Chinese Insurance Industry's Rapid Response to COVID-19: New Products Launched Within 24 Hours and Claims Initiated for Dr. Li Wenliang

Unprecedented.

Jiang Guanjun used these four words to evaluate the response speed of insurance companies during this epidemic. Jiang Guanjun is a partner at Mingde Actuarial Consulting Company. He believes that during this epidemic, many insurance companies responded quickly and demonstrated excellent efficiency.

At the beginning of 2020, the health insurance industry did not welcome news that its market size had reached one trillion yuan; instead, it faced the grim reality of a rapidly rising number of infections due to the spreading pandemic. In response, the health insurance sector, which prioritizes risk control above all else, rose to the challenge.From regulatory bodies such as the China Banking and Insurance Regulatory Commission (CBIRC) and the National Healthcare Security Administration (NHSA), to traditional insurance giants like Ping An Insurance, China Taiping, and China Life Insurance, and further to innovative companies such as Tencent WeSure, Shuidi, and Yuanxin Huibao, a series of significant measures have been introduced to combat the pandemic, steadfastly safeguarding the victory in this critical battle from the perspective of medical expense coverage.

Following the outbreak, the National Healthcare Security Administration swiftly introduced policies stipulating that all medical expenses for confirmed patients would be fully covered by the state. Subsequent policies further extended national health insurance coverage to include medical costs for suspected cases. The China Banking and Insurance Regulatory Commission also promptly issued relevant guidelines, mandating the establishment of green channels for insurance claims settlement and strengthening insurance innovation. Major insurers such as Ping An Insurance and China Pacific Insurance quickly rolled out numerous innovative measures, including expanding the scope of medical insurance coverage and shortening waiting periods. Innovative companies like Tencent Weibao and Shuidi launched free insurance products to safeguard the lives and health of frontline healthcare workers.

Stakeholders in the health insurance industry have responded decisively, bolstering the critical battle against this epidemic.

On January 23, 2020, the China Banking and Insurance Regulatory Commission (CBIRC), the National Healthcare Security Administration (NHSA), and ten other ministries and commissions jointly issued the landmark document “Opinions on Promoting the Development of Commercial Insurance in the Social Services Sector,” which once again provided strong support for the development of health insurance.and proposed a plan to strive for the commercial health insurance market size to reach 2 trillion yuan by 2025.

Furthermore, this document explicitly outlines five key areas of focus for future efforts: improving health insurance products and services, strengthening the protection function of commercial pension insurance, vigorously developing commercial insurance in sectors such as education, childcare, domestic services, culture, tourism, and sports, supporting insurance fund investments in social service sectors including healthcare and elderly care, and perfecting the insurance market system.

Three days after the release of this policy-setting document for industry development, the China Banking and Insurance Regulatory Commission (CBIRC) published the “Notice on Strengthening Financial Services in the Banking and Insurance Sectors to Support Prevention and Control of the Novel Coronavirus Pneumonia Epidemic” on its official website. The notice emphasized key directions such as enhancing online business services, prioritizing claims processing for customers infected with the novel coronavirus, appropriately expanding coverage scope, and ensuring all eligible claims are paid.

Overview Chart of Key Policy Documents During the Pandemic

On February 3, to support the critical efforts in combating the epidemic, multiple secondary departments of the China Banking and Insurance Regulatory Commission (CBIRC) urgently issued several important notices, proposing a number of more specific measures:

1. It is strictly prohibited to hype up insurance products by exploiting the epidemic, and it is strictly prohibited to organize industry gatherings or conduct concentrated client visits.

2. Appropriately expand insurance coverage. Support life and health insurance companies, under the premise of controllable risk, in removing restrictions such as waiting periods (observation periods), deductibles, and designated hospital requirements for customers with novel coronavirus pneumonia within disease insurance and medical insurance products. Support the extension of coverage liability in accidental injury and disease insurance products to include novel coronavirus pneumonia. Property and casualty insurance companies may extend coverage to include liability for novel coronavirus pneumonia in short-term health insurance products such as critical illness insurance.

3. Establish a green channel to ensure timely delivery of claims services, streamline the claims process, and improve the efficiency of insurance claim settlements.

The above are key documents in the health insurance sector during the pandemic. In the immediate aftermath of the outbreak, the National Healthcare Security Administration and other relevant departments promptly issued policies.Clarify the role of the national medical insurance as a safety net for COVID-19 patients.

On January 23, the National Healthcare Security Administration and other authorities issued the "Notice on Ensuring Medical Security for the Novel Coronavirus Pneumonia Epidemic." The notice stipulates: making every effort to ensure that patients receive timely treatment without being hindered by cost concerns; ensuring that designated medical institutions are not impeded in providing care due to regulations on global budget management of medical insurance; and ensuring that patients’ access to medical services is not affected by financial burdens. Medical expenses related to novel coronavirus pneumonia shall be settled and managed under the single-disease payment model of basic medical insurance.

For patients diagnosed with novel coronavirus pneumonia, the portion of medical expenses borne by individuals after payments from basic medical insurance, critical illness insurance, and medical assistance in accordance with regulations shall be subsidized by fiscal funds to ensure comprehensive coverage.Medications and medical services used for patients diagnosed with novel coronavirus-infected pneumonia, if compliant with the diagnosis and treatment protocols formulated by health authorities, may be temporarily included in the coverage of the basic medical insurance fund. For patients diagnosed with novel coronavirus-infected pneumonia who receive medical treatment outside their home regions, treatment shall be provided prior to settlement, and the regulation reducing the reimbursement rate for out-of-area referrals shall no longer apply.

On January 27, the General Office of the National Healthcare Security Administration, the General Office of the Ministry of Finance, and the General Office of the National Health Commission jointly issued the "Supplementary Notice on Ensuring Medical Security for the Novel Coronavirus Pneumonia Epidemic." The notice stated that, to implement the decisions and deployments of the CPC Central Committee and the State Council, ensure medical security during the novel coronavirus pneumonia epidemic, and effectively cover the medical expenses of suspected cases, additional measures would be taken beyond those already in place for confirmed cases. During the epidemic period, for medical expenses incurred by suspected patients as defined in the diagnosis and treatment protocols for novel coronavirus pneumonia issued by health authorities, after payments are made through basic medical insurance, critical illness insurance, and medical assistance in accordance with regulations, the portion borne by individuals shall be covered through comprehensive safeguards. Local governments where treatment is received shall formulate fiscal subsidy policies and allocate funds accordingly, with the central government providing appropriate subsidies based on circumstances.

On February 2, the General Office of the National Healthcare Security Administration reissued the “Notice on Optimizing Medical Insurance Handling Services to Promote the Prevention and Control of Novel Coronavirus Pneumonia.” The notice specifies that during the epidemic, a “long-prescription” reimbursement policy shall be implemented; for patients with chronic diseases such as hypertension and diabetes, upon evaluation by physicians at treating hospitals, the prescribed medication supply may be extended to up to three months. Meanwhile,Appropriately extend the reimbursement period for medical expense coverage under the 2019 healthcare security services. Ensure that patients’ access to medical care is not hindered by financial concerns, and that designated hospitals are not impeded in providing treatment due to payment policies.

Under strong regulatory intervention, a robust defense line has been established for patients’ medical expenses during the pandemic, with the national basic medical insurance fund serving as the safety net and commercial insurance acting as a supplement. Specifically,Specifically, medical expenses incurred from the diagnosis, isolation, and treatment of COVID-19 during the pandemic are covered by basic medical insurance, while death benefits, lost wages due to missed work, costs associated with concurrent critical illnesses, and treatment for sequelae are covered by commercial insurance.

Following the outbreak, more than 20 insurance giants, including Ping An Insurance, China Taiping, and PICC, swiftly mobilized to donate funds and supplies. As of February 3, a total of 23 insurance institutions—including the Insurance Association of China, PICC, China Life, China Re, Ping An Insurance, and Taikang Insurance—had contributed over RMB 300 million in donations.

In addition to direct cash donations, these insurance giants have also provided insurance coverage with sum assured amounts ranging from RMB 200,000 to over RMB 1 million to the city of Wuhan, as well as to disease control and medical personnel deployed from across China to Wuhan to combat the pneumonia outbreak, along with their families, armed police officers and soldiers, frontline media workers, and courier and logistics staff. For instance, China Life donated a total sum assured of RMB 90 billion, while Sunshine Insurance provided coverage exceeding RMB 100 billion. As epidemic prevention and control efforts advance, the population covered by such insurance protection continues to expand.

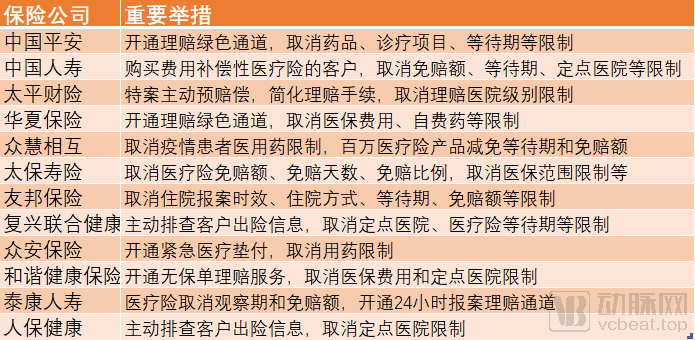

At the product level, major insurance companies have also rapidly introduced exceptional measures, such as waiving observation periods and waiting periods, eliminating deductibles, and removing restrictions on covered medical services and designated hospitals.

(Key Initiatives by Some Insurance Companies During the Pandemic)

Taikang Life Insurance issued a statement clarifying that diseases caused by novel coronavirus infection are covered under standard claims; it waived the 30-day observation period and deductibles for medical insurance and enabled advance claim payments. Ping An Insurance launched five humanitarian care measures, including waiving restrictions on medications, diagnostic and treatment items, waiting periods, and deductibles. Hongkang Life Insurance activated a green channel for critical illnesses, assisting customers who had already filed claims with medical consultations and arranging accompanying services. Zhonghui Mutual Insurance announced waivers of waiting periods and deductibles for its million-yuan medical insurance products in response to pneumonia caused by the novel coronavirus.

In terms of claims settlement, major insurance companies have also activated green channels to expedite the process. Ping An Insurance rapidly completed six claim settlements and four advance payments, with a total payout amounting to nearly RMB 730,000. Dajia Life Insurance, upon receiving a claim report from a customer in Wuhan, waived certain procedural requirements; after collecting the beneficiary’s documentation, it finalized the claim within 10 minutes and disbursed the payment within 30 minutes. China Life Insurance also promptly settled claims for eight insured individuals, including patients and frontline anti-epidemic workers. Taikang Insurance, after donating special insurance coverage with a sum insured of RMB 200,000 per person to medical staff in Wuhan, quickly processed its first such claim for a Wuhan healthcare worker, paying out RMB 200,000.

Regarding the measures taken by insurance companies during this pandemic, Jiang Guanjun believes that “this is not only a reflection of corporate social responsibility but also a test for the industry.” However, he notes that with medical expenses being covered by the state, the risk borne by commercial insurers is relatively low; the key area for commercial insurance to focus on lies in addressing patients’ post-pandemic sequelae after the outbreak ends.

In the early hours of February 7, Dr. Li Wenliang of Wuhan Central Hospital passed away due to COVID-19 infection. The Wuhan Municipal Human Resources and Social Security Bureau recognized that Dr. Li, as a medical worker, was unfortunately infected while fighting the COVID-19 epidemic and died despite rescue efforts, thereby certifying his death as work-related. According to calculations, Dr. Li’s work-related injury insurance benefits are as follows: a one-time death allowance of RMB 785,020 and a funeral allowance of RMB 36,834.

Regarding commercial insurance, Dr. Li Wenliang’s death falls within the scope of insurance liability. According to Taikang Life Insurance’s official WeChat account, it has been verified that Dr. Li Wenliang was a policyholder of Taikang Life Insurance and met the criteria for death benefit coverage; the death benefit has now been paid out in accordance with standard procedures.

Based on public information from other insurers, PICC has currentlyAccording to the previously establishedInsurance coverage plan completed with a total payout of RMB 800,000. Among this, PICC Property and Casualty Company paid RMB 500,000, and PICC Life Insurance paid RMB 300,000. The entire amount of RMB 800,000 was transferred to Dr. Li Wenliang’s family on the same day. BOCOM Life Insurance promptly initiated the claims process for Dr. Li Wenliang, honoring its public commitment made on January 26 regarding the novel coronavirus outbreak. The company decided to pay a total death benefit of RMB 1 million to his legal beneficiaries in accordance with the policy terms. To minimize additional burden on Dr. Li’s family, all claims procedures and payments were completed online through a “no-face-to-face” approach on the morning of February 8.

Furthermore,Ping An Insurance, Guohua Life Insurance, etc.Multiple insurance companies have also initiated claims procedures.

During this epidemic, a number of innovative health insurance companies also delivered standout performances.

During the New Year holiday, Tencent WeSure, led by CEO Liu Jiaming, saw key personnel from various departments cancel their leave and take proactive measures, working through the night to develop the product. The product evolved from an initial concept to its final launch and customer release.“Medical Insurance Protection · Special Edition for Novel Coronavirus Pneumonia” Launched in Just 24 Hours. This product offers a fixed quota of 100,000 units, providing zero-premium coverage for frontline medical personnel.

WeSure Vice President Zhang Wen is virtually on call 24/7, overseeing the company’s product, development, and marketing efforts. “He basically responds to messages promptly at any time,” said one employee. Due to his daily presence on the front lines of business operations to provide strategic guidance, Zhang fell ill with a fever from prolonged overwork, yet he still got up early the next day to drive business progress.

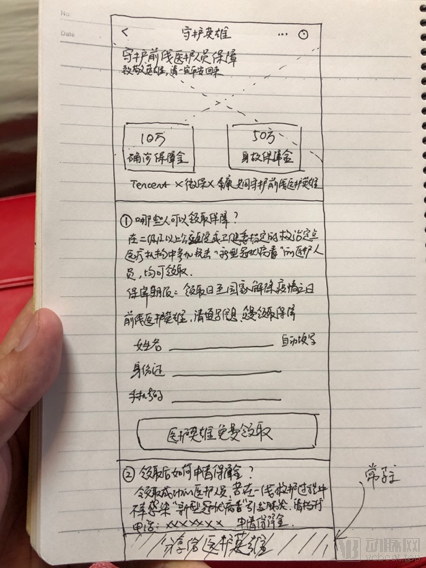

Starting from the second day of the Lunar New Year, the entire WeSure project team was resting at 1 or 2 a.m. and beginning work at 8 a.m. the next day. A WeSure employee recalled the situation: “On the second day of development, it was already 2 a.m., yet our developers were still syncing up on progress in the group chat; some only returned home then, only to resume production verification punctually at 8:30 a.m. the following morning. Our product and design colleagues also operated in ‘crunch mode’ around the clock, regardless of whether it was day or night. Liu Dongdong, Director of our company’s Design Center, did not have a computer at home, so he hand-drew a prototype of the product interface. The design team quickly followed up with polished designs, which was truly moving.”

The image shows a hand-drawn prototype of the product page by WeSure employees in an emergency situation.

“After we went live, we joked around in the work group chat, amazed that we had actually managed to develop a product in just one day.”

In addition to providing exclusive free coverage to frontline healthcare workers, on February 5, WeSure also offered unlimited “WeMed Insurance · Free COVID-19 Coverage” to people across China, with each individual eligible for up to RMB 50,000 in COVID-19 coverage; it further provided RMB 100,000 in free COVID-19 coverage to over 30 million WeSure policyholders, bringing the total coverage amount to more than RMB 3 trillion.

Shuidi Insurance, in partnership with AXA Insurance, has donated the “Worry-Free Epidemic Protection” insurance policy to frontline healthcare workers and journalists, providing a death benefit of RMB 600,000 for confirmed cases and RMB 100,000 for accidental deaths. Additionally, through Shuidi’s charitable fundraising platform, Shuidi has collaborated with multiple nonprofit organizations to raise RMB 43 million.

Yuanxin Technology and Yuanxin Huibao, under the Miaoshou Doctor brand, have also launched “Yiqi Bao,” providing RMB 100,000 in medical coverage to healthcare professionals and their immediate family members.

(Innovative Health Insurance Products During the Pandemic)

From the perspective of insurance product design, the development of insurance products must adhere to the law of large numbers. However, novel coronavirus pneumonia is a newly emerging disease with no historical data available. During this epidemic, the introduction of these health insurance products represents an unprecedented innovation.

Following the outbreak, regulators such as the China Banking and Insurance Regulatory Commission (CBIRC) and the National Healthcare Security Administration (NHSA), traditional insurance giants like Ping An Insurance and China Taiping, as well as innovative health insurers such as WeSure and Shuidi, all responded swiftly. They established a robust defense line covering medical expenses in the fight against the pandemic, demonstrating their commitment and responsibility in rising to the challenge.

From the perspective of the health insurance industry, the pandemic has had a negative impact on many sectors of society, but it has positively boosted the commercial health insurance sector. The outbreak served as a practical test for industry development and raised public awareness of insurance to a certain extent. Undoubtedly, the industry will maintain the momentum seen in 2019 and continue its rapid growth.

The pandemic is ruthless, but we care! VCBeat has selected a highly cost-effective epidemic insurance product from our trusted partners to help safeguard the health of you and your family. This product, "COVID-19 Care Insurance," is offered by Abao Insurance in collaboration with JD Allianz Insurance. For specific details, please refer to the detailed description of the insurance product. You may scan the poster to learn more and purchase as needed.