PPD Rebounds with 11.11% Surge Post-Re-IPO: Can the Debt-Relieved CRO Giant Stage a Comeback?

Pharmaceutical Product Development

Global Contract Research Organization (CRO)

VCBeat learned that on February 6, 2020, U.S. time, PPD, the giant American CRO, went public again to raise capital after being taken private. In this offering, PPD issued a total of 600 shares0 million shares were issued at $27 per share, the top end of the pricing range, raising a total of $1.62 billion. The stock opened at $31 on its debut day, up 14.81%. It then eased slightly, closing at $30, for a gain of 11.11%. PPD’s current market capitalization stands at $10.18 billion, successfully surpassing the $10 billion mark.

(Chart source: Tiger Brokers)

Prior to its privatization in 2011, PPD was once among the most promising CRO companies globally. However, its growth slowed somewhat after going private. By 2018, total revenue had only doubled compared with 2010, reflecting an annual growth rate of approximately 10%. In addition, PPD currently carries a substantial amount of external debt; the proceeds from this IPO will be used primarily to repay the debt accumulated by PPD.

Behind the balance sheet showing insolvency, what is PPD’s actual capital position? And how will it turn the tide in its future development?

Founded in 1985, PPD is one of the earliest CRO companies established globally. When PPD made its debut on the secondary market in 1996, its IPO price had already reached $16 per share. Thereafter, PPD’s development remained relatively steady until 2009.

In 2009, the outbreak of the subprime mortgage crisis and the ensuing economic downturn had a significant impact on the CRO industry. Many CRO companies experienced stagnant or even negative growth in 2009, including PPD. PPD’s revenue decreased by $135 million year-over-year in 2009, representing a 9% decline. However, this situation did not last long; by 2010, PPD’s revenue had returned to normal levels. At that time, PPD resumed revenue growth, generating annual net profits of approximately $200 million, holding around $640 million in cash and about $520 million in working capital, with total assets nearing $2 billion, making it a high-quality asset.

Large-scale M&A in the CRO industry seems to be commonplace. Today, the world’s two largest CRO companies, Labcorp and IQVIA, are both the result of mergers between CRO giants. WuXi AppTec was also nearly acquired by CRL back in the day. Therefore, high-quality assets like PPD immediately attracted capital attention. However, PPD’s privatization process differed from that of other companies; it did not voluntarily delist like WuXi AppTec, nor was it acquired by another corporate entity, but rather underwent privatization through an acquisition by a private equity fund.

In 2011, The Carlyle Group and Hellman & Friedman acquired PPD at $33.25 per share, for a total transaction value of $3.9 billion. In retrospect, PPD at the time boasted robust cash flows, sustained performance growth, and operated in a high-growth sector; its price-to-earnings ratio of over 20x clearly undervalued its market worth. These two investment firms should have reaped substantial profits from their investment in PPD.

However, following its privatization, PPD’s development fell short of expectations. According to the latest disclosed revenue figures, PPD’s revenue in 2014 was $1.92 billion, representing only a 30% increase from $1.47 billion in 2010. Such performance was clearly unacceptable for a company like PPD. Consequently, starting in 2016, PPD embarked on a path of mergers and acquisitions.

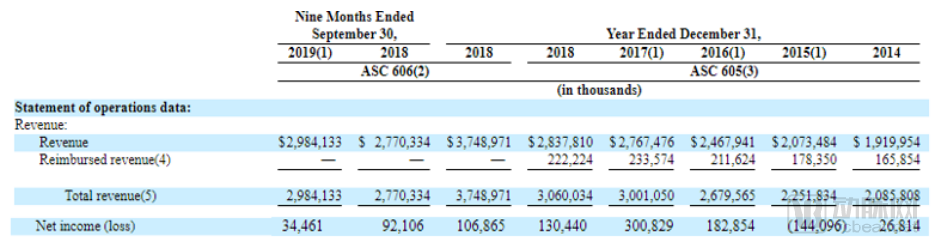

Partial Financial Data of PPD

PPD’s M&A Activity in Recent Years

Between 2016 and 2019, PPD completed five acquisitions over a four-year period. The primary objective of these acquisitions was to further strengthen its clinical research capabilities and expand its business capacity in real-world evidence (RWE) studies. Following two major acquisitions in 2016, PPD’s overall revenue, particularly from its clinical research segment, showed significant improvement. However, this growth momentum was short-lived. Under the same revenue recognition standards, PPD’s total revenue growth rates for 2018 and the first nine months of 2019 were only 1.97% and 7.72%, respectively.

Net profit figures are even more concerning. In 2017, PPD’s net profit reached $300 million. By 2018, however, it had shrunk to $130 million. In the first nine months of 2019, net profit declined further to just $34.46 million.

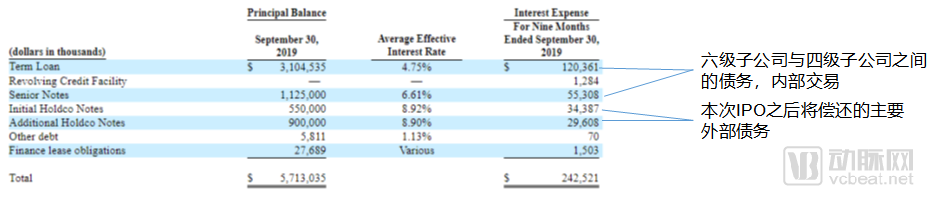

Major Debt Profile of PPD

In addition to its mediocre revenue performance, PPD’s debt situation appears even more perilous. According to PPD’s prospectus, total debt amounts to $5.7 billion, exceeding its total assets. All proceeds from this IPO will be used to repay $1.45 billion in debt maturing in 2022. Even after this repayment, PPD will still carry $4.23 billion in debt.

In reality, two key components of PPD’s liabilities—term loans and senior debt—are intragroup transactions, originating as borrowings by PPD’s original operating entity, “Pharmaceutical Product Development, LLC,” from its indirect parent company, “Jaguar Holding Company II.” In the 2017 restructuring, “Jaguar Holding Company II” became an indirect subsidiary of the current listed entity, “PPD, Inc.,” thereby converting these related-party obligations into intragroup transactions. This reclassification caused both liabilities and assets to increase simultaneously, without materially affecting the company’s operational performance.

Apart from debts arising from intercompany transactions, PPD’s external liabilities primarily consist of $1.45 billion in debt that will be repaid with the proceeds from this initial public offering (IPO). In other words, following the IPO, PPD’s external liabilities will be nearly reduced to zero. Although its cash reserves will be significantly depleted, the elimination of annual interest payments after settling these external debts should allow PPD’s net profit to return to a healthy level.

PPD has been engaged in drug development services for over 30 years, providing comprehensive clinical development and laboratory services to pharmaceutical, biotechnology, medical device, and government organizations, as well as other industry participants. PPD helps clients accelerate the time-to-market for new drugs, ensuring extended market exclusivity periods post-launch.

Today, PPD has approximately 23,000 employees globally and operates 100 offices across 46 countries and regions. Over the past five years, PPD has conducted more than 2,100 clinical trials, with its laboratory scientists completing over 57,000 drug development projects and processing more than 7,600 compounds. In 2018 alone, PPD contributed to 66 drug approvals and established collaborations with more than 300 biotechnology companies.

Although PPD’s financial performance has been mediocre in recent years, it remains one of the largest CRO companies globally. Its strong market positioning, long-term stability in clinical trial services, rapidly growing laboratory services, and early strategic investments in real-world studies may all help PPD stage a comeback against headwinds.

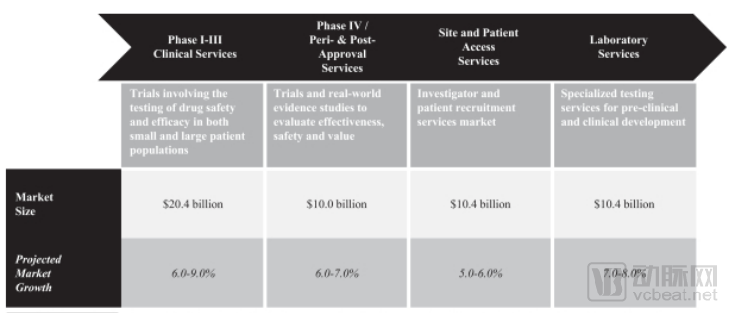

Market Size Estimates in PPD’s IPO Prospectus

PPD estimates in its prospectus that its total addressable market exceeds $51 billion, encompassing clinical trial services, pre- and post-approval services, site and patient registry services, and laboratory services. Under the current development landscape of the CRO industry, three major trends are driving the continuous expansion of the industry’s potential market size.

First, pharmaceutical companies’ R&D expenditures are continuously increasing. From 2008 to 2018, the average annual growth rate of Investigational New Drug (IND) applications in the United States was 30%, while pharmaceutical companies’ annual R&D spending grew at an average rate of 3.3%. These increases will drive the prosperous development of the CRO market.

Second, the complexity of clinical development is continuously increasing. Many factors are driving clinical research toward greater complexity, such as more complex treatment modalities, more specific inclusion and exclusion criteria, a greater number of clinical endpoints, and heightened demands for clinical evidence. These challenges make it increasingly difficult for pharmaceutical companies to conduct clinical trials independently, thereby intensifying the demand for clinical CROs.

Third is the growth of new biotechnology and biopharmaceutical companies. As more products utilizing novel biotechnologies enter clinical trials, an increasing number of biotech firms are partnering with CROs to ensure the smooth conduct of their clinical studies. According to relevant data, the outsourcing penetration rate among biopharmaceutical companies has risen from 36% in 2007 to 49% in 2018, and this figure is expected to continue growing in the future.

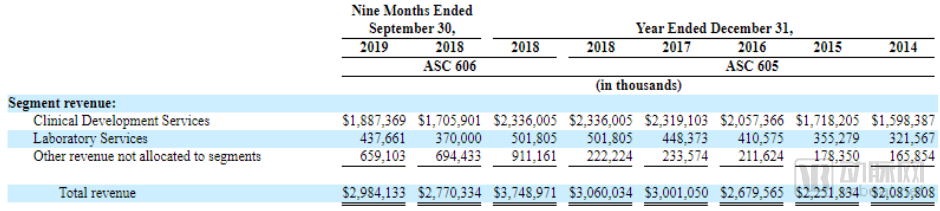

PPD's Revenue Composition

Clinical trial services currently constitute the core business segment of PPD and have long represented the primary source of its revenue. PPD offers clients a service model distinct from those of other clinical CROs, maintaining competitive advantages particularly in two key areas: patient recruitment and clinical trial sites.

Over the past five years, further consolidating its advantages in clinical trial services has remained at the core of PPD’s development strategy. Of the five companies it acquired, three were directly related to clinical trials, with a specific focus on clinical trial site management and patient recruitment.

During the initial patient recruitment phase, PPD constructed a large dataset comprising demographic information for 100 million authorized U.S. households and health records of 20 million previously screened candidates. These data enabled PPD to identify and recruit eligible clinical trial participants from its own database at maximum speed.

In terms of global collaboration, PPD’s AES delivery model ensures consistent execution of clinical trials across more than 180 investigative sites in 17 countries spanning five continents. Over the past five years, this system has been utilized in over 750 studies, including those conducted by PPD itself, its clients, and other CROs using the system.

PPD offers a comprehensive suite of laboratory services, including bioanalysis, biomarkers, vaccines, GMP, and central laboratory infrastructure, to support early-stage drug development. PPD has assembled a highly qualified scientific team of 430 professionals, including 160 PhDs and 270 Master’s degree holders.

Among various laboratory services, biotechnology products are helping PPD build its core competitive advantages. PPD developed its dedicated PPD Biotech model in 2014 and has continuously iterated on it. Currently, the platform’s average success rate has increased from approximately 26% in 2016 to over 35% in 2019.

In terms of revenue, the proportion of laboratory services in PPD’s total revenue has been continuously increasing, maintaining a high growth rate since 2014. In the first nine months of 2019, revenue grew by 18.3% compared to the same period last year.

PPD is a global leader in real-world evidence (RWE) studies, with its current coverage spanning 35 countries and regions worldwide. In addition to RWE studies, PPD’s research team of up to 450 professionals can assist clients in conducting health economics, epidemiology, and market access research. To strengthen these capabilities, PPD acquired Evidera, a real-world evidence company, for $170.5 million in 2016, and subsequently purchased Medimix International for $37.8 million in 2019. Looking ahead, real-world evidence will remain one of the key drivers of PPD’s growth.