Global Digital Health Funding Sees Slight Decline in 2019 Despite Six IPOs, Reports Rock Health and StartUp Health

Recently, Rock Health and StartUp have successively released their investment and financing reports on the digital health sector in 2019. Similar to the statistical data from VCBeat (WeChat ID: vcbeat), both organizations observed a slight downturn in the total global healthcare financing in 2019. VCBeat has compiled these two reports, and we will first look at the summary from Rock Health.

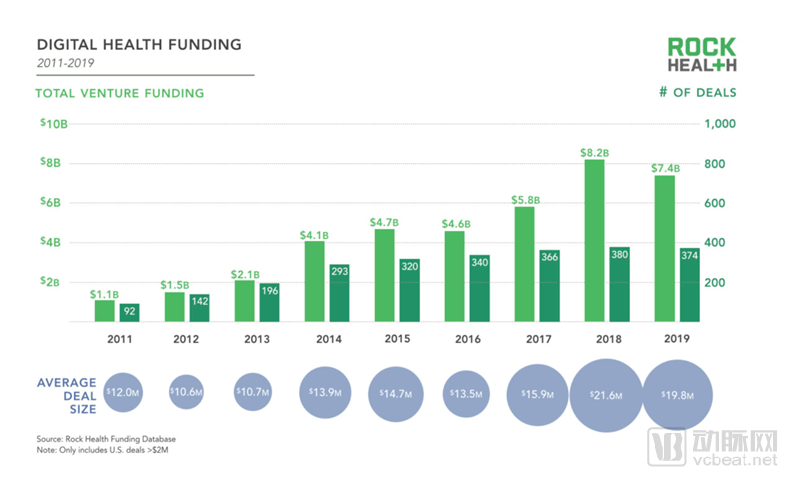

Over the past decade, digital health has evolved from a peripheral interest for investors to a major sector, now accounting for nearly one-tenth of all venture capital funding in the United States. In 2019, 359 U.S. digital health startups raised a total of $7.4 billion from 627 investors. There were 112 deals throughout 2019, and six digital health companies went public for the first time; however, merger and acquisition activity in the industry has gradually declined.

Digital Health Investment Declines

In 2019, U.S. digital health startups raised a total of $7.4 billion, marking the second-largest funding year on record. Since Rock Health began tracking this sector in 2011, the number of deals declined slightly for the first time. After surging by 32% between 2017 and 2018, the average deal size in the industry fell to $19.8 million in 2019. Overall, entrepreneurs in digital health and healthcare still secured numerous record-breaking investments.

As anticipated at the end of 2018 (also a record-breaking year), the growth trajectory of venture capital investment in digital health was expected to slow down in 2019. The total investment amount was 10% lower than the record $8.2 billion set in 2018. This decline can be attributed to a slight decrease in the number of late-stage deals in 2019. At the end of 2018, two late-stage deals accounted for $800 million of the total funding. However, the two companies that successfully went public in 2019 (Peloton and Livongo) collectively raised $655 million in 2018, which accounted for 80% of the funding difference between 2018 and 2019. Therefore, it is more likely that 2020 will see a trend toward slowing growth rather than a reduction in overall investment.

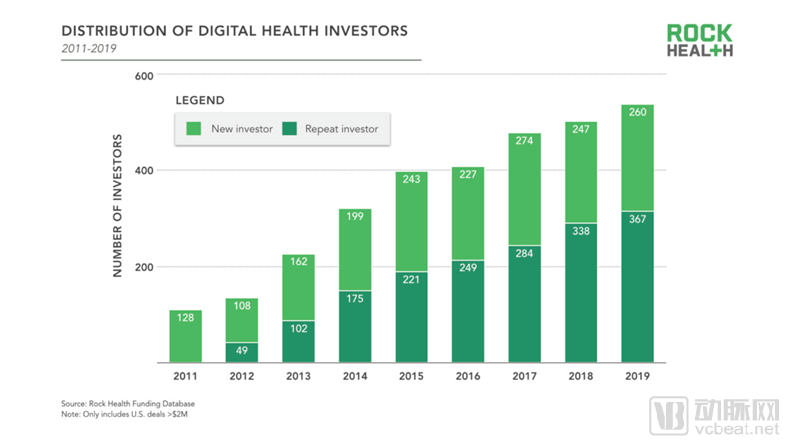

In 2019, nearly 60% of active investors had previously invested in the digital health industry. Compared with first-time investors, many investors have made multiple repeat investments in the digital health sector over the past four years. Moreover, the proportion of repeat investors has reached a new high, including independent non-corporate venture capital funds and private equity (PE) firms.

1. Venture capital (VC) firms generally invest in companies at various stages, from the seed round to Series D and beyond.

- In 2019, 62% of venture capital investors were repeat investors.

- Meanwhile, since 2014, more than 50% of venture capital investors have been repeat investors.

2. Corporate Venture Capital (CVC), primarily investing in mid-stage (Series B+) and later stages

- In 2019, 64% of CVCs were repeat investors.

- Since 2018, over 50% of CVCs have been repeat investors.

3. Private equity (PE), growth, hedge funds, and asset management firms primarily invest in late-stage rounds (Series D and beyond).

- In 2019, 56% of late-stage investors were repeat investors,

- Since 2015, approximately 50% of investors have been repeat investors.

“I have been actively investing for many years. Numerous innovations are rapidly evolving, and a significant influx of talent is entering the digital health sector. Now, an increasing number of companies are finally validating my investment thesis and demonstrating cost-effectiveness, while creating genuine value. Entrepreneurship is no longer just a dream.”

——Alyssa Jaffee, Vice President of 7wire Ventures

Six Digital Health Companies Successfully Went Public in 2019

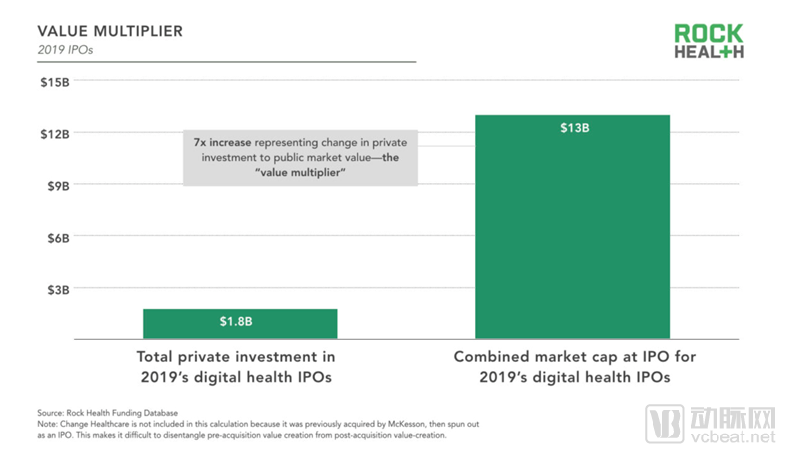

After a three-year IPO drought, six digital health companies went public in 2019: Livongo, Health Catalyst, Phreesia, Change Healthcare, Peloton, and Progyny. As of January 1, 2020, the combined market capitalization of these six IPOs totaled $17 billion. The 2019 wave of initial public offerings is validating the risk model for long-tail investments in the digital health sector (companies that require relatively few investments to generate substantial returns).

Temporarily excluding Change Healthcare (as it was previously acquired by McKesson), the founders and employees of the other five companies collectively secured $1.4 billion in investment, transforming five “startup concepts” into companies valued at $13 billion and achieving successful initial public offerings (IPOs). “Whether a 7x growth multiple can be achieved” serves as an effective metric for assessing whether these startups have truly realized the “total value multiplier” made possible by the capital provided by their investors.

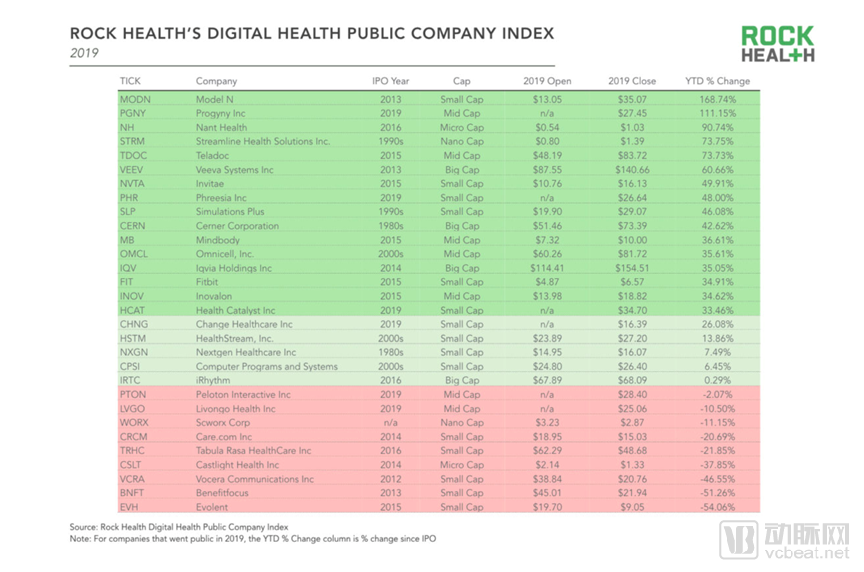

The Digital Health Company Index rose by 31% in 2019, in line with the performance of the S&P 500. Athenahealth was taken private by the private equity firm Veritas Capital, and Medidata Solutions was acquired by the European software company Dassault Systèmes. If Google’s acquisition proceeds as scheduled, Fitbit will also be excluded from the list this year.

Investment in the Digital Health Market Will Be More Cautious

In the final months of 2019, more than a dozen conversations between Rock Health and other investors indicated that the peak of the current investment cycle was drawing to a close. Although market volatility was expected to increase and IPO windows were anticipated to narrow, investors remained committed to deploying capital into technology companies—albeit at a potentially slower pace than in recent years—to address the significant challenges and opportunities within the U.S. healthcare industry.

“I am concerned that investor sentiment may have shifted significantly over the past month or two, but I believe this has not been widely reported. Moreover, entrepreneurs have made no plans or preparations for the real risks posed by an imminent recalibration of the capital markets. Amidst ongoing turbulence, Sino-U.S. frictions, and a myriad of other factors, with the U.S. presidential election approaching and the smoke from the trade war yet to fully clear, the stalemate between the two sides could persist for another year or two. Consequently, if startups remain stagnant and fail to achieve their key milestones, they will face an exceptionally harsh funding winter.”

——Michael Greeley, General Partner at Flare Capital Partners

IPOs May Slow Down in 2020

In the first half of 2019, the healthcare sector remained a hotbed for initial public offerings (IPOs). However, broadly speaking, 2019 saw a surge in startups going public collectively. In the second quarter alone, 62 companies from various industries listed on different markets, raising a total of $25 billion, marking the highest trading volume in nearly four years.

However, the lackluster performance of several high-profile star companies, including Uber, Lyft, and Slack, in the months following their IPOs, coupled with the dramatic saga of WeWork’s attempted public listing, may erode public investors’ confidence in these startups. Investors are concerned that the valuations of some large startups, such as unicorns, have been inflated in private markets, leaving little room for growth once they enter the public market. Furthermore, the cohort of companies that went public in 2019 was among the least profitable since the dot-com bubble. These trends and potential risks associated with startups will also pose headwinds for digital health companies aiming to launch IPOs in 2020.

Despite the Risks, the Ten-Year “Bull Market” Continues

As the decade-long bull market may be nearing its peak, some venture capitalists interviewed by Rock Health have stated that they are preparing for an economic and stock market downturn. Although we will not attempt to make economic forecasts, uncertainties—including escalating foreign policy tensions, trade wars, a global economic slowdown, and elections—are exerting external pressure on venture capitalists.

Over the past decade, a robust economy and low interest rates have been a boon for venture capital firms raising new funds, driving cash reserves at venture capital and private equity firms to record levels. Although these war chests can provide a buffer against future market contractions—ensuring that investors will still have capital to deploy into startups even if the macroeconomic environment deteriorates suddenly—entrepreneurs should prepare for a tighter venture capital market in the coming year.

“The funding environment inevitably undergoes continuous changes throughout the year. At the beginning of the year, we only saw early signs, and risk aversion among venture capital investors had not yet fully taken hold. By mid-year, the market began to rationalize somewhat, partly because tech unicorns went public and encountered difficulties. Currently, market sentiment has cooled, but I don’t believe this represents an overcorrection. It simply means that the upward momentum has not been sustained.”

—Amy Belt Raimundo, Managing Director of Kaiser Permanente Ventures

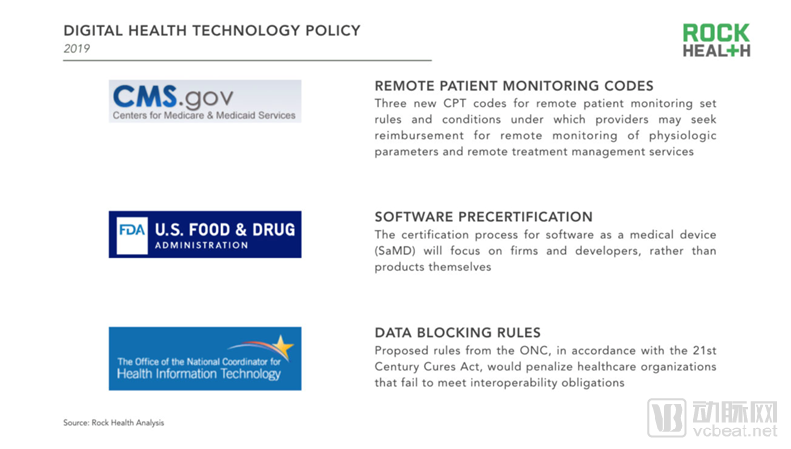

Policies Will Continue to Drive the Development of Digital Health

U.S. federal policy can sustain the direction of innovation by establishing rules and standards and reducing regulatory uncertainty. In 2019, the CMS, ONC, and FDA continued to establish new ground rules for the healthcare system:

- CMS has established reimbursement codes for Remote Patient Monitoring (RPM)

- FDA completed retrospective testing of the pre-certification program

-ONC has completed the collection of public comments on its proposed data rules

These policies collectively form the foundation of the U.S. federal government’s digital health technology policy, building upon the HITECH Act enacted a decade ago. This long-term commitment to healthcare digitization has afforded the industry a certain degree of resilience against short-term market fluctuations.

StartUp Health also released its 2019 Annual Investment and Financing Report in January. The data showed that 2019 continued the strong upward trend in funding for health innovation seen over the past decade. With 727 deals totaling more than $13.7 billion, 2019 was the second-highest year on record for healthcare investment, and this trend continues. That said, both Rock Health and StartUp Health observed a decline in investment and financing figures in 2019 compared to 2018.

StartUp Health dubbed 2019 the “Year of the Patient,” driven by substantial institutional investments in patient-centric tools such as Bright Health and Capsule. However, these developments did not emerge solely in 2019. For instance, funding within initiatives like the “Moonshot” has generally been dominated by care delivery services, particularly outside the United States. Notable examples include major deals involving consumer-focused healthcare provider Babylon Health and China’s Penguin Almond. The combined value of just these two transactions reached $800 million (excluding JD Health’s $1 billion Series A financing, which was not included in StartUp Health’s statistics).

Significant Progress Has Been Made in the Field of Women's Health This Year. In the Fourth Quarter of 2019, the Program Secured Over $85 Million in Funding, Bringing the Total for the Year to $425 Million.

This includes the financing of The Pill Club ($51 million), which enables women to order contraceptives online and have them delivered to their doorsteps; Elvie ($42 million), a femtech hardware company; and Gennev ($40 million). StartUp Health has been committed to helping women manage their menstrual cycles and address menopause-related issues.

On the other hand, capital deployed this year has also highlighted other areas worthy of investment and innovation that merit attention. Sectors related to drug addiction and pediatrics underperformed, securing only $96 million and $118 million in funding, respectively. In fact, none of the top investors this year invested in innovative enterprises focused on drug addiction. Additionally, education and content-related investments received the least funding, totaling just $120 million.

Nevertheless, gaps exist in every market, and we see opportunities in these areas. We are committed to continuously focusing on these sectors through new approaches, thereby ushering in a new era of global innovation hubs and bold investors.

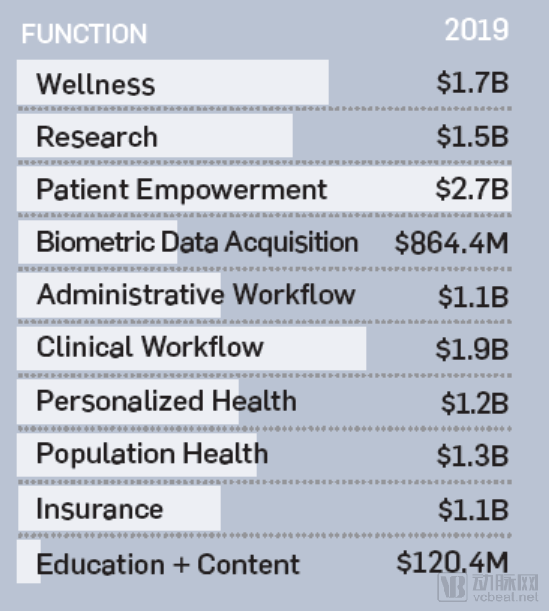

Each company in the StartUp Health Insights database is categorized into one of the following 10 segments, representing its primary value driver. Data by segment provides deep insights into investment trends across each area, enabling a clearer understanding of the market landscape and the proportion of investment allocated to each segment.

Investment Spectrum Chart

As mentioned above, we dubbed 2019 the “Year of the Patient” due to the significant funding provided by numerous investment institutions for “patient empowerment” tools. However, other noteworthy trends also emerged. For instance, substantial capital inflows (totaling $3 billion) into areas supporting clinical and administrative workflows will translate into significant investments in healthcare infrastructure. Institutional investments in insurance companies will continue to expand universal health coverage, whereas the education sector received the least investment and warrants continued attention.

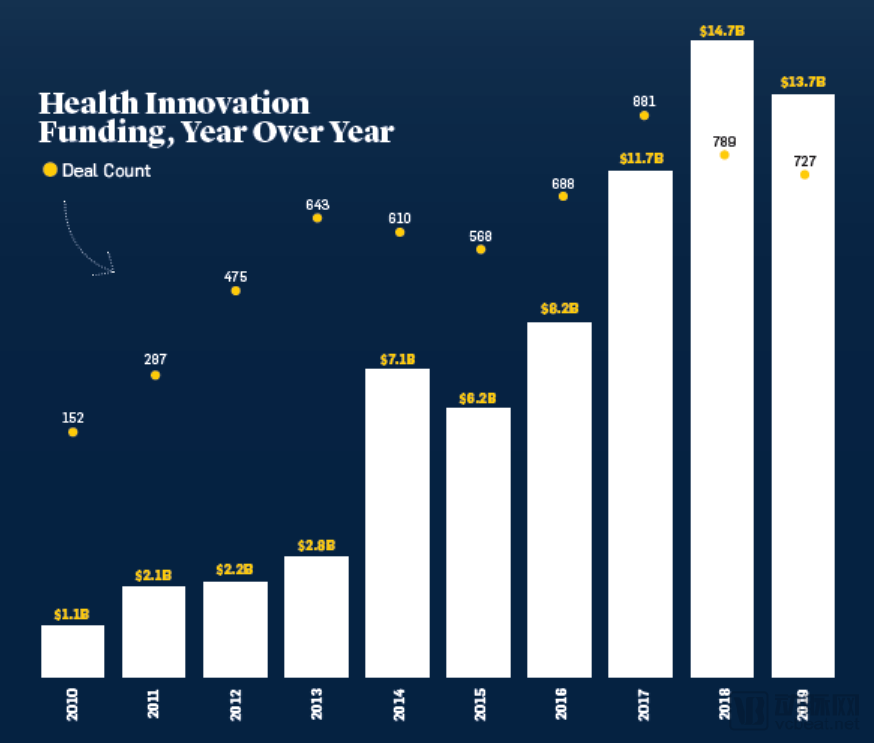

Since 2010, the health sector has raised $7 billion.

The health innovation sector continues to maintain a strong upward trajectory, a trend we have been tracking for nearly a decade. Although each fluctuation in this curve can be analyzed through past quarterly reports, these figures tell a simple yet compelling story: the development of health innovation is now both sustained and rapid. In just ten years, 4,300 startups have secured funding, with financing levels increasing tenfold and the number of investors seeing similar growth.

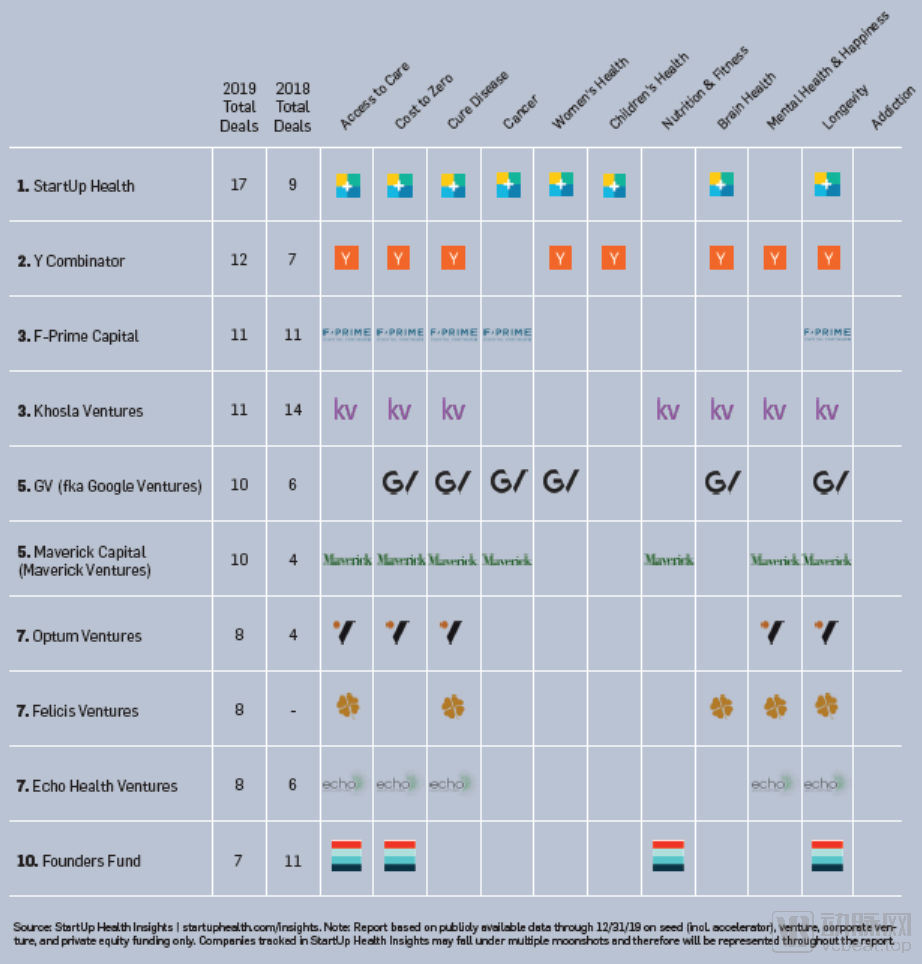

Most Active Investors

Over the past decade, we have made significant strides in both the depth and breadth of health innovation investment. In 2010, a total of 168 investment firms were recorded. By 2019, this number had reached 1,344. Investors such as F-Prime, Khosla Ventures, Y Combinator, and GV have diversified their capital across five or more subsectors. The data also reveals disparities among different investment firms, clearly indicating that substantial capital has shifted away from the field of opioid addiction.

Global Investment Surges in the East

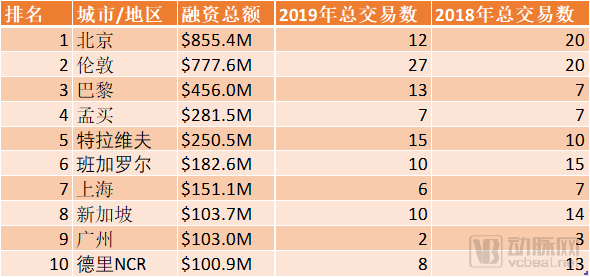

As a leader in health innovation, China accounts for three of the top ten most investment-worthy cities in 2019. In terms of total transaction volume, London ranks first, while Paris and Tel Aviv achieved significant growth in 2018. Notably, despite the prevalence of innovation in the Global South, no cities from South America or Africa have made it onto the list. It is time for investors to broaden their horizons and look globally.

Top 10 Cities for Financing Outside the United States

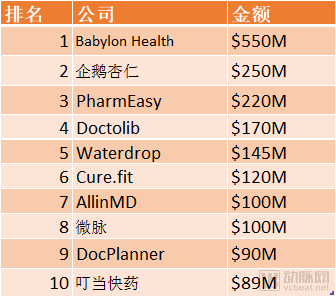

Top 10 Largest Funding Rounds Outside the United States

Source: StartUp Health Insights | startuphealth.com/insights.

U.S. Coastal Cities Remain at the Forefront of Investment

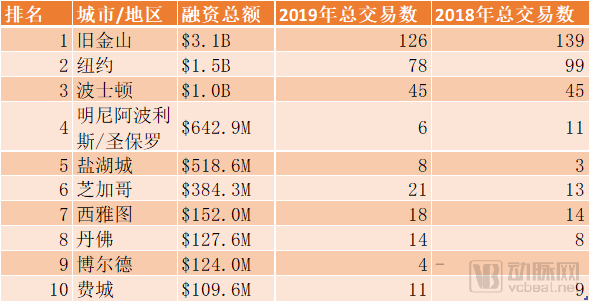

San Francisco, New York, and Boston, as pioneers in health innovation, show no signs of slowing their investment trends. A review of major deals in 2019 reveals that these regions accounted for ten investments exceeding $100 million each. Clearly, large-scale transactions are becoming the new normal. Multiple cities are showing signs of significantly increased investment activity. Compared with 2018, Chicago, Salt Lake City, Seattle, and Denver all saw substantial increases in the number of deals. Only five non-coastal cities appeared on the list, and none were located south of the Mason-Dixon Line, indicating that numerous opportunities for innovation still exist in untapped markets.

Top 10 U.S. Cities for Financing

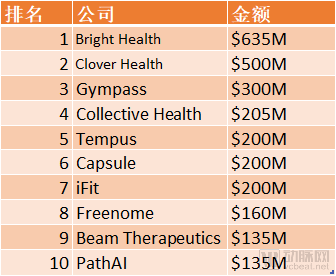

Top 10 Financing Deals in the United States

Source: StartUp Health Insights | startuphealth.com/insights.

Translation: Zhou Qianyun

Source:

https://rockhealth.com/reports/in-2019-digital-health-celebrated-six-ipos-as-venture-investment-edged-off-record-highs/

https://www.startuphealth.com/2019-q4-insights-report