2019 Global Healthcare Investment & Financing Report: 2,449 Deals, $47.3B Raised, and 140 IPOs

Perceptive Advisors

Private Hedge Fund Sponsor

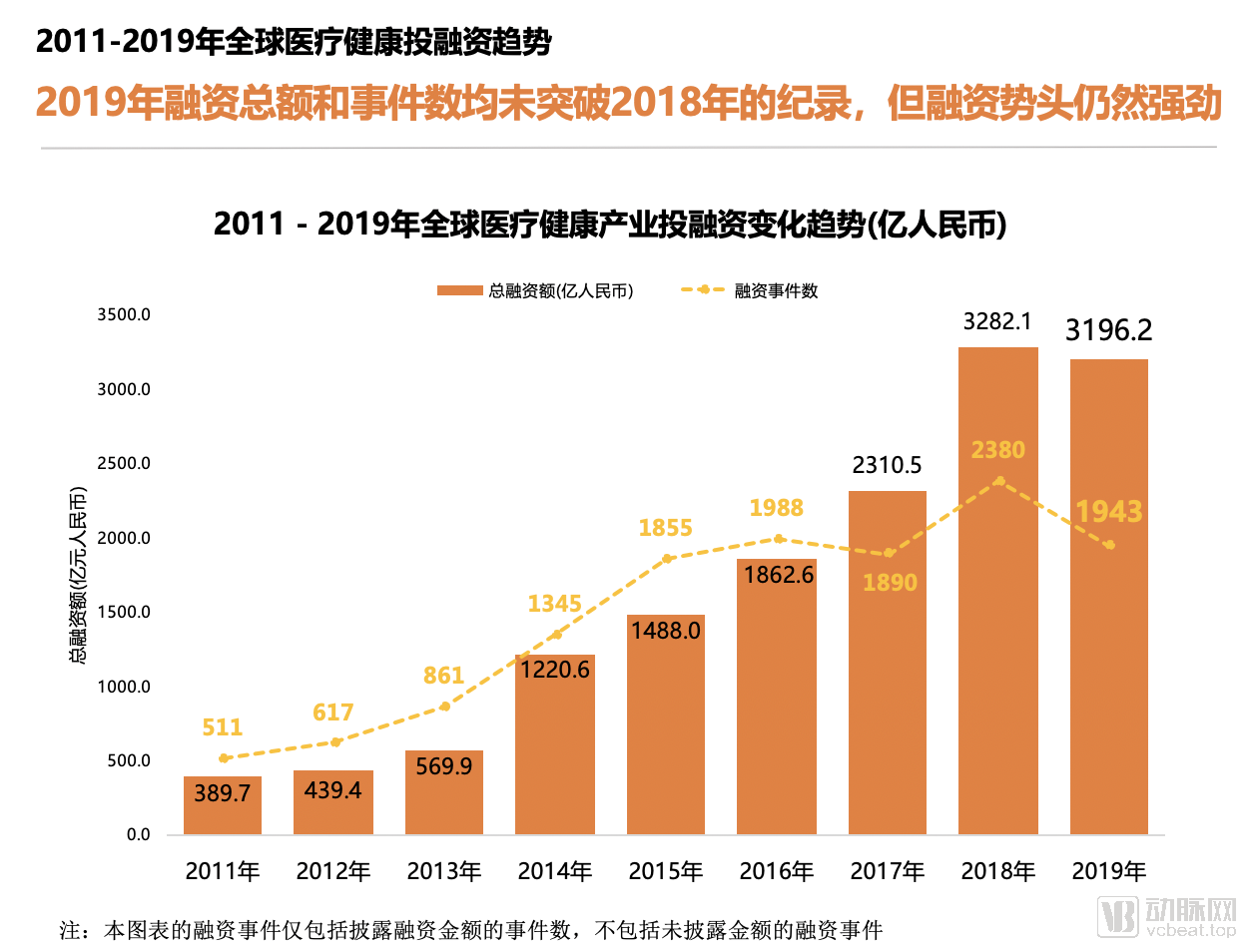

I. In 2019, both the total amount of global healthcare investment and financing and the number of deals declined, failing to surpass the 2018 record; however, the financing momentum remained strong.

II. In 2019, the number of investment and financing deals in China’s healthcare industry dropped sharply, yet the total funding amount remained the second highest on record.

III. In 2019, the hottest areas in the field of biotechnology abroad were neurological diseases, the microbiome, women's health, and mental health, which emerged as new highlights.

IV. In 2019, domestic healthcare and pharmaceutical financing in China reached its highest level, with medical device projects being the most numerous; innovative oncology drugs and health insurance emerged as new highlights.

V. Among the top 10 most active global healthcare investment firms in 2019, three were from China; these firms consistently favored new drug development and biotechnology.

VI. In 2019, a total of 136 companies were listed on the US, Hong Kong, and A-share markets, with an average time from establishment to listing of 9 years and 8 months, and an average stock price increase of 47%.

VII. Top 10 Global Healthcare Financing Deals of 2019: Two Chinese Companies Make the List, with JD Health Leading the Pack Through Its Over $1 Billion Series A Financing Round

Total Global Healthcare Financing Volume and Number of Deals Both Failed to Surpass 2018 Records, but Financing Momentum Remains Strong

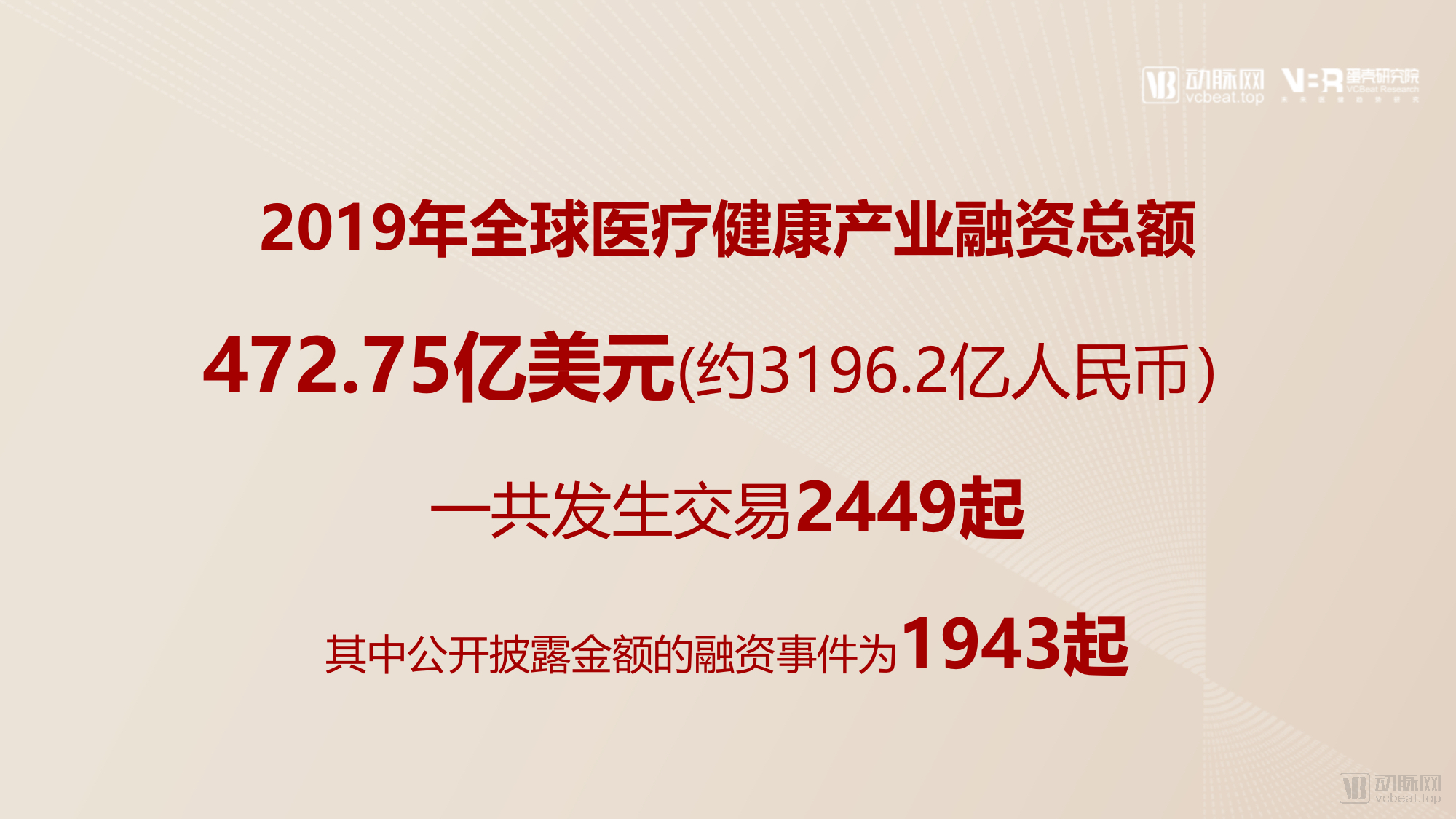

In 2019, a total of 2,449 financing deals occurred in the global healthcare industry, with 1,943 deals disclosing the amounts publicly. The total financing amount reached USD 47.275 billion (approximately RMB 319.62 billion).

After seven consecutive years of growth, total global healthcare financing experienced a slight pullback, with the number of financing deals declining by 18.4% year-on-year; nevertheless, both the financing volume and the number of deals remained at their second-highest levels in history.

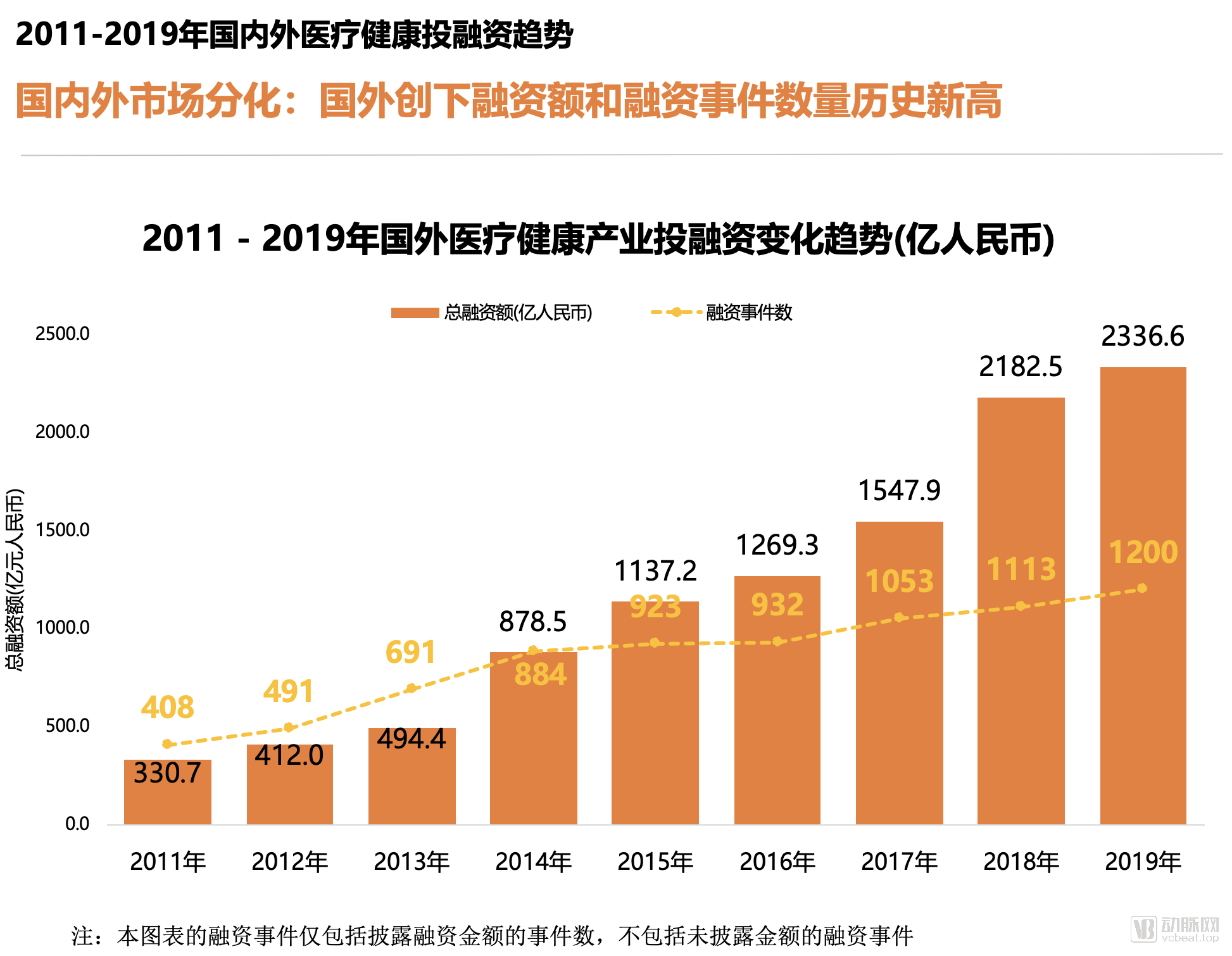

Overseas Markets Set New Records for Total Financing Amount and Number of Financing Deals

In 2019, healthcare investment and financing trends in China differed from those abroad.

Abroad, the healthcare industry continued to thrive in 2019, with total financing increasing for the eighth consecutive year. Despite a slowdown in growth rate, it reached a historic high of $34.561 billion (approximately RMB 233.66 billion). The number of financing events also hit a record high of 1,366 (of which 1,200 had publicly disclosed amounts).

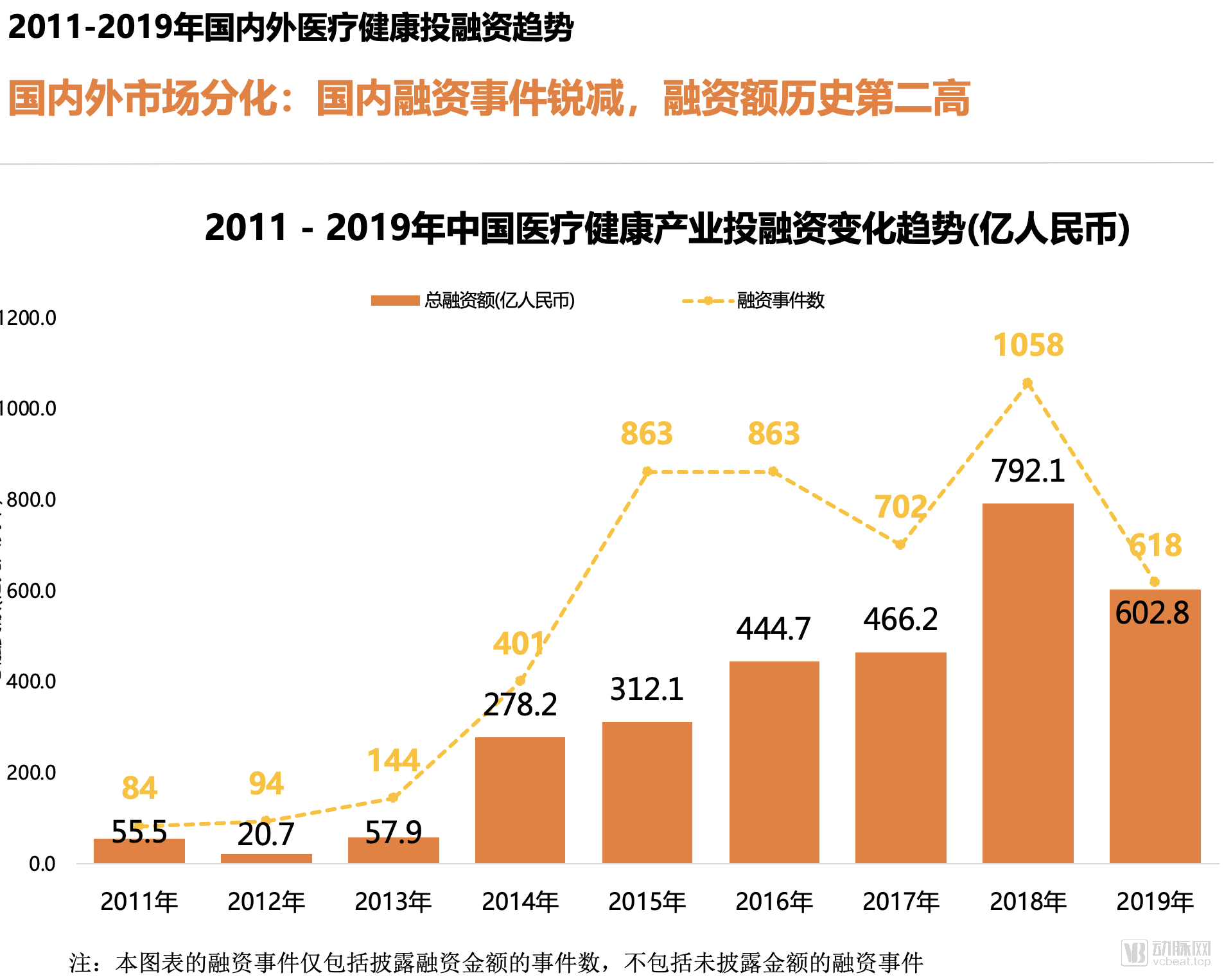

China’s Financing Events Plummet, Yet Total Funding Remains Second-Highest in History

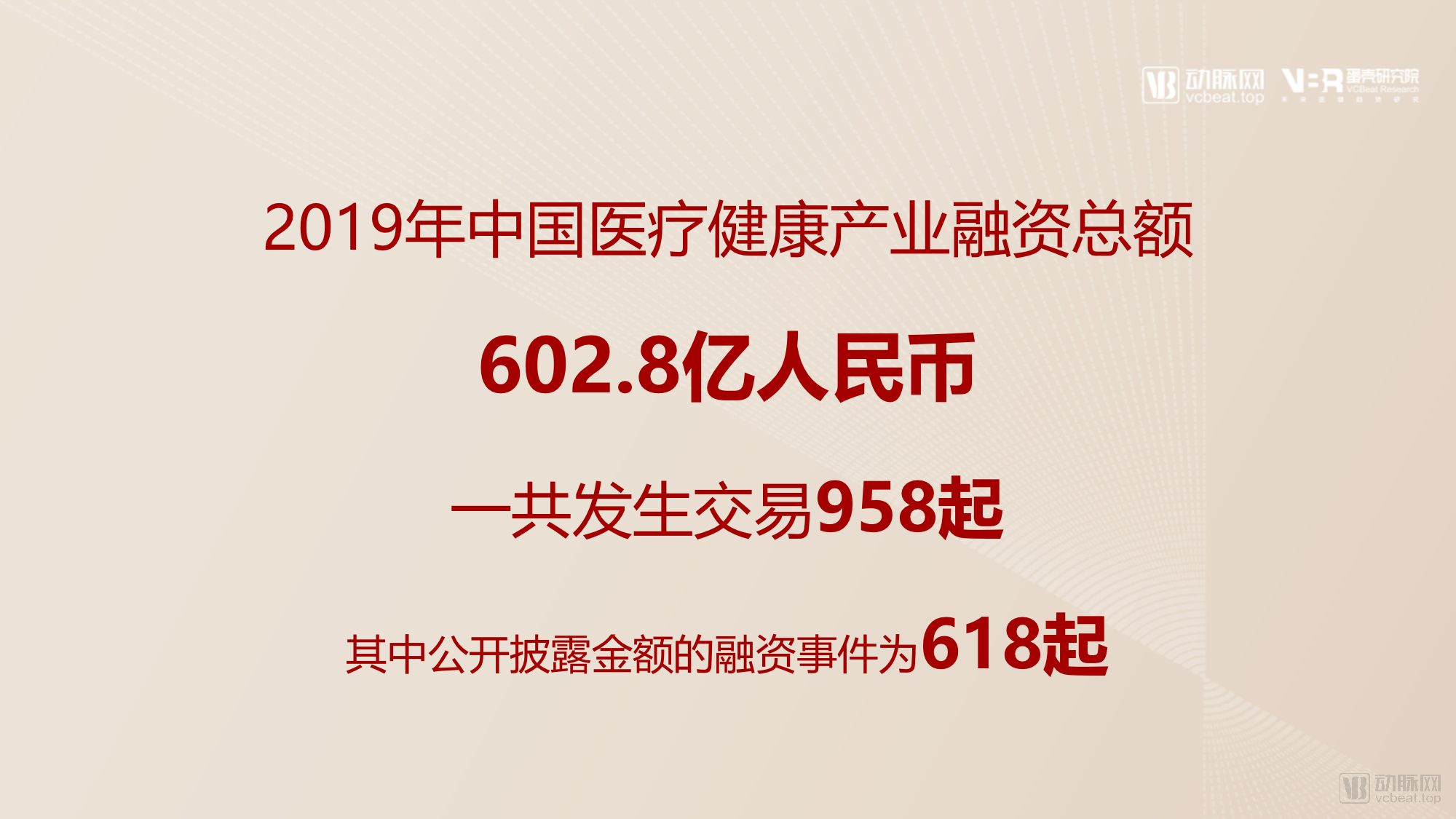

Compared with overseas markets, the domestic investment and financing landscape in 2019 was relatively severe. China’s healthcare industry witnessed a total of 958 financing events (618 of which publicly disclosed amounts), marking the lowest level since 2015 and nearly halving compared to 2018. The total financing amount reached RMB 60.28 billion, a year-on-year decrease of 24.6%, yet it remained the second-highest in history.

Amid the broader capital market environment in China, investors have become more cautious in their decision-making, making it increasingly difficult for Chinese healthcare startups to secure financing.

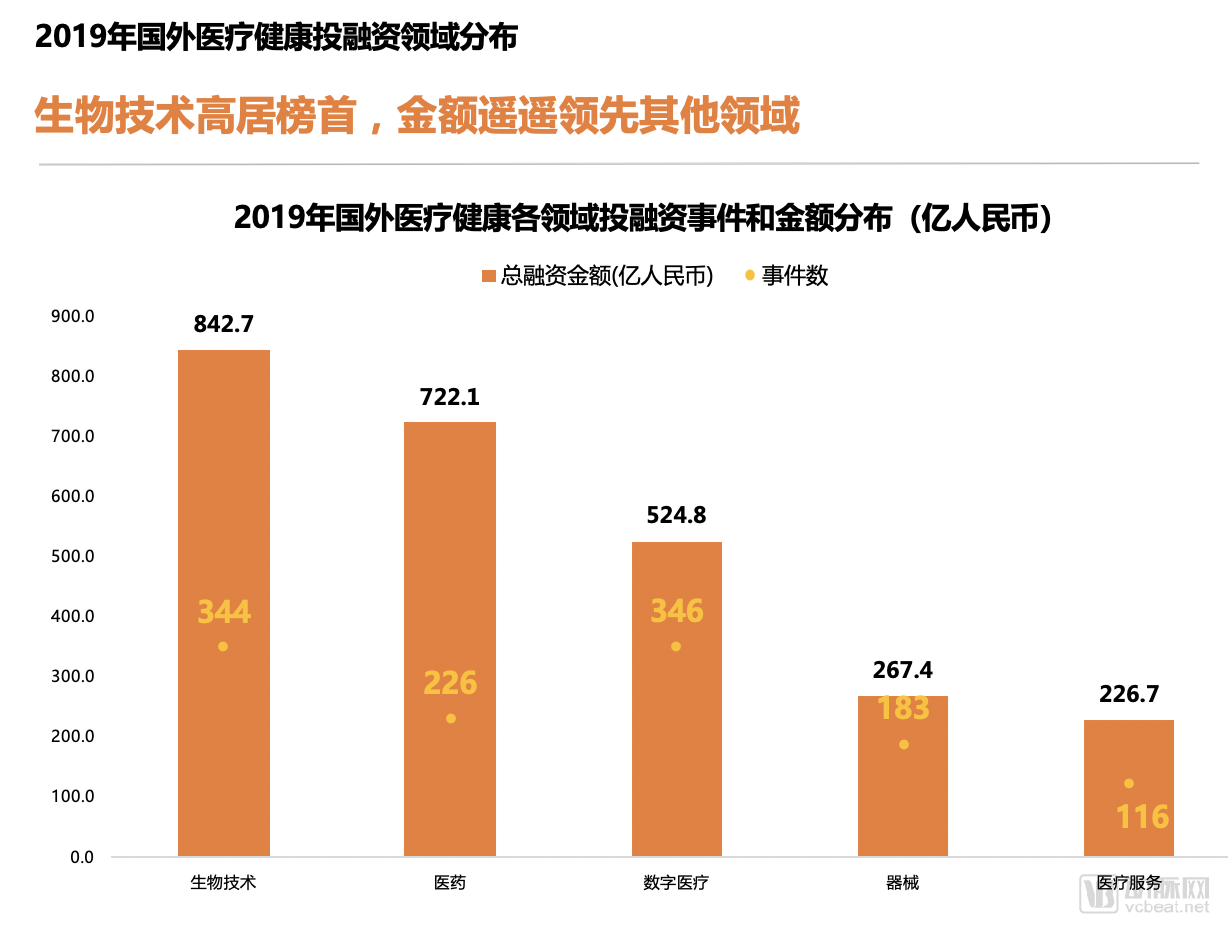

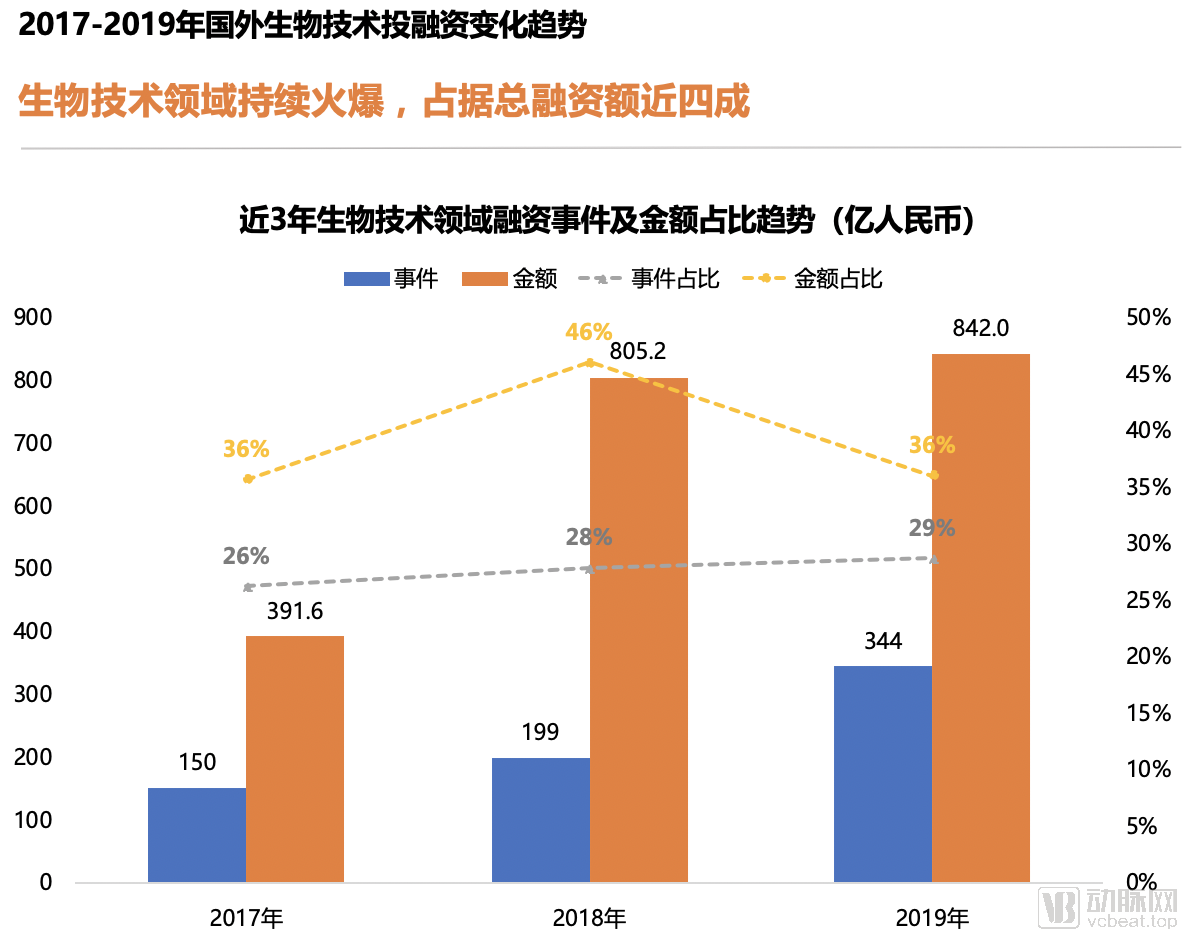

Biotechnology Tops the List, Far Ahead of Other Fields

Biotechnology emerged as the hottest sector for healthcare investment and financing abroad in 2019, with total funding reaching $12.465 billion (approximately RMB 84.27 billion), accounting for about 36% of the total financing amount.

There were 346 financing events in the digital health sector, making it the most active area for foreign investment in 2019.

Over the past three years, the average annual proportion of financing amount in the foreign biotechnology sector has exceeded 35% of the total financing amount; meanwhile, the proportion of financing events has steadily increased year by year, maintaining a strong development trend.

Financing and investment in the biotechnology sector are dominated by experienced investors who have invested in the field two or more times, while new investors who have invested only once account for a smaller share. The proportion of experienced investors remains stable, with over 20% of institutions investing in the sector two or more times each year.

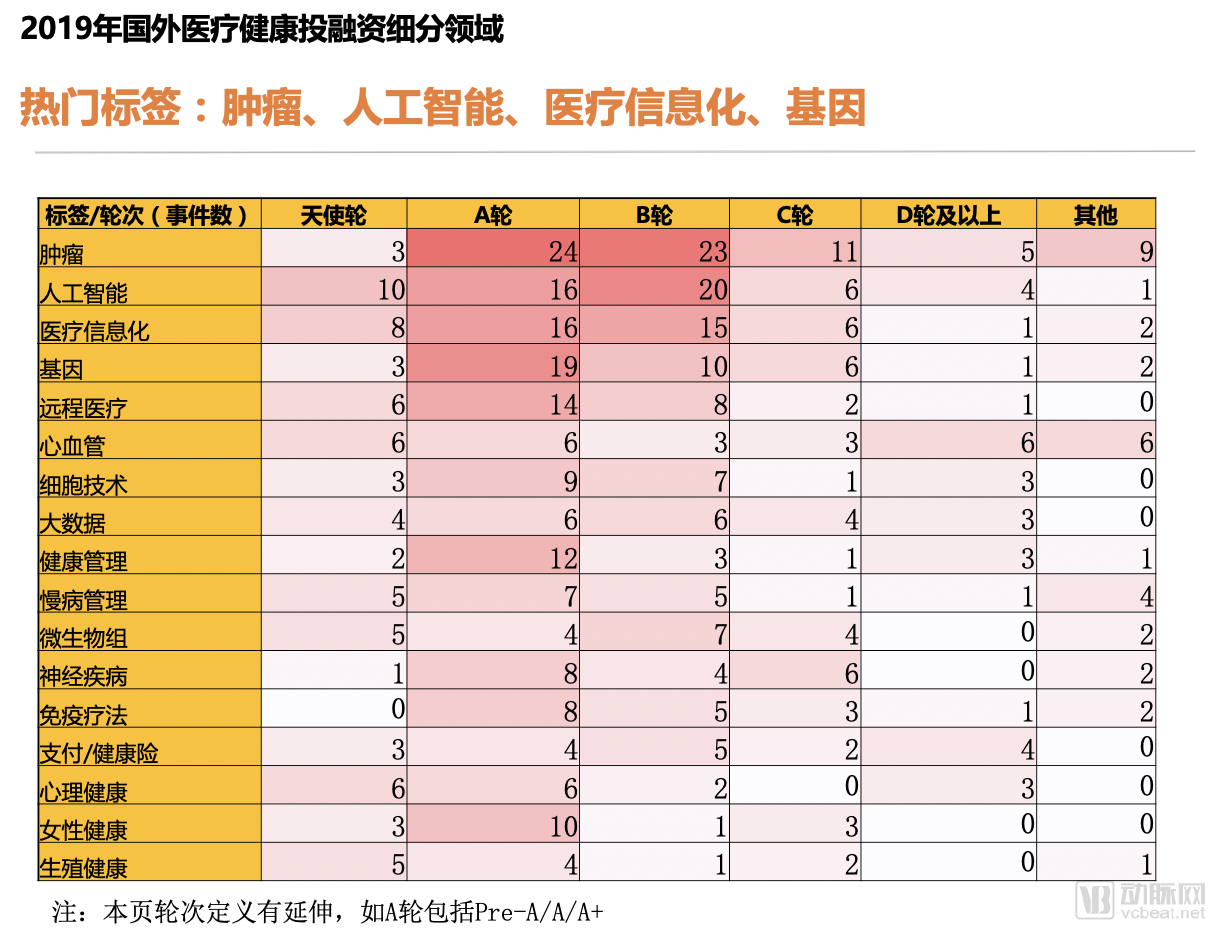

#Hot Tags: Oncology, Artificial Intelligence, Healthcare Informatics, Genes

In 2019, topics such as oncology, artificial intelligence, healthcare informatics, and genomics garnered significant attention abroad.

From immunotherapy and cell therapy for tumors to the application of gene technology, the deepening integration of artificial intelligence scenarios, and the rise of emerging niche sectors such as women’s health and mental health, a global trend is emerging toward bidirectional precision innovation in both technologies and models of healthcare solutions.

2019 Overseas Investment Highlights by Sub-sector: Neurological Disorders, Microbiome, Mental Health, Women's Health

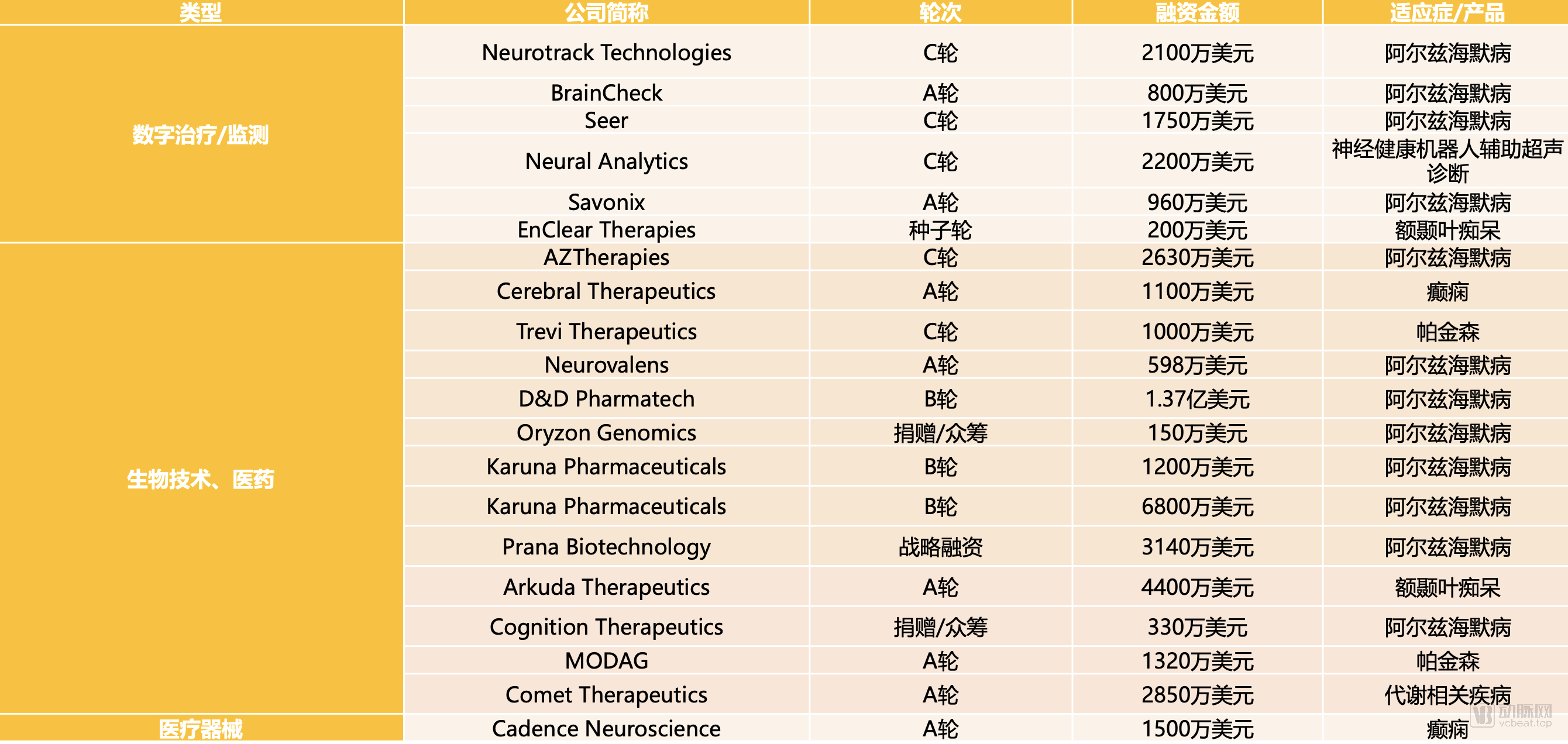

2019 Overseas Funding Projects for Neurological Disorders

As new drug development for neurological disorders has repeatedly encountered setbacks, therapeutic options remain limited and clinical outcomes have been less than satisfactory, with few breakthroughs in recent years. However, as industry understanding of neurological diseases has become increasingly clear, pharmaceutical giants that previously failed are returning to the field; coupled with the continuous advancement of clinical trials by innovative companies and the rise of digital therapeutics, 2019 saw a significant number of financing projects focused on neurological diseases.

These companies fall primarily into two categories: digital health companies focused on brain health and the prevention of neurocognitive disorders, and pharmaceutical R&D and biotechnology companies targeting neurological diseases.

2019 Overseas Microbiome Financing Projects

In 2019, a total of 32 microbiome companies abroad completed financing rounds, with most being in early stages, including five seed-stage companies, indicating that emerging forces are continuously entering this field.

Most microbiome startups are focused on gut microbiota research. Although no products have yet reached the market, successive scientific discoveries have illuminated the promising future of microbiome-based therapies. Conditions such as cancer immunotherapy, Alzheimer’s disease, diabetes, and obesity represent either significant unmet medical needs or vast market opportunities. Driven by these factors, investment interest in microbiome therapeutics is gradually intensifying.

2019 Overseas Mental Health Financing Projects

In 2019, there were a total of 19 financing events related to mental health abroad, primarily at the seed and Series A stages. These companies mainly focused on areas such as online psychotherapy, chatbot development, and mental health assessment.

According to the World Health Organization, depression is currently the fourth leading cause of global disease burden and is projected to become the second largest contributor, surpassed only by cardiovascular diseases. In an environment where pharmacological treatments yield limited efficacy, innovations in mental healthcare are extending into the digital health sector, encompassing digital therapeutics and mental health services.

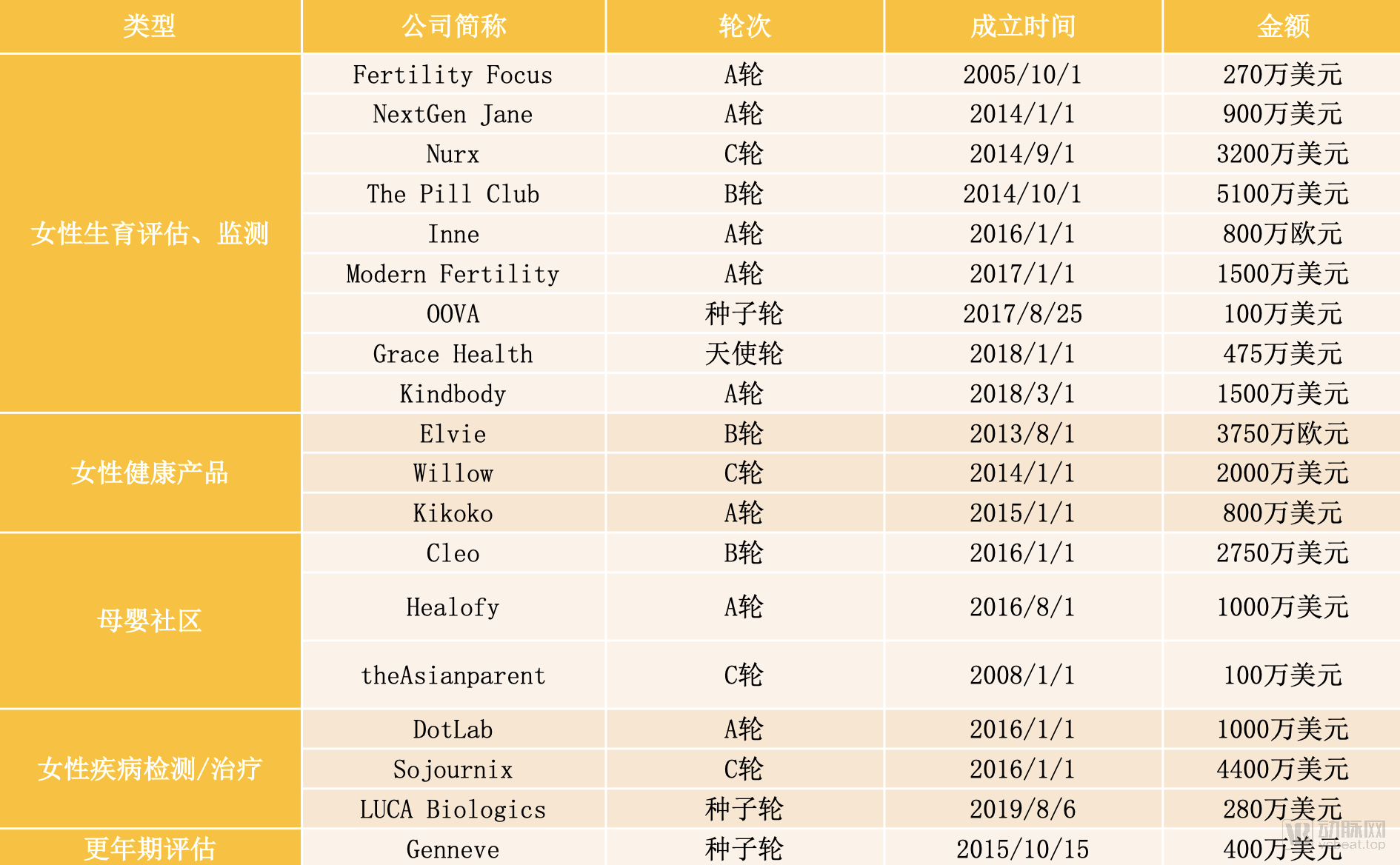

2019 Overseas Financing Projects in Women’s Health

In 2019, there were a total of 19 financing deals related to women’s health overseas, primarily at Series A. Among these, the largest financing round was $52 million raised by Nurx, a home HPV testing company. Currently, some startups are establishing direct-to-consumer (D2C) connections with patients through telemedicine models. With the emergence of digital diagnostics and biomarkers, new solutions will address women’s health issues in a more targeted manner, particularly in the area of reproductive health.

Medical device projects were the most numerous, while pharmaceutical fundraising reached the highest amount.

The overall trends in China’s healthcare investment and financing market in 2019 remained consistent with those of 2018, with the medical devices sector recording the highest number of financing deals, while the pharmaceutical sector attracted the largest total funding amount. In 2019, China’s digital health sector experienced robust growth, with 82 financing deals raising a cumulative total of RMB 19.01 billion. Notably, JD Health contributed nearly 30% of the total digital health funding through its standout Series A round, which exceeded USD 1 billion.

Highlights in Subsectors of China’s Healthcare Investment and Financing: Innovative Oncology Drug R&D and Health Insurance

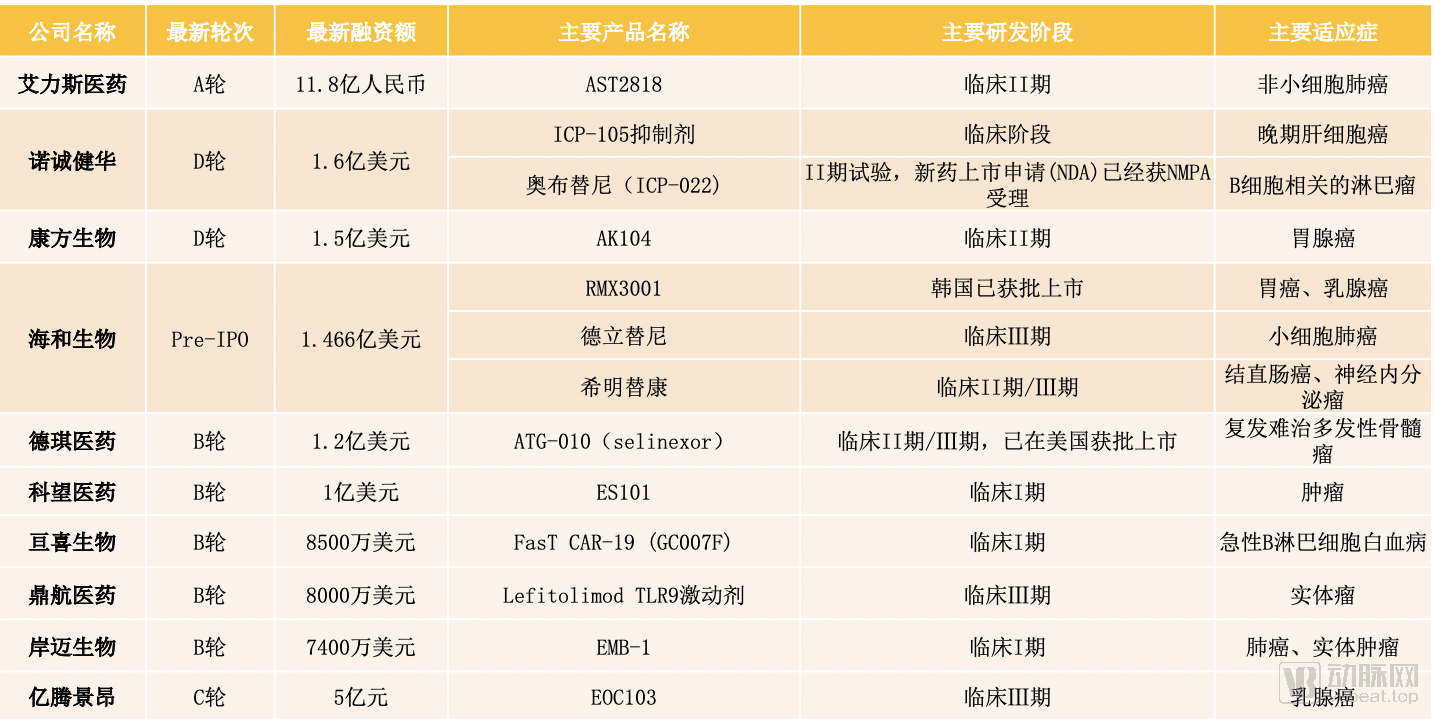

Top 10 Oncology Innovative Drug Companies with the Highest Financing Amounts in China in 2019

In 2019, within the pharmaceutical industry—which secured the highest total funding—oncology was the most prominent therapeutic area, with immunotherapy garnering significant attention.

In line with policy trends, pharmaceutical innovation remained the keyword for 2019. The Vaccine Administration Law and the newly revised Drug Administration Law were promulgated and came into effect on December 1, 2019. These laws encourage innovation through higher-level institutional design and establish regulatory oversight over the entire lifecycle of drugs and vaccines.

2019 Financing Projects of Chinese Health Insurance Companies

On the same day, three companies announced financing rounds; one company secured funding three times within a single year, with the largest single round exceeding RMB 1 billion. Major investors including Sequoia China, Alibaba, and Tencent entered the fray.Undoubtedly, health insurance emerged as a dark horse in China’s healthcare investment and financing market in 2019.

According to data from the China Banking and Insurance Regulatory Commission (CBIRC), the health insurance market achieved a compound annual growth rate (CAGR) of 35.95% from 2013 to 2018, with premium income reaching RMB 544.813 billion in 2018. Based on this growth trajectory, the market size is projected to surpass the RMB 1 trillion mark by 2021 at the latest.

Three Chinese Firms Among Top 10 Most Active Healthcare Investors in 2019

In 2019, Perceptive Advisors was the most active global investor in healthcare and medical services, with a total of 24 investments throughout the year. Its frequent investment areas included genetic testing, cancer screening, and oncology drug development.

Qiming Venture Partners, Lilly Asia Ventures, and Sequoia Capital China entered the TOP 10.

Most active investment firms share a common focus on biotechnology and new drug development; GV and F-Prime Capital Partners are particularly attentive to the digital health sector.

F-Prime Capital was the most active investor in the digital health sector in 2019, investing in a total of 14 digital health companies throughout the year, with a focus on areas such as artificial intelligence and big data.

The landscape of active investors in the healthcare and medical industry has remained relatively stable over the past five years, with the vast majority of institutions appearing on the list more than twice; OrbiMed, in particular, has been ranked for five consecutive years. In 2019, foreign active institutions engaged in investment activities more frequently.

27 Companies Become Capital Favorites, Co-Invested by Two or More Active Institutions

Among the top ten healthcare investment institutions by number of investments in 2019, 27 companies received backing from two or more of these firms, reflecting the potential and strength of these startups.

Schrödinger and Insilico Medicine, both AI-driven drug discovery companies, have each garnered interest from three active institutional investors.

Beyond the perennial hotspots of oncology and gene technology in recent years, artificial intelligence and digital health have continued to advance, while capital investment in drug discovery for neurological disorders is experiencing a resurgence. Two neurotherapeutics companies, Blackthorn Therapeutics and Passage Bio, have both secured cross-investments from active institutional investors.

Notably, two biopharmaceutical companies, SpringWorks Therapeutics and Frequency Therapeutics, completed their Series B and Series C financing rounds, respectively, in 2019, and successfully went public through initial public offerings (IPOs) in the same year, achieving an exceptionally rapid capital exit in the pharmaceutical industry.

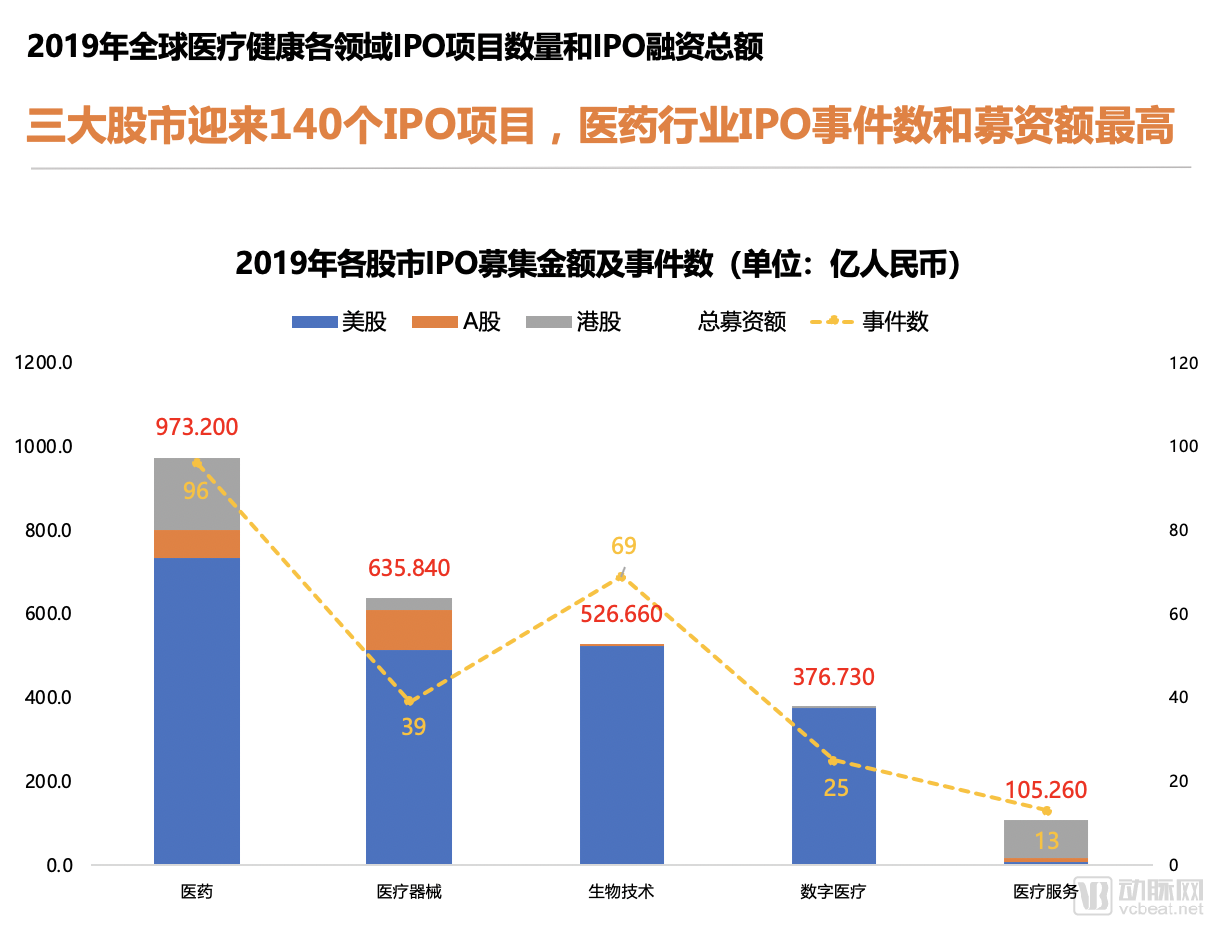

The Three Major Stock Markets Welcome 140 IPO Projects, with the Pharmaceutical Industry Leading in Both Number of IPOs and Capital Raised

In 2019, the three major stock markets—U.S. stocks, A-shares, and Hong Kong stocks—welcomed 140 newly listed healthcare companies. Among them, 102 were listed on U.S. exchanges, capturing an absolute majority of the total capital raised across the three markets; additionally, 20 companies were listed on A-shares, and 18 on Hong Kong stocks.

In terms of sector distribution, the sub-sectors with the highest total fundraising remained pharmaceuticals, medical devices, and biotechnology; meanwhile, the number of IPOs in biotechnology ranked second, trailing only pharmaceuticals.

Meanwhile, China witnessed a wave of initial public offerings (IPOs) among healthcare companies. Throughout the year, a total of 34 Chinese healthcare companies were listed on the STAR Market and the Hong Kong Stock Exchange.

On the morning of June 13, 2019, Chipscreen Biosciences successfully became the first biopharmaceutical company to list on the STAR Market. The launch of the STAR Market and the implementation of new listing rules for biotechnology companies on the Hong Kong Stock Exchange have accelerated the IPO pace of domestic biopharmaceutical enterprises. In the future, the number of listings in the biotechnology and pharmaceutical sectors is expected to achieve another breakthrough.

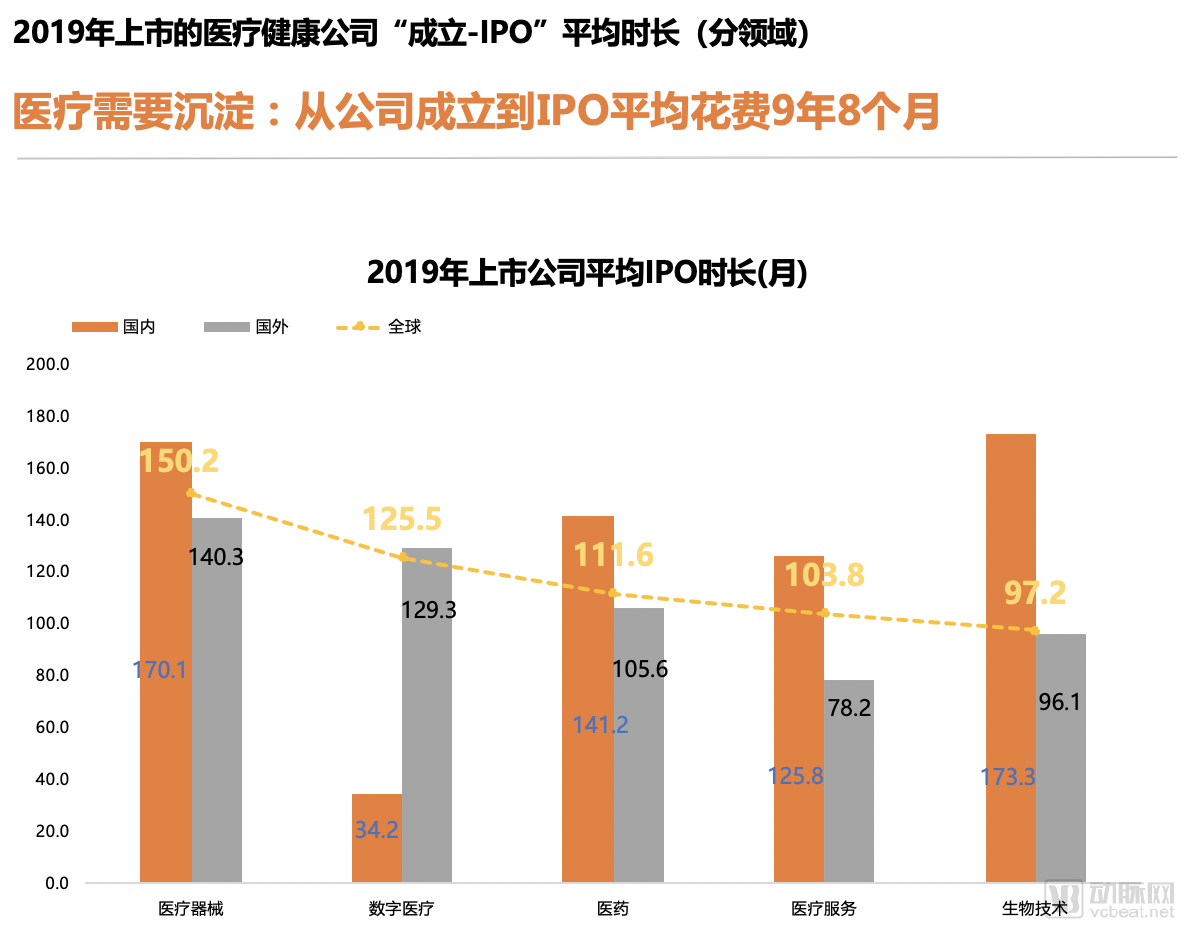

Healthcare Requires Accumulation: It Takes an Average of 9 Years and 8 Months from Company Founding to IPO

Among the 140 healthcare companies that went public in 2019, the average time from founding to IPO was approximately 117 months (9 years and 8 months). Even the fastest-moving biotechnology companies took an average of 8 years to list.

Compared with the average time to IPO for companies domestically and internationally, Chinese companies generally experience a longer duration, partly due to differing listing requirements across stock markets. The A-share market imposes explicit financial profitability criteria and entails a lengthier review process, whereas the U.S. and Hong Kong stock markets are relatively more flexible. However, with the establishment of the STAR Market, Chinese healthcare companies will have more flexible IPO options.

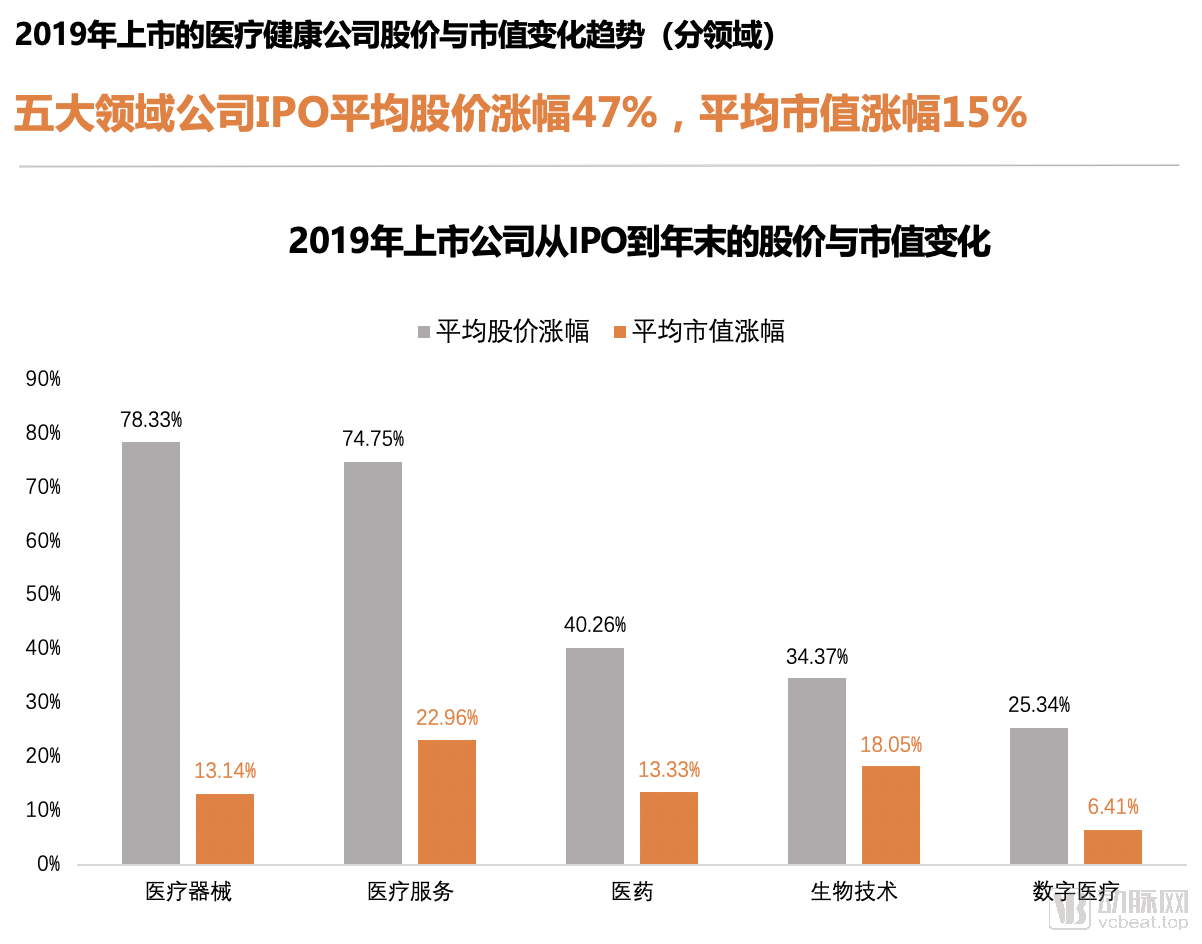

In 2019, the average share price of listed companies rose by 47%, and their market capitalization increased by 15%.

Among the 140 healthcare companies that went public in 2019, the average stock prices of companies across various sectors rose to varying degrees, with an average increase of 53%. Notably, both the medical devices and healthcare services sectors saw gains exceeding 70%.

The surge in stock prices within the medical device sector was primarily driven by the more than 200% gains of MicroPort NeuroTech and VitaFlow Medical, both listed on the STAR Market in 2019. Meanwhile, the rise in the healthcare services segment was largely attributable to Pharmaron, a CRO company listed on China’s ChiNext board in January 2019, whose stock price soared from RMB 7.66 at issuance to RMB 54 by year-end, representing a seven-fold increase within one year.

Compared with stock price fluctuations, the average increase in the company's market capitalization was relatively moderate, at 15%.

In 2019, the five countries with the highest total financing in the global healthcare investment and financing market were the United States, China, the United Kingdom, Switzerland, and France; the five countries with the most financing events were the United States, China, the United Kingdom, Israel, and Switzerland.

In 2019, the United States led the world with 647 financing deals and $18.3 billion (RMB 129.83 billion) in funding, followed closely by China. Together, the U.S. and China accounted for 78% of the total global financing amount and 81% of all financing deals.

Israel is one of the countries with the highest healthcare efficiency worldwide, boasting nearly 30 years of accumulated data from its healthcare system, 98% of which has been digitized. Although Israel’s funding volume was not high in 2019, it ranked fourth globally with 28 innovative projects, demonstrating particular prominence in the digital health sector. Companies such as Healthy.io, a smart urinalysis company, and Early Sense, a provider of smart hospital bed sensors, completed new rounds of financing.

In 2019, California, USA, recorded a cumulative total of 200 healthcare financing and investment transactions, raising $5.64 billion (approximately RMB 39.5 billion), making it the region with the highest frequency of global healthcare venture capital investments.

Massachusetts, leveraging its renowned biotechnology industry cluster and abundant medical resources, has surpassed the more economically developed New York to become the second-largest U.S. state for healthcare investment and financing, though it still lags far behind California in terms of scale.

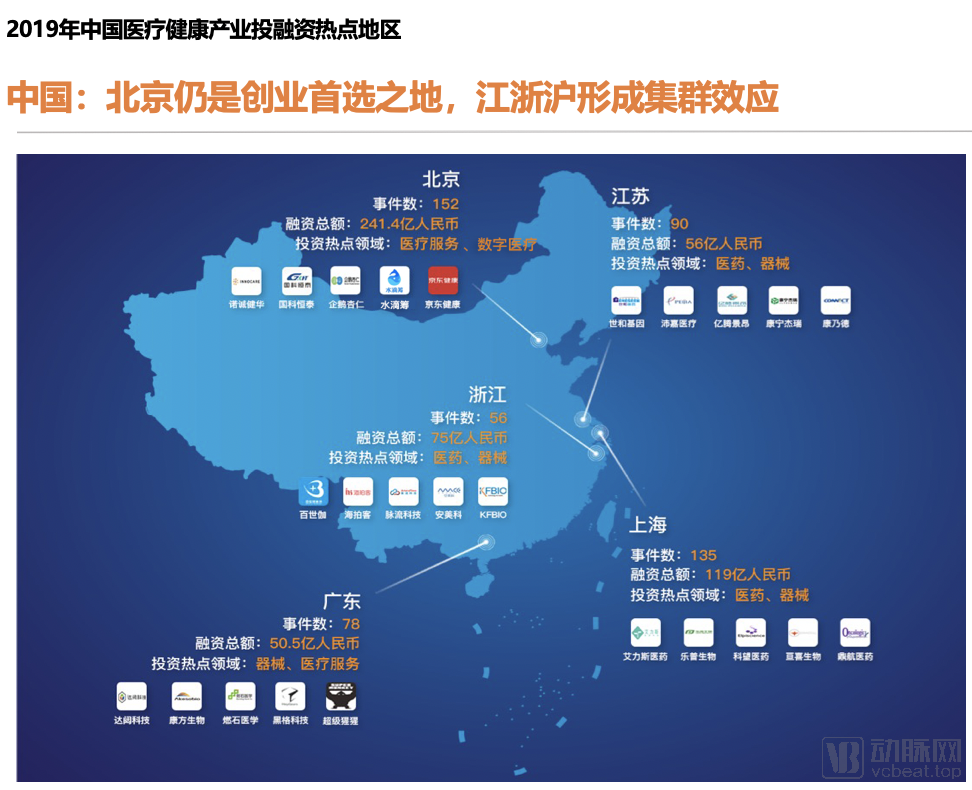

In terms of the scale of healthcare investment and financing in individual provinces and municipalities, the five regions with the most concentrated healthcare investment and financing activities in China in 2019 were Beijing, Shanghai, Guangdong, Jiangsu, and Zhejiang, in descending order.

Beijing has recorded a cumulative total of 150 financing events, raising RMB 22.45 billion, and remains the top choice for entrepreneurs. Notably, three companies that secured substantial funding—JD Health, Penguin Almond, and Waterdrop Inc.—are all headquartered in Beijing.

From the perspective of regional cluster development, the Jiangsu-Zhejiang-Shanghai region has seen its influence in the healthcare industry expand significantly in recent years, and is expected to form China’s largest healthcare industry cluster in terms of investment and financing scale.