2019 Future Healthcare Industry Tree Report: Demand-Supply Perspective on Industrial Structure and Three-Dimensional View of Sector Evolution

Over the past five years, VCBeat Research has continuously tracked and studied emerging medical technologies and innovative models, developing frameworks such as the “Domain” Model, the Impossible Trinity of Healthcare, and the Healthcare Big Data Bowtie Model. At the 2019 Future Healthcare Top 100 Conference, it released the “2019 Future Healthcare Industry Tree Report.” This article is an excerpt from the report; you can scan the mini-program QR code below to download the full version for free.

During our research, we found that it is difficult for innovative segments to find their proper positioning and a coherent logical framework, as they are constrained by the traditional structural system of the healthcare industry, which centers on an upstream-downstream architecture. Therefore, this report aims to present some of our reflections:

① Following the core shift in demand, analyze the demand trends of healthcare service institutions from four perspectives: social, economic, policy, and ecological;

② Develop an industry map for healthcare innovation;

③ Explore solutions in niche sectors, analyzing the required scenarios as well as tools and corporate case studies under technological and business model innovation.

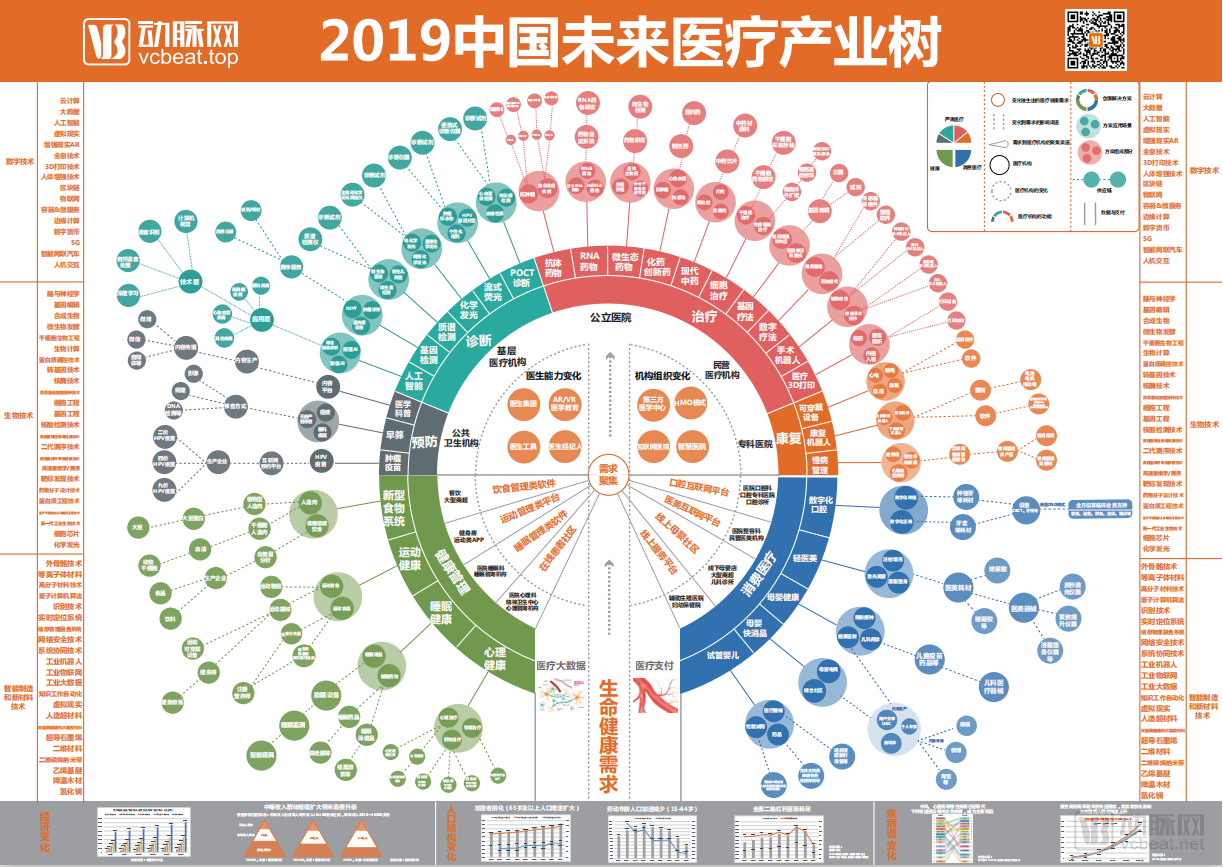

2019 China Future Healthcare Industry Tree(Due to limited clarity caused by compression, a high-resolution version of "The Future Healthcare Industry Tree" can be downloaded for free from the VCBeat report section.)

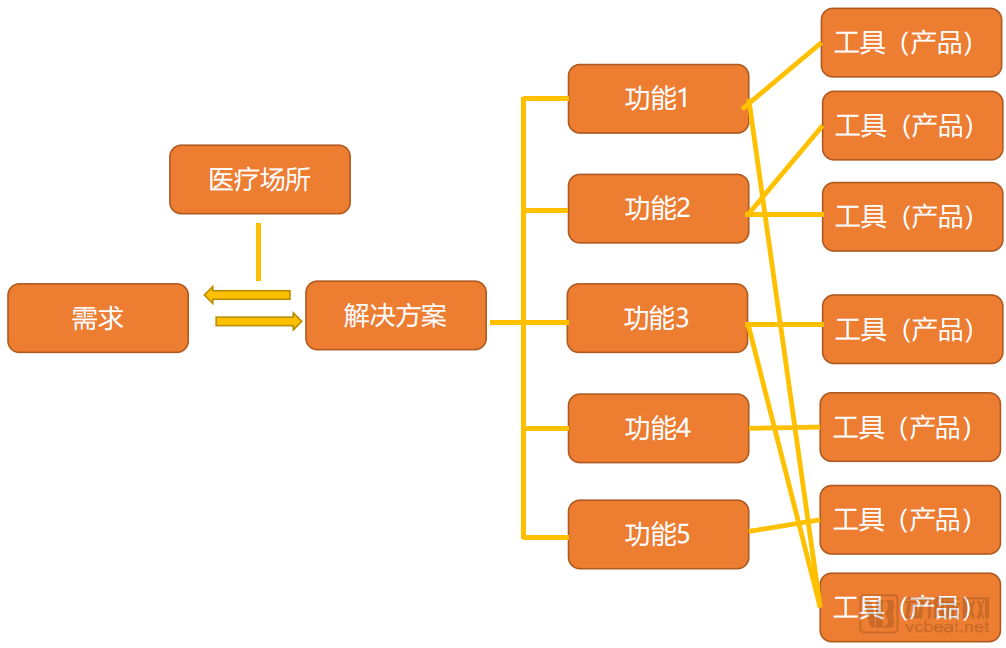

In the healthcare industry, patient needs are categorized into therapeutic needs, health maintenance needs, and “enhancement needs.” These needs are met within healthcare settings dominated by medical institutions, which address patient demands through integrated solutions that combine physicians with medically functional devices. Industry research involves uncovering the functional components and corporate landscapes underlying these solutions, leveraging long-term tracking to gain insights into industry trends.

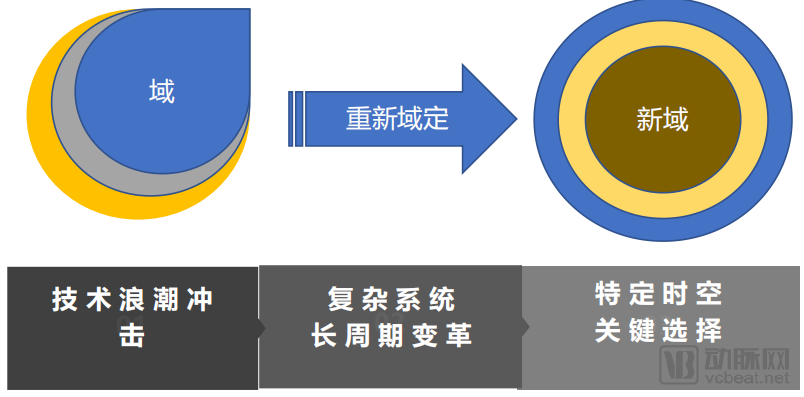

Domain Model is the foundational model for VCBeat’s industry research. We believe that only through major transformation can significant opportunities arise. The phased challenges in industrial development will reach a new equilibrium through such transformation, presenting a major opportunity for all stakeholders.

1. Ecological Composition:Underlying technologies, the resulting distribution of interests, and the rules, mechanisms, and legal frameworks that coordinate social operations.

2. Domain, Re-domain:When key technologies within a domain gradually evolve and ultimately undergo fundamental changes, the old domain transitions into a new one, and the economic operating model achieves a new stability on this basis. This process is known as re-domaining.

3. Relationship Time:The process of transitioning from an old domain to a redefined one is rarely accomplished overnight; it typically requires 20 years or even longer, a duration that philosophers refer to as “relational time.”

Based on the domain model, VCBeat has proposed a series of related inferences to help understand and recognize the process of industry development.

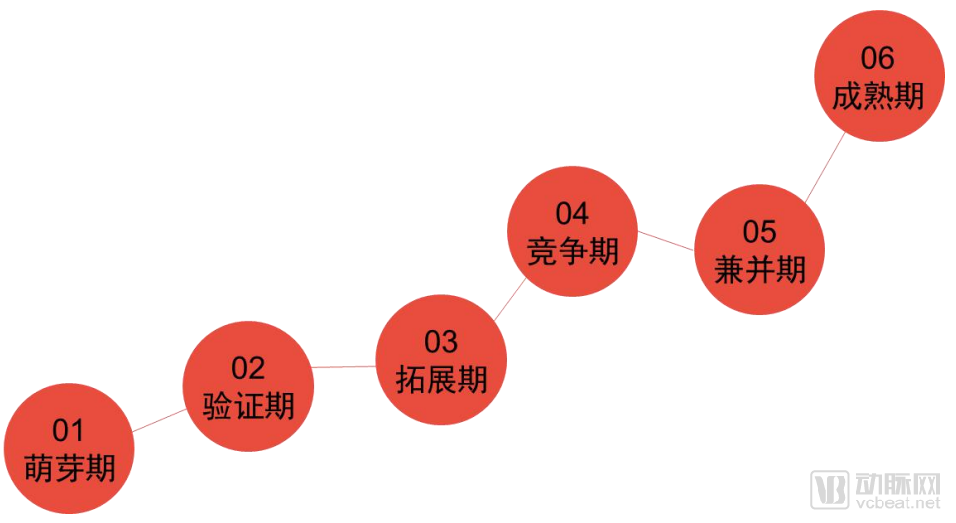

We categorize the development of innovative enterprises into six stages: inception, validation, expansion, competition, merger and acquisition, and maturity. Enterprises at each stage face distinct core tasks, namely concept proposal, technology validation, confirmation of industrial partnerships, capital validation, revenue validation, and profit feedback, respectively.

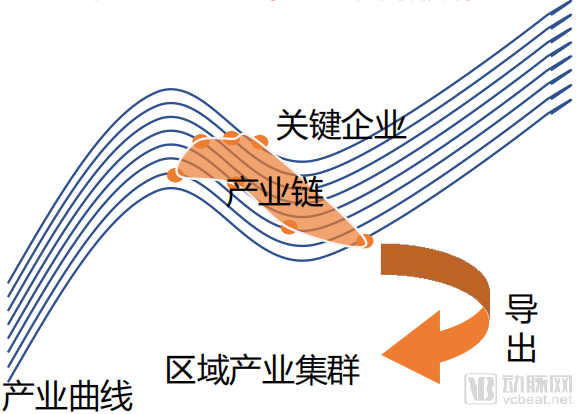

Along the technology-driven industrial development curve, a large number of new enterprises are inevitably generated. The specific spatial carriers for these new enterprises may be selected either consciously or unconsciously. Industry development driven by core technologies may resonate with the regional development of carrier platforms, thereby creating the potential for the emergence of future benchmark cities in healthcare.

We have re-examined the roles and interrelationships of the seven key elements in the healthcare industry, establishing a framework for viewing the healthcare sector. Based on this perspective, we have constructed the following “Future Healthcare Industry Tree.”

Driven by three major technology clusters, new demands are being efficiently aggregated and deeply integrated with specific scenarios, thereby activating entirely new markets. As the sole proactive element, policy serves as a critical switch and valve for industrial evolution. The nearly RMB 400 billion in healthcare funds invested in this sector over the past six years have acted as a key driving force. On this basis, the existing industrial structure is being reinterpreted through different logics, while the combination of production factors is being dismantled and reconfigured.

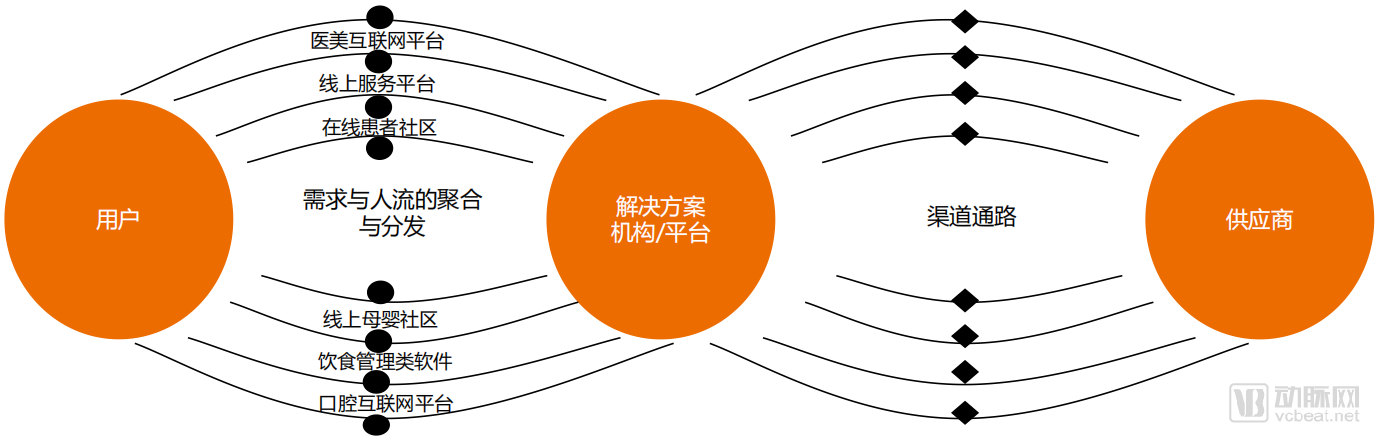

In the industrial ecosystem we have built, demand, solutions, and supplier positioning serve as three key nodes, connected by traffic pathways and market channels; we will also analyze their evolving dynamics.

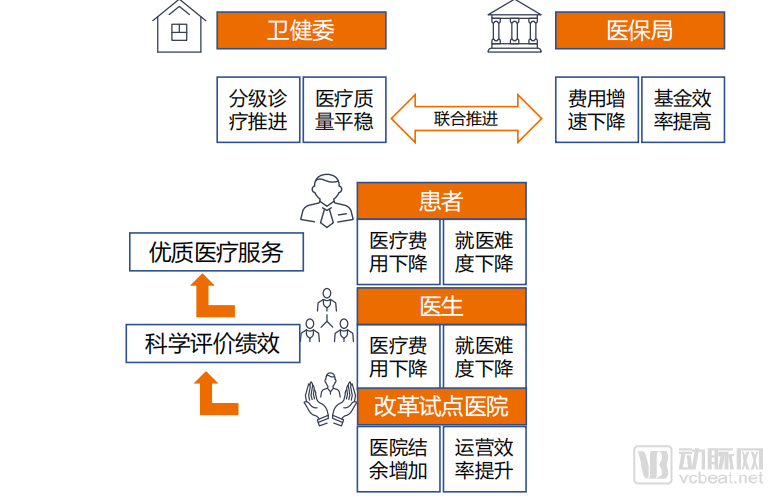

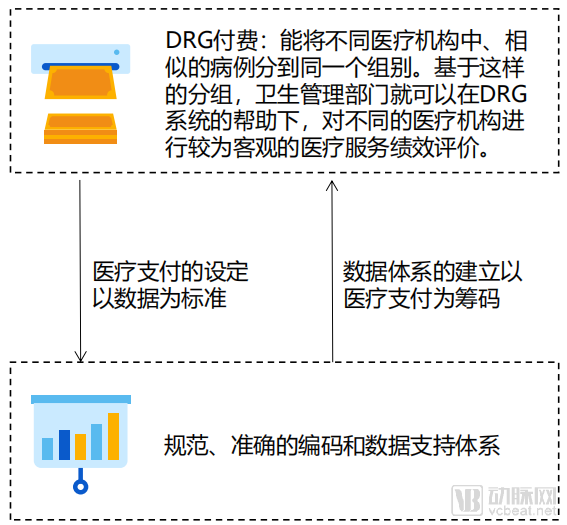

Healthcare payment reform has always been the primary task of healthcare system reform. However, despite the transition from fee-for-service and global budgeting to diagnosis-related group (DRG) payment models, the array of approaches remains bewildering, and the financial burden on medical insurance continues to intensify. Currently, fragmented, illogical, and non-standardized data have become significant pain points for hospitals in conducting data research. The National Healthcare Security Administration acts as the representative for all healthcare demand-side stakeholders and engages in performance-based negotiations with healthcare solution providers.

With the comprehensive rollout of DRG-based payment policies, big data-driven lean hospital operations will inevitably become a key strategic direction for hospital development and serve as the foundational guarantee for advancing value-based healthcare. By establishing Clinical Data Repository (CDR) and Operational Data Repository (ODR) data centers, hospitals will further usher in a new era of scientifically guided clinical pathway decision-making, centered on patient- and condition-specific service value and oriented toward cost management.

PolicyIt is the flow control valve that regulates industrial progress, and the only proactive element that industry promoters can master.

Industrial PolicyIndustrial policy refers to the aggregate of various policies through which the government intervenes in the formation and development of industries to achieve specific economic and social objectives. The primary functions of industrial policy are to address market failures and ensure efficient resource allocation; to protect and nurture emerging domestic industries; to smooth out economic fluctuations; and to leverage late-mover advantages while enhancing adaptive capacity.

In the operation of a market economy, industrial policy plays a guiding role. This guiding function primarily includes: adjusting the supply and demand structure of goods to help achieve balance between supply and demand in the market; regulating the capital market through credit preference policies such as differential interest rates to facilitate the rational flow and optimized allocation of funds; and breaking down regional blockades and market fragmentation to promote the development and formation of regional markets and a unified national market.

Industrial policy can regulate the economic structure, namely the industrial structure, industrial organizational structure, and regional layout of industries, so as to achieve rational allocation of social resources among various industries, sectors, enterprises, and regions, thereby gradually optimizing the industrial structure. Meanwhile, it can also adjust supply by promoting or restricting the development of certain industries, transforming the industrial structure, and adjusting inter-industry relationships, ensuring that both the total volume and structure of supply meet demand, thus achieving balance in both aggregate and structural terms between supply and demand.

However, industrial policy formulation inherently involves a certain degree of lag. New industries emerge from innovation, which is typically unpredictable; consequently, industrial policies are usually formulated only after innovations have already occurred. Furthermore, the development of industrial policies requires a comprehensive process including research, pilot programs, and broader implementation, thereby introducing inherent time delays. As a result, industrial policies are often rolled out only after an industry has explored multiple pathways, accumulated practical experience and lessons learned, and developed the corresponding capacity to absorb and implement such policies.

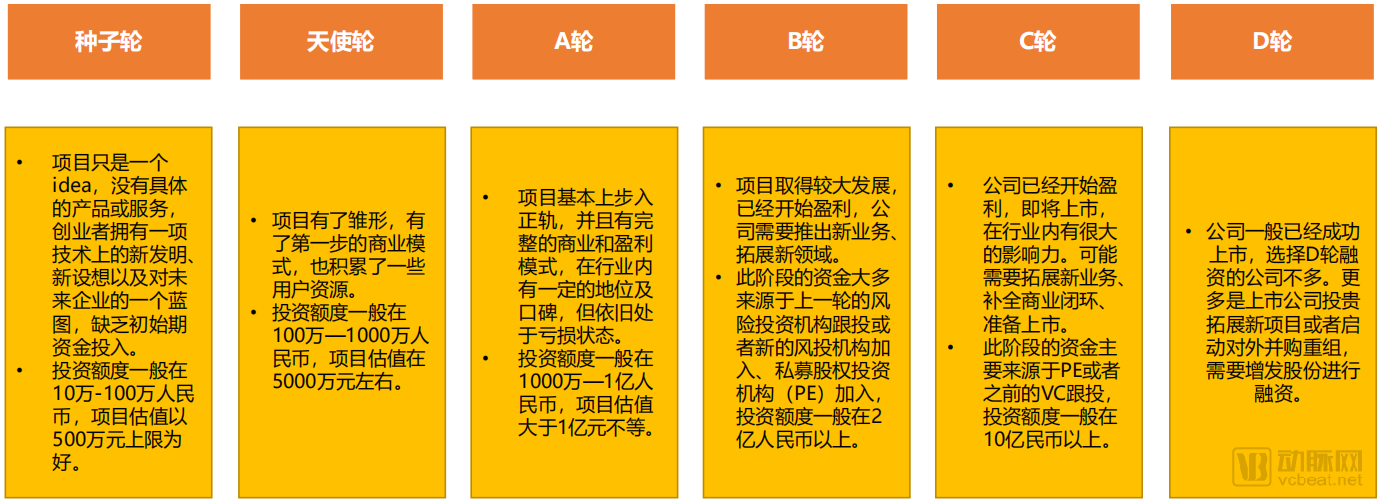

In industrial development,CapitalIt has served more as a catalyst, accelerating the growth of high-potential niche sectors.

We typically divide the healthcare sector into three major categories: medical services, pharmaceuticals, and medical devices.

AtHealthcare Services CompanyIn terms of investment, as a knowledge-intensive sector, the healthcare services industry inevitably places paramount importance on talent in its operations. The core of investing in healthcare services lies in how to attract, develop, and retain talent, and how to design effective talent incentive mechanisms.

InPharmaceutical Companiesin terms of investment, intellectual property and independent innovation are hot topics of interest to capital.

InMedical Device CompanyIn terms of investment, capital is increasingly focused on the R&D capabilities of medical device companies themselves, with a long-term view toward ensuring their products possess core competitiveness on a global scale. Beyond independent R&D capability, investors place greater emphasis on a company’s product capabilities, channel capabilities, and resource integration capabilities.

By analyzing capital investment trajectories, we have identified six key areas as the “golden tracks” for the future of rehabilitation: rehabilitation robotics, telerehabilitation, rehabilitation informatics, musculoskeletal rehabilitation, rehabilitation nursing, and cardiopulmonary rehabilitation.

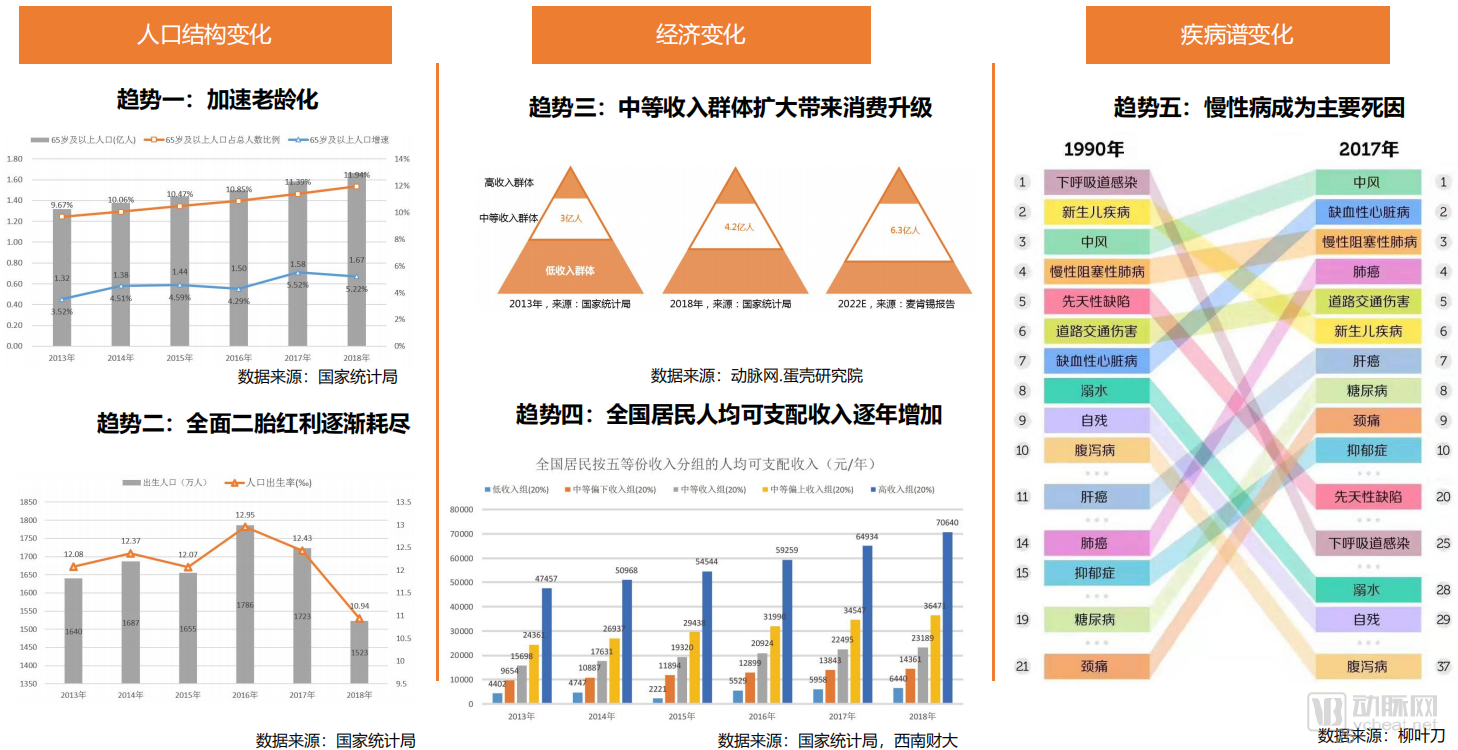

The driving forces behind changes in the healthcare industry lie in the rapid evolution of economic conditions, demographics, and disease spectra. Shifts in the economic landscape directly impact people’s ability to pay, while changes in demographics and disease spectra reflect shifts in the primary patient populations and healthcare demands.

Beyond the source, changes in technology, healthcare organizations, and social ideologies are also influencing the development of the healthcare industry.

FromThe Evolution of TechnologyFrom the perspective of, technological advancements will lead tochanges in other technology-related factors, thereby deducingReorganization of productive forces. As technology advances, therebyenhancing the quality of the labor force, means of labor, and subjects of laborAs technological capabilities advance, productivity will thereby reach a higher level.a step; therefore, technology has constrained the development of productivity.In the current era, technological development is the growth point of productivity.In modern society, the invention of the steam engine brought about transportationTransportation, textile, and smelting industries’ transformation, modernProductive forces emerged on the basis of the steam engine. Medical techadvancements in surgical techniques have driven generations of biomedical and healthcareThe upgrading of medical devices has become the driving force behind healthcare productivity.Make it longer.

Healthcare Organizationsan open subsystem within the broader social systemsystem, influenced by the social environment. Therefore, healthcare organizations must rootAdopt measures in accordance with changes in the productive forces and relations of production within the social systemCorresponding organizational structures to maintain adaptability to the environment.The activities of healthcare organizations are carried out under constantly changing conditions in the form of feedbacka process that trends toward organizational goals. Therefore, it is necessary to base decisions on the medical teamFormulate near-term and long-term objectives based on the prevailing conditions, and act in accordance with the situation.The demand for medical services is endless; in addition to the need for disease cure, patients...demand, as well as the need to improve health. Therefore, hospital organizations must becomeFor an open system, maintain acuity and stand from the patient's perspectivedegree, integrating the productivity changes brought by technology into patient needs.

With technological advancement, productivity innovation, and healthcare organization restructuringAdjustment,Patient-Centered Healthcare AwarenessBegins to form.Patient-centered medical awareness is the foundation of high-quality healthcare.an important component. At its core, it is based on the environment, culture,Differences in healthcare systems, recognizing patients and their families asAs a key member of the treatment team and the protagonist, prioritize the patient's valuevalues, personal preferences, and special needs into their treatmentwithin the plan.

The digital technologies, biotechnologies, intelligent manufacturing, and new material technologies emerging in this era are jointly shaping an interconnected long-term future. Leveraging general-purpose technologies such as the Internet of Things (IoT), 5G, gene sequencing, and big data, we are on the cusp of an intelligent era characterized by continuous sensing and seamless computing. Innovations in medical technology have already begun to emerge across prevention, diagnosis, treatment, and rehabilitation, exemplified by HPV vaccines, cell therapy, AI-driven medical diagnostics, and robotics.

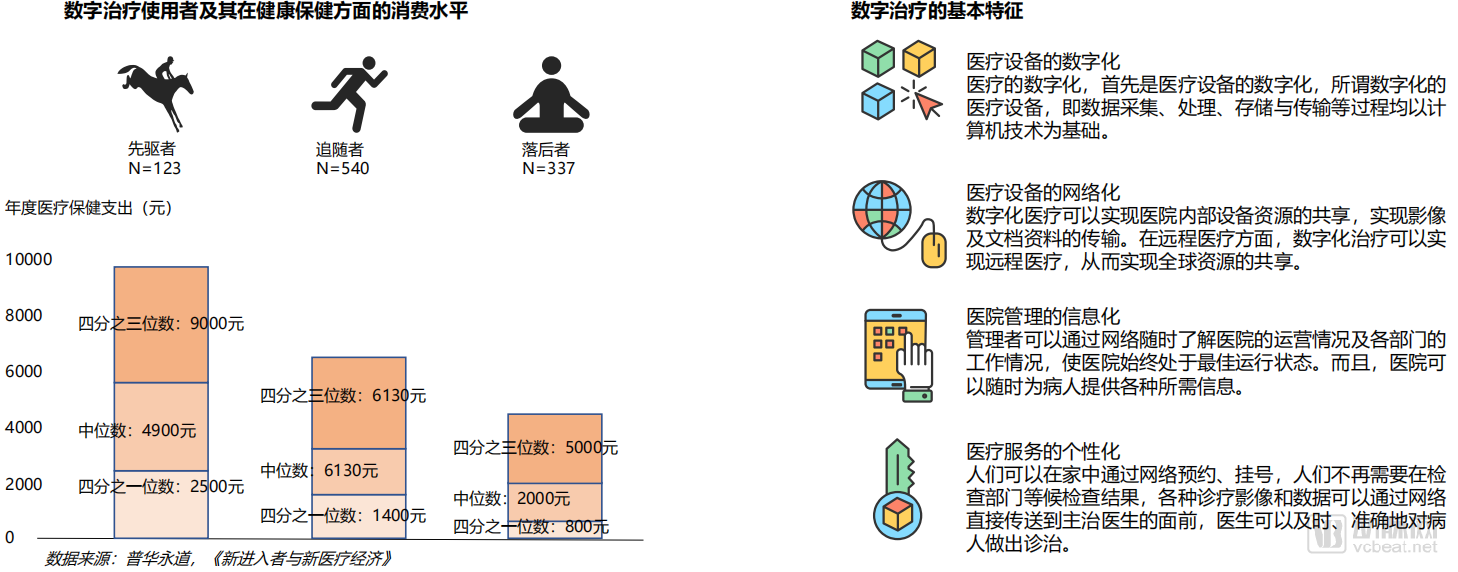

Digital therapeutics is a new, modernized healthcare model that applies contemporary computer and information technologies throughout the entire medical care process, representing both the developmental direction and management objective of public healthcare. According to BCG’s forecast, China’s digital therapeutics market will experience rapid growth over the next five years, with its value projected to reach $110 billion by 2020.

Digital therapeutics is far more than a simple aggregation of digital medical devices; it represents a new, modernized approach to healthcare that applies contemporary computer and information technologies throughout the entire medical process. In digital therapeutics, patients can complete consultations with minimal procedural steps, while physicians’ diagnostic accuracy is significantly improved. Patient electronic health records capture all current and historical health information, greatly facilitating clinical diagnosis and patient self-monitoring. This enables true remote consultations by allowing comprehensive access to patient data, thereby delivering rapid and effective services. Another major advantage of digital healthcare is the ability to share resources between medical equipment and medical experts. For healthcare institutions, maintaining a database with comprehensive health information enhances authority, and the establishment of robust health information systems can substantially boost competitiveness.

From a medical perspective, disease treatment is a gradual process that requires long-term follow-up and behavioral intervention, involving the processing and transmission of vast amounts of information. Digital therapeutics represents an emerging trend driven by technological advancements. Taking artificial intelligence (AI) as an example, it is precisely due to the development of AI technology that the scope of digital therapeutics has expanded into AI-related fields.

Regardless of how digital healthcare evolves in the future, it will always be built upon existing technologies. No matter how powerful the functions of future hospitals become, they will be realized on a fundamental framework. This framework can be simply summarized into four components: digital medical devices, networks composed of these digital devices, digital healthcare systems operating on top of these networks, and services based on these digital healthcare systems.

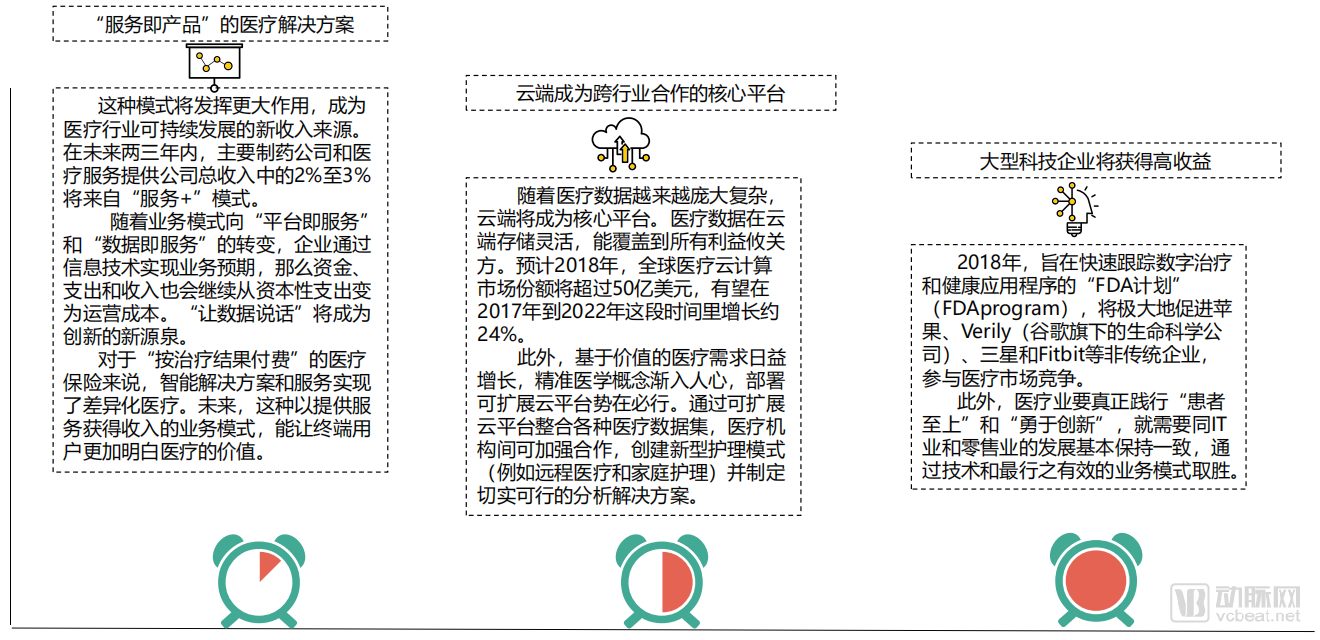

The wave of digital therapeutics will bring ecological and interactive changes to the medical treatment process, driving three major trends: “service-as-a-product” healthcare solutions, the cloud becoming a core platform for cross-industry collaboration, and large technology companies reaping high returns.

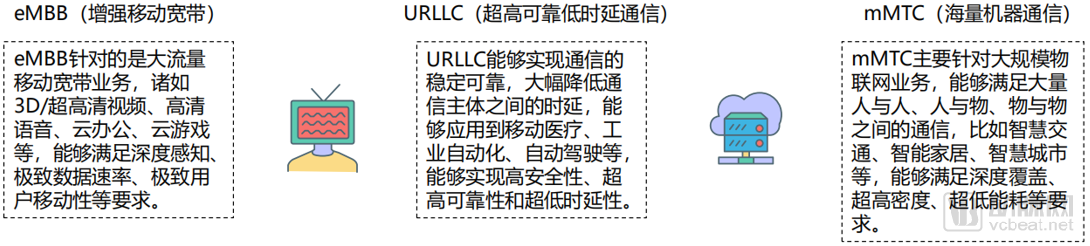

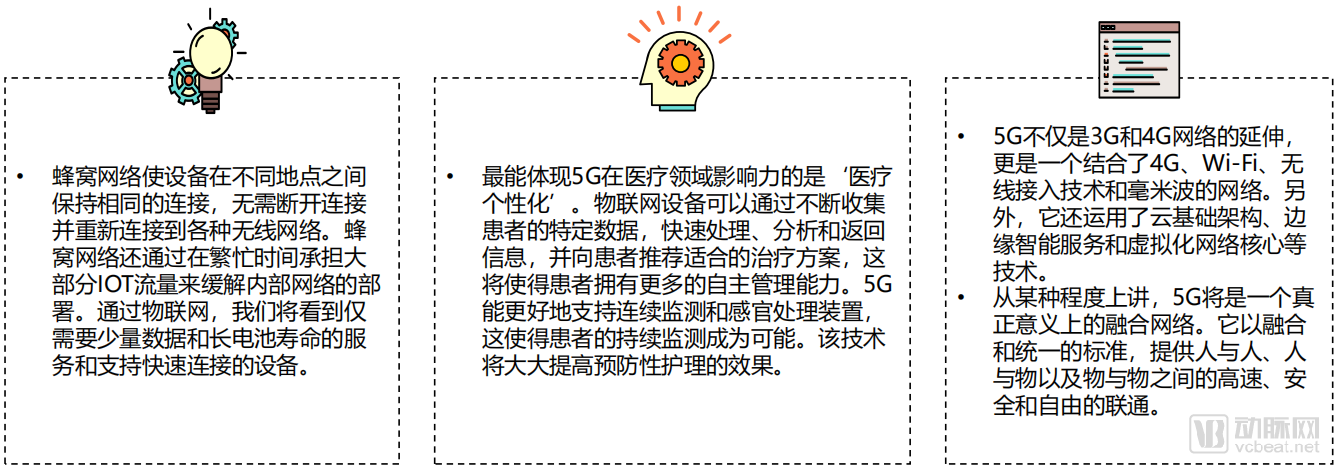

5G integrates a series of advanced communication technologies, including millimeter wave, small cells, network slicing, and beamforming. It provides mobile network support for applications across various industries, such as voice, audio-video, gaming, VR/AR, artificial intelligence, the Internet of Things (IoT), and robotics, thereby driving the digital transformation of the entire socio-economic landscape. 5G offers mobile communication support for high-definition video, IoT, VR/AR, and robotics, and will be widely applied in sectors such as smart transportation, mobile healthcare, cloud gaming, smart homes, and industrial automation. The volume of data generated will grow exponentially, with user peak rates reaching 10 Gbps, ushering in an era of explosive data growth.

5G is able to provide communication guarantees for technological applications across various industries, thanks to the support of a series of key technologies behind it. For instance, high-frequency millimeter waves offer high bandwidth and large information transmission capacity. Network slicing allows for the configuration of multiple independent or shared communication networks based on the requirements of different application scenarios. Additionally, end-to-end technology enables direct data transmission between devices without relying on third-party base stations, thereby reducing latency.

Therefore, whether in terms of its new features or the key technologies on which it is based, the performance metrics demonstrated by 5G are unmatched by previous generations of mobile communication systems. How, then, does 5G achieve its application value through its architecture?

Cellular, Wi-Fi, and Bluetooth enable cross-platform usage of the Internet of Things (IoT), while 5G serves as the connecting link. IoT devices have diverse functionalities and data requirements, all of which can be supported by 5G networks.

5G differs from its predecessors in terms of connected devices, fast and intelligent networks, backend services, and ultra-low latency. These characteristics make a fully interconnected world possible. By 2020, 5G networks will support over 20 billion connected devices and 21.2 billion connected sensors, enabling access to 44 zettabytes of data collected from various devices ranging from smartphones to remote monitoring equipment. This ecosystem will make true big data a reality.

In the healthcare sector, not all scenarios require 5G, nor is 5G sufficiently perfected to support every application scenario. Based on preliminary research and a review of relevant literature, we have found that 5G can fully leverage its advantages only in medical scenarios that involve large-scale data transmission, require high-definition video, or demand low-latency information transfer.

Wireless MonitoringWireless monitoring refers to the real-time, continuous surveillance of patients’ vital signs, such as blood pressure, blood glucose levels, and heart rate, using vital signs monitors or wearable smart devices, and transmitting this physiological data to healthcare professionals via wireless communication. Wireless monitoring must continuously, in real time, and dynamically reflect the vital signs of the monitored individual, transmitting analyzed and processed data to the display terminals of medical staff to enable real-time situational awareness. This is particularly critical for patients with sudden-onset diseases, as the alarm response time of wireless monitoring systems directly impacts the emergency rescue response time. In addition to monitoring medical devices and patients’ vital signs, these systems can also facilitate control over certain equipment. For instance, in wireless infusion monitoring, a 5G-based wireless infusion management system can leverage Internet of Things (IoT) devices, such as infusion monitors, to track patients’ infusion progress in real time. Leveraging the low-latency characteristics of 5G networks, the system can rapidly alert nurses if needle dislodgement occurs or when the infusion is nearing completion, enabling prompt intervention by nursing staff and thereby preventing medical incidents.

Massive Internet of ThingsThe Internet of Medical Things (IoMT) ecosystem will encompass millions or even billions of low-power, low-bit-rate medical health monitoring devices, clinical wearables, and remote sensors. Relying on these instruments, physicians can continuously collect patient medical data, such as vital signs and physical activity. This data is received in real time by healthcare providers, enabling them to effectively manage or adjust treatment plans. Furthermore, these data support predictive analytics, allowing physicians to more rapidly identify health patterns in monitored individuals, thereby improving diagnostic accuracy.

Technological upgrades in the healthcare industry have created significant opportunities for telecom operators to penetrate new value chains, fostering collaboration across the entire Internet of Things (IoT) ecosystem. It is projected that by 2026, operators with a combined turnover of $76 billion will transition toward 5G-enabled healthcare solutions. Successful transformation will hinge on robust collaboration among diverse stakeholders within the industrial chain. According to Ericsson ConsumerLab’s report, “Healthcare to Home Care,” 86% of cross-industry decision-makers believe that, beyond their role as network providers, operators can also offer system integration as well as application and service development.

To enable a shift in how patient applications are handled, patient data must be centrally stored, ultimately transforming hospitals into data centers and physicians into medical data experts. This will allow patients to access medical databases online, helping them easily manage the quality and efficiency of their care. Forty-five percent of cross-industry experts believe this will represent a revolutionary breakthrough in healthcare services, while 47% of telecommunications decision-makers consider secure access a key challenge. One expert stated, “Through these monitoring technologies, 5G will undoubtedly provide the capability for doctors to stay connected with patients, whether outside an ambulance or in the patient’s home.”

At present, 5G technology is not yet mature. However, by 2019, the first wave of suppliers plans to unlock its full potential. According to a market report by IHS, sales of 5G technology are projected to reach $1.1 trillion by 2035, accounting for more than 9% of the global 5G economy, which is estimated at $12.3 trillion. This impact is roughly equivalent to adding an economy the size of India’s current GDP to the global economy. Furthermore, the value chain associated with 5G is expected to generate $3.5 trillion in output and create 22 million new jobs worldwide. Achieving these goals will require more than just leveraging the technology itself. The industry has already begun shifting toward outcome-based models, and changes in government policy will help accelerate this transition—for instance, by providing incentives to suppliers through tax breaks and other policy measures. Policies must safeguard innovation and intellectual property rights to ensure that 5G developers receive appropriate compensation.

CAR-T therapy is no longer a novel concept. Since the approval and market launch of two CAR-T products by Novartis and Kite in 2017, global enthusiasm for cellular immunotherapy has rapidly intensified. Its R&D pipeline now ranks first in the entire field of cancer immunotherapy, and immunotherapy is regarded as the fourth pillar of cancer treatment, following radiotherapy/chemotherapy, surgery, and targeted therapy. According to a report in Nature Reviews Drug Discovery, as of March this year, there were 1,011 approved or investigational cellular immunotherapies worldwide, an increase of 258 from the same period last year. Among these, CAR-T therapies accounted for more than half, totaling 568 products, which represents an increase of 164 compared with March 2018, reflecting the industry’s strong enthusiasm for CAR-T therapy. The United States and China had more than 400 and 300 approved and investigational cellular immunotherapy products, respectively, together accounting for approximately three-quarters of the total.

In addition to enthusiasm from the industry, national healthcare insurance systems have also demonstrated acceptance and recognition of CAR-T therapy. Following the inclusion of CAR-T therapy in the national health insurance schemes of the United Kingdom and the United States, Japan announced its inclusion in May this year. On October 30, Kymriah, the world’s first CAR-T therapy developed by Novartis, received implicit approval for clinical trials in China. These developments indicate that demand in European and American markets will continue to grow, and China may also introduce this drug for clinical use in the future.According to Coherent Market Insights, the global CAR-T cell therapy market is projected to grow at a compound annual growth rate (CAGR) of up to 46.1% from 2018 to 2028.In the coming years, North America will continue to account for more than 50% of the global market share for CAR-T cell therapy, with Europe ranking second. However, as China advances its CAR-T-related policies and intensifies R&D efforts, an increasing number of companies are entering the CAR-T industry. China is poised to overtake competitors in the near term and capture a significant portion of the global market share.

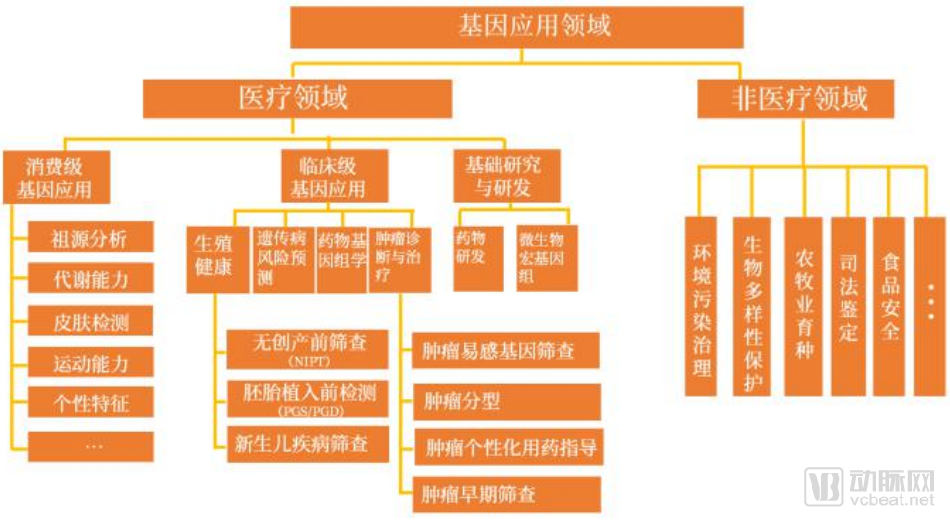

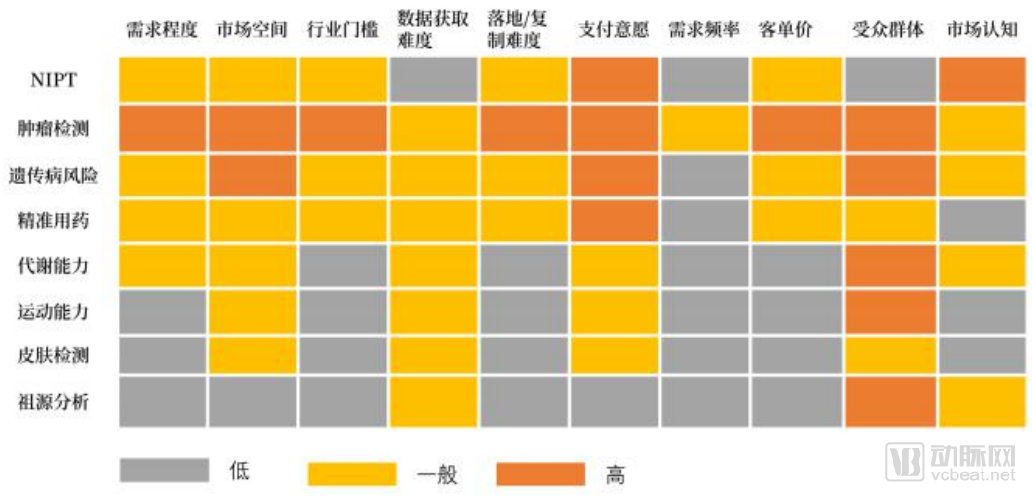

The applications of genetic testing are primarily concentrated in the healthcare sector, with the most commercialized segments poised for the strongest future growth. Advances in gene sequencing technology have enabled individuals to explore their genetic origins, while progress in genetic interpretation and gene editing has ushered in a new era of proactive health management. Currently, genetic technologies are mainly applied in both medical and non-medical fields. We have developed a series of evaluation metrics specifically for genetic technologies in the healthcare sector to conduct commercial assessments and identify the segments with the most promising growth potential.

Based on current research directions in genetic testing, its applications are generally categorized into medical and non-medical fields. The medical field primarily encompasses consumer-grade genetic applications, clinical-grade genetic applications, and basic research and development.

Based on the indicator system of VCBeat and Eggshell Research Institute, we can evaluate gene applications. It is highly likely that tumor detection, genetic disease risk prediction, precision medication, and metabolic capacity applications will become the areas with the best development momentum in the future.

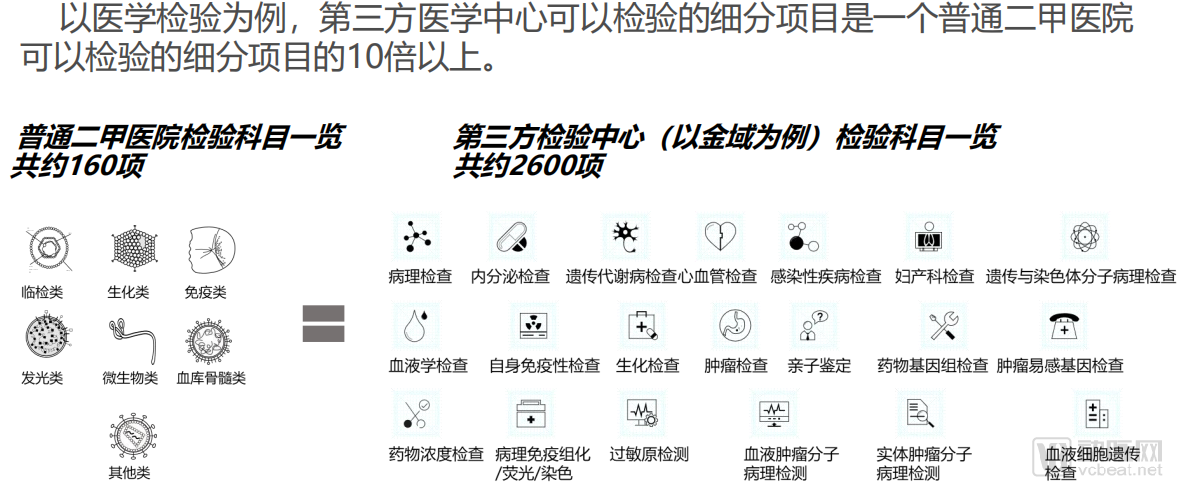

Third-party medical service providers, also known as "independent medical service institutions," refer to entities established outside the traditional hospital system that specialize in providing specific diagnostic, laboratory testing, or specialized medical services.

In October 2013, the government issued the “Several Opinions on Promoting the Development of the Health Service Industry,” vigorously developing third-party services and guiding the establishment of specialized medical laboratory centers and imaging centers. On February 21, 2017, the National Health and Family Planning Commission added five new categories of medical institutions: medical laboratories, pathology diagnosis centers, medical imaging diagnosis centers, hemodialysis centers, and hospice care centers. In August 2017, the National Health and Family Planning Commission introduced another five categories of independently established medical institutions, including rehabilitation medical centers, nursing centers, sterile supply centers, small and medium-sized ophthalmic hospitals, and health examination centers.

According to data from the 2018 China Health and Family Planning Statistical Yearbook, there are currently 29,000 hospitals nationwide.There are nearly one million medical and health institutions. If it is required that all primary-level medical and health institutions establish laboratory testing services,Radiology and Pathology: Significant Shortage of Practitioners.Centralize the establishment of third-party medical institutions and open them to primary care facilities, ensuring quality whileFacilitates the concentration of limited medical resources and enables regional resource sharing.

MeanwhileAdvances in medical device technology have standardized certain medical procedures, enabling their delivery outside hospital settings.Feasibility Support.Some high-end technologies do not generate sufficient patient volume at a single hospital, making them cost-ineffective. IfThe provision of services by independent third parties, managed through contractual agreements, facilitates quality control and ensures medical quality.Quantity and Safety.

Therefore,Under the guidance of the tiered diagnosis and treatment policy, the status of third-party medical institutions has been recognized to achieve broader regional resource sharing.

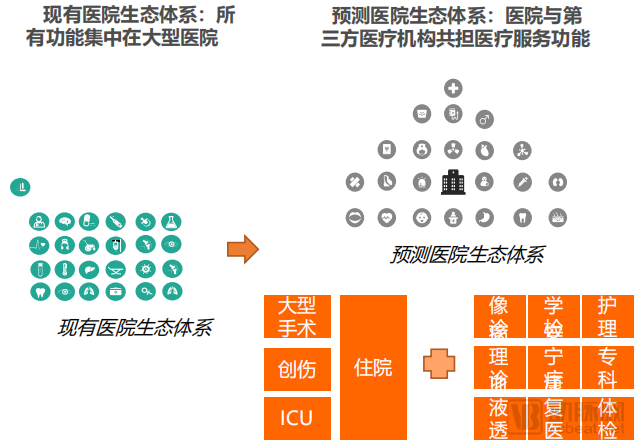

Amid the development trends of third-party medical institutions, we predict that hospitals will undergo a functional shift outward, forming an ecosystem in which hospitals and third-party medical institutions jointly deliver healthcare services.

Based on VCBeat’s accumulated industry insights, we roughly categorize third-party medical service providers into four distinct markets, using a market size of RMB 50 billion as the threshold for market capacity and a count of 200 related enterprises as the threshold for competitive landscape. As the market structure and business models become increasingly clear, potential and niche markets are entering their growth phase.

Third-party medical service providers essentially fall under the category of capital-intensive service industries. Their characteristic lies in the difficulty of scaling up; however, once they achieve scaled development, the “Matthew Effect” becomes more pronounced, offering substantial potential returns. A key competitive factor in the third-party medical services industry is financing capability, as only with continuous capital support can these institutions expand and realize the potential for chain-based and group-oriented development. The second critical factor is operational capability, because third-party medical service providers involve diverse aspects and functional requirements; operators must fully coordinate and integrate various resources to ensure the enterprise maintains steady growth. Between these two factors, we believe that the management team’s operational capability is the key to securing capital support, making it the more important of the two.

Industry standards and operational guidelines have been issued, while relatively unregulated sectors such as health checkups and ophthalmology are engaged in cutthroat competition.Meanwhile, imaging centers and pathology centers that serve clinical practice have a key observation point in this process: the state’sThe reallocation direction of these existing resources.For example, the replacement cycle for imaging department equipment is 10–15 years, and we are now approaching the next wave of equipment upgrades.We need only to observe the level of state support for imaging equipment in Tier II and Tier I hospitals.

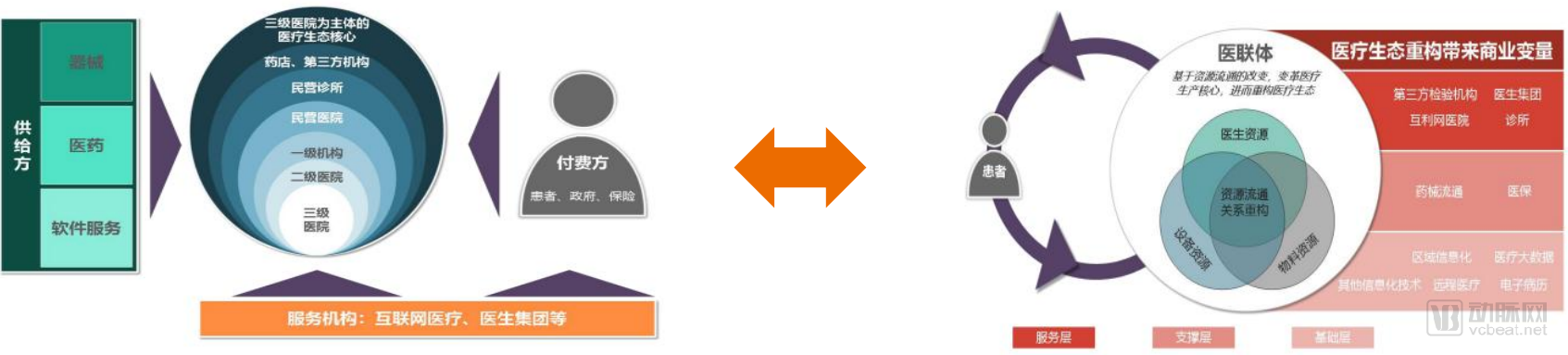

Traditional healthcare institutions are delineated by geography. Medical consortia, leveraging advanced information technology, have redefined the boundaries of these traditional entities. Within a medical consortium, multiple healthcare institutions in a given region are integrated as functional departments based on their respective capabilities and strengths, through functional segmentation and task redistribution. Consequently, the medical consortium operates as a larger, unified healthcare institution, where geographical constraints are weakened and the boundaries of traditional healthcare institutions are redefined.

Profound transformations within healthcare institutions, particularly in their internal relationships, will inevitably impact external suppliers, payers, and various service providers. Formally speaking, the Medical Consortium policy redefines the business relationships among healthcare institutions; from a commercial perspective, reforms driven by medical consortia are bound to dismantle the traditional healthcare value chain. For market participants, this shift conceals substantial changes and risks, while also harboring significant business opportunities.

By leveraging medical consortia, the internal linkages within the institutional framework—the core of the healthcare ecosystem—are transformed, thereby influencing the interrelationships among external payers, suppliers, service providers, and the ecosystem’s core. This shift drives a restructuring of the value distribution system and creates new commercial opportunities.

“Smart Hospital” is a concept derived from technology and outcomes; it is neither a mere accumulation of technologies nor a synonym for any single function. A smart hospital is characterized by informatization, intelligence, and internet integration.

Informatization refers to the establishment of multi-dimensional data systems and their integration platforms within hospitals. Intelligentization denotes the application of big data, cloud computing, Internet of Things (IoT) technologies, automated equipment, robotics, and intelligent workflow and operation management systems. Internet-based transformation involves the deployment of mobile applications that facilitate data input and output for medical staff and patients across pre-diagnosis, intra-diagnosis, and post-diagnosis stages. Smart hospitals enable interconnectivity among patients, medical personnel, healthcare institutions, and medical devices, thereby enhancing hospital operational efficiency and optimizing the experience of medical services throughout the pre-diagnosis, intra-diagnosis, and post-diagnosis phases.

In August 2014, the National Development and Reform Commission (NDRC), jointly with the Ministry of Industry and Information Technology (MIIT) and six other ministries, issued the “Guiding Opinions on Promoting the Healthy Development of Smart Cities,” which proposed advancing the development of smart hospitals and telemedicine. This marked the first time that the concept of building “smart hospitals” was officially introduced. Subsequently, both central and local governments rolled out a series of policies, propelling the construction of smart hospitals into a period of rapid growth.

From top-level design to local policies, and from technical guidance to evaluation metrics, the release of a series of policies has driven the empowerment of hospitals by new technologies such as artificial intelligence, information technology, the Internet of Things (IoT), big data, and cloud computing, facilitating the implementation of smart hospitals with higher efficiency and better services. It is expected that in the near future, clear definitions of smart hospitals and specific policy support for their construction will be rolled out successively.

The healthcare journey shapes patients’ overall experience in hospitals. For a long time, the cumbersome process—including queuing, registration, waiting for consultation, payment, examinations, follow-up visits, additional payments, treatment, medication pickup, and discharge—has led to inefficient service delivery and decreased patient satisfaction. Currently, many hospitals are undertaking healthcare process reengineering, with outpatient services serving as a prime example.

Outpatient services serve as the window of hospital care. Leveraging information technology, outpatient departments offer appointment-based scheduling and time-slot consultations to rationally organize the patient journey, thereby reducing wait times. This approach enhances the optimization of patient care, streamlines service processes, minimizes unnecessary patient movement and waiting within the hospital, improves service quality, and greatly facilitates access to medical care for patients.

The Construction of Future Smart Hospitals Will Face Ten Major Demands:

Improving healthcare quality and avoiding medical errors require effective data support and necessary human resources.

Medical safety, such as quantifying drug efficacy through Internet of Things (IoT) and intelligent technologies, and continuously monitoring patient vital signs.

Reduce physicians' workload and enhance their efficiency by automating standardized and norm-based clinical workflows, thereby improving the overall productivity of healthcare professionals.

Enhance the experience of patients and physicians by developing internet-based application systems, such as patient service platforms and optimized physician work platforms.

Optimize processes by streamlining cumbersome workflows through mobile devices.

Enhance resource utilization by leveraging Internet of Things (IoT), intelligent, and interconnected technologies to enable smart management of hospital resources, thereby improving the effective utilization of expert, equipment, and ward resources.

Reduce healthcare costs by establishing corresponding systems to optimize hospital management and achieve cost-containment objectives.

Enhance the level of scientific decision-making, supported by artificial intelligence systems to meet this need.

Enhance the Level of Scientific Research and Support Hospital-Based Research Through Big Data Technology.

Enhanced medical collaboration facilitates interdisciplinary coordination within hospitals, inter-hospital healthcare synergy, and seamless interoperability across various systems.

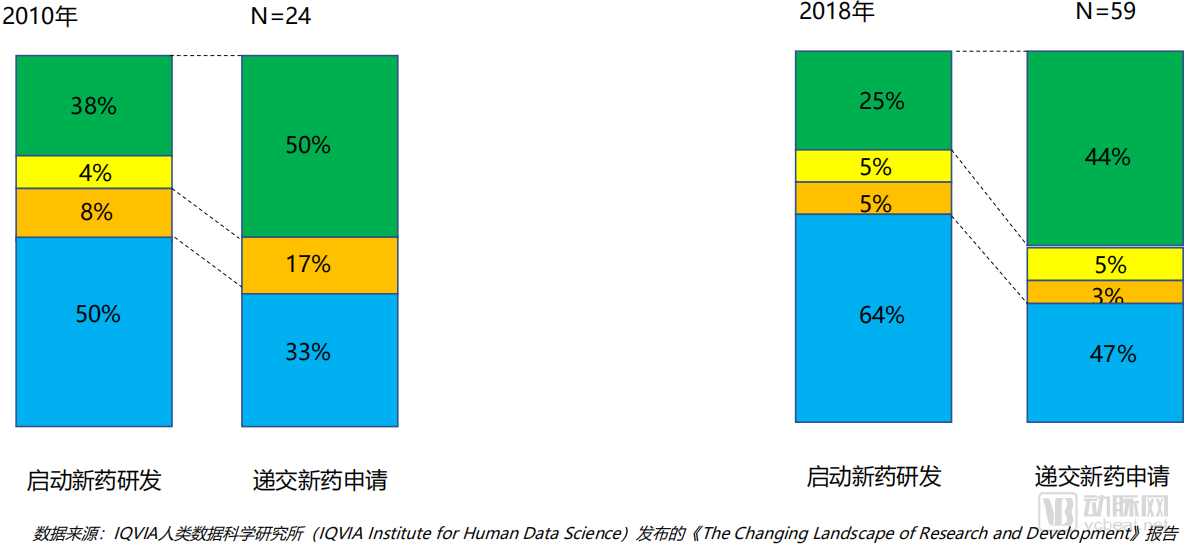

Among the 59 new drugs approved in the United States in 2018, fewer than half were submitted by large pharmaceutical companies. Moreover, among the approved drugs, 64% of the new medicines originated from initial R&D activities conducted by emerging biopharma (EBP) companies.

Emerging biopharmaceutical companies (EBPs) are defined as those with global annual sales of less than $500 million and R&D expenditures of less than $200 million in the most recent year. These EBP companies not only initiated the development of the majority of newly approved drugs but also advanced 66% of their pipeline products to the stage of submitting new drug applications. This indicates that these EBP companies have made significant contributions to initiating innovative R&D and possess both the willingness and capability to drive product development through to the submission of new drug applications.

The value chain of pharmaceutical companies is shifting. From the perspective of ecosystem building, they are transforming their business models in terms of processes, services, and stakeholder engagement to provide patients with comprehensive digital solutions that include products.

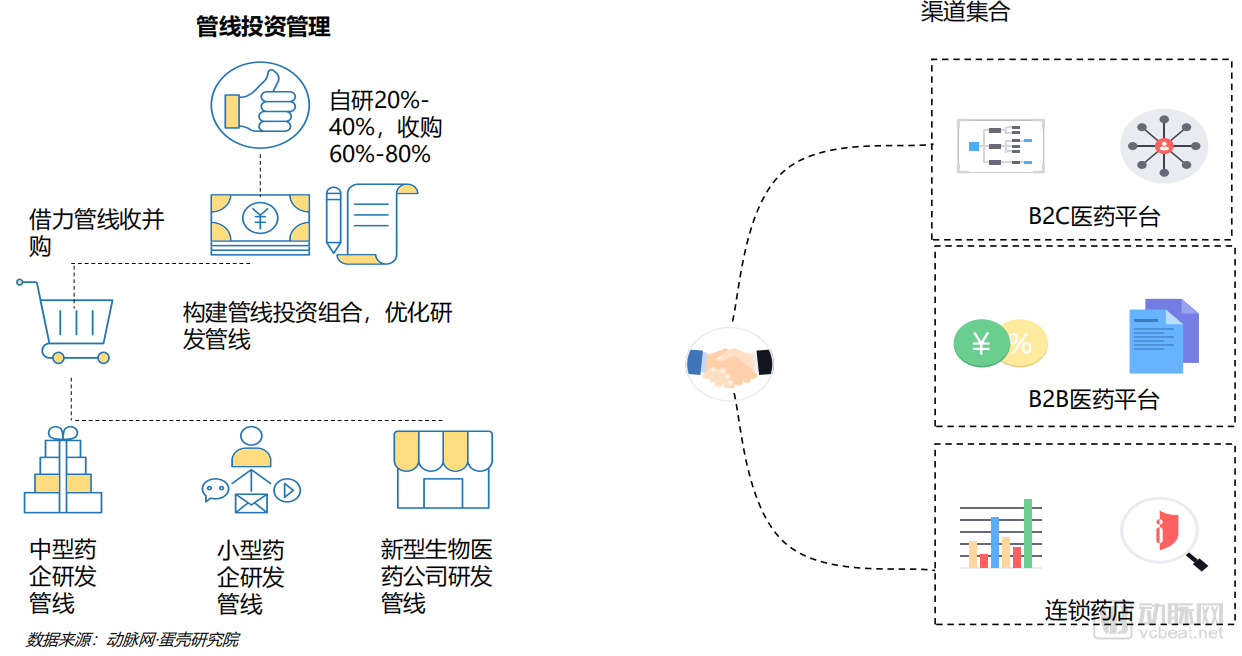

Data from late-stage clinical research pipelines indicate that novel biopharmaceutical companies accounted for 72% of all late-stage R&D projects in 2018, while large pharmaceutical companies accounted for only 20%. Large pharmaceutical companies primarily rely on pipeline investment strategies, such as mergers and acquisitions, to strengthen their R&D pipelines. Consequently, the fundamental logic of pipeline investment management for many large pharmaceutical companies has become enhancing their pipelines by investing in in-development or soon-to-be-launched blockbuster drugs, thereby achieving product portfolio complementarity and synergistic scale effects.

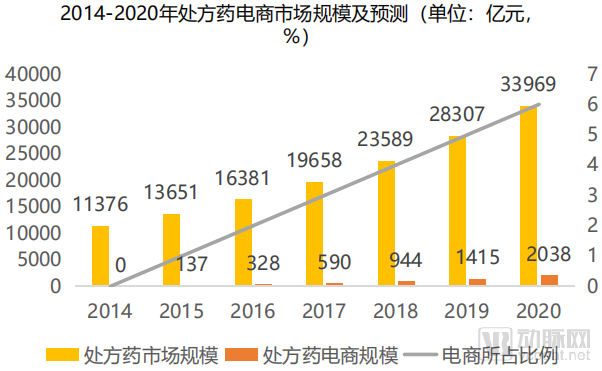

With the gradual implementation of the “4+7” volume-based procurement policy, the drug procurement model has undergone significant changes. In addition to striving to win bids for the in-hospital market, pharmaceutical companies are adapting to the trend by leveraging e-commerce platforms to open up new marketing channels and make a substantial entry into the out-of-hospital market.

Establishing platforms to reduce distribution costs via internet channels is essential for alleviating pressure. After embracing online operations, many pharmaceutical companies have witnessed a substantial average increase in revenue from pharmaceutical e-commerce, far exceeding the growth rate of traditional pharmaceutical distribution and sales models. The “Internet + Healthcare” model has brought immense hope and possibilities to pharmaceutical enterprises.

Declining marginal costs have made it more profitable for pharmaceutical companies to bolster their R&D capabilities through the acquisition and merger of drug pipelines. Meanwhile, driven by economies of scale, it is more beneficial for small and medium-sized pharmaceutical enterprises to sell their R&D pipelines to larger firms to support their own development. Policy initiatives and the consolidation of marketing channels are inevitable paths for pharmaceutical companies to reduce costs. In the future, China’s pharmaceutical industry will see a trend toward channel simplification. This streamlined channel structure imposes higher demands on market operations while offering greater development opportunities for companies with competitive product portfolios.

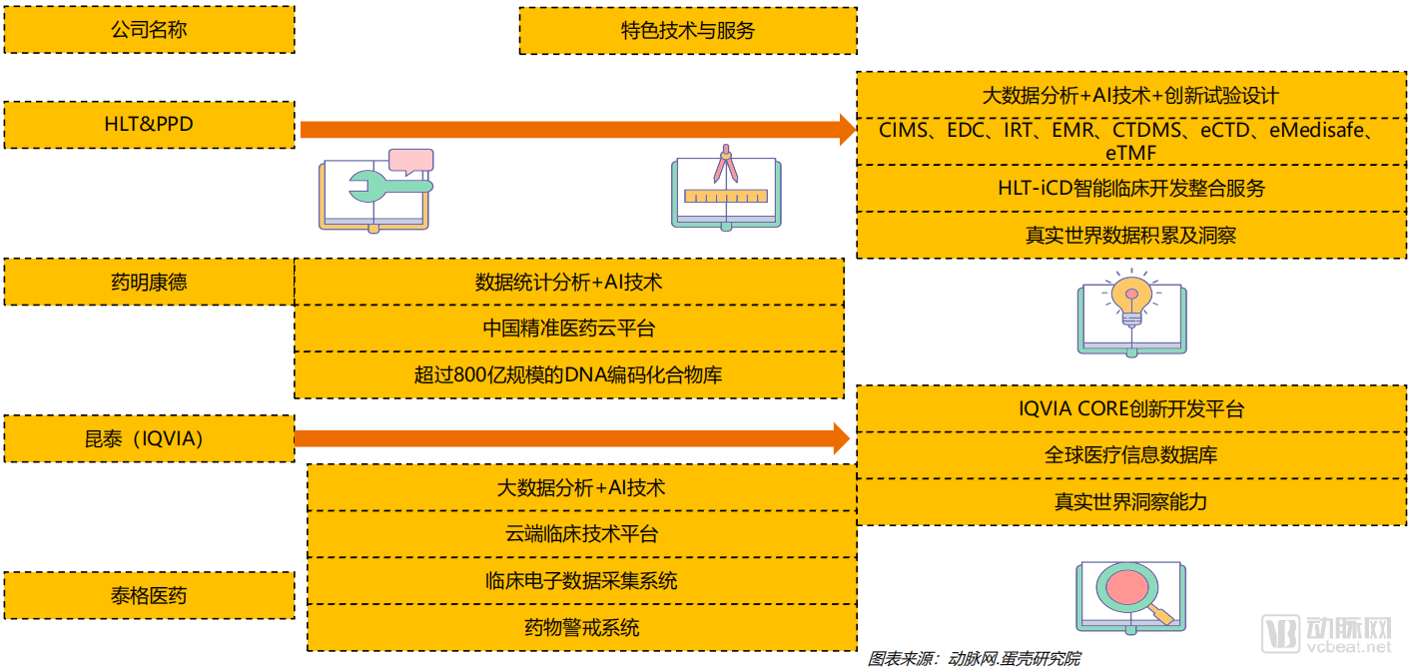

CRO (Contract Research Organization), or contract research organization, refers to an academic or commercial scientific institution that provides specialized services to pharmaceutical companies and R&D institutions during the drug development process through contractual agreements. Here, CROs are the primary representatives of the trend toward smaller, high-value research institutions.

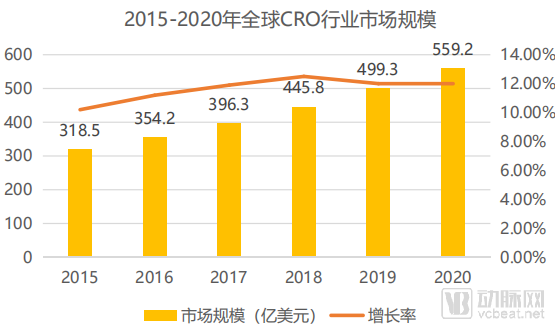

Despite the rapid development and expanding market size of the global CRO industry, high R&D costs are driving a gradual shift toward emerging countries such as China and India, where the CRO sector is relatively mature and labor costs are lower. According to data from the Southern Institute of Pharmaceuticals, China’s CRO market size was only RMB 37.9 billion in 2015, rising to RMB 67.8 billion in 2018, representing a compound annual growth rate (CAGR) of 21% from 2015 to 2018. Conservatively estimated, the Chinese CRO industry will maintain an annual growth rate of approximately 20% over the next two to three years, with the market size approaching RMB 100 billion by 2020.

As global pharmaceutical companies face declining R&D success rates, prolonged development cycles, and rising R&D costs, the return on investment for new drug development continues to decline. To reduce their own R&D expenses and mitigate risks, pharmaceutical companies are increasingly outsourcing part or all of their new drug R&D activities to small, specialized research organizations.

Furthermore, as multiple blockbuster patented drugs expire globally, pharmaceutical companies are facing a "patent cliff." In a bid to capture market share and maintain dominant positions, international pharmaceutical giants have ushered in a new wave of drug research and development. To enhance efficiency and reduce R&D costs, an increasing number of pharmaceutical firms are outsourcing to small, specialized research institutions through the Contract Research Organization (CRO) model. With the CRO penetration rate continuously rising, the development prospects for these small, specialized research institutions remain promising.

High-value, miniaturized CROs are defined in contrast to traditional CROs. They primarily refer to CRO enterprises that leverage innovative technologies such as big data, AI, and cloud computing to accelerate clinical trial processes, shorten drug development cycles, and reduce R&D costs, or that innovate their business models to provide preclinical and clinical trial services with greater precision, efficiency, and leanness. Consequently, traditional CROs are also gradually strategizing in this direction, deepening their professional expertise and strengthening the provision of specialized technologies and services.

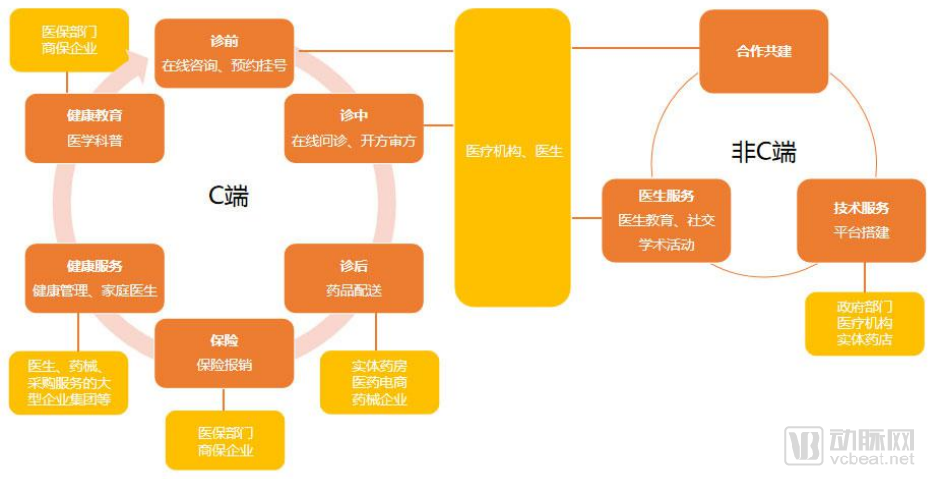

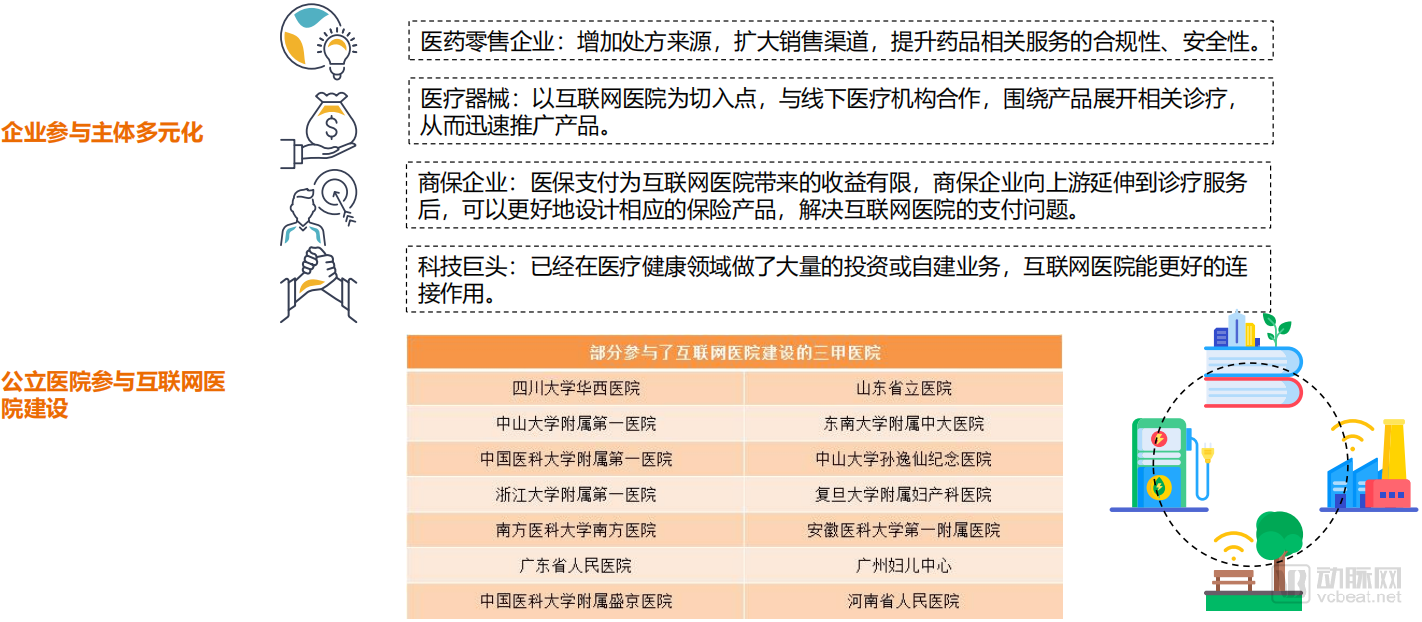

In the schematic diagram, orange represents the business processes of internet hospitals targeting different user groups, while yellow indicates the participants connected to these respective processes. Currently, with medical institutions and physicians at their core, internet hospitals have nearly connected all participants in the healthcare industry through self-built or collaborative business operations.

After years of exploration, internet hospitals finally achieved policy certainty in 2018, entering a new stage of development. In 2019, the construction of internet hospitals entered another peak period; as of November 8, 2019, an additional 125 enterprises had participated in the development of internet hospitals.

To date, internet hospitals have long moved beyond the initial stages of appointment registration and online consultations. They no longer merely provide follow-up visits for certain common and chronic diseases and “Internet+” family doctor contracting services as stipulated in the Administrative Measures for Internet Diagnosis and Treatment (Trial). Instead, using these services as a starting point, they are continuously expanding their offerings and enhancing connectivity. Therefore, based on the construction and development trends of internet hospitals this year, we believe that the industrial ecosystem of internet hospitals is gradually maturing, with its scope steadily expanding.

Why Are Internet Hospitals Continuously Expanding to Build a More Comprehensive Industrial Ecosystem? We Primarily Explore the Reasons from Two Perspectives: Market Demand and Policy Guidance.

From the perspective of market demand:

Purely medical needs are low-frequency and involve relatively low per-customer transaction values, making it difficult to achieve profitability through online consultations alone. In contrast, healthcare encompasses multiple stages with varying frequencies of demand. Notably, consumer-grade medical services and health management needs are gradually increasing. By leveraging online consultations as a bridge, internet hospitals can facilitate broader connectivity while ensuring compliance in diagnosis and treatment, thereby better exploring sustainable revenue models.

JD Health, which previously focused primarily on pharmaceutical e-commerce, unveiled a new strategy this year centered on “health management,” following its entry into the internet hospital sector in late 2017. This strategy aims to connect and integrate the entire industry chain, merge diverse medical resources, and provide users with products and services that span the full life cycle and cover all health-related scenarios. In an interview with VCBeat, JD Health CEO Xin Lijun stated that few sectors within healthcare and medicine operate in isolation; entering this field inevitably involves nearly all aspects of it. This underscores that internet hospitals can hardly sustain themselves through standalone diagnostic and treatment services, making comprehensive connectivity crucial.

From a policy perspective

The newly revised Drug Administration Law specifies the list of drugs prohibited from online sales, which does not include prescription drugs. This implies that the online sale of prescription drugs is not explicitly banned, although specific regulatory measures remain to be formulated by the regulatory authorities. As internet hospitals have already been granted prescribing authority for follow-up consultations on certain common and chronic diseases, they will become a major source of prescriptions for online prescription drug sales, thereby accelerating the integrated development of internet hospitals with pharmaceutical e-commerce platforms, pharmacies, and pharmaceutical and medical device enterprises.

Furthermore, the lack of integration with medical insurance payment systems has long been regarded as a major obstacle to the development of internet hospitals. On August 30 this year, amid keen anticipation from the industry, the National Healthcare Security Administration officially issued the “Guiding Opinions on Improving Price and Medical Insurance Payment Policies for ‘Internet+’ Medical Services,” providing clear direction for medical insurance payments in internet hospitals. Starting in October, Yinchuan began piloting medical insurance reimbursement for online consultations for hypertension and diabetes at internet hospitals. The introduction of national medical insurance policies and the launch of local pilots have been encouraging for the industry, as they represent further recognition of internet hospitals and provide greater impetus for online management of common and chronic diseases. However, the national policy imposes strict requirements on pricing items for “Internet+” medical services, emphasizing core diagnostic and treatment components. This means that internet hospitals built with corporate participation will find it difficult to generate substantial revenue directly from medical insurance funds; instead, they should explore new technologies and services to promote cost reduction and efficiency improvement in healthcare delivery.

Diversification of Participants in Internet Hospitals

A review of the development of internet hospitals reveals that, in the early stages, enterprises involved in their construction were primarily internet or health IT companies. Leveraging their technological advantages, these firms rapidly facilitated the digital transformation of hospitals. However, since the beginning of this year, we have observed a further diversification of the enterprises participating in the development of internet hospitals. In addition, public hospitals are increasingly establishing their own internet hospital platforms.

For tertiary hospitals, establishing internet hospitals can migrate offline medical resources online, improving the efficiency of medical services for common and chronic diseases. For complex and critical cases, methods such as remote consultations and collaboration within medical consortiums can facilitate the downward distribution of high-quality medical resources, thereby promoting the implementation of tiered diagnosis and treatment, or preventing patients from seeking care across regions, thus alleviating the issue of uneven distribution of medical resources.

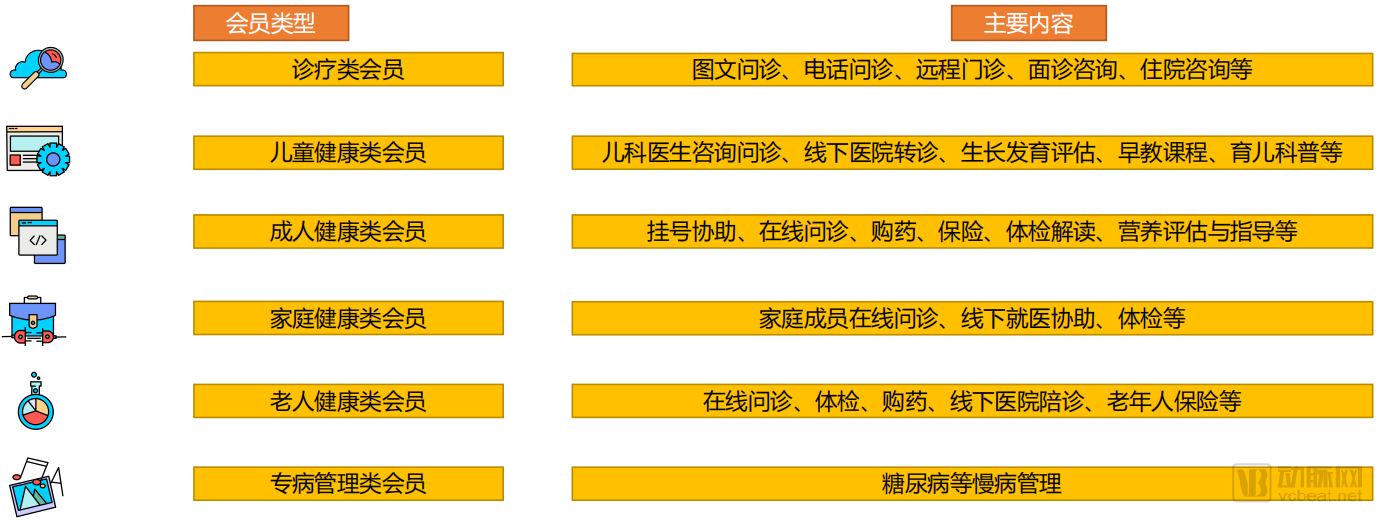

Integrated Resource-Based Membership Services Become a Common Profit Model

After building an industrial ecosystem, internet hospitals can significantly expand the range of integrable resources. By consolidating these resources, they can offer bundled services tailored to user needs. Consequently, membership-based services have become a common revenue model.

We have categorized the primary membership product types offered by major internet hospitals. These products integrate core clinical services with extended health management offerings, aligning the needs of specific patient populations across varying frequencies to add value to medical care and enhance the matching of resources with demand. Upon purchasing a membership, users are entitled to certain discounts and even complimentary services for select items.

In summary, once the industrial ecosystem of internet hospitals is established, it will further integrate connected resources, thereby enabling more precise positioning for itself.We anticipate these trends may emerge in the future.

Specialized Internet Hospitals Cover a Broader Range of Categories

In accordance with policy regulations, internet hospitals are permitted to diagnose and treat common and chronic diseases and issue prescriptions; however, there is no strict definition for what constitutes “common” or “chronic” diseases. Currently, many internet hospitals have begun by focusing on specialized fields. This year, JD Health also announced that it would launch disease-specific management programs for conditions such as cardiovascular and cerebrovascular diseases, diabetes, and mental disorders. From the perspectives of both policy guidance and market demand, specialization and chronic disease management represent favorable strategic choices for internet hospitals, facilitating better resource integration and intensive utilization.

Internet Hospitals Have Become a Key Channel for Pharmaceutical Distribution

Patients require more effective and affordable medications, particularly high-quality new drugs; meanwhile, pharmaceutical companies need more precise and efficient distribution channels. By effectively integrating disease screening, pharmaceutical retail and delivery, and insurance payment services, internet hospitals can serve as a robust bridge between pharmaceutical companies and patients.

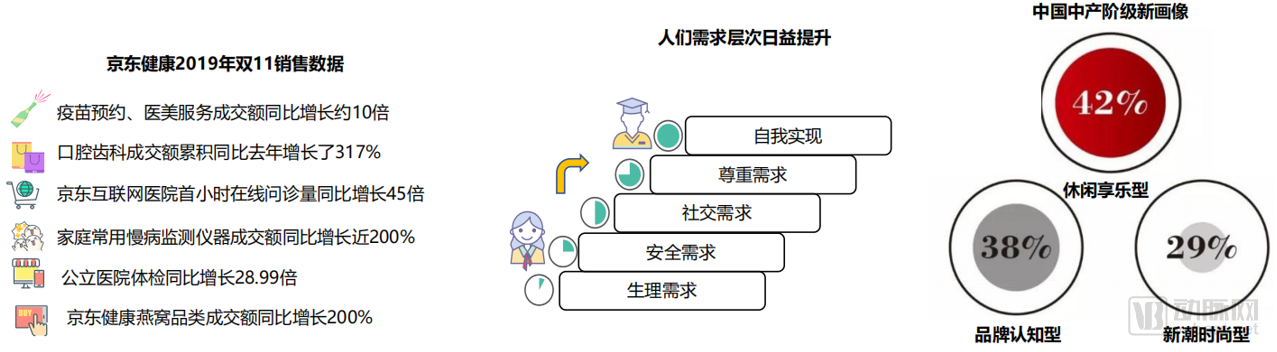

Consumer healthcare broadly refers to market-driven medical services that are not covered by public funding and are voluntarily chosen by consumers. It encompasses fields such as plastic surgery, minimally invasive cosmetic procedures, anti-aging treatments, dentistry, ophthalmology, obstetrics and gynecology, dermatology, weight management, nutrition, mental health, and pet care. Characterized by high per-transaction costs and high repurchase frequency, consumer healthcare targets consumers rather than patients.

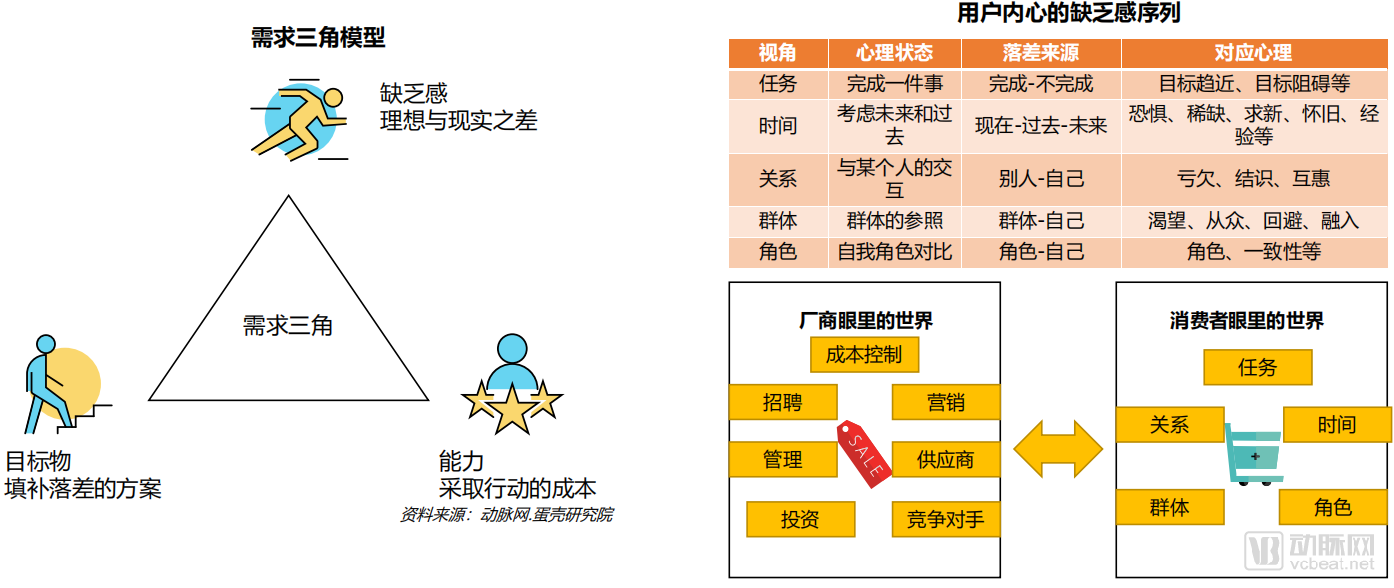

Consumer demand is an internal state in which individuals, driven by a perceived physiological or psychological deficiency, strive to achieve satisfaction; it serves as the fundamental motivation for various human activities. Innovation in consumer healthcare lies in grounding strategies in user needs, constructing user models, and developing innovative products. Demand originates from the sense of lack at the apex of the triangular model, requiring manufacturers to explore what specific deficiencies exist within users’ inner psyche.

These consumer demands are primarily reflected in patient-centered care and patient experience. A survey conducted by Johns Hopkins Hospital in the United States revealed that 70% of patients desire communication in a manner they can understand, while also expecting to be treated with respect during their care.

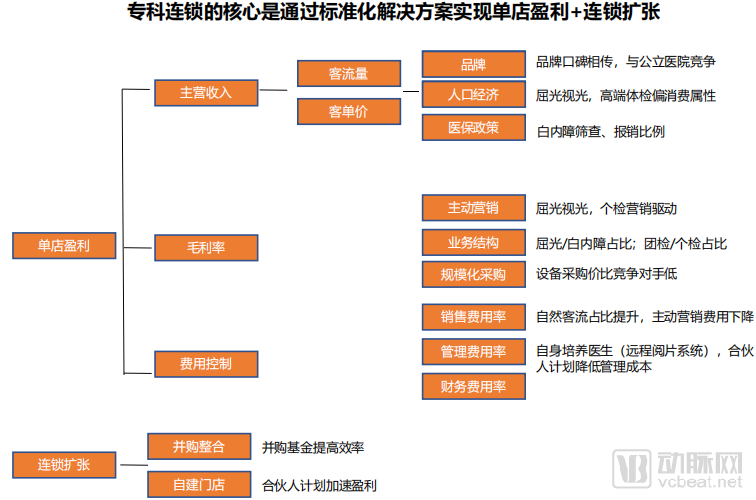

Specialty chain providers built on standardized solutions are on the rise. Particularly in ophthalmology, dentistry, and health check-up sectors, representative industry leaders have emerged, leveraging standardized solutions to scale from single-store profitability to chain expansion.

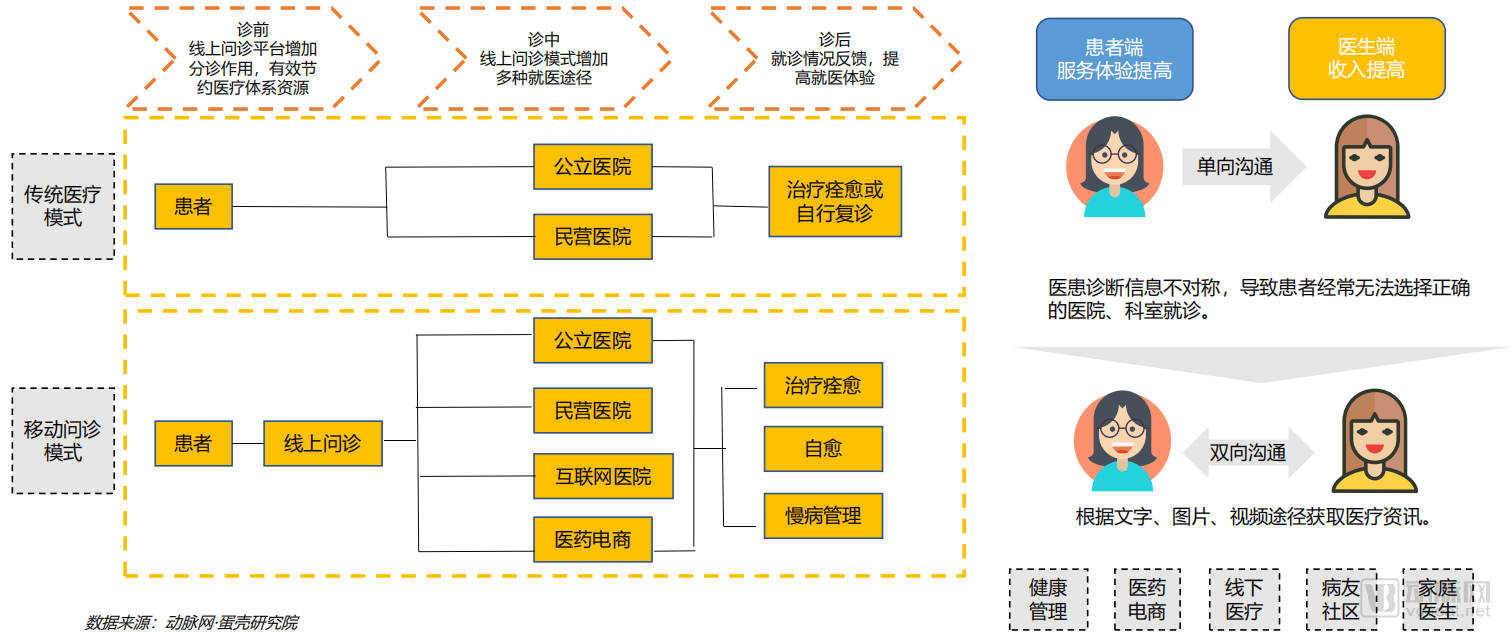

Search behavior refers to the process by which patients search for information related to medical services and products, make selections based on the acquired information, and thereby obtain their ideal medical services and products with minimal input. The purpose of patients’ information search is to reduce information asymmetry in the healthcare service market, identify and evaluate the value and quality of medical services, mitigate uncertainty risks, facilitate informed decision-making, lower healthcare costs, and ultimately maximize patient benefits.

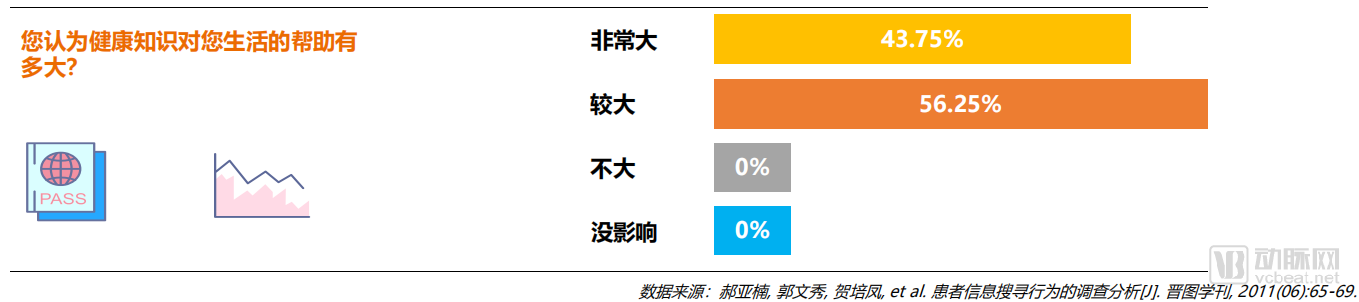

The data indicate that the vast majority of individuals perceive health knowledge as having a significant impact on daily life, and they devote considerable time to gathering available information prior to medical consultations to reduce uncertainty. This underscores patients’ insatiable demand for information.

Healthcare delivery is a vast system. Although medical information constitutes only a part of healthcare services, it directly impacts the effectiveness of communication between physicians and patients. Understanding the hierarchical nature of patients’ information needs enables hospital administrators and service designers to pinpoint key patient requirements, thereby addressing medical information needs in an organized and targeted manner. On one hand, satisfying patients’ information needs enhances their healthcare experience; on the other hand, it highlights the added value inherent in healthcare services.

Patients typically begin their searches on Baidu but spend considerable time sifting through the results to identify reliable sources. Given the specialized nature of medical information, an increasing number of patients are turning to professional physicians’ websites, as they place greater trust in expert opinions. According to data from Kantar’s “2018 China Doctor/Patient Digital Life Survey Report,” Chinese patients spend at least 26 hours online per week, with 29% of that time devoted to seeking healthcare-related information. The topics of greatest interest to Chinese patients include medical and disease education, medication guidance and references, and online consultations. However, patient satisfaction remains low, primarily due to skepticism about the quality of the information they find.

Patients are most interested in basic disease knowledge/health education, wellness and healthcare information, as well as drug information and usage instructions.

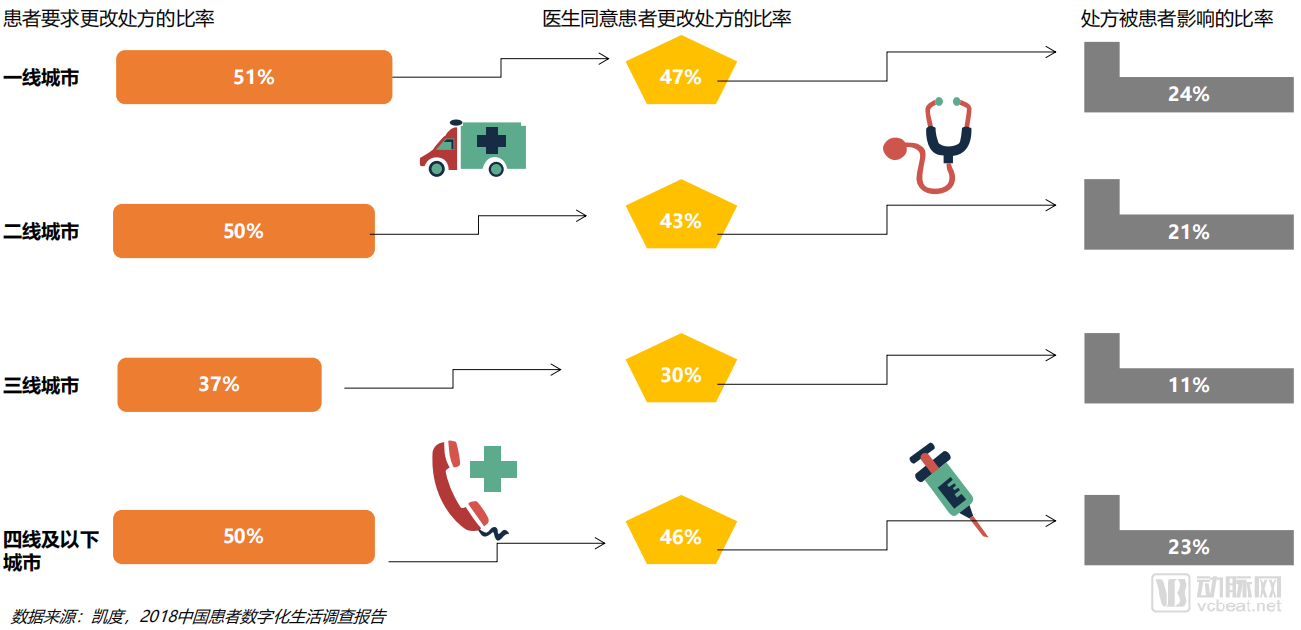

As patients gain increasing access to information through digital platforms, they have become more proactive in expressing their healthcare preferences. The model of shared decision-making between physicians and patients is gradually emerging, with China being the country where this approach is most prevalent. In the treatment of low-risk conditions such as fever and the common cold, physicians may even fully defer to patients’ preferences.

Even so, the information gap between patients and physicians remains unbridgeable. Patients’ extreme lack of information during medical care increases the risks and uncertainties they face when accessing healthcare services. The pronounced information asymmetry between doctors and patients is a key feature that distinguishes the healthcare market from other markets. Due to the highly specialized nature of medical services, most patients lack adequate knowledge about healthcare delivery, and they also have limited access to hospital management information throughout the treatment process.

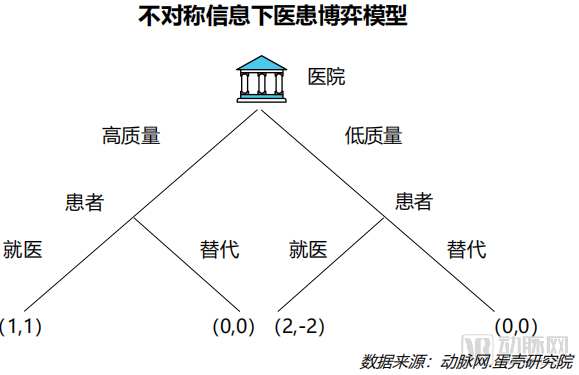

According to the doctor-patient game theory model under asymmetric information, if patients believe that hospitals will provide high-quality medical services, they will choose to seek medical care. Knowing this, hospitals will opt to provide low-quality medical services. In this scenario, the hospital’s profit reaches 2, significantly higher than the normal profit level, indicating that the hospital has gained excess profits. Meanwhile, the patient’s utility is -2, meaning their interests are harmed, although the patient is unaware of this beforehand.

Information asymmetry renders patients passive in the consumption of medical services; while patients typically take the initiative to seek out hospitals, they passively receive care, lacking the ability to choose the type or content of medical services and must comply with all arrangements made by the hospital.

It is precisely because information asymmetry is inherently insurmountable that a series of products and services aimed at reducing the information gap between doctors and patients have emerged in the market, seeking to capture the demand opportunities within this niche.

In the future, internet-based healthcare will, to some extent, reduce the information asymmetry between patients and physicians. However, as most online consultations remain limited to minor ailments, online reviews are unlikely to encompass the full spectrum of medical treatments.

In summary, information asymmetry between doctors and patients leads to adverse selection and moral hazard in the healthcare market, reduces market efficiency, and harms patients’ interests. Therefore, appropriate measures should be taken to alleviate this information asymmetry. Nevertheless, an information vacuum between patients and physicians persists across all practicing doctors. To address this, we propose the following three perspectives:

Establish a Medical Information Disclosure System

Medical information of concern to hospital patients is disclosed through appropriate channels to facilitate patient access.

The medical information disclosure system, on the one hand, can increase the volume of information available to patients and reduce their information search costs; on the other hand, the system itself serves a signaling function, whereby high-quality hospitals are more willing to disclose their information to the public to differentiate themselves from other hospitals.

Strengthen Doctor-Patient Communication and Establish an Interactive Doctor-Patient Relationship

In the traditional active-passive doctor-patient relationship, there is a lack of communication; hospitals assume an active role while patients passively receive treatment. Establishing an interactive doctor-patient relationship enables patients to actively participate in their care, with both parties engaging in collaborative negotiation and joint decision-making regarding the formulation and implementation of medical plans, thereby minimizing information asymmetry.

Hospitals Enhance Medical Service Quality and Build Brand Reputation

A strong brand serves as a signal in itself; hospitals convey this signal to patients by building their brand, thereby differentiating themselves from competitors.

Online consultation platforms are becoming a major medium for physicians’ brand building. Physicians enhance their influence through personal branding, and patients’ preference for doctors with strong brand equity is emerging as an industry trend.

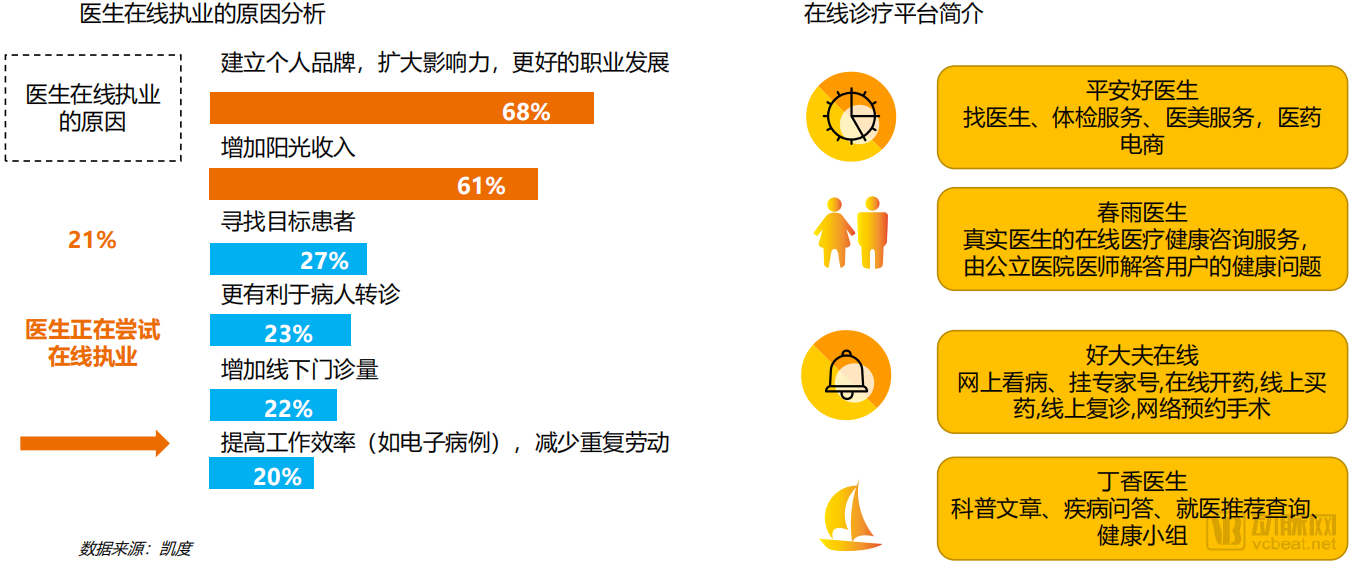

Overall, it is evident and irreversible that physicians are increasingly relying on digital technologies to support their medical practice. Physicians are becoming more conscious of building their personal brands and are eager to increase their transparent, legitimate income, for which digital technologies offer effective avenues. Under the influence of healthcare reform policies such as multi-site practice and tiered diagnosis and treatment, more physicians are likely to embrace and attempt to conduct medical interactions and services via the internet in the future.

It has become an inevitable trend for physicians to build independent personal brand IPs, particularly for senior attending and associate chief physicians. These professionals possess strong medical service awareness and capabilities, are willing to explore diverse forms of interaction, and are eager to establish their own brands. As healthcare reform enters its “deep-water zone,” physicians will increasingly move toward multi-site or even free practice, making brand building essential.

A collective shift in mindset among physicians has led to increasingly stronger doctor-patient interactions, which serve as one of the key pathways to further increasing compliant income. Survey data indicates that seven major activities—medical knowledge and information access, medical literature/data searches, use of professional medical tools, continuing medical education (CME), industry communication and networking, doctor-patient interactions, and compliant income-related activities—account for the majority of physicians’ online time spent on medical matters. Notably, “compliant income” emerged for the first time in the 2017 survey as one of the primary online activities for physicians.

In the future of physician brand building, we believe the following key points are essential:

Mass media campaigns can reach a vast audience, but the resulting patient base tends to be highly dispersed, with relatively few high-value cases. In contrast, cultivating one’s own professional platform may require gradual effort, yet it is more likely to attract well-targeted patients. Therefore, it is not necessary to limit oneself to any single approach.

In the past, brands were built through traditional media. In the era of "Internet Plus," there is a greater need for precise brand building with an emphasis on speed. This precision is primarily reflected in two aspects: precision in medical specialties and precision in targeting patients.

1.Precision in Expertise; Physicians must focus before broadening their scope in academic and clinical pursuits, learn to make trade-offs, and maintain a clearly defined professional identity with distinct characteristics.

2.Precision in Patient CareHospital publicity targets the general public on a broad scale, whereas individual physician studios cater to niche audiences. Large hospitals prioritize marketing and communication strategies aimed at acquiring new patients, employing a many-to-many model with nearly unlimited patient acquisition potential. In contrast, an individual physician’s brand operates on a one-to-many model with inherent capacity limits; once clinical throughput reaches its ceiling, the focus shifts to maintaining patient relationships and maximizing share of wallet from existing patients. The expansion of influence relies heavily on word-of-mouth referrals from satisfied patients.