How Insurers Are Leveraging Sickness-Inclusive Policies to Break Through the Health Insurance Price War

With the maturation of public health insurance and commercial health insurance, more innovative trends have emerged in the insurance sector, making it possible to purchase insurance with pre-existing conditions.

On November 12, 2019, the China Banking and Insurance Regulatory Commission (CBIRC) published the newly revised “Administrative Measures for Health Insurance” on its official website. The new regulations, which include provisions such as “encouraging new products to adapt to emerging needs” and “supporting the integration of health management,” have paved the way for insurance coverage for individuals with pre-existing conditions.

In 2019, the market for insurance covering pre-existing conditions was highly active. On the same day, two insurers launched new products, while another company introduced six such insurance products within a single year. During the transition from spring to summer in 2019, a new niche market was being incubated.

For traditional insurance companies, insuring individuals with pre-existing conditions has long been a taboo practice, as healthy individuals constitute their target customer base. According to data from the World Health Organization, only 15% of China’s population is in a state of good health. Consequently, the focus of competition among insurance companies has converged on this 15% segment.

Among the remaining 85%, 15% comprises individuals with diagnosed diseases, while 70% are in a state of sub-health. This 85% market segment includes the population with the strongest demand for insurance coverage—a lucrative yet cautiously approached opportunity for insurers. Traditional health insurance faces a crisis of product homogenization, with price wars imminent. These prevailing conditions compel insurers to pursue innovation. Consequently, insurers are extending their focus to the uncharted territory of insuring individuals with pre-existing conditions.

On May 22, 2019, the official website of the National Health Commission released the Statistical Bulletin on the Development of China’s Health and Wellness Undertakings in 2018. The bulletin indicated that China’s total health expenditure in 2018 was estimated at RMB 5.79983 trillion, with individual out-of-pocket health spending amounting to approximately RMB 1.6 trillion. This creates a market worth trillions for commercial insurance to cover individual expenditures. In April 2018, China’s first Blue Book on Health Management: Report on the Development of China’s Health Management and Health Industry (2018) was published. The Blue Book pointed out that there were approximately 300 million people suffering from chronic diseases in China.

According to the “China Inclusive Finance Index Analysis Report (2018)” released by the Financial Consumer Rights Protection Bureau of the People’s Bank of China on October 21, 2019, China’s per capita insurance density in 2018 was RMB 2,724.49. A rough estimate suggests that the market size for insurance covering pre-existing conditions exceeds RMB 800 billion.

Challenges are opportunities. Providing practical and effective insurance products for patients may become a breakthrough strategy for insurers, serving as a key avenue to redefine the value of health insurance.

Which companies have taken the first step? What are the challenges in developing insurance for individuals with pre-existing conditions, and how can they be addressed? This article will outline the development of such insurance in China by examining innovative case studies.

Insurance for Individuals with Pre-existing Conditions is insurance designed for people with pre-existing medical conditions. This population is not limited to those with chronic diseases; it also includes patients with serious illnesses, such as cancer.

Common chronic diseases mainly include cardiovascular and cerebrovascular diseases, diabetes, cancer, and chronic respiratory diseases. Among these, cardiovascular and cerebrovascular diseases encompass hypertension, stroke, and coronary heart disease. Chronic diseases are characterized by their long duration and significant harm, severely impairing patients' labor capacity and quality of life, while also imposing a substantial economic burden on society and families.

According to statistics from the National Cancer Center, China sees approximately 3.8 million new cases of malignant tumors annually, with the cumulative number of diagnosed cancer patients and their families reaching tens of millions. Compared with the healthy population, individuals with pre-existing conditions represent a segment largely overlooked by commercial insurance providers, despite their stronger demand for insurance coverage.

Can individuals with pre-existing conditions reach a settlement with commercial insurance providers? The answer is yes.

Most insurance products deny coverage to individuals with pre-existing conditions that are moderately severe; for instance, hypertension classified as Grade III or higher is excluded from insurance coverage. In fact, individuals with pre-existing conditions are not ineligible for insurance; rather, insurance products designed for such populations impose higher requirements on insurers compared to those tailored for healthy individuals.

Tax-advantaged health insurance and elderly cancer medical insurance (for the "three highs" population) are currently the most common insurance products targeted at individuals with pre-existing conditions.

In 2015, pilot programs for individual tax-advantaged health insurance were launched, with the government encouraging commercial insurers to allow individuals with pre-existing conditions to enroll. Directly approved by the China Insurance Regulatory Commission (CIRC), this tax-advantaged health insurance, often referred to as “mini social security,” has faced the dilemma of being well-received in principle but poorly adopted in practice. This is because the so-called “encouragement” carries an element of compulsion.

As is well known, tax-advantaged health insurance covers both healthy individuals and those with pre-existing conditions. While insurers are prohibited from denying coverage based on an applicant’s medical history, they are also required to guarantee renewability and maintain a simple loss ratio of no less than 80%. Consequently, insurance companies have shown limited enthusiasm for offering tax-advantaged health insurance products.

Tax-advantaged health insurance offers broad coverage and service scopes, with no explicit restrictions on conditions outside the national medical insurance catalog, and includes comprehensive health management services. It is priced based on a base risk rate, which is adjusted according to underwriting assessments at the time of specific coverage issuance.

Due to multiple factors, the premium rates for tax-advantaged health insurance products are relatively high, and the underwriting process is complex, resulting in low enrollment enthusiasm among healthy individuals and young to middle-aged adults. Currently, the market size for tax-advantaged health insurance remains very limited. Major participants in this market include Ping An, China Life, Sunshine Insurance, New China Life, Taikang, and Minsheng Insurance.

Geriatric cancer medical insurance primarily targets individuals aged 70 to 80. Taking Ping An Health’s “i Kang Bao · Geriatric Medical Insurance (Three Highs Version)” as an example, a history of conditions such as hypertension, diabetes, gallstones, or lumbar disc herniation does not preclude enrollment; applicants can purchase the policy under standard terms. In 2016, Taikang Online launched its geriatric cancer medical insurance product, marketing it with the selling point that individuals with common chronic conditions such as the “three highs” and diabetes were eligible for coverage. The product rapidly gained widespread popularity in the market.

The “Analysis Report on Cancer Insurance Products for the Elderly under the Life Insurance Product Alliance,” released by the Insurance Association of China, shows that the cumulative gross written premiums for cancer insurance targeting the elderly increased from RMB 650 million in June 2015 to RMB 3.138 billion in June 2017. However, the eligibility criteria are narrow, resulting in a limited customer base. In the field of medical coverage for elderly cancer patients, insurers such as Taikang Online, Anxin Property & Casualty Insurance, PICC Property and Casualty Company, Ping An, and China Pacific Insurance have participated.

Insurers need to further refine their insurance product offerings and enhance their capabilities in risk forecasting and control. By establishing a comprehensive risk management system across pricing, operations, underwriting, and claims settlement, they can mitigate the risk of high loss ratios. Kong Qingkun, Senior Director of Product R&D at ZhongAn Insurance, stated, “Industry data shows that health insurance has a high loss ratio. As the dividends from the health insurance market gradually diminish, competition will center on who can develop more refined products, thereby managing claims payouts and costs more effectively.”

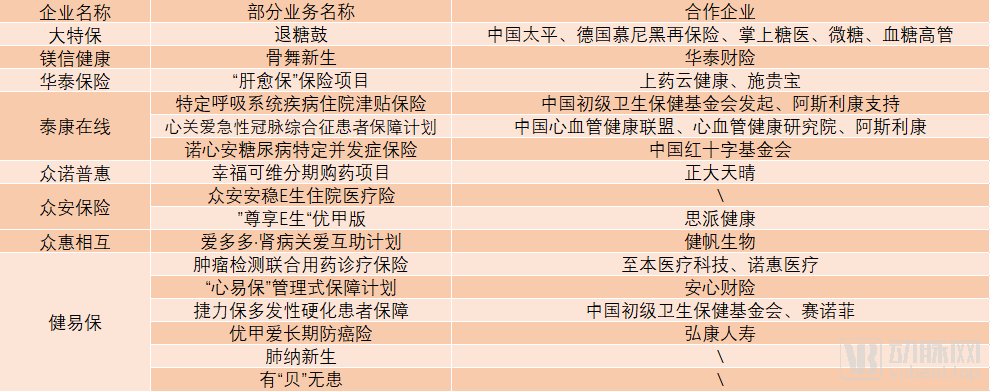

Numerous insurance companies have begun to explore underwriting for individuals with pre-existing conditions. VCBeat has compiled information on such offerings from several insurers:

Compiled from public sources; graphic by VCBeat

In 2015, after completing a RMB 180 million Series A financing round, Da Te Bao partnered with China Taiping and Munich Re to launch “Tui Tang Gu,” the first insurance product in China allowing for a fully online underwriting and enrollment process. This innovation broke the traditional insurance model that excludes individuals after they have developed an illness. The product specifically targets individuals already diagnosed with type 2 diabetes, providing coverage for four high-prevalence diabetic complications: post-stroke sequelae, end-stage renal disease, amputation, and blindness. In terms of pricing, premiums for this diabetic complication insurance are adjusted based on factors such as each patient’s duration of diabetes (i.e., “diabetes age”) and chronological age.

ZhongAn Insurance, established in 2013, is China’s first internet-based insurance company. When it began exploring insurance coverage for individuals with pre-existing conditions in 2018, ZhongAn Insurance chose to start with lower-risk medical conditions. Kong Qingkun stated, “Insurance for individuals with pre-existing conditions is an uncharted territory. On one hand, it requires time to accumulate data; on the other hand, we hope to ensure a more solid foundation in our exploratory efforts.”

ZhongAn Insurance’s Anwen E-Sheng Inpatient Medical Insurance covers medications not included in the social security formulary, features a RMB 10,000 deductible, and reimburses 90% of out-of-pocket expenses after social security or public medical reimbursement. Eligible applicants are those with either type 2 diabetes or primary hypertension; however, individuals diagnosed with both conditions are excluded from coverage.

The "Zunxiang E-Sheng Youjia Edition" relaxes underwriting conditions: patients with thyroid ultrasound results classified as TI-RADS 1–3 within the past five years are eligible for coverage, provided they meet the health declarations. Post-thyroidectomy patients may also apply for enrollment in the "Zunxiang E-Sheng" Youjia Edition once their condition has stabilized.

In 2019, Jianyibao made frequent innovative moves in the field of insurance coverage for individuals with pre-existing conditions. This young company, founded in 2017, has now become a leader in the market for insurance covering pre-existing conditions. On February 5, Jianyibao partnered with Zhiben Medical Technology and Shanghai Nuohui Medical to launch China’s first innovative payment insurance product targeting “integrated diagnosis and treatment” for cancer. Jianyibao customized an insurance plan titled “Cancer Testing and Combination Therapy Diagnosis and Treatment Insurance.” Under this plan, patients who undergo tumor genetic testing using Zhiben Medical Technology’s next-generation sequencing (NGS) platform and agree to enroll in the insurance can receive commercial diagnosis and treatment insurance free of charge.

By integrating pharmacies, commercial insurance companies, and pharmaceutical manufacturers, Jianyibao is a company dedicated to providing insurance innovations and services to the 450 million people in China living with pre-existing conditions. As of December 2019, Jianyibao had established data connectivity with over 100 national chain brands and more than 37,000 chain stores across over 300 cities in China, covering more than 450,000 policyholders.

It is an objective reality that purchasing insurance while already ill has become a major trend, yet numerous unresolved issues also objectively persist.

Patient compliance is a particularly prominent issue. In the management of chronic diseases, patients must contend with inertia. Taking thyroid conditions as an example, while the prevalence of thyroid nodules is high, most are benign; malignant cases account for less than 5%, and the majority of thyroid cancers progress slowly with high cure rates. Consequently, thyroid cancer is often referred to as an “indolent tumor” or “lazy cancer.” Precisely because of this perception, many patients with such “lazy cancers” indeed adopt a lax attitude toward their thyroid nodules, failing to undergo timely examinations or seek prompt medical attention. This delay causes them to miss the optimal window for treatment, ultimately allowing the disease to progress into a truly problematic condition.

Laziness is not only evident before the consultation; disease management during the clinical encounter must also be taken seriously. It is well known that poor glycemic control in patients with diabetes can lead to various complications, including retinopathy, renal failure, macrovascular disease, neuropathy, and amputation. Many patients, driven by a sense of complacency or wishful thinking, relax their self-discipline, thereby leading to disease progression.

The aforementioned circumstances compel insurance companies to shift their product models from passive reimbursement to active management, thereby enhancing patient adherence and ultimately reducing overall claims payouts for critical illness and complication coverage.

Taikang Online’s disease-specific insurance products place significant emphasis on cultivating patient adherence. For its Hospitalization Allowance Insurance for Specific Respiratory Diseases, Taikang Online incorporates medication and disease management adherence as a prerequisite for claims settlement. Furthermore, the Heart Care Protection Plan for Patients with Acute Coronary Syndrome explicitly states that only patients who “must continuously take guideline-recommended dual antiplatelet therapy for 12 months” are eligible to enroll in this plan. Additionally, Taikang Online provides refined whole-course patient management services, employing methods such as patient follow-up and education to enhance patient adherence.

Furthermore, Zhonghui Mutual’s kidney disease insurance and “Tui Tang Gu” are all products that integrate insurance coverage with disease management. While customers receive insurance protection, they also gain access to related medical services. On one hand, these health insurance products feature lower sum-assured amounts, which reduces the operational risk for insurers; on the other hand, their policy terms are typically one year, making risks controllable. If the loss ratio becomes excessively high, the products can be discontinued at any time.

Data Is the Key to Insurance for Individuals with Pre-existing Conditions

How to Determine the Controllable Scope of a Disease? How to Convince Insurers to Believe in or Be Willing to Offer Insurance for Pre-existing Conditions? Big Data Support Is Also Needed. Insurers’ data sources include, first, historical claims data and, second, partnerships with data companies. Data is the foundation of risk control, playing a crucial role in product development, claims processing, and underwriting.

When designing insurance coverage for individuals with pre-existing conditions, insurers must thoroughly understand key information such as the common demographic profiles of patients, disease onset cycles, and cure rates. On this basis, they should establish actuarial models and leverage up-to-date medical data to adjust their products. By integrating multiple components—including disease screening, diagnostic and treatment services, therapeutic regimens, medication discounts, and rehabilitation management—insurers can use insurance products as a vehicle to deliver standardized health management services.

This not only requires insurance companies to make significant efforts in specific disease areas but also to conduct long-term and effective data tracking and monitoring for these conditions, ultimately enabling the development of effective health insurance products. However, there are still many pain points in the healthcare industry’s data landscape, such as widespread data silos, low levels of standardization, and limited data usability.

With the advancement of big data and artificial intelligence, medical data is no longer as difficult to obtain as it once was. By leveraging new technologies such as big data, insurance companies can access relevant data and integrate health management data with clinical diagnosis and treatment data. This enables precise assessment of chronic disease risks and insurance factors at different stages, thereby making it possible to launch insurance products that allow individuals with pre-existing conditions to obtain coverage.

Take Jianyibao’s “Euthyrox Long-Term Cancer Insurance” as an example. Yang Chao, a product manager at Jianyibao and a participant in the development and design of the Euthyrox Long-Term Cancer Insurance, stated in an interview that the project’s R&D team included not only product actuaries but also experts with medical backgrounds. The team collected domestic and international journals, papers, reports, and other literature related to thyroid cancer, and conducted analysis and organization leveraging their professional expertise.

In collaboration with Hongkang Life Insurance, Jianyibao has sequentially acquired core findings and data on thyroid cancer subtyping, the quality and outcomes of surgical procedures both domestically and internationally, average postoperative patient survival, and the incidence rate of second primary cancers. For instance, through a review of relevant literature, the product R&D team found that, in the long term, thyroid cancer progresses slowly, is associated with prolonged survival and high cure rates, and allows for maintained quality of life.

In 2018, The Lancet published “Survival Rates of Cancer Patients in China, 2003–2015.” Among the findings, the five-year relative survival rate for thyroid cancer increased from 67.5% in 2003–2005 to 84.3% in 2012–2015. Such data serve as sample statistics for analysis by insurance companies and enhance the persuasiveness of insurance products entering the market.

Fang Zhiwu, Chairman of Wanhu Liangfang, stated that data serves as the cornerstone of both the insurance and health management industries. The company’s core competencies lie in its capabilities for data acquisition, analysis, and application. By leveraging its accumulated medication and health data from patients with chronic diseases, Wanhu Liangfang analyzes patterns in medication usage, the likelihood of complications, and the presence of adverse drug-seeking behaviors. “These data points can serve as the basis for pricing different risk factors in insurance underwriting, and they also form the core strategic foundation for mitigating pre-contractual adverse selection and enabling post-enrollment health management.”

Zhanlue Data, which completed a nearly RMB 100 million Series B financing round in July 2019, is a technology company specializing in risk control for health insurance. Leveraging two core technologies—evolutionary machine learning and knowledge graphs—Zhanlue Data conducts in-depth data mining and builds precise models around dimensions such as population incidence rates, disease progression cycles, and medical costs. This enables data-driven personalized pricing while supporting a digital claims process with intelligent risk control, accurately identifying and excluding unreasonable expenses, performing smart audits, and preventing fraud.

Technology-empowered insurance has become an industry consensus. The emergence of technologies such as artificial intelligence and blockchain has driven the intelligent transformation of risk control in the insurance sector, enhancing the precision of risk identification. Methods for risk early warning and risk management are gradually shifting from “manual” to “intelligent” approaches.

Channels and Payment Innovation Empower Insurance for the Chronically Ill

Online and offline sales promotions, along with referrals from acquaintances, are the primary ways traditional insurance reaches customers. However, the "non-essential" nature is a pain point for all insurance products. The core value of insurance lies in its "protection" function, which is inherently intangible. Healthy individuals cannot tangibly perceive the importance of insurance products, and thus lack the willingness to purchase them.

For patients with pre-existing conditions who cannot afford treatment costs, insurance for such conditions serves as a “lifeline in times of dire need.” The key question is: how can insurers identify and reach this population?

Compiled from public information; graphic by VCBeat

Compared with life insurance and property & casualty insurance, health insurance generally has lower premiums and often relies on the sales channels of life and P&C insurers. However, some innovative enterprises are unwilling to be confined to this model; they have developed innovative channels capable of reaching patient populations, such as partnerships with pharmacies, hospitals, patient management platforms, or service-oriented enterprises.

Zhangshang Tangyi, Weitang, and Xuetang Gaoguan are the first batch of partners for “Tuitangbao.” As apps specifically designed to serve diabetic patients, these three platforms have established a foundational user base of individuals with diabetes. This has enabled Datebao to precisely reach its target customers. Zhonghui Mutual has received multiple forms of support from Jafron Biomedical. In addition to financial backing, Jafron Biomedical has provided access to resources from more than 4,000 public hospitals at the secondary level or above with nephrology departments across China, offering a stronger foundation for serving a broad patient population.

JianYiBao has adopted a three-pronged strategy: first, partnering with pharmaceutical and medical device companies to provide coverage amounts when patients purchase specific prescription drugs for single-disease conditions; second, offering membership services to chronic disease patients enrolled in chain pharmacy programs; and third, collaborating on product promotion through medical channels. Among the five key healthcare channels—tertiary hospitals, county-level hospitals, township health centers, community hospitals, and retail pharmacies—JianYiBao is solidifying its presence in retail pharmacies while simultaneously expanding into community hospitals and county-level hospitals.

“Money means more chances of survival.” This statement captures the helplessness of families impoverished by illness. Compared with slowly progressing chronic diseases, cancer imposes stricter demands on treatment timelines. Yet, faced with high-priced “anti-cancer drugs,” patients still struggle with affordability and access. The concern that “taking the medication does not guarantee a cure and may further burden their families” remains a source of anxiety for patients.

Meanwhile, due to the limited capacity of public health insurance and insufficient involvement of commercial insurance, a group of patients in urgent need of anti-cancer assistance has received minimal support. To address this predicament, some innovative enterprises have started from the payment side to alleviate patients’ financial concerns.

On September 18, 2019, WeSure, in collaboration with Taikang Online and Medbanks Health, launched comprehensive patient solutions for individuals and families with confirmed cancer diagnoses, including “interest-free installment payments” for specialized anticancer drugs and “treatment efficacy risk protection.” In the event of the insured patient’s death due to accident or illness, WeSure will also waive the outstanding loan balance.

Wanhu Liangfang provides comprehensive solutions in the field of insurance for individuals with pre-existing conditions, specifically designed to address the dual challenges of chronic and critical illnesses among the elderly. By identifying causes through early screening for critical illnesses, implementing “three-fixed” management for chronic diseases (fixed timing, fixed dosage, and fixed location) to reduce treatment costs and improve survival rates, and leveraging pharmaceutical benefits to secure premium funding for critical illness coverage.

In addressing patient access, Wanhu Liangfang has chosen to collaborate with municipal health commissions and healthcare security administrations in select cities, establishing central pharmacies as a supplement to community health service centers to reach patients with chronic diseases. Currently, Wanhu Liangfang is operating in Wuhu (Anhui Province), Taiyuan and Yuncheng (Shanxi Province), Guizhou Province, and other regions. This initiative has not only reduced medication costs for local patients with chronic conditions but also significantly promoted the tiered diagnosis and treatment system. It is reported that Wanhu Liangfang is also expanding its online channels, aiming to leverage the internet to broaden its service coverage.

Beyond the aforementioned pain points, Wang Chunxiao, a partner at Jianyibao, believes that patient awareness of insurance still needs to be improved in the development of insurance for individuals with pre-existing conditions. Since insurance agents have historically promoted the concept that “insurance products are a precautionary measure,” and policies targeting healthy individuals have long dominated the health insurance sector, the notion that “one cannot purchase insurance after falling ill” has become a widespread consensus. Consequently, these traditional selling points will now serve as constraints on the growth of insurance for individuals with pre-existing conditions.

Moreover, while existing smart devices and in-diagnosis monitoring can ensure that insurers effectively manage the entire access assessment and process for patient underwriting, there is still a lack of policy guidelines and pathway support for chronic disease management. Taking diabetes as an example, the concept of blood glucose fluctuation is relatively broad; if clear definitions were provided through clinical guidelines, the feasibility of subsequent claims processing and underwriting for insurance covering pre-existing conditions would be significantly enhanced.

Final Thoughts

In 2019, innovative health insurance experienced a surge in popularity, and its pain points gradually came to light. As products targeting the preferred-risk healthy population become saturated, where should insurers go from here?

For the health-conscious segment, insurers need to continuously innovate insurance product structures, refine their product portfolios, and introduce preventive coverage as well as high-quality, affordable options to meet the health protection needs of a broader population.

For individuals with pre-existing conditions, insurance companies can leverage technological tools such as big data and artificial intelligence to enhance actuarial data support for diseases, improve capabilities in integrating medical resources and controlling costs, and strengthen refined risk control and dynamic pricing abilities. By offering more personalized products and services tailored to specific diseases across different age groups, genders, and populations, insurers enable consumers to obtain health insurance coverage that better suits their individual needs.

Insurance for individuals with pre-existing conditions represents a blue-ocean segment within the health insurance market, where both product design and distribution channels remain in their early stages. However, driven by the growing number of individuals with suboptimal health or chronic diseases, rising health-related demands, and policy measures aimed at controlling medical insurance expenditures, this market is poised to evolve into a trillion-yuan industry.