ShanZhen Founder Wu Hongxing: 'Parents’ Health, Just ShanZhen' – Solving the Elder Care Dilemma for 400 Million Post-80s and Post-90s Chinese

Shanzhen

Operator of Internet Physical Examination Service Platform

Internationally, a region is considered to have entered an aging society when the population aged 60 and above accounts for 10% of the total population. By this standard, China entered an aging society around 1999. Over the past two decades, the proportion of China’s elderly population has doubled, resulting not only in significant pressure on national and social eldercare systems but also in increasingly prominent “eldercare anxiety” among the 400 million individuals born in the 1980s and 1990s. At the recently concluded VCBeat 2019 Top 100 Future Healthcare Companies Conference, Wu Hongxing, Founder and CEO of Shanzhen, shared his insights on eldercare issues.

Data shows that the majority of China’s population growth over the past decade has come from the elderly population. While attention is focused on the increasingly severe reality of aging, many overlook a critical fact: driven by the dual policies of family planning and the expansion of university enrollment, the children of these elderly individuals have undergone an irreversible demographic migration, moving progressively farther away from their aging parents.

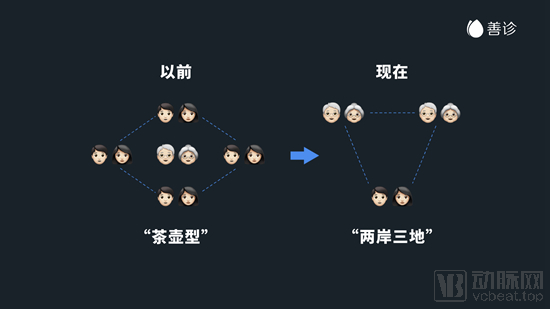

“As family structures undergo a fundamental shift from the ‘teapot’ model to the ‘cross-strait and three regions’ model, the elderly care patterns for the post-80s and post-90s generations will gradually transition from hands-on care by their children to purchasing professional services,” pointed out Wu Hongxing, founder of Shanzhen. He emphasized that aging is not a local variable but a global one, and the resulting market changes will be structural.

Fundamental Shifts in Family Structure

Shanzhen, founded by Wu Hongxing, is an internet platform that provides a one-stop parental health management solution for children working away from home. “We have been seeking efficient solutions to population aging. However, the user profile of Shanzhen consists mainly of young people working in first- and second-tier cities while their parents remain in their hometowns,” explained Wu Hongxing. “China has 400 million individuals born in the 1980s and 1990s. The families they form typically follow the ‘4-2-1’ model, where a couple supports one child while also caring for four elderly parents, resulting in immense pressure. A typical application scenario for Shanzhen’s solution is as follows: Children pay an annual fee, and Shanzhen provides their parents with one-stop services—including health checkups, health management, and insurance payment support—within a specified period.”

Separating the payers of elderly care services (i.e., children) from the service recipients (i.e., parents) has, to some extent, stimulated the demand for health services among the elderly population. By the end of 2019, Shanzhen had cumulatively served 6 million users, extending its service coverage to more than 270 prefecture-level cities across China, and establishing a network that enables working children in higher-tier cities to manage the health needs of their parents residing in lower-tier cities.

“Young people want to know their parents’ true health status, while also seeking solutions should any health issues arise.” In 2019, Shanzhen collaborated with the industry to launch senior medical insurance specifically designed for the elderly, providing medical payment solutions to address potential risks associated with aging care. Since then, Shanzhen has successfully established a comprehensive closed-loop system to help children manage their parents’ health.

Population aging is not a phenomenon unique to China, but a common challenge faced by an increasing number of countries. Regarding elderly care solutions, China’s current pension insurance system, consistent with that of developed overseas nations, comprises three pillars: the basic pension scheme, enterprise supplementary pension schemes, and individual savings-based pension schemes. Currently, in terms of both scale and coverage, basic old-age insurance far exceeds enterprise supplementary pension insurance and individual savings pension insurance, resulting in extreme imbalance among the three pillars. In addition to the mounting pressure of elderly care, the most immediate issue brought about by population aging is the increased healthcare burden on society as a whole. Against the backdrop of the current pension supply landscape, how to improve the health status of the elderly population, identify scientifically sound and reasonable strategies to hedge against age-related disease risks, and prevent “poverty caused by illness” or “relapse into poverty due to illness” has become another topic worthy of exploration.

“Statistics from 2017 show that the elderly, accounting for 17% of the total population, consumed nearly 70% of medical expenditures. ‘If we assume that the proportion of the elderly population reaches 30% in the future, China’s medical expenses may face a structural deficit at that time, making innovation in the structure and model of the broader health industry essential,’ pointed out Wu Hongxing. The relative deterioration of demographic structure has opened up new avenues for thinking about the direction of health insurance innovation.”

Shanzhen Founder and CEO Wu Hongxing Delivers Speech at 2019 VB100

First, the timing of health management interventions is shifting from late to early. The law of large numbers applied in insurance implies that only a small minority can consume the premiums paid by the majority. Demographic analysis reveals an irreversible trend toward population aging, which will lead to a relative decline in the number of premium payers and a rise in the proportion of those utilizing healthcare services. “In the short term, reducing disease incidence is not feasible; the correct solution may lie in shifting from passive medical treatment to active preventive management.”

Under the passive healthcare model, patients are often already in the advanced stages of disease upon diagnosis. Taking diabetes as an example, patients typically seek medical attention only after complications such as foot gangrene or blindness have developed, incurring costs of hundreds of thousands of yuan without achieving a cure. Wu Hongxing believes that the core strategy to optimize this situation is to avoid waiting for diseases to worsen before seeking solutions, by advancing the timing of health management interventions. For instance, in the early stages of diabetes, routine tests such as glycated hemoglobin (HbA1c) and liver and kidney function assessments can be used to control the progression of complications. “Only in this way can we structurally improve medical efficiency and fundamentally address the problem of high healthcare costs.”

For health insurance, a proactive prevention-oriented health management model leads to higher upfront costs but reduced claims expenses. In Wu Hongxing’s view, the shift of cost expenditure for health insurance products from the backend to the frontend is emerging as a new trend. At present, market awareness of health insurance has become relatively mature. While the rapid influx of numerous players has driven swift expansion in the market size of health insurance, high loss ratios resulting from extensive and粗放 (rough) management have become a key pain point constraining the profitability of health insurance products. “Merely optimizing efficiency is not enough,” emphasized Wu Hongxing. “The health insurance industry requires structural adjustments to create new opportunities.”

On the other hand, against the backdrop of an accelerating aging population, there has been a substantial surge in demand for health insurance among elderly “non-standard” individuals. Risk control will become a key factor constraining the sustainability and profitability of health insurance products. Traditional static risk-control methods may need to shift toward more flexible and precise dynamic approaches to meet these emerging demands.

The key points of risk control in health insurance differ from those in property and life insurance, which focus on reducing the probability and amount of claims. Health insurance should enhance the ability to safeguard users’ health while improving claims efficiency. “Health insurance covers not only users’ financial status but also their capacity for a healthy life,” emphasized Wu Hongxing. “Our approach to risk control should extend beyond merely reducing the likelihood of claims to encompassing service capabilities in health management.”

In Wu Hongxing’s view, the core imperative for health insurance operators in driving market adoption of a product is not to establish extensive sales channels, but rather to precisely define the service structure covered by the product and strike a balance between traffic acquisition and monetization capabilities.

Based on statistical analysis of its proprietary health database for middle-aged and elderly individuals, Shanzhen found that approximately 64% of parents exhibited four or more abnormal findings in their medical examinations, while only 2% of elderly individuals who underwent health checkups had no abnormalities. Furthermore, health examination data indicate that one or more of the following conditions—hyperlipidemia, hypertension, hemorrhoids, arterial diseases, and diabetes—are prevalent physical abnormalities among the middle-aged and elderly population.

Health conditions exhibiting varying degrees of abnormalities make middle-aged and elderly individuals highly susceptible to being classified as “Non-standard Population". Although the average life expectancy in China has exceeded 77 years, most existing health insurance products in the insurance market set the maximum age limit for coverage at around 60 years. 'Individuals aged 60 to 80, who are at high risk of disease, are left without health insurance coverage. This severe imbalance between supply and demand not only places immense pressure on the social security system but also exposes every family to significant financial risks associated with elderly care,' said Wu Hongxing."

Therefore, Shanzhen has attempted to include “non-standard groups” within the scope of health insurance coverage by leveraging medical examination services and data risk control technologies, thereby creating value for users. By integrating health management services, it enhances user stickiness, ensuring that more elderly individuals have health protection while improving their overall health status at the source through measures such as health management, thus minimizing the elderly care risks faced by their children. According to Wu Hongxing, Shanzhen helps the insurance industry improve its “Non-Standard Population“Health risk identification and pricing capabilities, collaborating with insurance companies to launch health insurance products specifically designed for the elderly—elderly medical insurance—and making them available for sale on multiple internet channels.

In the design of medical insurance for the elderly, Shanzhen has leveraged its physical examination network to transform the traditional risk control logic of health insurance, which previously defined insurable populations based solely on age. By incorporating multi-dimensional data and refining user health profiles on an individual basis, Shanzhen aggregates data across various levels to precisely define the scope of coverage.

Wu Hongxing stated that in 2020, Shanzhen would further upgrade its risk control capabilities and integrate a wide range of practical and effective health management services into its health insurance products, thereby enhancing user experience and boosting “Non-standard Population” health management adherence, further collaborate with the insurance industry to enrich elderly health insurance products, and based on more efficient risk and liability management, enable more high-age “non-standard groups” to benefit, provide better insurance for more elderly people, and alleviate the concerns of the post-80s and post-90s generations striving away from home.