Alere: A 15-Year POCT Pioneer’s Journey Through Over 100 Acquisitions to Abbott Acquisition

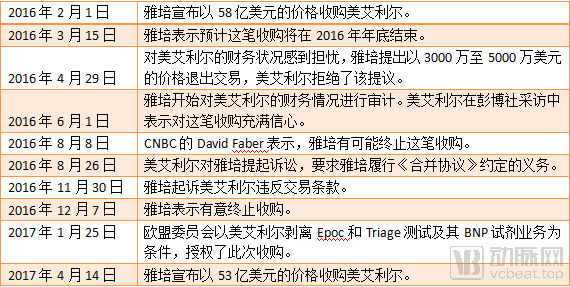

After weathering multiple controversies, Abbott ultimately announced in April 2017 that it would acquire Alere for $51 per share, at a total value of $5.3 billion.

Founded in 1991 and headquartered in Waltham, Massachusetts, USA, Meridian Bioscience is an in vitro diagnostics company specializing in the research and development, manufacturing, and sales of POCT reagents and medical devices.

Alere boasts specialized products and expertise covering more than 100 disease categories, providing high-end diagnostic testing products to over 100 countries, including those in North America, Europe, Australia, Japan, and Israel. Data shows that in 2016, Alere generated $2.376 billion in revenue and captured a 20% share of the global point-of-care testing (POCT) market (excluding blood glucose monitoring).

In just 15 years, Alere went from its founding in the United States to becoming a leader in the point-of-care testing (POCT) sector, and ultimately to being acquired by Abbott. VCBeat seeks to analyze Alere’s development history and core business lines, exploring how it grew into a POCT leader and the reasons behind its acquisition by Abbott.

Aggressive M&A to Build Massive Scale in the POCT Sector

In 1991, Jewish entrepreneur Ron Zwaszniger founded SelfCare, the predecessor of Abbott Diabetes Care (formerly known as MediSense), with a few thousand dollars in startup capital, and developed Medisense, the world’s first-generation blood glucose meter.

In 1996, SelfCare sold Medisense to Abbott for $880 million, enabling Abbott to successfully enter the blood glucose monitoring sector. In 2001, the company sold its second-generation blood glucose meter, LifeScan, to Johnson & Johnson for $1.3 billion. These two transactions allowed the company to rapidly accumulate substantial capital.

After divesting its blood glucose business, SelfCare concentrated its operations on toxicology testing, cardiac markers, and infectious disease testing. In 2000, SelfCare was renamed Inverness and listed on the American Stock Exchange (ASE).

From 2001 to 2005, Inverness’s growth in the in vitro diagnostics sector was unremarkable, with annual revenue hovering around USD 300–500 million.

In 2006, Inverness announced the full acquisition of ACON Laboratories, a clinical diagnostics reagent company based in San Diego, including its diagnostic reagent manufacturing plant in Hangzhou. This acquisition made ACON’s Hangzhou facility the base for Inverness to transfer production from developed countries.

The turning point occurred in 2007.

In 2007, Inverness acquired Biosite from Beckman for $1.8 billion, a deal that catapulted Inverness to prominence.

Biosite specializes in point-of-care testing (POCT) and protein antibody immunoassay technologies, having launched dozens of product series, including those for drug abuse screening and cardiac biomarker detection. Following the acquisition of Biosite, Inverness’s annual revenue surpassed $1 billion, solidifying its leadership position in the POCT sector, particularly in toxicology and cardiac biomarkers.

Since then, Inverness has frequently appeared in the capital M&A market. In 2007 alone, Inverness acquired 21 companies.

Summary of Medtronic’s Partial Acquisition Events; Data Sourced from the Internet

In 2007, following the acquisitions of Biosite, Choletech, and Cholestech Corp., Alere’s revenue increased by 98.93%. Notably, after acquiring Biosite, the company’s operating profit surged by 6,703.1%.

In 2010, on the occasion of its 10th anniversary, Inverness consolidated the brands of its more than 60 subsidiaries under the unified name Alere, advancing toward the concept of “connecting patients to healthcare management” with the aim of building a more renowned POCT brand.

In 2013, Alere acquired Epocal, a company specializing in blood gas and electrolyte diagnostics. Following the integration of Epocal’s blood gas analysis system, Alere’s annual revenue reached $3 billion.

Throughout Alere’s more than decade-long history, mergers and acquisitions have been the central theme of its growth. Through aggressive M&A activity, Alere has become one of the leaders in the point-of-care testing (POCT) sector. As of January 2017, Alere’s market capitalization stood at $3.47 billion, with an enterprise value of $5.9 billion.

Boasts a rich product portfolio, with three core business lines accounting for 93%

Alere’s product portfolio comprises 13 independently developed product lines and 11 acquired product lines, covering diagnostics for cardiovascular diseases, toxicology testing, infectious disease diagnostics, women’s health testing, and oncology testing. Among these, the three major product lines—cardiovascular disease testing, toxicology testing, and infectious disease testing—account for 93% of the total.

Cardiac Markers

Alere is the global leader in point-of-care testing (POCT) for cardiac biomarkers, boasting the most comprehensive product portfolio, including: heart failure assays (BNP, single marker); acute myocardial infarction assays (Myo, CK-MB, cTnI, triple-marker panel); thromboembolism assays (D-Dimer, single marker); chest pain panels (Myo, CK-MB, cTnI, BNP, quadruple-marker panel); and dyspnea panels (Myo, CK-MB, cTnI, BNP, D-Dimer, quintuple-marker panel).

Triage is a leading, next-generation rapid diagnostic testing system comprising a meter and various test devices. It enhances physicians’ ability to diagnose critical conditions and symptoms, including heart failure and myocardial infarction, and assists in the assessment of patients with pulmonary embolism.

In 2016, Triage had a global installed base of 16,000 units and generated $197 million in sales, with 51% of its revenue coming from regions outside the United States. In 2017, Triage was acquired by Quidel for $400 million.

Additionally, the CHOLESTECH LDX analyzer is one of Alere’s flagship products. This device can accurately and comprehensively test blood lipids, cholesterol, and blood glucose within five minutes.

Infectious Disease Testing

In the field of major infectious disease testing, Alere is a global leader with comprehensive solutions. Its product portfolio includes world-class testing instruments for HIV, influenza, malaria, norovirus, Legionella, Group A Streptococcus, dengue fever, and respiratory syncytial virus (RSV).

In 2016, sales of Alere’s infectious disease testing product portfolio reached $770 million, up from $710 million in 2015, securing the company the number one global market share in this segment.

Alere CD4 is the world’s first portable point-of-care CD4 testing system, facilitating convenient antiretroviral therapy for HIV patients. The Alere CD4 system comprises the Alere T-lymphocyte counter and the Alere CD4 lymphocyte test kit. It is designed to determine the absolute count of CD3+/CD4+ T cells in capillary or venous whole blood. Automated testing is initiated simply by inserting the test cartridge, with results available within 20 minutes. Furthermore, the system has no components requiring maintenance and can be operated in both laboratory and non-laboratory settings.

*Clostridioides difficile* is a common bacterium responsible for healthcare-associated infections and diarrhea in hospitalized patients. Infection with this bacterium is often associated with the development of pseudomembranous colitis, a condition that can increase mortality rates sharply to 35–50%. Alere’s C. DIFF QUIK CHEK COMPLETE is currently the only rapid test kit capable of simultaneously detecting glutamate dehydrogenase (GDH) antigen and *C. difficile* toxins A and B, providing comprehensive diagnostic information in under 30 minutes with a single test.

Toxicology Testing

Alere offers drug and alcohol testing products for hospitals, physician offices, criminal justice agencies, rehabilitation centers, occupational health clinics, and homes.

Maiyier's DDS 2 Saliva Drug Testing System enables rapid screening for six common drugs of abuse using saliva samples, delivering results within five minutes and serving as an effective alternative to urine testing. Its portability, lightweight design, and ease of use make it an ideal choice for roadside drug screening.

Poor operational integration led to acquisition by Abbott

Since the 1990s, mergers and acquisitions (M&A) integration has been a prevailing trend in the in vitro diagnostics (IVD) industry. As a pioneer in the point-of-care testing (POCT) sector, Alere acquired over one hundred companies, yet ultimately could not avoid being acquired by a major industry giant.

After reaching $3 billion in revenue in 2013, Alere’s revenue began to decline continuously, while its assets and liabilities kept rising and remained at high levels. In addition to the financial crisis, Alere also faced pressure from court investigations and multiple product recalls.

In April 2017, Abbott announced the acquisition of Alere at $51 per share, for a total value of $5.3 billion. This acquisition propelled Abbott past Siemens and Danaher to become the second-largest global supplier in the in vitro diagnostics sector, trailing only Roche.

Amid mounting pressures on Alere, the acquisition was fraught with twists and turns and stretched out for over a year.

Industry insiders generally believe that Alere’s strength lies in its comprehensive product portfolio, while its weakness stems from an overly rapid pace of mergers and acquisitions and ineffective operational integration, leading to sustained losses. Abbott, on the other hand, is weak in R&D, with a sluggish product portfolio and iteration, but boasts superior brand strength and operational capabilities. Therefore, this acquisition represents a complementarity of strengths for both companies.

Following the acquisition, Alere brought new sales growth opportunities to Abbott. Alere’s diagnostic products for diseases such as HIV, dengue fever, and malaria helped expand Abbott’s product portfolio. After completing the acquisition of Alere, Abbott reported sales revenue of $30.58 billion in 2018, representing an 11.64% increase from 2017. Within its diagnostics business, Alere generated $2.072 billion in revenue for Abbott.

Mergers and acquisitions have long served as a strategic approach for companies to rapidly expand their product portfolios and capture market share. BioMérieux built an IVD empire by acquiring 21 companies for $1.7 billion, while Danaher emerged as a leading player in the medical device sector through 47 acquisitions.

Alere established its leadership in the POCT sector through extensive acquisitions; however, inadequate post-merger integration led to significant operational challenges. Additionally, its expansion into health management services adversely impacted the company’s cash flow. Therefore, companies should maintain a measured pace when pursuing mergers and acquisitions and prioritize effective post-merger business integration.