Innovation in Pharmaceuticals Accelerates: AI Integrates into Full Drug Development Lifecycle — Two Landmark Reports Launched at VB100 2019

From December 20 to 22, the “2019 Future Healthcare Top 100” Forum, hosted by VCBeat and co-hosted by KPMG China, Legend Capital, BV Baidu Venture Capital, Weilai Capital, Puhua Capital, Tsinghua Nomura China Research Center, Changling Capital, Legend Star, Yuanjing Capital, the Internet Hospital Branch of the Chinese Association of Research Hospitals, Aimeda, Zero2IPO Capital, and Yanzhi, kicked off at the Jiuhua Villa in Beijing.

With over 5,000 registrants, this year’s conference features 15 forums: Future Healthcare Summit, Top 100 Summit, Leaders’ Summit, Health and Medical Fund Partners Summit, China-Japan Health Industry Development Forum, Innovative Drugs Forum, Innovative Health Insurance Forum, Digital Pathology and Precision Diagnostics Forum, Health Management Forum, Medical Devices Forum, Internet Hospital Forum, Smart Hospital Construction Forum, Pharmaceutical Digital Marketing Forum, Biotechnology Forum, and Medical AI Forum, covering the 11 hottest sectors of 2019.

The 2019 Future Healthcare Top 100 Innovative Drugs Forum, co-hosted by VCBeat and Aimeda Pharmaceutical Consulting Co., Ltd., took place throughout the day on December 21. It brought together leading enterprises and institutions from all sectors of the innovative drug industry, including industry, academia, research, and investment. Distinguished attendees provided in-depth analyses of future development trends and opportunities in the field of innovative drugs, examining them from multiple perspectives such as technological transformation, R&D strategies, and investment trends.

The morning session on the 21st focused primarily on drug mechanisms and clinical development strategies. The featured speakers included Cai Daqing, Founding Managing Partner of Sherpa Capital; Xu Hong, Chairman of Ameda (Beijing) Pharmaceutical Information Consulting Co., Ltd.; Kang Xiaoqiang, Founder of WellBiologics; Liu Jing, Deputy Medical Director at NuoSiGe (RisingMed); Tang Li, Vice Chairman and Chief Technology Officer at Huahao Zhongtian Biopharma; Chen Penghui, Partner at Boyuan Capital; Li Shichen, Director of Product Operations at Han’s Union; and Shi Yuankai, Deputy Director of the National Cancer Center and Vice President of the Cancer Hospital, Chinese Academy of Medical Sciences (listed in order of presentation).

On the afternoon of the 21st, discussions primarily focused on the application and future prospects of artificial intelligence technology in innovative drug research and development. The guest speakers included Zhang Suyang, Founding Partner of Volcanic Stone Capital; Lu Yinying, Director of the Tumor Diagnosis, Treatment, and Research Center at the 302nd Hospital of the Chinese People's Liberation Army; Tan Haibin, Vice President and Chief Commercial Marketing Officer of Pharmaron (SaiFu Medicine); He Zhi, President of Happy Life Technology Group (HLT); Yang Haiding, Founder and CEO of YanZhi; Hu Qitong, CTO of Yaoling Medical Technology; Lai Lipeng, Co-founder of XtalPi; and Feng Dongzhi, Operations Director at Yudao Bio (listed in order of presentation).

Below is a summary of the key points from each speaker:

On the Joys and Concerns of Innovative Drugs: The joy lies in the rapid technological advancements both domestically and internationally, with significant progress made in various emerging therapeutic modalities. Many new startup teams, particularly those engaged in innovative fields abroad, are returning to China to drive innovation. Some domestic innovation teams have already approached a globally leading position and will continue to explore more uncharted territories in the future. We have also observed that many policies in China have been introduced, and those already released are being steadily advanced.

On the downside, domestic payment capacity in China remains inadequate, and the approval speed for certain imported drugs is still faster than that for domestically produced innovative drugs. Furthermore, numerous other specific challenges are embedded throughout the R&D process of innovative drugs.

Today, I would primarily like to discuss innovative drug investment with you through the four key stages of fundraising, investment, management, and exit.

“Fundraising” in investment has, on the whole, yielded few cause for celebration. With limited capital available, it is essential to recognize the current landscape and strive for growth. Much has already been said about the “concerns,” primarily because exiting RMB-denominated investments in China is indeed exceedingly difficult. The prolonged inability to realize returns can significantly impair an institution’s operations. These issues are intertwined with China’s broader capital market and will require time to resolve.

From the perspective of investment, a positive development for us is the reduction in noise and competition. We are pleased to see that some of our peers have matured, recognizing that strong early-stage results in pharmaceutical investments do not necessarily guarantee favorable long-term outcomes. What concerns us about the Chinese market? The shrinking pool of co-investors. Previously, it was straightforward to collaborate with several institutions to deploy $100 million; now, securing even $70–80 million requires considerable effort. Nevertheless, high-quality projects continue to attract sophisticated investors. We have also been fortunate, as some of our portfolio companies have still delivered outperformance.

From the perspective of market cultivation, there will be certain changes in the regulatory landscape for new drugs. The dynamics of payers are a critical factor influencing future investment returns. If drug prices continue to decline, it is likely that not only generic drugs but also innovative drugs will be affected. At the other end of this spectrum lies the question of who will bear the cost for gene therapies, gene editing, and various other frontier innovative medicines. China indeed needs to establish an appropriate commercial health insurance payment system, and we remain optimistic about this sector.

“Exit” is one area that shows some positive signs; the STAR Market and Hong Kong’s Chapter 18A are both encouraging developments. However, we also observe that innovative drug companies listed in Hong Kong and the United States have opportunities for follow-on financing, whereas the specific situation on China’s STAR Market remains unclear. If innovative drug enterprises cannot access follow-on financing after their IPOs, yet their subsequent clinical pipelines require further capital support, these companies may find themselves in a stalemate.

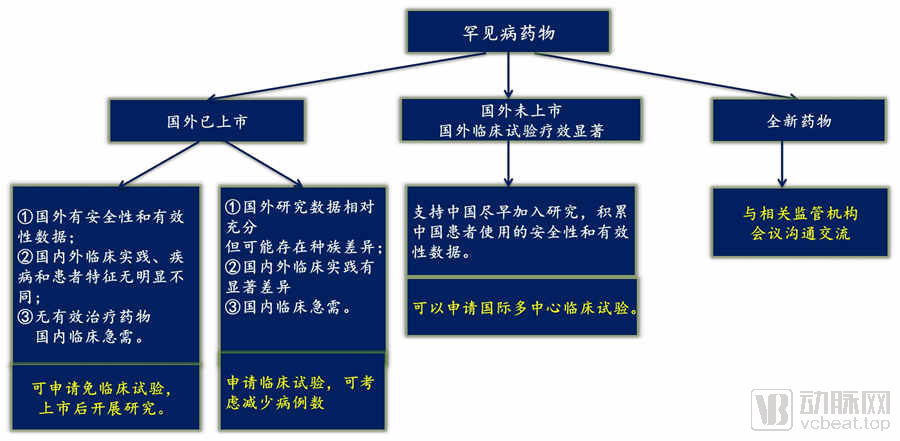

Why Are So Many Large International Pharmaceutical Companies Focusing on the Rare Disease Market? Beyond Corporate Social Responsibility, Profit Motives May Be an Even Greater Driver. According to the “Orphan Drug Report 2019” published by EvaluatePharma, global orphan drug sales reached $131 billion in 2018 and are projected to reach $242 billion by 2024, growing at twice the rate of non-orphan drugs.

Rare diseases affect a small patient population, entail limited market demand, and involve high research and development (R&D) costs, resulting in a severe shortage of clinically available treatments. Globally, there are more than 7,000 rare diseases, yet fewer than 10% have approved therapeutic options. To bolster pharmaceutical companies’ motivation and enthusiasm for orphan drug R&D, governments in many countries have introduced a series of incentive policies and measures related to orphan drug development.

Market exclusivity is a key post-approval protection measure for orphan drugs. For instance, in the United States, the market exclusivity period is seven years, granting a degree of monopoly status after drug launch. There are also significant tax incentives, including a 50% credit for U.S. clinical research expenses. Additionally, special approval pathways are established to expedite drug marketing authorization.

Driven by supportive policies across various countries, the orphan drug market has achieved substantial growth. Notably, six of the top ten drugs by global sales in 2018 had received “Orphan Drug” designation from the U.S. FDA. Drugs such as Keytruda, Opdivo, and Revlimid were initially launched with orphan drug status and gradually expanded to include multiple indications for both rare and non-rare diseases.

China remains an underdeveloped area in the field of rare diseases. For a long time, China has lacked fundamental data on rare diseases, and relevant regulations and policies have remained largely absent. Compared with the international market, China’s orphan drug market is still marginalized. On a positive note, the country is increasingly prioritizing this area; in 2018, China released the First Batch of Rare Diseases Catalogue, and the National Health Commission launched a rare disease registration system.

Nevertheless, China still faces immense pressure in the research and development (R&D) of orphan drugs. On one hand, the limited market demand for rare diseases, coupled with high risks and lack of profitability, has led pharmaceutical companies to selectively “ignore” this field. On the other hand, new drug development encounters numerous challenges: ① relatively weak basic research and insufficient translational capacity in China; ② limited prior experience in participating in international multicenter studies on rare diseases, and a scarcity of research centers capable of conducting clinical trials for rare disease drugs; ③ difficulties in implementing clinical trials. China needs to establish and improve incentive policies and measures related to orphan drug R&D, such as granting market exclusivity to trade time for market access.

Furthermore, under China’s current medical security system, limited health insurance funds fail to cover the high costs of many rare disease medications, leaving patients with a substantial financial burden. In contrast, commercial insurance serves as the primary source of treatment funding for rare disease patients in the United States. Looking ahead, China could introduce commercial insurance mechanisms to help alleviate the financial burden of medical care for these patients.

Amid the dual pressures of national reimbursement negotiations for innovative drugs and centralized volume-based procurement for generics across China, domestic enterprises are even more reluctant to venture into the rare disease sector. Therefore, in addition to top-level design and policy advocacy at the national level, it is recommended that detailed implementation rules be established to safeguard the tangible interests of enterprises. Furthermore, strategies such as designated production for scarce drugs could be adopted for niche rare disease medications to address issues of patient access to treatments.

Finally, regarding recommendations for enterprises, Xu Hong stated that domestic companies dedicated to the research and development of rare disease drugs should proactively participate in promoting the establishment and improvement of China’s rare disease policies, while also defining their strategic positioning and selecting pathways suited to their own development.

For traditional pharmaceutical companies, venturing into the rare disease sector represents a pathway for upgrading and transformation, which also helps build corporate reputation and shape brand image. For innovative enterprises, it is advisable to draw on international experience, fully leverage existing global data and resources, and formulate global R&D strategies for rare disease drugs.

In either scenario, the ultimate goal for enterprises today is to deliver products with clinical value in order to reap market benefits. This can be achieved by either addressing currently unmet clinical needs or providing alternative options within existing treatment regimens to reduce the medication burden.

Tumor immunotherapy targets tumor-infiltrating immune cells. By modulating these immune cells, it indirectly kills tumor cells. Currently, tumor immunotherapy holds the greatest promise for curing cancer.

Currently, inhibitors targeting two main checkpoints have been approved: one group targets PD-1 and PD-L1, and the other targets CTLA-4. These two checkpoints are fundamentally different. CTLA-4 primarily prevents excessive activation of T cells in lymph nodes, whereas PD-1 mainly suppresses T cell activity within the tumor microenvironment. This is the primary distinction between them.

PD-1 and PD-L1 inhibitors have been approved for many types of cancer, but response rates vary significantly. In some cancers, the response rate is only slightly above 10%, whereas in melanoma it can reach 40%–50%. This variation is related to the mutational landscape of different tumors as well as the tumor microenvironment. When discussing combination therapies involving PD-1 and PD-L1 inhibitors, the differences in response rates become even more pronounced.

Where Do the Opportunities Lie for PD-1 and PD-L1, or CTLA-4? The Opportunity Lies in Combination Therapies Based on Tumor Immunotherapy Drugs. Theoretically, All Targets That Enhance Tumor Immunity Can Be Combined with PD-1.

Currently, combination therapies are advancing rapidly in four areas: combination with other immune checkpoint inhibitors, oncolytic viruses, VEGF inhibitors, and TGF-β inhibitors.

Future profitability opportunities for PD-1 monoclonal antibodies will lie in combination therapies. However, the mechanisms underlying these combination therapies remain poorly understood. In research on combination therapies, animal studies alone are insufficient. Notably, for many diseases, there are no suitable animal models for evaluating combination treatments; for instance, appropriate models are lacking for dual-target combination therapies. Another critical challenge is biomarkers: identifying suitable biomarkers to enhance the efficacy of PD-1-based combination therapies remains a significant hurdle.

Tumor heterogeneity is significant, with substantial variations in PD-L1 expression across different sites. This variability extends beyond PD-L1 to other therapeutic targets as well. Consequently, determining the optimal approach to combination therapy under such circumstances remains a challenge.

Another issue is toxicity, which has not been widely reported thus far. At least from what we have observed with PD-1 and PD-L1 inhibitors, the incidence of adverse events associated with the combination of anti-PD-1 and CTLA-4 therapy has increased from 16% to 55%, indicating that this toxicity is quite severe.

Furthermore, there is the challenge of overcoming the paucity of anti-tumor T cells within tumors. Progress has been made in this area through the use of bispecific antibodies that bridge T cells and tumor cells, thereby enabling non-specific T cells to exert cytotoxic effects against the tumor. In my view, this therapeutic approach will pose significant competition to CAR-T therapy for two primary reasons: first, bispecific antibodies have demonstrated favorable efficacy; second, the manufacturing lead time for CAR-T therapy is protracted, which many patients cannot afford to wait.

Overall, drug development in China exhibits the following characteristics.

The review timeline for New Drug Applications (NDAs) is being progressively shortened; furthermore, the time lag between U.S. approval and availability of certain imported drugs in China is also gradually narrowing.

Furthermore, the approval of all new drugs is guided by clinical needs. The types of approved drugs have become highly diversified, particularly in oncology, covering both major and rare cancer types.

Another point worth noting is that drug approval pathways have become increasingly diversified. Previously, many drug approvals were based on Phase III trials involving more than 300 patients. This year, numerous approved drugs have gained authorization through various routes, including bridging studies, single-disease Phase II trials, key studies as part of international multicenter trials in which China participated, and even direct acceptance of overseas data.

In 2018, experts from the Center for Drug Evaluation (CDE), led by Mr. Zhou Ming, published a dedicated article providing a detailed introduction to the conditions for approving single-arm trials and key considerations during the trial process. The article also noted that after the first domestically developed new drug with independent intellectual property rights received conditional approval based on a single-arm trial, drugs not eligible for single-arm studies would no longer be supported for registration via this pathway. Concurrently with the initiation or upon completion of the single-arm trial, a confirmatory Phase III trial must be conducted to ultimately ensure the drug’s full approval for market launch.

Considerations for Biosimilar Development: Overall, the primary objective in biosimilar development is to demonstrate similarity to the reference product, thereby streamlining research and reducing costs. The clinical development pathway for biosimilars is relatively straightforward; regulatory approval is generally granted based on a Phase I pharmacokinetic/pharmacodynamic (PK/PD) comparative study and a Phase III trial confirming therapeutic equivalence.

For certain biosimilars already marketed abroad, if preliminary studies demonstrate minimal ethnic differences, the sample size may be reduced through statistical methods based on the principle of consistency. In accordance with the ICH E17 guideline on multi-regional clinical trials and the principle of equivalence and consistency, the odds ratio of the objective response rate (ORR) can be selected as the basis for efficacy analysis. Demonstrating consistency suffices for regulatory approval and market authorization.

For pharmaceutical companies engaged in new drug development, defining the product’s positioning is critical during the early stages of R&D. In this process, it is essential to first understand the current diagnostic and therapeutic landscape of the intended target indications, assess unmet patient needs, and evaluate the significance of these needs. Additionally, companies must analyze how their products can differentiate themselves from existing alternatives. A thorough understanding of current standards of care and the competitive market landscape is also required. This approach ensures a clear strategic direction for the product’s research and development.

Overall, the Center for Drug Evaluation (CDE) continues to encourage innovation in its broad strategic direction. It aims to gradually align China’s regulatory practices with those of the U.S. Food and Drug Administration (FDA) and foster the emergence of novel design methodologies. For instance, this past September, the CDE issued specific guidelines on statistical considerations for clinical trials. Therefore, innovative pharmaceutical companies should engage in early communication and dialogue with the CDE, and incorporate its recommendations into their discussions and development of study designs.

We initiated our innovative drug research as early as 2001. Following a series of preclinical and clinical trials, we submitted our New Drug Application (NDA) in March 2018 and were granted priority review in June. However, to date, we are still awaiting the market launch of the new drug.

Our Phase I clinical study was designed with a dose-escalation regimen involving consecutive administration at doses of 35 mg, 40 mg, and 45 mg. Among the 15 patients with advanced metastatic cancer enrolled in our Phase I clinical trial, 3 achieved a partial response (PR) out of the 13 efficacy-evaluable patients, which represents a highly favorable outcome for a Phase I clinical trial.

As an innovative anticancer chemotherapy drug that demonstrated significant efficacy in its Phase I clinical trials back in 2009, it has still faced considerable challenges to reach where it is today. There are many investors present here who may well understand the difficulties we encountered in securing financing at that time. Consequently, although we obtained approval for subsequent Phase II clinical trials, we lacked the funds to initiate them. It took another one to two years before we successfully raised capital and commenced the Phase II clinical study.

In our two Phase II clinical trials, over 90% of patients in both the combination therapy and monotherapy groups had previously received anthracycline- and taxane-based regimens, and were undergoing second-line, third-line, or even fourth-line treatment. Nearly 50% of the patients had received more than four lines of therapy.

Our Phase II efficacy results showed an objective response rate (ORR) of approximately 28% in the monotherapy group, which increased to over 40% with combination therapy. The median progression-free survival (PFS) was 5.4 months for monotherapy and reached 7.9 months for combination therapy.

Building on the Phase II results, we initiated a Phase III trial in combination with capecitabine in 2014. In our Phase III study, the combination regimen was compared against capecitabine monotherapy, demonstrating a progression-free survival (PFS) extension of more than 4 months and a 54% reduction in the risk of disease progression.

Innovative drugs are granted priority review, with an average turnaround time of nine months. We submitted our application over a year and a half ago, yet we are still awaiting review. The primary issue is that many experiments were conducted too early, resulting in an excessively long preclinical development period. Given the significant policy changes implemented in 2017 and 2018, many aspects of our early-stage R&D, particularly pharmaceutical development (CMC) work, may not fully align with current standards.

“Everyone is saying that hope lies ahead; we have already seen the light at the end of the tunnel. We hope this product will be brought to market as soon as possible, to benefit patients with advanced-stage cancer.”

There is still significant room for improvement in the overall survival rates of cancer patients in China compared to the global average. For instance, there remains a substantial gap between China’s lung cancer mortality rate and the world average. Furthermore, the prognosis for cancers with high incidence in China, such as liver cancer, gastric cancer, and esophageal cancer, remains unfavorable.

Early detection remains a challenge, but the most critical issue is actually the treatment of patients with intermediate- to advanced-stage disease. This is not unique to China; it is a global phenomenon, as patients with intermediate- or advanced-stage cancer constitute a very large proportion of cases. Even in the United States, advanced-stage lung cancer accounts for more than half of all cases. The management of advanced-stage disease primarily relies on systemic, multidisciplinary comprehensive therapy centered on pharmacological interventions, making drug development particularly crucial.

We conducted a retrospective analysis and summary of the landscape of anticancer drugs in China over the past decade. Clinical trials of anticancer drugs in China have made rapid progress in the last ten years. Particularly since 2012, benefiting from the National Science and Technology Major Project on Major New Drug Innovation, the state has provided not only financial support but, more importantly, policy incentives, which have attracted significant social attention and spurred the development of a large number of drug candidates. By 2016, these candidates had sequentially entered clinical trials, resulting in very rapid growth over the most recent three-year period.

Since the 1990s, drug development guided by precision medicine has undergone significant changes, particularly due to advances in the study of driver genes. In recent years, gene target-driven drug development has become the primary research and development direction for diseases such as non-small cell lung cancer.

Patients with EGFR-TKI–sensitive mutations account for 40%–50% of all cases of advanced lung adenocarcinoma in China; therefore, we have a substantial patient population, and our research is increasingly garnering international attention.

China’s first independently developed new drug was Icotinib. From the synthesis of the compound in 2002 to its market launch in 2011, it took a decade of dedicated effort. This drug is, in fact, a milestone in innovative drug research and development in China since the reform and opening-up. The development of Icotinib coincided with the process of pharmaceutical industry reform in China. Many changes in approval and evaluation systems were continuously explored and shaped during this period, forming the initial concepts.

Immunotherapy has witnessed a surge in recent years. At this year’s World Conference on Lung Cancer, the results from the CheckMate 017/057 studies revealed that the five-year survival rate was 2.6% in the control group and reached 13.7% in the experimental group treated with Opdivo—a remarkably significant finding.

Current treatment approaches differ significantly from those of a few years ago. Patient stratification has become increasingly refined, with the selection of targeted therapy, immunotherapy, or chemotherapy alone guided by biomarkers, pathological findings, and PD-L1 expression levels. Consequently, research findings continue to reshape clinical practice. Among all cancer types, lung cancer has witnessed the most substantial therapeutic advancements in recent years.

Conquering lung cancer requires the collective efforts of our industry to advance the research and development of new drugs and novel therapeutic approaches. Through continuous exploration, we aim to provide patients with advanced-stage disease with the best and most precise treatments, while simultaneously reducing the physical burden they endure during therapy. Only in this way can we help patients live longer and better lives, thereby achieving the strategic goals set by our nation.

The 14th, 15th, and 16th Five-Year Plans explicitly state in their fifteen-year development outlines that our strategic goal is to fully meet the health needs of the Chinese population with domestically developed pharmaceuticals. These are not low-quality generic drugs of the past, but the most advanced and superior medicines available worldwide.

Whether we are investors, entrepreneurs, or scientists, the country has provided us with a vast arena to showcase our talents and unleash our boundless wisdom—a historic window of opportunity.

The first point is data. Data alone has been growing in a parabolic trajectory since its inception, with a growth rate characterized by a second-order derivative. Nothing else exhibits such unidirectional growth without decline, and at an accelerating pace. Moreover, this trend is set to continue; it is estimated that within the next three years, the volume of data will increase more than tenfold. Why has such an enormous amount of data emerged seemingly out of nowhere? Why are we witnessing an ever-increasing surge in data generation at this juncture?

3.5 billion years ago, the earliest primitive cell emerged on Earth. Everyone in this room today is a descendant of that primordial cell. Since we all originated from the same single cell, there exist numerous structural relationships among us. For instance, there is only a 1% genetic difference between mice and humans. Although a mouse’s heart weighs approximately 1 gram while a whale’s heart weighs around 1 ton, all mammals exhibit a consistent ratio of four heartbeats per breath. This indicates that inherent, structured relationships exist within vast amounts of biological information.

The second point is the development of hardware, which has advanced rapidly over the past two to three decades. Current Intel chips offer 20,000 times the processing power of the vintage Pentium 286. Earlier hardware architectures evolved from 4-bit, 8-bit, and 16-bit to 32-bit and 128-bit, becoming increasingly complex. Now, as AI integrates into a growing number of specialized applications, hardware designs will shift away from the traditional 64-, 32-, 16-, and 8-bit structures toward lower bit-widths to improve data loading and storage efficiency.

Third, regarding software, we essentially laid the foundation for the latest data-processing software in 2012, including technologies such as convolutional neural networks, deep learning, and big data processing.

These three points are closely related to the development of AI. Why discuss AI? Because AI will play a significant role in the healthcare sector, including areas such as new drug discovery and data analysis. This is the first topic we will address today.

The second aspect involves other technologies that are developing in parallel with AI, such as genomics and proteomics. If the cost of “reading” can be reduced, DNA data storage will also become a highly promising application area.

Many aspects of the genome are not solely related to disease. With the advancement of genomic technologies, capabilities such as genetic testing have become relatively well-established, followed by personalized therapy and drug development. Currently, 97% of drugs are associated with specific targets, while only 3% are target-agnostic.

Why have we discussed so much about AI? What has AI fundamentally rendered obsolete? It is experience. Any product derived from the accumulation of experience is susceptible to being displaced by AI. Therefore, AI will become a powerful tool in drug development. Why are genomics and proteomics singled out? Because they bear significant responsibility.

The application of artificial intelligence and gene technology will bring about a revolution in the experience-driven aspects of clinical medicine, particularly in evidence-based medicine, which has a 3,500-year history. This is its most significant achievement.

Since 2016, the General Office of the State Council has successively issued documents emphasizing the implementation of telemedicine, promoting the establishment of medical consortia, and advancing the sharing of regional medical resources. These documents also stress that medical consortia should actively leverage internet technologies to accelerate the vertical integration of medical resources, foster an orderly tiered diagnosis and treatment system, and promote the development and application of big data. As a top-tier domestic and military medical institution for infectious diseases and liver diseases, the Fifth Medical Center of the Chinese PLA General Hospital (formerly the 302nd Hospital of the Chinese People's Liberation Army) leads a collaborative alliance of approximately 70 to 80 hospitals across China. It bears the responsibility of standardizing clinical diagnosis and treatment in this field, as well as researching, developing, and promoting new technologies. However, it has encountered numerous difficulties during long-term practice:

The first challenge is a shortage of personnel. Primary healthcare institutions consistently have numerous complex cases requiring our joint consultation, and the continuous emergence of new diagnostic and therapeutic concepts and technologies necessitates our efforts in dissemination and training. However, our limited staffing and working hours prevent us from addressing all these demands. Therefore, through collaboration with experts in computer science and internet technology, we have transformed our knowledge and experience into diagnostic and therapeutic robots, thereby facilitating the substantive implementation of medical consortiums.

The second aspect is standardized treatment. Although industry associations release various guidelines and consensus statements annually, these updates are significantly delayed at the primary care physician level, and most practitioners are unable to independently address complex clinical issues. Under such circumstances, the only viable approach to improving the quality of clinical healthcare in China is through information technology. Given that primary care physicians lack the opportunities and time for learning and professional development, an intelligent software system can be employed to resolve these challenges. This was our original intention.

We call this system the "Intelligent Doctor." This project provides physicians with a tool that guides them in delivering standardized care to patients with hepatobiliary tumors and enables the management of complex diseases. As a clinical decision support system (CDSS), it addresses 70% of common clinical scenarios. For the remaining 30% of highly complex cases that cannot be resolved through the system, we have established a remote multidisciplinary team (MDT) consultation channel.

In subsequent developments, we have expanded into clinical research and project-based studies, including new drug research. Through our shared network, we have now begun signing contracts for numerous new drug studies, with more to come in the future. As this platform has just been launched, we will be able to conduct large-scale studies in the future. Meanwhile, we are establishing a database to accumulate case records.

On our platform, physicians remain the ultimate decision-makers. The system merely provides systematic diagnostic and therapeutic recommendations along with supporting evidence (such as clinical guidelines, consensus statements, literature, clinical study reports, and drug package inserts). This empowers physicians to make more confident decisions and recommend treatment plans to patients based on solid evidence.

Leveraging this platform, we can also conduct extensive real-world studies. This year has already seen substantial output. We collect continuous specimens during clinical use by physicians and perform various tests. Ultimately, through the integration of large-scale data, we have developed numerous algorithmic models for disease prognosis prediction.

Many pharmaceutical companies are also discussing collaborations with us. With our software, the management of Phase IV clinical trials for newly launched drugs can fully automate and streamline the work of CROs and CRCs. All information and data can be structured and standardized, addressing the previous issue of incomplete data. These are the goals we aim to achieve in the next two to three years.

"Our experience in working with medical big data over the years has shown that our problem is not a lack of data, but rather a lack of quality, which is the biggest issue."

Through our shared network, we have established several partnerships, with more to come in the future. After six months of implementation, expert reviews across various fields, supported by big data analytics, have provided valuable insights for optimizing our overall framework. To date, we have successfully achieved the current functionalities. We believe this represents a highly effective model.

In 2018, the global pharmaceutical market was valued at approximately $1.25 trillion, with the United States accounting for 40% and China for 11%. As population aging intensifies in China, the growth rate of its pharmaceutical market over the next decade is expected to slightly outpace the global average, projected at 6%–8%.

We believe that between 2015 and 2018, China introduced national policies to support and encourage the development of the pharmaceutical and healthcare industries, steering the sector toward a greater emphasis on R&D and quality, as well as alignment with international standards, thereby promoting industrial growth and enhancing future competitiveness. The enterprises that benefited most during this period were biotechnology companies. These refer to small, R&D-driven pharmaceutical firms specializing in one or multiple specific fields, which achieved significant progress over these years thanks to their inherent capabilities and policy support.

In 2019, the policy landscape continued to encourage innovation, yet it differed from the policies implemented between 2015 and 2018. As previously noted, the 2015–2018 policies were oriented toward supporting innovation and aligning with international standards. However, these measures did not fundamentally shift the sales-driven mindset of generic drug companies in China, where revenue from generic drugs remained their primary focus. The overall policy adjustments in 2019 aimed to steer large pharmaceutical companies specializing in generics toward innovative research, compelling them to pursue innovation as a prerequisite for future development.

Capital flocked into the pharmaceutical and healthcare industry as early as 2012–2013, or even earlier. The first shift in capital dynamics occurred in late 2017; however, due to the strong momentum of China’s innovation-driven policies at the time, investment inertia persisted into 2018, making the capital cooling observed in late 2017 less pronounced. By the fourth quarter of 2018, the decline in market enthusiasm had become evident across multiple indicators, including capital inflows and R&D expenditures in the pharmaceutical sector.

I believe that policy-driven factors are always at play when doing business in China. Riding the tide of national strategy yields twice the result with half the effort. Never before has China supported the development of innovative drugs as strongly as it does now. This is the best era for the development of China’s pharmaceutical industry.

Future innovation and high-end generic drugs will be a key development trend for us. Even major international pharmaceutical companies have accumulated substantial capital through innovation. More importantly, we must closely follow policy developments, monitor regulatory changes, and stay attuned to the current trends and directions set by the state.

For large pharmaceutical companies, the majority of R&D funding is derived from sales revenues. Consequently, they face relatively balanced pressures and enjoy a high degree of autonomy. These large corporations possess abundant clinical resources. However, they also encounter other challenges, such as low efficiency, insufficient investment, continuously rising labor costs, and limited flexibility in pursuing innovation. Therefore, they often leverage CRO platforms to support their R&D activities or strengthen their R&D capabilities through acquisitions and other means.

Innovative R&D companies generally benefit from prime geographic locations, facilitating talent acquisition. Although these enterprises are typically small in scale, they often maintain a portfolio of three to five products at various development stages. Most boast high-caliber leadership and provide robust technical platforms. However, being predominantly in early-stage development, they tend to operate within narrow therapeutic areas, resulting in significant product homogenization and intense competition. Their financing relies heavily on venture capital and other investment forces. Given their strong emphasis on optimizing R&D timelines, these companies preferentially engage integrated-platform CROs to deliver efficient, rapid, and professional end-to-end drug development services.

Future competition in clinical trials will follow a “production based on sales” model, a concept previously absent from the pharmaceutical industry. In the past, drug supplies were scarce, and regulatory authorities received few applications; therefore, both generic drugs and new drugs could be marketed and sold immediately upon approval. However, with numerous approvals now being granted, companies must consider how to accelerate product launches and whether their products will have the opportunity to be included in the National Reimbursement Drug List after launch. Consequently, market considerations must be addressed earlier, particularly in fields such as biopharmaceuticals. The design of animal studies and early-stage models in biopharmaceutical development is highly dependent on the intended indications. If the scope and direction of the indications are uncertain, even Investigational New Drug (IND) application approval may not be secured. From this perspective, a key question arises: How can indications be determined at an early stage?

Stakeholders can draw on established practices from other industrial sectors by adopting analytical and decision-making approaches based on medical data. This has already become commonplace at well-known clinical institutions in Europe and the United States. For instance, in the clinical development of oncology drugs, considerations include how to more precisely screen patients for clinical trials, determine optimal drug combinations, select appropriate dosages, establish the sequence of administration, and define the duration of treatment. These questions can now be addressed in advance through the integration of intelligent technologies with data-driven research.

Since its establishment in 2013, HLT has closely followed industry development trends. Guided by its mission of “Data Intelligence, Green Healthcare,” the company has continuously explored and advanced in technology-driven smart clinical trials, strategically positioning itself in this field. By leveraging advanced technologies and professional services, HLT has collaborated with top-tier medical institutions in China to build a “Medical Data Intelligence Platform,” assisting these institutions in efficiently conducting clinical operations, scientific research, and hospital management.

Furthermore, HLT has accumulated substantial expertise in disease modeling, having collaborated with numerous medical institutions and experts across China to develop standardized datasets for over 40 diseases. At the core of HLT’s technology is the construction of ultra-large-scale medical knowledge graphs based on real-world scenarios, which enables partner medical institutions and experts to handle projects more efficiently.

Through years of accumulation and refinement, and addressing the pain points and challenges in clinical trial services, HLT has launched iClinical Development (hereinafter referred to as “HLT-iCD,” Intelligent Clinical Development Services). This platform is an intelligent, full-cycle service platform for innovative drug development, with its advantages primarily reflected in clinical trial registration and protocol design, clinical operations efficiency, and comprehensive CRO services covering the entire process, including SMO.

In 2018, medical insurance expenditures reached RMB 1.76 trillion, a year-on-year increase of 13%, while revenues amounted to RMB 2.11 trillion, representing an 11% growth. On the surface, medical insurance revenues exceeded expenditures; however, this surplus included RMB 400 billion in fiscal subsidies from the central government. Should these fiscal subsidies fluctuate, further adjustments to medical insurance policies may be implemented to ensure that revenues remain higher than expenditures. Consequently, it is evident that China’s ultimate payer—the medical insurance system—will face significant challenges. Amidst tight revenue and expenditure conditions, pharmaceutical companies have increasingly expanded their portfolios of innovative drugs and out-of-pocket medications. Many manufacturers seek to identify niche markets where their products can achieve robust sales in China without being adversely affected by price reductions resulting from volume-based procurement (VBP) and medical insurance reimbursement negotiations. Additionally, numerous healthcare industry funds have gradually shifted their investment strategies, with approximately 30% of their allocations now directed toward consumer healthcare, aiming to mitigate the impact of national medical insurance policy regulations.

On the other hand, major Chinese pharmaceutical companies are continuously increasing their R&D expenditures. For instance, in 2018, BeiGene had the highest drug R&D investment in China, surpassing Hengrui Medicine. However, the overall pace of pharmaceutical R&D has not accelerated, and there have been no significant breakthroughs in new drug development; progress remains challenging. Globally, the return on investment (ROI) for pharmaceutical R&D is generally declining. This trend is driving large global pharmaceutical companies to shift from in-house product development to licensing transactions. In this context, China’s pharmaceutical R&D market may become a key engine for future licensing deals. Consequently, we are seeing an increasing number of pharmaceutical companies and healthcare funds engaging in licensing and new drug development, including the aforementioned BeiGene and Zai Lab.

One of Yanzhi’s shareholders is among China’s largest CMO companies, with extensive collaborative partnerships. We currently offer several data-driven platforms and tools, primarily designed to help CROs enhance the digitalization of pharmaceuticals and healthcare. Additionally, we facilitate licensing-in and licensing-out collaborations for pharmaceutical companies.

Additionally, we have established a presence in several regions, specifically Southeast Asia and South America. Our partners and teams in Southeast Asia are facilitating the export of China’s new drug systems to less developed countries. Beyond the European and U.S. markets, these less developed regions offer substantial market potential. In terms of overall licensing transactions, we have access to extensive channels and diverse models of collaboration.

We typically conduct real-world studies by collecting real-world data, performing statistical analysis and data mining, and ultimately generating real-world evidence to support the academic and market value of our pharmaceutical products.

Three representative cases correspond to three key research objectives: drug safety, efficacy, and pharmacoeconomics.

Conducting real-world studies aims to demonstrate the safety of drugs in real-life settings, such as in patients with multiple comorbidities and concomitant medications, identify which patient populations derive greater benefit, or determine which groups may be at risk for specific harms. Additionally, these studies encompass pharmacoeconomic research, providing data support for health insurance negotiations, Diagnosis-Related Groups (DRGs), and other activities related to pharmacoeconomics.

In summary, conducting real-world studies offers pharmaceutical companies value in two main areas: academic evidence and commercial value.

Our real-world studies face challenges in the following six aspects:

First, changes in data volume;

Changes in the quality of secondary data;

Third is the change in data channels;

Fourth is the change in data modalities;

5. Data observation: time variation;

Changes in the Sixth Data Dimension.

To address the collection of these six types of real-world data, we need to leverage new tools of the new era, such as big data processing, artificial intelligence, and blockchain, to help us efficiently conduct large-sample real-world studies.

When artificial intelligence is integrated with large-scale real-world studies, it primarily enhances efficiency, quality control, and data analysis. Furthermore, it holds value in supporting clinical trials through applications such as medical image screening and drug molecule-based prediction.

First, efficiency. Collecting data through registered RCT studies may be difficult to implement in large-sample studies, both in terms of cost and efficiency itself. In the Yaoling system, there are not only more sources for data collection, but also efficient tools that ensure various modalities of data, such as medical images, photos, text, voice, etc., can be automatically captured into the EDC, significantly reducing manual work.

If efficiency is sufficiently high, another critical aspect is quality control—can we ensure that quality remains equivalent or even improves after integrating machine-based processes? First, we do not rely entirely on machines; instead, we adopt a human-machine collaborative workflow. Our final quality assurance still adheres to Good Clinical Practice (GCP) requirements, with human personnel signing off and performing the final review step, thereby achieving highly efficient operations. Furthermore, beyond passive monitoring and review, particularly when dealing with very large sample sizes, we employ an active early-warning Risk-Based Monitoring (RBM) system. This system integrates data from data management systems, operational systems, and management systems, breaking down data silos. Through algorithmic analysis, it establishes an RBM framework tailored for Real-World Studies (RWS), enabling proactive risk prediction in our research and reducing the likelihood of trial failure.

The third direction is big data analytics. After acquiring large volumes of data, we not only perform statistical analysis using traditional methods but also leverage classic data mining algorithms, such as clustering and outlier analysis, to explore unknown trends and patterns within the data.

Finally, Yaoling is also exploring applications in several other areas. The first involves the use of medical imaging (CT, MRI) and physiological signals (ECG, EEG) for patient screening. The second employs Graph Neural Networks (GNNs) to predict adverse events. The third is Robotic Process Automation (RPA). The fourth focuses on model interpretability.

During the roundtable session of the morning forum,Chen Penghui, Partner at Boyuan CapitalAs the moderator, I engaged in a discussion with four panelists on the challenges and opportunities facing China’s innovative drug R&D amid its rapid development. Each panelist shared their insights from the perspective of their respective fields.

Li Shichen, Director of Product Operations at Han’s Union, first addressed investment trends in the CRO industry. The so-called “capital winter” has persisted intermittently for some time, extending beyond just the current year. Nevertheless, investment in the innovative drug sector remains relatively active. Furthermore, regarding policy support for stem cell innovation, the regulatory landscape in China was initially unclear and ambiguous. In recent years, however, comprehensive guidelines have been issued, ranging from macro-level policies to micro-level details. This has led to substantial progress and breakthroughs in the clinical translation and application of stem cells, as well as in new drug development this year. Overall, given the convergence of favorable factors—including clarified policies, an abundance of talent, and improving capital sentiment—the market opportunities and future potential in cell therapies, particularly in the stem cell field, remain significant following the post-bonus period and the gradual easing of policy restrictions. Capital markets also hold a highly positive outlook on this sector.

Kang Xiaoqiang, founder of Weilizhibo, believes that the current climate is less a “capital winter” and more a gradual process of rationalization. The lack of sustainability in investment models in recent years is, in the long run, a positive development. Particularly with the crowded PD-1 space, other immunotherapies have struggled to match the efficacy of PD-1 and PD-L1 inhibitors, prompting industry players to seek the next breakthrough in tumor immunology. CD47 has shown some efficacy in lymphomas and hematologic malignancies, but no significant benefits have yet been observed in solid tumors. In his view, the next stage of development will likely focus on combination therapies and bispecific antibodies, building further upon the foundation of PD-1 inhibition.

Liu Jing, Deputy Medical Director at Nuosige Medicine, noted that in pharmaceutical R&D—particularly in early-stage development and quantitative pharmacology—Nuosige’s consulting services have been playing an increasingly important role among its collaborative partners in recent years. By engaging from the preclinical drug development phase and providing specialized guidance, Nuosige offers substantial support for later clinical stages, helping pharmaceutical companies achieve more accurate strategic positioning. Therefore, she believes that the future trend will see a growing emphasis on trial design and development pathway planning among all innovative new-drug enterprises.

Tang Li, Vice Chairman and Chief Technology Officer of Huahao Zhongtian Biopharma, believes that the capital winter the company experienced in 2010 was likely harsher than the current downturn. At that time, investors were scarce, and securing financing was extremely difficult. Reflecting on the journey thus far, she considers the earlier period to have been more challenging from a capital perspective. Furthermore, while hot topics in the innovative drug sector currently include small-molecule targeted therapies, large-molecule antibody drugs, and cell therapies, the field of small-molecule chemotherapy agents, where the company operates, remains in a prolonged winter.

During the afternoon roundtable forum, Liu Zongyu, Executive Dean of VCBeat Research Institute, joined three corporate representatives to discuss the application scenarios of artificial intelligence and information technology in new drug development, as well as the challenges currently being faced.

Hu Qitong, CTO of Yaoling Medical Technology, stated that while the volume of clinical data is immense, it largely lacks effective annotation, posing a significant challenge for general AI companies. However, for Yaoling, its clinical research business is inherently a process of extracting relevant clinical information for analysis, which itself constitutes a data annotation and curation process initiated and funded by sponsors. Secondly, when encountering an entirely new research domain, the question arises as to how to rapidly apply past "experience." While this is effortless for humans, for machines, it primarily involves combining transfer learning with knowledge graph reasoning. Third, and most critically, is the role of human involvement. Once algorithms reach a certain level of accuracy, the resources and capital required for further improvements increase exponentially. In the vast majority of cases, as a company, we consider the return on investment for actual projects, adopting a human-machine collaborative approach to ensure that artificial intelligence effectively augments human work.

Lai Lipeng, co-founder of XtalPi, believes that when evaluating the impact of new technologies on drug development, it is essential to balance efficiency and cost. From a cost perspective, while AI methods can reduce expenses in early-stage novel drug screening, we also emphasize achieving superior results at costs comparable to those of traditional computational methods. Drug development expenditures increase progressively as the R&D process advances. By leveraging advanced computational or AI-driven approaches, multiple downstream targets—such as activity, metabolism, toxicity, and side effects—can be evaluated at the earliest possible stages. Through such comprehensive assessments, AI methods can help partners mitigate the risk of late-stage failures. Furthermore, AI enables the provision of multiple series of candidate compounds at an early stage, offering partners greater flexibility in decision-making. This ensures that, during later-stage advancement, the integration of AI with computational chemistry not only reduces the risk of failure but also provides more high-quality options for informed decision-making.

Feng Dongzhi, Operations Director at Yudao Bio, pointed out that from a global perspective, an entire ecosystem for new drugs—spanning discovery, R&D, clinical trials, and market launch—has been established worldwide. Companies need to focus on how to better integrate within this ecosystem. Bringing a new drug to market is a journey of more than ten years; not every company or team stays involved from scratch all the way to commercialization. Instead, participants engage in a relay race, with Yudao Bio being one of them. Some companies specialize in marketing, while others focus on areas where they have the highest efficiency. Overall, new drug development increasingly requires collaboration among enterprises across all stages of the value chain.

Concurrently with the Innovative Drug Forum, VCBeat’s VBInsight released the China Rare Disease Industry Research Report, co-produced with Aimeda, as well as its self-produced 2019 Research Report on the Development of the Innovative Drug Sector. Both reports leverage data to provide an in-depth analysis of the current state of industry development from multiple dimensions—including policy, market, products, and key subsectors—and offer forecasts on the future direction of the industry.

China Rare Disease Industry Research Report

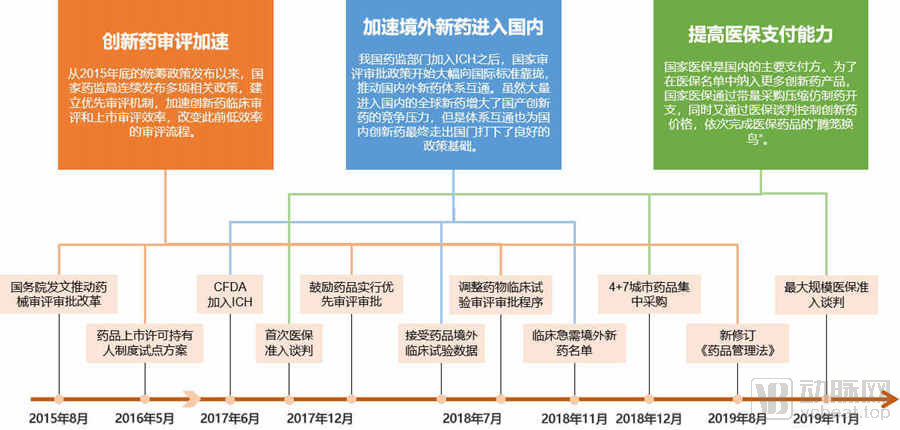

Since 2015, the Chinese government has issued a series of policies and regulations to deepen reforms in the pharmaceutical industry, covering clinical trial data verification, consistency evaluation, review and approval reform, priority review and approval, the CFDA’s (now NMPA) accession to the ICH, adjustments to and negotiations for the National Reimbursement Drug List, and the pilot “4+7” volume-based procurement program along with its nationwide expansion. These reform measures have been closely interconnected and implemented with unprecedented intensity, dispelling the darkest clouds over the pharmaceutical sector. As a result, there has been a surge in clinical development and marketing applications for innovative drugs since 2015, including in the long-neglected field of rare disease treatments.

For overseas companies, drugs already marketed abroad can rapidly enter the Chinese market through pathways such as “clinically urgent need” and “priority review.” According to statistics from the Drug Clinical Trial Registration and Information Publicity Platform, only 13 rare disease drug varieties were involved in international multi-center clinical trials conducted by overseas companies in China between 2014 and 2017. With China vigorously promoting the development of rare disease therapeutics, for drugs not yet marketed abroad, it is a preferred strategy for overseas companies to conduct multi-center clinical trials in China to accumulate clinical data from Chinese patients.

For domestic enterprises, the development of innovative drugs for rare diseases in China is still in its early stages. Communication with regulatory authorities during the development process, particularly in the early research and development phase, is essential. If significant technical issues arise, timely communication between the enterprise and the Center for Drug Evaluation (CDE) will, to a certain extent, improve the quality and efficiency of corporate decision-making and reduce decision-making risks.

The National Healthcare Security Administration is working to reduce the financial burden of medications for rare diseases through health insurance negotiations and volume-based procurement.

On July 18, 2019, the Management Committee of the Rare Disease Prevention and Control Development Special Fund under the China Health Promotion Foundation was established in Beijing. As a public welfare fund dedicated to supporting the prevention and control of rare diseases in China, the special fund is committed to promoting a series of related public welfare activities, including rare disease screening, diagnosis, treatment, education, academic exchanges, and orphan drug research and development.

Corporate and private charitable donations can help alleviate the medication cost burden for patients with rare diseases to a certain extent.

VCBeat believes that the only sustainable solution is to commercialize orphan drugs, leveraging profit incentives to encourage companies to strengthen R&D in this area and bring more medications to market, thereby addressing cost issues from a business perspective. In alleviating the financial burden on patients, efforts should not rely solely on the government and pharmaceutical companies; commercial insurance must also play its due role. Currently, commercial medical insurance, critical illness insurance, and accident insurance products are highly mature in the market, yet few insurance products cover medical expenses for rare diseases. It is understood that there is currently only one consumer-type critical illness insurance product in the market that includes coverage for specified rare disease medical expenses. Although insurance products targeting rare disease medical costs are scarce, they still offer a viable model for market-based operations. Furthermore, companies developing and launching orphan drugs could collaborate with insurance providers to explore diverse models, thereby reducing launch risks for enterprises and lowering the medication burden for patients.

Certainly, when designing rare disease insurance products, insurers cannot do without essential baseline data—such as epidemiology, patient population size, and market potential—all of which need to be collected with the aid of internet-based tools. Insurance companies are poised to play an even more significant role in the field of rare disease treatment.

The above is an excerpt from the report. Please scan the following mini-program code to access the full report.

2019 Research Report on the Development of Innovative Drugs

Development Characteristics of the Innovative Drug Sector

Policy Support for Innovative Drugs in China

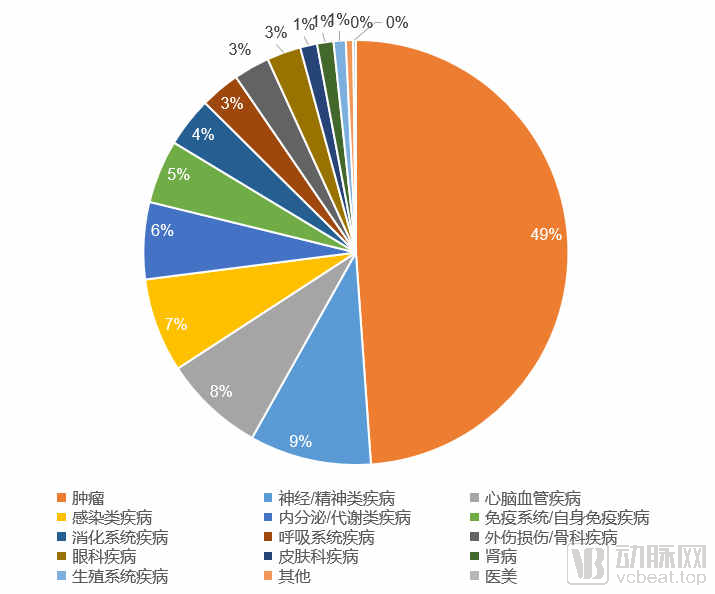

In May 2019, VCBeat cleaned and analyzed all active, industry-funded clinical studies listed on ClinicalTrials.gov.

According to our statistics, oncology-related clinical trials account for nearly half of all clinical trials conducted globally.

Another five disease categories each accounted for more than 5%, namely neurological/psychiatric disorders, cardiovascular and cerebrovascular diseases, infectious diseases, endocrine/metabolic disorders, and immune/autoimmune diseases.

The above is an excerpt from the report. Please scan the following mini-program code to access the full report.