2019 Global Medical Device Capital Market Report: Innovation Shines, Consolidation Prevails

Amid the escalating global pandemic, the healthcare and life sciences sector has once again become the focal point of market attention. As a key area of long-term focus and deep cultivation, the China Renaissance Healthcare team has continued its tradition in this early spring, when warmth is still interspersed with chill. By examining five major sectors—biopharmaceuticals, IVD and genetic testing, medical devices, healthcare services, and smart healthcare—as well as capital markets, the team strives to provide a comprehensive overview of the development trends in the global healthcare industry over the past year.

Looking back at 2019, the capital market in the medical device sector opened up new exit channels thanks to the STAR Market and the new Chapter 18A regulations of the Hong Kong Stock Exchange. Private equity financing continued its previous trend of focusing on small but high-quality deals, while international giants steadily advanced their mergers, acquisitions, and investment collaborations in strategic pipeline areas. In line with the industry’s capacity and potential, imaging, orthopedics, cardiovascular, and surgery remained key specialties attracting capital attention.

Following the major reshuffle of the pharmaceutical industry in 2018 due to the "4+7" centralized procurement program, the medical device sector faced its own pivotal moment in 2019. Anhui Province and Jiangsu Province launched pilot centralized procurement policies for high-value consumables with a high degree of standardization, with orthopedics, cardiovascular, and ophthalmology devices being the most heavily impacted. Building on years of prior clinical data collection by the government, these measures aim to further drive down prices, prevent misuse, and strengthen regulatory oversight. Although the sales performance of leading companies is expected to suffer significant short-term impacts, this shift will likely facilitate import substitution and increase industry concentration in the medium to long term.

In 2019, a cohort of innovative medical device companies that had recently obtained regulatory certification faced the challenges of commercialization under the new normal. At the other end of the spectrum, a group of companies that had progressed through their development cycles and achieved initial business scale actively explored opportunities for initial public offerings (IPOs). Looking ahead to 2020, it is poised to become a landmark year for further industry consolidation and standardization.

This issue will analyze and share the capital market performance of the global medical device sector over the past year, focusing on three aspects: private equity financing, IPOs, and mergers and acquisitions.

In December 2018, the proposed winning bids for the pilot program of centralized drug procurement, involving four municipalities directly under the central government and seven provincial capitals or cities with independent planning status, were announced successively. The selected drugs saw significant price reductions, leading to an immediate decline in the secondary market valuations of the relevant pharmaceutical companies. Amidst heightened scrutiny, the other shoe dropped in 2019 as policies targeting high-value medical consumables were implemented.

1. On July 19, 2019, the General Office of the State Council issued and implemented the Reform Plan for the Governance of High-Value Medical Consumables. Core provisions include establishing a unified coding system and information platform, implementing medical insurance access and dynamic adjustment of the reimbursement list, improving classified centralized procurement methods, eliminating markups on medical consumables, and formulating medical insurance payment policies. The state has further intensified adjustments to the ratios of pharmaceutical costs, medical device costs, and service fees.

2. In July, Anhui Province initiated the first round of centralized procurement, selecting spinal implants and ophthalmic intraocular lenses (IOLs) as the pilot products. Eighteen provincial-level public medical institutions in Anhui Province implemented the negotiated prices, with a procurement cycle of one year. Eleven companies were awarded bids for orthopedic spinal products, and four companies were awarded bids for ophthalmic IOLs. The overall average price reduction for orthopedic spinal implants was 53.4%, while that for artificial intraocular lenses was 20.5%.

3. In July and September, Jiangsu Province conducted two rounds of volume-based procurement negotiations for high-value medical consumables. The price reductions for cardiovascular interventional devices, orthopedic joints, and ophthalmic intraocular lenses were more aggressive than those in Anhui Province, and the coverage was expanded to 107 member institutions of the Provincial Sunshine Procurement Alliance.

4. In October, Shandong issued the "Implementation Plan for Centralized Procurement on the High-Value Medical Consumables Platform of the Shandong Provincial Public Resource Trading Center (Trial)."

5. In December, the Leading Group for Deepening the Reform of the Medical and Healthcare System under the State Council issued a document to comprehensively promote the medical reform experiences of Fujian Province and Sanming City. This includes implementing centralized volume-based procurement of drugs and medical consumables. It is reported that by the end of September 2020, Jiangsu, Anhui, Fujian, Qinghai, Zhejiang, Chongqing, Sichuan, Shaanxi, Hunan, Ningxia, and Shanghai were to take the lead in exploring volume-based procurement of high-value medical consumables.

Although the provinces, hospitals, and product categories currently subject to centralized volume-based procurement (VBP) for medical devices are limited, a new round of industry reshuffling has already begun, with promising prospects ahead. The new normal favors enterprises with extensive commercial distribution channels, robust bidding capabilities, stable product quality, and certain innovative technological barriers. In contrast, companies that are small in scale, have regionally constrained channels, and offer homogeneous products will lose their eligibility to compete in this landscape. The past business model of settling for modest success is no longer sustainable, making industry consolidation imminent.

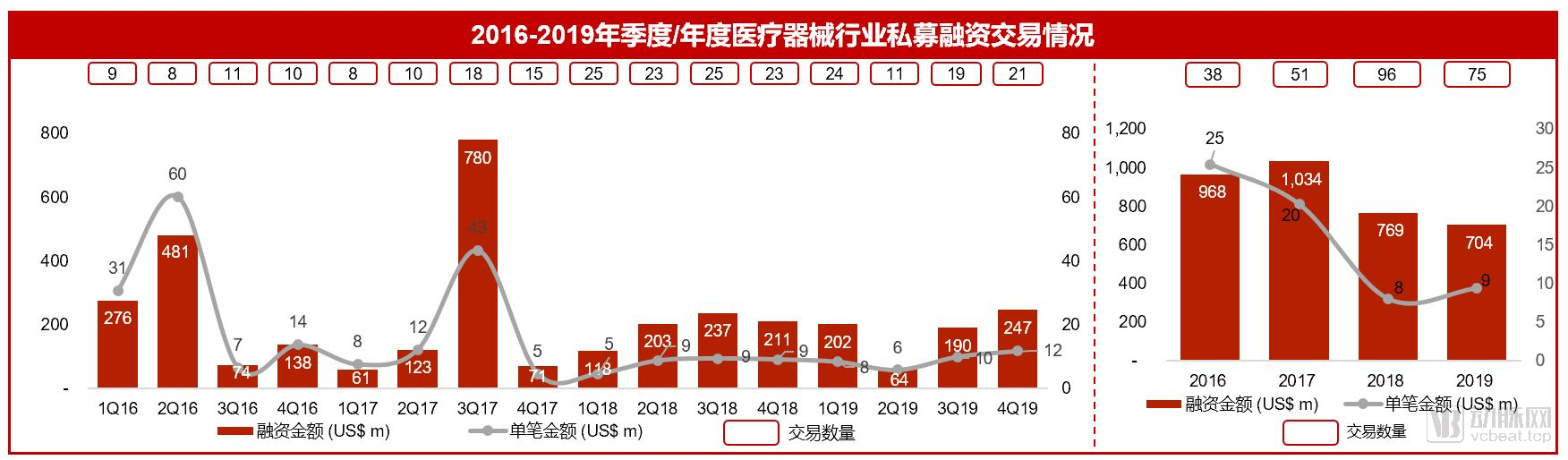

1. Private Equity Financing for Chinese Medical Devices Remains Normal

In 2019, the total disclosed financing amount in the medical device sector was approximately $700 million, representing an 8.6% year-on-year decline from 2018. The total number of transactions stood at 75, a 21.9% decrease compared to 2018.

Data Source: Public Market Information

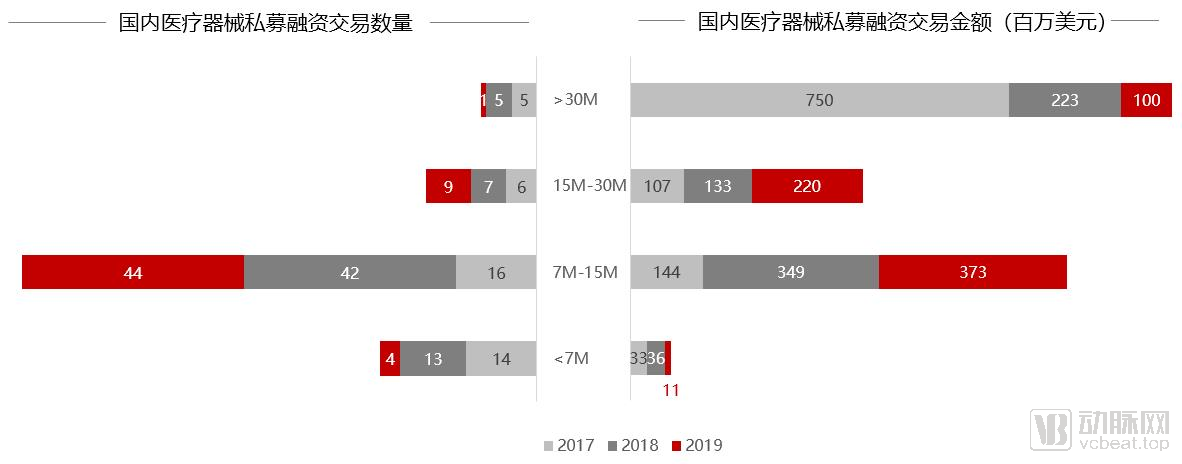

Among these, Peijia Medical secured the largest single financing round, amounting to $100 million. There were nine transactions in the $15–30 million range and 44 financing deals between $7 million and $15 million. A total of 58 transactions with disclosed financing amounts were recorded, with an average fundraising amount of $12.13 million, representing a 9.6% increase compared to 2018.

Data Source: Public Market Information

From the perspective of specific sub-sectors, private equity financing transactions with funding scales of approximately RMB 100 million include the following:

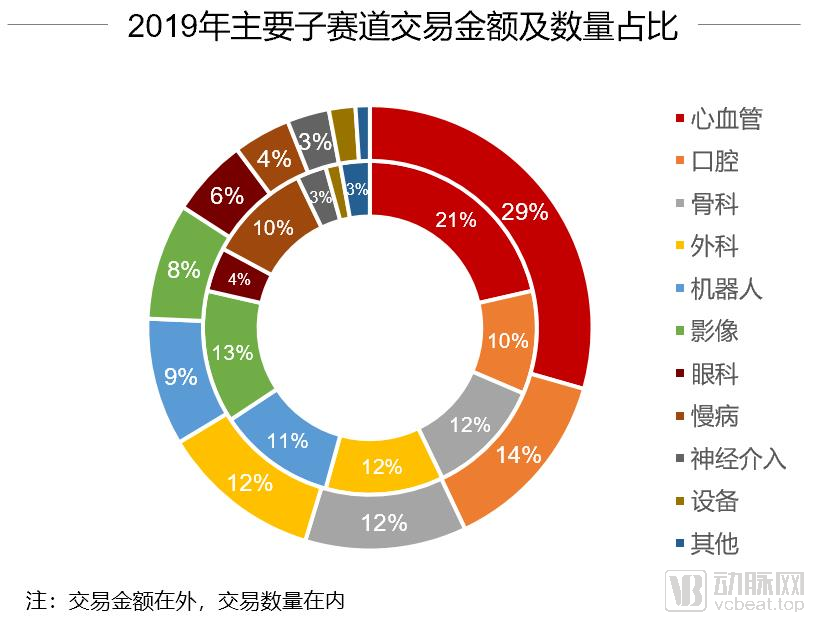

Investment in medical devices remains focused on high-value consumables, particularly Class III implantable medical devices. The concentration of investment tracks has changed little compared to previous years, with innovative companies in cardiovascular, dental, orthopedic, and surgical fields dominating the landscape. Meanwhile, emerging sectors such as surgical robotics, ENT (ear, nose, and throat), and tumor ablation have also garnered significant attention. The热度 (heat/popularity) of these sectors is closely tied to global industry developments and M&A trends. For instance, Johnson & Johnson’s $5.75 billion acquisition of surgical robotics company Auris Health, officially announced in February 2019, sparked a new wave of interest and project screening in China’s medical robotics sector. In June, Varian Medical Systems’ $185 million acquisition of Endocare, a manufacturer of cryoablation and microwave ablation products, and Elicon, which provides embolization therapies for liver cancer treatment, ignited investor interest in the tumor ablation field.

2. 2019 Overseas Private Equity Market: A Flourishing Landscape of Sectors and a Surge in Transactions

In 2019, the total amount of private equity financing for overseas medical devices reached $7.2 billion. The United States dominated with an absolute advantage of $4.8 billion. Israel, as a super hub for innovative technologies, remained in the top three, with financing amounts reaching $370 million, second only to France ($440 million). In addition to sectors similar to those in China, such as orthopedics, cardiovascular, neurology, peripheral vascular, and dentistry, there was also extensive involvement in areas where China lacks development, including ophthalmology, urology, hemodialysis, dermatology, and diabetes.

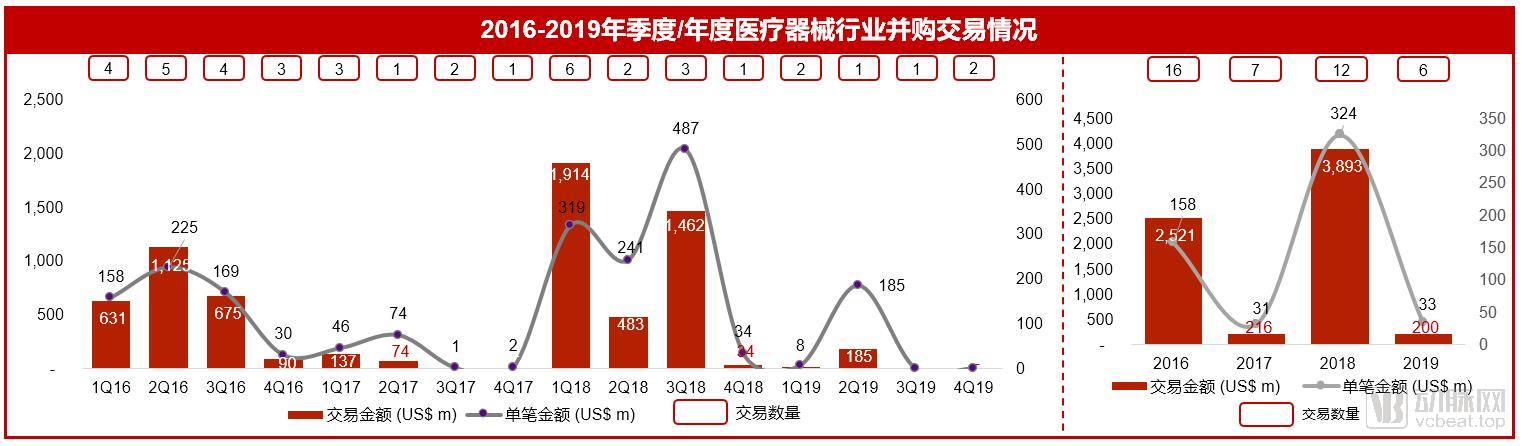

According to disclosed transaction data, M&A activity in China’s medical device sector continued to shrink significantly in 2019. The total M&A transaction value for the year amounted to USD 200 million, representing only 5% of the 2018 level. The number of M&A transactions totaled 33, approximately 10% of the 2018 figure.

Data source: Public market information

Overseas M&A activity remained robust, with the total value of disclosed transactions reaching $34.6 billion in 2019. Three blockbuster deals exceeding $4 billion each firmly secured the top three spots for the year: 3M’s $6.7 billion acquisition of wound care company Acelity and its subsidiary KCL; Johnson & Johnson’s $5.75 billion acquisition of surgical robotics firm Auris Health; and Boston Scientific’s $4.2 billion acquisition of interventional medicine company BTG.

Acelity: This medical technology company, which focuses on surgical applications and wound care, has a subsidiary, KCI, that leads the advanced dressings market with a rich product portfolio, generating $1.5 billion in revenue in 2018. Through this acquisition, 3M will enhance its position in the wound care sector, particularly in high-end (novel) medical dressings.

Auris Health: Founded and led as CEO by Dr. Frederic Moll, known as the father of surgical robots. Prior to Auris Health, Dr. Moll had founded three companies, including the renowned publicly traded company Intuitive Surgical (da Vinci Surgical System). The acquisition of Auris Health enabled Johnson & Johnson to obtain surgical robotic technology for airway procedures and lung cancer detection.

BTG: Its business portfolio spans three areas: interventional medicine products, vascular products, and acute drug antidotes. This acquisition marks Boston Scientific’s largest deal since its $27 billion purchase of cardiac device manufacturer Guidant in 2006, aiming to further enhance its capabilities in the interventional medical field.

Colflax Acquires DJO Global, the Sixth-Largest Player in Orthopedics, Creating a New Growth Platform in the High-Margin Orthopedic Solutions Market.

Fortive Acquires Johnson & Johnson’s Ethicon Advanced Sterilization Products (ASP) Division, Propelling Fortive into the Rapidly Growing Medical Disinfection and Sterilization Market, While J&J Enhances Overall Growth Through the Divestiture

The Merger of Fresenius and U.S. Home Dialysis Equipment Manufacturer NxStage: Following the acquisition agreement reached in 2017, the U.S. Federal Trade Commission finally approved the merger in February 2019, enabling Fresenius to enter the more affordable home dialysis market.

Corindus: This platform is currently the only robotic system approved by the FDA and bearing the European CE quality mark for coronary intravascular and peripheral vascular interventional procedures, capable of reducing radiation exposure to physicians. Siemens’ successful acquisition of Corindus has opened new frontiers in its clinical care business.

Cantel Medical, a provider of instrument reprocessing, infection prevention products and services, completes acquisition of Hu-Friedy: Hu-Friedy is a global manufacturer of dental instruments and instrument post-processing workflow systems with a 111-year history serving the dental industry. This acquisition creates a comprehensive provider of infection prevention, instrument, and instrument management solutions to optimize dentists’ needs for excellent clinical performance and best-in-class infection prevention practices.

Ophthalmic Medical Technology Company Glaukos Acquires Ophthalmic Pharmaceutical and Medical Device Company Avedro, Introducing Keratoconus Drug Therapy.

Vertiflex developed a minimally invasive surgical system designed to improve physical function and reduce pain in patients with lumbar spinal stenosis. The company generated $60 million in sales in 2019 and received an upfront payment of $465 million, along with milestone payments over the following three years, from Boston Scientific upon its acquisition. This product line will be integrated into Boston Scientific’s Neuromodulation division.

When it comes to initial public offerings (IPOs) in the medical device sector, one cannot overlook the new vitality injected into this industry by the STAR Market.

On July 22, 2019, as MicroPort Endovascular and Nanwei Medical rang the opening bell for the medical device sector on the STAR Market, Chinese medical device companies gained access to a new channel in the capital markets. Within the first six months of the board’s launch, a total of 16 pharmaceutical and biotechnology companies successfully listed, including seven medical device firms, accounting for nearly half of the total. This made medical devices the most sought-after subsector within the biomedical industry.

In terms of post-IPO price gains on the STAR Market, medical device companies have led the entire biopharmaceutical sector. As of December 31, 2019, the average gain for the 16 listed companies was approximately 90%, while the average gain for medical device firms reached 105%. Among them, MicroPort Scientific (Nanwei Medical), HeartCare Medical, and SinoMedical all posted gains exceeding 100%. The average price-to-earnings (P/E) ratio of medical device companies on the STAR Market stood at 76.43, ranking first among the four major sectors.

It is worth noting that the revised Chapter 18A of the Hong Kong Stock Exchange Listing Rules, enacted in late 2017, not only provided a fast-track channel for biotechnology companies but also opened a new pathway for medical device enterprises that had not yet generated revenue or profits. Following the listing of numerous biopharmaceutical companies on the Hong Kong stock market, Venus Medtech’s successful IPO became the first case for a medical device company, leading the 2019 medical device IPOs with a total fundraising amount of $368 million.

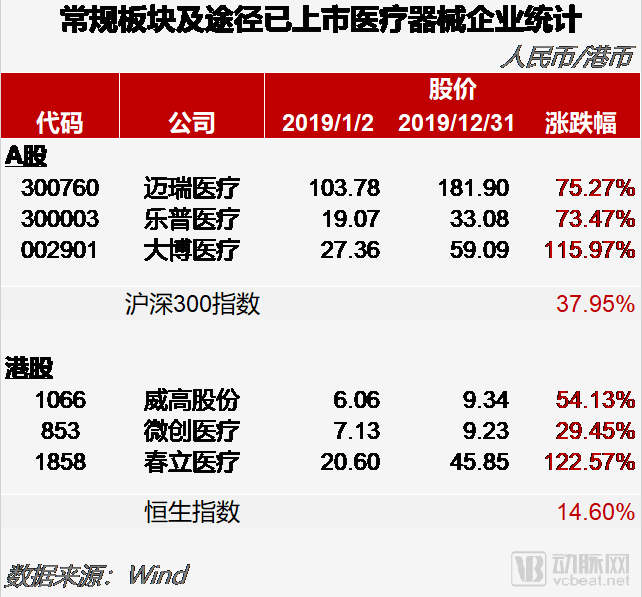

Listed medical device companies also delivered strong performance in 2019. Here, we highlight six companies listed on the A-share and Hong Kong stock exchanges, primarily operating in orthopedics, implants, cardiovascular, and peripheral vascular sectors. These companies achieved substantial gains across different market segments, outperforming the broader market, with growth momentum comparable to that of companies on the STAR Market. The robust revenue growth of these firms has bolstered investor confidence in the capital markets, driven by both the expansion of overseas distribution channels and the accelerating trend of import substitution in the domestic market.

We believe that the strong investor appetite for medical device companies in China’s secondary market is driven not only by the fresh vitality injected by the STAR Market, but also primarily by the fact that the balanced and stable profile of R&D cycles and capital investment ratios in the device sector better aligns with the preferences of A-share secondary market investors. We expect this trend to continue in 2020, making it a landmark year for STAR Market listings in the medical device industry. Moreover, the enthusiasm in the secondary market will continue to bolster confidence among primary market investors and renew their focus on the medical device segment. Subsectors with directly comparable listed peers—such as ophthalmology, electrophysiology, and orthopedic joints—are expected to be key areas of interest in the private equity market this year.

In contrast to the booming domestic market, the enthusiasm for medical device IPOs in overseas stock markets has remained largely flat compared with previous years. Only six companies listed on NASDAQ in the U.S., with an average first-day gain of approximately 85% and an average fundraising amount of $94 million. Among them, Silk Road Medical, which focuses on the research and development of minimally invasive devices for Transcarotid Artery Revascularization (TCAR), led the pack with a $120 million raise, drawing significant attention from investors.

1. High-value consumables remain the most favored assets in the capital market, but the pandemic has also introduced new investment logics, with manufacturers of low-value consumables such as masks and gloves, as well as companies with advanced product lines like ECMO, becoming new focal points for investors.

2. Investors have placed renewed emphasis on companies’ self-sustaining cash-generating capabilities. Tightening belts in pipeline progress management, strategic pacing, and cost control can bolster shareholder confidence and help companies weather the poor start to the first half of 2020.

3. Several platform-based clusters will emerge in China, rapidly consolidating the small and fragmented medical device assets accumulated over the past two decades through the synergy of capital and top-tier professional managers, thereby giving rise to industry giants.

4. The market has raised new requirements for medical device entrepreneurs. Simply imitating overseas benchmark products no longer guarantees easy access to funding. To meet the expectations of the capital markets, companies must demonstrate comprehensive capabilities, including long-term pipeline planning, product improvements tailored to the Chinese market, clinical registration, mass manufacturing, quality control, and breakthrough marketing strategies.