microfluidics, their goal was to enhance analytical capabilities; however, once the concept of microfluidic chips was proposed, researchers quickly realized that reducing device dimensions would bring numerous benefits.

The “micro” in microfluidics refers to the miniaturization of experimental instruments and equipment (with dimensions ranging from tens to hundreds of micrometers); “fluid” indicates that the experimental subjects are fluids (with volumes ranging from nanoliters to attoliters); and “control” signifies the manipulation, operation, and processing of fluids on miniaturized devices. As a foundational technology, it integrates knowledge from multiple disciplines, including chemistry, fluid physics, microelectronics, and new materials. In theory, any experiment involving fluids should have a place for microfluidic technology.

Microfluidic chips are downstream application units of microfluidic technology. They employ MEMS technology to construct miniature biochemical analysis systems on solid chip surfaces, thereby enabling rapid and accurate processing and detection of inorganic ions, organic substances, proteins, nucleic acids, and other specific targets. By integrating key steps such as sample preparation, biochemical reactions, and result detection—traditionally performed in laboratories—onto a single small chip, they are hailed by the industry as “Lab-on-a-Chip.”

Following the development of capillary electrophoresis on a chip by Manz and Widmer in 1990, both the scientific community and industry actively engaged in this emerging field, undertaking research and development of various microfluidic chips with capillary electrophoresis as the primary application. Two years later, medical device companies such as Agilent, Shimadzu, and Hitachi had completed the development of their respective microfluidic products/systems and introduced them to the market.

In 1994, Mike Ramsey, a researcher at Oak Ridge National Laboratory in the United States, improved the sample injection method for chip-based capillary electrophoresis based on the original work of Manz and Widmer, thereby enhancing its performance. In the same year, the first International Conference on Micro Total Analysis Systems was held in Enschede, the Netherlands, bringing microfluidic chips fully into the public eye. The following year, Caliper Life Sciences, the world’s first company dedicated exclusively to microfluidic chip technology, was established in Massachusetts, USA.

History of Microfluidics Technology Development (Charted by VCBeat)

Since the inception of the first microfluidics technology company in 1995, microfluidic chips have officially embarked on the path of commercialization and industrialization. Rapid prototyping methods for chips using PDMS, as well as soft lithography-based microvalves and micropumps, were proposed successively. In 1999, Agilent Technologies and Caliper Life Sciences jointly launched the first commercialized microfluidic chip instrument, which was applied in the fields of bioanalysis and clinical analysis.

Microfluidics, a technology that had been developing abroad for a decade, did not officially enter China until the early 21st century. With the gradual rise of the in vitro diagnostics (IVD) industry in China, microfluidics has only become widely recognized in recent years.

A Flourishing Landscape of R&D Technologies

The first shot in the microfluidics race was fired by Lab on a Chip. Founded in 2001, this journal is dedicated to publishing research articles on microfluidics technology. A year later, China hosted its first academic conference focused on microfluidics—the inaugural National Conference on Micro Total Analysis Systems held in Beijing—marking a breakthrough in the large-scale integration of microfluidic chips.

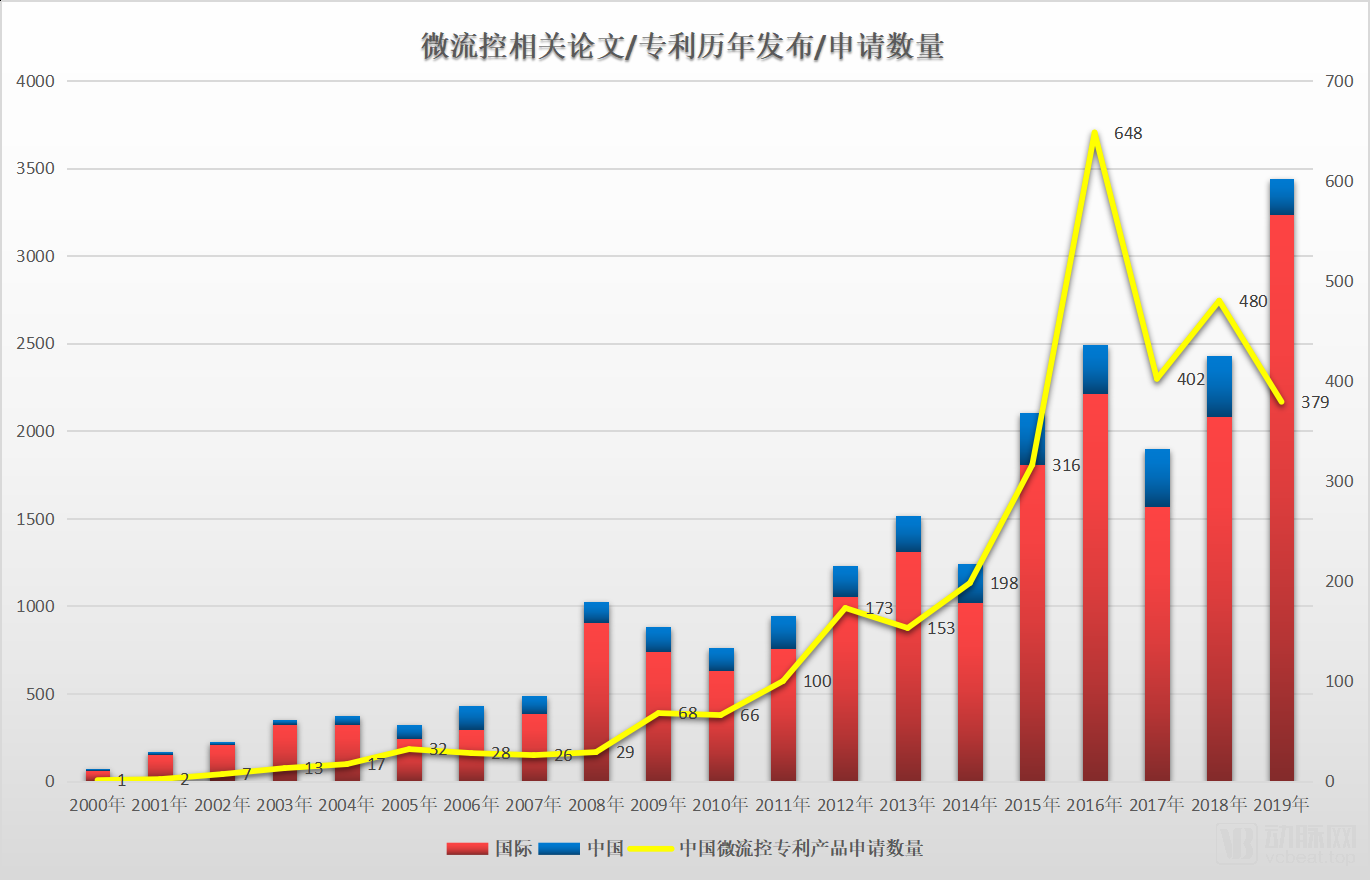

China’s research into microfluidics began at this point. Starting in 2002, a wave of patent applications for microfluidics-related products gradually emerged in China. By 2012, the annual number of such applications had reached 100, peaking in 2016 with over 600 applications filed in a single year. Although the annual number of patent applications has since declined somewhat, it has remained above 400 per year. Meanwhile, Chinese scientists rank second worldwide in the number of published papers in the field of microfluidics, and China ranks second only to the United States in the number of patent applications for microfluidics-related products.

Statistical Chart of the Annual Number of Microfluidics-Related Papers Published and Patents Applied for in China and Abroad Since the 21st Century (Chart by VCBeat)

With the deepening research on microfluidic technology year by year, people have also made more in-depth explorations in related fields such as material selection and process technology for microfluidics.

In terms of fabrication materials for microfluidics, silicon, a semiconductor material, was initially the preferred choice for manufacturing microfluidic chips. However, due to the continuous expansion of application scenarios for microfluidic chips, silicon has been abandoned because it cannot withstand high pressure and is incompatible with optical detection techniques.

This was followed by the advent of glass-based microfluidic chips. Glass offers excellent electroosmotic and optical properties, making it theoretically an ideal material for fabricating microfluidic chips. However, glass is difficult to pattern via photolithography and etching; the fabrication process is complex, time-consuming, and costly, which has hindered its large-scale adoption.

In contrast, polymeric materials demonstrate distinct advantages. Polymer processing is straightforward, raw materials are inexpensive, and they exhibit favorable properties such as excellent electrical insulation, high-voltage resistance, thermal stability, biocompatibility, gas permeability, and a low elastic modulus. These characteristics enable their widespread application in capillary electrophoresis microchips, biochemical reaction chips, and various optical detection systems. Organic polymers, represented by polydimethylsiloxane (PDMS), have become the preferred materials for the fabrication of microfluidic chips.

Furthermore, regarding fabrication processes, the techniques currently widely used in microfluidic chip manufacturing include photolithography, etching, molding, hot embossing, LIGA technology, laser ablation, and soft lithography; detailed operational procedures will not be elaborated herein.

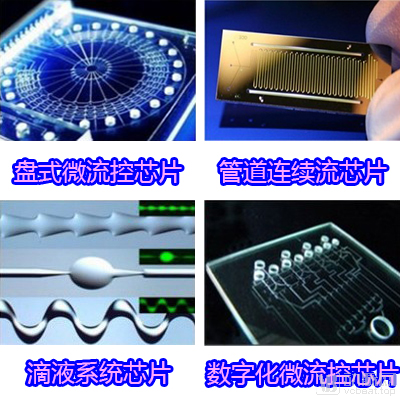

Microfluidic manipulation technology represents the final step in fabrication; the selection of different forces for fluid control results in significant variations in the final design of microfluidic chips. Currently, the most prevalent type is the disc-based microfluidic chip, which was proposed by Professor L. James Lee in 1998 (centrifugal microfluidic CD-ELISA technology).

Four Types of Microfluidic Chips (Illustrated by VCBeat)

In addition to disc-based microfluidic chips, other mainstream microfluidic platforms include digital microfluidic chips, continuous-flow channel chips, and droplet-based system chips. Differences in application scenarios entail distinct forces for fluid control, ultimately leading to variations in their physical configurations.

Digital microfluidic chips are thin and lightweight, resembling paper, and often utilize external forces such as electromagnetic fields to drive fluid flow. Continuous-flow microchannel chips are widely used in the field of circulating tumor cells (CTCs), enabling selective identification, capture, and high-throughput screening of specific cells in blood; these chips are typically driven by capillary forces. Droplet-based microfluidic chips manipulate discrete microdroplets and are suitable for single-cell analyses such as digital PCR and next-generation sequencing. Additionally, there are paper-based microfluidic chips that use paper as a substrate instead of silicon, glass, or polymers, with fluid propulsion primarily relying on the capillary action of the internal fibers of the paper.

Focus on the In Vitro Diagnostics Field

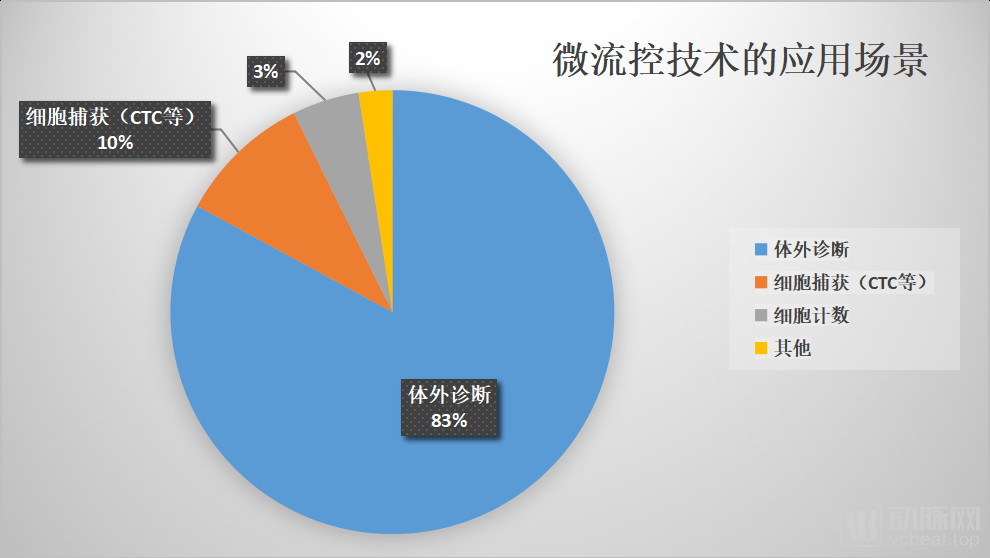

After more than a decade of development, microfluidic technology has evolved beyond its initial applications in capillary electrophoresis to explore a broader range of uses. Owing to their high degree of integration, ability to process large numbers of samples in parallel, rapid analysis, low energy consumption, and minimal contamination, microfluidic chips are now employed in diverse scenarios, including biomedical research, drug synthesis and screening, environmental monitoring and protection, health quarantine, forensic identification, and detection of biological reagents.

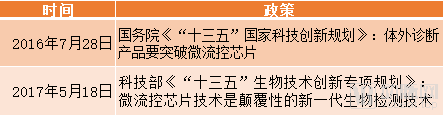

Among these numerous application scenarios, microfluidics shares a particularly strong connection with in vitro diagnostics (IVD). As early as 2002, coinciding with the first academic conference on microfluidics, China began providing annual financial support of tens of millions of RMB to companies engaged in microfluidics research, thereby promoting the development of domestic microfluidics technology. On July 28, 2016, the State Council issued the “13th Five-Year Plan” for National Scientific and Technological Innovation, which explicitly stated that “IVD products must achieve breakthroughs in key technologies such as microfluidic chips and single-molecule detection, develop major products including fully automated nucleic acid testing systems, and create reagents for early diagnosis and precision treatment diagnosis of major diseases, as well as high-precision diagnostic products suitable for primary healthcare institutions.”

Subsequently, the Ministry of Science and Technology issued the "Special Plan for Biotechnology Innovation during the 13th Five-Year Plan Period," which explicitly included microfluidic chips in next-generation biodetection technologies and described them as disruptive technologies.

The integration of microfluidics with in vitro diagnostics has been officially recognized at the policy level, with nearly 90% of domestic companies developing microfluidic chips applying them to the field of in vitro diagnostics.

In addition to policy drivers, the in vitro diagnostics (IVD) sector has become the largest segment of the microfluidics market, a development inseparable from the rapid growth of the IVD field in recent years. China’s IVD industry achieved a compound annual growth rate (CAGR) of 18.7% from 2017 to 2019. The IVD market size reached RMB 60.4 billion in 2018 and is projected to exceed RMB 70 billion in 2019. The IVD sector has spurred innovation in foundational technologies, making it the first industry where microfluidics technology has been commercially implemented.

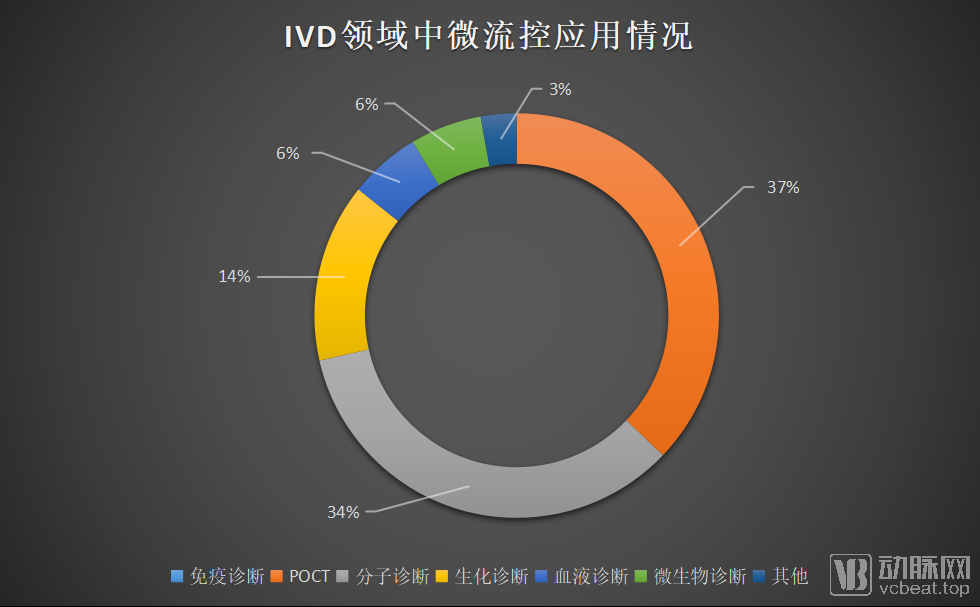

Currently, the in vitro diagnostics (IVD) sector can be segmented, in descending order of market share, into immunoassay diagnostics, clinical chemistry diagnostics, molecular diagnostics, point-of-care testing (POCT), hematology diagnostics, microbiology diagnostics, and others. Given the characteristics of microfluidic chips—miniaturization, high efficiency, and low cost—they have the most significant enabling impact on the POCT segment within the IVD industry. The demand for microfluidic chips in POCT diagnostic devices is continuously increasing, making POCT the primary driver for the development of the microfluidics industry.

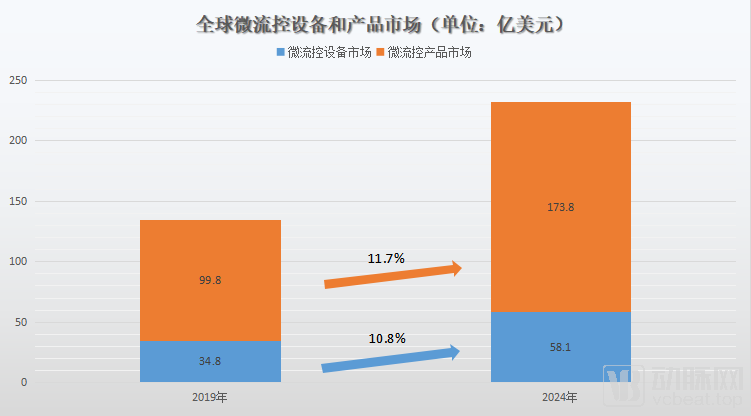

According to the latest statistical data from Yole analysts, the global market size for microfluidics products reached $9.98 billion in 2019, while the microfluidics devices market reached $3.48 billion. From 2019 to 2024, the compound annual growth rate (CAGR) for the microfluidics products market was as high as 11.7%, and the CAGR for the microfluidics devices market was 10.8%. It is projected that by 2024, the microfluidics products market will reach $17.38 billion, and the microfluidics devices market will reach $5.81 billion.

(Data source: Yole report)

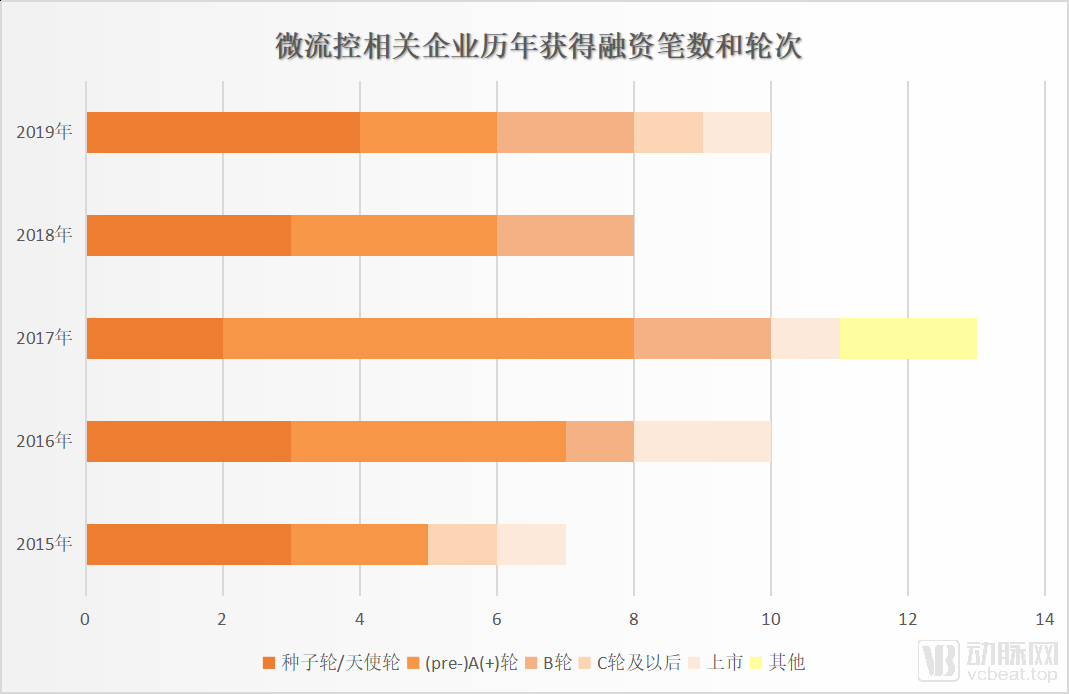

Given such a vast market, capital will certainly not miss the opportunity. VCBeat has surveyed nearly 50 companies in China currently involved in the research and development of microfluidics technology, compiling statistics on the number and rounds of financing they have secured since 2015.(Note: Undisclosed financing information is excluded from the statistics, which are based on valid data from 26 companies. As most companies did not disclose their financing amounts, changes in financing amounts in recent years were not statistically analyzed.)

Since 2016, an average of more than 10 financing deals per year have been invested in companies involved in microfluidics technology, with the majority occurring at or around the Series A stage (including Pre-A and A+ rounds). 2019 marked a harvest year for microfluidics technology, as four in vitro diagnostic (IVD) companies specializing in this field—Rongzhi Biology, Jingzhun Medical, Singleron Biotechnologies, and Lanyu Biology—each secured financing amounts in the range of hundreds of millions of RMB.

Among them,Rongzhi BioThe “QuanPLEX Microfluidic Nucleic Acid Quantification Platform” is a microfluidic genetic testing platform based on quantitative fluorescent PCR technology. It has developed three diagnostic applications: the QuanPLEX Rapid Identification System for Foodborne Pathogens, the QuanPLEX Avian Influenza Virus Detection System, and the QuanPLEX Respiratory Pathogen Detection System.

Jingzhun MedicalThe company focuses primarily on molecular diagnostics within the in vitro diagnostics (IVD) sector, having established six major molecular diagnostic technology platforms: real-time quantitative PCR (qPCR), first-generation Sanger sequencing, second-generation next-generation sequencing (NGS), capillary electrophoresis fragment analysis, fluorescence in situ hybridization (FISH), and microfluidic chips. It has also entered into a cooperation agreement with the Shanghai Institute of Microsystem and Information Technology of the Chinese Academy of Sciences regarding microfluidic chip technology.

Singleron BiotechnologiesFocused on developing next-generation molecular diagnostic tools—massively parallel single-cell sequencing, the company launched its first product in this field, the “Singleron GEXSCOPE™ Massively Parallel Single-Cell RNA Sequencing Product,” early this year. The product offers a comprehensive solution that includes proprietary microfluidic chips, all necessary reagents, and bioinformatics analysis software.

Lanyu BiotechIts highlight lies in the pioneering active microfluidics technology platform, which can deliver precise test results from clinical whole blood samples within 5 minutes. To date, it has established several R&D platforms, including a rapid immunoassay diagnostic platform, a handheld electrochemical coagulation platform, and a fully automated rapid nucleic acid diagnostic platform.

Not only that, but 2019 also saw a major milestone in the field of microfluidics—MicroPoint BioDelisted from the NEEQ. Weidian Bio is a company specializing in the research, development, manufacturing, and sales of point-of-care testing (POCT) devices and accompanying bio-diagnostic test cartridges for the medical field. The company holds 13 invention patents across multiple technological domains related to microfluidic bio-diagnostic test cartridges. Its primary offerings include two major technology platforms: mLabs and qLabs. The mLabs platform is used for detecting cardiac markers and infection markers, while the qLabs platform is designed for four categories of tests—PT/INR, APTT, PT/APTT, and PT/APTT/FIB/TT—to enable real-time monitoring of coagulation status in patients on medication.

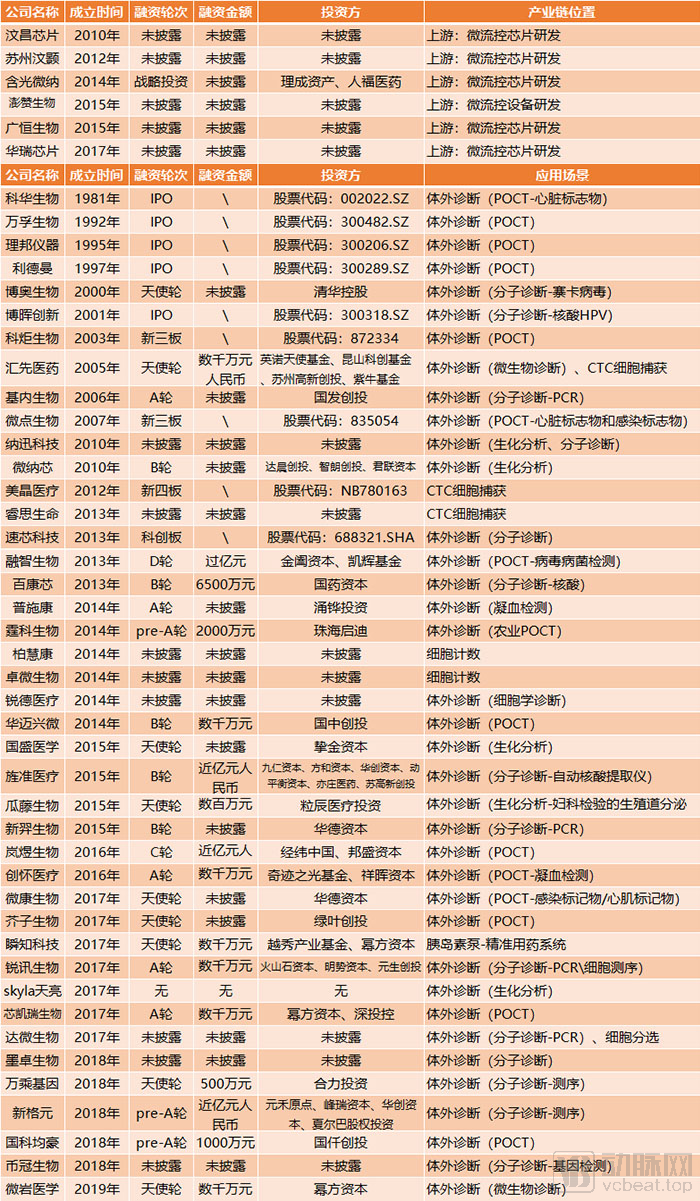

Overview of Domestic Microfluidics Companies

VCBeat has compiled a list of domestic companies currently involved in microfluidics technology, organizing them in ascending order by founding date and providing a brief classification.(Note: Data compiled from public sources. Companies with inaccurate or unlisted data are welcome to contact VCBeat for further discussion.)

Statistical data reveal that there are currently relatively few companies in China operating in the upstream segment of the microfluidic chip industry. Most enterprises are situated in the mid-to-downstream stages, adopting a “self-developed and self-marketed” model—designing microfluidic chips based on their own business needs and then implementing them in practical applications. Li Chen, Director of Partnership Expansion at Rongzhi Biology, also noted that only a handful of companies truly master the core upstream technologies of microfluidics, with the supply of upstream microfluidic chips essentially limited to just one or two providers.

Upstream enterprises in the microfluidics industry primarily process and manufacture chips based on the application development needs of midstream companies. The market potential of these upstream players is contingent upon the market size of the midstream sector. Furthermore, since most domestic companies independently develop their core microfluidics technologies rather than outsourcing production to upstream manufacturers, the upstream market has been somewhat constrained. However, with the continued advancement of biotechnology in China, application scenarios for microfluidics will continue to expand. As demand for mass production of microfluidic chips rises in the future, upstream R&D enterprises that establish an early presence will gain a first-mover advantage.

In addition to the focused field of in vitro diagnostics, several companies are applying microfluidic technology for single-cell-level operations. For instance, Huixian Medicine, Meijing Medical, and Ruisi Life Sciences all utilize microfluidic technology to manipulate (capture) circulating tumor cells (CTCs).

HuiXian MedicineA microfluidic chip with a series-parallel, multi-layer architecture comprising tens of thousands of channels has been designed. This single-chip platform incorporates over ten thousand microchannels, enabling the simultaneous capture of multiple target cells or pathogens. Furthermore, the multi-channel design ensures physical isolation between molecular detection units, preventing cross-interference among reactions. This allows for parallel multiplexed testing of a single sample as needed, featuring high-throughput and rapid detection capabilities. The system facilitates the rapid enrichment of rare cells and the swift detection of pathogens such as bacteria, fungi, viruses, and parasites.

Meijing MedicalThe independently developed next-generation CellRichTM automated circulating tumor cell capture device received approval from the China Food and Drug Administration (CFDA) in February 2018, becoming the only nationally certified automated dual-mode circulating tumor cell screening device in China based on patented microfluidic chip technology for immunomagnetic separation, enabling precise capture of circulating tumor cells (CTCs) from human peripheral blood.

Ruisi LifeLeveraging core microfluidic biochip technology, we have developed the Cellab Thomas I Circulating Tumor Cell (CTC) Pre-processing Workstation and the Celligo ST10 CTC Isolation and Enrichment Kit. This highly integrated system enables efficient, non-destructive one-step isolation and enrichment of CTCs without requiring pre-treatment steps such as red blood cell lysis. The enrichment efficiency exceeds 95%, with a white blood cell depletion rate of up to 99.9% and a red blood cell removal rate approaching 100%.

Circulating Tumor Cells (CTCs) are a class of cells that detach from the tumor's basement membrane during tumor progression and enter the bloodstream through the tissue stroma. By detecting cell-free DNA (ctDNA) derived from the lysis of CTCs in the blood, it is possible to diagnose and monitor tumors in patients via liquid biopsy.

The number of circulating tumor cells (CTCs) present in peripheral blood is extremely low, typically ranging from only 1 to 10 per milliliter of blood. Sequencing can be performed only after successful CTC capture. The integration of microfluidic technology has opened new possibilities for CTC isolation. CTCs and white blood cells exhibit significant differences in their deformability characteristics. Microfluidic chips allow white blood cells, which are larger than the chip’s microporous channels, to pass through due to their high deformability, whereas CTCs are retained because of their limited deformability.

In addition to companies that capture CTCs, there are also companies that enumerate CTCs.Baihuikang Biotech, the company has developed a microfluidic multicolor fluorescence cell counter that integrates magnetic cell sorting technology with immunocytochemical staining for the detection of circulating tumor cells (CTCs) in peripheral blood of patients with colorectal cancer. By leveraging a microfluidic analysis and counting system, it enables both quantitative enumeration and morphological analysis of tumor cells.

There is also a company that specializes in cell counting using microfluidic counting technology.Zhuowei MicrobiologyBy leveraging microfluidic technology, Zhuowei Microbiology controls the cell focusing layer to an extremely thin thickness of just a few to ten micrometers. Combined with Coulter impedance detection, this approach enables absolute counting of all particles in the sample. Currently, Zhuowei Microbiology has launched several products, including the FIL PLUS High-Precision Flow Imaging Cytometer, the CL Flow Cytometry Coulter Counter, the FIL Flow Imaging Cytometer, and the CC PLUS Handheld Coulter Counter.

Lastly, it is worth mentioning thatInstant Knowledge Technology, theyLeveraging its microfluidic chip pump technology platform, the company is an innovative developer of high-end medical devices and one of the few globally capable of providing precision micro-dosing solutions that ensure continuous, accurate injection while revolutionarily reducing mass production costs. These systems target therapeutic areas such as diabetes, chronic pain, postoperative analgesia, and growth hormone deficiency.

Directions and Challenges in Microfluidics

In 2003, microfluidics was named by Forbes magazine as one of the 15 most important inventions shaping the future of humanity; in 2004, it was listed by the U.S. publication Business 2.0 as one of the seven technologies that will change the future. Honored with such acclaim, microfluidics has lived up to expectations, successfully transitioning from the laboratory to commercialization and emerging as the most cutting-edge detection technology in in vitro diagnostics (IVD) today. Aligned with the research trends toward miniaturization, integration, and intelligence, the application of microfluidic technology in IVD is an inevitable trend. The advent of microfluidic chips is poised to bring about a fundamental technological revolution in the field of life sciences.

Shi Weiyang, founder of Wancheng Genomics, recalled the decision to adopt microfluidics technology: “Wancheng Genomics aimed to achieve high-throughput single-cell analysis, so we surveyed the mainstream technical approaches internationally, which predominantly rely on microfluidics technology.”

The primary bottleneck of current high-throughput single-cell sequencing technologies is their reliance on a single modality, limiting their application primarily to transcriptomics. In contrast, droplet microfluidics-based multi-omics single-cell sequencing technologies ultimately enable the simultaneous measurement of multiple types of omics information from individual cells in a single assay. Notably, droplet-based microfluidic chips are most commonly employed in single-cell analysis.

Meanwhile, microfluidic technology enables diagnostic assays that were previously confined to laboratory settings to be performed on a single chip. This not only reduces consumable and time costs but, more importantly, integrates multiple detection techniques into one platform, thereby enhancing detection efficiency. As microfluidic chip fabrication technologies continue to mature and various novel materials are developed, microfluidic chips will become more functionally comprehensive and achieve higher levels of integration.

However, Zhang Yan, founder of MicroRock Biotech, bluntly stated, “There is no such thing as a free lunch; there are no ‘handouts.’” He noted that while microfluidic technology offers convenience, it comes with corresponding “costs,” referring to the pain points associated with this technology.

I. Complex manufacturing processes and low yield rates

The “micro” in microfluidics necessitates “precision manufacturing,” involving multidisciplinary knowledge and skills across medicine, biology, chemistry, and engineering. As an integrated product, microfluidic chips consolidate functions such as micro-volume sample handling, sequential mixing and reaction, separation, analysis, and detection, all of which require rational design of components like valves, fluidic channels, and reaction chambers. The complex manufacturing process imposes high technical demands; without robust interdisciplinary expertise and specialized microfluidic technology, the high barrier to R&D inevitably leads to reduced product yield rates.

II. Challenges in Cost Control and Mass Production

“If production costs are disregarded, microfluidic chips can accomplish nearly all the processes required for sample pretreatment,” said Li Chen. However, for a technology to be successfully implemented, it must undergo industrialization. Behind mass production lies a practical challenge: how to reduce manufacturing costs? “Whoever can achieve low-cost, large-scale production of microfluidic chips will be better positioned to gain market access.”

Due to the high technical barriers and complex manufacturing processes associated with microfluidics, coupled with the recent downturn in the real economy—which hinders the research and development of high-tech products—reducing the production cost of microfluidic chips has become an urgent priority for companies. “From a macro perspective, we can lower production costs by selecting inexpensive ‘forces’ and materials, and the chip design should not be overly complex,” said Zhang Yan. “Centrifugal force” is one such low-cost force, requiring neither complex equipment nor intricate chip structures. A typical example of centrifugal microfluidic chips is the disc-based microfluidic chip.

In addition to selecting appropriate forces and materials, manufacturing processes must also be considered for the mass production of microfluidic devices. “It is only when you proceed to large-scale production of microfluidic chips that you realize conventional photolithography techniques cannot meet the demands of high-volume manufacturing,” explained Yan Jing, founder of Huixian Medicine. “Currently, the industry has begun adopting micro-injection molding for the mass production of microfluidic chips, thereby reducing production costs.”

In vitro diagnostics (IVD) served as the initial platform for microfluidics technology, but it is by no means the last. Beyond the medical sector, microfluidics is currently seeing extensive application in point-of-care testing (POCT) within agriculture. For instance, Thunder Technology has leveraged microfluidic chips to develop rapid detection instruments for pesticide residues. The fact that microfluidics first found commercial footing in the IVD industry is attributable not only to the strong alignment between the technology and IVD requirements but also to the inherent development of the IVD field itself. Yan Jing corroborates this view, stating, “Microfluidics technology can be applied across many fields; from a research perspective, its applications are extremely broad. However, it has achieved industrialization first in the IVD sector, partly due to the maturity of the IVD industry.”

In the future, as industries involving fluid dynamics—such as 3D printing, organ-on-a-chip and biomimetic organs, and drug efficacy/toxicity studies—continue to develop, the application landscape for microfluidic chips is expected to expand significantly, making it a field well worth watching.