InnoCare Pharma, Co-Founded by Dr. Yigong Shi, Enters Final Three Days of IPO Subscription

InnoCare

Innovative Drug Developer

InnoCare, an innovative drug company co-founded by Dr. Shi Yigong, sparked intense discussion when it first applied for its IPO. In a few days, InnoCare is set to become another pre-revenue biopharmaceutical company listed in Hong Kong.

InnoCare’s IPO subscription opened on March 11, with three days remaining until the closing date. So, is InnoCare worth investing in? Is it merely riding the hype on Shi Yigong’s reputation, or does it truly have substantive strengths?

Based on our review of InnoCare’s prospectus and related materials, we present the following insights:

1. The core team members have an average of over 20 years of experience in related fields, with most having held key positions at international industry giants;

2. The Scientific Committee, led by Dr. Yi Gong Shi and Dr. Zemin Zhang, boasts strong expertise;

3. Morgan Stanley and Goldman Sachs Group served as joint sponsors, with 12 institutions subscribing to $160 million worth of shares;

4. The flagship product, the BTK inhibitor orelabrutinib, has the potential to be best-in-class; New Drug Applications (NDAs) for its two primary indications have been accepted by the Center for Drug Evaluation (CDE);

5. Additionally, there are two drug pipelines in clinical stages and six preclinical molecules, with a well-structured pipeline layout;

6. Ample cash reserves, sufficient to support corporate development for the next several years.

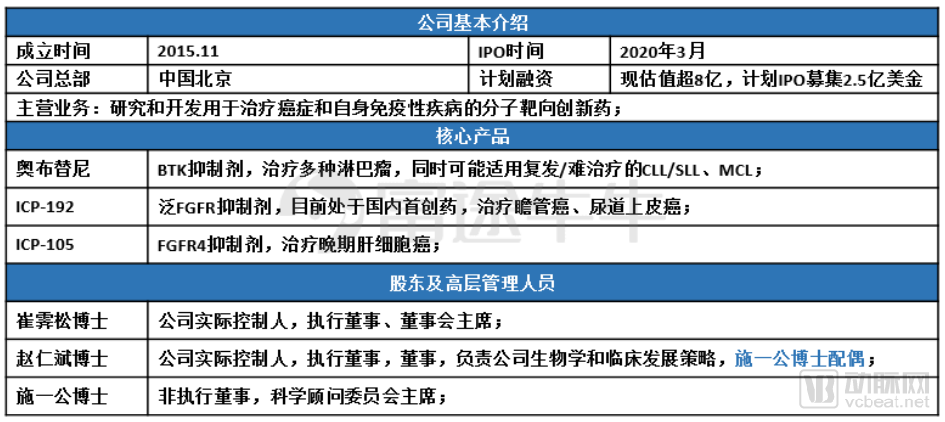

InnoCare Basic Information (Compiled by Futu Securities)

InnoCare is a clinical-stage biopharmaceutical company dedicated to the discovery, development, and commercialization of Best-in-Class and/or First-in-Class therapies for the treatment of cancer and autoimmune diseases.

InnoCare's Pre-IPO Financing History

Backed by a stellar team, InnoCare secured a total of $218.8 million in financing prior to its IPO. Its investor roster includes prominent biopharmaceutical investment firms such as Vivo Capital, CCB International Capital, and Lotus Lake Innovation Capital.

InnoCare’s listing is jointly sponsored by Morgan Stanley and Goldman Sachs Group. Previous projects jointly sponsored by these two investment banks include Xiaomi, Meituan, WuXi AppTec, and Innovent Biologics. Their renewed collaboration to support InnoCare provides additional assurance for the company’s public offering process.

On March 13, InnoCare added 12 cornerstone investors, including Vivo Funds, Golden Valley Global Limited (a USD fund under Zhengxingu), Hankang Biotech Fund, Miaocheng Group, Matthews Asia Funds (a fund under Soros), Rock Springs Capital Master Fund, Tiger Pacific Master Fund, Octagon Investments Master Fund, China Structural Adjustment Fund, Orient Sun Rise Global, Athos Asia Event Driven Master Fund, and WT Investment. The 12 institutions collectively subscribed for approximately US$164 million (approximately HK$1.28 billion) worth of shares, accounting for about 59.66% of the offered shares based on the mid-price, with a six-month lock-up period.

InnoCare’s ability to secure such substantial capital support is a testament to its distinct competitive advantages. For innovative drug development companies, the two most critical factors are undoubtedly the team and the pipeline of drugs under investigation.

Among the founding team of InnoCare, Dr. Shi Yigong, a renowned structural biologist in China, needs no further introduction regarding his distinguished career.

In October 2019, when InnoCare, a company less than six years old, filed its prospectus with the Hong Kong Stock Exchange, it sparked considerable controversy. Shi Yigong had previously stated in a speech that “encouraging scientists to start businesses is the straw that breaks the camel’s back,” arguing that “it is impossible for one person to simultaneously serve as a university professor, a corporate executive, and a financial manager.” Consequently, his own venture into entrepreneurship and subsequent public listing led many to question Shi Yigong, accusing him of falling prey to the “true fragrance” law (i.e., eventually succumbing to the very thing he once criticized). So, what is the actual situation?

In fact, although Shi Yigong is a co-founder of the company, he is not directly involved in its operations and management. Instead, he serves as Chairman of the Scientific Advisory Committee, providing guidance on the company’s R&D direction. In addition, Shi Yigong serves as a non-executive director of the company. Non-executive directors do not hold day-to-day operational roles; their function is primarily one of oversight, monitoring, and balance.

Therefore, Shi Yigong has not actually deviated from his original aspiration in conducting scientific research. In his most famous speech, he also stated that “we should encourage scientists and technologists to transfer their achievements and patents to enterprises, allowing them to participate through consulting or as scientific advisors.” Thus, Shi Yigong’s involvement in the founding of InnoCare aligns with his long-held views on the translation of scientific research into practical applications.

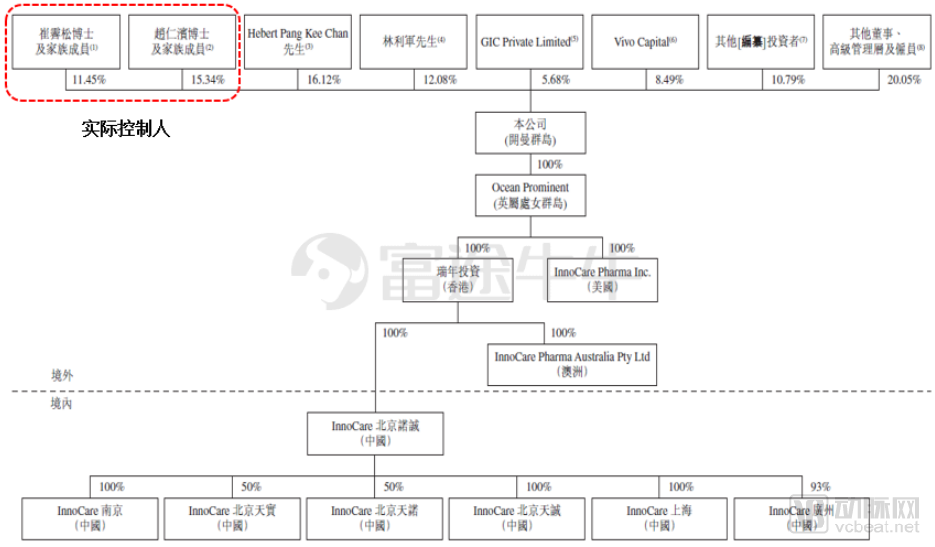

InnoCare's Shareholding Structure

The current actual controllers of InnoCare are its co-founder, Dr. Cui Jisong, and Dr. Zhao Renbin, the wife of Shi Yigong.

Zhao Renbin received his Bachelor of Science degree in Biological Sciences and Biotechnology from Tsinghua University in 1991. He studied under the same mentor as Shi Yigong, albeit two cohorts later. The two subsequently went to the School of Medicine at Johns Hopkins University in the United States to pursue their doctoral degrees, graduating in 1995.

In his subsequent career development, Zhao Renbin did not choose to stay at the university with Shi Yigong to devote himself to scientific research; instead, he opted to pursue a career in industry. From 2002 to 2008, he served successively as Senior Scientist, Researcher, and Chief Scientist at Johnson & Johnson. He later served as Director of Drug Discovery Biology at BioDuro, a subsidiary of PPD, where he accumulated extensive experience in clinical research.

Therefore, after joining InnoCare, Dr. Renbin Zhao served as the Company’s Executive Director and Executive Director of Biological and Clinical Development Strategy, fully leveraging his expertise.

Dr. Cui Jisong, another co-founder of InnoCare, has also dedicated many years to the pharmaceutical industry. After completing his postdoctoral research at the Howard Hughes Medical Institute, Dr. Cui joined Merck & Co. as the Head of the U.S. Early Development Team for Cardiovascular Diseases. He was later invited by PPD to serve as CEO and Chief Scientific Officer of its Chinese subsidiary, BioDuro.

Co-founding InnoCare with Dr. Shi Yigong, Dr. Cui Jisong also assumed the roles of Chairman of the Board and Chief Executive Officer, taking full charge of the company’s operations and management.

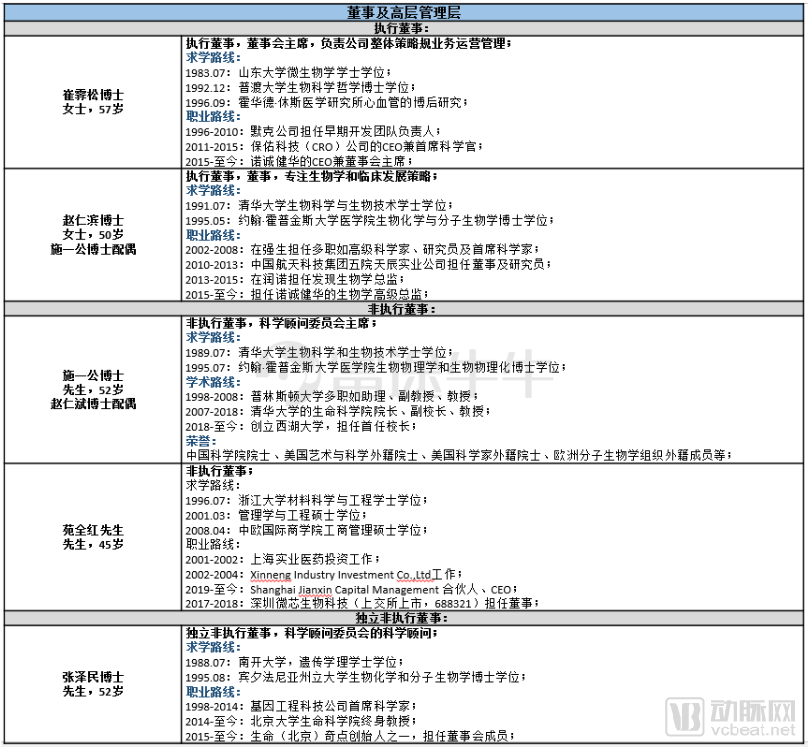

Other members of InnoCare’s management team have also accumulated more than 20 years of experience in their respective fields, having held key positions at pharmaceutical giants such as Roche, Pfizer, and Bristol-Myers Squibb.

In addition to the management team, InnoCare’s Scientific Committee is truly star-studded. Needless to mention Dr. Shi Yigong, it also includes Dr. Zhang Zemin, Deputy Director of the BIOPIC Center at the School of Life Sciences, Peking University, and former Chief Bioinformatics Scientist at Genentech and Roche; Dr. Li Zhanguo, Director of the Clinical Immunology Center/Department of Rheumatology and Immunology at Peking University People’s Hospital, and Director of the Institute of Rheumatology and Immunology; and Dr. Arnold J. Levine, Member of the U.S. National Academy of Sciences and the U.S. National Academy of Medicine, Permanent Honorary Professor at the Institute for Advanced Study, Princeton, and the co-discoverer of p53. Such a distinguished Scientific Committee has laid a solid technical foundation for InnoCare.

InnoCare’s Core Team (compiled by Futu Securities)

InnoCare's Main R&D Pipeline

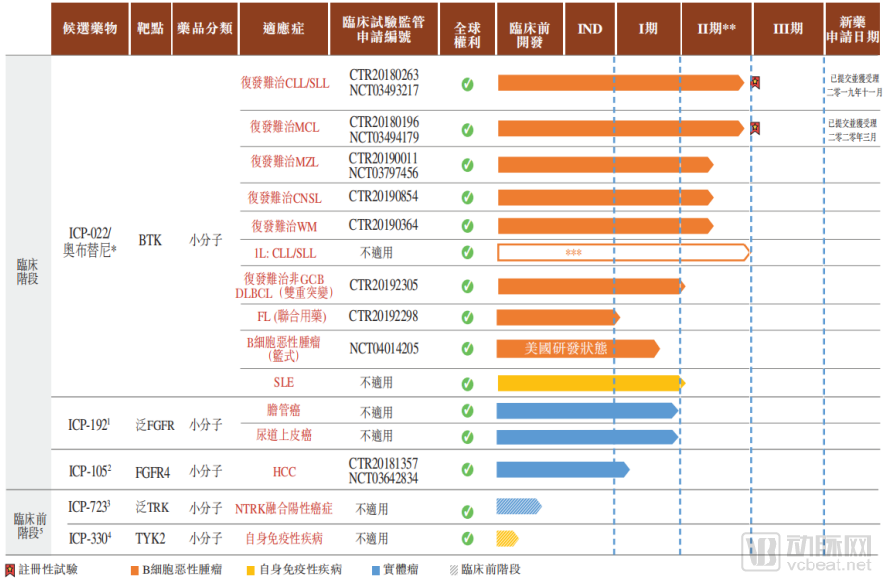

According to the disclosures in InnoCare’s prospectus, its pipeline currently comprises five major products under development, each targeting a different molecular target. Three of these products have entered the clinical stage, while the other two remain in the preclinical stage.

Its flagship product, orelabrutinib (ICP-022), is a novel BTK inhibitor with potential best-in-class status, indicated for the treatment of various B-cell malignancies and autoimmune diseases.

Major R&D Milestones of Orelabrutinib (Compiled by VCBeat)

To date, the research and development of orelabrutinib has progressed very smoothly, and the New Drug Applications (NDAs) for its two major indications have both been accepted by China’s Center for Drug Evaluation (CDE).

Ibrutinib, the world’s first BTK inhibitor, was launched in the United States as early as 2013. In 2019, its total sales reached $8.085 billion, representing a 30.3% increase from 2018 and maintaining its position as the best-selling tyrosine kinase inhibitor globally.

Because ibrutinib also has effects on some targets other than BTK, there has been ongoing global controversy regarding its specific mechanism of action. Some argue that its activity against these off-targets influences the drug’s efficacy, while others contend that it is precisely these additional targets that allow ibrutinib to stand out.

The announcement of the clinical trial results for orelabrutinib appears to have put an end to these debates. In December 2019, InnoCare presented Phase II clinical trial data on orelabrutinib in relapsed/refractory mantle cell lymphoma (R/R MCL) and relapsed/refractory chronic lymphocytic leukemia/small lymphocytic lymphoma (R/R CLL/SLL) at the 61st American Society of Hematology (ASH) Annual Meeting.

In R/R MCL, orelabrutinib achieved an ORR (overall response rate) of 85.9%, including a CR (complete response rate) of 27.3% and a PR (partial response rate) of 58.6%. In contrast, the final results of the comparable ibrutinib trial PCYC-1104 showed an ORR of only 68%, with CR and PR rates of 21% and 47%, respectively.

In R/R CLL/SLL, orelabrutinib also demonstrated significant efficacy and safety. The ORR among the 80 patients reached 88.8%, with an additional 5% of patients achieving stable disease, resulting in an overall disease control rate of 93.8%. Only 16 patients (20% of the total) experienced at least one severe treatment-related adverse event.

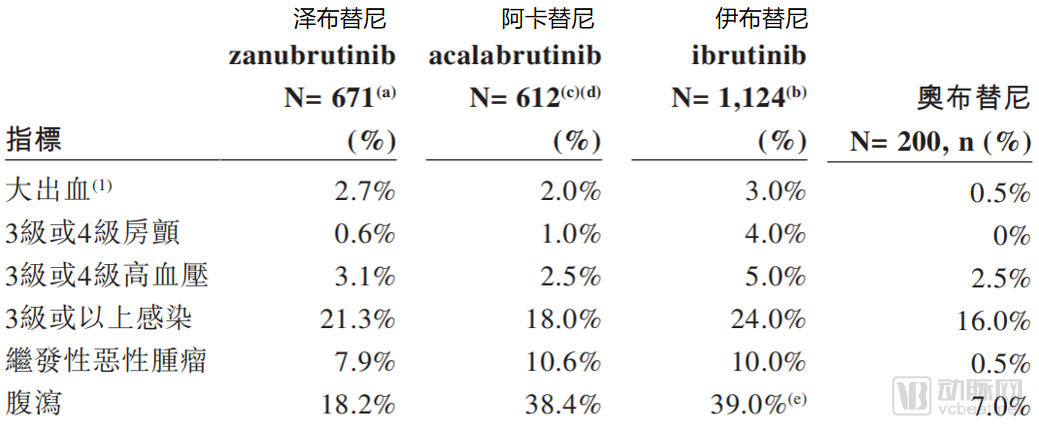

Comparison of Adverse Event Rates Among Four BTK Inhibitors

Compared with other BTK inhibitors, orelabrutinib’s greatest advantage lies in its superior safety profile. In a cohort of 200 patients, the overall incidence of adverse events associated with orelabrutinib was extremely low. Major bleeding and secondary malignancies, which are commonly observed with other drugs in the same class, were rarely reported in patients treated with orelabrutinib. The incidence of diarrhea was substantially reduced to 7%, compared with 18.2% for zanubrutinib, while the rate of grade 3 or higher infections decreased from approximately 20% to 16%. Thus, orelabrutinib has significantly improved upon the historical adverse event profile of BTK inhibitors, enabling patients to maintain a better quality of life during treatment.

In addition to filing for New Drug Application (NDA) approval in China, clinical trials for these two indications have also been initiated in the United States, with the potential for sequential market launches in both countries in the future.

InnoCare has already made advance preparations for the future production and sales of orelabrutinib following its market launch. The company is currently constructing a 50,000-square-meter manufacturing facility in Guangzhou, with an annual production capacity of 1 billion tablets, which is expected to be completed in the fourth quarter of 2020. Meanwhile, InnoCare has begun building its sales team, which is projected to expand to 80–90 sales representatives by the end of 2020.

For ibrutinib’s third major indication, WM (Waldenström’s macroglobulinemia), InnoCare has also initiated corresponding clinical trials, which have progressed to Phase II. InnoCare is actively expanding the indications for orelabrutinib to cover a broader range of B-cell lymphomas and, in the field of autoimmune diseases, investigating its therapeutic efficacy in systemic lupus erythematosus.

Although ibrutinib has been included in the National Reimbursement Drug List, its price of RMB 17,010 per bottle still requires mantle cell lymphoma (MCL) patients to pay approximately RMB 7,000 out-of-pocket each month. This expense remains a significant financial burden for most families. Therefore, if orelabrutinib can maintain reasonable pricing after market launch, it is well-positioned to challenge ibrutinib’s dominant position in the BTK inhibitor market, leveraging its superior efficacy.

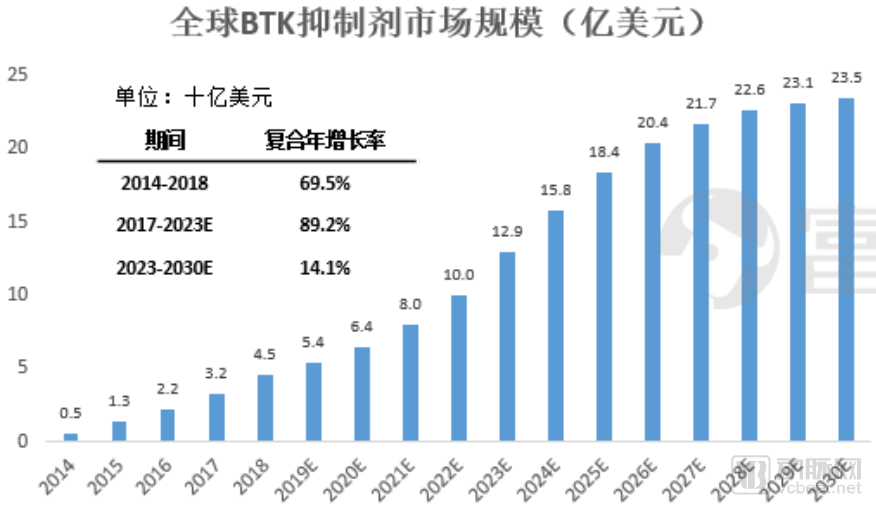

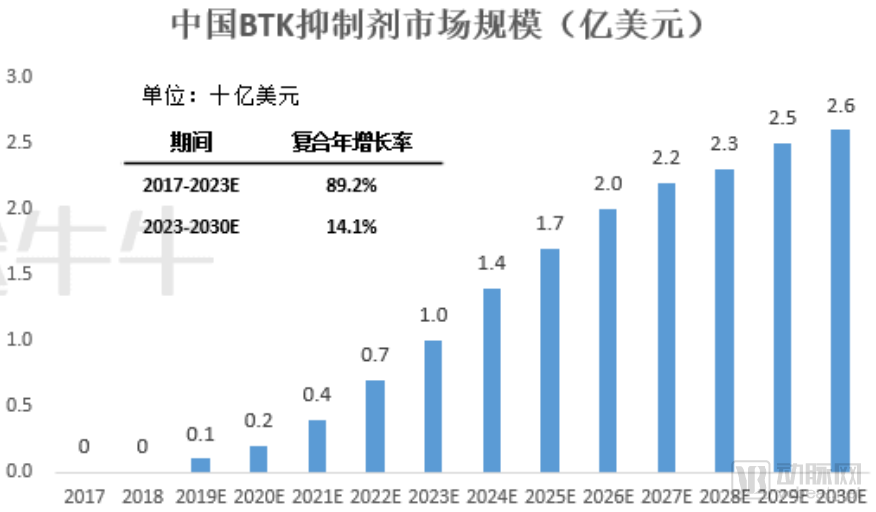

Data source: Frost & Sullivan, InnoCare prospectus, compiled by Futu Securities

According to Frost & Sullivan’s analysis, the global BTK inhibitor market is currently in a phase of rapid growth and is projected to peak at $2.35 billion by 2030. The domestic BTK inhibitor market in China remains in its early stages, with substantial room for future expansion. Orelabrutinib, which has already been submitted for marketing approval, has secured a certain first-mover advantage and is poised to claim a significant share in the future BTK inhibitor market.

ICP192 and ICP105 are two additional drug pipelines of InnoCare currently in the clinical stage, targeting pan-FGFR and FGFR4, respectively.

Global Pan-FGFR Inhibitors Under Development

Currently, no pan-FGFR inhibitors have been launched in China. Globally, only Janssen Pharmaceuticals’ Balversa (erdafitinib) was approved for marketing in April 2019. In China, ICP-192 is the pan-FGFR inhibitor with the most advanced clinical progress after erdafitinib. Moreover, in addition to the urothelial carcinoma indication for which erdafitinib has already been approved in the United States, ICP-192 is currently under investigation for cholangiocarcinoma.

Global FGFR4 Inhibitors Under Development

Regarding FGFR4 inhibitors, only InnoCare’s ICP-105 and CStone Pharmaceuticals’ CS3008 have entered clinical trials in China. Other drugs have not yet initiated clinical trials in the country. The few drugs currently in clinical development are primarily indicated for hepatocellular carcinoma.

In terms of its preclinical drug pipeline, InnoCare has developed six candidate drugs currently in the preclinical stage. Among these, ICP-723 and ICP-330 have largely completed their preclinical studies and are poised to enter the clinical development phase.

ICP-723 is a second-generation small-molecule pan-TRK inhibitor intended for patients with tumors harboring specific TRK mutations, with an Investigational New Drug (IND) application expected to be submitted in the first quarter of 2020; ICP-330 is a small-molecule inhibitor targeting TYK2 for the treatment of T cell-mediated autoimmune diseases, with an IND application expected to be submitted in the second half of 2020.

As evident from its drug pipeline, InnoCare has established a comprehensive and globally leading portfolio. This includes orelabrutinib, for which a New Drug Application (NDA) has been submitted; ICP-192 and ICP-105, which have entered clinical development; and ICP-723 and ICP-330, which are poised to enter clinical trials. The well-stratified progress across its various drug pipelines enables InnoCare to plan its future development goals in a structured manner, advance product launches and clinical applications according to a predetermined schedule, and allocate limited resources rationally among multiple initiatives.

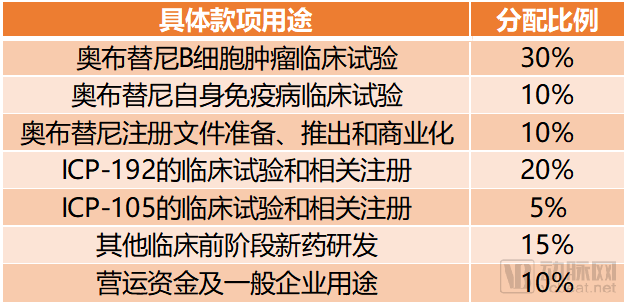

Based on the median issue price of HK$8.56, InnoCare will ultimately receive net proceeds of HK$1.99936 billion.

InnoCare’s Primary Use of Funds Raised (Compiled by VCBeat)

Of the funds raised by InnoCare in this financing round, the largest portion—50% of the total amount (approximately HK$1 billion)—will be allocated to uses related to orelabrutinib. Of the remaining funds, approximately 20% will be used for the regulatory filing and clinical trials of ICP-192, while only 5% has been allocated to ICP-105.

This also means that among InnoCare’s objectives for the next phase, the highest priority will be to advance the market launch of orelabrutinib while accelerating the development progress of ICP-192. The research and development of other products will continue to proceed as planned.

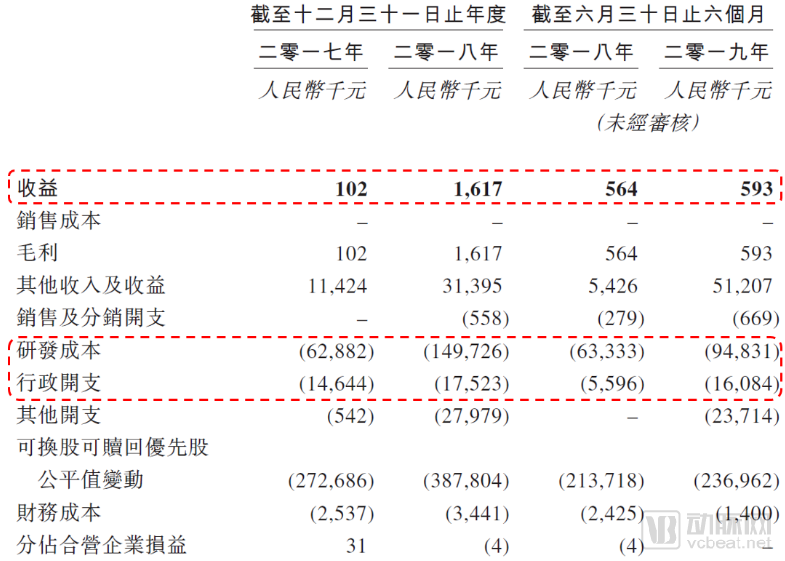

InnoCare's Key Financial Data

InnoCare is currently in the drug development stage and has not generated any revenue from product sales. Therefore, the company’s primary cost structure consists mainly of R&D expenses and administrative expenditures. As its product pipeline advances, particularly with the launch of Phase III clinical trials for orelabrutinib, InnoCare’s R&D spending may see further substantial growth in the future.

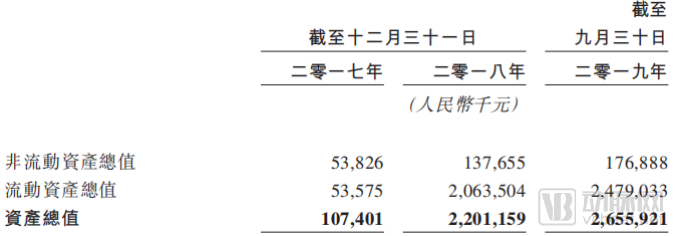

InnoCare's Asset Profile

Although substantial cash burn remains inevitable in the future, InnoCare is well-prepared. According to disclosures in its prospectus, as of September 30, 2019, InnoCare held total current assets of RMB 2.4 billion. Coupled with approximately HKD 2 billion raised through this IPO, these funds are sufficient to meet InnoCare’s capital requirements over the next several years.

Risk Warning

1) Investment in innovative drugs is characterized by long cycles, substantial capital requirements, and high uncertainty;

2) InnoCare focuses primarily on first-in-class and best-in-class drugs, thus venturing into more uncharted territories, which results in a higher failure rate compared to its industry peers;

InnoCare’s IPO Subscription Is Underway: Futu’s 4 Key Advantages for New Listings

0 Cash Subscription: Pledge HK stocks, US stocks, or A-share Connect assets to boost purchasing power; easily subscribe even with a fully invested portfolio and no cash on hand.

Margin Subscription: Leverage of up to 10x is available through margin financing (i.e., with a principal of 10,000, you can subscribe to new shares worth 100,000).

Ultra-Low Interest Rates: Annual interest rates for bank-financed subscriptions start as low as 1.6% (subject to minor adjustments based on funding conditions)

Grey Market Trading: Early Buying and Selling of New Shares via the Grey Market

For more IPO subscription strategies, contact Futu’s channel business manager via WeChat.

*Cover image source:InnoCare Prospectus