Hygeia Healthcare Files for Hong Kong IPO: A Leading Chinese Oncology Group with 10 Hospitals and Advanced Radiotherapy Capabilities

VCBeat (WeChat ID: vcbeat) has learned that on February 17, Hygeia Healthcare Holdings Co., Ltd. (“Hygeia Healthcare”), a leading oncology healthcare group in China, formally applied for an initial public offering (IPO) on the Main Board of the Hong Kong Stock Exchange, with Morgan Stanley and Haitong International serving as joint sponsors.

According to available information, Hygeia Healthcare is a specialized medical investment group with Sino-American joint venture backing. Centered on oncology, it focuses on the investment, construction, and operational management of chain cancer treatment facilities and neurology medical institutions. Zhu Yiwen serves as the Chairman of the Group, and Ji Hairong is the President.

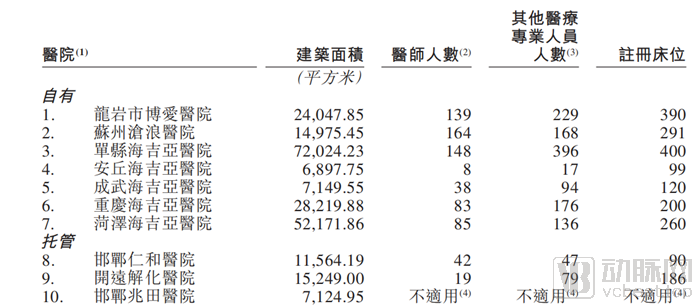

Since its establishment in 2009, Hygeia Healthcare has operated or managed a network of ten oncology-focused hospitals across seven cities in six provinces in China through organic growth, a series of strategic acquisitions, and collaborations with hospital partners, holding direct equity ownership or management rights. In addition, the Company provides services to 14 hospital partners (including its entrusted hospitals) across nine provinces in China for their radiation therapy centers.

Hygeia Healthcare’s Hospital Network Centered on Oncology

According to Frost & Sullivan, Hygeia Healthcare is China’s largest oncology healthcare group in terms of the number of hospitals under its ownership and revenue generated from radiotherapy-related services as of 2018. Furthermore, Hygeia Healthcare ranks first among all oncology healthcare groups in China based on the number of radiotherapy devices installed in its hospitals and radiotherapy centers as of 2018.

After 11 Years in Business and on the Verge of an IPO, How Has Hygeia Healthcare Managed to Stand Out in the High-Barrier Private Oncology Hospital Market?

Development History

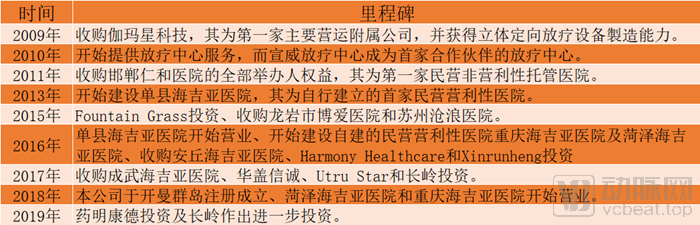

Hygeia Healthcare’s history dates back to 2009, when its founder, Zhu Yiwen, acquired Gamma Star Technology, a manufacturer and intellectual property owner of stereotactic radiotherapy equipment.

Acquisition of GammaStar

According to available information, Gamma Star Technology, established in 2007, is primarily engaged in technological development, technical services, technical consulting, and the transfer of R&D achievements within the field of oncology medical equipment.

Gamma Star Medical’s flagship product, the Gyro Knife—officially named the “Gyroscopic Rotating Cobalt-60 Radiosurgical Treatment System”—adopts a rotation principle similar to that of aerospace gyroscopes. It mounts the Cobalt-60 radiation source on a gyroscopic structure that rotates synchronously along two perpendicular axes, hence the name “Gyro Knife.”

At its inception, Gamma Star Technology secured an $8.73 million Series A financing round from IDG Capital, Lianxun Venture Capital, Qiming Venture Partners, and Shanghai Angel Investment. In October 2016, the company completed its Series B financing with participation from Boyu Capital, Huagai Capital, and others. In 2017, it closed its Series C round, led by investors including BOC Guangdong Financial Holdings and Huagai Capital.

Since 2010, Hygeia Healthcare has collaborated with hospital partners to provide radiotherapy center services, including: (i) providing consulting services for radiotherapy centers; (ii) authorizing the use of patented stereotactic radiotherapy equipment and certain other radiotherapy equipment (as applicable) at the radiotherapy centers; and (iii) providing related maintenance and technical support services for the radiotherapy equipment supplied.

The collaboration has enhanced Hygeia Healthcare’s service capabilities, providing it with in-depth insights into local markets and thereby enabling further expansion of its medical services network.

Building Hospital Networks

A key strategic move involves Hygeia Healthcare establishing its hospital network by founding new hospitals and acquiring existing ones.

Since 2012, three new hospitals have been successfully established, constructed, and put into operation. In 2019, two additional hospitals were founded but construction has not yet commenced. The hospitals are: Shanxian Hygeia Hospital, Chongqing Hygeia Hospital, Heze Hygeia Hospital, Liaocheng Hygeia Hospital, and Dezhou Hygeia Hospital.

Meanwhile, Hygeia Healthcare has also expanded its hospital operations through strategic acquisitions, having acquired four private for-profit hospitals to date: Longyan Bo'ai Hospital, Suzhou Canglang Hospital, Anqiu Hygeia Hospital, and Chengwu Hygeia Hospital.

Therefore, Hygeia Healthcare’s journey from inception can be summarized as follows: by acquiring patented technologies and managing hospital radiotherapy centers, it ultimately established a nationwide hospital network through both self-construction and acquisitions.

Milestones in the Development of Hygeia Healthcare

China's Oncology Medical Services Market

China is a vast and rapidly growing oncology healthcare services market. According to Frost & Sullivan, the number of new cancer cases in China rose from approximately 3.8 million in 2014 to approximately 4.38 million in 2018, and is expected to further increase to approximately 5.0 million in 2024. Tier-3 cities and other lower-tier cities account for the largest proportion of new cancer cases in China.

Oncology is a branch of medicine dedicated to the screening, diagnosis, and treatment of cancer. Currently, methods for cancer screening and diagnosis primarily include imaging examinations, tumor marker testing, endoscopy, pathological examination, and genetic testing. Therapeutic options for cancer mainly encompass surgery, radiation therapy, interventional radiology, chemotherapy, targeted therapy, and immunotherapy.

As demand for oncology medical services continues to rise, the total revenue of China’s oncology medical services market increased from RMB 204.0 billion in 2014 to RMB 332.3 billion in 2018, representing a compound annual growth rate (CAGR) of 13.0%. It is expected to further grow at a CAGR of 11.9% from 2019 to 2024, reaching RMB 658.3 billion in 2024.

The Chinese oncology medical services market is characterized by low rates of early screening and low penetration of radiotherapy, indicating significant growth potential and substantial unmet market demand.

Rapid Growth of Private Cancer Hospitals

From the perspective of service providers, oncology medical institutions include hospitals and other healthcare facilities, such as maternal and child health hospitals capable of treating pediatric and gynecological cancers, with hospitals accounting for the vast majority of revenue from oncology medical services. Hospitals providing oncology medical services, or cancer hospitals, can be primarily categorized into: (i) public and private general hospitals with oncology departments; and (ii) public and private specialized oncology hospitals.

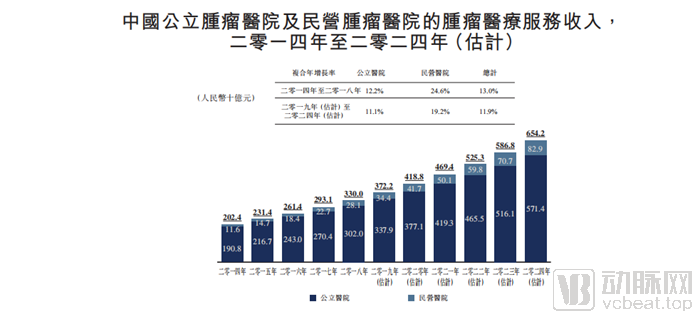

The total revenue from oncology medical services generated by cancer hospitals in China increased from RMB 202.4 billion in 2014 to RMB 330.0 billion in 2018, representing a compound annual growth rate (CAGR) of 13.0%. It is expected to further grow at a CAGR of 11.9% from 2019 to 2024, reaching RMB 654.2 billion in 2024, indicating faster growth compared to the overall hospital market in China.

Public and Private Oncology Hospital Medical Services Market

Specifically, the revenue growth rate from oncology medical services provided by private cancer hospitals in China has exceeded that of public cancer hospitals. The relevant revenue increased from RMB 11.6 billion in 2014 to RMB 28.1 billion in 2018, representing a compound annual growth rate (CAGR) of 24.6%. It is expected to further grow at a CAGR of 19.2% from 2019 to 2024, reaching RMB 82.9 billion in 2024.

# The Radiotherapy Treatment Services Market Has Significant Growth Potential

In terms of treatment modalities, radiotherapy is one of the most common oncology treatment regimens. However, the penetration rate of radiotherapy in China is significantly lower than that in developed countries. In 2015, only 23% of cancer patients in China received radiotherapy, compared with 60% in the United States. Furthermore, in 2018, the number of radiotherapy devices per million population in China was merely 2.5, whereas it was 14.2 in the United States, 11.0 in Switzerland, 9.1 in Australia, and 8.7 in Japan.

Radiotherapy utilizes high-energy radiation to destroy malignant cancer cells or other benign tumor cells. Since the discovery of X-rays in 1895, radiotherapy has rapidly developed worldwide and is now considered applicable to a wide range of cancers, including solid tumors and leukemia. Approximately 70% of cancer patients require radiotherapy at various stages of disease progression, where it may be administered as a standalone treatment or in combination with surgery or chemotherapy.

In particular, radiotherapy is considered a foundational treatment option for various localized tumors, such as nasopharyngeal carcinoma and lymphoma. Radiotherapy is also widely used as adjuvant and neoadjuvant therapy before or after surgery or chemotherapy, and has been proven highly effective in achieving local tumor control, thereby resulting in higher five-year survival rates.

Furthermore, when a cure is unlikely to be achieved, radiotherapy can provide palliative care and alleviate cancer-related symptoms. In addition to malignant tumors, radiotherapy can be used to treat benign tumors as well as certain cerebrovascular, neurological, and psychiatric disorders.

Radiotherapy equipment includes external beam radiotherapy (EBRT) devices and brachytherapy devices. The main EBRT devices used in China include conventional and advanced linear accelerators such as CyberKnife and TomoTherapy, cobalt-60 stereotactic radiotherapy systems such as Gamma Knife, as well as proton and heavy ion radiotherapy systems. The main brachytherapy devices used in China include gamma-ray afterloading units and neutron afterloading units.

The Radiotherapy Treatment Services Market Is Growing at a Faster Pace

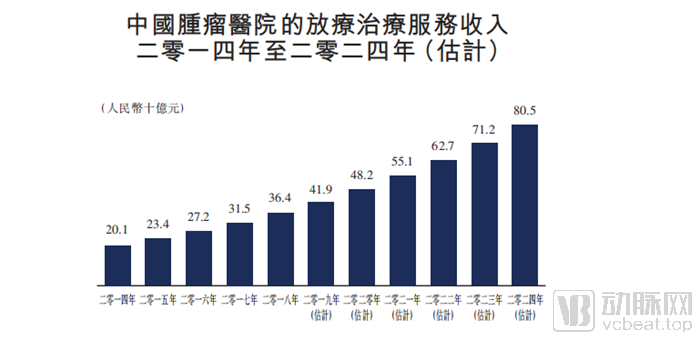

Compared with the overall oncology medical services market, the radiotherapy treatment services market has demonstrated faster growth in terms of revenue generated by oncology hospitals. Revenue from radiotherapy treatment services at oncology hospitals increased from RMB 20.1 billion in 2014 to RMB 36.4 billion in 2018, representing a compound annual growth rate (CAGR) of 15.9%. This figure is expected to further increase from RMB 41.9 billion in 2019 to RMB 80.5 billion in 2024, at a CAGR of 14.0%.

By geographic market, Tier-3 and other cities account for the largest share of China’s oncology hospital market. Revenue generated by oncology hospitals in Tier-3 and other cities increased from RMB 113.6 billion in 2014 to RMB 188.1 billion in 2018, representing a compound annual growth rate (CAGR) of 13.4%. This figure is expected to further rise from RMB 212.8 billion in 2019 to RMB 383.1 billion in 2024, at a CAGR of 12.5%.

Revenue and Expansion Strategy

Specifically, Hygeia Healthcare’s revenue is primarily derived from three sources:

Revenue Sources of Hygeia Healthcare

First, hospital operations: private for-profit hospitals providing a range of oncology medical services and other healthcare services;

Second, third-party radiotherapy services, providing radiotherapy center consulting services to private radiotherapy centers, authorizing the use of patented stereotactic radiotherapy equipment, and offering related maintenance and technical support services for the patented stereotactic radiotherapy equipment;

Third, hospital trusteeship services involve managing and operating private non-profit hospitals in which the sponsor holds equity interests, and collecting management fees therefrom.

Hospital operations as the core business

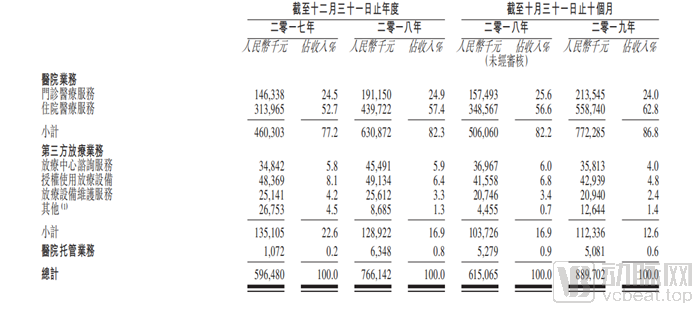

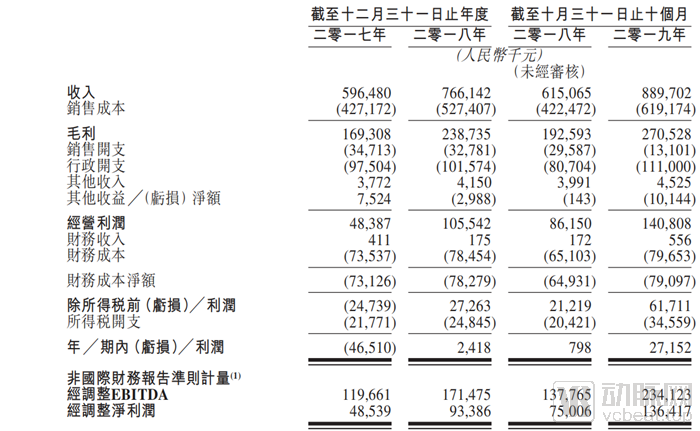

In terms of revenue, it increased by 28.4% from RMB 596.5 million in 2017 to RMB 766.1 million in 2018. In the first ten months of 2019, revenue rose by 44.7% year-on-year from RMB 615.1 million in the same period of 2018 to RMB 889.7 million. The company’s gross profit margins were 28.4%, 31.2%, and 30.4% in 2017, 2018, and the first ten months of 2019, respectively.

Hygeia Healthcare's Annual Revenue

Hospital operations, which account for more than 80% of total revenue, have recorded substantial year-on-year growth for consecutive years and served as the primary driver of revenue expansion. The segment reported a net profit of RMB 2.418 million in 2018, compared with a net loss of RMB 46.51 million in 2017. In the first ten months of 2019, it generated a net profit of RMB 27.152 million, versus only RMB 798,000 in the same period of 2018. Nevertheless, the cost of sales remained excessively high, standing at 71.61%, 68.84%, and 69.59% in 2017, 2018, and the first ten months of 2019, respectively.

Furthermore, Hygeia Healthcare provides services to the radiotherapy centers of 15 hospital partners (including hospitals under its management), with cooperation terms ranging from 3 to 15 years. In addition, it has entered into cooperation agreements with another 23 hospital partners for their radiotherapy centers located in 13 provinces, including Shandong, Anhui, Jiangsu, Jiangxi, Hunan, Ningxia, Hebei, Henan, Tibet, Guizhou, Liaoning, Guangdong, and Sichuan. These radiotherapy centers are expected to commence operations within the next few years.

In terms of patient visits, the total number of outpatient visits at its affiliated hospitals was 691,400, 760,776, 629,763, and 790,683 in 2017, 2018, the first ten months of 2018, and the first ten months of 2019, respectively. During the same periods, the total number of patients receiving radiotherapy treatment using patented stereotactic radiotherapy equipment at partners’ radiotherapy centers was 57,613, 58,056, 47,405, and 49,346, respectively.

As part of Hygeia Healthcare’s development strategy, we have been committed to expanding our network of tumor-centric hospitals and radiotherapy centers, upgrading our existing affiliated hospitals to enhance service capacity and broaden our service offerings, while continuously improving the quality of medical services and further elevating brand awareness, ultimately achieving centralization of key functions and operational rationalization.

During this period, Hygeia Healthcare introduced investors, including Fountain Grass, Harmony Healthcare, Xinrunheng, Changling, WuXi AppTec, Huagai Xincheng, and Utru Star, who became shareholders of the Group. The company’s long-term growth trajectory is expected to continue, driven by rising market demand and Hygeia’s ongoing expansion efforts.

Opportunities and Risks

Looking at the oncology medical services market occupied by Hygeia Healthcare, future growth will continue to be driven primarily by two key factors.

First, population aging and the rising number of cancer patients. The accelerating trend of aging, extended life expectancy, and the increasing prevalence of chronic diseases will further drive demand for healthcare services in China. Specifically, the incidence of cancer in China is rising year by year.

Second, shortage and uneven distribution of medical resources. With the rapid increase in cancer incidence and heightened awareness of cancer treatment, outpatient visits and hospital admissions at oncology medical institutions in China have been on the rise. However, oncology medical resources in China remain in short supply. For instance, bed occupancy rates at oncology medical institutions have long remained at overloaded levels. In 2018, the bed occupancy rate at specialized oncology hospitals in China reached 106.1%, the highest among all types of specialized hospitals.

Meanwhile, the Chinese oncology medical services market is also characterized by limited and unevenly distributed medical resources, which are primarily concentrated in first-tier and second-tier cities. For instance, in 2018, the number of radiotherapy devices per million population was 4.5 in first-tier cities and 3.1 in second-tier cities, compared with 2.2 in third-tier and other cities.

Furthermore, the number of operational beds in hospital oncology departments per million population is 147 in third-tier and other cities, compared with 180 in second-tier cities and 197 in first-tier cities. Rising market demand coupled with supply shortages will attract more social capital investment, thereby stimulating rapid growth in the oncology medical services market.

Although operating in a high-demand sector, Hygeia Healthcare still faces potential risks, such as competition, technological barriers, and physician resources.

Hospitals under Hygeia Healthcare primarily compete with public and private general hospitals as well as specialized hospitals in the same regions. With the rapid growth of China’s healthcare services industry, more domestic or foreign investment may be drawn into the market. Future competition among market participants is expected to intensify, and players with substantial financial, marketing, or other resources may drive large-scale consolidation and mergers and acquisitions.

Furthermore, from a financial perspective, Hygeia Healthcare’s new hospitals typically generate lower revenue and incur higher operating costs during their initial operational phase. Significant expenditures are also incurred prior to the opening of new hospitals, such as renovation costs, rental expenses, and equipment costs. It generally takes several months for new hospitals to achieve monthly break-even, and even longer to recoup the initial investment. Therefore, the number of newly opened hospitals may continue to have a certain impact on profitability.

Hygeia Healthcare’s business relies heavily on the ability of its hospitals to identify, recruit, and retain a sufficient number of qualified physicians, which is critical to service quality, reputation, convenience, medical professionals, medical equipment, and pricing.

Finally, a defining characteristic of the healthcare services industry is its frequent improvements and technological advancements. Given the continuous and rapid technological innovation in this sector, new services and equipment may be introduced from time to time. The success of Hygeia Healthcare depends on the ability of its hospitals to adapt to such technological changes, which will also incur significant expenditures; this adaptability is fundamental to Hygeia Healthcare’s survival.