2019 Global Biopharma Report: Innovation Amid Capital Volatility

Amid the escalating global pandemic, the healthcare and life sciences sector has once again become the focal point of market attention. As a key area of long-term focus and deep expertise, the Huaxing Healthcare team has continued its established practice in this early spring, when warmth is still interspersed with chill. By examining five major segments—biopharmaceuticals, IVD and genetic testing, medical devices, healthcare services, and smart healthcare—as well as the funding landscape, the team strives to provide a comprehensive overview of the development trends in the global healthcare industry over the past year.

Looking back at 2019, the global life sciences and technology sector, led by the United States, continued to thrive. Various transaction models—including private financing, initial public offerings (IPOs), mergers and acquisitions (M&A), and collaborations—flourished, with numerous landmark deals frequently emerging. In terms of clinical progress, targeted therapies shone brightly, outshining immuno-oncology (IO).

In contrast, China’s emerging biopharmaceutical industry has shown markedly divergent performance across primary and secondary capital markets: private equity financing entered a trough after peaking in 2018; initial public offerings (IPOs) on the STAR Market significantly outperformed those in Hong Kong; and merger-and-acquisition deal volume reached a three-year high. Major policy initiatives—including updates to the National Reimbursement Drug List and the implementation of volume-based procurement—along with continuous reforms by the Center for Drug Evaluation (CDE), have steadily narrowed the time lag between new drug approvals in China and abroad, leading to the gradual dissipation of systemic dividends in the biopharmaceutical sector.

Both large traditional pharmaceutical companies and small- to medium-sized biotechnology firms are increasingly recognizing that committing to genuine innovation and competing in the global market has become an imperative for survival and growth, rather than merely one option among many.

The inaugural report focuses on the global biopharmaceutical sector, summarizing capital market performance over the past year and detailing trends in international collaborative transactions and clinical development highlights.

2019 was a year of policy innovation for China’s biopharmaceutical industry. In August 2019, China’s Drug Administration Law underwent its first major revision in 18 years. This revision involved multiple adjustments, such as clarifying the Marketing Authorization Holder (MAH) system; implementing a filing system for clinical trials; ensuring accountability through drug traceability; and replacing the accreditation of clinical trial institutions with a self-declaration and follow-up inspection mechanism.

The Chinese National Reimbursement Drug List (NRDL), which had remained unchanged for eight years, was updated again in 2019. Under this new dynamic, frequent updates to the NRDL are expected to become the norm. For originator drugs whose patents have expired, the national volume-based procurement (VBP) policy—aimed at “making room for new innovations”—has expanded from the initial “4+7” pilot model to a nationwide scale, thereby inflicting a certain blow to pharmaceutical companies that failed to secure places in the centralized procurement lists.

The National Medical Products Administration’s ongoing reforms have sparked a surge in new drug approvals. Historically, the launch of new drugs in China lagged behind overseas markets by 5–10 years; however, statistics on all new drugs approved in China in 2019 show that this gap has narrowed to approximately four years, with some drugs achieving approval within one year or even less. Although market enthusiasm for new drugs has cooled somewhat, it continues to attract substantial capital inflows. We believe that the pharmaceutical and biotechnology sectors will continue to play one of the most critical roles in China’s capital markets.

>>>>

1. Private Financing for China’s Pharmaceutical and Biotech Sectors Cools Down

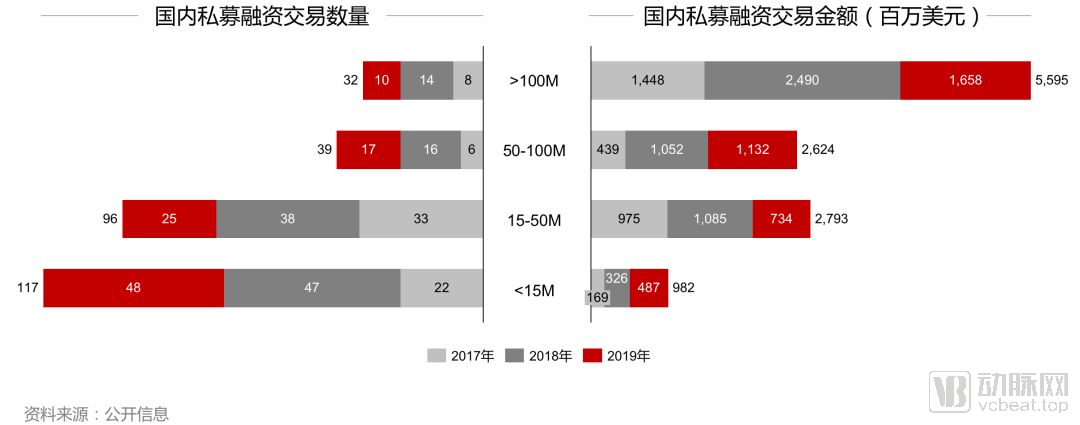

In 2019, based on the disclosed transaction data for private financing in China’s pharmaceutical and biotechnology industry, the total financing amount reached $4 billion, a 20% decrease from 2018; the number of transactions totaled 117, a 20% decline from 2018; and the average transaction size was approximately $34 million, down 13% from the previous year.

The number of projects with single-round financing amounts exceeding $100 million and those ranging between $15 million and $50 million decreased by 29% and 34%, respectively, marking a significant decline. The total financing amounts for these two categories both dropped by 33%. In contrast, the number and value of transactions with single-round financing between $50 million and $100 million remained relatively stable. While the total number of transactions with single-round amounts below $15 million showed little change, the corresponding financing amount increased significantly.

In 2019, early-stage growth companies seeking single-round financing of approximately $30 million faced significantly increased difficulties. Venture capital enthusiasm in the pharmaceutical industry shifted toward earlier stages, driving a counter-trend increase in the total financing amount for deals under $15 million. Meanwhile, market fervor for star projects with financing rounds exceeding $100 million cooled down.

Data indicates that over the past year, investment institutions in the pharmaceutical industry have adopted a more conservative stance, with a noticeable decline in the amount per transaction and a clear trend toward earlier-stage investments. Although the decrease in large-scale financing reflects a cooling of market enthusiasm, financing for companies in the mid-to-late growth stages has continued to grow steadily. It is projected that numerous exit opportunities will emerge over the next two years, driving the entire industry into a virtuous cycle.

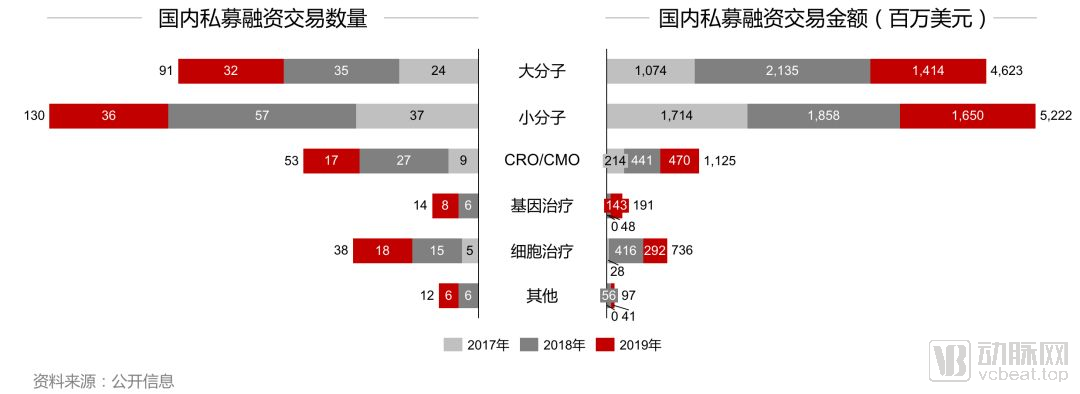

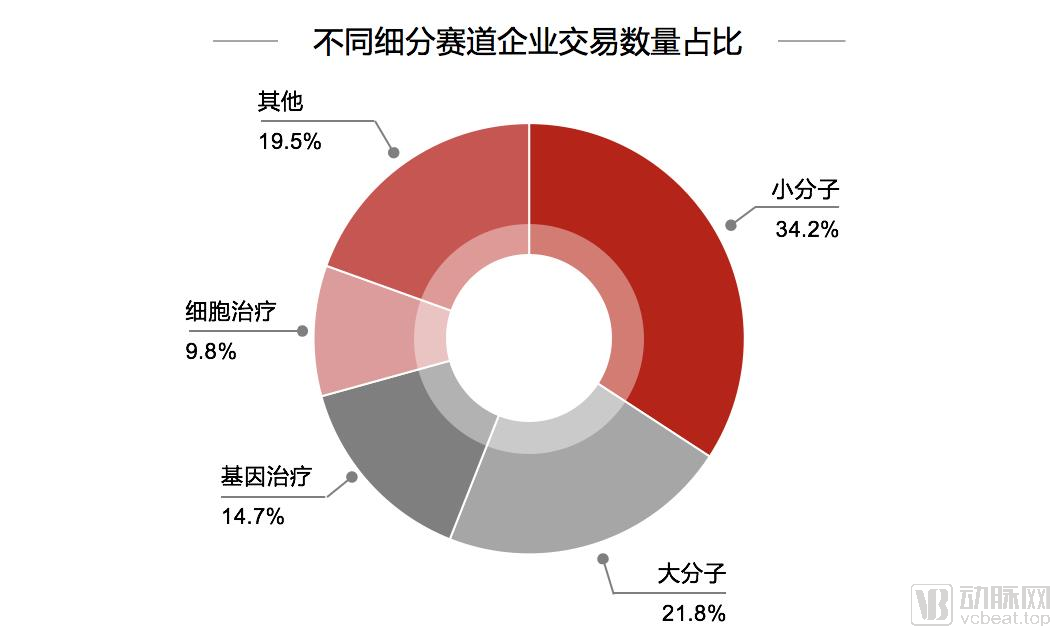

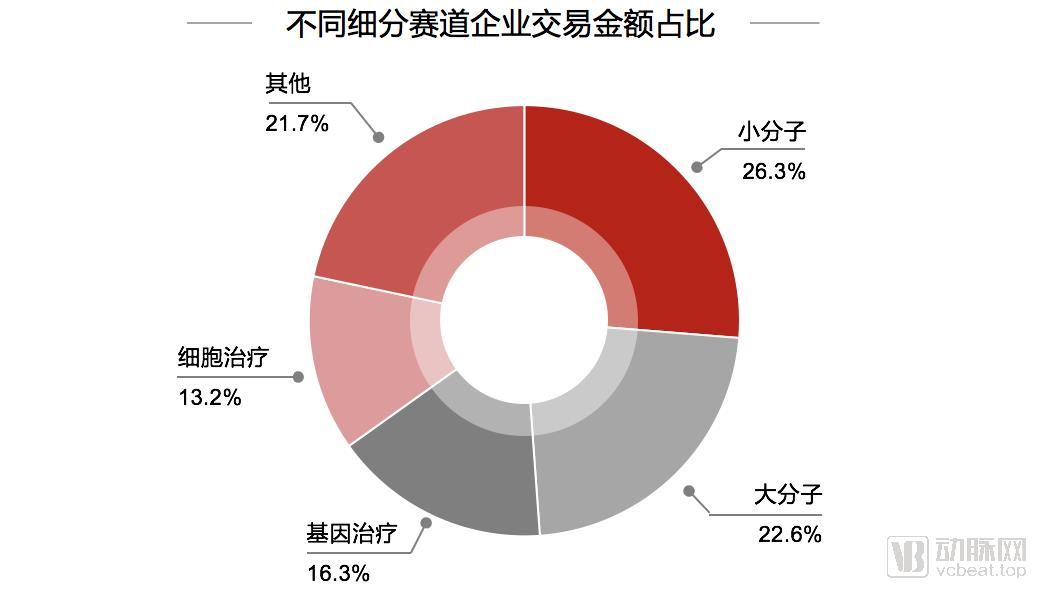

From the perspective of capital market performance in niche sectors, large molecules and small molecules remain the two most active fields; however, both the number of financing deals and the total amount raised have declined significantly compared with 2018.

The number of CRO/CMO transactions decreased from 27 in 2018 to 17 in 2019, while the total financing amount increased from $440 million in 2018 to $470 million in 2019, representing a 70% rise in the average financing amount per transaction.

The number of transactions in the cell therapy sector remained relatively stable in 2019, while the average amount raised per financing round decreased compared to 2018. With the successful market launch of overseas gene therapy products, the gene therapy sector has emerged as a significant force. Although the number of transactions increased by only two compared to 2018, the total industry financing for the year was nearly three times that of 2018.

We believe that early-stage companies capable of demonstrating preliminary clinical data and efficient execution will be highly attractive to investors. Meanwhile, growth-stage and late-stage companies that effectively address clinical pain points and possess strong global innovativeness will increasingly gain market favor in the future.

2. Overseas private financing in biotechnology approaches the fervor of 2018, with multiple mega-funding deals emerging

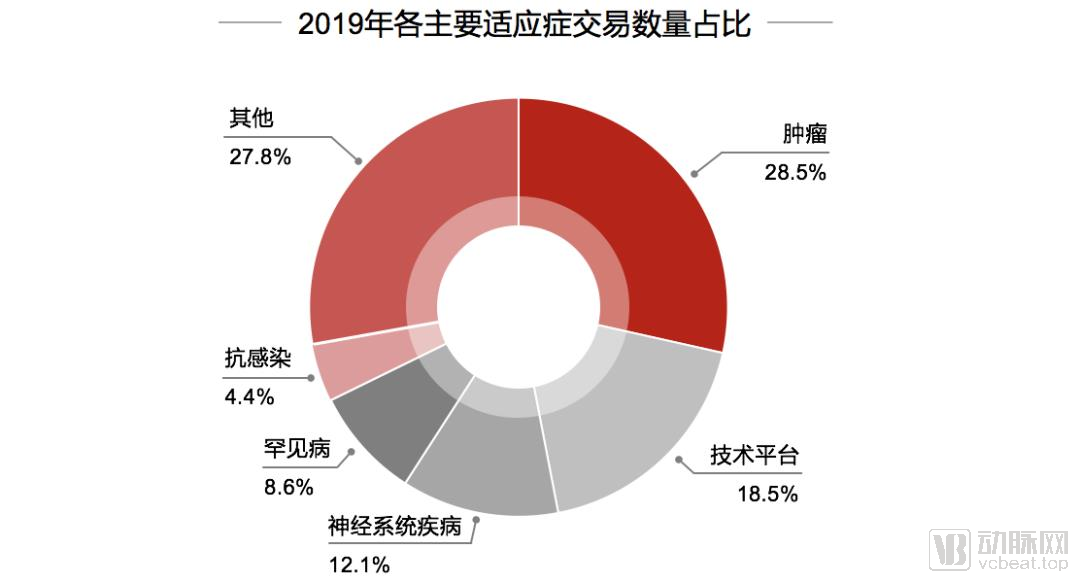

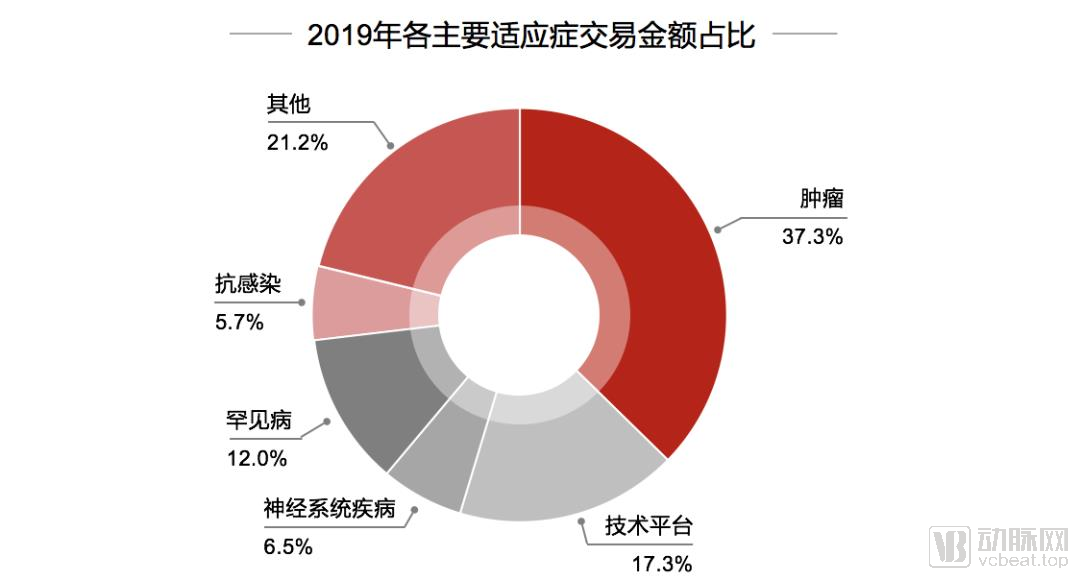

In 2019, the total value of private equity financing transactions in the overseas pharmaceutical and biotechnology sectors amounted to $13.8 billion, representing a slight decline from the previous year. From the perspective of therapeutic indications, oncology remained the hottest field, accounting for one-third of both the number of transactions and the total transaction value. Technology platform companies followed closely, representing 17%-18% of both the number of transactions and the total value. Rare diseases and neurological disorders each accounted for approximately 10%. Anti-infectives and other various indications together comprised 30% of both the number of transactions and the total transaction value.

In 2019, the overseas private equity market saw six “fundraising giants” with individual financing rounds exceeding $200 million:

ADC Therapeutics, headquartered in Lausanne, Switzerland, specializes in the development of highly potent targeted antibody-drug conjugates (ADCs). In July 2019, the company completed a $103 million Series E financing round, bringing the total amount raised in this series to $303 million.

Nuvation Bio, dedicated to the development of oncology drugs, was founded by David Hung, the former President and CEO of Medivation and a serially successful entrepreneur. The company attracted significant investor enthusiasm upon its inception, raising $275 million.

Anthos Therapeutics was co-founded by Blackstone Life Sciences, with a $250 million investment, and Novartis, focusing on advancing next-generation targeted therapies for patients at high risk of cardiovascular disease.

Century Therapeutics, built on induced pluripotent stem cell (iPSC) technology, provides a substantial pipeline of allogeneic, off-the-shelf therapeutic products and successfully raised $250 million in financing in 2019.

BridgeBio focuses on novel, clinical-stage targeted gene therapies and was co-led by KKR and Viking Global Investors in a nearly $300 million investment round.

BioNTech is Europe’s largest private biotechnology company, focusing on the mRNA therapeutics sector. It secured a total of $695 million across two financing rounds in 2018, followed by a $325 million Series B round in 2019, and subsequently listed on the Nasdaq, becoming the third-largest biotechnology company publicly traded in the United States.

From the perspective of specific sub-sectors, small-molecule drugs lead the pack, accounting for approximately 34%; large-molecule drugs follow closely with a 22% share; cell therapy and gene therapy account for 10% and 15%, respectively. In 2019, these two fields saw 15 financing deals each exceeding $100 million.

Against the backdrop of a slight decline in the overall overseas private equity financing market, the total amount raised in Series A rounds fell by 31%, while the number of Series B deals exceeding $100 million increased significantly. This indicates that traditional venture capital firms have slowed their pace of investment in early-stage projects, opting instead to support Series B companies and those approaching an initial public offering (IPO). The number of transactions involving platform-type companies remained unchanged compared with 2018, but the total financing amount dropped markedly, with the median deal size decreasing from $47 million in 2018 to $16 million in 2019.

It is worth noting that trends in the overseas capital markets for the pharmaceutical and biotechnology sectors are exactly the opposite of those in China. While the total financing amount for early-stage projects has decreased, the number of large-scale financing deals has increased, reflecting strong investment enthusiasm from overseas investors. The IPO market is expected to remain robust over the next one to two years, with valuations also set to rise.

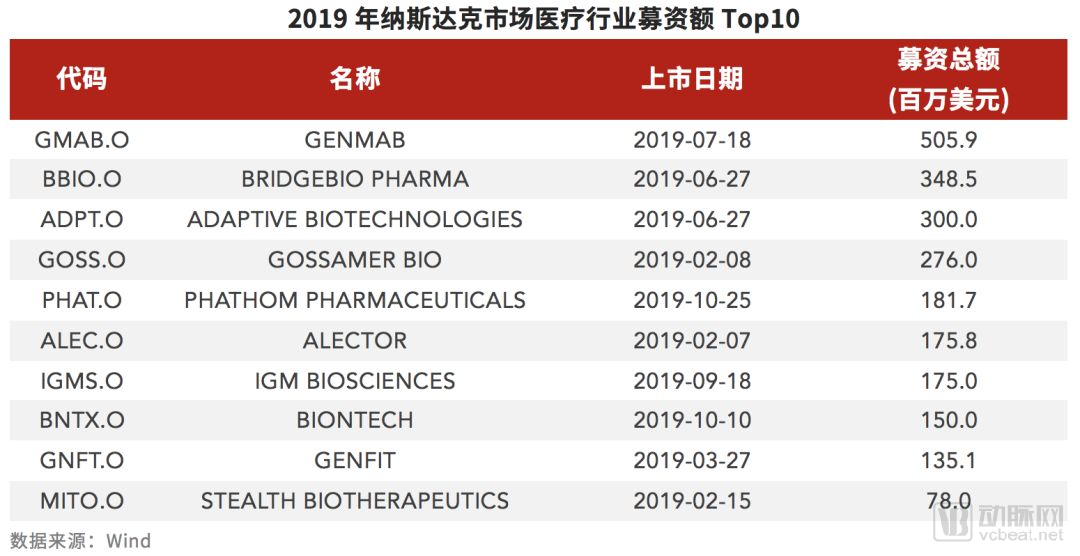

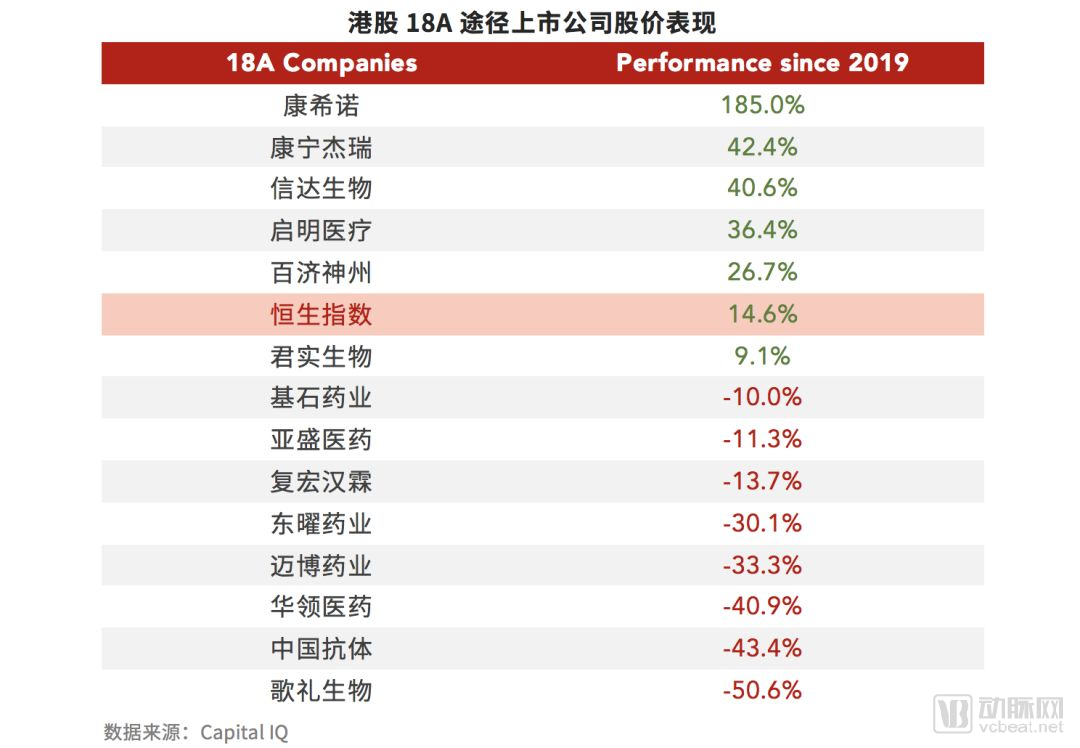

In 2019, pharmaceutical companies from mainland China, Hong Kong, and the United States exhibited varied performance in their initial public offerings (IPOs). Hansoh Pharma led globally with $1.1 billion raised. However, the total capital raised by the top ten pharmaceutical companies listed in Hong Kong exceeded that of the top ten in the U.S. by $1.5 billion, demonstrating the strong fundraising capability of China’s secondary market. Post-listing performance also diverged significantly among companies listed via the STAR Market, the conventional Hong Kong listing route, and Chapter 18A of the Hong Kong Stock Exchange: companies listed on the STAR Market have seen an average price increase of nearly 200%, with a median gain of 165%; those listed through the conventional Hong Kong route, except for Viva, outperformed the Hang Seng Index; while most companies listed under Chapter 18A, with the exception of CanSino Biologics and Y-Biologics, saw their share prices fall below the IPO price. This indicates that investors in Hong Kong’s secondary market favor companies with products nearing commercialization, robust pipelines, and therapies targeting high-potential treatment areas.

According to disclosed transaction data, both the number and value of M&A transactions in China reached their highest levels since 2017. The total M&A transaction value for the year was approximately $4 billion, more than four times that of 2018, while the number of M&A transactions totaled 20, representing a 25% increase from 2018.

Bristol Myers Squibb’s (BMS) acquisition of Celgene, Takeda’s completion of its acquisition of Shire, and AbbVie’s announced acquisition of Allergan have emerged as the three most high-profile mega-mergers this year.

BMS overcame significant obstacles to finally acquire Celgene, gaining access to its drug development pipeline covering hematologic diseases, solid tumors, and inflammation and immunology. Leveraging Shire’s leading position in rare diseases and plasma-derived therapies, Takeda was able to strengthen its core franchises in oncology, gastroenterology, and neuroscience following the merger, while also expanding its overall scale. Allergan’s medical aesthetics products, Botox and Juvederm, are both blockbuster products in the global medical field; post-merger, its business will span immunology, hemato-oncology, medical aesthetics, neuroscience, women’s health, eye care, and virology. The consolidation of these pharmaceutical giants will significantly reshape the global pharmaceutical landscape. For instance, the combination of AbbVie and Allergan propelled the new entity’s revenue past that of Novartis and Merck & Co., ranking it among the top five globally. Against the backdrop of declining returns on investment (ROI) from internal R&D, the wave of mergers and acquisitions among large pharmaceutical companies is set to intensify.

From a therapeutic perspective, gene therapy has emerged as one of the hottest sectors for mergers and acquisitions among biotechnology companies this year. Novartis’s Zolgensma, approved for the treatment of spinal muscular atrophy (SMA) in children under two years of age, has successfully reached the market, offering patients unprecedented survival rates. Within one month after administration, patients experience rapid improvements in motor function, and gains in unsupported motor ability can be sustained long-term. This milestone breakthrough has also made Zolgensma the most expensive drug in history, with a one-time treatment cost of $2.1 million. The approval and launch of Zolgensma served as a catalyst that ignited the market, prompting Roche, Novartis, Biogen, and Astellas to make successive moves in this field.

Meanwhile, oncology and immunotherapy remain highly active. In the oncology space, Pfizer has focused its attention on kinase inhibitors. In June 2019, Pfizer acquired Array BioPharma at a 62% premium, primarily valuing two key products: Braftovi (encorafenib) and Mektovi (binimetinib), which are used in combination as an oral therapy for malignant melanoma.

Eli Lilly’s $8 billion acquisition, announced in early 2019, brought Loxo Oncology’s tumor-agnostic pipeline into sharper focus. Subsequently, Bayer elected to exercise its rights under a prior agreement, securing global development rights to two of Loxo Oncology’s tumor-agnostic anticancer agents.

Amid repeated skepticism from Wall Street over its acquisition strategy, GSK successfully acquired TESARO. The subsequently released promising clinical data for TESARO’s flagship product, a PARP inhibitor, significantly alleviated external doubts. Meanwhile, Zai Lab, TESARO’s partner in China, successfully secured regulatory approval for olaparib in the Chinese market.

In April 2019, Novartis acquired the NLRP3 antagonist developed by IFM Therapeutics, a star company in the field of immunotherapy, for a total value of nearly $1.6 billion. STING and NLRP3 are both key components of innate immunity. Following numerous breakthroughs in adaptive immunity, increasing attention is now being directed toward innate immunity. In addition to their relevance to immunotherapy, both NLRP3 and STING have human gain-of-function variants; individuals carrying these variants exhibit hyperactive immune responses, which enhances the predictability of clinical outcomes for related drug candidates.

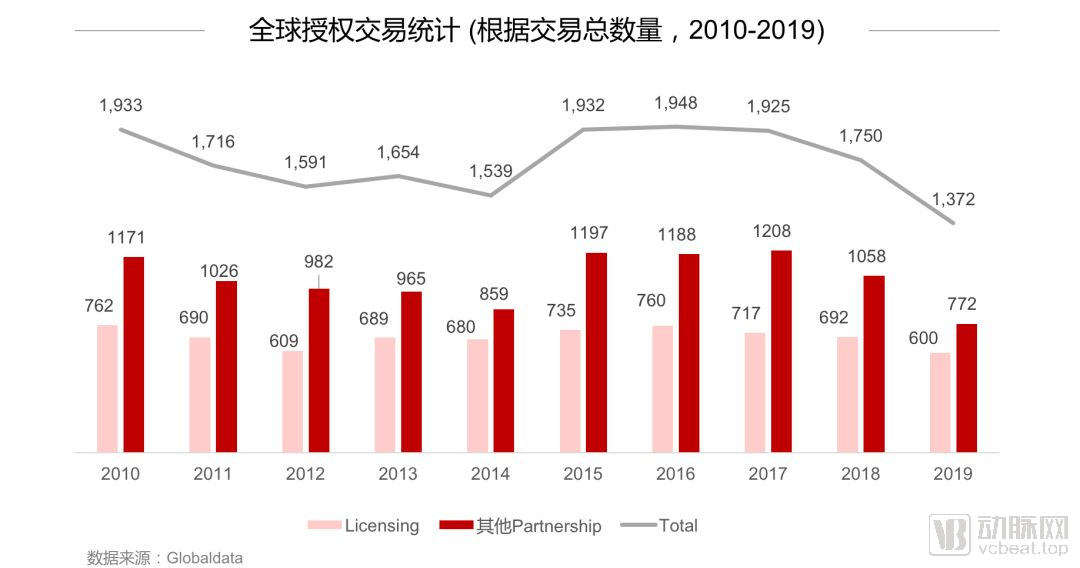

1. Global Collaboration Transaction Value Hits Record High

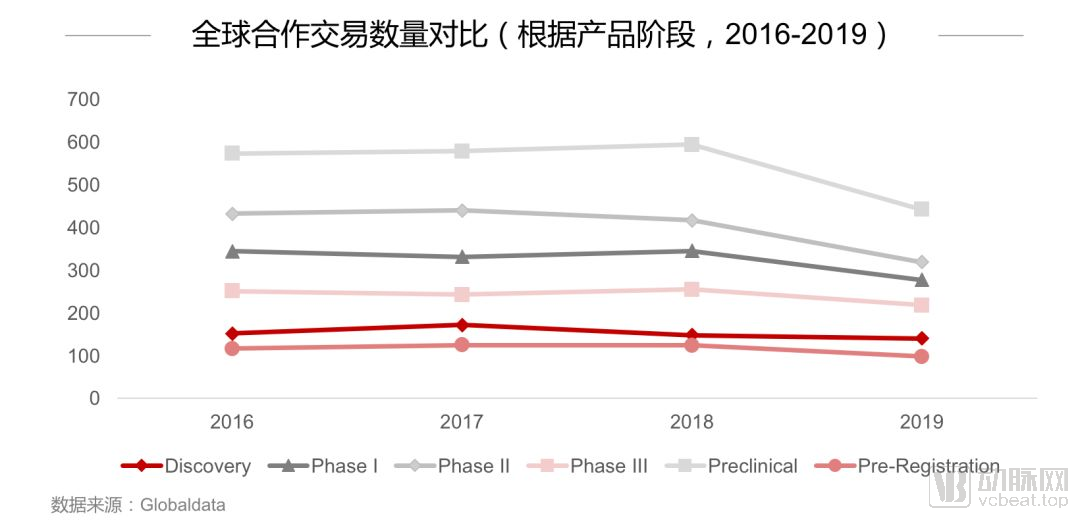

Looking back at 2019, the total number of global collaborative transactions declined significantly compared with previous years, yet the total transaction value reached a new high since 2017, amounting to $115.7 billion. Collaborative deals such as co-development, co-marketing, and joint ventures followed the same overall trend; however, licensing transactions experienced a decline in both volume and value in 2019, with marked decreases in both the number of deals and the total transaction amount.

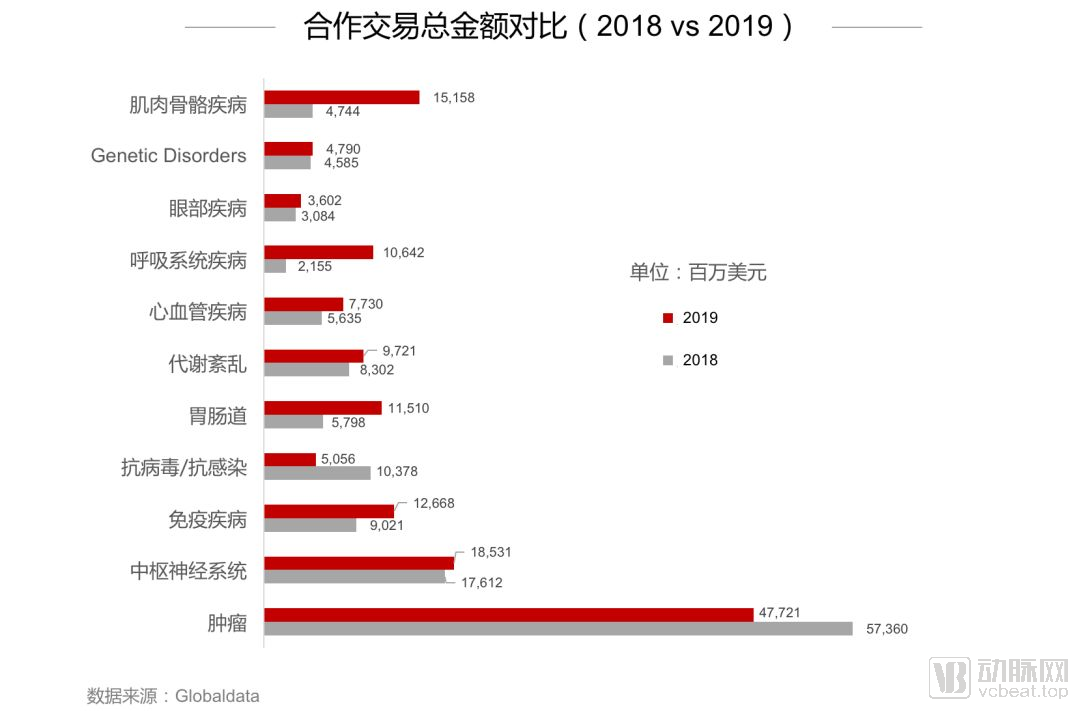

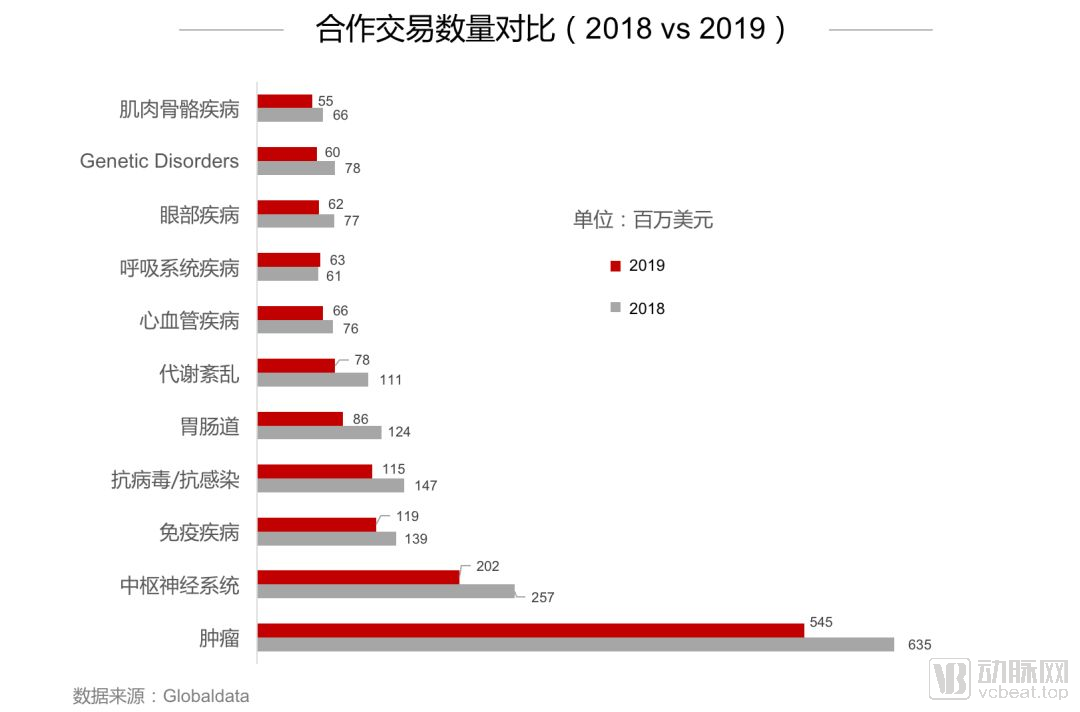

In terms of therapeutic area rankings, oncology and central nervous system (CNS) disorders firmly held the top two positions in both total transaction value and volume. However, it is noteworthy that both the total transaction value and number of deals in oncology declined significantly in 2019 compared to 2018. In recent years, the surge of interest in cancer immunotherapy led to a high frequency of transactions; however, as numerous pharmaceutical companies entered the field, an increasing number of cancer types have become saturated markets (“red oceans”) with intense competition. Consequently, some pharmaceutical companies began shifting their focus in 2019 toward indications with relatively less competition but substantial market potential, such as gastrointestinal diseases (e.g., NASH, IBD), respiratory diseases (e.g., pulmonary fibrosis, asthma), and musculoskeletal disorders (e.g., osteoporosis).

We have observed that there were few breakthroughs in the global antiviral and anti-infective fields over the past year, leading to a significant decline in transaction enthusiasm. With the outbreak of the COVID-19 pandemic, people have once again realized that many viral infectious diseases, particularly respiratory viral infections, remain untreatable or cannot be completely eradicated. The unmet clinical needs are substantial, and we believe that new-mechanism drugs will continue to attract attention in the future.

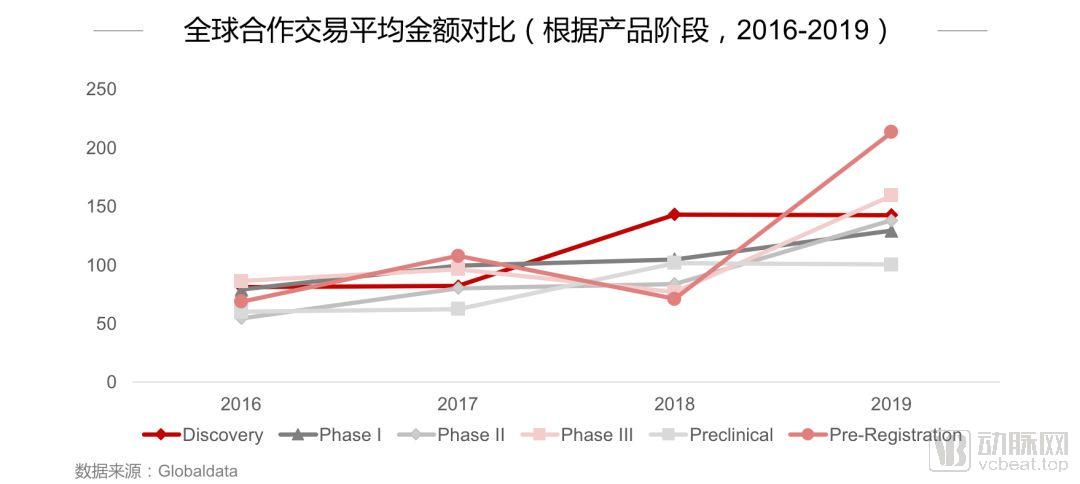

From a product stage perspective, in 2019, except for a slight increase in the number of products in the Drug Discovery phase, the number of products in all other stages declined to varying degrees. The Pre-clinical stage saw the largest proportional decline, yet its absolute number remained the highest. In terms of average transaction value, deals involving late-stage products (Phase II to Pre-registration) showed an upward trend, with Pre-registration products experiencing the most significant increase. This reflects that, against the backdrop of an economic downturn and rising drug development failure rates, the market places greater value on late-stage products with a higher likelihood of successful commercialization.

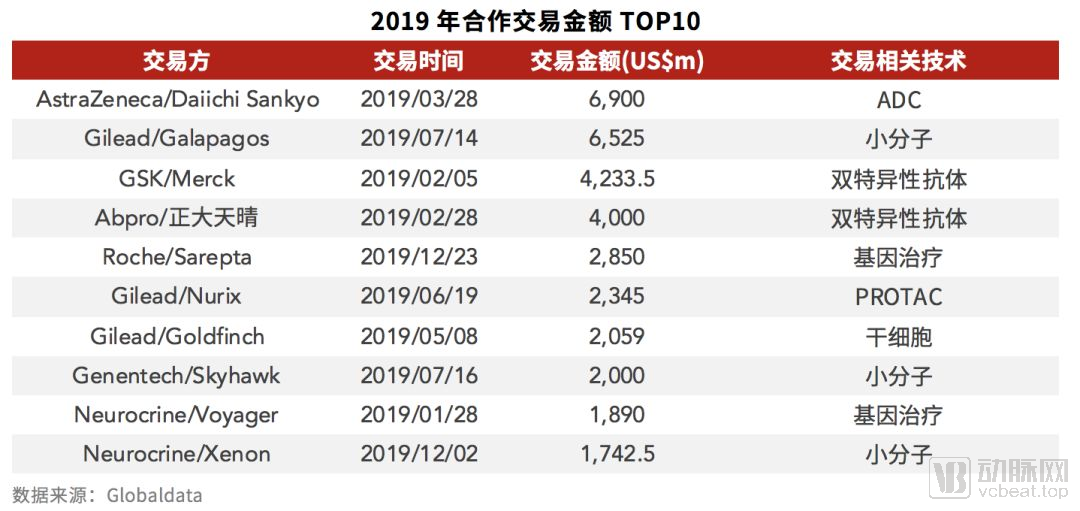

In terms of total transaction value, major pharmaceutical companies continue to increase their investments in new technologies. Among the top ten deals, gene therapy and bispecific antibodies each accounted for two spots, while antibody-drug conjugates (ADCs), stem cells, and PROTACs each claimed one spot. It is foreseeable that more drug-like molecular entities will emerge in the field of disease treatment in the future.

>>>>

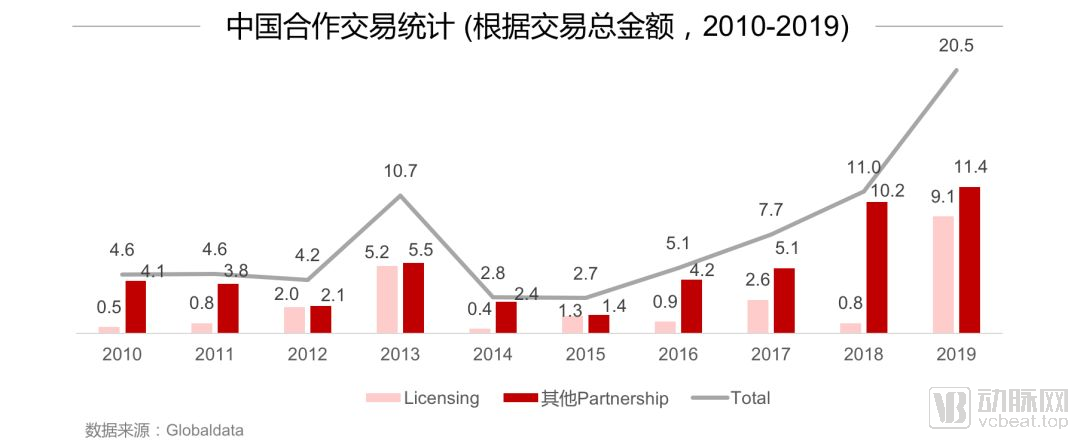

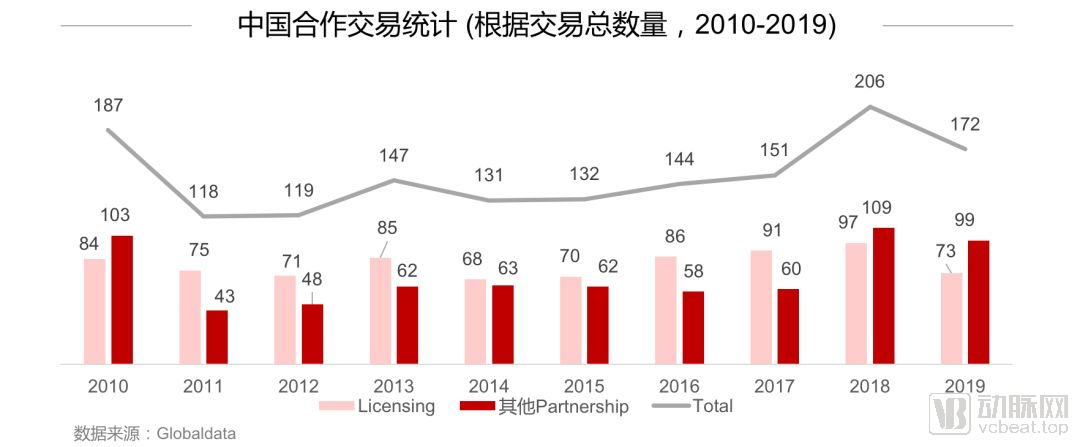

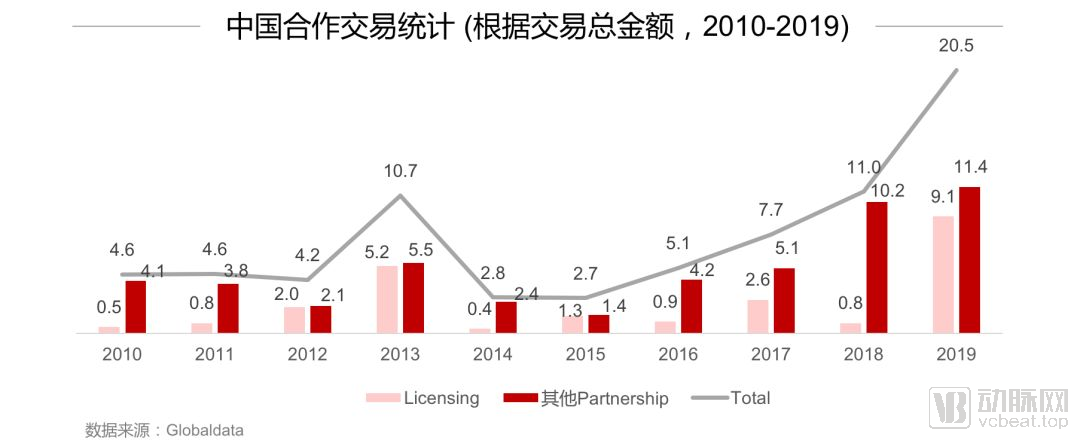

2. Significant Increase in Transaction Value of China Collaborations

The growth in the total value of collaborative transactions in China was primarily driven by licensing deals, reflecting the increasing demand to divest long-tail assets as China’s biopharmaceutical industry advances and international pharmaceutical companies undergo strategic transformations. Meanwhile, a growing number of Chinese companies are seeking to leverage external innovations to address domestic gaps. This enthusiasm for product in-licensing has also pushed up the valuation of licensing deals involving Chinese biopharmaceutical firms. The largest licensing deal in 2019 was a collaboration between Cytovant—a company co-founded by LunSheng Bio and Roivant Sciences—and Medigene for the development of innovative cell therapies in Asia, with a total transaction value of $1 billion. In terms of upfront payments, the licensing agreement between Everest Medicines and Immunomedics for the antibody-drug conjugate (ADC) sacituzumab govitecan ranked first, with an impressive upfront payment of $125 million.

As licensing deal prices continue to rise, it is becoming increasingly challenging for Chinese pharmaceutical companies to seek out high-quality, cost-effective overseas assets, particularly those offering only China-specific rights. With the government imposing stricter controls on drug prices, whether future returns in the Chinese market can cover the substantial costs of in-licensing has become a critical question for every CEO of a biopharmaceutical company operating under the license-in model, making astute judgment in product selection more important than ever.

Beyond in-licensing, as their R&D capabilities have improved, an increasing number of Chinese companies are expanding globally by licensing out their own products. This strategy not only generates substantial economic returns but also serves to validate their internal R&D strength. In 2019’s outbound licensing (License-out) deals from China, HitGen led the pack, securing multiple product licensing agreements with Mitsubishi Tanabe Pharma, Leo Pharma, and Nippon Shinyaku. License-out transactions have gradually become a critical benchmark for assessing a company’s core R&D capabilities. In particular, striking License-out deals with international pharmaceutical companies can attract greater attention from capital markets, providing significant leverage for corporate financing. Among collaborative deals conducted in China, Chia Tai Tianqing ranked first after reaching a $4 billion immuno-oncology co-development agreement with Abpro Therapeutics. The two parties will leverage Abpro’s proprietary antibody discovery platform, DiversImmune, to develop multiple innovative bispecific antibody therapies. This deal ranks among the top five globally.

As proprietary products face impending patent cliffs, the “4+7” volume-based procurement program continues to deepen, and the core generic drug business confronts severe challenges, Chinese domestic pharmaceutical companies have clearly demonstrated their resolve to pivot toward the forefront of innovation, particularly in the currently hot field of cancer immunotherapy. However, due to limited prior R&D accumulation, licensing-in products or engaging in collaborative development to fast-track new drug R&D has become the preferred strategy for major domestic pharmaceutical firms. In addition, among the top 10 deals, Hansoh Pharmaceutical (with two transactions), Simcere Pharmaceutical, and Guangzhou Xiangxue all secured spots. It is believed that we will see more domestic pharmaceutical companies actively joining the ranks of innovative drug development by licensing in innovative pipelines through collaborative transactions; China’s collaboration and licensing market in 2020 will remain vibrant.

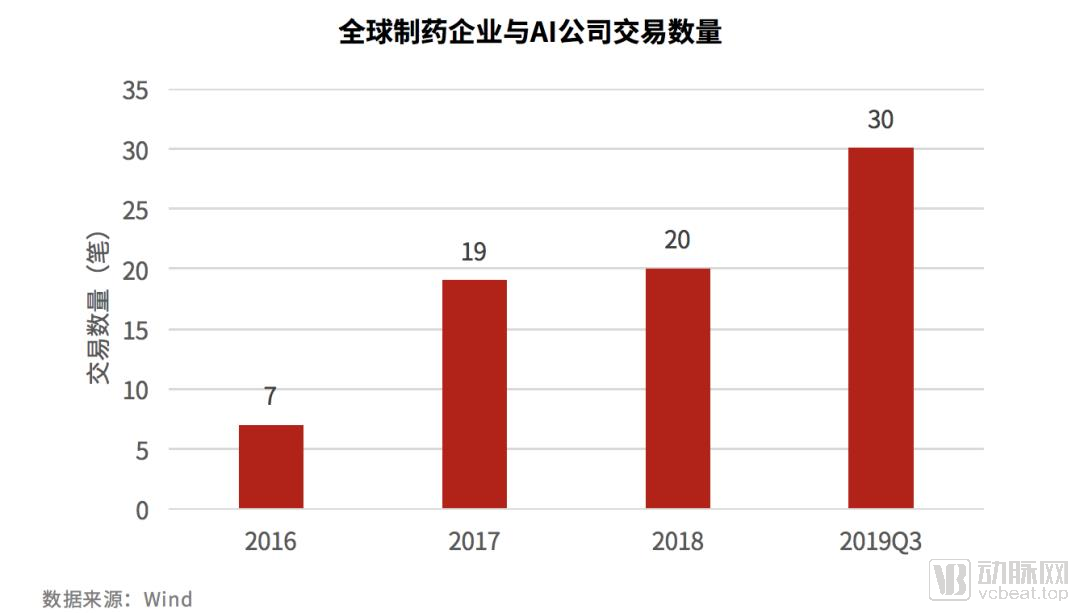

Notably, two of the top ten deals were related to AI-driven drug discovery: a $1.5 billion transaction between Hansoh Pharmaceutical and Atomwise, and a $200 million collaboration between Jiangsu Chia Tai Fenghai Pharmaceutical and Insilico Medicine. In 2019, the integration of AI technology with new drug development became increasingly tight, with major international pharmaceutical companies actively entering the field. By the end of the third quarter of 2019, the number of transactions had already far exceeded the total for the entire year of 2018. As data accumulates and algorithms are validated in actual R&D processes, AI is expected to address key pain points in current new drug development, including high costs, long timelines, and high failure rates. Its role will become increasingly important in the future, and collaborations between Chinese pharmaceutical companies and AI firms will enter a new era.

1. Targeted Therapy Shines Brightly

In 2019, small-molecule drugs returned to the spotlight, overshadowing the once-dominant large-molecule cancer immunotherapies. Multiple targets, including pan-cancer therapies, PARP, and BTK, as well as previously considered “undruggable” targets such as KRAS, garnered widespread attention in 2019.

1) Pan-cancer therapy

Major Developments in Pan-Cancer Therapies in 2019: In January, just two months after Loxo’s pan-cancer novel drug Vitrakvi—a first-in-class innovative therapy targeting NTRK gene fusions—received FDA approval in the United States, Loxo was acquired by Eli Lilly at a 68% market premium. Roche’s Rozlytrek (entrectinib) was approved sequentially in Japan and the United States in June and August, respectively, providing a new treatment option for patients with NTRK fusion-positive non-small cell lung cancer (NSCLC). During the same period, Roche was collaborating with its subsidiary Foundation Medicine to develop personalized medicines and advanced diagnostic technologies, aiming to utilize this companion diagnostic, currently under regulatory review, to help identify patients with various NTRK gene fusions. As more pan-cancer therapies become available in the future, treatment paradigms are expected to gradually shift from a one-size-fits-all approach to precise, individualized therapies with more accurate targeting and higher efficacy.

2) BTK

BTK was another hot target in 2019. Ibrutinib, the first BTK inhibitor to reach the market and developed by Johnson & Johnson, generated sales exceeding $2.536 billion in the first three quarters of 2019. Meanwhile, later entrants such as BeiGene’s zanubrutinib and InnoCare Pharma’s orelabrutinib are also eyeing this lucrative market. Zanubrutinib became the first domestically developed anti-cancer drug from China to receive FDA approval. Although it failed to demonstrate statistically significant superiority over ibrutinib in the primary endpoint of a head-to-head trial, its commercial prospects remain promising. InnoCare Pharma’s orelabrutinib has had its new drug application accepted by the NMPA for the treatment of relapsed/refractory chronic lymphocytic leukemia (CLL)/small lymphocytic lymphoma (SLL).

It is evident that multiple BTK inhibitors, both domestic and international, have entered or are approaching commercialization, indicating that competition for this target will inevitably intensify. Notably, during the 2018 negotiations for inclusion in China’s National Reimbursement Drug List (NRDL), ibrutinib secured its place on the oncology reimbursement list with an 80% price reduction, posing a significant challenge to the subsequent commercialization of its competitors in China.

3) PARP

PARP inhibitors also shone brightly in 2019, with olaparib and niraparib standing out as the most prominent agents.

The Phase III clinical trial results of olaparib for the treatment of pancreatic cancer, presented at ASCO, were impressive. In the same year, AstraZeneca and Merck jointly announced the Phase III clinical trial results of PAOLA-1 and PROfound for olaparib at ESMO. The release of these two sets of results not only further solidifies olaparib's leadership in maintenance therapy for ovarian cancer but also expands its reach into the field of prostate cancer treatment. Olaparib has become the only PARP inhibitor to date with research achievements across ovarian cancer, breast cancer, pancreatic cancer, and prostate cancer, making it the most extensively and deeply studied drug in this class. Additionally, olaparib is the first PARP inhibitor approved for marketing in China.

Niraparib has been approved in the United States for the treatment of ovarian cancer and fallopian tube cancer. The rights for the Greater China region are held by Zai Lab, which has obtained approvals in Hong Kong, Macau, and mainland China over the past 18 months for the treatment of ovarian cancer (with additional approval for fallopian tube cancer in Hong Kong). Currently, niraparib is the PARP inhibitor with the highest market share in Hong Kong.

As the first PARP inhibitor approved in China for first-line maintenance treatment of ovarian cancer, olaparib was successfully included in the National Reimbursement Drug List through price negotiations, significantly reducing the medication burden for patients with ovarian cancer. Although niraparib’s approval has not displaced olaparib’s leading position in the first-line setting, it provides domestic patients with additional therapeutic options. Competition in China’s PARP inhibitor market is expected to intensify, posing significant challenges to other PARP inhibitors still in the development pipeline.

4) KRAS

Over the past year, small-molecule drug development has achieved multiple breakthroughs, with several candidates demonstrating favorable clinical outcomes against targets previously considered undruggable. Among these challenging targets, KRAS is regarded as the “Mount Everest” of small-molecule targets, and Amgen’s AMG510 is undoubtedly the most noteworthy candidate. Its impressive Phase I clinical data are encouraging: at a dose of 960 mg, 54% of patients with non-small cell lung cancer (NSCLC) exhibited a therapeutic response, the disease control rate was 100%, and no significant adverse reactions were observed.

In addition to KRAS monotherapy, combinations with other small-molecule drugs also warrant attention. Several companies have initiated combination therapies involving KRAS and SHP2 inhibitors, or KRAS inhibitors combined with other agents targeting the ERK signaling pathway, and multiple partnerships have been established in this field. For instance, Boehringer Ingelheim and Lupin entered into a product licensing deal valued at $720 million, and Novartis reached a product collaboration agreement with Mirati. Meanwhile, Novartis has formed a long-term strategic partnership with Sixth Element Capital (6EC) and the Cancer Research UK Beatson Institute to jointly develop novel KRAS inhibitors for the treatment of refractory cancers.

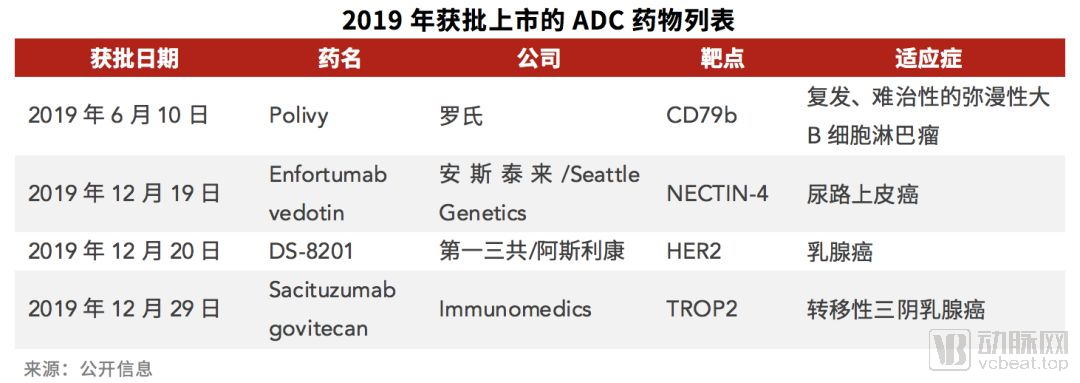

5) Global ADC Market Reignites Competition

In 2019, the ADC field experienced a surge of momentum, achieving breakthroughs across private equity financing, collaborative deals, and clinical progress, thereby dispelling the gloom that had persisted for years.

In March, Daiichi Sankyo announced a global development and commercialization agreement with AstraZeneca for its investigational HER2-ADC novel drug, DS-8201. Under the terms of the agreement, AstraZeneca will pay Daiichi Sankyo an upfront payment of $1.35 billion, along with milestone payments of up to $5.55 billion, bringing the total potential transaction value to $6.9 billion. For AstraZeneca, which has been cautious in its acquisition strategy, this deal ranks as its second-largest transaction, following the $13.7 billion acquisition of MedImmune. The global pivotal Phase II results for DS-8201 were encouraging, demonstrating an objective response rate (ORR) of 61% and a progression-free survival (PFS) of 16.4 months in patients who had failed an average of six prior therapies. Notably, the Biologics License Application (BLA) received rapid FDA approval just two months after submission. In addition to its approved indication as a third-line treatment for HER2-positive breast cancer in patients who have progressed on T-DM1, DS-8201 has also demonstrated efficacy in HER2-low expression populations, significantly expanding the beneficiary population beyond the current definition of HER2 positivity. Daiichi Sankyo is currently conducting trials for DS-8201 across multiple indications, including first-line treatment for HER2-low breast cancer, gastric cancer, non-small cell lung cancer, and colorectal cancer. DS-8201 represents one of the most strategic moves positioning AstraZeneca to join the top tier in the oncology field.

Within a single year, four drugs received approval, reigniting competition in the antibody-drug conjugate (ADC) space and drawing participation from multiple international giants. Currently, Roche, Pfizer, and Seattle Genetics occupy the first tier with approved products, while AstraZeneca has become a key player in the ADC market through its acquisition of DS-8201. Numerous biotechnology companies follow closely behind. There are currently over 80 ADC candidates in clinical development, with 20 having entered Phase II/III trials. Three ADCs have submitted Biologics License Applications (BLAs), and five have advanced into Phase III clinical trials. Ambrx, with operations in both China and the United States, has been deeply engaged in the ADC field for many years. Recently, the HER2-ADC developed in collaboration between Ambrx and Zhejiang Medicine has demonstrated a favorable dose-response relationship and an excellent safety profile. Competition in drug development is inseparable from capital support. As mentioned earlier, ADC Therapeutics completed its Series E financing expansion in July, raising a total of $303 million. This funding will support clinical trials of five ADC candidates for both hematologic malignancies and solid tumors.

2. Tumor immune competition remains intense

1) The Era of Tumor Immunotherapy in China Officially Begins

On December 31, 2019, tislelizumab, an anti-PD-1 antibody independently developed by BeiGene, was officially approved by the National Medical Products Administration (NMPA), marking it as the fourth domestically developed PD-1/PD-L1 inhibitor in China. Among the six PD-1/PD-L1 monoclonal antibodies approved by the U.S. Food and Drug Administration (FDA), Merck’s Keytruda, Bristol Myers Squibb’s (BMS) Opdivo, Roche’s Tecentriq, and AstraZeneca’s Imfinzi have already been launched in the Chinese market. Currently, a total of eight PD-1/PD-L1 monoclonal antibodies have been marketed in China, officially ushering in the era of cancer immunotherapy in the country.

Whether for BMS or Merck & Co., the pricing of PD-1 inhibitors in China is nearly half their retail prices abroad, with domestic pharmaceutical companies also driving down prices. Innovent Biologics’ Tyvyt saw a 63.7% price reduction, becoming the only PD-1 drug included in the National Reimbursement Drug List in 2019. BeiGene plans to announce its pricing after the 2020 Spring Festival. Given the current market landscape, we speculate that BeiGene will introduce a highly competitive pricing strategy to secure a share in the fierce competition.

2) Overseas oncology immunotherapy achieves breakthroughs across multiple indications, with combination therapy remaining the focal point

Oncology immunotherapy remains a key area in overseas clinical development. Monotherapy with PD-L1 inhibitors has achieved a breakthrough in small cell lung cancer, an indication that had seen no progress for many years, while combination therapies continue to be the focal point of competition.

Lung cancer, which has the highest mortality rate among all cancers globally, is primarily divided into two major types: non-small cell lung cancer (NSCLC) and small cell lung cancer (SCLC). NSCLC accounts for approximately 85% of all lung cancer cases, while SCLC constitutes 15%. Given its larger market share, many pharmaceutical companies favor the development of drugs for NSCLC. Approved first-line immunotherapies for NSCLC include Merck’s Keytruda and Roche’s Tecentriq. At the end of 2019, Bristol Myers Squibb’s (BMS) combination of Opdivo and Yervoy met the co-primary endpoint of overall survival as a first-line treatment for NSCLC and has since received Priority Review from the FDA. BMS’s CEO stated that the use of Opdivo and Yervoy as first-line therapy for NSCLC will be a key focus over the next two years. This development is poised to become one of the most critical assets in the competitive landscape of oncology immunotherapy between BMS and Merck, while also intensifying competition around combination therapies based on CTLA-4 and PD-1 inhibitors.

Unlike NSCLC, SCLC progresses rapidly and is aggressive, with a 5-year survival rate of only 2% for patients diagnosed at stage IV. For two decades, patients had few treatment options beyond chemotherapy. In 2019, Keytruda was approved for third-line treatment of SCLC. More importantly, Tecentriq in combination with chemotherapy was approved as first-line therapy for extensive-stage small cell lung cancer (ES-SCLC). In November, the U.S. FDA also accepted AstraZeneca’s supplemental Biologics License Application (sBLA) for Imfinzi, indicated for previously untreated patients with extensive-stage small cell lung cancer, and granted the application Priority Review designation.

Triple-negative breast cancer (TNBC) accounts for approximately 15% of all breast cancer cases. Compared with other subtypes, it is characterized by rapid progression and a poor prognosis. Clinical treatment options for TNBC are very limited, relying primarily on chemotherapy. Roche’s Tecentriq, in combination with chemotherapy, significantly prolonged overall survival in patients receiving first-line treatment for TNBC and was approved for market launch in March 2019.

Roche Announces New Data from the Phase III IMbrave150 Study of Tecentriq in Combination with Avastin (bevacizumab) for Unresectable Hepatocellular Carcinoma, Showing a 42% Reduction in Risk of Death and a 41% Reduction in Risk of Disease Progression or Death Compared to Bayer’s Nexavar (sorafenib). Roche Has Submitted a Supplemental Biologics License Application (sBLA) to the FDA for Tecentriq Plus Avastin in Previously Untreated Unresectable Hepatocellular Carcinoma, Poised to Become the Leading First-Line Therapy for Liver Cancer.

As the above summary indicates, the rivalry between Merck & Co.’s Keytruda and Bristol Myers Squibb’s (BMS) Opdivo is set to continue. In particular, the significant progress made by Opdivo in combination with a CTLA-4 antibody as first-line treatment for non-small cell lung cancer (NSCLC) will help BMS reverse its current downturn. Roche, the traditional oncology powerhouse ranking among the top three, may be a latecomer to the field of tumor immunotherapy, but it has achieved successive breakthroughs in first-line treatments for multiple major indications, including small cell lung cancer (SCLC), triple-negative breast cancer (TNBC), and hepatocellular carcinoma (HCC), emerging as the most formidable competitor to Merck and BMS.

3. Next-Generation Cell Therapies Begin to Shine

In 2019, the field of cell therapy saw a continuous stream of positive developments. Yescarta, the first-generation immune cell therapy product, generated $456 million in revenue for Gilead in 2019, exceeding expectations and representing a 73% year-over-year increase. At the end of 2019, following its initial approval for diffuse large B-cell lymphoma (DLBCL), Yescarta demonstrated renewed momentum in relapsed/refractory mantle cell lymphoma (R/R MCL). Results from a global, multicenter Phase II clinical trial indicated significant and durable efficacy with a manageable safety profile, and a Biologics License Application (BLA) for R/R MCL has subsequently been submitted to the FDA. It is conceivable that once the MCL indication is approved, Yescarta’s market share will far surpass that of Novartis’ Kymriah.

Notably, in December 2019, Fosun Kite, the company responsible for the industrialization of Yescarta in China, officially inaugurated its first CAR-T cell therapy manufacturing facility in Zhangjiang, which will further accelerate the industrialization of Yescarta in China. In February this year, the National Medical Products Administration (NMPA) accepted Fosun Kite’s marketing application for China’s first CAR-T product. In October 2019, Novartis also announced that it had received implicit approval from Chinese regulators to initiate clinical trials for Kymriah, with the proposed indication being relapsed or refractory aggressive B-cell non-Hodgkin lymphoma.

First-generation CAR-T therapies still face numerous challenges, while emerging biotechnology companies are actively leveraging next-generation CAR technologies to produce more affordable, safer, and more effective cell therapies. Gracell Biotechnologies’ bispecific CAR-T therapy, presented at the 2019 ASH Annual Meeting, has significantly addressed common issues associated with first-generation CAR-T therapies, such as drug resistance and safety concerns. Fate Therapeutics and Century Therapeutics are focusing on off-the-shelf cells derived from induced pluripotent stem cells (iPSCs). In September 2019, Fate Therapeutics’ iPSC-derived universal natural killer (NK) cell therapy, FT516, received FDA approval to commence clinical trials. Poseida Therapeutics combines high-fidelity gene editing systems with non-viral piggyBac (PB) DNA transposon technology to generate CAR-T cells primarily within the T memory stem cell (Tscm) subset.

After years of dormancy, tumor-infiltrating lymphocyte (TIL) therapy reemerged in 2019 as a promising force in the fight against solid tumors. Iovance’s LN-145 TIL therapy achieved a 44% overall response rate and an 11% complete response rate in patients with cervical cancer, earning Breakthrough Therapy Designation from the U.S. Food and Drug Administration (FDA). This therapy is poised to become the first cell-based immunotherapy approved for the treatment of solid tumors.

From CAR design and cell type selection to functional modulation, gene editing, and delivery system optimization, new technologies and methodologies are continuously emerging in the field of cell therapy. This sector is expected to remain highly dynamic for the foreseeable future.

4. Gene Therapy Captures Global Attention

Gene Therapy Shines in 2019. In May, Zolgensma, a gene therapy for spinal muscular atrophy (SMA) using an AAV vector, was launched. As the second viral vector-based gene therapy approved by the FDA, it signifies the growing maturity of this therapeutic approach. BioMarin’s AAV-based gene therapy for hemophilia has been submitted to the European Medicines Agency (EMA) and is expected to reach the market in 2020. CRISPR, as a cutting-edge hotspot technology, holds immense potential not only as a direct therapeutic modality but also for applications in cell therapy and drug screening. In November, positive data were announced from the first clinical trial of a CRISPR-based therapy conducted in the United States. CTX001, a CRISPR/Cas9 gene-editing therapy developed by CRISPR Therapeutics and Vertex Pharmaceuticals, achieved positive interim results in its Phase 1/2 clinical trial.

After experiencing a downturn in the first decade of the 21st century, small nucleic acid drugs ushered in a second wave of enthusiasm with the 2018 market launch of Alnylam’s siRNA therapy, Onpattro (patisiran). In November 2019, Alnylam’s second siRNA drug, Givlaari (givosiran), was approved for the treatment of acute hepatic porphyria (AHP) in adults. Among the top 10 global licensing deals in 2019, three were RNA-related. In addition to the aforementioned transaction between Genentech and Skyhawk, the fifth-largest deal was a $1.67 billion agreement between Roche and Dicerna for the co-development of innovative therapies for chronic hepatitis B. The sixth-largest was a $1.55 billion transaction involving Pfizer, Ionis, and Akcea for antisense therapies targeting patients with certain cardiovascular and metabolic diseases. With advancements in technology and sequencing, reduced costs, improved stability of small nucleic acid drugs due to RNA modification technologies, and the emergence of highly efficient and safe delivery systems, small nucleic acid drugs continue to achieve breakthroughs. Particularly in the field of liver diseases, including liver cancer as well as other metabolic or fibrotic conditions, small nucleic acid drugs may even assume a mainstream position owing to their inherent superior targeting capability.

Meanwhile, in 2019, we also witnessed the potential of small nucleic acid drugs beyond the field of rare diseases. The outstanding performance of inclisiran, developed by The Medicines Company, in pivotal Phase III clinical trials for lowering low-density lipoprotein cholesterol (LDL-C) has bolstered confidence in the future application of small nucleic acid therapeutics in large-indication areas. Coupled with the convenience of administration (less frequent dosing) and lower manufacturing costs compared to large-molecule drugs, the development of small nucleic acid drugs is poised to enter a new era in the coming years.

In contrast to gene therapies and small nucleic acid drugs, which have seen successive approvals in recent years, mRNA drug development remains in the early clinical stages. mRNA drugs offer significant advantages as they do not enter the cell nucleus, do not alter the genome, exhibit only transient activity, and can be degraded through physiological metabolism. Furthermore, the simplicity and low cost of mRNA production substantially shorten the development timeline and reduce the costs associated with new drug development. At the 2019 ASCO Annual Meeting, Moderna presented encouraging interim results from clinical trials of its personalized cancer mRNA vaccine, mRNA-4157, administered either as monotherapy or in combination with Keytruda.

5. The Path in the NASH Field Is Long and Arduous, but a Breakthrough Is Imminent

2019 was hailed as the inaugural year for NASH. Amidst high expectations, the first NASH drug is finally approaching: on September 27, Intercept Pharmaceuticals submitted a New Drug Application (NDA) to the FDA for obeticholic acid in the treatment of NASH. The global competition in NASH drug development has become increasingly intense, with more than 40 candidates having entered Phase II clinical trials or later stages. In China, over 20 pharmaceutical companies have NASH products in their pipelines; however, these domestic investigational products remain in preclinical or early-stage clinical development, lagging behind their international counterparts.

However, the path to victory remains uneven, with numerous failures in this field in 2019. Enanta’s FXR agonist EDP-305 barely met its primary endpoint, but severe pruritus occurred in 47% of patients in the high-dose group. CymaBay’s PPARδ agonist seladelpar failed to outperform placebo in a Phase II clinical trial for NASH. Genfit’s elafibranor did not demonstrate superior efficacy over placebo in improving liver fibrosis and reducing hepatic steatosis in a Phase II clinical trial. Conatus’ pan-caspase inhibitor emricasan failed to meet its primary endpoint in a Phase IIb clinical trial involving patients with decompensated cirrhosis.

Insights from numerous failed cases indicate that targeting multiple pathways is key to achieving sustained clinical efficacy. NASH complications include various chronic metabolic disorders, such as diabetes, hypertension, and hyperlipidemia, suggesting that NASH is essentially a metabolic disease. Currently, apart from Tobira/Allergan’s CVC, most drugs that have demonstrated efficacy in Phase 2b/3 clinical trials are metabolic modulators targeting the underlying metabolic nature of NASH.

In the future, combination therapy, personalized targeted therapy, and indication expansion will be the three major trends in the field of non-alcoholic steatohepatitis (NASH). The use of personalized targeted drugs relies primarily on precise diagnosis via biomarkers to determine which targets are actively expressed in organs, particularly the liver, thereby guiding the selection of appropriate medications. However, due to the current lack of comprehensive diagnostic tools in the field, the application of targeted therapy still requires extensive exploration over a prolonged period. Many NASH targets have been derived from other indications, while novel NASH targets can also be extended to other disease areas, bolstering confidence in new drug development.