Mapping the Logic and Implementation Pathways of China's 2019 Healthcare Policies: 11 Key Areas and 240 Policy Measures

On January 1, 2020, the new edition of the National Reimbursement Drug List came into effect.

The scene of health insurance negotiation experts engaging in “soul-stirring price slashing” remains vividly etched in our memories, representing one of the moments from the largest-scale negotiation since the establishment of China’s health insurance system.

The negotiation experts’ successive price cuts, capped by a final “killer move” of trimming just four cents, reflect the strong bargaining power demonstrated by the National Healthcare Security Administration since its establishment in areas such as medical insurance negotiations and centralized drug procurement. Reform measures represented by these efforts have far-reaching implications, where a single change can trigger system-wide effects.

Following the institutional reforms, the National Health Commission (NHC), the National Healthcare Security Administration (NHSA), and the National Medical Products Administration (NMPA) have assumed distinct yet interconnected roles, focusing respectively on healthcare services, medical insurance, and pharmaceuticals. 2019 marked the first full year of operation under the new structure, during which the three agencies demonstrated significant activity: the NHC issued 161 policy and regulatory documents, the NHSA released 26 major policy papers, and the NMPA promulgated 61 regulatory instruments.

In addition, the General Office of the State Council, the National Development and Reform Commission, and the Ministry of Finance have also issued multiple documents pertaining to the medical and health industry. In 2019, two important laws—the Vaccine Administration Law and the newly revised Drug Administration Law—came into effect.

VCBeat (WeChat ID: vcbeat), aligning with key industry focuses, has outlined multiple policy highlights and their interconnections to create a comprehensive overview of healthcare policies, facilitating a quick understanding of the overall logic behind China’s 2019 healthcare policies.

2019 Healthcare Policy Panorama, Chart Compiled by VCBeat Based on Publicly Available Policy Documents

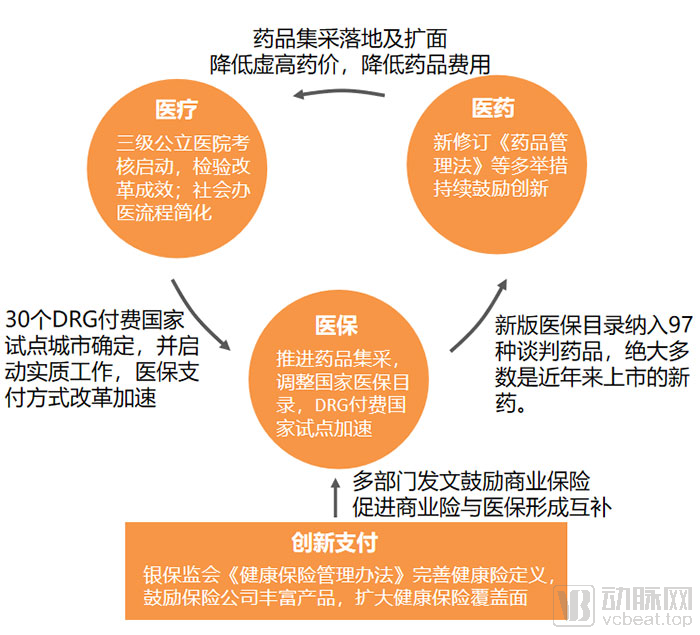

As healthcare reform enters deeper waters, the coordination among medical services, health insurance, and pharmaceuticals (“three-medical linkage”) became more closely integrated in 2019. Key policies and their interconnections are as follows: Centralized drug procurement has squeezed out price inflation, reshaping the landscape of drug production and distribution; tertiary public hospitals faced a “major examination,” with assessment indicators comprehensively reflecting the implementation of reform measures; the national-level DRG (Diagnosis-Related Groups) system launched pilot programs, serving both as a reform of health insurance payment methods and as an important data source for performance evaluation of public hospitals; the National Reimbursement Drug List underwent significant adjustments, enhancing coverage capacity while sending a clear signal of support for innovation.

It is worth noting that the primary focus of basic medical insurance is to ensure broad coverage and adequate protection. Meeting diverse healthcare needs requires the mobilization of social resources, and in 2019, commercial health insurance received encouragement from multiple sectors.

Next, we will focus on key policies selected from four major areas—medical care, medical insurance, pharmaceuticals (including medical devices), and innovative payment—covering 11 sub-sectors and over 240 policy items. We will interpret these policies, analyze the impact of the new regulations, and present data demonstrating the outcomes of policy implementation across various sectors in 2019.

Medical services are closely linked to patients, hospital physicians, pharmaceuticals, and medical devices, constituting a vital component of the healthcare system. We will examine the policy trends of 2019 from the perspective of the three main providers of medical services—public hospitals, private healthcare institutions, and internet hospitals—with the National Health Commission playing a leading role.

Public Hospital Performance Assessment: Evaluating the Effectiveness of Reforms

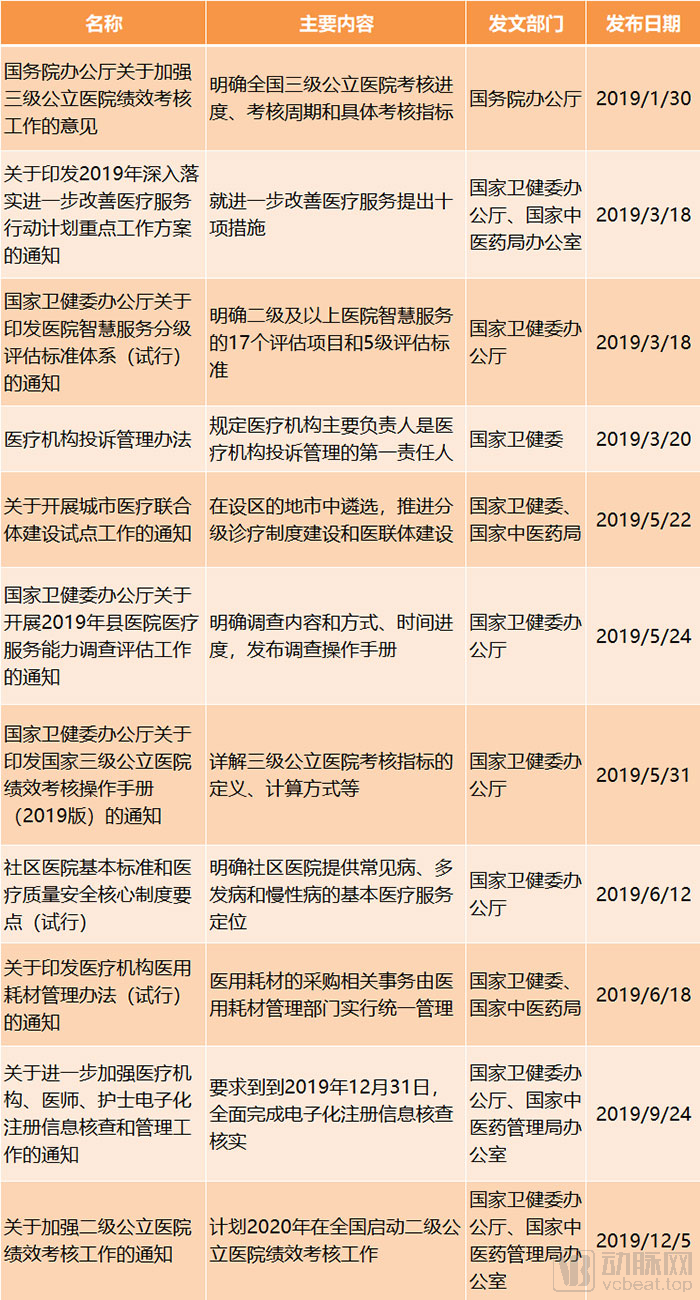

Key Policies and Main Content for Public Hospitals in 2019, Chart by VCBeat

In 2019, policies for public hospitals primarily focused on improving the quality of medical services, promoting tiered diagnosis and treatment, and advancing the construction of smart hospitals—key themes in the reform of public hospitals in recent years. How effective has the implementation of these initiatives been? In January 2019, the national government launched the first-ever performance assessment for tertiary public hospitals, integrating these issues into a unified evaluation framework.

The assessment is divided into three phases. In 2019, the assessment of 2018 data was conducted: hospitals completed self-evaluations by the end of September, provincial authorities completed assessments of tertiary hospitals within their jurisdictions by November, and the National Health Commission completed the analysis of monitoring indicators by December. Starting from 2020, the aforementioned three phases of work for the previous year’s data must be completed annually between January and March.

The assessment established 55 specific indicators across four dimensions: medical quality, operational efficiency, sustainable development, and satisfaction evaluation.

Selected Performance Indicators for Tertiary Public Hospitals, Chart by VCBeat

We have selected certain indicators for illustration, among which those that should be gradually increased or decreased particularly reflect the objectives of the assessment.

For example, assessing the number of patients referred downward aims to promote tiered diagnosis and treatment and the decentralization of high-quality medical resources; gradually increasing the proportion of nationally centralized procurement drugs can help reduce medication costs and squeeze out gray areas in drug distribution; raising the proportion of medical service revenue reflects the need to place greater emphasis on the labor value of medical personnel following the implementation of zero-markup drug policies and centralized drug procurement; reducing the incidence of complications among surgical patients and curbing cost increases are intended to improve medical quality while avoiding overtreatment.

Assessment results will serve as a crucial basis for hospital development planning, fiscal investment, determination of the total performance-based wage pool, and adjustments to medical insurance policies, as well as an important reference for the selection and appointment of secretaries of the Communist Party organizations, presidents, and leadership team members of public hospitals.

With the comprehensive implementation of performance evaluations for tertiary public hospitals, assessments for secondary public hospitals are also set to commence. As these evaluations become routine, the management of public hospitals will become more precise, enabling timely tracking of reform implementation and ensuring that policies do not remain mere formalities.

Simplified Procedures for Private Medical Practice, Raised Entry Thresholds

In recent years, the state has continuously introduced policies to encourage private investment in healthcare. Accompanied by capital inflow and physicians’ multi-site practice, the number of private medical institutions has long surpassed that of public ones. However, this process has also exposed certain challenges for privately run healthcare providers, such as complex approval procedures and uneven quality of care.

Key Policies and Highlights for Private Healthcare Providers, Chart by VCBeat

A review of the policies promoting privately run medical institutions in 2019 shows that most were jointly issued by multiple departments. This is primarily because the approval and regulation of such institutions involve not only the health authorities but also other agencies, including those responsible for business registration and fire safety.

In accordance with the "Notice on Optimizing Cross-Departmental Approval Procedures for Socially Operated Medical Institutions," both for-profit and non-profit medical institutions are required to complete only three steps. Meanwhile, environmental impact assessments are subject to classified management, with filing-based administration applied to those having minimal environmental impact. Medical institution facilities with a construction area of less than 300 square meters or an investment of less than RMB 300,000 are exempt from fire protection design review and completion acceptance filing procedures.

In 2019, ten cities, including Shanghai and Shenzhen, began piloting new regulations and standards for clinics. These new rules and standards also streamlined the establishment process by replacing administrative approval with a filing-based management system, eliminating minimum area requirements, and removing restrictions on site selection. The new regulations also require physicians to have practiced in medical institutions for at least five years after registration and to hold a title of attending physician or higher, raising the threshold for clinics’ soft capabilities.

It is evident that the policy trends for private healthcare providers share similarities with those for public hospitals, as both are shifting their focus from scale to quality. The simplification of registration procedures aims to facilitate entry into the industry for professionals with genuine medical expertise, thereby addressing the previous tendency of private hospitals to prioritize profit-seeking, which led to over-treatment and frequent medical disputes. In such a policy environment, healthcare institutions that prioritize improving medical quality and emphasizing treatment outcomes are more competitive and better positioned to enhance patient trust in the industry.

The Policy Framework for Internet-Based Healthcare Has Been Basically Established

After years of exploration, internet hospitals finally achieved policy certainty in 2018, entering a new peak period of development in 2019.

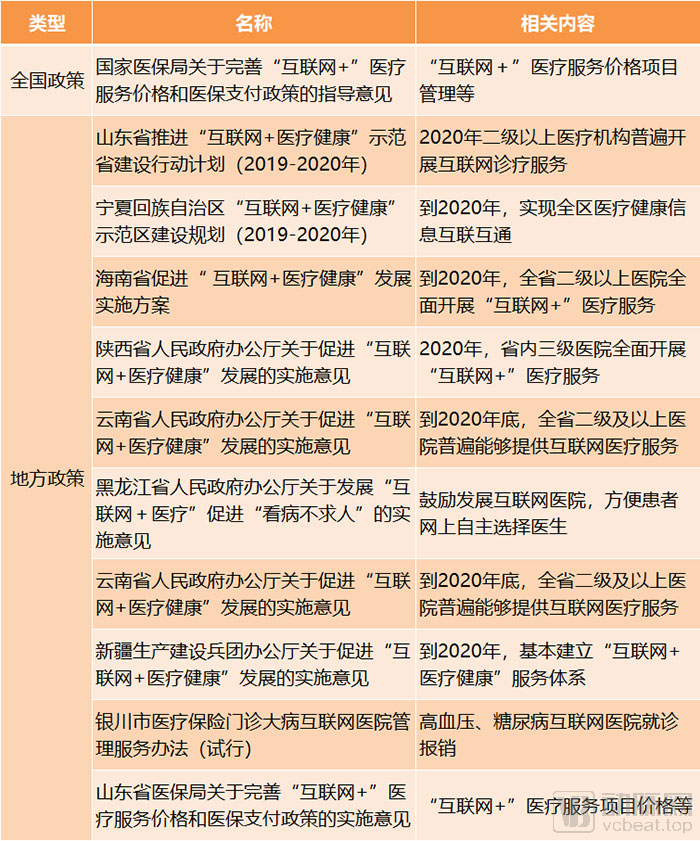

Key Policies and Highlights of Internet Healthcare in 2019, Chart by VCBeat

In 2019, policies on medical insurance reimbursement for internet-based healthcare were introduced. Subsequently, Yinchuan in Ningxia and Shandong Province respectively issued corresponding implementation measures, establishing service prices and reimbursement rates.

However, medical insurance reimbursement for internet-based healthcare covers only the core diagnostic and treatment components, whereas internet-based healthcare provides a diverse range of services built upon initial consultations. Consequently, it is difficult for internet healthcare companies to generate substantial revenue directly through medical insurance; instead, they should explore new technologies and services to promote cost reduction and efficiency improvements in healthcare delivery.

In 2019, various regions across China accelerated the implementation of national internet healthcare policies by issuing detailed implementation rules and establishing provincial-level regulatory platforms for internet medical services, thereby providing safeguards for the development and oversight of internet hospitals. Under policy guidance, not only did public hospitals extensively build internet hospitals, but a diverse range of enterprises also participated in their development. Beyond internet healthcare companies, health IT firms, and pharmaceutical e-commerce platforms, pharmaceutical manufacturers, medical device companies, and insurance providers have also joined this growing trend.

For public hospitals, internet hospitals are a vital tool for expanding service reach and optimizing the distribution of medical resources; for enterprises, they serve as a key connector integrating healthcare, pharmaceuticals, and insurance, thereby enabling compliant business operations.

As the largest payer in China’s healthcare system, the National Healthcare Security Administration (NHSA) has been under intense scrutiny since its establishment. In 2019, the NHSA spearheaded the formulation and implementation of three major policies: centralized drug procurement, adjustments to the national medical insurance reimbursement list, and pilot programs for Diagnosis-Related Groups (DRG).

Implementation and Expansion of Centralized Drug Procurement

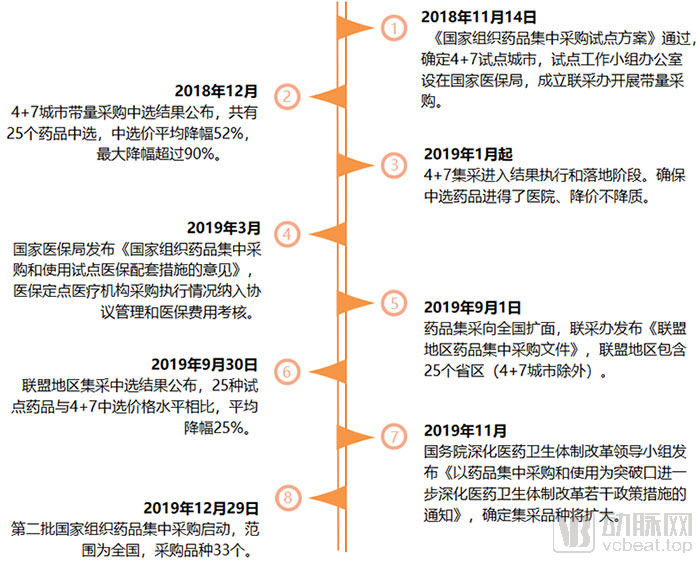

The "4+7" centralized volume-based procurement was launched in late 2018, selecting 11 cities—Beijing, Tianjin, Shanghai, Chongqing, Shenyang, Dalian, Xiamen, Guangzhou, Shenzhen, Chengdu, and Xi’an—as pilots for the national organization of drug volume-based procurement.

The General Office of the State Council, the National Healthcare Security Administration (NHSA), the National Health Commission (NHC), and the National Medical Products Administration (NMPA) have established a Working Group for the Pilot Program on Centralized Drug Procurement and Use Organized at the National Level. The NHSA is responsible for formulating the pilot plan, related policies, and overseeing implementation. Representatives from each pilot city have formed a Joint Procurement Office (hereinafter referred to as the “JPO”). The Shanghai Pharmaceutical Centralized Bidding and Procurement Affairs Management Office undertakes the daily operations of the JPO and is responsible for specific implementation.

Following the announcement of the winning bids for the “4+7” centralized procurement in December 2018, implementation began in 2019. In September 2019, the Joint Procurement Office issued further documents to expand the scope of centralized procurement nationwide, with the national government organizing a consortium of 25 provinces and autonomous regions (excluding the original “4+7” cities) to conduct volume-based procurement. We have outlined the key implementation steps for drug centralized procurement as follows:

Key Implementation Milestones of National Drug Centralized Procurement, Chart by VCBeat

The "4+7" volume-based procurement program led to significant price reductions for winning generic drugs; some manufacturers chose to voluntarily lower prices even without winning bids, in an effort to maintain market share.

Some pharmaceutical companies strive to win bids in centralized procurement, even at the cost of successive price reductions, and do so with multiple products. For instance, Zhejiang Huahai Pharmaceutical won bids for as many as six drugs during the “4+7” centralized volume-based procurement (VBP). The company’s semi-annual report indicated a slowdown in its year-on-year revenue growth in the first half of the year, with VBP being one of the significant contributing factors. Nevertheless, Huahai Pharmaceutical continued to participate actively in the subsequent alliance-region VBP launched in September, securing bids for seven drugs. Notably, the winning bid prices for the same drugs in the alliance regions were even lower than those in the initial “4+7” VBP.

In China, a market dominated by generic drugs, although the volume-based procurement policy has caused significant distress to pharmaceutical companies, many still seek to trade price for volume in an effort to maintain their market share at all costs. However, as most of these companies possess integrated supply chains—manufacturing both finished formulations and active pharmaceutical ingredients (APIs), among other products—they remain highly competitive.

In 2019, centralized drug procurement and usage were identified as a breakthrough point for further deepening healthcare reform. On December 29, the second round of national centralized drug procurement was launched, involving nationwide participation and covering 33 drug varieties. Going forward, the overall prices of generic drugs will continue to decline. Pharmaceutical companies with single-product portfolios, weak innovation capabilities, and high marketing expense ratios are highly likely to be eliminated from the market or face transformation.

National Reimbursement Drug List Adjustment Sees Largest-Ever Drug Price Negotiations

The 2019 major adjustment to the National Reimbursement Drug List (NRDL) involved a significant number of drugs being added and removed, resulting in substantial changes to the drug structure. The routine admission segment saw the addition of 148 new drugs, covering medications for major diseases such as cancer and rare diseases, chronic conditions, and pediatric use. The most closely watched aspect of this adjustment was the negotiated admission segment, where both the number of newly added negotiated drugs and the total number of negotiated drugs reached record highs.

We have outlined the timeline for catalog adjustments and key data as follows:

Key Milestones in the 2019 Adjustment of the National Reimbursement Drug List, Chart by VCBeat

For individual drugs, Humira, the former “blockbuster king,” had a peak price of RMB 7,800 per injection. Since 2019, its price has been reduced to RMB 3,160 per injection in certain regions, with the negotiated price further lowered to RMB 1,290 per injection, representing a substantial 59% reduction. Innovent Biologics’ Tyvyt (sintilimab) successfully entered the negotiation at RMB 2,843 per vial (100 mg/10 mL), marking a significant 63.73% price cut.

It is inevitable that negotiated drugs will enhance medical insurance coverage, and their impact on the pricing of innovative drugs is also evident. While innovative drugs indeed entail high R&D costs, this does not mean that price pressures will lead to reduced or absent innovation. Large multinational pharmaceutical companies are all innovation-driven enterprises, and innovation will remain their core competitiveness. Pharmaceutical companies can leverage digital technologies to improve R&D efficiency and reduce costs; meanwhile, they should strategically structure their product pipelines to pursue differentiated competition.

Furthermore, once a drug is included in the National Reimbursement Drug List (NRDL), it can rapidly scale up volume to capture market share and secure a first-mover advantage within the same therapeutic area.

National DRG Payment Pilot Accelerates Health Insurance Payment Reform

How Popular Are DRGs? The 4th National Diagnosis-Related Groups (DRG) Forum, held not long ago, attracted more than 2,000 participants from across China, including heads of administrative departments, hospital presidents, DRG managers, and experts, with all sub-forums fully attended.

In 2019, 30 cities were designated as national pilot cities for Diagnosis-Related Group (DRG) payment reform. Following the three-step approach of “top-level design, simulation testing, and actual payment implementation,” these cities were required to ensure simulated operations in 2020 and initiate actual DRG-based payments in 2021.

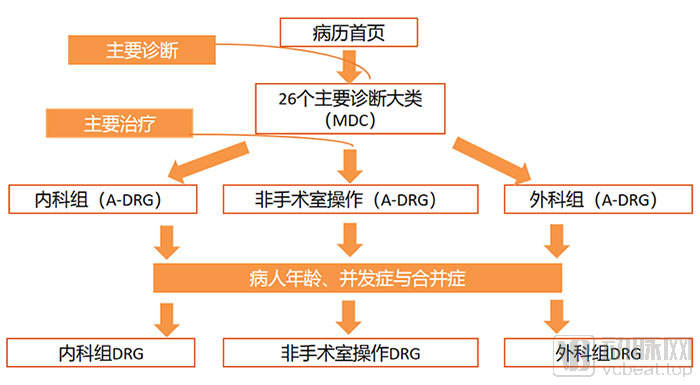

The National Healthcare Security Administration also integrated previous DRG versions to formulate a nationally unified grouping scheme, namely CHS-DRG, which was released on October 24. CHS-DRG categorizes diagnoses into 26 major groups based on ICD-10 codes, and further forms 376 A-DRG groups according to treatment methods. Taking regional differences into account, CHS-DRG does not provide further subdivision; instead, it leaves the detailed refinement to individual provinces.

CHS-DRG Grouping Process, Chart by VCBeat

In the future, DRG will not only serve as a more refined method for health insurance payment but also act as a crucial tool for evaluating healthcare service performance and managing medical costs, carrying significant implications.

Although Beijing, Zhejiang, and other regions had previously made some attempts at DRG-based payment, the DRG system involves numerous stakeholders and features a complex operational framework. Upcoming practical challenges include how physicians assign inpatient medical records to DRG groups, how hospitals incorporate DRGs into performance evaluations, how health insurance agencies use DRGs for payment, and how DRG grouping schemes are dynamically maintained and adjusted. As per the established schedule, the timeline is tight and the tasks are substantial. This readily explains why hospital administrators place such high importance on this initiative.

The exploration and implementation of Diagnosis-Related Groups (DRGs) will remain a key priority for healthcare security administrations, health commissions, and hospitals for the foreseeable future, while also becoming a core business focus for healthcare IT enterprises. As new challenges may emerge and adjustments be made accordingly, there is still a long road ahead before DRGs are fully adopted across China. VCBeat will continue to monitor and report on these developments.

“Innovation” has been a buzzword in the pharmaceutical and medical device sectors in recent years. Previously, national support for innovation primarily focused on the review and approval processes. As innovative drugs and devices increasingly enter their commercialization and return-on-investment phase, the government is gradually strengthening the optimization of registration procedures and enhancing regulatory oversight of distribution channels. Within the framework of relevant laws, the National Medical Products Administration (NMPA) leads the formulation and implementation of specific policies governing the research and development, registration, and production of pharmaceuticals and medical devices.

Multi-Pronged Measures to Encourage Drug Innovation

In 2019, the Vaccine Administration Law and the newly revised Drug Administration Law were promulgated and came into effect on December 1. These laws encourage innovation through higher-level institutional design and establish regulatory oversight over the entire lifecycle of drugs and vaccines.

2019 Laws and Major Policies Related to Pharmaceuticals, Chart by VCBeat

The newly revised Drug Administration Law establishes the comprehensive implementation of the Marketing Authorization Holder (MAH) system, requiring MAHs to establish a quality assurance system and assume responsibility for all processes and aspects of drug development and lifecycle management, including non-clinical studies, clinical trials, production and operation, post-marketing research, adverse reaction monitoring, reporting, and handling. This accountability-driven management model will place greater pressure on pharmaceutical companies, thereby promoting standardized industry development.

On the other hand, allowing drug marketing authorization holders to outsource drug production and distribution to other enterprises breaks the integrated “R&D, production, and sales” model. This enables companies across different segments to form flexible partnerships, each fulfilling its respective responsibilities, thereby enhancing the efficiency of drug innovation.

Meanwhile, the separate GMP and GSP certifications have been abolished; however, this does not mean that GMP and GSP standards have been eliminated. Instead, compliance with these standards has been incorporated into the inspection processes for drug manufacturing and distribution licenses. This implies that failure to meet GMP or GSP requirements will result in the direct revocation of a company’s drug manufacturing or distribution license, thereby substantially raising the regulatory bar for pharmaceutical enterprises.

The introduction of the Vaccine Administration Law reflects the state’s implementation of the strictest oversight over vaccines. Research and development, manufacturing, and distribution are all managed in accordance with the highest standards, and severe penalties are imposed for any violations to prevent vaccine safety incidents.

Furthermore, the release of the second batch of overseas new drugs urgently needed for clinical use can accelerate the market entry of these drugs in China and compel domestic companies to intensify their innovation efforts. The National Medical Products Administration’s basic considerations on using real-world evidence to support drug development have pointed out a safer and more effective direction for clinical trials in innovative R&D.

Therefore, drug innovation remains the key theme for 2019.

Expanded Scope of Consistency Evaluation: Injections and Vaccines Included

To ensure the safety and efficacy of pharmaceutical products and enhance the overall standards of the generic drug industry, the Consistency Evaluation of Quality and Efficacy for Generic Drugs was officially launched in 2017. As required, oral solid dosage forms of chemical generic drugs approved for market launch before October 1, 2007, and included in the National Essential Medicines List (2012 Edition), were to complete the consistency evaluation by the end of 2018.

However, in December 2018, the National Medical Products Administration issued a notice adjusting the evaluation timelines, stipulating that uniform evaluation time limits would no longer be applied to drugs included in the National Essential Medicines List.

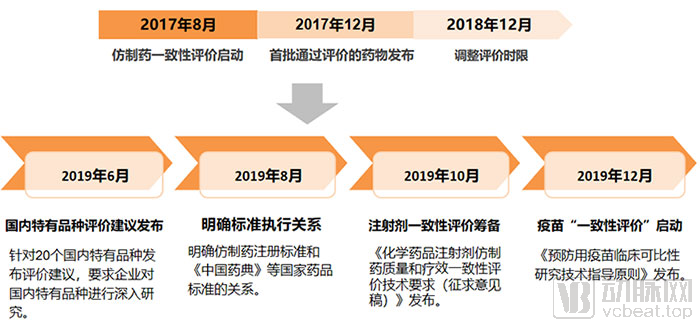

NMPA Accelerates Generic Drug Consistency Evaluation Progress | Graphic by VCBeat

From the perspective of policy changes in the consistency evaluation since 2019, there are mainly two aspects: First, the policy interpretation for the evaluation work has become more detailed, as seen in the evaluation recommendations for domestically unique varieties and the clarification of implementation standards. As a major country in generic drugs with a high proportion of such products, China faces a systematic and large-scale project in consistency evaluation. Given the significant variations in production processes among different drugs, substantial time and effort are required to conduct research and establish in vivo or in vitro evaluation methods tailored to the characteristics of each variety. During this process, issues are inevitable, and information asymmetry between the Center for Drug Evaluation and pharmaceutical companies may arise. More detailed interpretations are essential to accelerate the progress of the entire initiative.

On the other hand, the scope of consistency evaluation has been expanded to include injections and vaccines. The technical requirements for consistency evaluation of injections have been released for public comment, specifying requirements for reference listed drugs, formulation, and manufacturing processes. Meanwhile, the Technical Guidelines for Clinical Comparability Studies of Prophylactic Vaccines, regarded as the “consistency evaluation” for vaccines, has also been issued. These guidelines apply to non-innovative vaccines whose efficacy is evaluated using immunogenicity surrogate endpoints, affecting 45 vaccine manufacturers and further demonstrating the state’s principle of implementing the strictest oversight over vaccines.

Based on the results, the National Medical Products Administration (NMPA) approved 17 and 77 drug specifications for consistency evaluation in 2017 and 2018, respectively, while a total of 174 drug specifications passed the consistency evaluation in 2019. This indicates that significant progress was made in this work in 2019, laying the foundation for the subsequent consistency evaluation of injections and vaccines.

Accelerated Review and Approval of Medical Devices Amid Tighter Regulation

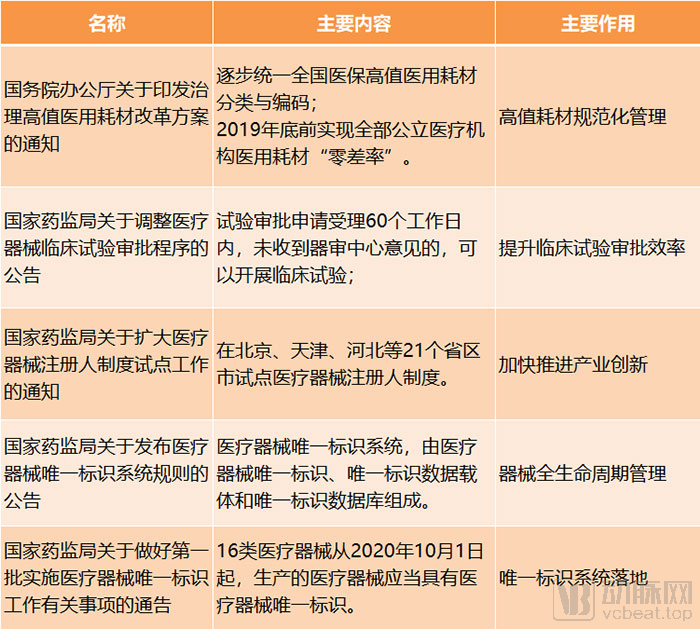

2019 Key Policies for Medical Devices, Chart by VCBeat

From the perspective of policies related to medical devices, initiatives such as the pilot program for the Marketing Authorization Holder (MAH) system and the establishment and implementation of the Unique Device Identification (UDI) system are all aimed at strengthening lifecycle management, aligning with the regulatory approach applied to pharmaceuticals.

It is worth noting that, in accordance with the "Notice of the General Office of the State Council on Issuing the Reform Plan for the Governance of High-Value Medical Consumables," all public medical institutions were to achieve zero-markup sales of medical consumables by the end of 2019, with the selling prices of high-value medical consumables aligned with their procurement prices.

By the end of 2019, public medical institutions eliminated markups on medical consumables. Meanwhile, the national government mandated improvements to classified centralized procurement methods. For high-value medical consumables characterized by substantial clinical usage, high procurement expenditures, mature clinical application, and production by multiple manufacturers, centralized procurement was explored on a category-by-category basis. Medical institutions were encouraged to jointly conduct volume-based negotiated procurement, and cross-provincial alliance procurement was actively explored.

Previously, public hospitals had fully implemented the zero-markup policy for pharmaceuticals, and centralized volume-based procurement of drugs had achieved phased results. Judging from the series of measures taken by the state regarding medical devices and consumables, not only is their regulatory approach aligning with that of pharmaceuticals, but the use of consumables in public hospitals and cost-containment efforts by medical insurance may also gradually synchronize with those for pharmaceuticals.

The "One-Invoice System" in the Circulation Sector Takes Shape

Key Points of Drug Distribution Policies in 2019. Arrows indicate the traditional distribution landscape, while lines represent the new distribution landscape. Graphic by VCBeat.

At the distribution level, in November 2019, the State Council issued the “Notice on Further Promoting the Experience of Fujian Province and Sanming City in Deepening the Reform of the Medical and Healthcare System,” pointing out that by 2020, in accordance with the national unified deployment, the scope of varieties of drugs subject to centralized procurement and use organized by the state should be expanded. Pilot provinces for comprehensive medical reform should take the lead in promoting direct settlement of drug payments by medical insurance handling agencies with drug manufacturers or distributors, while other provinces should also actively explore this approach.

This appears to signal the imminent arrival of the “single-invoice system.” In fact, provinces and municipalities such as Guangdong, Zhejiang, and Hubei have previously encouraged or piloted the “single-invoice system.” If the “single-invoice system” is rolled out nationwide, distribution enterprises will be significantly impacted.

In the traditional distribution landscape, distributors primarily assumed the roles of advancing funds and delivering goods. The “single-invoice system” implies a diminished role in fund advancement, leaving distribution as their sole function. However, given the uneven capacity of local healthcare security administrations and medical institutions to make timely payments, it remains uncertain whether pharmaceutical companies can receive prompt and full settlement. Therefore, nationwide implementation of the “single-invoice system” will require a considerable amount of time.

However, amidst this trend, distribution companies must still plan ahead. Large enterprises can leverage their robust distribution networks to extend their industrial chains and identify new growth drivers, while smaller firms should pinpoint their niche and collaborate with larger players to help enhance market penetration.

Furthermore, regarding online sales of prescription drugs, which were the primary concern in the retail sector in 2019, the newly revised Drug Administration Law no longer prohibits such sales. However, in November, the National Development and Reform Commission and the Ministry of Commerce released the 2019 Edition of the Negative List for Market Access, which stipulates that “drug manufacturers and distributors shall not sell prescription drugs directly to the public via mail order or internet transactions in violation of regulations.” This provision was interpreted as a ban on online sales and mail-order delivery of prescription drugs. Notably, this item is marked with a ★ symbol, indicating that it is a management measure temporarily included in the list due to insufficient legal authority at its current level, and that legislative procedures should be expedited to address this gap.

Therefore, the online sale of prescription drugs has not been fully liberalized; instead, it must be conducted in accordance with regulations, pending the introduction of future regulatory requirements.

As previously mentioned, pharmaceutical and vaccine policies place significant emphasis on lifecycle management. In 2019, the National Medical Products Administration (NMPA) made concerted efforts to advance the development of information-based traceability systems for vaccines and pharmaceuticals, issuing relevant technical standards. The Vaccine Traceability Collaborative Service Platform is scheduled to officially launch by the end of March 2020, while an information-based drug traceability system will be established as soon as possible for essential medicines and drugs covered by medical insurance reimbursement.

Unlike the electronic drug supervision codes used before 2016, the primary responsibility for vaccine and drug traceability now lies with drug manufacturers and distributors, while circulation enterprises and user institutions bear responsibility for their respective links in the supply chain. In the future, pharmaceutical companies will face greater regulatory pressure; however, implementing robust traceability measures serves as a form of self-protection, enabling clear attribution of liability through the traceability system in the event of safety incidents.

2019 was undoubtedly a year of significant momentum for the health insurance sector. The General Office of the State Council, the National Health Commission, the National Development and Reform Commission, and the Healthy China Action Promotion Committee all issued policy documents encouraging and supporting the development of commercial health insurance.

Key Health Insurance Policies and Relevant Departments in 2019, Chart by VCBeat

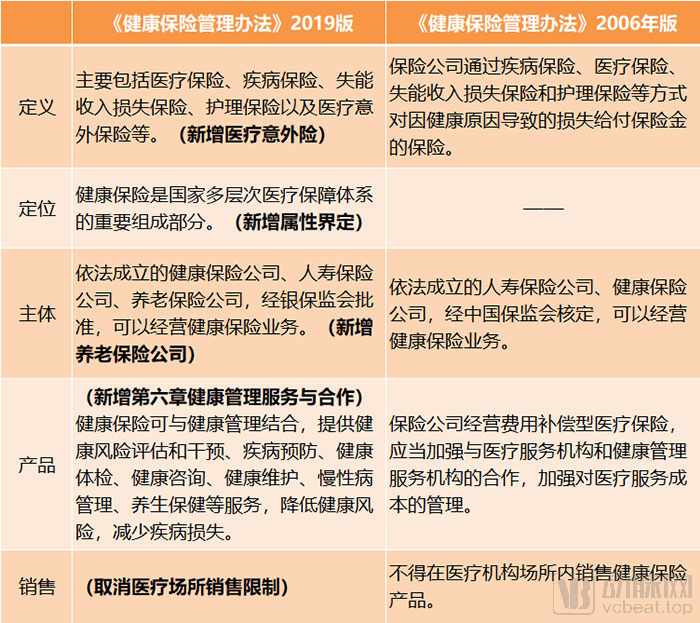

As the competent regulatory authority, the China Banking and Insurance Regulatory Commission (CBIRC) promulgated the newly revised Administrative Measures for Health Insurance in 2019, marking the first major overhaul since the measures were implemented in 2006. The Measures explicitly define “health insurance as an important component of China’s multi-tiered medical security system,” thereby further clarifying the direction for the complementary development of commercial health insurance and the national basic medical security system.

Comparison of Major Changes Between the Two Versions of the Measures for the Administration of Health Insurance, Chart by VCBeat

It is worth noting that Chapter 6 of the new measures constitutes newly added content, devoting substantial space to explaining the integration of health insurance with health management services.

Strengthening user health management in health insurance products can yield multi-party benefits. For users, maintaining good health is inherently preferable to falling ill; for insurers, promoting user health translates into reduced disease-related claims and improved overall profitability; and for healthcare security and public health authorities, a healthier population naturally leads to lower medical expenditures and more efficient utilization of public healthcare resources.

Currently, many innovative health insurance companies have leveraged technological means to engage in interactions and provide other health services to users, thereby encouraging them to proactively monitor their own health. This approach aligns with the broader healthcare paradigm shift from a disease-centric model to a health-centric one.

Having understood the overall policy logic and implementation pathways of 2019, we also seek to identify the progress and achievements made in policy execution during that year. We continue to examine this issue from four perspectives—medical care, pharmaceuticals, health insurance, and innovative payment models—by collecting data from multiple public sources. Due to varying timelines in the release of operational data by different departments, the cutoff dates for the collected data are not uniform; however, we have endeavored to present the most up-to-date information available.

Initial Results Seen in Medical Cost Control

Based on the operational data of public hospitals from January to May 2019, the average cost per outpatient visit and hospitalization either decreased or increased only marginally compared with the same period in 2018, when measured at comparable prices (note: comparable prices refer to prices adjusted to exclude the impact of price fluctuations).

Key Healthcare Data for 2019. Source: National Health Commission; Graphic by VCBeat

However, since the comprehensive implementation of the “4+7” centralized volume-based procurement (VBP) began in March 2019, followed by the expansion to alliance regions in September, the impact of drug VBP on controlling healthcare costs had not yet been fully realized by May. Moreover, as only 25 drugs were included in the pilot VBP at this stage, with more categories expected to be added in the future, there remains further room for reducing medical expenses.

Data from private hospitals show a considerable increase in overall outpatient and emergency visits, yet the growth in discharges remains modest. This indicates that patients still prefer public hospitals when hospitalization is required. In recent years, the state has introduced various policies to support private hospitals; however, their overall medical quality and patient trust continue to lag behind those of public hospitals. Beyond simplifying administrative procedures for establishing privately funded medical institutions, further institutional breakthroughs are needed in the future to incentivize the inflow of high-quality medical resources into the private healthcare sector.

In 2019, internet hospitals entered a new phase of concentrated development. By October, there were 269 internet hospitals, marking a shift from construction to operation and from quantity to quality.

Stable Surplus Rate of Medical Insurance

Based on the operation of the medical insurance fund from January to October 2019 as reported by the National Healthcare Security Administration, and using the data and calculation methods from the 2018 Statistical Bulletin on the Development of China’s Basic Medical Insurance, we calculated the surplus rates for employee basic medical insurance and urban-rural resident basic medical insurance in 2019 (Note: Surplus rate = [Fund Balance (Fund Income – Fund Expenditure) / Fund Income] × 100%).

Performance of the National Healthcare Security Fund; Source: National Healthcare Security Administration; Graphic by VCBeat

With economic development and rising household income levels, the revenue of the medical insurance fund has been growing annually. However, as medical expenses increase, expenditures from the fund have also risen correspondingly. The surplus rate, derived from a comprehensive calculation of revenue, expenditure, and surplus, serves as an indicator of the fund’s operational status to some extent; within a reasonable range, a higher surplus rate is preferable. The surplus rate for January–October 2019 remained stable compared to the overall surplus rate in 2018.

However, much like the operational status of hospitals, the full potential of the centralized drug procurement policy has yet to be realized. As a series of bold reforms by the National Healthcare Security Administration continue to be implemented, the medical insurance fund is expected to move toward a more sustainable and robust state.

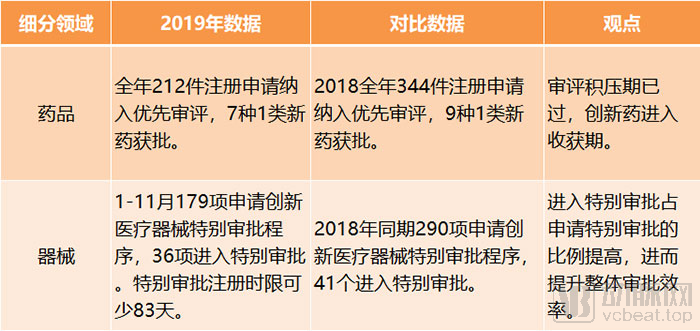

Innovative Drugs Enter the Harvest Period

As the country has accelerated drug review and approval processes in recent years, the backlog issue has been further resolved. We have observed that since 2019, the number of drugs included in the priority review program has decreased, and the number of projects applying for the special approval procedure for innovative medical devices has also declined.

Key Data in the Pharmaceutical Sector, 2019. Source: National Medical Products Administration; Graphic by VCBeat

From the results, innovative drugs have entered a harvest period. In 2019, seven Class 1 new drugs were approved in China. Although this did not maintain the explosive growth seen in 2018, these drugs are of high value.

In 2019, Hengrui Medicine and BeiGene’s PD-1 monoclonal antibodies were successively approved. With this milestone, all four domestically produced PD-1 monoclonal antibody products that had submitted New Drug Applications (NDAs) have been launched on the market, marking the official entry of competition into the phase of indication expansion.

During the adjustments to the National Reimbursement Drug List (NRDL), price negotiations have rapidly incorporated a large number of innovative drugs. In the future, NRDL negotiations will become routine, enabling innovative drugs with superior efficacy to gain reimbursement coverage more quickly and achieve rapid sales volume growth.

Health Insurance: A Bumper Harvest in Capital and Operations

Key Health Insurance Data for 2019. Source: China Banking and Insurance Regulatory Commission, public reports; chart by VCBeat

In 2019, the health insurance sector not only gained strong recognition from capital markets—with nearly 20 companies securing billions of yuan in financing—but also demonstrated robust overall business growth. From January to November 2019, gross written premiums for health insurance (Note: premium income from original insurance contracts recognized by insurance companies) reached RMB 656.4 billion, a year-on-year increase of 29.74%, surpassing the total gross written premiums for the entire year of 2018. Based on this growth rate, the health insurance market size is projected to exceed one trillion yuan in 2020.

Although the role of commercial health insurance within the national multi-tiered healthcare security system is more clearly defined, offering promising prospects for the future, the industry must do more than just optimize and diversify its products. It also needs to enhance the professionalism of practitioners and strengthen consumer education, thereby shifting the focus from traditional relationship-driven sales to genuine product- and health-oriented services, ultimately ushering in a phase of sustainable and healthy development.

Comprehensive Promotion of Salary Reform in Public Hospitals

By the end of February 2020, all regions were to comprehensively advance the reform of the compensation system in public hospitals according to local conditions, and implement and improve policies related to performance-based pay in primary healthcare institutions. In 2020, the National Health Commission, the Ministry of Human Resources and Social Security, the Ministry of Finance, and other departments jointly formulated specific measures to align the connotation of medical service revenue with the compensation system.

Physicians undergo lengthy training, face high occupational risks, and deal with significant technical challenges, so they naturally expect commensurate professional rewards. The key to hospital compensation reform lies in truly channeling the savings from squeezing out inflated prices of pharmaceuticals and medical consumables into reflecting the labor value of healthcare professionals. This cannot be achieved overnight; however, as reforms in other areas yield results, compensation reform should keep pace.

Expanding Scale of Centralized Drug Procurement, High-Value Consumables Set for Centralized Procurement

The expansion of drug categories included in centralized procurement is an inevitable trend. In accordance with the requirements of the State Council’s Leading Group for Deepening the Reform of the Medical and Healthcare System, priority will be given to including in the centralized procurement scope those drugs whose originator prices are higher than those in major countries and neighboring regions, those with significant price gaps between originator and generic drugs, as well as essential medicines that have passed the consistency evaluation.

Furthermore, the trend toward centralized volume-based procurement of high-value medical consumables has become clear. However, challenges related to inconsistent standards and classifications must first be addressed. A national-level initiative to standardize the classification and coding of medical consumables is currently underway, aiming to achieve comprehensive interoperability and sharing of information on medical consumables across China, promote open and transparent pricing, and lay the foundation for full-scale volume-based procurement.

Further Improvement of Infrastructure, DRG Simulation Operation

The national DRG pilot program was required to complete its simulation run in 2020, laying the groundwork for actual payment implementation in 2021. Therefore, in 2020, it was necessary to gradually improve infrastructure in both software and hardware aspects. The state would supervise and evaluate the simulation operations and deploy subsequent work.

For hospitals, under the trend of DRG payment reform, it is necessary to gradually shift from the previous model of increasing revenue by expanding service volume to a new model that boosts income by improving diagnostic and treatment quality while reducing medical costs.