Annual Review of Smart Rehabilitation Devices: From Chasing Tech Hype to Solving Real Clinical Problems

Changzhou is one of the leading hubs for the development of rehabilitation equipment in China. Changzhou’s rehabilitation assistive devices account for one-fifth of the global product categories, with annual sales exceeding RMB 10 billion. The city alone is home to more than 400 manufacturers of medical devices and rehabilitation assistive products.

However, in Changzhou, there is not a single publicly listed rehabilitation equipment company. In contrast, the international rehabilitation device sector is home not only to multinational corporations such as Invacare Corporation, Medline Industries, and Dynatronics, but also to a cohort of promising emerging technology companies, including Ekso Bionics and ReWalk.

Overall, China’s rehabilitation equipment industry is characterized by small-scale, fragmented, and disordered operations. In the face of a substantial market gap, a number of domestic enterprises focused on the research, development, and manufacturing of intelligent rehabilitation devices have emerged, with product portfolios encompassing cutting-edge exoskeleton robots and innovative smart rehabilitation equipment.

From scratch, the intelligent rehabilitation equipment industry has not been around for long, but its development path has not been smooth sailing. Through practical trial and error, engineers have discovered that the products most needed in clinical settings may not necessarily be those assembled with the strongest algorithms, chips, sensors, and motors. After re-examining the reality of the development of domestic rehabilitation departments, people have begun to recognize that addressing clinical needs and problems is the real necessity.

VCBeat (WeChat ID: vcbeat) interviewed seasoned investors and practitioners in the intelligent rehabilitation industry. Based on our analysis, we have drawn the following conclusions:

1. The implementation of DRG policies and medical insurance cost containment will drive rapid expansion of the rehabilitation market.

2. Hospital needs define the R&D direction, with hospitals requiring comprehensive solutions; these comprehensive solutions must demonstrate replicability at the primary care level.

3. R&D Misconceptions: Foreign experience cannot be blindly replicated; it is essential to adopt a medical-engineering collaborative approach to address clinical pain points and focus on patients’ daily living needs.

In 2019, financing in the smart rehabilitation equipment sector declined compared to 2018, with both the number of funding rounds and the total amount raised decreasing. In contrast to previous years, which saw industry mergers and acquisitions and multiple financing deals, the capital market adopted a more sober and cautious stance toward smart rehabilitation equipment in 2019.

2019 Financing Review of Intelligent Rehabilitation Devices: Data from the VCBeat Database

This shift is not limited to the capital sector; significant changes are also evident in the rehabilitation field, as seen from the product launches since 2019.

From the perspective of leading industry players, multiple companies began to refine their upper-limb rehabilitation robot products in 2019. Meanwhile, exoskeleton robots, which had previously garnered significant attention, entered a post-approval market introduction phase, with no substantial changes observed in 2019.

From a clinical perspective, there are currently few rehabilitation devices that truly meet the needs of clinical treatment. The intelligent rehabilitation equipment introduced in the industry in 2019 mainly featured several key characteristics, including integration with specific scenarios, data-driven capabilities, and greater reduction in the workload of clinical therapists. Compared to the surge of new products in the previous two years, rehabilitation equipment products in 2019 focused more on continuously aligning existing product concepts with clinical demands.

The barrier to entry for rehabilitation robots is relatively low, and the market demand in rehabilitation is well-defined, offering potential for rapid short-term growth. The key challenge lies in the high requirements for product portfolios and distribution channels. The fragmented nature of the industry makes it difficult to meet supply chain demands, necessitating policy-driven development.

Furthermore, the market potential for individual rehabilitation robotics products is limited, necessitating a diverse product portfolio; moreover, as rehabilitation robots typically do not involve consumables, a sustainable profitability model is currently lacking.

Meanwhile, in 2019, we observed that the low entry barriers for rehabilitation robots and the clearly defined market demand for rehabilitation services led to the emergence of more products with low technological thresholds in the intelligent rehabilitation equipment market. For instance, compared to traditional mobility wheelchairs, intelligent standing-assist walking robots enable patients to move independently through mechanical design, thereby helping them regain confidence in their daily lives.

In terms of market channels, such products are primarily sold through the China Disabled Persons’ Federation (CDPF). For enterprises, securing CDPF approval for compliant products is sufficient to establish a foothold in the market. Furthermore, in 2019, many intelligent rehabilitation products were promoted via short-video social media platforms with extensive reach, such as Douyin and Kuaishou, achieving favorable results.

Reviewing the development of intelligent rehabilitation equipment, we must broaden our perspective to encompass the entire rehabilitation sector and even the broader healthcare environment. Currently, the hospital market remains the primary market for intelligent rehabilitation devices, as the consumer (B2C) market is still highly immature. In the B2C segment, the user base and the paying customers do not overlap; the purchasers are typically healthy individuals, while the users include caregivers, therapists, and patients. The domestic development of intelligent rehabilitation equipment in China is still in its early stages, with a relatively fragmented and disordered market. Since purchasers seeking professional rehabilitation equipment still require medical consultation, market education in the B2C sector continues to rely heavily on physician channels.

However, we can also observe that certain products are penetrating the consumer market through entirely new marketing approaches. For instance, many walking-assist robots are being promoted via Douyin (TikTok).

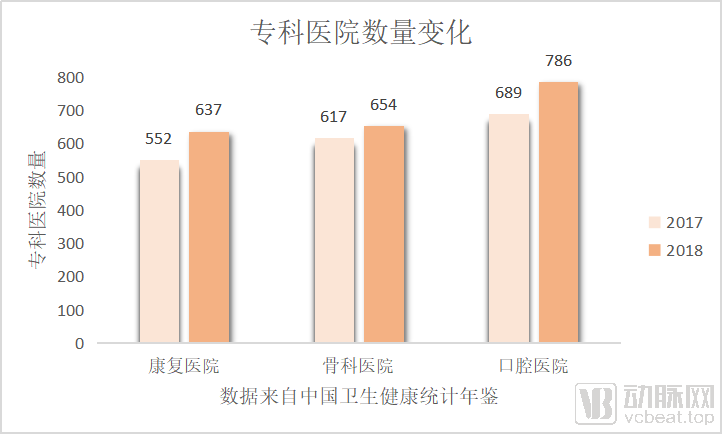

For the development of rehabilitation hospitals, we are now in an era of unprecedented leapfrog growth. Data show that the number of rehabilitation hospitals in China was 552 in 2017 and rose to 637 in 2018, including 434 in urban areas and 203 in rural areas, representing a growth rate of 15.3%.

By comparison, the number of orthopedic hospitals increased from 617 in 2017 to 654 in 2018, representing a growth rate of 5%. The growth rate of rehabilitation hospitals even exceeded that of dental hospitals, which stood at 14% from 2017 to 2018. This clearly demonstrates the strong growth momentum of rehabilitation hospitals.

If aging and heightened rehabilitation awareness are the fuel for the development of China’s rehabilitation industry, then policy is the spark that ignites it.

Policies encouraging the development of the rehabilitation industry have been continuously advanced. As early as 2011, the General Office of the Ministry of Health issued the “Work Plan for Pilot Programs on Establishing and Improving the Rehabilitation Medical Service System.” In 2015, the State Council issued a document encouraging social forces to establish institutions integrating medical care with elderly care. In 2016, 20 medical rehabilitation items, including comprehensive rehabilitation assessment, were included in the coverage of basic medical insurance. In 2018, the National Health Commission clarified that a large number of secondary hospitals would undergo transformation, transitioning into rehabilitation hospitals or geriatric nursing hospitals.

VCBeat has compiled the relevant policies in the rehabilitation field for 2019. As shown in the table, more detailed and regulatory policies were introduced in 2019. These policies are guiding the rehabilitation industry toward establishing implementable standardized operations, integrating with various practical settings such as communities, elderly care institutions, and hospitals, formulating rehabilitation work systems, and accelerating the standardization of diagnosis and treatment processes for various diseases.

In addition, local governments in Sichuan, Shandong, Jiangsu, Hunan, Hainan, Jiangxi, and Inner Mongolia have all issued implementation plans for the rehabilitation assistive devices industry to accelerate its development.

In addition to directly guiding the development of rehabilitation medicine, health insurance cost-containment policies are also indirectly promoting the growth of rehabilitation hospitals.

In 2019, the key terms in the healthcare industry were inseparable from medical insurance cost containment and Diagnosis-Related Groups (DRGs). As the largest payer in the healthcare sector, changes in payment mechanisms will drive transformation across the entire industry.

Su Zhonghe, Managing Director of the Pharmaceutical and Healthcare Fund at Mifang Capital, told VCBeat: “This period coincides with a transformation in China’s healthcare payment system. Due to significant pressure on the national medical insurance fund, cost containment measures are being implemented for patients during the treatment phase. Regardless of the specific regulatory approaches adopted, these measures will ultimately lead to a stratification of patients in acute and critical stages, thereby reducing the average length of hospital stay. Previously, hospitals might have allowed patients to remain hospitalized indefinitely. However, reforms in payment methods will objectively delineate between the acute care phase and the rehabilitation phase for patients.”

In fact, a similar shift of patients to rehabilitation hospitals driven by payment methods occurred in the United States 30 years ago. Data show that the number of rehabilitation beds in the U.S. doubled between 1985 and 1995, with the compound annual growth rate of rehabilitation expenditures reaching 20%. The primary driver of this growth was the prospective payment system based on Diagnosis-Related Groups (DRGs), established in 1982, which capped total treatment costs for acute-phase rehabilitation and shortened treatment durations. This measure spurred a surge in demand for post-acute rehabilitation services, leading to rapid development of specialized rehabilitation hospitals.

In addition to rapid growth, another keyword for the rehabilitation industry over the past year has been “market penetration into lower-tier regions.”

Gu Jie, CEO of Fourier Intelligence, stated, “We are clearly observing a trend on the front lines: rehabilitation services are gradually decentralizing to lower-tier institutions. Within a comprehensive three-tier rehabilitation network, rehabilitation should not be an exclusive specialty of top-tier hospitals. The secondary tier should include maternal and child health hospitals, or appropriately equipped general people’s hospitals and traditional Chinese medicine hospitals. Finally, services should extend to the grassroots level, encompassing community health service stations, community hospitals, nursing homes, and similar institutions.”

Gu Jie also pointed out that the biggest pain point in primary rehabilitation medical care lies in the complex variety of patients faced by rehabilitation departments, which span multiple specialties. It is necessary to build rehabilitation service capabilities at the primary level and provide high-quality rehabilitation technologies.

VCBeat has learned that in the United States, health insurance covers more than 90% of medical, rehabilitation, and elderly care expenses. Of the remaining 10%, a significant portion is paid by commercial insurance, leaving patients with an out-of-pocket expense of only 5% for treatment at rehabilitation facilities. In 1982, U.S. health insurance adopted a prospective payment system based on Diagnosis-Related Groups (DRGs) for acute-phase rehabilitation. For patients with clear diagnoses, standardized treatment protocols, and shorter hospital stays, hospitals actually have considerable profit margins, which incentivizes them to expand departmental infrastructure.

Although rehabilitation hospitals are experiencing rapid growth, the essential elements supporting their operations—such as talent, equipment, and payment systems—have yet to fully mature. The development of rehabilitation medicine in China must not only confront a complex historical context but also adapt to new technology-driven factors. Consequently, the evolution of rehabilitation medicine in China will exhibit distinct local characteristics.

In contrast to the talent development and payment systems, which require long-term cultivation and exploration, intelligent rehabilitation equipment, as a new technological variable, not only serves as an important supply-side resource but also reduces labor input in the rehabilitation process, thereby transforming the business model and operational framework of rehabilitation medicine.

For the current stage, the intelligent rehabilitation equipment required by rehabilitation hospitals and departments is no longer just simple rehabilitation tools.

Su Zhonghe pointed out: “Many companies imitate foreign products in their R&D efforts, simply replicating whatever products are available abroad. In reality, these manufacturers fail to truly understand the industry’s transitional phase, as well as the pain points and needs of hospitals.”

For example, in the U.S. clinical rehabilitation landscape, hospitals require a substantial number of rehabilitation assessment devices because the insurance reimbursement system ties payments to patients’ assessment scores. If a patient scores 1 at admission and 5 at discharge, insurers will reimburse for the four levels of functional improvement achieved in between. In China, however, such rigid demand for rehabilitation services has not yet taken shape.

The simplistic approach of borrowing foreign models has proven incompatible with local conditions; merely importing technology without developing a suitable system makes it difficult for intelligent medical devices to gain hospital acceptance. Clearly, intelligent rehabilitation equipment in China follows its own developmental trajectory.

So, where lie the pain points in rehabilitation demand within China’s hospitals? Undoubtedly, the most significant bottleneck in China’s rehabilitation sector is a shortage of personnel. This refers not to patients, but to physicians—specifically, a lack of doctors with systematic, experience-based treatment expertise.

In China, there is only one rehabilitation therapist per 100,000 people, whereas most developed countries have 60 therapists per 100,000 people.

In addition to the quantitative shortfall, the existing structure of rehabilitation professionals is also highly imbalanced. The domestic training of rehabilitation professionals primarily focuses on sports rehabilitation. Most of the “rehabilitation physicians” currently working in the fields of neurological and cardiac rehabilitation are former clinical or traditional Chinese medicine (TCM) practitioners who transitioned to rehabilitation departments after obtaining their attending physician credentials.

A shortage of rehabilitation healthcare professionals has prevented many rehabilitation hospitals from operating normally. For individual rehabilitation devices, hospital requirements are clear: safety, efficacy, and affordability. However, products that merely meet these three criteria are not what is most needed for establishing rehabilitation departments or hospitals.

Currently, the equipment best suited to the needs of rehabilitation hospitals is that which enhances their capacity to deliver rehabilitation services.

In short, at this stage, hospitals require rehabilitation equipment that can meet a comprehensive set of rehabilitation needs and enable the rapid operation of the rehabilitation department. They prioritize equipment that can be practically utilized to generate tangible benefits, rather than standalone high-tech products. Furthermore, cost is the second key concern for hospitals; they need solutions that allow therapeutic services to operate in a cost-effective manner.

Wang Daoyu, founder of Shanghai Zhuodao Medical Technology Co., Ltd., stated, “From a clinical perspective, there are currently few rehabilitation devices that truly meet the needs of clinical treatment. The cost of rehabilitation robots must be well controlled. At present, reimbursement rates for services in this field under China’s medical insurance system remain relatively low, so it is essential to consider departmental financial accounting and return on investment. Most hospitals cannot afford high-end imported equipment, which often carries price tags of several million yuan. We have positioned our product prices in the range of tens of thousands to hundreds of thousands of yuan, ensuring high quality and safety while enabling rehabilitation institutions to recoup their procurement costs within approximately one year under normal patient volumes.”

In Wang Daoyu’s view, the shortage of therapists in Chinese hospitals is the most significant pain point. To address this, Zhuodao has embedded a vast array of prescriptions aligned with rehabilitation therapy logic into its product design. By digitizing and visualizing the treatment process and efficacy data, the system reduces the workload of clinical therapists by more than 80%, truly achieving intelligent rehabilitation and machine substitution for human labor.

Yan Han, General Manager of Limaidi, a developer and manufacturer of intelligent rehabilitation equipment, told VCBeat, “Safety and efficacy are undoubtedly fundamental requirements for hospitals. However, hospitals also expect rehabilitation devices to partially replace manual labor. Although we are a manufacturer of intelligent rehabilitation equipment, our service to hospitals goes beyond simply selling them a piece of equipment; we provide customized, comprehensive solutions. We place greater emphasis on enhancing the sustainable operational capabilities of rehabilitation hospitals. Our solutions even extend to detailed aspects such as the design of the hospital’s interior decoration style.”

The trend of providing holistic solutions to hospitals has been put into practice by multiple enterprises. Gu Jie also believes, “Hospitals today are more eager for rehabilitation companies to help them build their rehabilitation service capabilities, which encompass equipment, technology, operations, and other aspects. We are currently offering comprehensive solutions to rehabilitation hospitals through a multi-party collaboration model.”

VCBeat has learned that at Fengzhen Traditional Chinese and Mongolian Medicine Hospital, a Grade II Class A hospital in Ulanqab, Inner Mongolia Autonomous Region, Fourier Intelligence has partnered with Zhuhai Ruihekang, a professional rehabilitation operations enterprise, to establish a comprehensive rehabilitation service system for the hospital.

In the past, it was common for patients from Inner Mongolia to be diagnosed at major hospitals in Beijing but unable to receive comprehensive rehabilitation treatment. While most hospitals of the same level in Inner Mongolia had not yet established rehabilitation departments, the Rehabilitation Department of the Chinese-Mongolian Hospital was already providing one-on-one functional training with dedicated specialists.

The establishment of the Rehabilitation Department at Fengzhen City Hospital of Traditional Chinese and Mongolian Medicine has met the rehabilitation needs of a broad patient population. Since its opening one year ago, the department has provided rehabilitation treatment to 400 patients.

Underpinning this is a professional intelligent rehabilitation module. This module integrates therapists, physicians, and operational staff; its software components include operational software, training software, prescription systems, medical insurance connectivity, and billing systems; while its hardware primarily consists of rehabilitation equipment. It is an integrated rehabilitation module product.

The designers have high expectations for this module, aiming to promote the intelligent rehabilitation module across China and drive the standardization of rehabilitation diagnosis and treatment nationwide.

We envision a healthy industrial chain ecosystem: the base of the rehabilitation device market consists of numerous low-barrier rehabilitation aids, the mid-tier comprises intelligent rehabilitation equipment, and the top tier features cutting-edge, advanced designs. However, the current R&D landscape in China shows that most enterprises are either concentrated on developing simple rehabilitation aids or focused on frontier technologies that are not yet scalable for widespread application, thereby failing to meet the clinical demand for efficient, intelligent, and practical devices.

One major reason is that among domestic R&D enterprises for intelligent rehabilitation equipment, most founders come from science and engineering backgrounds, resulting in limited involvement of professional rehabilitation physicians in product design.

Wang Daoyu stated, “The rehabilitation therapy process involves complex scenarios, and a single product cannot meet all clinical needs. At this stage, the clinical sector requires rehabilitation robot products tailored to specific application scenarios, while ensuring no safety risks to patients. This necessitates that robotics R&D teams collaborate closely with rehabilitation therapists and physicians to develop an increasing number of robotic solutions addressing challenges in rehabilitation therapy.”

For rehabilitation and assistive device products, the purchasers are typically healthy individuals, while the users include caregivers, therapists, and patients. From a product design perspective, it is essential to address the pain points of multiple stakeholders and meet the needs of both the purchasers and the users.

Although companies focused on cutting-edge technologies can gain recognition from capital markets abroad, this model still lacks the support of a mature financial environment in China.

Su Zhonghe stated, “In the United States, high-end, cutting-edge products appear to have a well-defined development pathway; for instance, high-tech companies like Ekso Bionics can go public. This is because the U.S. capital markets are more receptive to high-tech products, allowing companies to list even if they only have a product prototype. However, this approach is certainly not viable in China. In my view, the most formidable barrier for a product is its alignment with clinical logic. If it does not conform to clinical logic, then regardless of how high your technological barriers are—no matter how many sensors, motors, or complex algorithms are involved—they cannot be considered the core competitive advantage.”

Whether developing products for hospitals or for the daily lives of people with disabilities, a shift in R&D mindset is essential. A good product is not meant to showcase the developer’s technical barriers, but rather to address patients’ problems and pain points.

In the United States, rehabilitation medicine gradually developed after the Vietnam War, taking over 20 years to establish a comprehensive rehabilitation system. In China, the sector began to gain momentum following the 2008 Wenchuan earthquake. In 2016, 20 medical rehabilitation services, including comprehensive rehabilitation assessments, were included in the basic medical insurance coverage. In recent years, rehabilitation hospitals have started to emerge. Given the relatively short history of the industry in China, it is challenging for rehabilitation companies to establish a complete product portfolio in the early stages.

Building a model suited to the development of China’s rehabilitation industry requires not only raising public awareness but also establishing and improving rehabilitation centers and departments within hospitals. It is essential to explore unified diagnostic and treatment standards for rehabilitation institutions at different levels and to refine the payment system. While intelligent rehabilitation equipment plays a limited role, it remains an indispensable link in closing the loop of the rehabilitation industry. In the future, developers of intelligent rehabilitation equipment must aim high while staying grounded; they should benchmark against top-tier frontier standards while tailoring solutions to the actual needs of hospitals, thereby jointly creating a promising future for rehabilitation care in China.