Analysis of China's Medical Device Market Access Amid Significant Policy Shifts in 2019

I. Overview of the Policy Environment

Following the launch of the new healthcare reform, China’s medical device industry has entered a new phase of development. It has now become a sunrise industry with a relatively comprehensive product portfolio, continuously strengthening innovation capabilities, and robust market demand. After the state implemented sweeping reforms in the pharmaceutical sector, the Chinese government has successively introduced policy measures to transform and regulate the domestic medical device market, aiming to further deepen and broaden the scope of healthcare reform.

Sources: China Drug Procurement Alliance Data, Ryan Partners Interview & Analysis

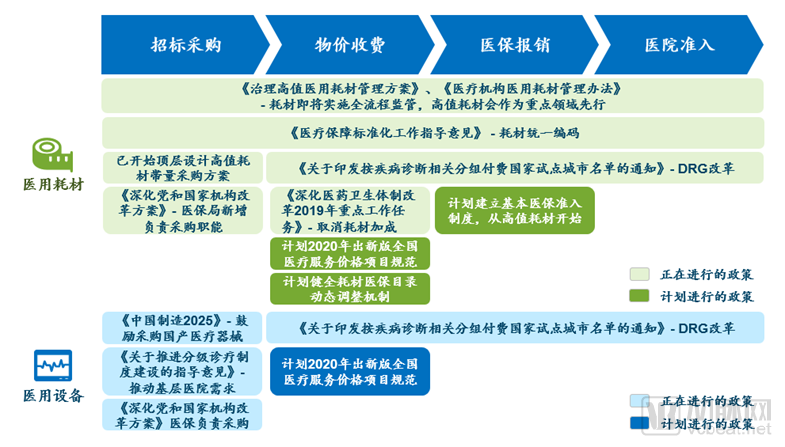

Given the characteristics of the current policy environment, the state has been continuously issuing policies to regulate key areas of management. Regulatory measures span all segments of the healthcare market access value chain:

Tendering and Procurement

A mix of procurement models coexists, primarily featuring online sunshine procurement (24 provinces), centralized bidding (2 provinces), provincial-municipal joint procurement (2 provinces), and exchange-based trading, with the primary aim of achieving “price reductions” for medical devices.

Pricing and Charges

Optimize the pricing of medical service items by adding or revising such items, excluding consumables.

Medical Insurance Reimbursement

Primarily based on fee-for-service reimbursement, with a small portion using single-disease payment, mainly applying the "exclusion method" principle.

Hospital Access

Assist in addressing cost control at hospitals, the pilot implementation of the "two-invoice system" for medical consumables, and administrative monopolies targeting imported products.

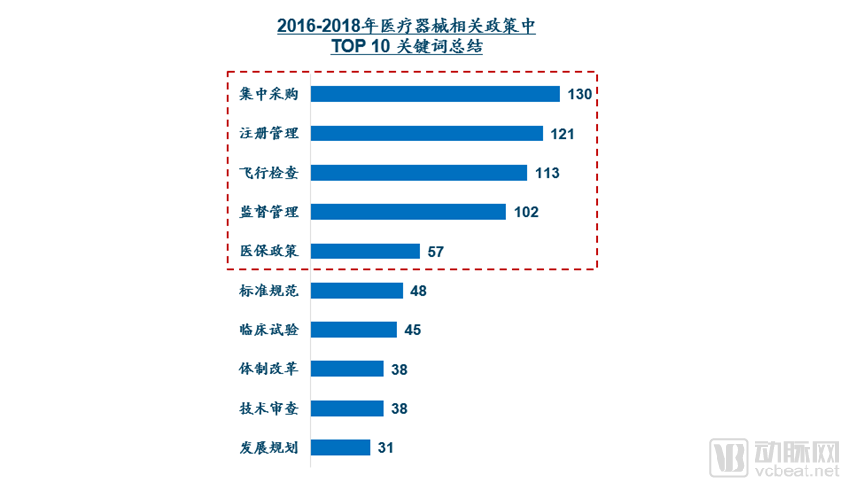

An analysis of the keywords in relevant policies reveals that terms such as centralized procurement, registration management, unannounced inspections, regulatory oversight, and medical insurance policies appear frequently, underscoring the state’s significant attention to these areas within the medical device sector.

Sources: China Drug Procurement Alliance data, Ryan Partners interview & analysis

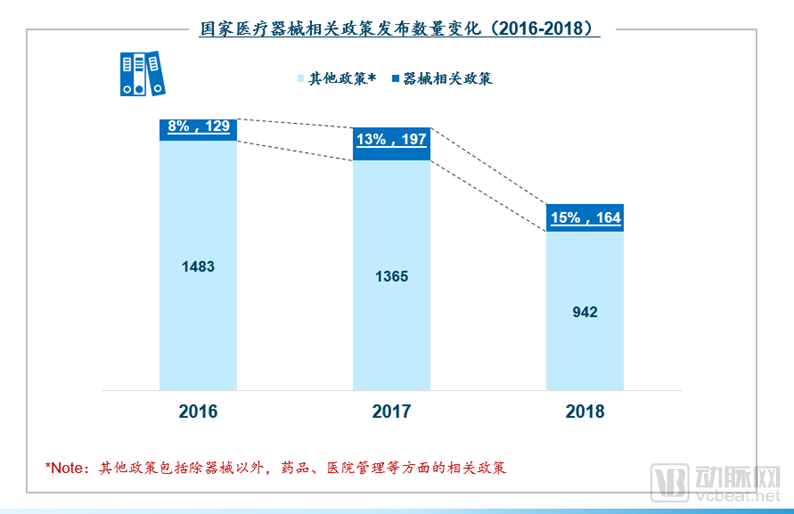

Overall, the policy environment for medical devices underwent dramatic changes in 2019, covering all segments of the market access value chain for consumables and equipment.

Sources: Ryan Partners interview & analysis

II. Analysis of Key Policies

1. Reform Plan for Medical Consumables and High-Value Consumables

As one of the key areas in the central government’s efforts to deepen healthcare reform, high-value medical consumables are undergoing prioritized, comprehensive, and end-to-end supply chain reforms.

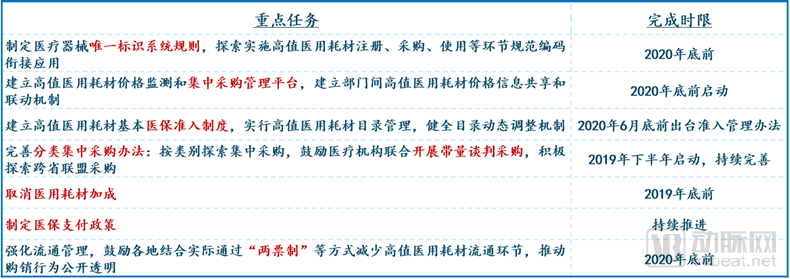

The Measures for the Administration of Medical Consumables in Medical Institutions were officially implemented on September 1, 2019, covering the following aspects:

Strict Definition of Medical Consumables

Established a supply catalog of medical consumables for healthcare institutions

It is mandatory that the procurement of medical consumables be selected from the centralized procurement catalog.

Establish a Tiered Management System for the Clinical Use of Medical Consumables

On July 31, the State Council issued the “Reform Plan for the Governance of High-Value Medical Consumables,” officially ushering in an era of comprehensive management and cost control for high-value medical consumables. Its key tasks include:

Sources: “Administrative Measures for Medical Consumables in Medical Institutions,” “Reform Plan for the Governance of High-Value Medical Consumables,” Ryan Partners interview & analysis

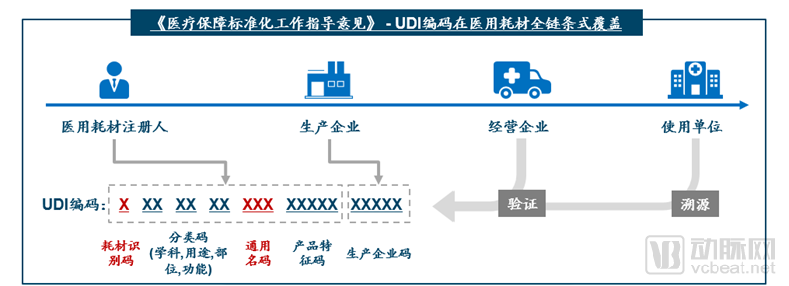

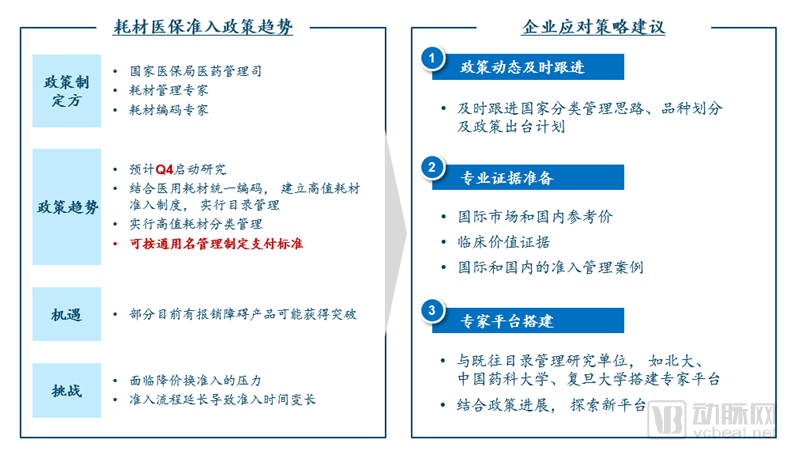

2. Unified Coding System for Medical Consumables (UDI)

The significance of the Unique Device Identification (UDI) system for medical consumables lies in its role as the foundation and cornerstone for future pricing, health insurance reimbursement, and tendering and procurement processes.

In the future, the Unique Device Identification (UDI) system will be applied in areas such as medical device adverse event reporting, product recalls, and traceability. It will also facilitate integration across healthcare and health insurance sectors, enabling data sharing among platforms for registration and approval, clinical application, and insurance reimbursement. This will significantly support the implementation of policies related to health insurance reform and centralized procurement.

Sources: “Guiding Opinions on Standardization Work in Medical Security,” Ryan Partners interview & analysis

Therefore, medical device manufacturers should take proactive measures and make adequate preparations in advance to address the market access risks and impacts potentially arising from the unified coding of consumables. If a product is not covered by the coding system, it will be excluded from critical market access processes such as fee scheduling, health insurance reimbursement, and centralized tendering and procurement. Consequently, enterprises must ensure that all their products are appropriately listed in the relevant directories.

Unified coding may fail to reflect product-specific features, leading to issues during bid grouping and potentially resulting in a “bad money drives out good” scenario. Therefore, companies must ensure that the key elements of their advantageous products are clearly differentiated within the catalog. Innovative products may face restrictions when entering the market, affecting recognition by regulatory authorities; thus, it is essential to promote the inclusion of innovative products and advanced technologies in the catalog. Unified coding for medical consumables cannot guarantee that competing firms will not influence the rationality and fairness of the catalog. Consequently, it is crucial to engage in policy discussions from the outset to counter unreasonable demands from competitors.

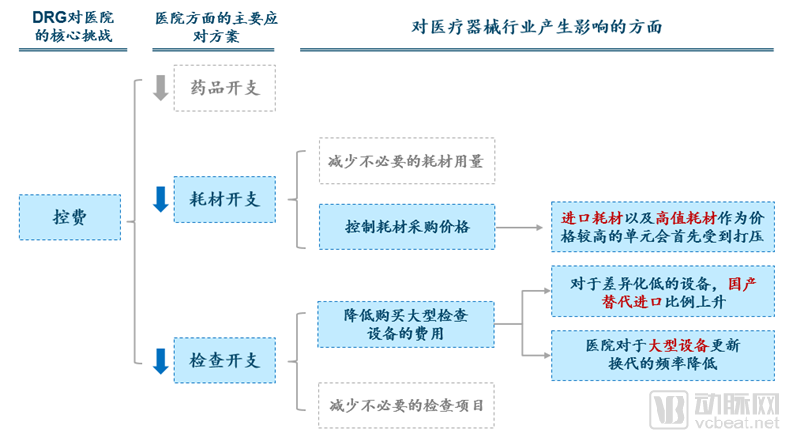

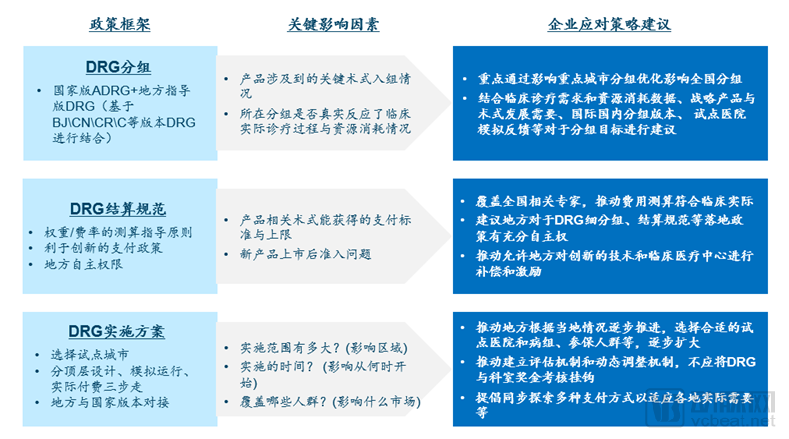

3. Reform of Medical Insurance Payment Methods (DRG)

The government aims to guide hospitals in standardizing medical practices and curbing unreasonable cost growth through reforms in the Diagnosis-Related Group (DRG) payment system. In 2019, four departments, including the National Healthcare Security Administration, issued the "Notice on Printing and Distributing the List of National Pilot Cities for Diagnosis-Related Group (DRG) Payment." The National Working Group on DRG Payment designated 30 cities, including Beijing and Tianjin, as national pilot cities for DRG payment. A simulated operation of this payment model was conducted in 2020, with actual implementation launched in 2021.

From the perspective of response measures and underlying logic adopted by hospitals, high-value consumables and imported medical devices will once again face elevated risks, thereby becoming the primary targets for adjustment.

Sources: Ryan Partners interview & analysis

Therefore, companies should review their core products and make strategic adjustments based on their respective stages in the product life cycle.

Products in the growth stage generally exhibit significant differentiation. As they are in an upward trajectory, high premiums can be sustained for a prolonged period, while the domestic substitution rate remains low. For such products, efforts should focus on enhancing their cost-performance ratio and accelerating market penetration in the early stages.

For differentiated products in the maturity stage, as price premiums become increasingly difficult to sustain and domestic substitution rates are high, companies should proactively strategize, elevate their competitive dimensionality, and explore new points of differentiation. In addition, sales teams need to employ more persuasive selling techniques, and appropriate price reductions should be implemented.

For products with minimal differentiation, which are currently in the late maturity or decline stage, the domestic substitution rate is very high, making it difficult to sustain a price premium. Therefore, companies producing such products should reduce investment, adopt streamlined sales models, and minimize the price gap with domestically produced alternatives.

Nevertheless, on a positive note, there remains some room and flexibility within different parts of the framework during the policy-making process, allowing enterprises to make appropriate adjustments.

The following provides a detailed analysis of how enterprises, as parties highly likely to be affected by the introduction of Diagnosis-Related Groups (DRG), should respond to and mitigate its impact across various stages.

Sources: Ryan Partners interview & analysis

III. Discussion by Market Access Phase

1. Bidding and Procurement Phase

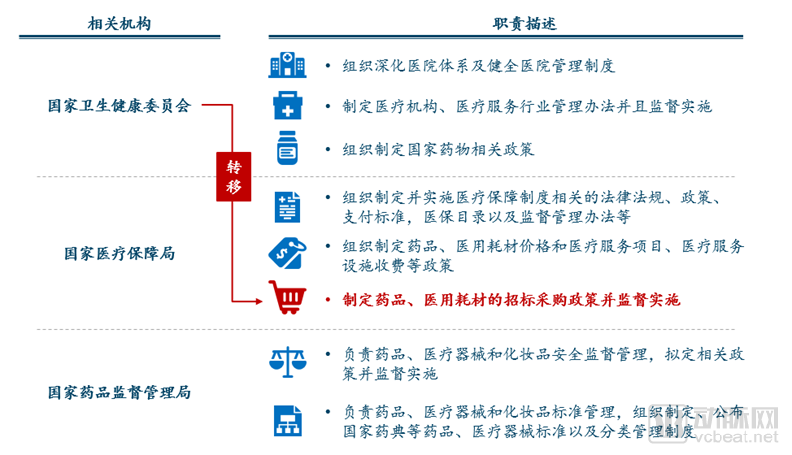

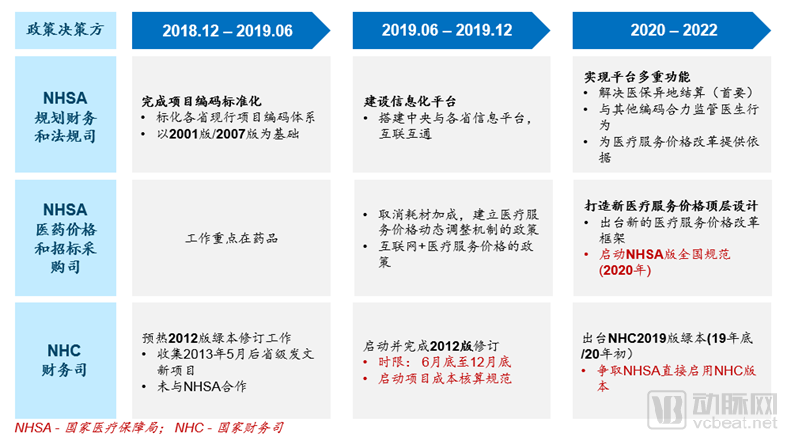

To support healthcare reform, the responsibility for formulating tendering and procurement policies and overseeing their implementation has been transferred to the National Healthcare Security Administration.

The newly established “National Healthcare Security Administration” integrates core functions across the healthcare value chain, including regulation, payment, pricing, and centralized procurement. Its authority directly spans the coordinated reform of the “three medical sectors” (pharmaceuticals, healthcare services, and health insurance). It will play a pivotal role in driving future comprehensive healthcare reforms and exert a decisive influence throughout the entire healthcare value chain.

Sources: “Plan for Deepening the Reform of Party and State Institutions,” Ryan Partners interview & analysis

In terms of consumables, with the success and deepening of volume-based procurement (VBP) for pharmaceuticals, centralized procurement—particularly for high-value medical consumables—has already begun and will inevitably expand gradually, with inter-provincial alliances serving as the pioneering front.

Pilot programs for the centralized procurement of high-value medical consumables were already launched last year in Anhui and Jiangsu provinces. The Beijing-Tianjin-Hebei Procurement Alliance has confirmed its participation, while the Western Alliance is highly likely to follow suit after ongoing assessments. Overall, following the “4+7” volume-based procurement initiative for pharmaceuticals, volume-based procurement of medical consumables by category—led by the National Healthcare Security Administration and local healthcare security bureaus—is expected to accelerate significantly.

Currently, the path and methodology for centralized procurement of medical consumables, which largely follow the approach used for pharmaceuticals, have been essentially established. However, due to the inherent characteristics of medical devices—such as a vast number of product specifications, complex models and applications, fragmented distribution channels, and weak traceability infrastructure—the pace of centralized procurement will be significantly slower compared to that of pharmaceuticals.

The primary challenges lie in, first, the significant difficulty of catalog integration. The medical device industry features numerous consumables that are custom-designed for individual physicians and dedicated devices tailored to specific clinical usage patterns.

Second, there are no clear regulations on product grouping. The current centralized procurement model only stratifies device quality based on manufacturers and product qualifications, while lacking clear definitions and standards for the classification of “product varieties.”

Nevertheless, it is believed that under the country’s series of reforms, the full implementation of volume-based procurement is only a matter of time. Therefore, for enterprises, passive avoidance is certainly not a viable strategy; instead, the appropriate response is to confront the opportunities and challenges brought by volume-based procurement and make proactive strategic preparations.

In light of the experience with centralized drug procurement, volume-based procurement for medical devices may face the following challenges:

Facing a significant price reduction, with an expected decrease of over 50%

Medical consumables that account for a significant proportion of healthcare costs have a substantial impact (e.g., balloon dilation catheters, coronary stents, infusion sets, bone plates, intraocular lenses, etc.)

Using market access as leverage, failure to reach a successful negotiation will result in exclusion from public hospitals.

Uncertainty remains as to whether supporting policies can achieve price reductions through volume-based procurement.

Poses a Disruptive Challenge to the Existing Pricing System and Procurement Model

Of course, beyond the challenges, there are also the following opportunities:

If policies provide a certain degree of exclusive procurement guarantees and companies accept price reductions, it will be conducive to market share expansion.

Reduce the pressure from upcoming tender projects and secondary price negotiations for hospital admission.

Shorten the product market access process to achieve rapid short-term market coverage

2. Pricing and Fee Charging Phase

Reducing the costs of pharmaceuticals and medical consumables, as one of the four key areas in deepening healthcare reform, will continue to remain a central theme of relevant policies.

In January 2019, the “Opinions on Strengthening the Performance Appraisal of Tertiary Public Hospitals” explicitly stipulated that indicators related to rational drug use should replace the sole reliance on the drug proportion metric for performance assessment.

Although not explicitly stated, reducing energy consumption and the proportion of drug costs will remain one of the targets of national policy efforts, albeit with greater room for adjustment and flexibility.

Since May 2019, the elimination of markups on medical consumables has been accelerated. To date, numerous provinces have successively introduced policies, and it is expected that reforms in this area will be completed shortly.

On the other hand, the National Healthcare Security Administration (NHSA) and the National Health Commission (NHC) have respectively issued new editions of the National Specifications for Medical Service Price Items, and the state has required all provinces to strengthen supervision over compliant charging practices in public hospitals.

Sources: Ryan Partners interview & analysis

3. Medical Insurance Reimbursement Process

Regarding medical insurance, research on the inclusion of medical consumables in the medical insurance coverage and the establishment of reimbursement standards is about to be initiated; enterprises should pay close attention to its progress.

Sources: Ryan Partners interview & analysis

In summary, it is evident that as the state achieves significant successes in pharmaceutical reform and regulation, governance and reform in the medical device industry will not lag far behind. State oversight in this sector may be delayed, but it will not be absent.

A deeper analysis reveals that reform and governance do not necessarily imply hindered corporate development. However, it is certain that passive avoidance is never a viable path to revitalization amidst reform. On the contrary, proactively embracing change is the key to seizing opportunities. We believe that enterprises best positioned to grasp the pulse of policy trends and actively adjust their strategies will surely capture new opportunities and create fresh possibilities amid the sweeping tide of change.

Author: Ryan Partners

Ryan Partners provides clients with comprehensive solutions, including global market research, market access strategies, and market potential assessments, among other business intelligence services. We help clients address various challenges encountered at different stages of the business cycle, enabling them to evaluate and understand market environments and potential opportunities, thereby enhancing their competitiveness in the global marketplace.

Website: http://www.ryan-partners.com/

WeChat Official Account: ruianshangwu