Fu Shinong of Sinovision: The Medical Device Market Is Entering a New Golden Era

SinoVision

Developer and Manufacturer of High-End Medical Imaging Equipment

Where Is the Next Breakthrough in Medical Devices? The Fragmented Market Landscape Is Gradually Becoming Clearer. A Cohort of Domestic Tech Companies, Specializing in Specific Scenarios, Has Emerged as Standouts and Is Flourishing Amid the Backdrop of Import Substitution.

Sinovision, a leading domestic manufacturer, has carved out a significant niche in China’s CT industry. This medical device company, dedicated to the research and development of CT imaging equipment, centers its technological strategy on differentiation, specialization, intelligence, and network connectivity.

Since its establishment in 2012, Sinovision has been dedicated to CT imaging equipment, continuously exploring the clinical value of CT imaging. To date, Sinovision has built three major business lines: a series of 16- to 128-slice large-bore CT scanners, a medical robotics series, and an intelligent imaging solutions series. Its business scope has expanded from radiology departments to interventional radiology, neurology, oncology, and other specialties. Furthermore, Sinovision’s integrated R&D approach, combining hardware (“equipment”) with software (“imaging cloud”), is driving imaging services beyond hospital walls, providing affordable, high-quality medical imaging services to a broader population.

At the tail end of 2019, VCBeat had the honor of inviting Mr. Fu Shinong, founder of Sinovision Technology (Beijing) Co., Ltd., to the VB100 Conference. During the event, Mr. Fu delivered a presentation titled “Domestic Large-Scale Medical Equipment in Revitalization: A Perspective from Medical Imaging.” His insights offer a glimpse into the future development of medical imaging devices.

Fu Shinong Interviewed by Reporters at the VB100 Conference

As a seasoned medical imaging professional, Fu Shinong has personally witnessed the development of China’s large-scale medical equipment industry over the past two decades. In the early 1990s, annual sales of CT imaging equipment in China stood at only around 200 units; this year, that figure has surpassed 4,000 units, representing more than a 20-fold increase.

Has this trend stalled today? On the contrary, from the perspective of the overall healthcare landscape, medical devices remain as vibrant as the rising sun.

The development direction of the industry can be discerned from a set of data. Globally, the sales volume of medical devices reached $451.9 billion in 2019, with an average annual growth rate of 5.1% over the past five years, and is expected to exceed $500 billion by 2024.

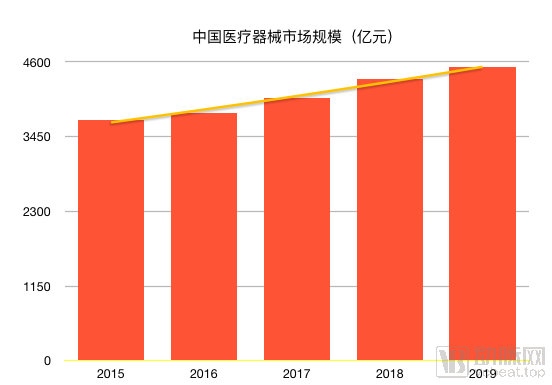

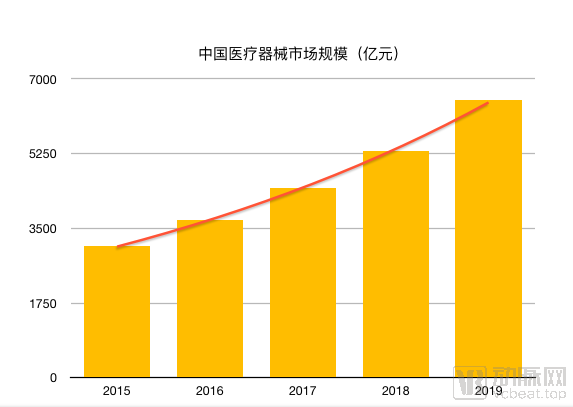

The Chinese market is even more dynamic. In 2015, the size of China's medical device market was RMB 308 billion; four years later, it reached RMB 650 billion, doubling in scale. The annual growth rate in 2019 alone reached 22.5%.

Behind the enormous market potential lies China’s relatively low penetration rate of large-scale medical devices and its low pharmaceutical-to-medical-device ratio. Statistical data from 2018 show that the total installed base of CT scanners in China was approximately 30,000 units, equivalent to 16.8 units per million people. In contrast, developed countries with more robust medical equipment infrastructure have significantly higher figures: Japan has 92.6 CT scanners per million people, and the United States has 32.2 per million. Regarding the pharmaceutical-to-medical-device ratio, China’s current ratio stands at 1:0.19, far below the global average of 1:0.7, while in developed countries, this ratio reaches 1:0.98.

It can be seen that China’s medical device industry is currently in a period of rapid growth. To identify the driving forces behind this trend, Fu Shinong addressed the issue from both subjective and objective perspectives.

“The so-called objective factors refer to the current situation where our overall development of medical equipment lags behind that of developed countries. China has a population of 1.4 billion, constituting a market size of approximately RMB 650 billion; whereas Japan, with a population of 120 million, has a medical device market size of about RMB 200 billion. In other words, our current per capita access is only 27% of Japan’s level. Therefore, the heightened public health awareness and the urgent demand for medical services indicate that there is still enormous room for growth in the medical device market, representing a rigid demand in our country.”

“From a subjective perspective, as healthcare is a foundational sector for public welfare, the state is vigorously promoting the development of related industries. Relevant institutions have implemented Diagnosis-Related Groups (DRG) and promoted tiered diagnosis and treatment systems, all aimed at continuously improving institutional frameworks to address the imbalance in medical resource distribution and the excessive concentration of high-quality resources. If patients are to be diverted to township-level facilities, this triage approach will inevitably necessitate substantial upgrades in the equipment capabilities and medical resource capacities of primary care hospitals.”

From a policy perspective, the implementation of global budget payment systems and the “zero markup” policy on drugs and consumables will eliminate the model of subsidizing healthcare with drug profits. Under this trend, medical device consumption may become a new foundation and growth driver for physicians’ and hospitals’ income. It is important to note that the growth in device consumption does not aim to shift more examination costs onto patients; rather, it seeks to enhance clinical value through more efficient equipment and extend early diagnosis and screening services to healthy populations, thereby achieving better health management.

In addition, the procurement of CT, MRI, and PET/CT systems by hospitals previously required national-level approval and certification; however, this authority has now been delegated to provincial-level agencies. Configuration permits for MRI systems below 1.5T and CT scanners with fewer than 64 slices have begun to be abolished. These policies have subjectively driven the development of the entire medical device industry.

Driven by these dual factors, both the number of domestic healthcare enterprises and the market size have seen substantial growth. To navigate this wave successfully, companies may need robust strategic support.

“First, imaging equipment must better respect physicians’ clinical habits and align with their daily workflow requirements. For a long period in the past, I worked at a foreign medical device company. When our key clients requested adjustments to the film printing process to match hospital practices, I relayed this feedback to our overseas headquarters. However, after two to three years of discussions, our company still failed to deliver a solution for Chinese users. This experience left a deep impression on me. As a Chinese enterprise, Sinovision Technology (Beijing) Co., Ltd. must be capable of addressing customer needs effectively and with the utmost speed. Currently, once a need is identified, we can typically resolve it within two months to half a year,” explained Fu Shinong.

“Another opportunity lies in import substitution. When I first entered this industry, nearly all major medical imaging products in China—including CT scanners, MRI systems, and X-ray machines—were imported. These products were extremely expensive; for instance, a dual-slice CT scanner could sell for RMB 5–6 million at that time. However, technological advancements have driven both technical upgrades and price reductions. The trajectory of the consumer electronics market yesterday mirrors that of large-scale medical devices today. Against this backdrop, we seize the early-mover advantage in import substitution by offering cost-effective products and services, aiming not only to serve healthcare institutions at all levels and patients but also to foster our company’s own development.”

“However, to achieve genuine import substitution, we must first possess mature proprietary technologies. ‘Over the past period, we relied heavily on certain components imported from the United States. When tariffs rose from 0.5% to 6%, the resulting cost increase indeed had a significant impact on us. Therefore, we made a firm commitment to independently master the key technologies involved in CT development,’ said Fu Shinong.”

From concept to actual development, Sinovision Technology (Beijing) Co., Ltd. has rapidly achieved independent production of key technologies—including CT detectors, gantry/scanning tables, control systems, medical software, image reconstruction algorithms, and advanced post-processing—leveraging its robust technical reserves and deep industry understanding. Its level of self-reliance is comparable to that of multinational corporations. Furthermore, Sinovision has obtained 10 NMPA certificates and 9 CE certificates, and holds core patents for all key CT technologies.

The changing times are also driving Sinovision’s continuous innovation. While maintaining CT imaging equipment as its core competency, Sinovision is continuously expanding into multidisciplinary applications and vigorously developing medical robotics and artificial intelligence technologies. The aim is to extend CT imaging technology beyond the radiology department, serving more clinical specialties, aligning more closely with clinical scenarios and patient needs, and thereby contributing to precision medicine.

“Large-scale imaging equipment is a traditional industry. In the past, we did not need to educate the market; by simply offering cost-effective, high-quality products, we could naturally secure a share of the market. However, as clinical scenarios become increasingly complex, we are leveraging technological innovation to build differentiated competitive advantages. For example, without increasing customers’ procurement costs, we have enlarged the CT bore diameter, enabling our CT systems to meet the requirements for routine high-definition diagnosis while also supporting radiotherapy simulation and localization, as well as minimally invasive interventional puncture procedures. Through cloud-based imaging solutions, we help medical consortia achieve seamless integration of resources between physicians at different levels of care, facilitating remote consultations and tele-education, thereby enhancing the diagnostic and treatment capabilities of primary healthcare institutions. Our interventional puncture robot significantly reduces the learning curve for physicians, ensuring precise puncture performance.”

“From a detailed perspective, in addition to traditional CT, we will place greater emphasis on supporting development for clinical treatment scenarios. For instance, by leveraging the movement of wide-degree-of-freedom robotic arm gantries, we can acquire high-definition images without any disturbance to patients during surgery, thereby providing precise guidance for surgical procedures. Remote real-time interventional navigation robots can assist physicians in remotely controlling needle insertion and puncture procedures, reducing radiation exposure while enhancing precision. From a macroscopic viewpoint, we will build upon our strength in CT imaging equipment and conduct in-depth research and development around technologies such as robotics, artificial intelligence, and cloud services, offering more interdisciplinary, multi-scenario solutions.”

In terms of market presence, Sinovision has already captured a significant share of the grassroots healthcare and non-public healthcare sectors. In 2020, the company will expand its sales footprint in high-tier public hospitals to further broaden its market reach.

Furthermore, customer recognition has brought Sinovision more sales opportunities, with the company’s sales revenue growth exceeding 50% in 2019. It is projected that Sinovision’s sales volume will increase by 1.5 to 2 times in 2020, which means that the company will build a larger-scale industrial base.

At the conclusion of his remarks, Fu Shinong stated, “The achievements made by domestic medical device manufacturers today are attributable to the favorable industrial environment, support from national policies, and the relentless efforts of participants across all sectors of the industry. In the late 20th century, it was difficult to find machining and manufacturing vendors in China that met required standards. However, we can now source high-quality machining and electronics manufacturing enterprises not only in the Pearl River Delta and Yangtze River Delta regions but also in the areas surrounding Beijing. These suppliers are even capable of providing advanced technologies such as microelectronics and vacuum electronics. Therefore, as we advance into the next era, we must recognize that we are not an isolated force; the development of the medical industry requires collective effort. By working together, all parties can help overcome challenges facing domestically produced medical devices, foster a healthy ecosystem for China’s medical equipment industry, and contribute to the Healthy China initiative.”