Key Development Priorities for Commercial Long-Term Care Insurance in Addressing Payment Challenges for Disabled Elderly

Grandma Wu and Grandpa Chen are an elderly couple, both in their eighties, who receive services under Shanghai’s Long-Term Care Insurance program through the Fushoukang·Shanghai Kangpu Nursing Station. Grandma Wu, aged 84, suffers from cerebrovascular disease and cognitive impairment, has been bedridden for many years, and experiences significant difficulties with eating and elimination. Before Shanghai implemented its long-term care insurance scheme, she was cared for at home by her 82-year-old husband, Grandpa Chen, due to financial and other constraints.

However, Grandpa Chen had long been plagued by lower back pain. While caring for Grandma Wu, he also had to take medication to alleviate his own back pain, which led to him collapsing from exhaustion on several occasions. After the implementation of the Long-Term Care Insurance program, both were assessed and qualified as beneficiaries of the insurance. They now receive in-home nursing services from Fushoukang·Shanghai Kangpu Nursing Station, with one-hour visits each in the morning and evening.

After receiving professional care, Grandpa Chen remarked, “My stress has truly eased significantly, and seeing her more comfortable now fills me with genuine joy.” Many families like Grandma Wu’s and Grandpa Chen’s are benefiting from subsidies under the Long-Term Care Insurance program, expressing strong affirmation and consistent praise for the services.

December 27, 2019, marked the third half-year milestone of the long-term care insurance pilot program. Over these three and a half years, from the issuance of national macro-level policies for the pilot, to the introduction of local implementation measures, and further to its promotion and development, discussions on long-term care insurance across all sectors have never ceased.

On March 5 this year, when delivering the Government Work Report to the Second Session of the 13th National People’s Congress on behalf of the State Council, Premier Li Keqiang stated: “Expand the pilot programs for the long-term care insurance system, so that the elderly can enjoy a happy old age.”

What Is Long-Term Care Insurance? What Is the Necessity of Its Role as a Payer?

How Have Policies Promoted Long-Term Care Insurance in Recent Years?

What is the current status of long-term care insurance implementation in China’s 15 pilot cities, and what challenges are being faced?

How Has Long-Term Care Insurance Developed Abroad? What Lessons Can Be Learned?

Where Are the Opportunities for Marketization of China’s Commercial Long-Term Care Insurance Market?

Based on the current key focal points within the industry, VCBeat (WeChat: vcbeat) attempts to analyze the future development trajectory of long-term care insurance in China, taking into account its current state of development.

# Long-Term Care Insurance and Long-Term CareWhen discussing long-term care insurance, it is essential to address long-term care. Long-term care refers to a range of health nursing, personal care, and social services provided over a sustained period to individuals who have lost their functional capacity or have never possessed a certain level of functional ability.

Currently, the number of disabled and semi-disabled elderly people in China has exceeded 40 million. This population represents a group with rigid demand for long-term care, requiring human resources to provide services. For a long period, these human resources were primarily provided by medical staff within hospitals, leading to problems such as significant occupation of medical resources, backlog of hospital beds, and increased expenditure on medical insurance funds.

Against this backdrop, the government has been exploring ways to shift care services for disabled elderly individuals out of hospitals, enabling them to receive long-term care at home or in specialized institutions. However, without support from medical insurance, the pensions of disabled elderly individuals are insufficient to cover the costs of long-term care. Although China’s pension levels have risen for 14 consecutive years since 2005, taking Beijing as an example, the average monthly pension in Beijing reached RMB 4,157 in 2019. In contrast, the cost of hiring a live-in caregiver for the elderly in Beijing typically ranges from RMB 5,000 to RMB 9,000 per month, while the lowest monthly fees charged by Beijing nursing homes for disabled elderly residents range from RMB 6,000 to RMB 8,000, with most exceeding RMB 10,000.

Aging before affluence, urbanization-driven miniaturization and “empty-nesting” of family structures, the “4-2-1” inverted-pyramid population structure resulting from the one-child policy, and the limited time and energy of younger generations to assume caregiving responsibilities have collectively spurred the emergence of long-term care insurance in China.

Long-Term Care Insurance refers to a type of health insurance that provides compensation for care expenses incurred when the insured, due to aging, illness, or other reasons, enters a state of physical or cognitive disability requiring specialized institutional or home-based care. Distinct from pension insurance, it targets urban employees and urban residents. Eligibility requires a prior assessment, and benefits are delivered either through government-procured nursing services or direct subsidies for caregiving activities.

In fact, long-term care insurance is an import, with its origins traceable to the 1970s when it first emerged in the form of nursing home insurance. To date, China’s long-term care insurance remains in a pilot phase, and there is ongoing debate among various stakeholders over whether it should be incorporated as the “sixth social insurance.”

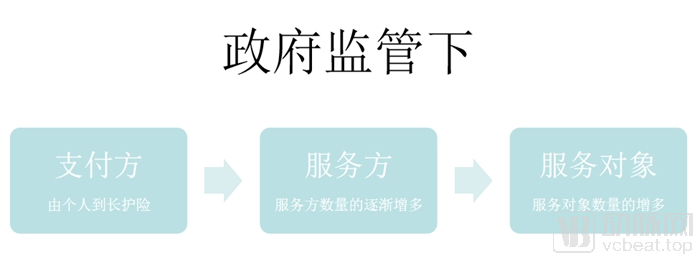

Changes in the Tripartite Dynamics Under China’s Long-Term Care Insurance Policy Regulation

It is undeniable that the development of the long-term care industry relies on four key forces: supply, regulation, payment, and service recipients. The VCBeat article “Where Will Long-Term Care for 40 Million Disabled Elderly Go? Four Solutions to Address Care Challenges” previously provided answers from the supply side. However, even with adequate supply, a lack of payment mechanisms still prevents the elderly from enjoying a secure and dignified old age.

In terms of payment, the government has consistently assumed the role of ultimate backstop, providing full subsidies for individuals in extreme poverty. Meanwhile, it has been continuously exploring subsidy mechanisms for disabled elderly individuals from the working class, having previously introduced measures such as nursing care subsidies. In June 2016, the General Office of the Ministry of Human Resources and Social Security issued the “Guiding Opinions on Launching Pilot Programs for the Long-Term Care Insurance System,” designating 15 regions—including Nantong City in Jiangsu Province, Qingdao City in Shandong Province, and Changchun City in Jilin Province—to pilot the long-term care insurance system, thereby officially ushering in the era of long-term care insurance in China.

Long-term care issues are, in essence, demographic challenges. According to data from the National Bureau of Statistics, China’s population aged 65 and above reached 166.58 million by 2018, accounting for 11.9% of the total population. Moreover, China faces a severe aging crisis, with an unprecedented pace and scale of population aging unseen anywhere else in the world.

In fact, China has had nursing care insurance since 2006. The Administrative Measures for Health Insurance, issued in 2006, categorized health insurance into four types: critical illness insurance, medical insurance, disability income loss insurance, and nursing care insurance. Among these, nursing care insurance further evolved to include long-term care insurance.

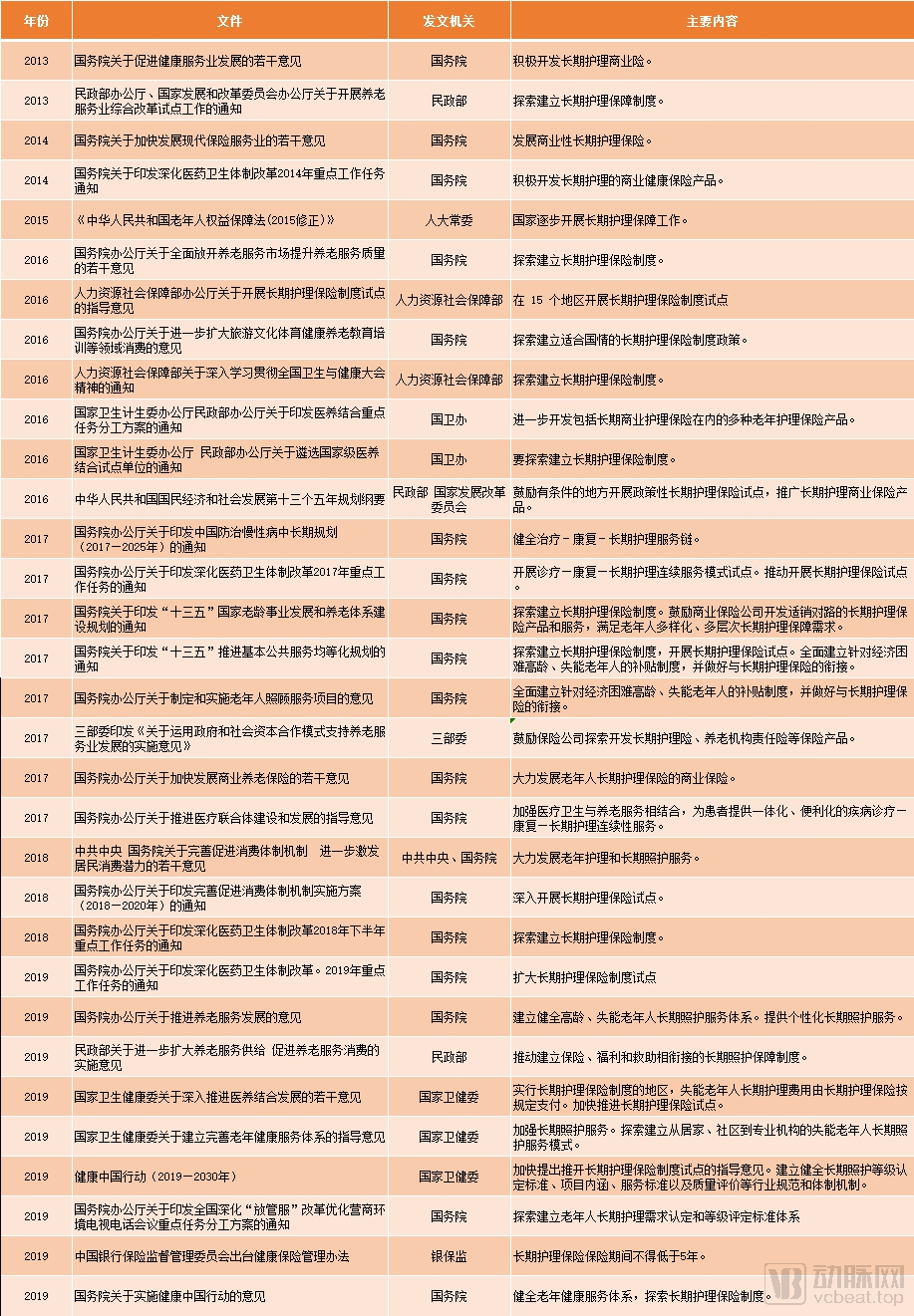

To understand the development of long-term care insurance (LTCI) in recent years, VCBeat has reviewed policies issued over the past seven years. During this period, the central government released a total of 32 policy documents, including 18 issued by the State Council, while relevant ministries such as the Ministry of Civil Affairs, the Ministry of Human Resources and Social Security, and the National Health Commission each issued two or three. Among all these policies, the most significant one is the “Guiding Opinions on Launching Pilot Programs for the Long-Term Care Insurance System,” issued by the Ministry of Human Resources and Social Security in 2016, which has played a pivotal role in the development of LTCI in China in recent years. The other 31 policy references appear only as minor clauses or brief mentions—sometimes just a dozen characters—embedded within broader policy documents. A review of policies from the past seven years shows that China’s promotion of long-term care insurance has gradually shifted from exploration and advocacy to accelerated and strengthened implementation. Throughout this period, efforts to promote commercial long-term care insurance have never ceased.

Source: Compiled by VCBeat based on public information

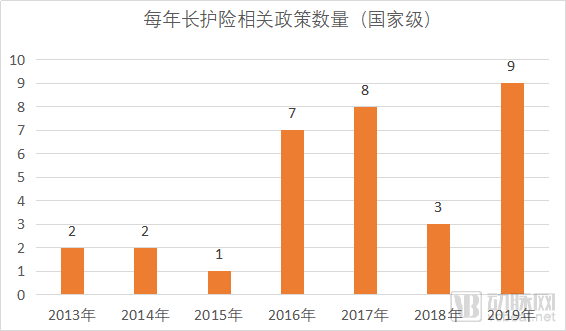

Number of Long-Term Care Insurance Policies by Year (National Level) | Chart by VCBeat

Observing the above policies, 2016 witnessed a significant surge in policy issuance following the promulgation of the Guiding Opinions on Launching Pilot Programs for the Long-Term Care Insurance System. Mentions in national-level policies jumped from just one legal document in 2015 to seven in 2016 and eight in 2017. Meanwhile, 2017 and 2018 also saw an intensive rollout of local-level long-term care insurance policies, with various regions introducing more practical and detailed measures tailored to their respective economic capacities and real-world conditions.

By 2019, the three-year pilot program had garnered positive feedback, with growing calls from all sectors of society for long-term care insurance. Meanwhile, in March, Premier Li Keqiang, representing the State Council, delivered the Government Work Report to the Second Session of the 13th National People’s Congress, stating: “Expand the pilot programs for the long-term care insurance system to ensure a happy old age for the elderly.” That year saw the issuance of as many as nine national-level policies promoting long-term care insurance.

However, among the 32 policies issued over these seven years, only one was specifically dedicated to long-term care insurance, while the others were dispersed across various policies related to elderly care, insurance, and integrated medical and elderly care services, with most constituting only a minor component. Furthermore, there were no clear provisions regarding the implementation details.

7-Year Policy Keyword Extraction | Graphic by VCBeat

From a content perspective, the focus has evolved from initial exploration, advocacy, and pilot programs in the early stages to accelerated implementation, strengthened measures, expanded coverage, and personalized services in later stages. Policy-driven initiatives have become more resolute and urgent. Furthermore, regarding commercial long-term care insurance, the approach shifted from initial promotion to further standardization in 2019.

Since the 15 pilot regions were designated in 2016, these areas have formulated their own specific plans based on their respective economic strengths and practical circumstances, establishing detailed provisions for covered populations, payment methods, and payment ratios/amounts.

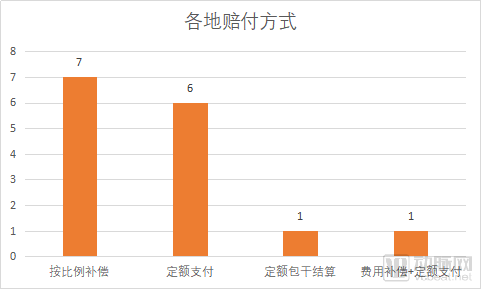

Source: Taiping Allianz Research Report, “Research Report on the Development Model and Practice of Commercial Long-Term Care Insurance in China”

An overview of the above pilot policy schemes reveals that while there are differences across regions, a careful analysis shows certain commonalities:

(1) Primarily based on proportional payment and fixed-amount payment

Proportional payment and fixed-amount payment are currently the more favored approaches across various regions, as they offer greater flexibility compared to lump-sum capped settlements. For instance, some regions have incorporated households into this system; if an elderly individual has family members available to provide care, the subsidy funds can be disbursed directly to the elderly person.

(II) The coverage primarily targets individuals with severe disability.

The “Guiding Opinions on Launching Pilot Programs for the Long-Term Care Insurance System” clearly stipulate the scope of coverage: “The long-term care insurance system targets insured individuals who have been in a disabled state for an extended period, with a focus on covering the costs of basic daily living care and medical nursing services closely related to basic daily living for those with severe disabilities.” Among the 15 pilot cities, eight adopted the Barthel Index as the basis for assessing elderly individuals with severe disabilities, with Changchun additionally introducing the Karnofsky Performance Status (KPS) scale for cancer patients.

(3) Classification of payment types is primarily based on home-based care, institutional care and medical services, and nursing services.

In the payment ratio/amount column, except for Chongqing, which is calculated at 50 yuan per person per day, other regions either calculate payments separately for home-based care and institutional care, or separately for medical services and nursing services.

(4) In principle, services must be received at designated medical, elderly care, and nursing institutions.

Regarding service providers and payment mechanisms, all 15 pilot cities require the signing of service agreements with designated medical, elderly care, and nursing service institutions to stipulate agreed-upon prices for long-term care services and insurance reimbursement standards. When care services are provided, insured individuals settle their out-of-pocket portions, while the long-term care insurance agencies periodically settle the portions covered by the long-term care insurance fund with the institutions. For home-based care or care received at non-contracted institutions, a few cities also provide subsidies to insured residents; for example, Anqing offers a nursing subsidy of RMB 15 per day for those receiving home-based care from non-contracted nursing service providers.

The significance of pilot programs lies in their capacity for trial-and-error learning and systematic review, which will lay the foundation for the comprehensive nationwide rollout of long-term care insurance (LTCI) in the future. However, as of now, LTCI has not yet been fully implemented across China. In addition to the immaturity of its development model, a key contributing factor is that the issue of financing remains unresolved.

The funding issue of long-term care insurance has become a focal point of discussion within the industry. The reliance of long-term care insurance on medical insurance observed during pilot programs poses significant challenges to its future financing, particularly given the current sustainability pressures facing medical insurance itself.

Amid limited funding levels and modest subsidies, calls from all sectors of society for commercial long-term care insurance, as a supplement to social security, are growing louder.

The "Action Plan for Promoting Health in the Elderly," released in July 2019, proposes nine indicators and 23 specific action items across three levels: individuals and families, society, and government. It aims to reduce the incidence of disability among adults aged 65 to 74 and slow the growth rate of dementia prevalence among those aged 65 and older over the next decade.

It is evident that disability among the elderly has become a relatively high-probability event, with the number of disabled individuals rising in tandem with the growing elderly population. Meanwhile, low- and middle-income groups constitute a significant proportion of China’s population. In this context, social security-based long-term care insurance is insufficient to cover the long-term care costs of the elderly, leaving substantial market potential for commercial long-term care insurance.

However, in reality, long-term care insurance accounts for less than 1% of the health insurance market share, indicating a relatively untapped market. As of the press deadline (December 17, 2019), data from the life and health insurance product database of the Insurance Association of China shows that there were 89 long-term care insurance products currently on the market. Among these, PICC Health Insurance Company Limited offered the largest variety, with a total of 33 products, followed by Kunlun Health Insurance Company Limited and Hexie Health Insurance Company Limited, with 10 and 8 products, respectively. Notably, 24 insurers were involved in offering long-term care insurance.

Source: Life Insurance Product Database of the Insurance Association of China; Graphic by VCBeat

According to queries of the Life Insurance Product Database of the Insurance Association of China, there were once 265 long-term care insurance products, whereas only 89 are currently available for sale. Further analysis reveals two primary reasons for this decline. On one hand, long-term care insurance is highly susceptible to adverse selection, and public awareness remains low, resulting in poor sales performance or financial losses. On the other hand, due to insufficient early-stage regulations, the former China Banking and Insurance Regulatory Commission (CBIRC) conducted a rectification campaign in 2017, leading to the discontinuation of a portion of these products.

Zhu Minglai, Director of the Center for Health Economics and Medical Security Research at Nankai University, told reporters, “The long-term care insurance that emerged at that time actually went off track. Because there were no standards for assessing disability among the elderly at the time, insurance companies ended up distributing benefits much like pensions—for example, paying a fixed monthly amount once individuals reached age 60. This approach failed to reflect the essential nature of care services.”

To reflect the nursing care nature of the service, the government has put forward the requirement of “government-led, socially operated, and market-oriented services.” Major insurance companies are leveraging this opportunity to further explore the lucrative long-term care insurance market. It is reported that ten commercial insurers, including Taikang Pension, Pacific Life Insurance, and China Life Insurance, are currently involved in the administration of long-term care insurance. Through government procurement, these insurers participate in pilot programs for policy-based long-term care insurance, providing services such as policy consultation, qualification verification, initial expense review, and fund settlement and disbursement.

Huang Chunfang from Taikang Pension Insurance told reporters that, as of the end of November 2019, Taikang had participated in the administration of long-term care insurance services in eight national-level pilot cities, including Jingmen (Hubei), Chengdu (Sichuan), Guangzhou (Guangdong), and Ningbo (Zhejiang), as well as 16 non-national-level pilot cities, including Shijingshan District (Beijing) and Jiaxing (Zhejiang). The company served over 15 million insured individuals and had cumulatively disbursed more than RMB 195 million in long-term care insurance benefits. In terms of building the long-term care insurance system, the company primarily focused on the following three areas:

First, assist in conducting policy research.Collect domestic and international policies and regulations to compile a policy compendium; analyze the characteristics of local policies, integrate them with local realities, and propose policy recommendations; regularly communicate and report on the progress of pilot regions to assist healthcare security authorities in timely understanding of implementation status across different areas.

Second, to assist in conducting baseline surveys on the local prevalence of disability and the current status of elderly care services.Assist cities in conducting surveys on the supply and demand for care services (including market supply of nursing institutions, estimation of nursing costs, and care needs of the disabled population), ensuring that policy formulation is evidence-based, scientific, and rational.

Third, it supports the calculation of financing and benefit standards.Leverage professional actuarial expertise to conduct projections on the aging and disability status of insured populations in pilot cities, total funding (including recommendations for funding channels and contribution ratios), contribution standards, benefit coverage levels, and long-term care costs. Based on these projections, prepare a long-term care insurance actuarial report with recommendations to provide an evidence base for formulating implementation plans.

This process enables the accumulation of data and experience, laying the foundation for the subsequent development of commercial long-term care insurance.

As population aging intensifies, efforts to address the challenges it poses have led to the emergence of four typical models of long-term care insurance systems worldwide: the market-led model represented by the United States, the dual-track system represented by Germany, the public-private partnership model represented by Singapore, and the universal social insurance model represented by Japan.

This article selects the United States, representing long-term care insurance with the highest degree of marketization, and Japan, representing long-term care with the greatest government responsibility.

The United States: The Rise and Fall of Commercial Long-Term Care Insurance

Among the U.S. population aged 65 and older, approximately 70% require various forms of long-term assistance with activities of daily living and medical care services. To address these challenges, the U.S. government has adopted a two-pronged approach: on one hand, it provides supplemental coverage for low- and middle-income individuals through public safety-net programs funded by federal and state transfer payments; on the other hand, it employs national policy support and market-based mechanisms, using policy incentives to encourage individuals to purchase commercial long-term care insurance.

Currently, approximately 60% of long-term care costs in the United States are covered by public insurance programs, with Medicare accounting for 20% and Medicaid for 40%. The remaining costs are primarily borne by commercial insurance (7%), out-of-pocket payments by individuals (29%), and other sources such as the Department of Veterans Affairs and charitable programs (4%). This demonstrates that while public insurance programs play a significant role in the U.S. long-term care insurance system, they have substantial limitations.

Consequently, the commercial long-term care insurance market has developed relatively well in the United States. According to a survey by Broker World magazine (2013), nearly 230,000 individual long-term care insurance policies were sold nationwide in 2012. However, in recent years, significant issues have emerged in the U.S. commercial long-term care insurance sector. According to an industry insider who wished to remain anonymous, the main problems include:

1. Underestimation of Premiums, Pricing Errors

Estimates and pricing for long-term care insurance are often determined two to three decades before the actual need for care arises. Previously, due to insufficient data and experience, factors such as increased life expectancy and rapid inflation were frequently overlooked. In this context, premium increases became inevitable, creating a vicious cycle of “price hikes–policy lapses–worsening loss ratios–further price hikes,” which ultimately led to product failure.

2. Strong adverse selection

For the elderly, disability is often a sudden event; acute conditions such as heart attacks and strokes can lead to full or partial disability. However, there is currently no clearly predictive model available in the industry. Consequently, this population exhibits a greater degree of adverse selection.

Japan: “Universal” Long-Term Care Insurance with 90% Reimbursement

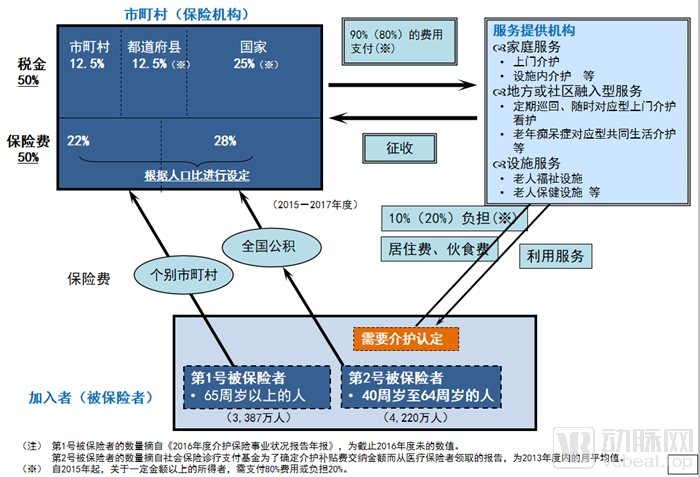

Japan’s long-term care insurance system, known as the “Kaigo Hoken” (Long-Term Care Insurance) system, was implemented on April 1, 2000, and currently covers nearly 100% of the population aged 65 and older.

Structure of the Long-Term Care Insurance System

Structure of the Long-Term Care Insurance System

Source: Remarks by Yoshiro Hano, First Secretary of the Consular Section/Economic Section, Embassy of Japan in China

As shown in the figure above, the beneficiaries of Japan’s Long-Term Care Insurance system include two groups: individuals aged 65 and older, and those aged 40 to 64 who are enrolled in health insurance.

Insured individuals under the Long-Term Care Insurance system are required to pay 10% (or 20%) of the service costs out-of-pocket, while the remaining 90% (or 80%) is covered by the Long-Term Care Insurance budget established by municipal governments. Municipal insurance premiums are funded 50% by contributions from insured individuals and 50% by public fiscal resources.

Due to the high proportion of social insurance coverage in Japan, the development of commercial long-term care insurance has remained sluggish. In recent years, as fiscal expenditure pressures have intensified, rumors have circulated that reimbursement rates under the public long-term care insurance scheme would be reduced. Consequently, Japan’s commercial insurance sector has gradually begun to explore opportunities in the long-term care insurance market.

A summary of the issues surrounding long-term care insurance in these two countries reveals that, on one hand, the development and pricing of commercial long-term care products rely on the accumulation of extensive, long-term empirical data, making it difficult to achieve a successful business model in the short term; on the other hand, excessively high social security reimbursement rates not only increase fiscal pressure but also hinder the market-oriented development of long-term care insurance.

So, what will commercial long-term care insurance in China do?

Compared to older generations, who tend to favor “saving,” those born in the 1980s and 1990s are more inclined toward “investing.” As public attention to health grows, health insurance will usher in greater opportunities for development.

Currently, the long-term care insurance market within the health insurance sector remains a blue ocean. However, most commercial insurers have shelved such products due to high risk coefficients. The health insurance industry is currently plagued by issues such as product homogenization and intense competition. For commercial insurers, developing innovative products is a key pathway to enhancing their core competitiveness.

For commercial insurance companies, data analysis derived from long-term administration of long-term care insurance, combined with factors such as inflation and increased life expectancy, will inevitably lead to the launch of suitable long-term care insurance products. VCBeat boldly predicts that the following types of long-term care insurance will become the preferred approaches for commercial insurers in the future:

1. Group Commercial Insurance

Given that disability is a high-probability event, insuring individuals separately poses excessive risk for insurance companies, whereas group policies can mitigate such risks. Among the current 89 long-term care insurance products, 13 are already group policies. Going forward, group long-term care insurance is likely to become a key focus for commercial insurers’ future development.

2. Co-developing long-term care insurance with elderly care enterprises

In 2016, Xinmei Mutual Insurance partnered with Qingmeng Elderly Care to launch the “Ai Hu Bao – Long-Term Care Protection Plan,” a product integrating insurance coverage with nursing services. Designed for elderly individuals who prefer aging in place but require long-term care, the plan allows policyholders, upon assessment and qualification for care needs, to receive professional in-home caregiving from certified nurses provided by Qingmeng. The coverage period spans five years, with the price locked in for the duration and no additional fees charged.

For insurance companies, partnering with a certain number of elderly care enterprises to share risks is also a method for developing and promoting long-term care insurance.

3. Develop long-term care insurance for the mid-to-high-end market

Zhang Qifeng, Marketing Director at Puqin Elderly Care, told reporters that, much like basic medical insurance, long-term care insurance serves only as a fundamental form of social security. Middle- and high-income individuals have certain expectations regarding service quality and environment. Therefore, there is considerable potential for developing commercial long-term care insurance products tailored to this demographic, whether for home-based care or care provided by mid- to high-end elderly care institutions.

4. A Combined Approach of Financial Subsidies and Service Purchasing

Insurance clients are distributed across the country. For most insurers, it is difficult to provide services individually to one or two insured persons in relatively remote areas; therefore, financial subsidies are primarily offered to this group. In contrast, in regions with a larger number of policyholders, insurers may purchase services locally for the insured.

References: Taiping Allianz Health Insurance Research Report, “Research Report on the Development Model and Practice of Commercial Long-Term Care Insurance in China”; Dr. Chen He’s research report released by the School of Public Health at Peking University, “Research Report on Financing Policies for Long-Term Care in China”; academic paper, “The U.S. Long-Term Care Insurance System: Origins, Structure, Issues, and Implications.” Special Acknowledgements