InshurCloud Files IPO Prospectus: Empowering Health Insurance for Patients with Pre-existing Conditions through Its 'Medical Brain'

At the 2019 Top 100 Future Healthcare Forum, Causa Cloud was ranked among the Top 10 Health Insurance Third-Party Administrators (TPAs) on the China List. Li Wei, CEO of Causa Cloud, also delivered a keynote speech titled “Medical Brain Empowering Health Insurance: Exploring New Models for Preventive Care” at the Innovative Health Insurance Forum. Following the event, Li Wei accepted an interview with a reporter from VCBeat (WeChat ID: Vcbeat), sharing insights into Causa Cloud’s explorations over the past two to three years in innovative insurance products, technology-enabled solutions, and the broader insurance sector.

New Policies and Models Help Address Pain Points in Health Insurance

As living standards and insurance awareness rise, the public is placing increasing importance on insurance. Health insurance, in particular, which is closely tied to physical well-being, has experienced explosive growth in recent years.

According to the "2018 China Commercial Health Insurance Report" released by the Insurance Association of China, the compound annual growth rate (CAGR) of health insurance premium income in China reached 38% from 2012 to 2017. Meanwhile, the latest data released by the China Banking and Insurance Regulatory Commission (hereinafter referred to as the "CBIRC") shows that from January to October 2019, the original premium income of health insurance in China amounted to RMB 614.1 billion, a year-on-year increase of 30.27%; the original claim payments for health insurance totaled RMB 183.8 billion, a year-on-year increase of 37.27%.

Based on this data analysis, the health insurance market size is projected to exceed RMB 1 trillion in 2020.

Despite rapid development, China’s health insurance industry still faces six major pain points: products, distribution channels, operations, services, risk control, and systems.

Product homogenization is a prominent pain point in China’s health insurance sector. Insurance products lack patent protection in their design phase; once an innovative insurance product is launched, other insurers quickly follow suit, leading to severe product homogenization across the industry.

Distribution channels represent the second major challenge for health insurance at present. The current health insurance market relies heavily on existing life insurance agents, making it difficult to achieve significant breakthroughs. Meanwhile, compared with countries that have well-developed commercial insurance markets, such as the United States, China’s distribution channel costs for health insurance are considerably high and continue to rise year by year. From 2016 to 2018, the proportion of distribution channel costs in total costs for China’s health insurance increased from 20% to approximately 30%.

The third pain point is operations. Unlike traditional life insurance, which involves limited customer interaction, health insurance requires frequent engagement with policyholders, making it a line of business with exceptionally high operational demands. The existing operational systems of insurance companies are ill-equipped to support the large-scale growth of health insurance.

The fourth pain point of health insurance, derived from operations, is service. Health insurance heavily relies on customers’ experience with services. From this perspective, service experience is a critical factor determining whether health insurance can achieve rapid and sustainable growth.

Risk control is the fifth major pain point in health insurance. Currently, most insurers prioritize rapidly scaling up health insurance premium volume. Their risk control strategies remain predominantly focused on “screening”—that is, selecting healthy individuals—while giving limited attention to how claims costs can be effectively managed for insured users. In reality, the health management module has the potential to play a significantly greater role in health insurance.

Finally, the system’s pain points are also worth noting. As an emerging line of insurance, most insurers do not have specialized core systems for health insurance; instead, they largely continue to rely on core systems designed for property and casualty insurance and life insurance.

To better regulate health insurance and promote the healthy development of the health insurance market, the China Banking and Insurance Regulatory Commission (CBIRC) released the Administrative Measures for Health Insurance on December 1. Compared with previous regulations, the new rules feature three highlights.

First, the new regulations explicitly allow for premium rate adjustments in long-term medical insurance to adapt to changes in disease patterns, advances in medical technology, and fluctuations in healthcare costs. Meanwhile, provisions related to premium rate floating for short-term individual health insurance have been removed, leaving pricing decisions to market forces, which better aligns with the current trend toward market-oriented premium rates. This provides excellent guidance for health insurance companies to implement health management initiatives and participate in pricing mechanisms.

Second, the new regulations raise the cap on the proportion of health management services within insurance costs to 20%, a significant increase from the 12% level in 2012. This indicates that regulatory authorities recognize health management as a crucial component of health insurance, thereby creating opportunities for the development of the health management sector.

Finally, the new regulations address three key areas, elevating the emphasis on new technologies to a significant level: first, they explicitly allow insurers, under certain circumstances, to review digital claim materials submitted by policyholders via the internet, thereby streamlining the claims process and enhancing service efficiency; second, they encourage insurers to establish information connectivity and data sharing with medical institutions and basic medical insurance authorities; third, they urge insurers to prioritize the application of new technologies, such as big data, in product development, risk management, and other operational segments.

Traditional insurance lines are centered around a single flagship product designed by the actuarial team, with the same standardized product sold to all customer segments. This model is no longer well-suited to current market trends. Consequently, health insurance will gradually shift toward a customer-centric approach in the future. What innovative opportunities exist in health insurance? Li Wei identifies three key areas for innovation in health insurance.

First, value-added services: an increasing number of insurance companies are focusing on innovative product services and product offerings. Second, new health and medical insurance products have seen significant improvements in the past one to two years, such as million-yuan medical insurance, critical illness insurance, and special drug reimbursement insurance. Finally, big data and intelligent technologies have created opportunities for health insurance in areas such as product marketing, pricing, and distribution channels.

Ultimately, these innovations will give rise to a customer-centric business model, thereby enabling health insurance providers to offer greater supply in product design, sales, and services to meet customer needs.

How Does Causa Cloud Empower Insurance Companies with Technology?

Data intelligence technologies and health tech are transforming the insurance industry. Technologies such as big data, artificial intelligence, blockchain, and smart hardware have been integrated throughout the entire insurance value chain, from application and underwriting to claims processing and customer service.

Nevertheless, the core business objectives of the insurance industry remain unchanged: growing premium volume and enhancing embedded value. Accordingly, Causa Cloud seeks to drive the insurance industry chain through four key areas: products, marketing, operations, and health management services.

Product

Driven by big data and artificial intelligence, the health insurance sector has seen significant innovation. For instance, insurers have begun launching interactive insurance products that integrate health management services. Policyholders can upload their health data after exercising to qualify for higher and more comprehensive coverage limits provided by the insurer.

The entire business process begins with data collection after obtaining authorization during the underwriting stage. User profiles are established through data cleansing, and matching insurance products are offered based on the analysis of user data. During the post-underwriting health management phase, policyholders are required to continuously upload health information to qualify for discounts; in turn, this enables insurers to provide better and more personalized health management services.

John Hancock, a U.S. life insurer with a 156-year history, launched its wearable device-based insurance program in 2018. This insurance product comprises two plans, requiring policyholders to complete health tasks outlined in the health management program. These tasks include meeting fitness and calorie goals, as well as achieving targets for body mass index (BMI), blood glucose, blood pressure, and heart rate.

Policyholders then upload their health data via wearable devices. As health initiatives reduce disease incidence, insurers’ risks are mitigated, enabling them to offer greater premium discounts to policyholders.

Statistics show that users participating in the interactive program experienced a 68% reduction in claim rates and a 60% decrease in policy surrender rates, resulting in substantial profits for John Hancock Life Insurance. This program also offers tangible benefits to policyholders: participants saw an average premium reduction of 10%, with potential annual savings of up to $600 on health food purchases.

Under this model, the interests of insurance companies, health management firms, and policyholders are aligned, moving away from the traditional zero-sum game. Meanwhile, this model enables up to 576 interactions per year between policyholders and insurers, far exceeding the mere two or three annual interactions typical under conventional insurance models.

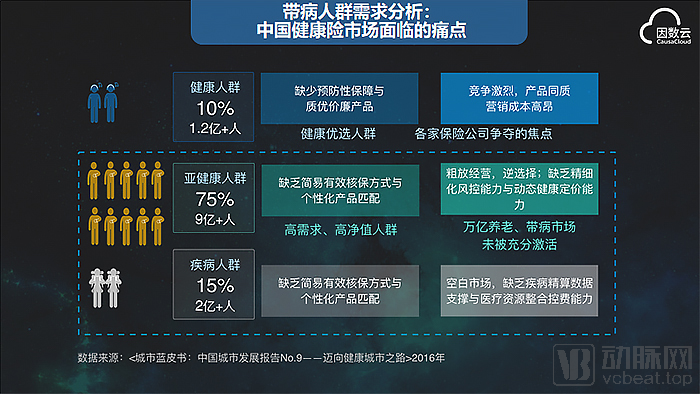

Insuring individuals with pre-existing conditions represents another strategic direction. According to statistics from the 2016 publication *Blue Book of Cities: China Urban Development Report No. 9 – On the Path to Healthy Cities*, only 10% of China’s population, approximately 120 million people, are considered healthy. This segment has become the primary focus of insurance companies, resulting in extremely fierce competition.

Relatively speaking, the sub-healthy population accounts for as high as 75% of the total population, presenting a broad market outlook and constituting a blue ocean market. Within this sub-healthy demographic, there is in fact a significant number of high-demand, high-net-worth individuals whose effective needs, including elderly care requirements, have not been adequately met.

Meanwhile, 15% of the patient population has no insurance coverage at all. This is largely due to insurers’ general lack of disease-specific actuarial data and limited ability to integrate medical resources for cost containment.

With the integration of technology, critical illness insurance and disease-specific insurance have emerged in the past one to two years. This has introduced a new dimension for policyholders—standard risks (healthy individuals) and substandard risks (non-healthy individuals)—enabling more granular segmentation of the insured population and filling previous market gaps.

Take breast cancer as an example. Traditionally, breast nodules have been considered a precursor condition to breast cancer; therefore, insurance products often list breast nodules as exclusions. However, by conducting comparative studies between high-risk populations and control groups using real-world data and analyzing the results with artificial intelligence algorithms, the industry has discovered that breast cancer actually involves numerous risk factors.

The impact of breast nodules on the incidence rate of breast cancer is even lower than that of DFI, which allows insurance products to exclude breast nodules from exclusion conditions and set appropriate premium rates for underwriting.

In November 2019, Causa Cloud partnered with Sunshine Life Insurance to launch a medical insurance product for specific pediatric hematologic diseases, significantly mitigating the financial risks associated with such conditions in children. The product’s design leverages big data and artificial intelligence to perform statistical analysis and actuarial calculations on real-world cost data, thereby lowering premium thresholds through a specialized coverage model tailored to specific diseases.

Causa Cloud is still exploring recurrence insurance for critical illnesses such as breast cancer. Statistics show that the probability of recurrence within five years after surgery remains high for breast cancer patients. Therefore, these patients are highly concerned about the risk of recurrence following their operations.

How can we provide insurance coverage for this population, leveraging insurance mechanisms to incorporate regular health check-ups and face-to-face consultations with physicians, thereby reducing the risk of recurrence? Causa Cloud is currently collaborating with insurance companies to explore such solutions.

“The population in China that truly needs protection has not actually been well served by insurance products. Leveraging our disease knowledge graph and specialty-specific disease models, we can analyze individuals previously deemed uninsurable, price their associated risks, and implement health management programs. As a result, we have made significant explorations in product development, including specialty-specific insurance and insurance for those with pre-existing conditions,” said Li Wei, introducing Causa Cloud’s initiatives in specialty-specific insurance.

Consequently, innovative insurance products such as coverage for individuals with pre-existing conditions or disease-specific policies, along with risk-based pricing and health management services, have become feasible through technological empowerment. As a health insurance technology company, Causa Cloud has conducted tens of billions of training iterations on its disease knowledge graph over the past five years. This has enabled the gradual development of its proprietary “Medical Brain,” which possesses the capability to implement risk-based pricing for populations with specific diseases or those in a sub-health state.

Nevertheless, Li Wei candidly acknowledged that the road ahead remains long. “Insurance for pre-existing conditions or disease-specific insurance is still in an exploratory phase and has not yet achieved scale; however, I believe this is a trend, though it will take time.”

Marketing

Technology-driven marketing in health insurance is primarily reflected in the screening of policyholders. Traditional insurance sales channels include agent-based and online channels, with the online model aiming for rapid, large-scale transactions, ideally targeting standard risks (healthy individuals).

Therefore, insurance products offered through internet channels are characterized by simple underwriting rules, clearly defined and non-refundable premiums, and relatively affordable prices, facilitating rapid transaction completion.

For certain applicants with questionable risk profiles, such as those with thyroid nodules, many insurers opted to decline coverage prior to the availability of medical big data statistics. In fact, data analysis reveals that thyroid nodules do not necessarily progress to thyroid cancer.

Meanwhile, patients with thyroid nodules may not even be aware of their condition, let alone know the TI-RADS classification of their nodules (with Category 4 indicating thyroid cancer). A definitive diagnosis can only be established through medical testing at healthcare institutions.

So, under what circumstances do thyroid nodules develop into thyroid cancer, and what is the proportion? Without statistical data, pricing is impossible. Causa Cloud, through intelligent data analysis, can inform insurance companies which previously declined applicants can be covered by increasing premiums, thereby meeting the insurers' business goals of revenue growth.

Causa Cloud has developed an online intelligent underwriting system. This “Intelligent Insurance Application Robot” is an interactive Q&A bot that helps insurance companies determine which substandard risks are eligible for coverage through interactive questionnaires. Compared with manual underwriting, the Intelligent Insurance Application Robot offers two advantages: 24/7 uninterrupted underwriting and improvement of the average underwriting quality across different underwriters.

Based on Great Wall Life Insurance’s operational experience, the trained intelligent underwriting bot can improve underwriting efficiency by 40%–60%, with an accuracy rate consistently exceeding 90%, comparable to that of experienced underwriters. Currently, this system has served nearly 20 insurance companies.

Operations

Medical big data and artificial intelligence can empower the operations of insurance companies. Taking underwriting as an example, medical records or physical examination reports provided by applicants in the form of images require authorization before they can be processed through OCR and medical data handling to generate standardized codes. This process is, in fact, highly challenging.

Medical data representation has not achieved full standardization. It took a prolonged effort, involving hundreds of engineers and medical annotators, for the industry to consolidate various expressions of disease diagnoses into unified ICD code groups.

Through medical data processing, these data are transformed into computable formats, ultimately forming a disease assessment model. By integrating this model with the underwriting rules of insurance companies, underwriting conclusions can be derived.

Intelligent underwriting is highly valuable for insurance companies, particularly during periods of rapid business growth when manual underwriting becomes overwhelmed. Artificial intelligence can rapidly provide underwriting decisions, requiring human reviewers only to conduct final verification.

Causa Cloud offers an OCR-assisted intelligent platform for medical data. By leveraging data annotation from medical experts and algorithm engineers, along with machine learning techniques, the platform delivers structured, normalized, and de-identified data outputs.

Meanwhile, this platform also offers certain auxiliary diagnostic capabilities. The system can cross-check the diagnoses, medical terminology, and medication orders entered by physicians against real-world diagnoses from other clinicians, thereby preventing input errors that could render the data unusable.

Causa Cloud’s Intelligent Medical Underwriting Engine empowers underwriting systems with disease-awareness capabilities. By leveraging machine processing powered by a disease knowledge graph, the system can rapidly analyze imaging files from applicants’ medical records to facilitate underwriting. Currently supporting 80 common diseases, the system reduces the time required for underwriting decisions from the previous 5 minutes to just 2 minutes, improving efficiency by 40%–60%.

Health Management Services

Integrating health management services with products is currently a trend in technology-driven health insurance. Li Wei mentioned that the wearable ring under Causa Cloud has passed CFDA certification and can be used to monitor blood oxygen saturation and heart rate changes. The transmission of authorized data can assist doctors in making decisions and enable early detection of warning signs for severe and critical illnesses.

In addition to wearable devices, big data and artificial intelligence also provide significant added value to health insurance. Clover Health, a U.S.-based health insurer, leverages big data to serve individuals with chronic diseases. Although its policyholders are individuals with pre-existing conditions, the company utilizes big data technologies and machine learning to predict chronic disease outcomes. This enables effective health management for patients, reduces the incidence of severe and acute medical events, and simultaneously lowers insurance claim payouts.

From 2013 to 2017, Clover Health’s membership grew from a few thousand to 25,550, with operating revenue reaching $275 million in 2017.

In 2015, by collecting medical data from 7,000 members to effectively reduce the incidence of complications and acute symptoms, Clover Health halved its readmission rate, which dropped from 12% in 2014 to 6% in 2015; the blood glucose control rate among diabetic patients nearly doubled compared with the baseline year; and the blood pressure control rate among hypertensive patients increased by 18%.

Causa Cloud also provides services similar to those of Clover Health. Currently, Causa Cloud has partnered with insurance companies to jointly build a data intelligence platform for data-driven managed care health insurance. This platform comprises multiple modules, including customized insurance for specific diseases, intelligent risk control, intelligent claims processing, health management services, and expert medical services.

Causa Cloud also offers the Causa Membership Program for patients, integrating their medical, pharmaceutical, insurance, and health service needs. By partnering with healthcare institutions and pharmaceutical companies, the program aims to provide enhanced membership benefits for individuals with chronic conditions, promoting better health through comprehensive health management. This initiative represents a key strategic focus for Causa Cloud’s future development.

Privacy

Regarding data security and privacy protection, Causa Cloud places particular emphasis on these aspects. All data processed by the company is obtained with appropriate authorization and undergoes de-identification. Taking thyroid cancer as an example, the de-identified data only reveals the progression from thyroid nodules to thyroid cancer. This process enables the identification of disease risk factors, which are then utilized for actuarial calculations and pricing, thereby safeguarding the privacy of policyholders who obtain insurance coverage while managing pre-existing conditions.

Li Wei stated that many companies in the big data and AI industry currently pay insufficient attention to privacy, leading to a relatively chaotic market. Causa Cloud is committed to expanding its market on the premise of adhering to regulations related to data security and privacy protection, with the aim of promoting greater standardization in the industry.

Causa Cloud’s InsurTech Product Matrix, Focusing on Underwriting, Claims Assessment, Health Management, Precision Marketing, and Customization of Novel Health Insurance Products

In Closing

The rapid growth of health insurance in recent years has indeed been driven by technological empowerment. By leveraging wearable smart devices, big data, and artificial intelligence, Causa Cloud has injected significant momentum into the development of the health insurance sector through technology.

Over the past two years or so, Causa Cloud has partnered with nearly 30 insurance companies, most of which are small and medium-sized insurers; it also counts large insurers such as China Pacific Insurance, China Life Insurance, and People’s Insurance Company of China among its clients.

Li Wei stated that over the past four to five years, the company has invested heavily in artificial intelligence talent and built a data intelligence model called the “Medical Brain,” which constitutes its core competitiveness.

As an enabler of the health insurance ecosystem, Causa Cloud specializes in product design, rate setting, and risk management for specific diseases, empowering insurance companies to achieve refined operations. Meanwhile, Causa Cloud has never lost sight of its eight-character vision: “Equal Coverage, Safeguarding Health.”

“We should provide more coverage opportunities to those in need of protection, rather than focusing more on selecting healthy individuals,” said Li Wei.