Four High-Potential Directions for China's Commercial Health Insurance Industry in 2020

In 2020, commercial health insurance, estimated to reach a trillion-yuan market scale this year based on its growth rate, will undoubtedly remain a sector of intense focus across the entire industry.

At the end of 2019, VCBeat and FanZhuo Capital jointly released the “2019 Report on Innovative Commercial Insurance.” The report focuses on the entire industrial chain of commercial health insurance, employing a top-down framework to analyze the market size, driving factors, industry status, and competitive landscape, while also forecasting future development trends in commercial health insurance. This article presents selected excerpts from the report; the full text can be downloaded for free by scanning the mini-program code below.

Scan the Mini Program QR code to download the “2019 Innovative Commercial Insurance Report” for free.

The main points of the report are as follows:

1. Amid the trends of consumption upgrading and shifts in disease patterns, consumers’ awareness of protection has continued to rise. Coupled with the excessively high out-of-pocket share of medical expenditures in China and the mounting pressure on social security spending driven by population aging, there is substantial societal demand for commercial health insurance. Meanwhile, the government has introduced multiple policies that directly or indirectly create favorable conditions for the development of the health insurance industry.

2. With the development of the internet and technological advancements, a large number of innovative enterprises have emerged in the industry. Innovative opportunities within this sector are primarily concentrated in upstream TPA services, midstream product design, and downstream sales platforms.

Demand-Side Growth Driven by Consumption Upgrading, Shifts in Disease Patterns, and Aging Trends

A review of the history of the global insurance industry reveals that its prosperity requires a certain economic foundation. When per capita GDP ranges between $2,000 and $10,000, the premium growth rate can reach 15% to 20%. Once per capita GDP exceeds $10,000, the first wave of insurance industry boom emerges, with insurance penetration (total premium income/GDP) doubling and sustaining this level for more than five years. Over the past five years, China’s per capita GDP has risen from $6,214 to $9,195, placing it precisely at the threshold of the first phase of rapid development. This indicates that China’s insurance industry is poised to enter a period of sustained high-speed growth.

As the middle-income population expands, the driving force behind social consumption growth will shift from population growth to an increase in per capita consumption. This upgrade in consumption structure also encompasses the rising demand among the growing middle class for high-quality and diversified commercial health insurance products.

Commercial health insurance addresses people’s demand for overcoming illness and extending lifespan, and these persistently strong demands are also influenced by changes in the human disease spectrum. In 2019, The Lancet, a leading international medical journal, published a study on the burden of disease in China. The findings revealed that the diseases with the highest incidence and mortality rates in China are no longer lower respiratory infections and neonatal disorders, but rather chronic diseases, such as stroke and ischemic heart disease. These conditions are characterized by long disease courses and typically slow progression, resulting in substantial medical costs that impose heavy burdens on individuals and families and cause significant economic losses to society.

Furthermore, population aging has also led to a rapid increase in healthcare demand. Data from the National Bureau of Statistics indicates that in 2017, the elderly accounted for 17% of the total population but consumed nearly 70% of total healthcare expenditures. It is foreseeable that, given the basic medical security system’s difficulty in bearing the increasingly heavy burden of elderly care, the commercial health insurance industry will become an essential sector.

Amid Changing Trends in Basic Medical Insurance Payment Pressure, Supply-Side Expansion Is Urgently Needed

Although China’s current medical insurance system has been fundamentally established, the proportion of out-of-pocket medical expenditures remains excessively high, imposing a significant burden on residents. In 2018, individual medical spending accounted for 39.4% of total healthcare expenditure. Moreover, the conditions for utilizing medical insurance are numerous and relatively stringent: reimbursement is subject to deductibles and coverage caps, and only expenses falling within the scope of the “Three Directories” and “Two Designated Institutions” are eligible. Costs outside this scope, those exceeding the coverage cap, or those below the deductible threshold are all borne by patients as out-of-pocket expenses. Furthermore, some more targeted medications with superior efficacy but high prices are typically excluded from the reimbursement list, thereby undermining the protective function of the medical insurance system.

According to the China Healthcare Development Report 2017, it was projected that the basic medical insurance fund for urban employees would experience a current-period deficit in 2017, with cumulative reserves turning into a severe shortfall of RMB 735.3 billion by 2024. Meanwhile, research reports from Frost & Sullivan indicate that the basic healthcare system will face significant pressure in 2026, urgently necessitating the involvement of commercial health insurance.

Health insurance serves as an effective supplement to the basic social medical insurance system and represents a key direction for the future development of China’s healthcare industry. On one hand, commercial health insurance, as a source of social security, helps alleviate the financial burden on the national medical insurance fund and leverages market mechanisms to assist hospitals in controlling costs reasonably. On the other hand, given the limited scope and coverage limits of China’s basic medical insurance—which excludes non-disease treatment items, specific therapeutic procedures, certain drugs, diagnostic and therapeutic equipment, and medical materials—the introduction of commercial health insurance helps fill gaps in the high-end market. It provides tailored services for high-income individuals who prioritize efficiency and quality while remaining price-sensitive.

Policy-Driven Demand for Health Insurance

Since the establishment of the National Healthcare Security Administration in 2018, a series of pilot policies have been implemented to optimize healthcare insurance payments. Among these, Diagnosis-Related Group (DRG) payment reforms and volume-based procurement, which directly target cost containment, have created new development opportunities for China’s commercial health insurance industry.

The implementation of Diagnosis-Related Group (DRG)-based payment helps curb overdiagnosis and overtreatment, significantly reduces the scope for kickback-driven drug sales, and facilitates cost containment within the medical insurance system. The rollout of DRG pilots not only transforms the market for medical services and products but also impacts commercial health insurance. Within this sector, disease-specific insurance policies primarily offering fixed indemnity will remain largely unaffected, whereas expense-reimbursement medical insurance, particularly inpatient-only coverage, will face substantial disruption. Changes in medical insurance payment rules have led to shifts in user demand; consequently, medical insurance products developed under the previous payment framework are encountering new market trends and must adapt to evolving claims requirements.

Volume-based procurement policy represents a reform of the traditional hospital drug bidding model, which only bid on drug prices without specifying quantities. It requires manufacturers to submit and negotiate quotes after the specific drug procurement volumes of hospitals are clearly defined in advance. Currently, the scope of volume-based procurement has expanded to 27 provinces and the Xinjiang Production and Construction Corps. As a result, the average price of selected drugs in the "4+7" pilot regions decreased by 25%, while the average price reduction for proposed selected drugs in the expanded regions reached 59%.

Both DRG and volume-based procurement aim to optimize health insurance payments. This will prompt hospitals, driven by profitability concerns, to reduce direct prescription dispensing through hospital pharmacies and instead require patients to purchase medications from retail pharmacies on their own, ultimately increasing out-of-pocket expenses for patients. In this context, commercial health insurance will serve as a beneficial supplement to basic medical insurance and gradually become an essential need in the healthcare sector.

Technology-Driven Iteration and Upgrading of Commercial Health Insurance

Before the advent of big data, commercial data were often derived from passive survey forms and lagging statistical figures. The emergence of the big data era has made it possible to collect and process massive volumes of data. Compared with traditional statistical methods that extrapolate from samples to represent the entire population, results derived from big data analytics are more precise. In the health insurance industry, big data can be applied across multiple stages—including product design and pricing, risk control, optimization of claims services, and precision marketing—driving fundamental iterative upgrades for the sector.

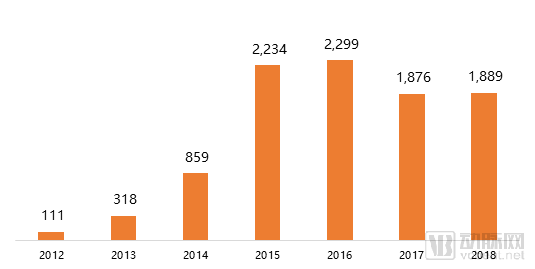

Furthermore, the widespread adoption of mobile internet has accelerated the establishment of user channels. Compared with traditional sales channels, younger demographics place greater trust in the internet and have long formed habits of online consumption. Meanwhile, the transparency characteristic of the internet aligns well with the proactive insurance purchasing and research behavior of younger consumers, creating ample room for explosive growth in internet-based insurance. Over the four-year period from 2012 to 2015, the scale of internet insurance premiums grew nearly 20-fold, with the penetration rate reaching 9.2% in 2015.

China's Internet Insurance Premium Scale

Market Size

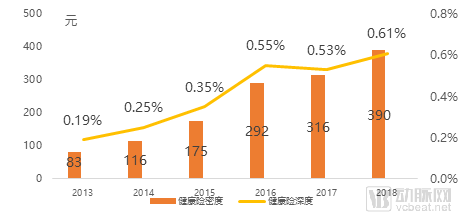

China’s commercial health insurance sector started relatively late. Although it has maintained sustained, rapid growth, its development remains at a primary stage, with a substantial gap compared to developed countries. In terms of premium penetration and premium density, China’s health insurance industry has seen rapid development: from 2013, when health insurance premiums accounted for only 0.169% of GDP with per capita premiums of RMB 83, these figures rose significantly by 2018 to 0.61% and RMB 390 per person, respectively.

(2013-2017 Density and Depth of China's Health Insurance)

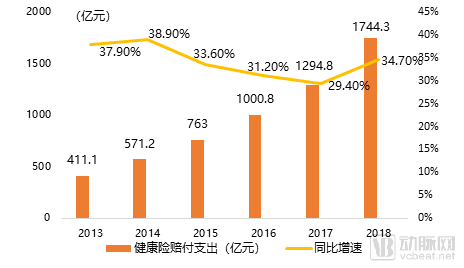

Health insurance claim payouts have shown an upward trend, reaching RMB 174.43 billion in 2018, with a growth rate of 34.7%. This substantial volume of claim expenditures has created potential opportunities for the related back-end services market.

2013-2018Annual Health Insurance Claims Expenditure and Year-on-Year Growth Rate (RMB 100 million)

Product Forms and Market Share

Health insurance is a type of insurance that provides benefit payments for losses resulting from health-related causes. It is categorized into four types based on product structure: medical insurance, critical illness insurance, income protection insurance, and long-term care insurance.

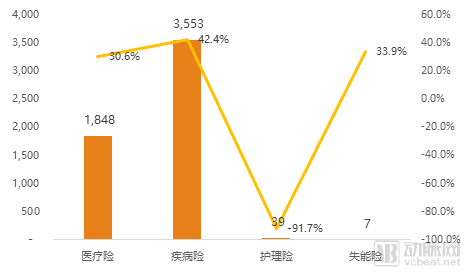

From the perspective of health insurance product development, individual critical illness insurance and medical insurance dominate the market, with distinct trends toward “life insurance-like” features and a focus on individual policies. First, in terms of product categories, disease insurance accounted for the largest share and recorded the fastest growth in the 2018 health insurance market. Premiums from disease insurance reached RMB 355.3 billion for the full year, representing a year-on-year increase of 42.4% and accounting for 65.2% of the total, primarily driven by long-term critical illness insurance. Medical insurance ranked second, with premium volume reaching RMB 184.8 billion, accounting for 33.9%.

2018 Scale and Growth Rate of Various Health Insurance Types (in 100 million yuan)

Industrial Chain

Rapid Growth in Health Insurance Drives Surge in Demand for TPA ServicesAs the health insurance sector experiences rapid expansion, Third Party Administrators (TPAs) are also seeing significant growth. Positioned upstream in the industry chain, health insurance TPA firms not only manage insurance operations but also maintain stable medical resources. By closely integrating with both insurers and healthcare providers, these TPAs effectively unify the roles of healthcare service provider and payer of medical insurance funds.

Health insurance TPA services in China began to develop primarily after 2012, initially focusing on handling outsourced, routine administrative tasks for commercial insurers. Consequently, China’s health insurance TPA sector remains in its early stages. Its traditional business lines mainly encompass claims processing, coordination of medical expense settlements, and reimbursement administration, while emerging business areas include risk control, product development, establishment of healthcare provider networks, and health management.

Positioned in the midstream of the industry chain are specialized health insurance companies and Managing General Agents (MGAs). Insurance companies in China’s health insurance market can be broadly categorized into four types: Chinese-funded property and casualty insurers, Chinese-funded life and health insurers, foreign-funded life and health insurers, and foreign-funded property and casualty insurers. Among these, life and health insurers primarily focus on long-term health insurance products, including critical illness insurance and medical insurance; whereas property and casualty insurers mainly sell short-term accident insurance.

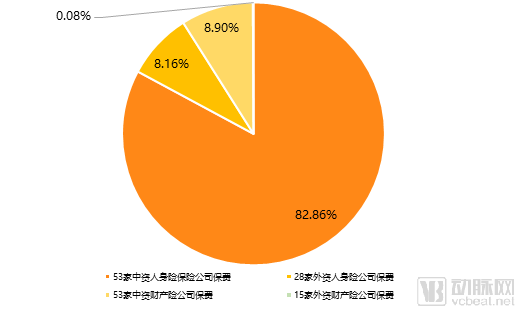

In China’s market, life insurance companies are the primary drivers of health insurance sales, with Chinese-funded insurers holding a larger share of premium income than foreign-funded insurers. According to data from the *China Commercial Health Insurance Report*, in 2017, the market share of life insurance companies in China far exceeded that of property and casualty insurance companies. The combined health insurance premium income of 28 foreign-funded life insurers and 53 Chinese-funded life insurers amounted to RMB 399.44 billion, accounting for 91.02% of the national health insurance premium income. Furthermore, in 2017, the gross written premiums of 43 foreign-funded insurance companies (including both foreign-funded life and property and casualty insurers) totaled RMB 36.17 billion, representing 8.3% of health insurance premium income, whereas Chinese-funded insurance companies captured a 91.7% market share, significantly surpassing their foreign-funded counterparts.

Market Share of Various Types of Insurance Companies in the Health Insurance Market in 2017

MGA, or Managing General Agent, is a specialized model of insurance agency wherein an insurer delegates its underwriting authority to an agent. Upon authorization, the agent acts on behalf of the insurance company to execute insurance contracts. The scope of delegated authority may encompass initial marketing activities (including the management and oversight of intermediaries and part-time agencies), followed by underwriting, temporary coverage issuance, policy issuance, payment processing, premium collection, reconciliation, and claims management. It may also extend to pricing management, internal risk control, and product customization, and can even include actuarial services and reinsurance arrangements.

Compared with traditional insurance intermediaries and agents, Managing General Agents (MGAs) possess advantages inherent to none of the traditional agency models. With flexible pricing and underwriting authority, as well as sophisticated commission structures, MGAs can effectively expand business volume and mitigate moral hazard among intermediaries. Meanwhile, they facilitate a win-win outcome for insurers, agencies, and insurance consumers, holding profound significance for the long-term development of the insurance industry.

Platform and channel companies are located at the downstream end of the industry chain. From the perspective of participants in internet insurance, the main categories are as follows:

1) Large internet companies. Representative examples include Alipay, Ctrip, NetEase, and JD.com, which entered the online insurance sector early on, as well as Tencent, Baidu, and Meituan, which have more recently expanded into this space. These companies primarily rely on their massive user traffic for monetization and conversion.

2) Insurance companies. As providers of insurance products and services, they have seen their influence gradually wane in the face of dominant distribution channels, with their bargaining power steadily diminishing. In particular, some insurers suffer from rigid operational mechanisms, complex management processes, and outdated IT systems, which fail to keep pace with the rapid development of the internet, leading to their gradual marginalization in the online insurance sector.

3) Internet-based intermediary companies. With the widespread adoption of the internet and growing consumer initiative in purchasing, third-party online intermediary platforms have rapidly emerged.

3. Major Tracks and Competitive Landscape of Enterprises

1) TPA Track

The emergence of TPA service companies stems from the "pain points" in the health insurance industry. First, domestic health insurance business is currently dominated by life insurance companies, with critical illness insurance accounting for a large proportion of their product mix. Although medical insurance has been growing rapidly, its scale remains relatively small, resulting in limited influence for medical insurance teams within insurance companies.

Under such circumstances, life insurers prioritize internal resource allocation and do not deploy large-scale medical operations teams, thereby precluding specialized operational capabilities. Furthermore, as health insurance accounts for a relatively small share of total social healthcare expenditure, insurers lack sufficient leverage over healthcare providers. This impedes their ability to establish high-quality medical service networks and implement effective cost control and utilization management measures, thus creating fertile ground for the emergence and development of third-party service providers.

The representative areas where third-party service providers have entered the market mainly include data services, medical services, underwriting and risk control, and claims management. The following are representative companies in China’s health insurance TPA (Third-Party Administrator) sector:

Selected Health Insurance TPA Companies

Players from various sectors are entering the health insurance TPA market, targeting core claims cost-control scenarios by offering services spanning pre-consultation health screenings, online consultations, and intelligent triage; in-consultation expedited appointment access, patient accompaniment, and claims settlement; and post-consultation hospital-aftercare and health monitoring.

2) MGA Track

Compared to models that enter the health insurance sector through TPA services or online sales, the MGA model more effectively integrates front-end sales, mid-stream product design, and back-end services with risk control. For startups, focusing on only a single segment of the health insurance value chain results in a relatively low market ceiling. In contrast, under the MGA model, service providers can achieve genuine cost containment in commercial health insurance and leverage resources across the entire health insurance value chain.

However, the development of Managing General Agents (MGAs) in China is currently in a nascent stage, with most intermediaries being sales-oriented. Their limited positioning has constrained their growth, and when combined with the moral hazards inherent in traditional intermediary models, this has led to a series of drawbacks and issues. Given the increasing maturity and growing influence of the MGA model abroad, as well as the current void in China’s MGA landscape and the existing deficiencies within its intermediary system, it is imperative to introduce the MGA model to China as soon as possible. This will allow MGAs to fully leverage their unique advantages and efficacy as the fourth type of insurance intermediary, thereby driving the development of China’s insurance industry.

Some Domestic Enterprises Currently Attempting to Launch MGA Businesses

3) Internet Sales Platform Sector

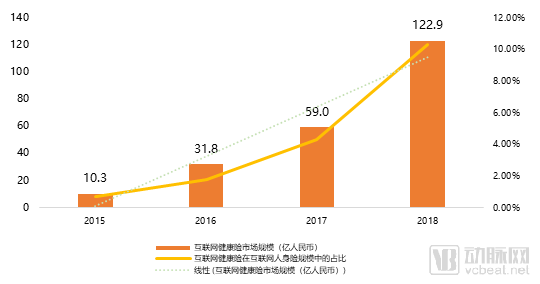

According to statistics from the Insurance Association of China, the gross written premiums for internet health insurance grew from RMB 1.03 billion in 2015 to RMB 12.29 billion in 2018, representing an 11-fold increase over three years. In terms of growth rate, internet health insurance achieved cumulative gross written premiums of RMB 12.29 billion in 2018, a year-on-year increase of 108.3%. The continuous expansion of the health insurance market is driven on one hand by substantial market demand for health insurance products, and on the other by the ongoing introduction of high-quality new products that meet the needs of policyholders.

Market Size of China's Internet Health Insurance (in RMB 100 million)

Among the sales channels for internet-based health insurance, third-party intermediary channels currently dominate. The entry points for third-party channels are illustrated in the figure below:

Internet Health Insurance Sales Model Map

Technology-Empowered Health Insurance

In the future, technology will further empower the health insurance industry. By leveraging big data and AI technologies, it will significantly enhance efficiency in channel expansion, precision marketing, differentiated services, product design, actuarial pricing, operational optimization, risk control, and healthcare network management.

- Big Data Applications: Integrating internal transaction data with massive external data from the industry and partners, combined with professional data analysis models, to better identify and prevent underwriting and claims risks, thereby enhancing anti-fraud capabilities; meanwhile, the establishment of enterprise databases provides the data infrastructure for artificial intelligence applications such as predictive analytics and behavioral analysis models.

- Artificial Intelligence: Automated and intelligent processing workflows. Robotic Process Automation (RPA) technology is employed to automate processes related to underwriting, claims settlement, policy administration, payments, and health management services. Optical Character Recognition (OCR) technology enables precise identification of health and medical documents, thereby enhancing business process efficiency while further enriching industry data. AI technologies, including Natural Language Processing (NLP), machine learning, and deep learning, are leveraged to provide customers with personalized and differentiated products and services, improving the efficiency and experience of claims handling.

More Complete Sales Channel System

Historically, China’s insurance distribution channels were dominated by individual insurance agents and bancassurance. However, as the intermediary market becomes increasingly regulated, the separation of production and sales is emerging as an inevitable trend.

In 2010, the China Insurance Regulatory Commission (CIRC) issued the “Opinions on Reforming and Improving the Management System of Insurance Agents,” advocating that insurance companies strengthen cooperation with insurance intermediaries to establish stable exclusive agency relationships and outsourced sales service models. The separation of production and distribution has become an overarching trend in the insurance industry. As independent third-party institutions, professional insurance intermediaries play a crucial role in linking consumers with insurance companies.

Intensifying competition in the upstream insurance sector has prompted some insurers to focus more on product design and reduce high operational costs to optimize their cost structures. Meanwhile, agencies concentrate on marketing, leading to a more refined division of labor between product development and sales, thereby enhancing overall industry efficiency.

Third-party insurance intermediaries can offer consumers a broader range of product choices, as well as more independent and objective advisory services. It is expected that intermediaries will become the primary channel for reaching consumers in the future.

Product Segmentation: Launch More Insurance Products Targeting Individuals with Pre-existing Conditions

In terms of product strategy, insurance companies will continuously innovate insurance product structures and refine their product portfolios to meet the health protection needs of a broader population. By integrating big data technology with product innovation, they will cater to specific non-standard risk groups across different age brackets and genders, such as those focused on pediatric diseases, women’s health, and middle-aged and elderly individuals. Targeting condition-specific risks within these demographics, insurers will deliver more personalized products and services, enabling consumers to secure health insurance plans better tailored to their individual circumstances.

Integration of the Industrial Chain and Enhanced Influence of Commercial Health Insurance

Insurance companies are beginning to establish their own health management platforms, extending their services from post-claim reimbursement to a full-process model encompassing early-stage prevention, mid-stage treatment, and late-stage rehabilitation. This approach aims to create a closed-loop managed healthcare security service, achieving a win-win scenario in both customer acquisition and cost control.

Insurance companies' pathways for strategic deployment in the healthcare sector include insurance-affiliated hospitals, health management centers, and internet-based insurance.

By investing in hospitals, insurance companies can directly access valuable medical data and engage in in-depth management of medical expenses. By establishing health management centers independently or in partnership with third-party institutions to provide services such as health check-up assessments and medical consultation assistance, they can facilitate early detection and prevention. Through internet-based management platforms, users participate in questionnaires, health consultations, and online assessments, enabling insurance companies to collect health data for subsequent data analysis, management interventions, and evaluation feedback.

Meanwhile, startups entering the health insurance sector from various angles will actively expand upstream and downstream through organic growth and M&A, continuously broadening their service boundaries. By building a health insurance ecosystem to achieve a closed loop and integrate more segments across the industry chain, they aim to enhance product development, pricing, medical services, and claims risk control.