Six Major Trends in the Medical and Health Industry Driven by Declining Birth Rates: Insights from Five Dimensions and Nine Data Sets

On January 17, the National Bureau of Statistics released data on China’s national economic performance in 2019. The number of live births in 2019 totaled 14.65 million, a year-on-year decrease of 3.8%. This figure is considerably more optimistic than the previously circulated online estimate of 11 million; although there was a decline, the magnitude was modest.

In fact, the demographic shifts at both ends of the spectrum—declining birth rates and accelerating population aging—have long been evident and have already drawn the attention of the healthcare industry. It is widely believed within the sector that the two subsegments most significantly impacted are maternal and child health, and elderly medical care and nursing.

However, demographic structure encompasses multiple distinct dimensions—including gender, region, education level, and marital and childbearing status—that interact with one another. Therefore, when examining changes in the demand side of healthcare services through the lens of demographic shifts, the perspective should not be limited to birth rates and population aging but should adopt a more comprehensive approach.

In this article, we examine demographic changes across five dimensions: age structure, marital and childbearing status, education level, urban-rural distribution, and consumption levels. We have compiled publicly available data from the past decade to provide robust empirical support for these dimensions. After considering the intricate interrelationships among these factors, we then project future trends in the healthcare industry.

At the end of 2019, the total population of mainland China surpassed 1.4 billion, an increase of 4.67 million from the previous year, with the overall population still on an upward trend. However, official projections indicate that the total population will peak around 2030 and subsequently decline continuously. Prior to the onset of this demographic decline, we have observed multiple shifts in the internal population structure.

Age Structure: Birth Rates Continue to Decline, Aging Issues Become More Prominent

First and foremost, of course, are the declining birth rate and population aging, which have long been a focus of attention within the industry.

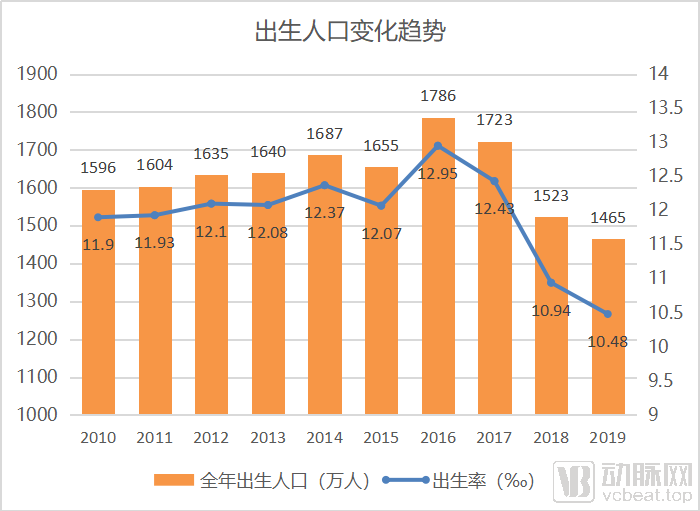

Trends in Birth Population, Source: National Bureau of Statistics, Chart by VCBeat

An analysis of birth population trends over the past decade reveals that the implementation of the “selective two-child” policy in 2013 and the “universal two-child” policy in 2015 led to baby booms in 2014 and 2016–2017, respectively. However, these peaks were short-lived; by 2018, both the number of births and the birth rate had declined sharply, falling even below the levels recorded in 2010.

In 2019, the number of live births and the birth rate continued to decline, albeit modestly.

This indicates that, under policy encouragement, families willing to have a second child have already done so. Many families remain reluctant to have a second child, or even a first, despite preferential policies in areas such as childbirth and taxation.

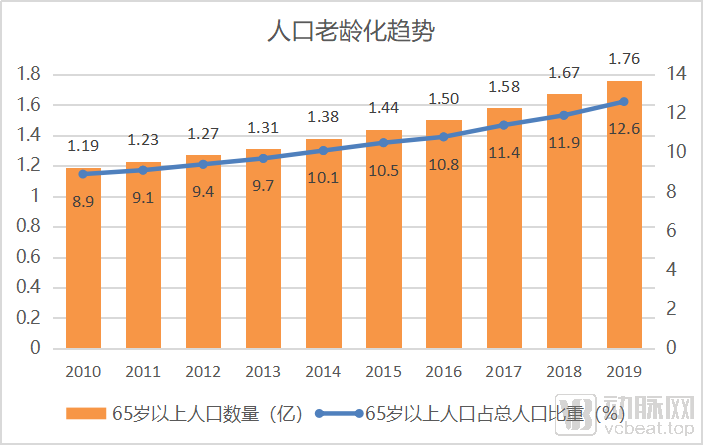

Trend of Population Aging. Data source: National Bureau of Statistics. Graphic by VCBeat.

Concurrent with the decline in birth rates, population aging has also emerged. Over the past decade, the number of elderly individuals aged 60 and above in China increased by 57.09 million, raising their proportion of the total population from 8.9% to 12.6%. As birth rates continue to fall, the challenge of population aging is expected to intensify in the future.

Marriage and Childbearing Status: Decline in the number of women of childbearing age and an overall decrease in marriage rates

Why Has the Birth Rate Declined? We Must Return to the Origin of Life, Focusing on Women of Childbearing Age and on Union Between Men and Women.

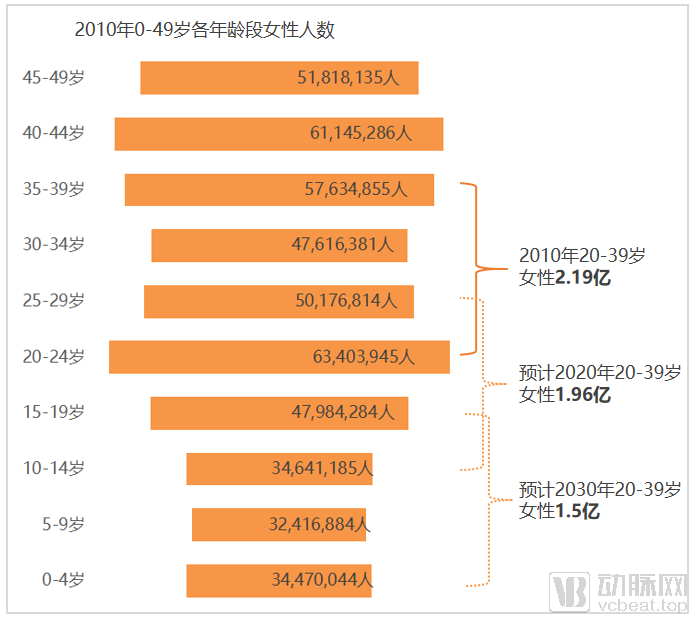

The National Bureau of Statistics defines women of childbearing age as those aged 15–49 based on physiological characteristics. However, official data indicate that among women who have given birth, the most prevalent age groups are 20–24, 25–29, and 30–34 years. Considering that the implementation of the universal two-child policy may also increase the fertility rate among women aged 35–39, we regard these four age groups as the primary childbearing population.

China conducts a national census in years ending with “0,” which includes detailed demographic statistics broken down by sex and age. As the Seventh National Population Census has not yet been conducted, the most accurate current data on the number of women of childbearing age still comes from the Sixth National Population Census conducted in 2010.

We developed a trend projection chart based on the number of females aged 0–49 years in each age group in 2010:

Data source: The Sixth National Population Census; dashed lines indicate estimated data. Chart by VCBeat

As can be seen from the chart above, the number of women in their prime childbearing years was approximately 219 million in 2010, is projected to be about 196 million in 2020, and is expected to drop to only 150 million by 2030. Over this 20-year period, the population of women in their prime childbearing years will decrease by 70 million.

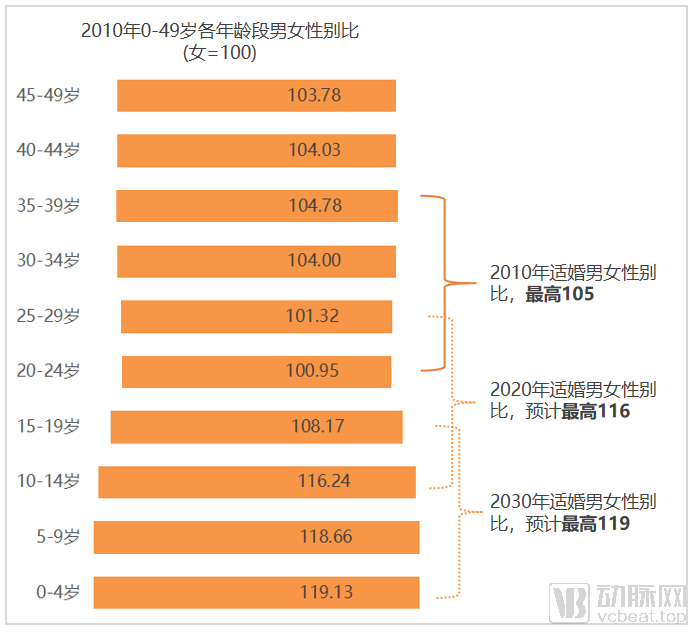

Meanwhile, the demographic structure also faces the issue of a gradually increasing sex ratio.

Data source: The 6th National Population Census of China; dashed lines indicate derived data. Chart by VCBeat.

As shown in the figure above, the sex ratio among men and women of marriageable age peaked at only 105 in 2010, whereas by 2030, when the marriageable population is predominantly composed of those born after 2000, the sex ratio is projected to reach as high as 119.

In years not ending in “0,” the National Bureau of Statistics conducts either a 1% population sample survey or a 1‰ population change survey. Survey data from 2011 to 2018 show that the sex ratio at birth for children aged 0–4 remained between 113 and 119, indicating that individuals born in the 2010s will also face the challenge of a high sex ratio.

The skewed sex ratio may result in some individuals having “no one to marry,” yet subsequent data indicate that many people are “unwilling to marry.”

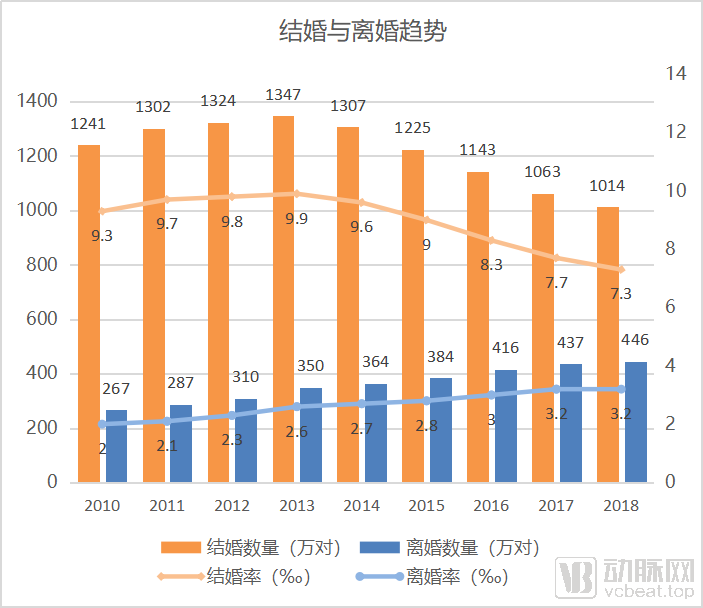

Marriage and Divorce Trends in Recent Years | Data Source: Ministry of Civil Affairs; Chart by VCBeat

According to data from the Ministry of Civil Affairs (note: as the Ministry has not yet released 2019 data, the latest available figures are from 2018), the number of marriages peaked in 2013 and has since declined sharply, falling to 10.14 million couples in 2018—a decrease of 3.33 million couples compared with 2013. While this decline is partly attributable to a shrinking population of marriageable age, the simultaneous drop in the marriage rate indicates that people’s willingness to marry has indeed diminished.

More critically, while the marriage rate continues to decline, the divorce rate keeps rising. This further indicates that people’s views on love and marriage have undergone significant changes, with traditional marital and family structures no longer serving as the primary life destination.

Cultural and Educational Attainment: Universal basic education and a growing population with higher education

The data from the first two dimensions indicate a severe demographic situation, but issues are rarely one-sided. For instance, data from the Ministry of Education show that China’s level of cultural and educational attainment is steadily rising (Note: As the Ministry of Education has not yet released 2019 data, the latest available data are from 2018).

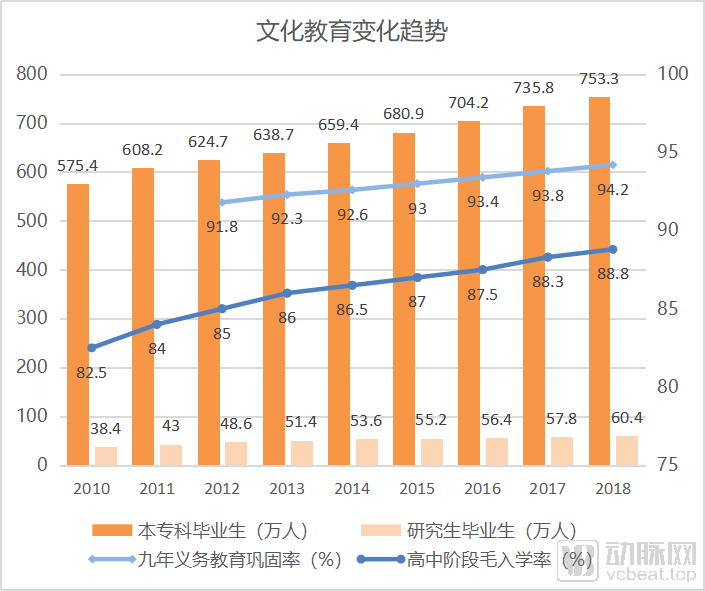

Trends in Cultural and Educational Attainment Levels, Source: Ministry of Education, Chart by VCBeat

We collected four datasets—the consolidation rate of nine-year compulsory education, the gross enrollment rate for senior secondary education, and the number of undergraduate/associate degree graduates and postgraduate graduates—which reflect the basic status of China’s basic education and higher education.

In the realm of basic education, China’s net enrollment rate for primary-school-age children reached 99.79% in 2011, meaning that virtually all school-age children were enrolled in primary education. Starting in 2012, the Ministry of Education began publishing the “nine-year compulsory education retention rate” in its statistical communiqués. This indicator is defined as the percentage of students in the final grade of junior secondary school relative to the number of students who entered the first grade of primary school in the same cohort, and it reflects the completion status of nine-year compulsory education. Since 2012, this figure has shown steady improvement.

In higher education, the number of graduates from undergraduate and junior college programs, as well as postgraduate students, continues to grow steadily. The increase in highly skilled labor has expanded employment opportunities and enhanced the capacity to create social wealth.

Regional Structure: Urban Employment and the Permanent Urban Population Continue to Increase

For a nation, knowledge strengthens national power. For individuals, knowledge changes destiny. The overall improvement in educational attainment has brought about changes in the employment structure.

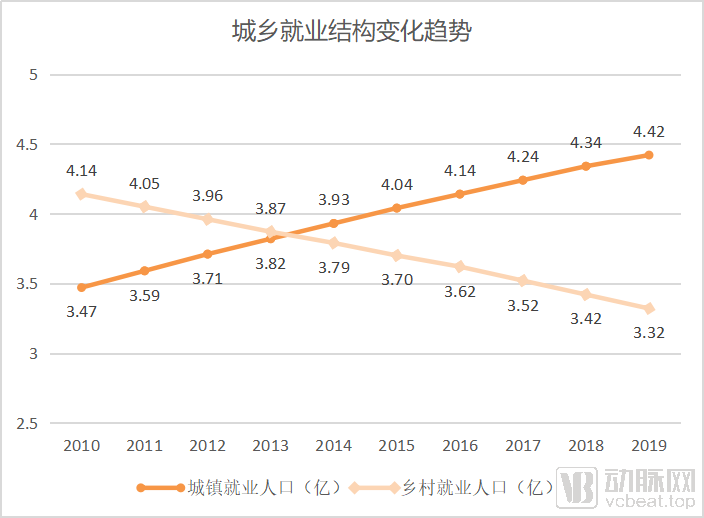

Changes in Urban and Rural Employment Structure. Data source: National Bureau of Statistics; graphic by VCBeat

With rising education levels and economic development, an increasing number of rural residents have migrated to urban areas for employment. As shown in the chart above, the number of urban employees has risen sharply, while the number of rural employees has declined steeply; since 2014, the urban employed population has exceeded the rural employed population. In 2019, the number of urban employees was nearly 100 million higher than in 2010.

Changes in the urban-rural employment structure will inevitably lead to transformations in urbanization.

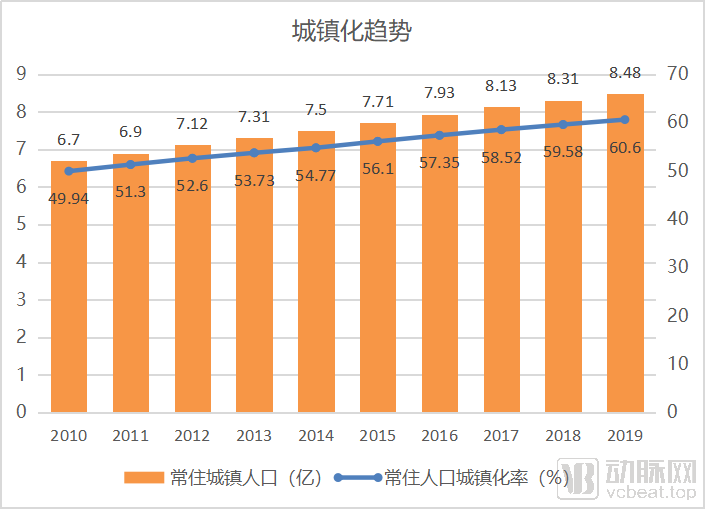

Urbanization Trends in Recent Years, Data Source: National Bureau of Statistics, Graphic by VCBeat

As shown in the figure above, in 2011, the urbanization rate of the permanent resident population exceeded 50% for the first time and has increased year by year since then, surpassing 60% by 2019. Over the past decade, the urban permanent resident population increased by 175 million. Meanwhile, the state has also facilitated the relocation of agricultural migrant populations with the capacity for stable employment and livelihoods in urban areas, enabling entire families to settle in cities and enjoy equal rights and obligations as urban residents.

Over the next decade, urbanization will remain a major trend for both the permanent resident population and the registered household population.

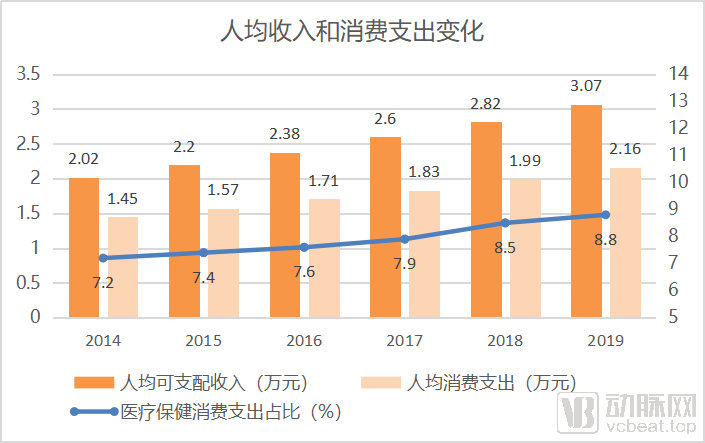

Consumption Level: Rising Disposable Income and Increased Healthcare Spending

Rising educational attainment and an increase in the urban employed population signify higher incomes, stronger purchasing power, and evolving consumer mindsets.

Changes in Revenue and Expenditure in Recent Years; Data Source: National Bureau of Statistics, Chart by VCBeat

As shown in the figure, the per capita disposable income of residents in China has been rising year by year, during which price factors should be taken into account. However, data from the National Bureau of Statistics shows that from 2014 to 2019, even after adjusting for price factors, the real growth rate of per capita disposable income remained at 5%-7.5%.

Meanwhile, per capita consumer spending and the proportion of healthcare expenditures are also increasing. The rise in healthcare spending may be linked to escalating healthcare costs, but it also reflects growing health awareness among the public.

Certainly, our collection of data across these five dimensions reveals far more than just a heightened awareness of healthcare. In the following section, we will comprehensively examine the intricate interrelationships among these dimensions and thereby deduce their implications for the medical and health industry.

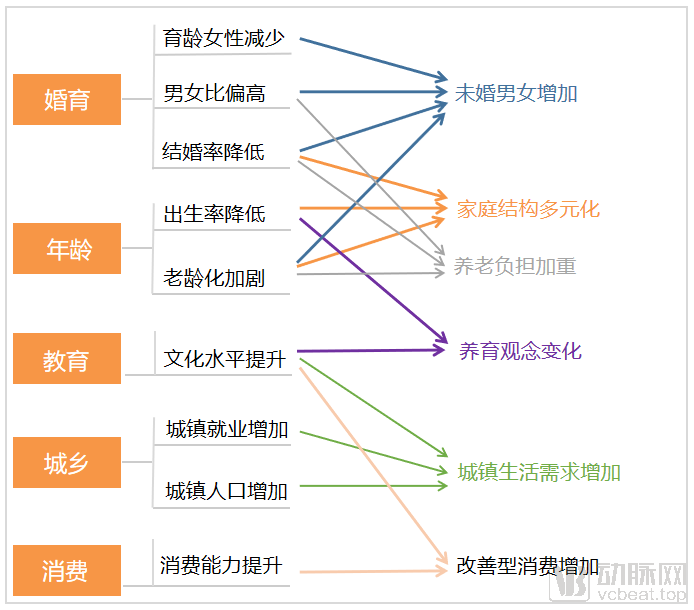

To more intuitively illustrate the relationships and trends across five dimensions and nine data sets, we present them visually in accordance with conventional practice.

Social Development Trends Under the Interplay of Multiple Dimensions, Chart by VCBeat

In the figure above, we demonstrate six social development trends based on changes across various dimensions of demographic structure. So, what are the implications of these trends for the healthcare industry?

Increased Physiological and Mental Health Needs Driven by the Growing Number of Unmarried Individuals

For example, data from the Sixth National Population Census showed that in 2010, there were more than 600,000 excess males compared to females in each of the 20–24 and 25–29 age groups. Based on population figures for the 0–4 and 5–9 age groups in 2010, it is projected that by 2030, the number of excess males in the 20–24 and 25–29 age groups will each exceed 6 million. The disparity between these two sets of data is no longer on the same order of magnitude.

Coupled with shifting attitudes toward marriage and a growing reluctance to tie the knot, unmarried men and women could become a substantial demographic. How to safeguard their physical and mental well-being is a consideration the health industry must address.

It is reported that at this year’s CES International Consumer Electronics Show, sexual health made its mainstream debut, demonstrating the event’s inclusivity toward the adult products industry.

In China, although the adult products industry has seen some growth in recent years, its market development remains constrained by traditional cultural influences. However, against this backdrop, the industry stands to usher in a new wave of opportunities if it can develop more user-centric products and expand into more appropriate sales channels.

Diversified Family Structures Bring Varied Family Health Needs

As concepts of marriage and childbearing evolve, it signifies that families now have more diverse composition patterns, primarily including:

① Three-Generation Household: A family composed of parents, their son and daughter-in-law (or daughter and son-in-law), and grandchildren;

② Two-generation households: three-member families consisting of parents and unmarried children, and four-member families formed under the two-child policy;

③ Small-sized households: DINK (Double Income, No Kids) families who choose not to have children after marriage, single-parent families resulting from rising divorce rates, and single-person households consisting of unmarried individuals.

Among these, the first two types of households are traditional families, and most current family-oriented health management products are primarily targeted at them. However, with the rise in smaller household sizes, how can we provide health management solutions tailored to their needs? We believe the following aspects should be considered:

In small households, dietary health is a risk factor in real-life scenarios. Long-term reliance on dining out and food delivery, which are often high in fat, salt, and sugar, constitutes a significant contributor to obesity, cardiovascular and cerebrovascular diseases, diabetes, other metabolic disorders, and cancer.

“Healthy China Action (2019–2030)” has already set forth a series of targets for residents’ rational dietary practices. In the course of implementation, the healthcare industry can also develop health management products tailored to such small households and strengthen public health education.

Furthermore, small households have relatively weak risk resilience when facing illnesses, particularly critical ones, and face greater pressure in terms of financial expenditures and disease care. Therefore, commercial health insurance can establish corresponding protection systems tailored to these small households.

Aging Population Drives Diverse Elderly Care Needs, While Rising Pressure on Public Health Insurance Promotes the Development of Commercial Health Insurance

As population aging intensifies, it has become an industry consensus that the elderly care sector will usher in a golden era of opportunity. Healthy aging encompasses prevention, diagnosis, treatment, and rehabilitation, with greater opportunities emerging in pharmaceuticals and medical devices for geriatric diseases, rehabilitation clinics, elderly care services, and senior living real estate.

Cardiovascular diseases, orthopedic conditions, and cancers exhibit high incidence rates among the elderly. Companies with flagship products and a leading position in these related fields will benefit from this trend. Furthermore, geriatric diseases are typically chronic. As middle-aged and older adults increasingly adopt mobile internet products, internet healthcare will deliver greater value in the management of chronic diseases among the elderly, potentially becoming an essential tool.

As previously mentioned, the proportion of unmarried individuals and single-person households is increasing. As time progresses and these individuals enter old age, particularly when they become partially or fully disabled, their need for caregiving will become more urgent.

For this population, both material needs—such as clothing, food, housing, transportation, and medical care—and spiritual needs—including companionship, social interaction, and psychological support—can only be met by society. Senior living real estate can provide such an integrated solution, and thus is poised for new growth.

With the aging population and a shrinking workforce, pressure on public medical insurance will continue to rise, making commercial insurance a critical payer. In fact, as education and cultural levels improve, people’s risk awareness has strengthened; the year-on-year increase in gross written premiums for commercial insurance demonstrates growing public acceptance. Particularly among younger generations, there is a greater emphasis on wealth accumulation and insurance planning to address future elderly healthcare needs, signaling a favorable period for the commercial insurance industry.

Shifting Self-Awareness and Parenting Philosophies Drive Changes in Maternal and Infant Health Needs

Indeed, the number of births is declining. In terms of volume, the decrease in newborns and new mothers means that the direct user base for the maternal and infant health industry is shrinking. However, the recent surge in popularity of mid-to-high-end postpartum care centers and private obstetrics hospitals demonstrates a pronounced trend of consumption upgrading in the maternal and infant sector, reflecting higher expectations from women and their families for maternity services.

Other industry insiders have stated that an increasing number of women are willing to invest more time and money in child-rearing, while also paying greater attention to themselves and being willing to pay for self-improvement.

Overall, as educational and cultural levels have risen, women have played a significant role in the workplace and in socioeconomic development. On one hand, they place greater emphasis on self-worth and have increased and higher demands for services related to pregnancy, childbirth, and postpartum recovery, so as to maintain their social image. On the other hand, as beneficiaries of education, their parenting concepts have undergone substantial changes, with greater trust placed in scientifically based child-rearing practices.

In the future, families choosing to have children or a second child will mainly fall into two categories: those with strong fertility intentions and those under low economic pressure. The former exhibit a strong willingness to pay, while the latter possess strong payment capacity; both factors are conducive to supporting the development of the maternal and infant health market. Therefore, even as the number of births declines, consumer demand will persist. The market should shift its focus from user quantity to deeply uncovering the actual needs at each stage of the value chain.

Rising Urbanization Rate Drives Greater Demand for Primary Healthcare

As previously calculated, from 2010 to 2019, the urban employed population increased by nearly 100 million, while the permanent urban resident population grew by 175 million. According to the National Population Development Plan (2016–2030), the urbanization rate will reach 70% by 2030, with a total population of 1.45 billion. Based on this projection, the permanent urban resident population in 2030 will reach 1.015 billion, representing an additional increase of 167 million compared to 2019.

Following the influx of a large population into urban areas, in addition to basic living needs such as clothing, food, housing, and transportation, there is also demand for medical and healthcare services, particularly primary care.

Currently, the state is vigorously promoting a tiered diagnosis and treatment system. In rural areas, primary healthcare focuses on addressing shortages of medical personnel and medicines, improving accessibility to care, and enhancing the quality of medical services. With the acceleration of urbanization, there is an urgent need to improve both the quantity and quality of primary healthcare in urban areas as well, creating strong demand for general practitioners and small clinics.

Meanwhile, the country is implementing a strategy for balanced population development, guiding the orderly flow of population in accordance with the following plan:

For urban agglomerations such as the Beijing-Tianjin-Hebei region, the Yangtze River Delta, and the Pearl River Delta, strictly control the population size of megacities and super-large cities;

For urban agglomerations such as the middle reaches of the Yangtze River and the Chengdu-Chongqing region, further strengthen and expand central cities, enhance their radiating and driving effects on surrounding underdeveloped areas, and build them into important national population clusters.

For urban agglomerations in eastern regions such as the Shandong Peninsula, the West Side of the Taiwan Strait, and Central-Southern Liaoning, further strengthen the coordinated development of large, medium, and small cities within these areas to enhance their appeal to populations migrating from central and western regions.

For the Harbin-Changchun, Central Plains, Guanzhong, Beibu Gulf, Central Shanxi, Hohhot-Baotou-Ordos-Yulin, Central Guizhou, Central Yunnan, Lanzhou-Xining, Ningxia along the Yellow River, and Northern Slope of Tianshan Mountain urban agglomerations, accelerate the formation of more growth poles to support regional development and guide the local clustering of population within these regions.

These plans indicate that when laying out healthcare services, enterprises should shift their focus to key population clusters designated by the state once the markets in existing large and megacities become saturated.

Rising Consumer Spending Power Drives Increased Demand for Aesthetic and Comfort-Oriented Medical Services

As residents’ purchasing power strengthens, their consumption demands become increasingly diverse. In recent years, household expenditure on healthcare has risen year by year. Although more granular data are not available, an overview of several subsectors in recent years reveals that, beyond essential diagnostic and treatment services, people are also seeking consumer-oriented healthcare services.

For example, private ENT and ophthalmology specialties have developed rapidly in the healthcare sector. In particular, listed industry leaders have emerged in ophthalmology, as people are increasingly concerned about the inconveniences caused by ENT and eye diseases and are both willing and able to seek treatment or improvement, especially for cataract surgery, myopia correction surgery, and optometric correction.

Furthermore, orthodontic treatment has also driven the growth of dental clinics. The development and iteration of the medical aesthetics industry further reflect people’s demand for beauty-related consumption.

In the future, as living standards continue to rise, consumer demand for medical services focused on comfort and aesthetics will continue to grow.

Demographic structure constitutes a complex system. While we analyze and assess as many dimensions as possible to identify industry trends, it is crucial to recognize that a significant shift in any single dimension can have far-reaching repercussions throughout the entire system. Therefore, the most critical task is to proactively forecast and monitor these changes, making corresponding adjustments in a timely manner.

On November 1, 2020, the National Bureau of Statistics will conduct the Seventh National Population Census to compile more detailed and timely demographic data. VCBeat will continue to monitor the situation closely, examining the most fundamental shifts on the demand side from multiple perspectives and exploring corresponding response strategies.

Note: Due to rounding, minor discrepancies may exist in some totals or differences.

VCBeat will intensify its monitoring of healthcare-related policies and policy data starting from 2020. Industry practitioners are welcome to contact the author via the WeChat account provided at the end of this article. Your insights would be greatly appreciated.