Four Key Trends Shaping China's Healthcare IT Sector in 2020: EHR Upgrades, CDSS Expansion, DRG Implementation, and Smart Service Ratings

Recalling the SARS outbreak that ravaged China 17 years ago, many hospitals were still in a vacuum regarding Hospital Information Systems (HIS) and Picture Archiving and Communication Systems (PACS). Lacking informational support, numerous hospital areas became significant sites for viral transmission.

From an informatics perspective, everything proceeded in an orderly manner during the fight against the 2019-nCoV epidemic. A radiologist at Wuhan Tongji Hospital told VCBeat, “We interpret thousands of CT scans every day, covering both patients from other regions and local residents. The entire process of data ingestion has remained smooth, with various imaging studies and laboratory test results for patients being accurately and rapidly integrated into their medical records. This has fundamentally supported the efficiency of Wuhan’s epidemic response.”

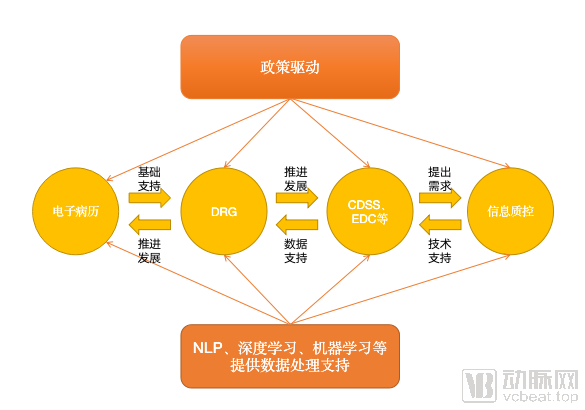

The current landscape is inseparable from the state’s emphasis on informatization and hospitals’ investments in it. Looking back at the development of informatization, since 2018, policies related to electronic medical records (EMR) have been introduced in quick succession. At the end of that year, the issuance of the “Notice on Printing and Distributing the Administrative Measures (Trial) and Evaluation Standards (Trial) for the Graded Evaluation of the Application Level of Electronic Medical Record Systems” ushered in a boom in China’s healthcare informatization market in 2019.

Electronic medical record (EMR) grading and interoperability initiatives are driving more than just basic healthcare informatization. Propelled by numerous policies in 2019, competition has intensified in specialized areas such as Clinical Decision Support Systems (CDSS), Diagnosis-Related Groups (DRG), and hospital-based quality control. Given the highly fragmented nature of the healthcare IT market, a growing number of enterprises have entered the fray in this new era of healthcare informatization.

At the beginning of 2020, VCBeat interviewed more than ten healthcare IT companies to review the key achievements in healthcare informatization development in 2019 and explore the direction of informatization development in 2020. The answers lie within the data.

As a sector heavily driven by policy, the development of hospital informatization features relatively long and slow cycles, whereas the introduction of key policies can often produce immediate and significant impacts on reforms within hospital information departments. In this context, the interpretation of such policies by enterprises, and indeed by the entire industry, becomes critically important.

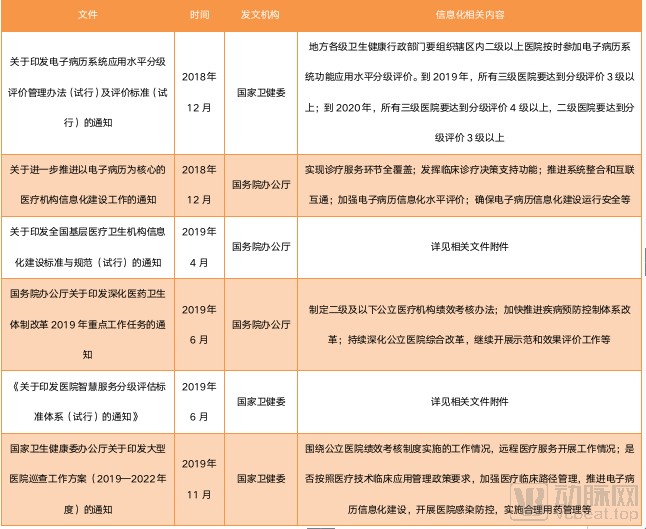

As the patient-centered care concept continues to strengthen, electronic medical records (EMRs) have become the core of healthcare informatization transformation and remain a key focus of policy emphasis. A statistical review of policies issued by the State Council and the National Health Commission from January 1, 2018, to December 31, 2019, reveals that nine policies explicitly outlined mandatory national requirements for EMRs. Notably, the “Notice on Issuing the Administrative Measures (Trial) and Evaluation Standards (Trial) for the Graded Evaluation of Electronic Medical Record System Application Levels,” released in December 2018, directly drove business growth for healthcare IT enterprises.

Selected Policies on Electronic Medical Records Since Late 2018

Policy documents from the past two years reveal that electronic medical records (EMR), promoted as the foundation of hospital information technology infrastructure, have frequently appeared in major policy initiatives and become a key focus of national health efforts. More critically, the performance evaluation of tertiary hospitals is now directly linked to their EMR implementation status, compelling hospitals to continuously enhance their EMR systems. Broadly speaking, in 2019, more than 7,000 hospitals across China applied for EMR grading assessments.

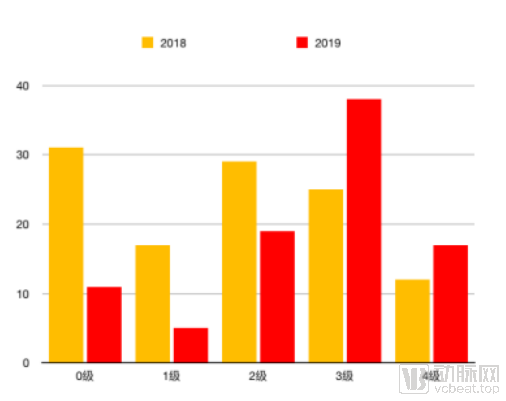

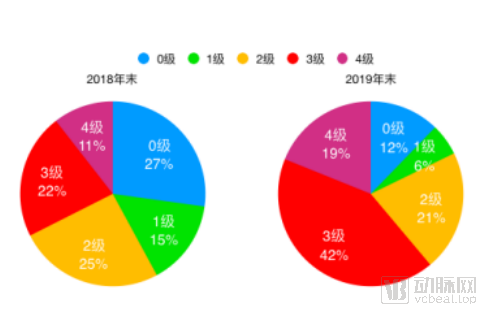

Taking the development of electronic medical records (EMR) in Beijing as an example, statistics on EMR implementation levels 0–4 at the end of 2018 show that hospitals at levels 0–2 accounted for one-third of the total. Hospitals at level 4 were the fewest, with only 12 institutions, representing 11%. Driven by policy initiatives, Beijing’s hospital EMR landscape improved significantly within just one year. By the end of 2019, the number of hospitals achieving level 3 EMR status reached 38, accounting for 42% and surpassing the combined total of hospitals at levels 0–2. Meanwhile, the number of hospitals reaching level 4 also increased, with 17 hospitals in Beijing meeting the level 4 standards.

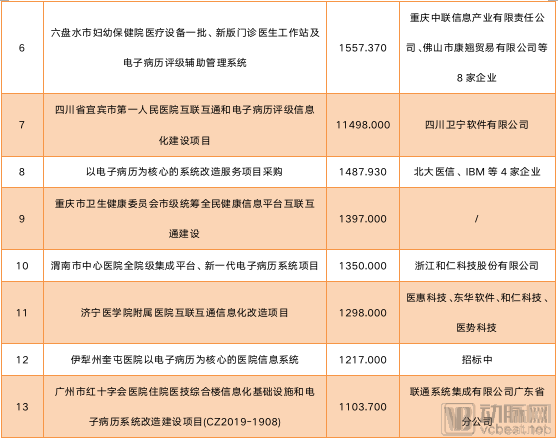

To gain a clearer understanding of how hospitals are driving upgrades in their accreditation ratings, VCBeat analyzed public tender data from 2019 (sourced from the China Government Procurement Network) and identified 227 tenders directly related to Electronic Medical Record (EMR) systems and Interconnectivity Maturity Assessments (excluding third-party investments and integrated turnkey projects). The data revealed that there were 13 tenders valued at over RMB 10 million, 37 tenders valued between RMB 5 million and RMB 9.99 million, and 177 tenders valued below RMB 5 million.

Status of 13 Targets Valued at Over RMB 10 Million

Project prices under different bidding scenarios to some extent reflect market segmentation; through simple calculations, we can estimate the electronic medical record (EMR) market share that different companies can capture.

However, few companies are capable of providing hospitals with high-quality, comprehensive electronic medical record (EMR) implementation services. Consequently, due to the uneven levels of informatization across different departments, hospitals often need to engage multiple IT vendors for system upgrades.

For listed companies such as B-Soft, Winning Health, and DHC Software, they possess sufficient capability and reputation to undertake the comprehensive informatization construction of hospitals. Taking B-Soft as an example, in 2018, the company helped multiple clients pass the 2018 Graded Evaluation of Functional Application Levels of Electronic Medical Record (EMR) Systems and the National Assessment of Maturity in Interconnectivity of Medical and Health Information. Among these clients, two achieved Level 6 EMR rating, eight achieved Level 5 EMR rating, and several hospitals passed the Level 4 Class A assessment for standardization maturity in interconnectivity. In these projects, the smart hospital construction project based on big data at Fujian Medical University Union Hospital had a total contract value of RMB 147 million (RMB 42 million for hardware and RMB 105 million for software).

He Bingyu, an analyst at Zhongtai Securities, once told VCBeat: “The adoption of the general contracting model to expand business will inevitably lead to increased industry concentration. We are currently in the first phase of this consolidation, which is expected to deepen further in the future. Under these circumstances, large enterprises will hold greater advantages when bidding for major contracts worth tens of millions of yuan.”

However, startups such as Ruikang Yongchuang and Senyi Intelligence still have opportunities. By segmenting niche markets and providing specialized, high-quality services, they are capturing greater market share through ecosystem development and alliance building.

“Hospitals typically have two options: one is to engage a comprehensive integrator to address all their informatics needs; the other is to work with several specialized vendors to tackle specific issues in a targeted manner,” said Liu Xiaoguang, founder of Ruikang Yongchuang. “Publicly listed vendors generally offer replacement solutions that involve tearing down and rebuilding hospital information systems from scratch, whereas we focus primarily on retrofitting solutions, thereby reducing clients’ implementation risks and costs.”

“Meanwhile, we do not wish to operate in isolation. Therefore, we are collaborating with numerous startups to pool our respective strengths and develop comprehensive solutions—this is our own approach to ecosystem building.”

Furthermore, the sales promotion efforts of startups exhibit distinct regional characteristics. Ruikang Yongchuang’s business is primarily concentrated in regions such as Jiangsu, Jiangxi, and Hubei, while Zhonglian Information focuses on the Southwest region, where it has secured major contracts amidst intense competition.

In addition to the clear segmentation in unit prices, the 2019 tender information also reveals some emerging trends. According to statistics from VCBeat, among the aforementioned 227 tender notices, there were 17 projects for specialized electronic medical record (EMR) systems. These projects covered a wide range of fields, such as EMRs for nutrition systems, emergency departments, myopia and refractive surgery specialties, dentistry, and cardiovascular cloud-based EMRs, with tender prices ranging from RMB 500,000 to RMB 3 million. The concept of specialized EMRs has been proposed in recent years, but a unified definition and product format have yet to be established. From the perspective of their intended purpose, specialized EMRs are built upon general EMR systems by integrating the specific characteristics of specialized diagnosis and treatment processes. They aim to create an integrated system for clinical care, management, research, and teaching, thereby better supporting specialized clinical practices and improving patient satisfaction.

Liu Xiaoguang stated, “Hospitals currently implementing specialty-specific electronic medical records (EMRs) fall into two categories. The first comprises research-oriented hospitals that have already achieved a high level of health informatics maturity and require specialty-specific EMR systems for further upgrading. The second category is driven by policy considerations; for instance, certain regions have introduced policies mandating hospitals to implement specialty-specific medical records for particular disciplines. However, overall, most hospitals are still focusing on EMR grading assessments, improving data quality through closed-loop management, enhancing clinical data repositories, and optimizing information systems to effectively support clinical practice. In the future, specialty-specific medical records should leverage standardized clinical data repositories to provide more specialized analytics and services.”

”

Zhang Jun, Vice President of Medical Affairs at Senyi Intelligence, stated, “With the enhancement of national healthcare service capabilities and the state’s further requirements for the quality and efficiency of medical services, electronic health records (EHRs) are being driven toward greater intelligence and specialization. Furthermore, as hospitals increasingly emphasize the development of specialized clinical capabilities, new demands are being placed on EHR systems. Therefore, it is projected that a new market for specialized electronic health records is likely to emerge within the next two to three years.”

“In terms of meeting the requirements for specialty-specific electronic medical records (EMRs), it is necessary to further leverage intelligent technologies to strengthen the development of closed-loop specialty care pathways, enable lifecycle-wide collection and documentation of specialty-specific data, enhance specialty-oriented data visualization and analysis, and provide intelligent clinical decision support based on specialty knowledge bases.”

The development of electronic medical records (EMRs) has standardized data issues at the source, thereby laying the foundation for the widespread adoption of data-driven software such as Clinical Decision Support Systems (CDSS) and Electronic Data Capture (EDC) systems.

The concept of Clinical Decision Support Systems (CDSS) has been around for decades, but it has only recently ceased to be a “pseudo-proposition.” During its development, the first challenge CDSS faced stemmed from the complexity of medical knowledge; there is no simple linear correspondence between clinical questions and the knowledge base, making general-purpose algorithms difficult to apply in practice. The emergence of artificial intelligence has, to some extent, addressed this issue. Natural Language Processing (NLP) can leverage convolutional algorithms to filter potential answers and deliver the most credible results.

However, AI has not fundamentally resolved the challenges facing Clinical Decision Support Systems (CDSS). Due to the non-standardized nature of electronic medical records (EMRs), Natural Language Processing (NLP) models trained on suboptimal data struggle to provide accurate answers and find it difficult to generate outputs correlated with EMR data. The grading and standardization of EMRs have alleviated this issue to some extent. Today’s CDSS can meet the application needs of general practice and certain specialized scenarios, enabling functionalities such as risk warning and prognosis prediction.

From a policy perspective, this also represents a significant opportunity. Zhang Jun stated, “The essence of the Electronic Medical Record (EMR) grading system is actually a comprehensive overhaul of hospital information systems centered on EMRs, aimed at improving the quality and efficiency of medical services and ensuring patient safety. As EMR grading advances to Levels 5 and 6, the requirements for clinical decision support become more stringent, further promoting hospital informatization transformation and enhancing clinical quality and safety.”

Comparison of the “Evaluation Methods and Standards for the Functional Application Level of Electronic Medical Record Systems (2018 Revised Draft for Comment)”

As shown in the table above, primary clinical decision support mainly provides alerts for simple conditions, such as rational drug use, including alerts for drug incompatibilities and contraindications, and offers a knowledge base of clinical practice guidelines. Intermediate decision support can handle relatively complex conditions, such as contraindication alerts for medication use based on factors like diseases mentioned in medical history, diagnosis, age, and gender, providing a knowledge system grounded in evidence-based medicine. Advanced decision support leverages big data processing and machine learning, integrating guidelines, evidence-based medical knowledge systems, and real-world data to enable early warning of clinical behaviors, prognostic analysis, and recommendation of similar medical cases.

Based on actual implementation in 2019, the graded version and the general practice version of Clinical Decision Support Systems (CDSS) have become the mainstream paid products for hospitals and community health institutions. Lingyi Zhihui’s general practice CDSS has been deployed in over 1,000 primary healthcare institutions, while Senyi Intelligent’s hospital-wide CDSS is currently being used by multiple hospitals across China.

However, similar to specialty-specific electronic medical records (EMRs), the future development trend of Clinical Decision Support Systems (CDSS) will inevitably shift from focusing on grading evaluations to specializing in specific clinical domains. Based on existing products, Yidu Cloud has developed CDSS solutions for liver cancer and other conditions; Jiahhe Meikang has created CDSS tools for breast diseases; Senyi Intelligence has developed CDSS for venous thromboembolism (VTE) prevention and control; Huimei Technology has built CDSS for myocardial infarction; LinkDoc Technology offers big data-driven oncology CDSS; and Yuwei Medical has constructed CDSS systems for prostate cancer, glioma, lymphoma, and other diseases. These products are expected to increase their market penetration as hospital information technology infrastructure continues to advance.

Data standardization also applies to products such as Electronic Data Capture (EDC) systems that rely on data as input. For research utilizing clinical data, the standardization of electronic medical records creates a more favorable research environment.

When it comes to policy-driven initiatives, Diagnosis-Related Groups (DRG) have emerged as another major force this year. On October 24, the National Healthcare Security Administration issued the technical standard titled “National Healthcare Security DRG (CHS-DRG) Grouping Scheme.” This official template has brought uniformity to the previously fragmented landscape of DRG (payment per service unit) grouping systems, firmly establishing DRG as the basis for health insurance reimbursement.

Currently, 30 cities have been designated as national pilot cities for Diagnosis-Related Group (DRG) payment, with requirements to conduct simulation operations in 2020 and initiate actual payments in 2021. Subsequently, various news reports emerged: Zhejiang Province is poised to become the first province in China to implement a unified DRG point-based payment system across its entire jurisdiction; and 74 medical institutions in Wuhan have been identified as the first batch of national DRG payment pilot units.

The advancement of Diagnosis-Related Groups (DRG) also relies on electronic medical records (EMR) as its foundation. When assessing the base payment rate for severe cases and determining disease weights, DRG systems require analytical processing of data from the medical record face sheet. However, if the data on the medical record face sheet is inconsistent with that in the EMR, the fundamental basis for reimbursement will be compromised.

Therefore, electronic medical records (EMRs) have supported the implementation of Diagnosis-Related Groups (DRGs) during their development, while DRGs, in turn, have influenced EMRs by promoting their standardization and quality controllability.

Prior to its formal, large-scale implementation in hospitals in 2020, Diagnosis-Related Groups (DRG) had already played a significant role in hospital performance evaluation and inter-regional competition among hospital specialties. Dr. Chen Bo, Director of the Big Data Center at the First Affiliated Hospital of Chongqing Medical University, told VCBeat, “By comparing the cost consumption index and time consumption index for the same disease across different hospitals, we can identify institutions with anomalous values and promptly pinpoint underlying issues. Furthermore, surgeons, such as those specializing in neurosurgery, often work under high intensity without receiving commensurate compensation. DRG may help rectify the ‘input-output ratio’ imbalance in medical practice.”

On July 25, 2019, the National Health Commission issued the “Notice on Printing and Distributing the Graded Evaluation Standard System for Hospital Smart Services (Trial),” requiring all 31 provinces, municipalities, and autonomous regions across China to complete the data submission for the evaluation within one month. This marked the official government-driven advancement of the “Smart Services” component within the “Smart Hospital” framework.

“The Notice” states: The National Health Commission has decided to carry out the 2019 Hospital Smart Service Grading Assessment in secondary and tertiary hospitals that utilize information systems to provide smart services, and has issued clear requirements for the grading assessment standards and methodologies for smart hospitals. The National Health Commission will conduct the assessment based on two aspects: the functionalities of informatics applications in delivering smart services to patients, and the perceived effectiveness by patients, with a total of six grading levels.

Compared with the many policies mentioned above, feedback from enterprises engaged in smart service construction indicates that the promotion of smart service grading was not significant by the end of 2019. The reasons for this are twofold: first, the grading system did not impose explicit requirements on hospital performance evaluations; second, smart services place certain demands on hospital informatization, requiring hospitals to prioritize the development of internal information systems before embarking on smart service grading.

Therefore, based on the situation in 2019, development in 2020 will continue to focus primarily on electronic medical records (EMR) and interoperability ratings, while widespread adoption of smart hospital ratings will still take some time.

Looking back at 2019, policies served as a lighthouse for the health informatics industry, illuminating the path for hospital development while providing clear direction for healthcare IT enterprises.

However, hospitals have limited capital and resources, making informatization upgrades a gradual process. Determining the sequence of implementation steps requires joint consideration of policy directives and hospital-specific needs. Therefore, while aligning with policies, enterprises must also account for hospitals’ construction progress and financial burden. Only practitioners who thoroughly understand policies and accurately grasp institutional needs can ensure their companies avoid missteps in development.

Overall, the ratings for electronic medical records (EMR) and for interoperability will remain highly prominent in the coming year; the wave of smart hospital construction will continue to gain momentum year after year; data governance under the Diagnosis-Related Groups (DRG) payment system will gradually unlock potential market opportunities; and as massive Machine-Type Communications (mMTC) and ultra-Reliable Low-Latency Communications (uRLLC) mature and standards become more refined, new 5G-enabled healthcare applications will successively emerge starting in 2020.

Thus, in the final phase of public hospital reform, striking a balance between policy and technological advancement, identifying the right pace of development; expanding the customer base and deepening the integration of information technology products; and accelerating project payment collection. These three aspects will present both opportunities and challenges for enterprises in the coming year.