Opportunities in Medical Institution 'New Infrastructure': How the Pandemic Acts as a Catalyst

The COVID-19 epidemic is being gradually brought under control in China. Many regions across the country have reported no new confirmed cases for several consecutive days, and existing patients are progressively recovering and being discharged. Under these circumstances, socioeconomic order needs to be gradually restored while ensuring effective epidemic prevention and control. Medical institutions nationwide must also gradually resume normal medical service operations while continuing to implement epidemic prevention and control measures.

At the macro level, the COVID-19 pandemic has inevitably inflicted a severe shock on the global economy and society. Many economists initially offered optimistic analyses and forecasts regarding the impact and long-term effects of the pandemic. However, as the virus began to spread worldwide, the focus of future projections shifted in another direction—toward mitigating the substantial impact of the global outbreak on the world economy.

According to the United Nations’ World Economic Situation and Prospects 2020, global economic growth slowed to 2.3% in 2019—the lowest level in a decade—with a rate below 2.5% generally considered indicative of a recession. Furthermore, the International Monetary Fund (IMF) projected that global economic growth in 2020 would be even slower than in 2019.

To address the post-pandemic economic downturn, on February 3, the Standing Committee of the Political Bureau of the CPC Central Committee made its initial deployment, calling for accelerated release of emerging consumption potential, active enrichment of 5G technology application scenarios, stimulation of terminal consumption such as 5G smartphones, and promotion of increased consumption in e-commerce, e-government, online education, and online entertainment.

Subsequently, within the 30-day period from February 3 to March 4, central authorities deployed tasks related to “New Infrastructure” at least five times, while local policy documents proliferated beyond count.

In fact, the concept of “new infrastructure” is not a recent topic. The official formulation of the term originated from the Central Economic Work Conference held in late 2018. When outlining the tasks for 2019, the conference pointed out the need to “accelerate the commercialization of 5G and strengthen the development of new-type infrastructure, including artificial intelligence, industrial internet, and the Internet of Things.”

New infrastructure generally encompasses sectors such as 5G, ultra-high-voltage power transmission, intercity high-speed railways and urban rail transit, charging stations for new energy vehicles, big data centers, artificial intelligence, the industrial internet, and the Internet of Things. Compared with traditional infrastructure, which primarily consists of railways, highways, airports, and bridges, China has significant room for development in this area.

The sudden outbreak has also exposed certain weaknesses in China’s healthcare system; meanwhile, emerging health information technologies have played a significant role in the pandemic response. Telemedicine, remote diagnosis and treatment with data sharing, biopharmaceuticals, and medical devices are also considered important components of new infrastructure development.

Guo Qiyong, Chief Expert and Dean of the Research Institute at Beijing Dongruan Wanghai Technology Co., Ltd., recently stated, “In the wake of the pandemic, the role of remote work, telemedicine, and data sharing in remote diagnosis and treatment will become even more prominent. China’s medical informatization and hospital informatization construction are poised for significant growth.”

To help healthcare institutions adjust and ensure sound operations, and to identify opportunities within the new infrastructure initiatives, VCBeat (WeChat ID: Vcbeat) has compiled relevant materials in an attempt to analyze and study the subsequent impacts of sudden epidemics on healthcare institutions and health administrative agencies.

Learning from History: The Impact of SARS on Healthcare Institutions in China

Let us first review the impact of the 2003 SARS outbreak on the operations of healthcare institutions. The shock of the SARS epidemic exposed significant deficiencies in China’s public health system. Subsequently, the state comprehensively strengthened disease prevention and control to enhance its capacity to respond to sudden public health emergencies, such as major infectious disease outbreaks.

On October 14, 2003, the Third Plenary Session of the 16th Central Committee of the Communist Party of China stated: “It is necessary to deepen the reform of the public health system. Strengthen the government’s functions in public health management and establish a healthcare system compatible with the socialist market economy.”

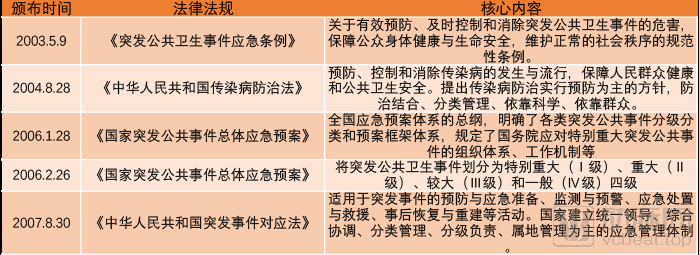

First, relevant laws and regulations were established to improve the emergency response mechanism for public health emergencies. From 2003 to 2007, the state issued a series of laws and regulations, among which the "Law of the People's Republic of China on the Prevention and Treatment of Infectious Diseases" was promulgated on August 28, 2004.

The National Emergency Response Plan for Public Health Emergencies, issued on February 26, 2006, was implemented multiple times during this outbreak and has gained widespread recognition. The core component of the plan is to classify public health emergencies—including those involving known or unknown infectious diseases—into four levels based on their nature, severity, and scope: Particularly Major (Level I), Major (Level II), Relatively Major (Level III), and General (Level IV).

Under this plan, the health administrative department of the State Council is required to establish a Health Emergency Office (Emergency Command Center for Public Health Emergencies), which shall be responsible for the day-to-day management of emergency response to public health emergencies nationwide.

In the event of an emergency, health administrative departments at all levels shall, under the unified leadership of governments at corresponding levels, be responsible for organizing and coordinating the emergency response to public health emergencies nationwide or within their respective regions. Based on the actual needs of emergency response efforts, they shall propose the establishment of national or local emergency command headquarters for public health emergencies. Meanwhile, health administrative departments at all levels shall also establish expert advisory committees for public health emergencies.

The disease prevention and control system was also accelerated and improved in the aftermath of the SARS outbreak. The Chinese Center for Disease Control and Prevention, established in early 2002, had basically completed the reform of provincial-level CDC institutions at that time, and the four-tier CDC system—central, provincial, prefectural, and county—was subsequently accelerated to completion. By 2019, a total of 3,443 CDCs had been established across China at the national, provincial, prefectural (municipal), and county levels.

Concurrently, the construction of a new direct online reporting system for disease control and prevention was accelerated. In January 2004, the National Network Direct Reporting System for Infectious Diseases and Public Health Emergencies (hereinafter referred to as the “Network Direct Reporting System”) became operational, marking a qualitative leap in China’s capabilities and methods for monitoring and reporting infectious disease outbreaks. Although its performance during the current outbreak has been subject to controversy, this system indeed played a significant role in previous infectious disease epidemics.

The SARS outbreak also spurred a new round of healthcare reform. On April 6, 2009, the Central Committee of the Communist Party of China and the State Council officially released the “Opinions on Deepening the Reform of the Medical and Healthcare System,” which explicitly called for improving the public health service system by “further clarifying the functions, objectives, and tasks of the public health service system, optimizing the allocation of personnel and equipment, and exploring effective models for integrating public health service resources.”

In 2003, China established the New Rural Cooperative Medical Scheme (NRCMS) targeting the rural population; in 2009, it introduced the Urban Resident Basic Medical Insurance (URBMI) for non-employed urban residents; these joined the Urban Employee Basic Medical Insurance (UEBMI), which had already been established in 1998 to cover urban employees. These three basic medical insurance schemes achieved universal coverage, with an enrollment rate exceeding 95% by 2011.

Meanwhile, the coverage scope and reimbursement ratios of medical insurance have been continuously improving. For employee basic medical insurance, the policy-based inpatient reimbursement rate has exceeded 80%, with the actual expense reimbursement rate surpassing 70%. For the New Rural Cooperative Medical Scheme (NRCMS) and urban resident basic medical insurance, the policy-based inpatient reimbursement rate rose from 54% in 2008 to 66% in 2018, while the actual expense reimbursement rate increased from 45% to 56% over the same period. In 2015, China fully established a critical illness insurance program for urban and rural residents, further alleviating patients’ financial burden.

By the end of 2006, the disease prevention and control system and the medical treatment and rescue system for public health emergencies had been basically established. A total of RMB 26.9 billion in construction investment was allocated by the central and local governments, with the central government providing a special fund of RMB 8.68 billion to complete 5,116 projects. The disease prevention and control system received an investment of RMB 10.5 billion for the construction of 2,448 projects. Infectious disease hospital wards and emergency rescue centers received an investment of RMB 16.4 billion for the construction of 2,668 projects.

From a macro perspective, the SARS epidemic had a profound impact on medical institutions and health administrative agencies. So, from a micro perspective, what impacts did the SARS epidemic have on hospital operations? A glimpse can be seen from the data in the China Health Statistics Yearbook over the years.

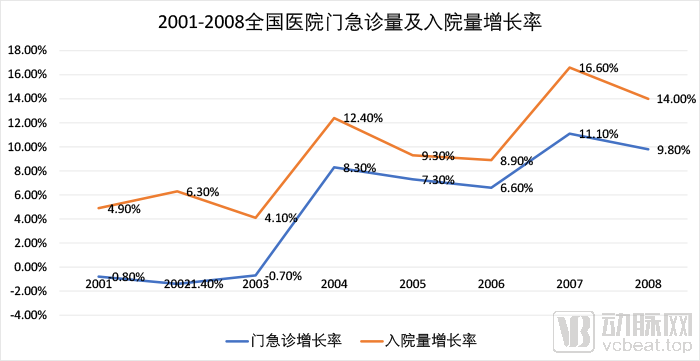

From 2001 to 2008, the national hospital admission growth rate in China was lowest in 2003, at only 4.1%; as the epidemic ended, the national hospital admission growth rate surged to 12.4% in 2004. This indicates that due to the impact of the epidemic, patients would avoid high-risk behaviors such as hospitalization unless absolutely necessary, and postpone them until after the epidemic had ended.

In terms of the growth rate of outpatient and emergency visits, the rate in 2003 was -0.7%, representing a certain rebound compared to the previous two years; however, it showed a significant gap when compared to the high growth rate of 8.3% recorded in 2004.

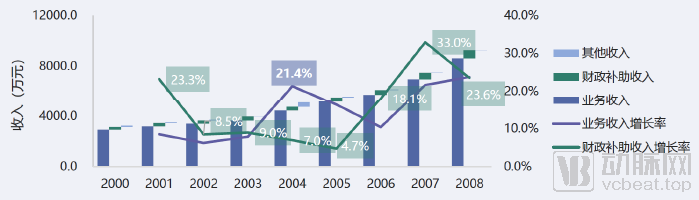

Annual Revenue Composition and Revenue Growth Rate of General Hospitals, 2001–2008; Image Source: Wanghai Kangxin HIA Data Platform

The decline in the growth rates of hospitalizations and outpatient/emergency visits, which are directly tied to core operations, naturally impacted hospital business revenue. In 2003, the year-on-year growth rate of business revenue for hospitals across China was 9%; in the following two years, this figure surged to 21.4% (2004) and 16% (2005), respectively. This trend directly reflects the dampening effect of the epidemic on business growth.

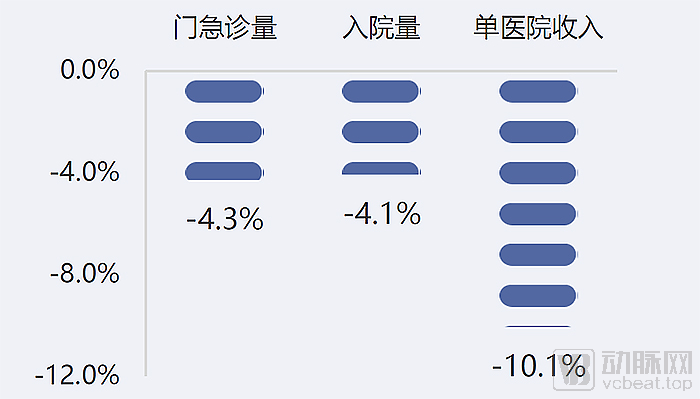

Variations of 2003 Indicator Data from Expected Values, Image Source: Wanghai Kangxin HIA Data Platform

Using the average of the actual values from the two years before and after the SARS outbreak as the estimated expected rate, the national total number of outpatient and emergency visits in China in 2003 was 4.3% lower than expected, the number of hospital admissions was 4.1% lower than expected, and hospital medical service revenue declined significantly by 10.1% compared to expectations.

Growth Rates of Total Outpatient and Emergency Visits in Hospitals Across China, 2003–2006. Image source: Wanghai Kangxin HIA Data Platform

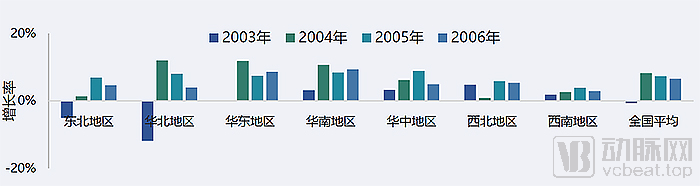

An analysis of data from various regions in China before and after the SARS outbreak also reveals a significant correlation between the epidemic and changes in outpatient and emergency visit volumes. In North China, the region most severely affected, outpatient and emergency visits in 2003 dropped sharply by 11.8% compared to the previous year. Among these, Hebei Province recorded the largest decline, at 19.4%.

In 2004, in the aftermath of the epidemic, although the number of outpatient and emergency visits in North China rebounded significantly to 163 million, the overall volume still failed to return to the 2002 level of 165 million.

Although South China was also a major epicenter of the epidemic at that time, with Guangdong Province recording the second-highest number of confirmed SARS cases after Beijing, the year-on-year growth rate of outpatient and emergency visits in South China was relatively high compared to the national average. This may be attributed to the concentration of medical resources in Beijing, located in North China, which attracted a large number of patients from other regions. As the epidemic intensified, many patients chose not to travel to the epidemic’s epicenter due to concerns about infection risks.

Overall, a comprehensive examination of the SARS outbreak and trends in healthcare service volume in affected regions around 2003 clearly shows that areas directly impacted by the epidemic experienced a decline in healthcare service volume that could reach 10% or more compared to the expected growth rate.

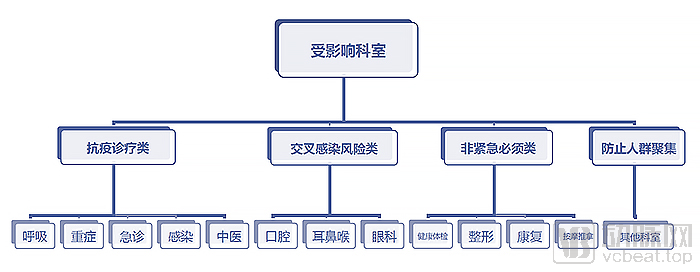

Based on the impact of the SARS outbreak on hospital departments, these departments can be categorized into four types: departments closely related to epidemic control, departments prone to cross-infection, departments with moderate infection risk but essential for operations, and non-urgent, non-essential departments.

Key Departments Related to the Epidemic refer to those directly involved in epidemic response, characterized by heavy workloads and severe disruption to routine clinical services. During the COVID-19 pandemic, these departments included critical care, respiratory medicine, emergency medicine, infectious diseases, and traditional Chinese medicine.

Departments prone to cross-infection may conduct necessary and emergency diagnosis and treatment, but require enhanced risk screening, which significantly impacts their clinical operations. These departments include stomatology, otolaryngology, and ophthalmology.

Departments with moderate but necessary infection risks refer to other common departments; as long as comprehensive risk management is implemented, the impact of the epidemic on their diagnostic and therapeutic activities will be relatively minor.

In addition, departments such as health check-ups, plastic surgery, rehabilitation, and massage therapy, which primarily rely on third-party medical institutions to provide healthcare services, are not considered essential or urgent during the pandemic. Due to risk considerations, regulatory authorities often recommend temporarily suspending these services.

COVID-19 presents rather complex symptoms, unlike any infectious disease in human history. While its epidemiological characteristics resemble those of influenza, certain clinical manifestations are akin to those of SARS. Therefore, the impact of SARS on various medical departments can also serve as a reference for the current outbreak.

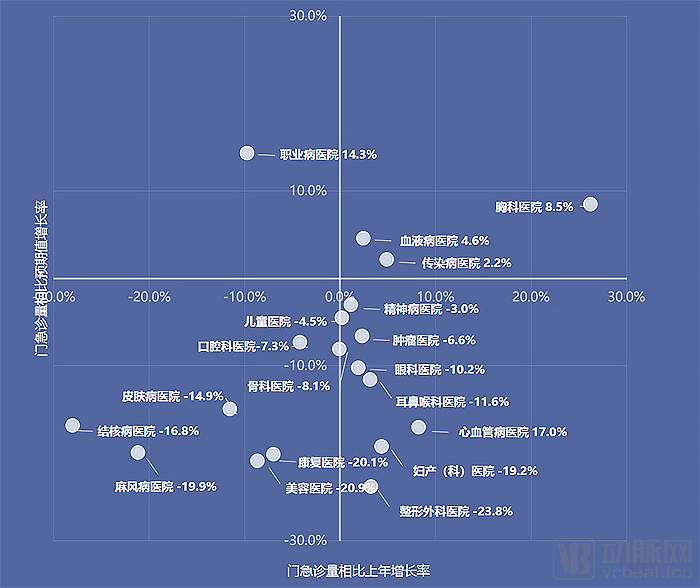

Based on the average of outpatient and emergency visit volumes in 2002 and 2004 as the expected value, an analysis of the year-on-year growth rate and the growth rate relative to the expected value for various types of specialized hospitals in 2003 reveals that the outpatient and emergency visit volumes of affected specialized hospitals were generally lower than the expected values.

According to statistics, except for thoracic hospitals, infectious disease hospitals, occupational disease hospitals, and hematology hospitals, where outpatient and emergency visit volumes exceeded expectations, the majority of specialized hospital departments fell below expected values by up to 20%, with plastic surgery departments falling short by as much as 23.8%. Even though cardiovascular specialty hospitals achieved an 8.2% growth, their outpatient and emergency visit volumes remained 17% lower than expected.

Overall, the situation during the SARS outbreak indicated that patients would avoid going to hospitals unless absolutely necessary until the epidemic was thoroughly resolved—for example, until confirmed cases completely disappeared, or effective and affordable treatments or vaccines became available.

What Level of Impact Does COVID-19 Have on Hospitals?

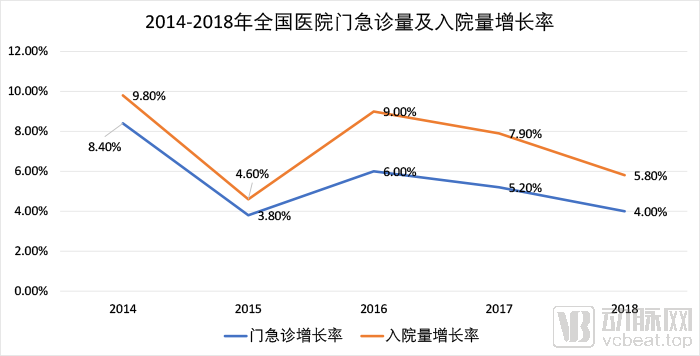

In recent years, the volume of outpatient and emergency visits and hospital admissions in China’s hospitals has maintained a steady growth trend, but the growth rate has continued to decline. In 2014, the growth rate of outpatient and emergency visits in Chinese hospitals was 9.8%, which dropped to 5.8% by 2018; during the same period, the growth rate of hospital admissions decreased from 8.4% to 4.0%.

According to data from the official website of the National Health Commission, the growth rate of total hospital outpatient visits in January–November 2019 declined to 5.4% compared with the same period in 2018, indicating a continued downward trend. The growth rate of hospitals’ medical service revenue gradually decreased from 15.2% in 2014 to 8.9% in 2018, with the overall revenue growth rate following a similar downward trajectory.

According to data from the World Health Organization (WHO), as of 10:00 Central European Time on March 7, there were a total of 101,927 confirmed cases of COVID-19 worldwide, with 3,480 deaths. The epidemic has spread globally, and its severity has far exceeded that of SARS. Meanwhile, the fact that the virus is also spreading in hot tropical regions suggests that it is unlikely to subside by summer. At the same time, due to various reasons, pandemic control in Europe and the United States is gradually approaching a state of loss of control. Based on cyclical predictions derived from the H1N1 pandemic, the impact duration of this outbreak will be longer than that of 2003, and it is highly likely to persist throughout the entire year of 2020.

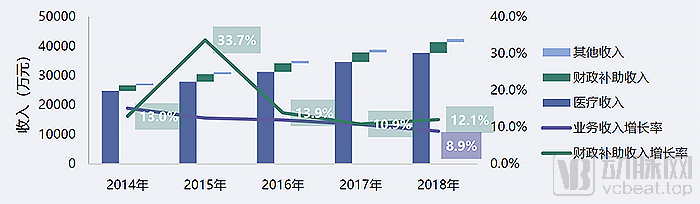

Annual Revenue Composition and Revenue Growth Rate of General Hospitals in China, 2014–2018. Image source: Wanghai Kangxin HIA Data Platform

Therefore, we believe that in 2020, the annual growth rates of patient visits and medical service revenue for most public hospitals across China will decline by at least 10% more than expected.

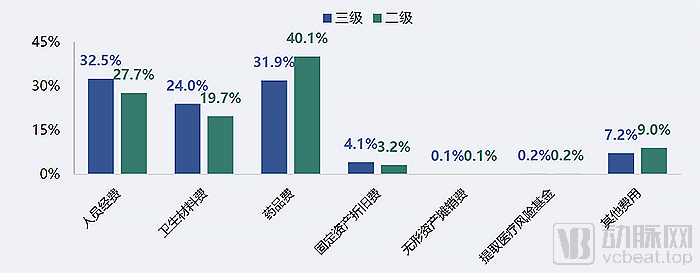

Cost Structure of Hospitals by Tier in 2018, Image Source: Wanghai Kangxin HIA Data Platform

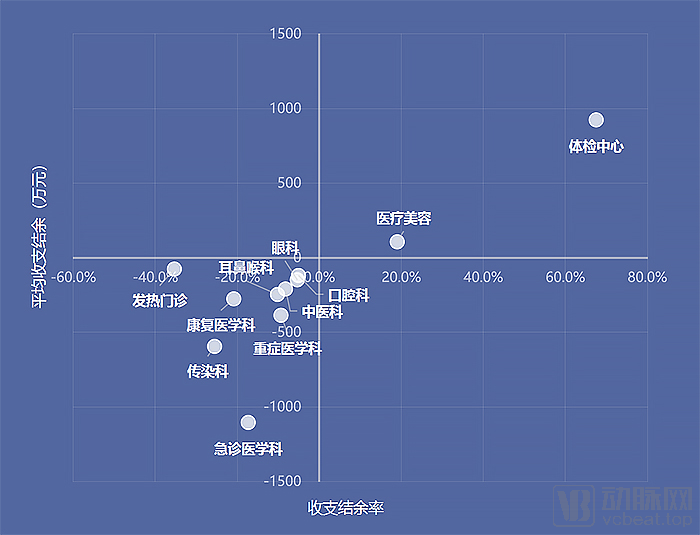

According to survey results from HIA-affiliated hospitals, the departments most severely impacted by the pandemic were often those with higher financial surpluses. The average surplus rate for non-urgent health examination centers reached as high as 67.5%, accounting for 1.5% of total departmental revenue; medical aesthetics also approached 20%. Given that public healthcare institutions hold certain advantages in providing consumer-oriented medical services, such services have become a significant supplement to hospital revenue.

Growth Rates of Total Outpatient and Emergency Visits in Various Specialized Hospitals in 2003 and Comparison with Expected Values; Image Source: Wanghai Kangxin HIA Data Platform

2003 Revenue and Expenditure Surplus by Department Type, Image Source: Wanghai Kangxin HIA Data Platform

Consumer healthcare has long been viewed favorably, with iResearch Consulting predicting that the medical aesthetics market will maintain a continuous growth rate of over 20% from 2019 to 2022. Prior to the outbreak of the pandemic, forecasts indicated that the market size of the medical aesthetics sector would reach RMB 211 billion in 2020, representing a 21.3% increase from the RMB 173.9 billion recorded in 2019.

The outbreak will have a direct impact on consumer healthcare services. To minimize risks, regulatory authorities will choose to temporarily suspend such services until the epidemic is fully under control.

During the pandemic, the Health Commission of Sichuan Province issued the "Notice on Further Implementing Level I Response to Standardize Diagnosis and Treatment Service Processes in Medical Institutions," which required the suspension of diagnosis and treatment activities in specialized hospitals and relevant departments of general hospitals, including stomatology, ophthalmology, otolaryngology, plastic (cosmetic) surgery, rehabilitation, health examination, traditional Chinese medicine acupuncture, and traditional Chinese medicine tuina (massage), with only necessary emergency diagnosis and treatment services retained. In fact, numerous hospitals across China have issued similar notices.

Of course, even if regulatory authorities ease controls, consumer willingness to spend on elective medical services will decline significantly due to fear of the epidemic and the non-urgent, non-essential nature of such services. According to Kantar’s consumer survey report on the COVID-19 pandemic, 50% of consumers reported that the pandemic had no impact on their willingness to undergo aesthetic medical procedures, while 25% experienced a decreased desire to consume and another 25% reported a strong desire to consume.

However, given the global spread of the pandemic, the nearly certain economic downturn will further suppress consumer spending willingness. The possibility that the growth rate of consumer healthcare in 2020 could be zero or even negative is not only present but has significantly increased.

In this scenario, public hospitals can still barely maintain operations, while third-party consumer healthcare institutions will face significant pressure. Consequently, medical aesthetics service platforms have introduced numerous incentive policies.

On February 2, So-Young Technology announced the launch of five major subsidy measures totaling over RMB 20 million for China’s medical aesthetics industry. Two key initiatives include waiving one month of platform usage fees for medical aesthetics institutions located in the four cities most severely affected by the epidemic, and providing more than RMB 20 million in customer acquisition resource subsidies to medical aesthetics institutions nationwide, along with substantial discounts or waivers on traffic fees, applicable across all resources.

Alibaba Health also stated that it would consider supporting consumer healthcare institutions through various measures, such as waiving platform operating fees for merchants, partnering with Alipay Insurance to provide free “Business Interruption Insurance” to merchants resuming operations, and integrating online marketing resources to offer comprehensive support.

With the full implementation of the zero-markup policy for medical consumables, revenue from pharmaceuticals and consumables—which previously accounted for a significant portion of hospital income—has been slashed, further exacerbating the already precarious operational status of public hospitals. Due to the impact of the pandemic, the scale of medical services has struggled to sustain growth. In particular, consumer-oriented medical specialties, which had previously demonstrated strong profitability, have been significantly affected by their inability to operate normally during the pandemic. Post-pandemic, these sectors are also expected to face intensified competition from private healthcare institutions.

Meanwhile, to avoid cross-infection caused by crowd gatherings and due to the general decline in patients’ willingness to seek medical care, the service volumes of all hospital specialties have dropped significantly below original expectations. Departments with a higher risk of cross-infection will be particularly affected. This situation will compel hospitals to focus on refined and lean operational management.

Image from the Wanghai Kangxin HIA Data Platform

Not all sectors have been adversely affected by the pandemic. Internet healthcare, which has benefited from the outbreak, may influence the future revenue and expenditure structure of hospitals. The penetration rates of internet healthcare scenarios—such as online consultations, virtual follow-up visits, e-prescription outflow, and medical insurance settlement—have risen significantly during the pandemic. As patients appreciate the convenience these services offer, these models are likely to gain greater recognition and continue to be implemented in the future.

Following the end of the pandemic, healthcare informatization will usher in a wave of development, with advancements in 5G technology providing a foundational boost to these efforts.

As the commercial deployment of 5G continues to advance, 5G networks are poised to become the new generation of network infrastructure for China’s healthcare system. By integrating technologies such as informational connectivity and edge intelligence, 5G is expected to enable healthcare institutions to make optimal use of limited medical resources. It will provide patients with informatized, mobile, and remote services in disease diagnosis, monitoring, and treatment, thereby significantly bridging the supply-demand gap in the existing healthcare system.

The Impact of COVID-19 on Health Administrative Authorities and Healthcare Institutions

The outbreak initially placed a severe strain on the healthcare system, leading many to speculate whether the situation might have been different if it had occurred in a region with more abundant medical resources. However, Wuhan, the epicenter of the outbreak, is in fact one of China’s top-ranking regions in terms of healthcare resources. According to the “2018 Briefing on the Development of Health and Healthcare Services in Wuhan” released by the Wuhan Municipal Health Commission, the city had a total of 61 tertiary hospitals, including 27 Grade A tertiary (Class III Grade A) hospitals.

Image from the Wanghai Kangxin HIA Data Platform

Wuhan has a total of 6,340 medical and health institutions, an increase of 269 from the previous year. Among these, there are 398 hospitals, 5,853 primary medical and health institutions, and 79 specialized public health institutions. These medical institutions collectively have 95,900 inpatient beds, with 86.5 beds per 10,000 people, ranking among the top in China.

Wuhan is home to a considerable number of top-tier hospitals. According to the “2018 Fudan Version China Hospital Ranking” released by the Institute of Hospital Management, Fudan University, five hospitals from Wuhan were included in the top 100, placing them in the second tier. Among them, Tongji Hospital Affiliated to Tongji Medical College of Huazhong University of Science and Technology ranked 8th nationwide, and Union Hospital Affiliated to Tongji Medical College of Huazhong University of Science and Technology ranked 12th nationwide.

Regrettably, even such abundant medical resources proved quite fragile during this outbreak. The most evident manifestation was the severe strain on healthcare capacity—large hospitals were overwhelmed, leading to significant cross-infection, while primary care institutions were largely unable to fulfill their roles.

To address this intractable problem, relevant authorities implemented a range of measures. From promoting tiered diagnosis and treatment to constructing makeshift hospitals for centralized quarantine, these efforts gradually alleviated the strain on medical resources.

Primary healthcare institutions, which should have served as the first line of defense, failed to play their intended role during the pandemic. The primary reason lies in the siphoning effect exerted by large medical institutions, which has left primary healthcare facilities struggling, rendered tiered diagnosis and treatment merely formalistic, and resulted in poor practical implementation outcomes.

According to media interviews with staff at primary healthcare institutions in Wuhan, significant practical challenges persist in terms of human resources, funding, and materials, regardless of whether the model involves tertiary hospitals assigning physicians for targeted counterpart support or secondary medical institutions leading regional medical consortia that encompass multiple community health centers. Even the chronic disease management programs, which are primarily promoted by local primary healthcare institutions, have yielded suboptimal results in actual practice.

The paper “Reflections and Recommendations on the Modernization of the Disease Prevention and Control System,” jointly authored by the Expert Group on COVID-19 Prevention and Control of the Chinese Preventive Medicine Association, also highlights the current difficulties faced by primary healthcare institutions and the tiered diagnosis and treatment system.

The article points out that there is a shortage of primary healthcare workers, the general practitioner system is difficult to implement in rural areas, and most public health personnel are transferred from nursing staff, elderly medical workers, and village clinic staff. The level of primary medical services is low, technical capabilities are poor, and they fall far short of meeting the needs of the people.

Meanwhile, the “siphoning” of medical resources caused by county-level medical alliances and medical consortia is severe. This phenomenon not only diverts rural patient cases upward but also centralizes human, financial, and material resources at higher levels, rendering the legal person governance structure of primary healthcare institutions virtually ineffective and leading to poor work accountability.

In contrast, a substantial number of basic public health service programs and emergency response tasks for public health incidents are borne by the scant few public health workers and village-level healthcare personnel at the grassroots level, making it difficult to guarantee their workforce size, competency, and motivation. Unscientific performance evaluation systems compel institution heads to focus primarily on medical revenue and public health program metrics, leaving staff overwhelmed with administrative burdens and unable to fulfill the original intent of these initiatives.

Disease control and prevention institutions at all levels are facing the same predicament as primary healthcare institutions. As public welfare Category I institutions, their functional role is clearly defined by various laws and regulations as providing technical guidance and support, without administrative management or independent decision-making authority.

Zhong Nanshan, head of the high-level expert group of the National Health Commission and an academician of the Chinese Academy of Engineering, recently stated, “The status of the China CDC must be elevated, and it should be granted certain administrative authority. If no adjustments are made, outbreaks like this will occur again in the future.”

The article “Reflections and Recommendations on the Modernization of the Disease Prevention and Control System” also points out that the development of the disease prevention and control system has seriously lagged behind, and has even been marginalized during the healthcare reform process. The implementation of performance-based salary reform within the disease control system ultimately devolved into a new round of egalitarianism (“big pot rice”), severely dampening the motivation of disease control personnel, leading to the loss of professional talent and an influx of non-professional staff.

In 2014, the project funding allocated under the National “Special Public Health Task Fund” amounted to RMB 529 million; by 2019, this budget had decreased to RMB 450 million, representing a year-on-year decline of 14.9%. In contrast, fiscal appropriations to public hospitals stood at RMB 3.619 billion in 2014 and rose to RMB 5.023 billion by 2019, marking a year-on-year increase of 38.8%.

As original revenue streams for disease control and prevention institutions are gradually phased out, inadequate fiscal support in most regions has severely hampered their operations and led to significant staff attrition. Beyond the retirement of senior experts, the majority of those leaving are mid-career and young professional backbones, with a near-complete exodus of outstanding talents such as recipients of the Outstanding Youth Fund.

Undoubtedly, in the post-pandemic era, the state will tilt resource allocation toward primary healthcare institutions and disease control and prevention agencies. This includes strengthening primary healthcare facilities to enable effective tiered diagnosis and treatment, and optimizing institutional frameworks to grant disease control agencies their due administrative authority, thereby jointly advancing the development of an integrated and collaborative mechanism for basic public health services.

In Conclusion

After 2003, the process of medical informatization accelerated sharply. Hospital informatization systems, primarily based on Hospital Information Systems (HIS) and Clinical Information Systems (CIS), as well as a nationwide infectious disease surveillance network and later regional public health big data platforms, were gradually established.

Following this epidemic, we believe that sectors related to healthcare informatization will also experience significant acceleration, particularly those that have demonstrated their value during the outbreak and areas where China urgently needs to address existing shortcomings.

For instance, the acceleration of healthcare informatization will drive upgrades to healthcare systems. Furthermore, the analysis and support provided by big data platforms are essential for clinical assessment, allocation of medical resources, regional public health platforms, and the development of medical insurance databases. VCBeat will continue to closely monitor the field of new healthcare infrastructure and provide the latest reports; please stay tuned.

References

Wanghai Kangxin HIA Data Platform: Reflections on Hospital Operations During the COVID-19 Pandemic

Legal System and Society, August 2009: Improvements and Development of China’s Public Health Policies Since SARS

People's Health Network: Universal Coverage of Basic Medical Insurance: An Epic Leap from 0 to 1

Chinese Journal of Epidemiology: Reflections and Recommendations on the Modernization of the Disease Prevention and Control System

Yicai: Is Wuhan’s investment in healthcare insufficient? Its medical prowess ranks among the top!

Ba Dian Jianwen: How Did the First Line of Defense in the Wuhan Epidemic—Community Health Service Centers—Fall?

Caixin: Pandemic Exposes Weaknesses in Disease Control System; Zhong Nanshan Recommends Granting Administrative Authority

Cinda Securities: Outlook on Public Health Reform in the Post-COVID-19 Era

Securities Daily: New Infrastructure for Healthcare IT in the Post-Pandemic Era: Market Size Exceeds RMB 100 Billion, with Investment Expected to Further Increase