Impact of the National Rollout of Volume-Based Drug Procurement from the '4+7' Pilot Cities on China's Pharmaceutical Industry

On September 1, 2019, the Shanghai Pharmaceutical Centralized Procurement Platform, known as the “Shanghai Sunshine Pharmaceutical Procurement Network,” released the *Document on Centralized Drug Procurement in Alliance Regions* (hereinafter referred to as the “Procurement Document”), issuing invitations for centralized drug procurement to pharmaceutical companies in regions outside the initial “4+7” pilot cities. On September 30, 2019, nine departments, including the National Healthcare Security Administration, issued the *Implementation Opinions on Expanding the Pilot Program of State-Organized Centralized Drug Procurement and Use* (hereinafter referred to as the “Implementation Opinions”), which provided overarching guidance for promoting centralized drug procurement nationwide. The initiative aimed to address the significant price disparities observed between the “4+7” pilot cities and non-pilot regions, thereby enabling eligible medical institutions across China to access high-quality, affordable pilot drugs. Marked by these two documents, the framework for nationwide volume-based drug procurement reform has been fundamentally established.

Following the implementation of the “Implementation Opinions” and the “Procurement Documents,” localities across China began to successively roll out their own detailed rules for volume-based drug procurement. These included the “Shandong Province Implementation Plan for Expanding the Pilot Program on National Centralized Drug Procurement and Use,” the 2019 “Gansu Province Implementation Plan for Implementing National Centralized Volume-Based Drug Procurement and Use,” and the “Zhejiang Province Implementation Plan for Expanding the Geographic Scope of the Pilot Program on National Centralized Drug Procurement and Use.” For the pharmaceutical manufacturing and distribution industry, although there had been years of advance signaling and psychological preparation, the nationwide formal implementation of volume-based drug procurement still delivered a significant shock to the entire sector. This article analyzes the impact of this reform initiative on pharmaceutical companies.

I. The Profound Connotations of the Volume-Based Procurement Reform for Pharmaceuticals

Centralized drug procurement has a long history. It refers to a purchasing method in which multiple medical institutions conduct centralized tendering and procurement, either voluntarily or under government leadership, to acquire necessary pharmaceuticals through a bidding process. Volume-based drug procurement is an upgraded version of centralized drug procurement. In this model, both the winning bid price and the purchase volume are taken into account during the implementation of centralized procurement. The purchase volume is explicitly specified during tendering or negotiated pricing, and pharmaceutical companies submit quotes based on the specific quantities required. This approach enables a more scientific exchange of volume for price, thereby reducing drug procurement costs. Price reduction is the primary objective of volume-based drug procurement.

The Beijing Volume-Based Procurement Platform previously released the document “Q&A with Reporters on the Pilot Program for National Centralized Drug Procurement.” In response to the question of why China launched the pilot program for centralized drug procurement, the head of the Pilot Program Office stated that it aimed to address the high cost of medical care for the public, enabling people to access higher-quality medicines at more affordable prices.

High drug prices have long been a persistent ailment in China’s healthcare industry. In particular, Chinese generic drug manufacturers have long enjoyed abnormally high profits. Unlike in other countries, where the expiration of originator drug patents typically triggers a “patent cliff” with sharp declines in sales and profits, this phenomenon has been notably absent in China. This has contributed to the backwardness of China’s pharmaceutical industry. The Chinese market sustains more than 7,000 pharmaceutical manufacturing enterprises, with approval documents for many drugs held by hundreds of companies capable of producing the same product, resulting in substantial social waste.

Against the backdrop of the rapidly increasing proportion of the elderly population in China, failure to control drug prices—particularly those of high-volume generic drugs—will inevitably lead to a substantial payment deficit in the medical insurance fund in the long run. Therefore, implementing volume-based drug procurement to eliminate inflated prices in the sales chain is an inevitable choice. This approach not only addresses the burden of high medical costs for the public but also reduces expenditures from the medical insurance fund, thereby achieving effective cost containment.

Since 2018, China has piloted volume-based drug procurement in four municipalities directly under the Central Government (Beijing, Shanghai, Tianjin, and Chongqing) and seven sub-provincial cities (Shenyang, Dalian, Xiamen, Guangzhou, Shenzhen, Chengdu, and Xi’an). These pilot cities are collectively referred to within the industry as the “4+7 Pilot Cities.” Following the conclusion of the pilot phase, and building on the implementation of centralized procurement results in the “4+7” pilot cities and provinces that had already adopted the policy, the national government organized relevant regions into alliances to conduct cross-regional alliance-based volume-based drug procurement in accordance with laws and regulations. These alliance regions specifically include 25 provincial-level administrative divisions: Shanxi, Inner Mongolia, Liaoning, Jilin, Heilongjiang, Jiangsu, Zhejiang, Anhui, Jiangxi, Shandong, Henan, Hubei, Hunan, Guangdong, Guangxi, Hainan, Sichuan, Guizhou, Yunnan, Tibet, Shaanxi, Gansu, Qinghai, Ningxia, and Xinjiang (including the Xinjiang Production and Construction Corps), excluding the “4+7” pilot cities located within these areas. As Hebei Province and Fujian Province had already proactively implemented volume-based procurement in earlier stages, they were not included in this procurement alliance. At this point, volume-based drug procurement has effectively expanded to all provinces and municipalities across China, excluding the Hong Kong, Macao, and Taiwan regions.

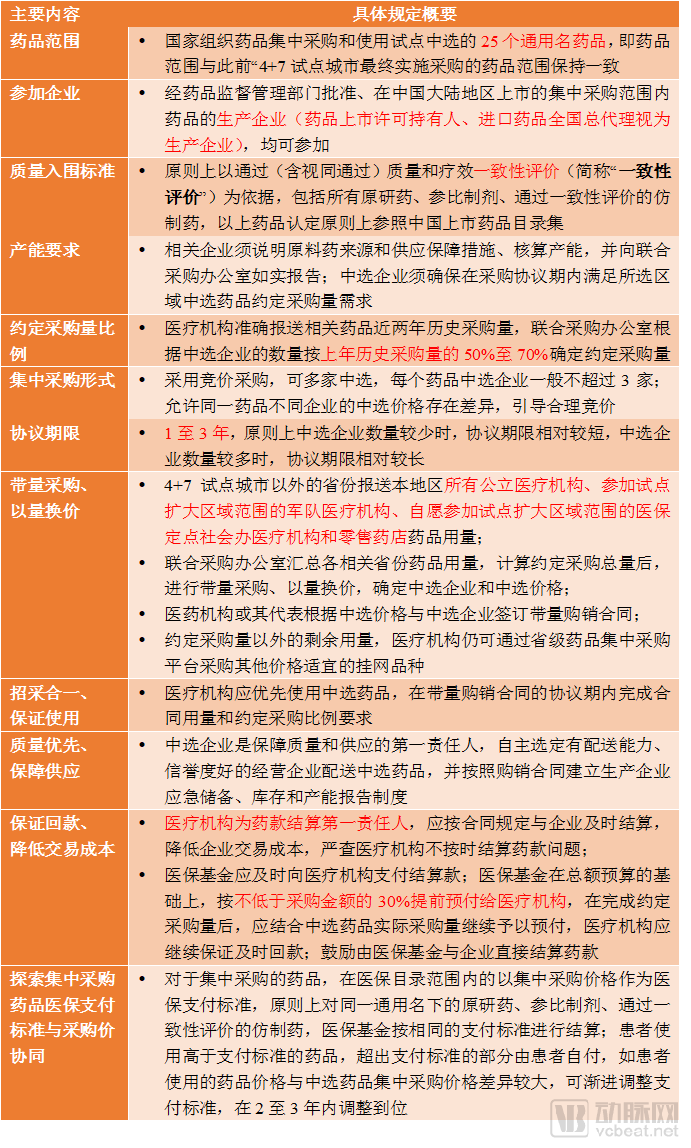

II. Main Contents of the "Implementation Opinions"

The “Implementation Opinions” require the nationwide promotion of the pilot model of centralized volume-based procurement for drug centralized procurement and use. The main contents are as follows:

In addition to the aforementioned provisions, to ensure that medical institutions fulfill their procurement obligations as stipulated in the centralized volume-based procurement agreements, the "Implementation Opinions" also impose requirements on medical institutions and healthcare professionals. It mandates the establishment of an incentive and risk-sharing mechanism between medical insurance handling agencies and medical institutions, characterized by "retention of savings and reasonable sharing of excess expenditures." For medical institutions that reduce medical insurance fund expenditures through the standardized use of selected medicines, their total annual medical insurance budget allocations shall not be reduced. Furthermore, if public medical institutions generate surpluses from their medical service revenues and expenditures, such funds may be pooled and used for personnel compensation in accordance with the "Two Permissibles" policy. The Implementation Opinions also require that the utilization of selected medicines be incorporated into the performance evaluations of both medical institutions and healthcare professionals.

III. The Profound Impact of Volume-Based Drug Procurement on Pharmaceutical Companies

Following the implementation of volume-based drug procurement in China, the country’s vast number of pharmaceutical enterprises face a stark choice: whether to participate in the bidding process for volume-based drug procurement.

Let us first examine the benefits of participating in the tendering process. To encourage greater participation from pharmaceutical companies, the "Implementation Opinions" incorporate more human-centered design elements in the following aspects:

(1) Increase the number of winning bidders for each individual drug item, allowing the benefits of centralized procurement to reach more pharmaceutical companies

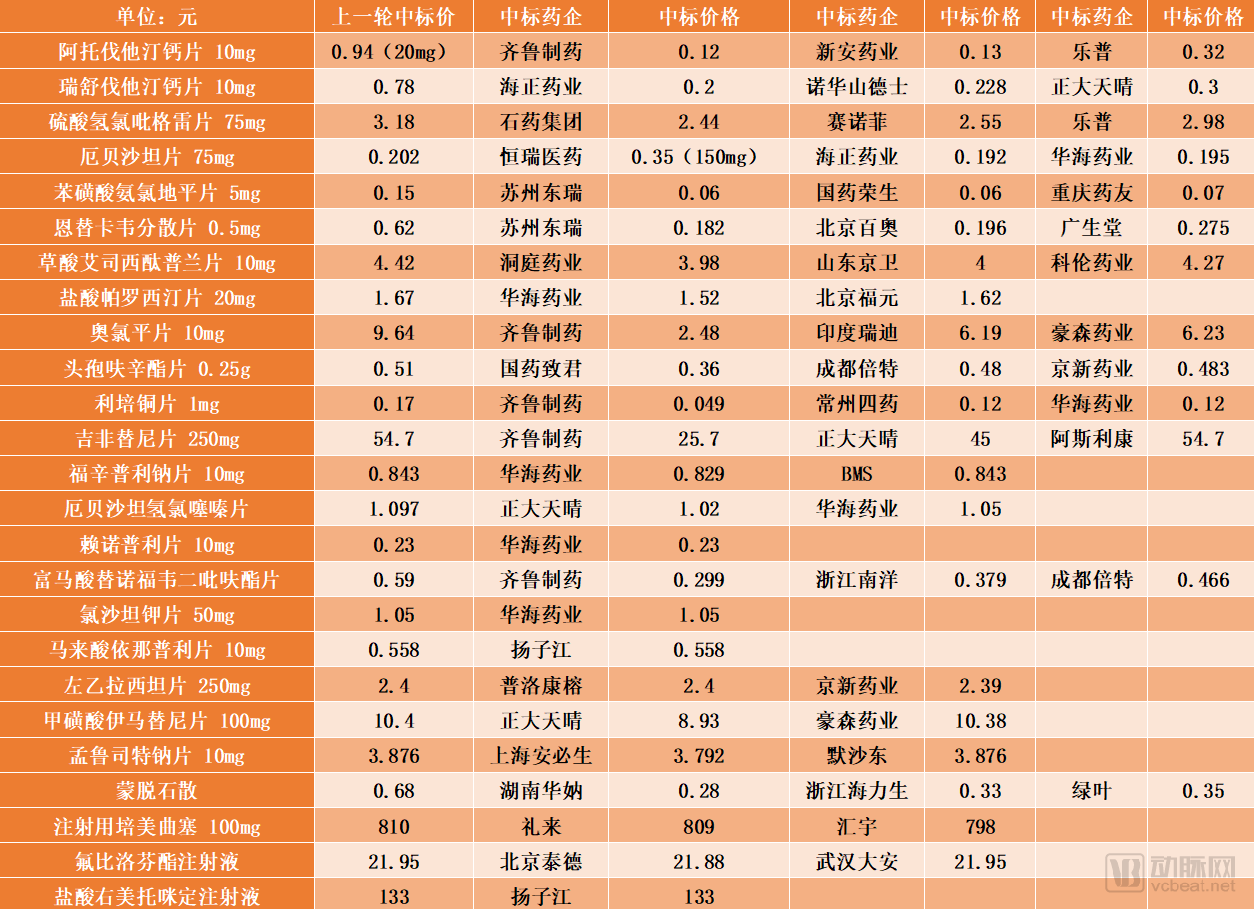

During the pilot volume-based procurement of pharmaceuticals in the "4+7" pilot cities, only one winning bidder was selected for each drug product. However, the Implementation Opinions revised this to allow generally no more than three winning bidders per drug. The Procurement Documents accordingly specified the agreed procurement volume and market share based on the number of winning bidders. Specifically, if there is only one winning bidder, the agreed procurement volume for the first year shall be 50% of the calculation base for the first year’s agreed procurement volume; if there are two winning bidders, it shall be 60%; and if there are three winning bidders, it shall be 70%. The agreed procurement volume for the second year shall be calculated based on the actual procurement volume of that drug in the first year, using similar proportions.

When multiple pharmaceutical companies win bids for the same drug variety, it avoids the problem of insufficient supply security that may arise when a single company wins the bid. This is particularly relevant in the current volume-based procurement program, where the reported drug usage volume from each province covers not only public medical institutions within the region but also military medical institutions participating in the expanded pilot areas, as well as designated social private medical institutions and retail pharmacies that have voluntarily joined the expanded pilot regions. With an increased base for calculating drug usage volumes, allowing multiple winners helps alleviate the pressure associated with exclusive supply arrangements. On another note, we understand that increasing the number of winning bidders enables more pharmaceutical companies to benefit from the procurement outcomes. Especially considering that over 100 pharmaceutical companies are already listed on China’s A-share capital market, if a company's key product fails to win the bid, its stock price often drops significantly the next day. To prevent a sharp decline in the valuation center of listed pharmaceutical companies, having two to three companies win the bid represents a relatively ideal solution.

Summary Table of Winning Bids for 25 Volume-Based Procurement Drugs:

Based on the above results, only four products were exclusively awarded to a single bidder, eight products were awarded to two companies each, and the remaining 13 products were awarded to three companies each.

(2) Emphasize the speed of procurement payment after winning the bid, requiring direct settlement by medical insurance or large prepayments.

Following the implementation of volume-based procurement (VBP) for pharmaceuticals, profit margins for winning bids have plummeted sharply. In some cases, the bid-winning prices have dropped by as much as 95% compared to pre-VBP levels. Although pharmaceutical companies can reduce sales costs for these products through measures such as downsizing their sales teams, the overall profit margin for VBP-winning drugs remains extremely thin. Under this widespread low-gross-margin environment, delayed settlement of procurement payments for supplied drugs—regardless of whether the paying entity is the medical insurance fund or healthcare institutions—could drive a number of VBP-winning pharmaceutical companies into insolvency.

According to the “Q&A with Reporters on Expanding the Geographic Scope of the National Centralized Drug Procurement Pilot” issued by the National Healthcare Security Administration on September 25 this year, since the implementation of volume-based drug procurement in the “4+7” pilot cities on April 1 this year, the procurement volume of the 25 selected drugs accounted for 78% of the total procurement volume of drugs with the same generic names as of the end of August this year, and the 30-day payment rate for the 25 selected varieties reached 97%.

Therefore, how to further accelerate the payment collection process for procurement has become a key factor in implementing volume-based drug procurement. Currently, two models have emerged: the Shanghai Model and the Beijing Model.

1. The Shanghai Model: Direct Settlement Between Medical Insurance and Pharmaceutical Companies

According to the “Tripartite Agreement on Purchase and Sale of Selected Varieties in Centralized Drug Procurement” attached to the “Supplementary Document for Shanghai Region of the ‘4+7’ City Centralized Drug Procurement” issued by the Shanghai Pharmaceutical Centralized Bidding and Procurement Affairs Management Office (hereinafter referred to as the “Shanghai Undertaking Agency”), the payment for selected drugs in the Shanghai region shall be advanced by the Shanghai Undertaking Agency to drug distribution enterprises in installments (50% of the total payment shall be made to the distribution enterprise within 5 days after the signing of the tripartite agreement; 45% shall be paid upon six months of implementation or when 50% of the procurement volume is reached; and 5% shall be retained for final settlement). Medical institutions shall pay the distribution enterprises for the selected drugs purchased from the 1st to the last day of the previous month by the 15th of each month. After the medical institutions confirm the invoices for the centrally procured selected drugs, the distribution enterprises shall remit the confirmed invoice amounts to the Shanghai Undertaking Agency by the 10th of each month to complete the repayment. Settlement between drug manufacturers and drug distribution enterprises shall be determined by mutual agreement.

In the Shanghai region, the aforementioned settlement method is essentially an exploration of direct medical insurance settlement. After the tripartite agreement on purchase and sales is signed, the Shanghai handling agency will advance funds directly to the distribution enterprises, while simultaneously supervising and monitoring healthcare institutions to ensure timely repayment, thereby guaranteeing that pharmaceutical companies receive their payments promptly.

2. The Beijing Model: After the medical insurance fund makes advance payments to healthcare institutions, these institutions settle accounts with pharmaceutical companies.

In accordance with the “Implementation Plan for Beijing’s Execution of the National Pilot Program on Centralized Drug Procurement and Use,” jointly issued by the Beijing Municipal Healthcare Security Administration and other relevant departments, healthcare institutions in Beijing are required to receive an advance payment from the medical insurance fund equivalent to 50% of the contractually agreed procurement amount. These institutions are also supervised to ensure timely payment for pharmaceuticals. Under this payment model, the medical insurance fund does not settle payments directly with pharmaceutical manufacturers or distributors; instead, it provides advance payments directly to healthcare institutions, thereby ensuring that they have sufficient funds to make timely payments for drug purchases.

Following the nationwide expansion of volume-based drug procurement, on October 24, 2019, the People’s Government of Shandong Province issued the Implementation Plan for Shandong Province to Carry Out the Expansion of the National Pilot Program for Centralized Drug Procurement and Use. According to this document, Shandong Province will adopt a payment settlement model similar to that of Beijing, whereby the medical insurance fund will prepay medical institutions an amount no less than 50% of the contracted procurement value for selected drugs; medical institutions are prohibited from delaying payments for pharmaceuticals.

Clearly, the Shanghai model is superior. Under this model, pharmaceutical companies receive payment upfront before supplying drugs, completely eliminating the risk of delayed payments for drug procurement. In contrast, under the Beijing model, while the repayment security for the first 50% of drug procurement costs is very high, there remains a possibility of minor payment delays by medical institutions for the remaining 50%.

Based on the actual outcomes of the current volume-based procurement (VBP) bidding process, nearly 100 pharmaceutical companies actively participated in the bidding. On September 24, 2019, the results of the national second round of VBP expansion bidding were announced. Although the average winning bid prices were lower than previously expected by the market, the capital market still responded: the stock prices of pharmaceutical companies with favorable winning bid outcomes rose or remained stable, while those of companies that failed to win bids dropped sharply.

On the other hand, international generic drug giants have accelerated their entry into the Chinese market. In July 2019, pharmaceutical giant Pfizer reached an agreement with global generic drug leader Mylan to merge Pfizer’s off-patent medicine division, Upjohn, with Mylan, thereby jointly establishing a new pharmaceutical company—Viatris. Also in that month, GlaxoSmithKline (GSK) transferred its Suzhou manufacturing facility and Lamivudine (brand name Heptodin), whose patent had expired, to Fosun Pharma. This move was widely regarded within the industry as GSK’s decision to divest Heptodin and refocus on the research and development of other innovative drugs. Meanwhile, Indian generic drug giant Cipla established a limited liability company in the Shanghai Free Trade Zone in May 2019 and set up a joint venture with Chuangnuo Pharmaceutical in Jiangxi Province.

Under pressure from both internal and external factors, the operating environment for China’s extensive generic drug manufacturers will become increasingly challenging; passing the consistency evaluation does not guarantee their security. For individual drug products, those included in the national volume-based procurement (VBP) program account for approximately 50–70% of the total market share in China (the remaining 30–50% is still procured independently by medical institutions; if purchases by non-medical-insurance-paying entities such as private hospitals are taken into account, this market share would be lower). However, the 25 drugs subject to VBP represent only a very small fraction of the vast number of marketed pharmaceutical products with marketing authorization in China. Even if a pharmaceutical company fails to win a bid, it will not face immediate catastrophe and will retain some room for survival in the short term. In the long run, however, it will inevitably be drawn into an unfavorable competitive landscape. This is particularly critical for companies whose flagship products are included in the centralized procurement list, where winning or losing the bid could determine their very survival.

Given that the scope of China’s volume-based procurement (VBP) for pharmaceuticals is bound to expand significantly beyond the current 25 drugs, and the market share of VBP-listed drugs within China’s total pharmaceutical market is poised to rise year by year, the country’s vast generic drug manufacturers will inevitably undergo intense consolidation to adapt to these market shifts.

Volume-based procurement will deeply promote internal consolidation within the generic drug industry. The generic drug market will become further concentrated in the future, with major products dominated by large pharmaceutical companies that possess high-level production capabilities and low-cost advantages. In the long run, numerous low-end generic drug manufacturers will either pivot to developing original innovative drugs with high profit margins and stable prices, move closer to large pharmaceutical enterprises through mergers and acquisitions to seek collective strength, or be ruthlessly eliminated by the market.

Author: Anjie Health Team

Contact WeChat ID: zjqc111111

Since 2016, the Healthcare and Life Sciences legal services team at AnJie’s Shanghai office has been actively involved in providing legal counsel for a wide range of healthcare-related projects. The team has assisted clients in acquiring a municipal centralized drug procurement platform and was invited to deliver a professional lecture themed “Antitrust Analysis of the ‘4+7’ Volume-Based Procurement Program.” With long-standing attention to regulatory and policy developments in this sector, we have prepared this article to share the latest updates with the broader community. We welcome further discussions with all interested parties on any detailed aspects.

Cai Hang: With over a decade of focus on investment and financing services in the healthcare, TMT, and artificial intelligence sectors, he has exerted significant influence in the field of venture capital legal services in China. Listed among “China’s 100 Legal Elite” by The Business Lawyer magazine, he is regarded as one of China’s most outstanding commercial lawyers. He has also been repeatedly recommended by leading legal ranking agencies such as Legal 500 and Legalband in the fields of TMT and venture capital. In addition to venture capital practice, he is highly proficient in mergers and acquisitions and capital markets. Mr. Cai serves as the Managing Partner of AnJie Law Firm’s Shanghai office.

Huang Yi: Primarily engaged in private equity investment and financing, mergers and acquisitions, restructuring, and compliance matters. She has provided advisory services to numerous renowned investment institutions for domestic and cross-border private equity investments, and offered professional support for corporate restructuring transactions. Her experience spans industries including healthcare, artificial intelligence, new retail, and education.