IVD in 2019: 17 Companies Raised Over $14M Amid Policy Shifts Toward Cost Reduction, Usage Control, Enhanced Regulation, and Industry Promotion

Over the past 40 years, China’s in vitro diagnostics (IVD) sector has achieved a leap from nothing to something. In 2019, the IVD industry experienced rapid development: the launch of the STAR Market enabled five Chinese IVD companies to go public; high-throughput sequencing firms such as 10x Genomics and Adaptive Biotechnologies completed their IPOs; China’s first PD-L1 detection kit was approved for market entry; and multi-cancer liquid biopsy assays received FDA approval. The outbreak of the novel coronavirus (2019-nCoV) at year-end served as a major test for China’s domestic IVD industry.

In early 2020,VCBeatSummaryChanges in the Three Core Elements of the In Vitro Diagnostics (IVD) Industry in 2019: Investment and Financing Data, Policies, and Market

1. In 2019, the number of financing and investment activities in the in vitro diagnostics (IVD) industry halved, while molecular diagnostics and point-of-care testing (POCT) remained highly popular. Differentiated segments emerged within the molecular diagnostics field, including infectious pathogen detection, single-cell technology, and gene editing.

2. Policies in the in vitro diagnostics (IVD) industry are characterized by four major directions: price reduction, usage control, strengthened regulation, and promotion of development.

3. The bundled procurement of clinical laboratory services is emerging as a future trend to drive down prices and enhance service quality; healthcare insurance cost-containment measures have a relatively limited impact on sectors with high technological barriers and high growth potential.

4. Third-party laboratories, benefiting from healthcare cost containment measures and the rapid growth of primary care, will trend toward specialization in the future.

5. Overseas companies are striving to make molecular diagnostics more affordable, expanding the boundaries of the in vitro diagnostics industry, and collaborating with pharmaceutical companies to develop emerging therapies.

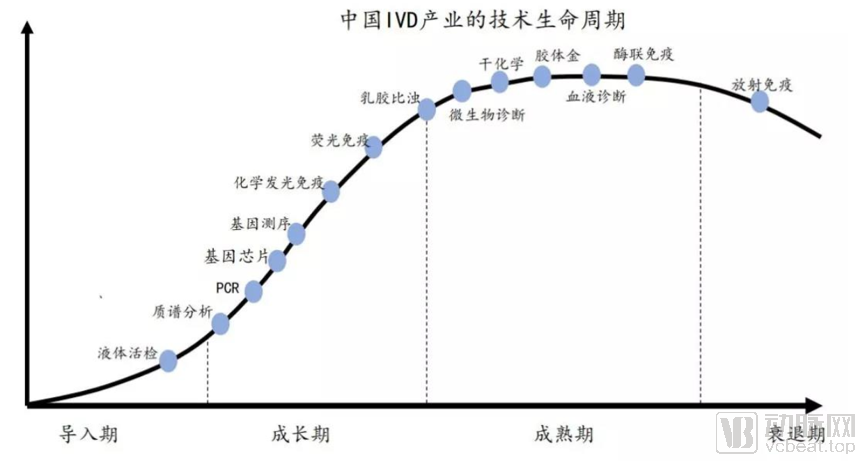

In China, the in vitro diagnostics (IVD) sector is primarily segmented into immunoassay, clinical chemistry, and molecular diagnostics, with clinical chemistry and immunoassay dominating the market and collectively accounting for over 60% of the share. However, recent data from Mordor Intelligence indicates that molecular diagnostics, owing to its broad range of applications, is experiencing rapid growth and has become the fastest-growing IVD subsector globally (with an annual growth rate of approximately 12% in recent years). The growth rate of China’s molecular diagnostics industry is roughly twice the global average.

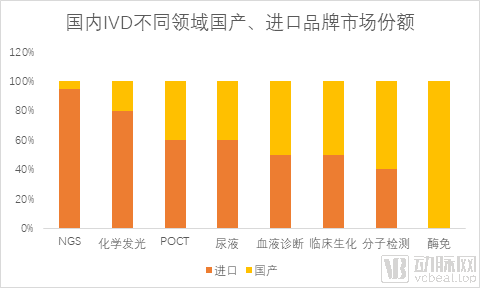

In the landscape of in vitro diagnostics (IVD) financing, traditional biochemical and immunoassay diagnostic companies have attracted limited attention, whereas advanced molecular diagnostics firms are more highly regarded in the capital market. Traditional immunoassay technologies have entered the maturity stage, while investors favor molecular diagnostics companies that are in the introduction or growth stages. As shown in Figure 2 below, molecular diagnostics not only exhibits a faster growth rate but also has a lower import market share.

Data source: Huaxia Jishi "White Paper on the Development of Listed Companies - In Vitro Diagnostics"

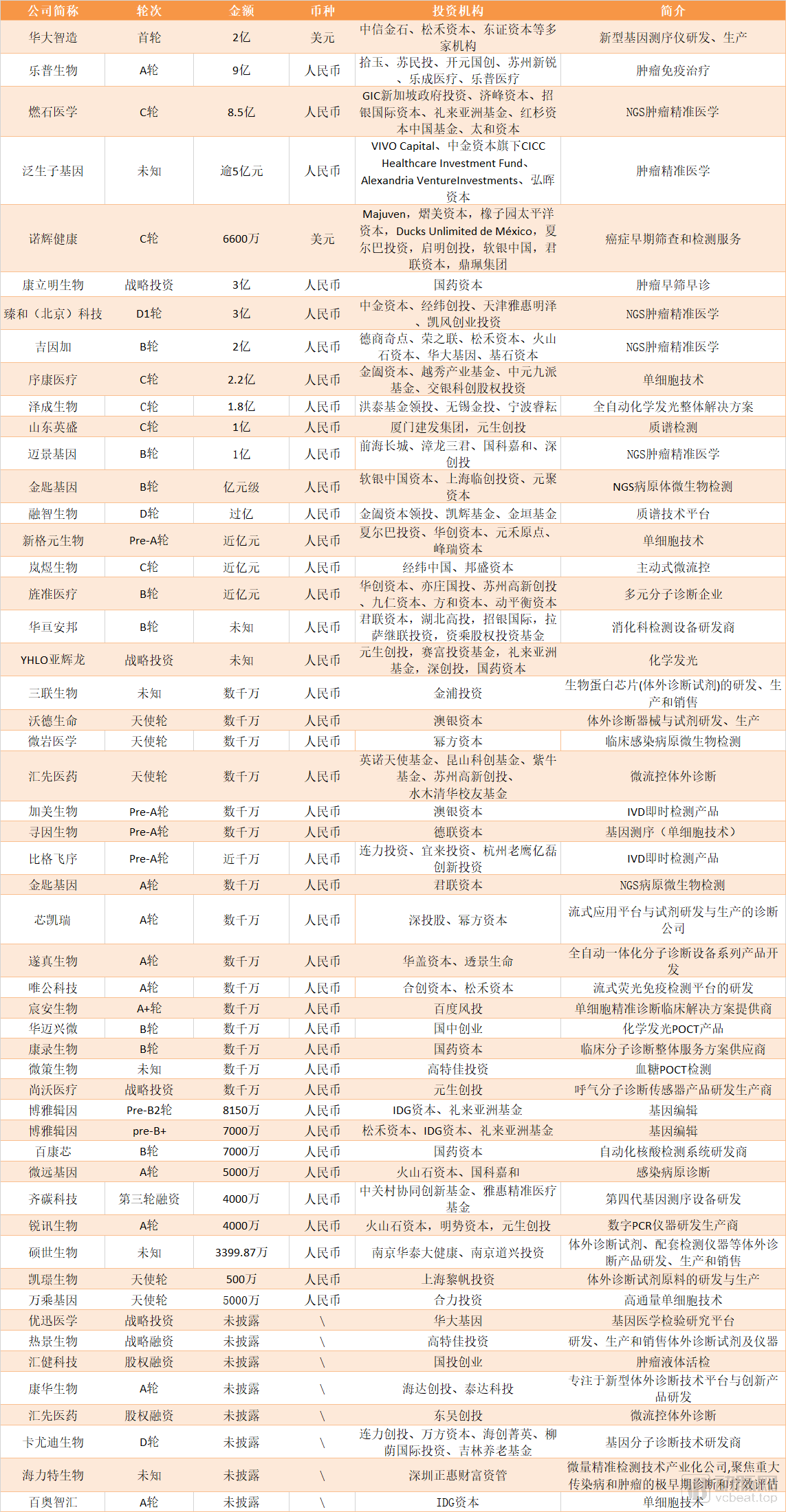

2019 In Vitro Diagnostics (IVD) Financing Data List

Data sourced from the VCBeat Dongguan Database

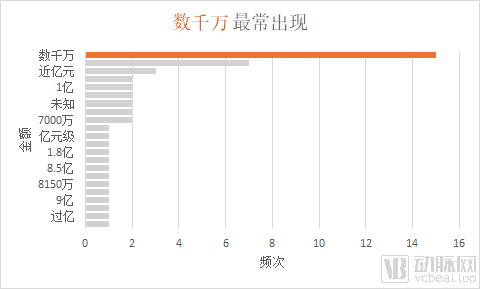

According to incomplete statistics from VCBeat, a total of 51 in vitro diagnostics (IVD) companies completed financing rounds in 2019. Among them, 17 companies secured funding amounts exceeding RMB 100 million, and some companies even obtained multiple rounds of financing within the year. Financing amounts in the tens of millions of RMB were the most frequent, with 15 companies raising funds in this range. Within this financing tier, the point-of-care testing (POCT) subsector was the most commonly funded.

In 2018, there were a total of 100 financing events in the entire in vitro diagnostics (IVD) industry, with publicly disclosed amounts reaching RMB 7 billion. The decline in IVD industry financing is primarily attributable to the current funding winter. Furthermore, an analysis of financing data reveals that the independent clinical laboratory segment, which secured over RMB 1 billion in total financing last year, recorded no financing activities this year.

It is worth noting that although there were fewer financing events in 2019 than in 2018, the number of deals exceeding RMB 100 million remained largely unchanged. In 2019, a total of 17 companies secured financing of over RMB 100 million, compared with 18 in 2018. This also corroborates the principle that “the strong grow stronger” during an industry downturn.

In 2019, the majority of companies securing over RMB 100 million in financing were primarily those involved in gene sequencing, with firms specializing in next-generation sequencing (NGS)-based precision oncology being the most numerous. Among these NGS-based precision oncology companies that raised funds in 2019, most were at Series B and C stages. In contrast, a total of 54 molecular diagnostics companies secured financing in 2018, predominantly at Series A. This suggests that capital investment in the molecular diagnostics sector has become more rational this year.

Some players are exiting the stage while others are making their entrance. An analysis of financing lists reveals that although most companies remain concentrated in the field of liquid biopsy for oncology, new forces such as metagenomic pathogen diagnosis for infectious diseases, gene editing, and single-cell technologies have also emerged among funding rounds exceeding RMB 100 million.

VCBeat has previously conducted an in-depth analysis of the field of metagenomic pathogen diagnosis for infectious diseases (Metagenomic Pathogen Detection Gains Momentum: An Interview with Industry Pioneers), we believe that the rise of pathogen detection has been facilitated by the decline in sequencing costs in recent years, and it also represents an attempt by NGS technology to explore new application spaces after facing intense competition in the NIPT market and the tumor genetic testing market.

In 2019, another subsector that attracted significant capital interest was single-cell technology. In September 2019, the U.S.-based single-cell technology company 10x Genomics went public on the NASDAQ, raising $390 million in its initial public offering (IPO) and emerging as the leader in this field. In China, five single-cell technology companies—Xukang Medical, Singleron Biotechnologies, BioAim Technologies, Xunyin Biology, and ChenAn Biology—completed financing rounds, with Singleron Biotechnologies raising nearly RMB 100 million.

At the genetic level, single-cell technologies can obtain more precise genetic information. At the protein level, analysis of proteins expressed by single cells allows for the direct identification of human immune-related targets, which can be applied in immune diagnostics, new drug development, and other areas.

VCBeat previously conducted an in-depth analysis of the industrialization of single-cell technology in the second half of this year.(With more than ten domestic companies gathering, how long will it take for single-cell technology to achieve industrialization?)We believe that single-cell analysis technologies have matured at both the genetic and protein levels; however, due to cost constraints, they have not been widely adopted in the market and are primarily used to support scientific research.

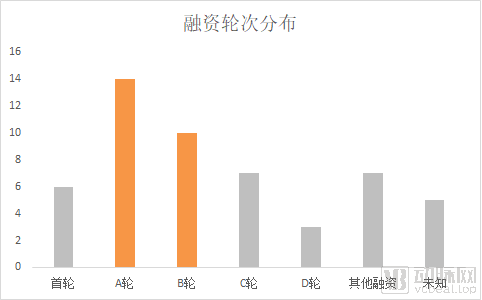

From a round-by-round analysis, Series A and Series B financings dominated the in vitro diagnostics (IVD) sector in 2019, indicating that the IVD market still holds substantial growth potential. Companies at the Series A stage primarily fall into three categories: those specializing in single-cell technology, point-of-care testing (POCT), and molecular diagnostics.

In terms of financing amounts, the most common range is tens of millions of yuan. Among the 15 companies that raised such amounts, the POCT sector attracted the highest level of investment. Compared with 2018, the number of financing events in the POCT field has declined; however, it remains a hot segment within the in vitro diagnostics (IVD) industry, second only to molecular diagnostics in terms of market interest.

Over the past decade, the in vitro diagnostics (IVD) market has experienced rapid growth, with China’s IVD market size maintaining a high growth rate of approximately 20%. This growth has been driven by rising living standards and increasing demand for healthcare services. Additionally, government subsidies for the procurement of medical equipment have served as a significant industrial driver. As healthcare is a sector heavily influenced by policy, VCBeat has compiled relevant policies from 2019 in the field of in vitro diagnostics to provide reference for the industry.

From a policy perspective, in 2019, national authorities issued multiple policies concerning the in vitro diagnostics (IVD) sector. The four major policy directions for 2019 were price reduction, usage control, strengthened regulation, and promotion of development.

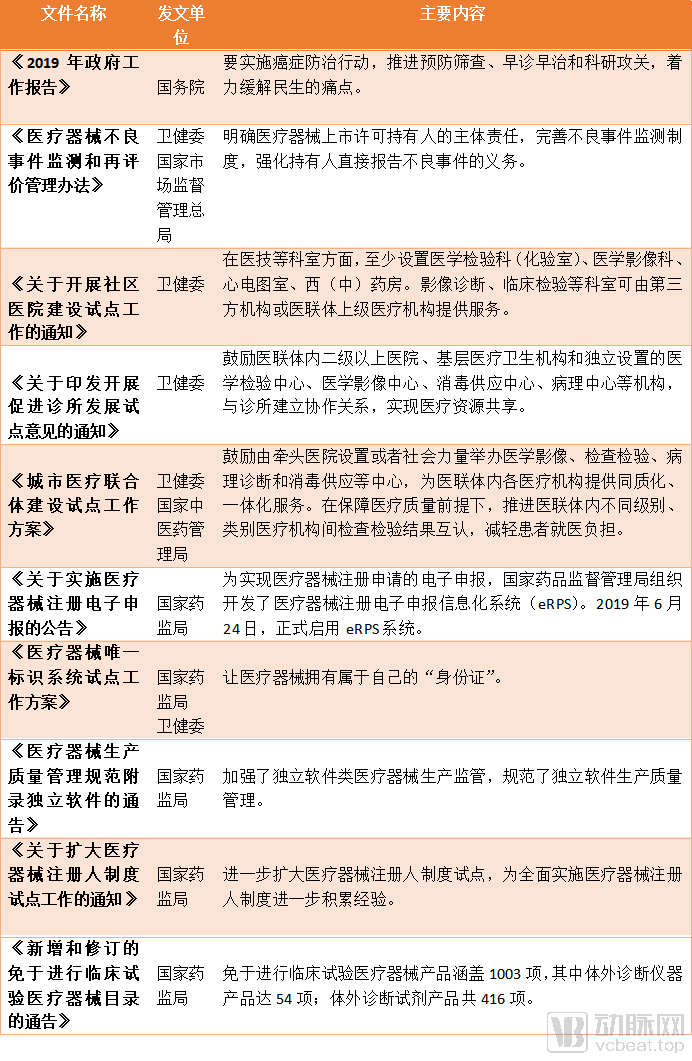

In terms of regulation, the government has introduced multiple policies that further specify requirements for the Unique Device Identification (UDI) system, Good Manufacturing Practice (GMP) for medical devices, adverse event monitoring, and the Marketing Authorization Holder (MAH) system. As a sunrise industry in China, the medical device sector has achieved an annual growth rate of approximately 15% in recent years. Strengthening regulatory oversight is a critical pathway to promoting orderly and innovative development in the medical device industry.

Furthermore, to curb unreasonable medical expenditure, the government has repeatedly introduced policies to reduce examination fees. As a result, the proportion of costs attributed to drugs and consumables has declined significantly, and fees for various diagnostic tests have also decreased, albeit modestly. In some cases, prices have even risen against the trend, largely because health insurance cost-containment measures have had limited impact on sectors with high technological barriers and rapid growth. As economic entities, hospitals are expected to shift greater focus toward their diagnostic departments in the future, using revenue from laboratory and diagnostic tests to offset losses from declining drug-related income.

From a policy perspective, promoting the development of third-party and regional medical laboratory centers was also a key focus of the 2019 in vitro diagnostics (IVD) policies. Benefiting from the tiered diagnosis and treatment system and healthcare insurance cost-containment measures, third-party and regional medical laboratory centers have seen robust growth. The market size is projected to exceed RMB 80 billion by 2024, accounting for 14% of the total revenue in the medical testing industry.

Based on an analysis of 2019 financing data and policy orientations, we believe that the three core changes in the in vitro diagnostics (IVD) sector in 2019 were reflected in cancer early screening, the in-hospital market, and the third-party laboratory testing market.

In 2019, early cancer screening was one of the hot sectors in the genetic testing industry.

The 2019 Government Work Report pointed out that it is necessary to implement cancer prevention and control actions, promote preventive screening, early diagnosis and treatment, and scientific research breakthroughs, focusing on alleviating the pain points of people's livelihood.

Cancer early screening companies Kangliming Biotech and New Horizon Health both completed financing in 2019. Specifically, Kangliming Biotech secured a strategic investment of up to RMB 300 million, while New Horizon Health closed its Series C funding round at up to USD 66 million, indicating that capital markets hold an optimistic outlook on the future prospects of the cancer early screening market.

In 2019, companies in the early cancer screening sector also saw significant developments. New Horizon Health launched “Gong Zheng Qing,” the world’s first urine-based HPV detection product; Kangliming Bio introduced Sinopharm Capital as a strategic investor, further enhancing the sales distribution network for its product “Chang An Xin.”

Early cancer screening is categorized into traditional testing and genetic testing. Notably, in addition to companies specifically focused on early cancer screening, many genetic testing firms also incorporated early cancer screening into their business scope in 2019, including BGI Genomics, Berry Genomics, and HuiRui Genomics.

Among them, BGI Genomics released two self-developed technologies for early cancer screening and a testing service for assessing the risk of hereditary breast and ovarian cancer susceptibility genes, thereby comprehensively expanding its presence in the field of early cancer screening. Huirui Gene announced that its PreCar project for early liver cancer screening had achieved another milestone, preliminarily realizing true early cancer detection ahead of the gold standard. Berry Genomics announced that it would launch additional genetic testing products based on the NextSeq CN500 sequencer, covering patients with mid-to-late stage cancers as well as early cancer screening.

Companies Leveraging Liquid Biopsy Technologies for Early Cancer Screening

VCBeat has compiled a brief overview of companies applying liquid biopsy technology for early cancer screening. In terms of cancer types, domestic companies in China primarily focus on screening for individual cancers with high incidence among the Chinese population (such as colorectal cancer and breast cancer), while few companies are capable of pan-cancer screening. This is because single-cancer screening benefits from more accumulated data, allowing for easier market entry and lower risk. Pan-cancer early screening, which can simultaneously detect multiple types of cancer, is expected to become the main direction for the future development of early cancer screening technologies.

From a technical perspective, early cancer screening is still in the early stages of research and sample data accumulation. Key challenges include the inability to effectively capture tumor-derived circulating tumor DNA (ctDNA), difficulties in determining the organ or tissue of origin for tumors, and the inability to accurately predict how methylation levels influence tumor evolutionary trends and metastatic preferences. In terms of market promotion, pain points such as high costs and lack of coverage by medical insurance also persist.

Additionally, Guo Libing, Managing Partner at Cybernaut, stated, “The domestic market for early cancer screening holds enormous potential, yet there remains a certain gap compared with overseas markets. Some foreign companies in the early cancer screening sector have already achieved relatively mature applications of microfluidics and nanotechnology. Furthermore, China still faces certain challenges in product miniaturization and equipment integration.”

In recent years, the most significant change in the field of in vitro diagnostics (IVD) has undoubtedly been the comprehensive bundling of clinical laboratory services. In 2019, the comprehensive bundling of clinical laboratory services remained one of the key terms in the IVD sector.

In June 2019, the China Government Procurement Network released a “Tender Announcement for Centralized Services for the Clinical Laboratory of Yangshan Branch of Xinyang Central Hospital.” The announcement stated that the Yangshan Branch of Xinyang Central Hospital in Henan Province sought third-party enterprises to provide centralized services for its clinical laboratory. The budget for this procurement was RMB 50 million, with a cooperation period of 10 years. The winning bidder would also participate in the subsequent regional clinical laboratory center project. Ultimately, KingMed Diagnostics and Sinopharm Medical Devices won the bid as a consortium.

This news story is a microcosm of the comprehensive outsourcing of clinical laboratory services in China’s secondary and tertiary hospitals. In recent years, an increasing number of hospitals have adopted such comprehensive outsourcing models. Relevant data indicate that approximately 1,000 hospitals underwent this type of outsourcing in 2016, and industry insiders estimate that by 2019, 20% of secondary and tertiary hospitals had outsourced their clinical laboratory services.

"Bundled procurement for the clinical laboratory" refers to a model in which hospitals and suppliers sign long-term, comprehensive contracts for the supply of consumables. Under this arrangement, the laboratory’s personnel and equipment remain under hospital management, while cost reductions are achieved through volume-based price negotiations. In addition to supplying consumables, the supplier is required to install equipment according to the hospital’s needs and may even undertake renovation work.

The primary providers of comprehensive laboratory bundling services are in vitro diagnostic (IVD) companies or third-party medical laboratories. The ultimate goal of such bundling is to serve clinical laboratory medicine more efficiently, conveniently, professionally, and effectively, while simultaneously reducing the procurement costs of reagents and consumables for the department. It is predictable that the rapid expansion of the bundling model is likely to reshape the competitive landscape of the entire IVD industry in the future.

However, some industry insiders believe that the current bundled service model for clinical laboratories has yet to find a balance between the market and end-users. An excessive pursuit of low costs may compromise upstream enterprises’ ability to ensure service quality and supply capacity, while excessively high costs would defeat the purpose of bundling. Therefore, the bundled service model for clinical laboratories still requires a period of refinement and improvement.

As the nation vigorously promotes the development of Medical Consortiums, regional clinical laboratory centers, as a key component of these consortiums, will receive substantial support. Once more than half of hospitals are integrated into bundled service packages, enterprises with incomplete product lines that cannot penetrate this bundled business model are likely to face consolidation or market exit. Only by comprehensively strengthening their advantages in pricing, technology, network coverage, and operations can companies secure a competitive edge in future developments.

Beyond the comprehensive bundling of clinical laboratory services, medical insurance cost-containment measures across various regions are shifting focus from pharmaceuticals to consumables and diagnostic tests. Consequently, whether reagents and equipment required by hospital clinical laboratories will be subject to centralized procurement has become a key concern for the in vitro diagnostics industry.

In this regard, respondents stated that in vitro diagnostic (IVD) reagents and equipment are not yet ready for centralized procurement in the short term, citing two reasons:

1. The prerequisite for centralized procurement is standardization; however, in vitro diagnostic (IVD) products feature complex specifications, diverse technical pathways, and imperfect product standards. Furthermore, the quality of IVD products from various manufacturers in China is currently uneven, with an urgent need to improve overall standards. Consequently, clinical laboratories tend to prioritize purchasing from brands with superior quality.

2. In vitro diagnostic (IVD) products are trending toward closed systems, making the management of existing installed bases and the adoption model for new instruments a significant consideration. Furthermore, China still relies on imports for certain reagents and instruments. Consequently, respondents believe that fully replicating the pharmaceutical reform pathway for IVD products presents considerable challenges.

From another perspective, the promotion of Diagnosis-Related Groups (DRGs) in the context of healthcare cost containment may lead to an increase in diagnostic service volume at both hospital and payer levels, with rising costs for certain tests and diagnostics better reflecting the value of clinical care.

For hospitals, with the implementation of medical insurance cost-control measures such as centralized procurement of drugs and consumables, the revenue mix will shift toward clinical testing. Overall data shows that the proportion of diagnostic expenses on the hospital side has been increasing year by year, while the price of testing for single diseases has risen rapidly.

Taking the revenue structure of a hospital in northern China as an example, in the first half of 2018, the proportion of revenue from drugs and consumables decreased by 30%, while laboratory testing revenue increased by 60%. Meanwhile, regarding the pricing of individual test items, the routine diagnostic panel for upper respiratory tract infections previously included only complete blood count (CBC) and C-reactive protein (CRP). Currently, the testing panel has expanded to include influenza A virus, influenza B virus, Mycoplasma pneumoniae, viral serology, and respiratory syncytial virus (RSV), among others.

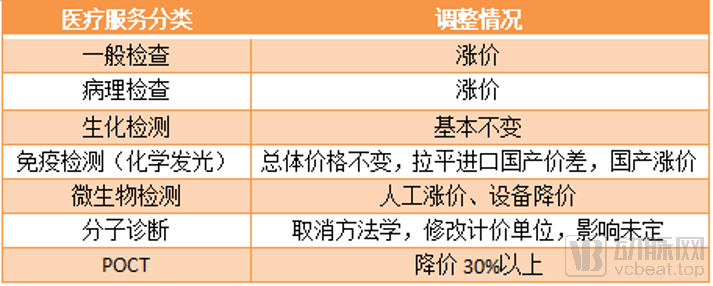

Currently, fees for laboratory tests are being adjusted across various regions. The adjustment of medical service prices in Beijing in June 2019 can be regarded as a bellwether.

Under Beijing’s price adjustment plan, laboratory testing prices have remained largely stable, a trend that generally favors the substitution of imported products with domestically produced alternatives. At the level of individual test items, fees for general laboratory tests and pathological examinations have increased, while prices for biochemical and immunoassay tests have seen little change, with only a few items experiencing price reductions. Meanwhile, molecular diagnostic tests have shifted from the previous methodology-based pricing model to a test-item-based pricing structure, making the system more scientific and rigorous.

In the short term, diagnostic costs for different patients will rise or fall following the reforms. In the long run, adjustments to laboratory test prices are expected to further standardize physicians’ prescribing behaviors, benefiting drugs, consumables, laboratory tests, and private-sector services that address essential therapeutic needs and major diseases. Thus, the impact of medical insurance cost-containment measures will be limited in subsectors characterized by certain technical barriers and rapid growth.

Another major trend in the in vitro diagnostics market is the growth of the third-party clinical laboratory testing market.

Several key drivers are propelling the development of third-party medical testing laboratories, with cost containment within the national health insurance system being the primary one. According to the “Report on Effectiveness Evaluation and Experience Summary of Third-Party Medical Laboratories” published by the Health Development Research Center of the National Health Commission, third-party medical testing can save more than RMB 10 billion annually for the national health insurance fund, accounting for 1% of its total expenditures.

Secondly, the tiered diagnosis and treatment system will also boost the development of third-party medical testing laboratories. The growth of these laboratories can help enhance primary-level testing capabilities, improve the comprehensive service capacity of county-level public hospitals, and integrate testing resources for greater accessibility at the grassroots level.

In China, tertiary hospitals offer approximately 500 testing items, while primary and secondary hospitals provide 200–300 items. In contrast, third-party medical laboratories can offer more than 2,000 testing items, with U.S. companies such as Laboratory Corporation of America Holdings and Quest Diagnostics providing up to 4,000 tests. The development of third-party medical testing laboratories will undoubtedly create greater market opportunities for grassroots healthcare institutions.

In recent years, the number of third-party medical testing laboratories in China has been growing rapidly. In 2010, there were only 89 independent clinical laboratories (ICLs) in China. Driven by favorable policies in recent years, ICLs have experienced rapid development. According to incomplete statistics, the number of ICLs in China reached 468 in 2016, 689 in 2017, and 1,272 in 2019.

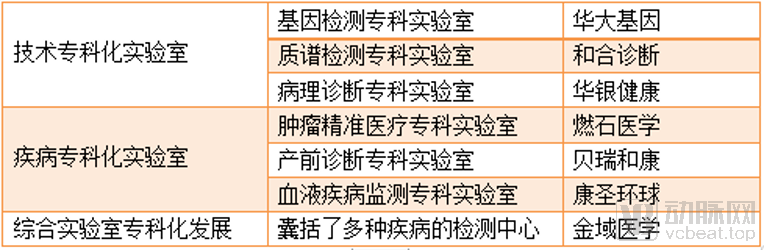

In the future, third-party medical laboratories may evolve toward specialization, differentiating into specialized entities such as technology-focused laboratories, disease-specific laboratories, and comprehensive laboratories.

Currently, KingMed Diagnostics, Dian Diagnostics, Adicon, and Daan Gene collectively hold over 70% of China’s third-party medical testing market. Going forward, companies that have yet to achieve economies of scale will face increasingly fierce competition. For small and medium-sized enterprises, building brand recognition and accumulating financial advantages represent one viable pathway to achieving rapid growth and overtaking competitors.

In China, a clear trajectory for the development of in vitro diagnostics (IVD) is import substitution. This is a relatively mature and widely recognized pathway. It is foreseeable that foreign IVD technologies will continue to lead those in China over the next 5–10 years. VCBeat has compiled a list of foreign IVD companies that have recently attracted significant attention.

Sherlock Biosciences Leverages Gene Editing for Portable, Ultra-Sensitive Molecular Diagnostics

Sherlock Biosciences is a very young company, having been established for less than a year. Sherlock Biosciences aims to enable molecular diagnostics anytime and anywhere.

Sherlock Biosciences owns two major technology platforms. One is the Sherlock platform, which is based on CRISPR technology and features extremely high sensitivity, high specificity, and minimal sample preparation requirements. Sherlock Biosciences has already demonstrated its effectiveness across various indications. The second platform is INSPECTR technology, a synthetic biology-based platform that does not require amplification, can be operated at room temperature, and enables comprehensive lateral flow solutions. By leveraging these two technologies either in combination or individually, Sherlock Biosciences aims to deliver rapid molecular diagnostics that are both simple and affordable.

SHERLOCK and INSPECTR have broad application potential and can be utilized in fields such as healthcare and agriculture. In the healthcare sector, these platforms can be used to detect infectious disease pathogens and cancer DNA; in agriculture, they can help users better manage crops and ensure food safety.

Currently, Sherlock Biosciences has completed its Series A financing round of $31 million, with investors including Baidu Venture Capital, Northpond Ventures, and the Open Philanthropy Project. Previously, Sherlock Biosciences had also secured a $35 million funding round.

Adaptive Biotechnologies Decodes the Human Immune System with Diagnostics

Adaptive Biotechnologies, founded in 2009, aims to develop and commercialize immune-driven clinical products tailored to each patient. Adaptive owns TruTCR, a proprietary T-cell receptor (TCR) discovery and immune profiling platform.

T cells and B cells circulate in our bloodstream. Adaptive Biotechnologies employs gene sequencing technology to read the genes of these cells and create an immune repertoire comprising billions of data points.

Adaptive Biotechnologies has also entered into collaborations with Microsoft and Genentech, a member of the Roche Group. The partnership with Microsoft primarily aims to leverage Microsoft’s cloud computing and machine learning technologies, while the collaboration with Roche seeks to utilize Adaptive Biotechnologies’ platform to accelerate the development of personalized cell therapies.

Mammoth Biosciences Builds a Search Engine for Biology

Mammoth Biosciences has developed the world’s first and only CRISPR-based diagnostic platform capable of detecting any biomarker or disease using DNA/RNA. In April 2018, Mammoth Biosciences officially commenced the development of CRISPR technology for clinical diagnostics.

The company was co-founded by CRISPR pioneer Jennifer Doudna, Stanford University PhDs Trevor Martin and Ashley Tehranchi, and University of California PhDs Janice Chen and Lucas Harrington. Among them, Jennifer Doudna also serves as the Chair of the Scientific Advisory Board.

Mammoth Biosciences’ vision is to provide a gene-editing-based technology platform capable of delivering an unlimited number of tests for healthcare, biosensors, and cross-industry applications in agriculture, manufacturing, and partnerships.

From the perspective of differences in development between China and abroad, the in vitro diagnostics (IVD) industry also experienced a decline in overseas financing in 2019. Mergers and acquisitions (M&A) and initial public offerings (IPOs) decreased in the later stages, with investment and financing activities concentrated primarily in early-stage Series A rounds. Notable IPO cases in 2019 included 10X Genomics and Adaptive Biotechnologies, both of which achieved valuations exceeding $2 billion after going public.

Furthermore, among the in vitro diagnostics companies that went public in 2019, two-thirds were R&D tool providers rather than manufacturers producing products directly for physicians and patients.

From a forward-looking perspective, the in vitro diagnostics (IVD) market offers numerous avenues for development, such as miniaturized sequencers, metabolomics, proteomics, ultra-sensitive molecular-level detection, amyloid-beta (Aβ) detection, room-temperature amplification, and non-invasive blood glucose monitoring. These technologies will inject new momentum into the growth of the IVD industry, although many of the currently demonstrated technologies still carry inherent risks and remain immature.

What Does 2019 Mean for the In Vitro Diagnostics Industry? In an interview, an entrepreneur told VCBeat, “The first half of the ‘golden decade’ for China’s in vitro diagnostics industry has come to an end; the market will bid farewell to unchecked growth, and the second half is just beginning.”

From medical alliances to integrated healthcare consortia, and from tiered diagnosis and treatment to DRGs, the healthcare industry is facing unprecedented challenges, which also bring new opportunities for in vitro diagnostics companies.

In 2019, the in vitro diagnostics (IVD) industry witnessed a series of positive developments. Following the launch of the STAR Market, several IVD companies, including Hotgen Biotech, Shuoshi Biotech, and Pumen Technology, went public on the board, providing a significant boost to the industry’s growth. Despite the broader capital market entering a downturn in 2019, IVD companies remained attractive to investors, with many securing substantial financing rounds.

Over the past decade, the most significant change among the top 10 global in vitro diagnostics (IVD) companies has been mergers and acquisitions between industry giants. In the Chinese market, however, changes have been even more dramatic, with a large number of rapidly growing, technology-driven IVD enterprises emerging and evolving into leaders in niche segments characterized by high technological barriers.

Will the in vitro diagnostics (IVD) industry continue to maintain rapid growth in the future? An investor in the IVD sector told VCBeat, “The IVD industry is technology-driven. With the continuous emergence of new technologies and products, this field will continue to experience rapid growth.”

The next decade is worth looking forward to.