Nearly RMB 3 Billion Addressable Market: Prospectus of the Next-Generation SPR Technology Detection Platform

Surface Plasmon Resonance (SPR) technology, as a universal detection platform, is widely applied in fields such as drug screening and scientific research for the analysis of affinity, binding specificity, and quantitative concentration between biomolecules. However, molecular interaction analyzers based on this technology are characterized by complex structures and core technologies monopolized by foreign entities, resulting in high instrument costs and hindering their widespread adoption.

In 2019, China’s Liangzhun Xlement developed a new generation of 3D nano-SPR chips, achieving a technological breakthrough that significantly reduced the cost of existing applications, broke the foreign monopoly on molecular interaction analyzers, and opened up new consumer-end application scenarios.

Who are the potential users of the new technology? What is the actual market demand? How competitive is it among similar products?Based on extensive market research data, VCBeat Research has released the “Market Research Report on Next-Generation SPR Technology Detection Platforms,” aiming to provide industry participants with authentic reference information. This article is an excerpt from the report; you can scan the QR code below to download the full version for free.

1. Surface Plasmon Resonance (SPR) technology is ushering in a new generation of technological breakthroughs (3D Nano-SPR);

2. The new technology has significantly reduced the application cost of the original technology to approximately one-tenth of its previous level;

3. As a universal testing platform, the new technology has expanded application scenarios for consumer-end users;

4. The new generation of molecular interaction instruments based on 3D nano-SPR technology will break the monopoly held by foreign companies;

5. The new generation of molecular interaction analyzers is expected to reach a market size of 800 million yuan in 2022;

6. Home-use non-invasive rapid detection device based on 3D nano-SPR technology, with a potential market size of approximately RMB 2.2 billion.

1. SPR Technology Innovation Drives Down Costs of Detection Platforms

1.1. Introduction to SPR Technology

1.2. Applications of Traditional SPR Technology: Molecular Interaction Analyzers

1.3. Next-Generation Technological Breakthrough: 3D Nano SPR Chips

2. New-Generation SPR Technology Opens Up Consumer-Facing Application Scenarios

2.1. B-Side: A New Generation of Cost-Effective Molecular Interaction Analyzers

2.2. Consumer Market: Tapping into the Untapped Market for Home-Use Non-Invasive Rapid Diagnostic Devices

3. Demand Side: A Potential Market Size of Nearly 3 Billion

3.1. Market Research on Target Users

3.2. B-side Market Research and Analysis: Over 80% of Small and Medium-sized Pharmaceutical Companies Show Purchase Intent

3.3. Market Research and Analysis of the Consumer Sector: General-Purpose Platforms Offer Broad Application Scenarios

4. Supply Side: New Products Hold Significant Advantages Over Peer Competitors

4.1. The New Generation of B-End Molecular Interaction Analyzers Offers Exceptional Cost-Effectiveness

4.2. Consumer-Grade Home Non-Invasive Rapid Testing Devices Enable Off-Site Diagnostic Transfer

5. Summary and Outlook

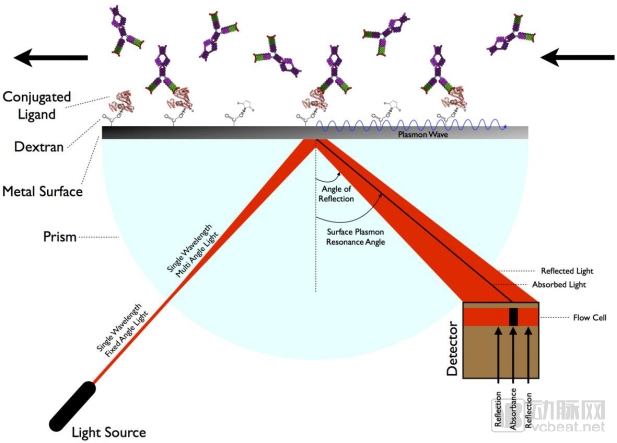

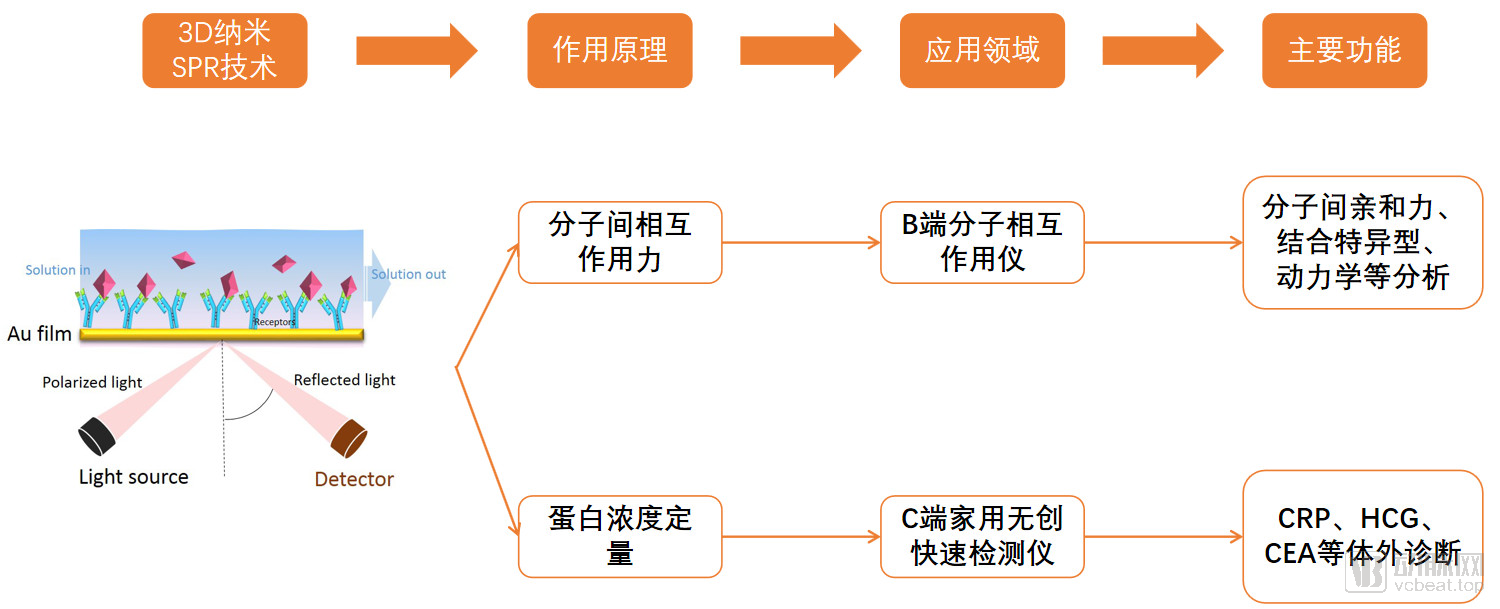

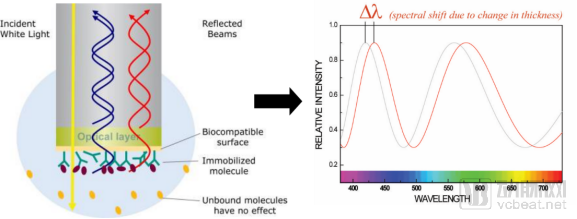

SPR is an optical sensing technology that involves three physical concepts:

Plasma: It is an electrically neutral substance composed of particles with different properties, such as cations, neutral particles, and free electrons, in which the positive and negative charged particles carry equal amounts of charge. It is the fourth state of matter, alongside solid, liquid, and gas.

Surface Plasmon Waves on Metal Surfaces: When incident light irradiates a metal surface, it induces longitudinal oscillations of valence electrons. The resulting charge density waves propagate along the interface between the metal and the dielectric, forming surface plasmon polaritons.

Evanescent Wave: refers to an electromagnetic wave generated on the side of the optically less dense medium when total internal reflection occurs as a light wave travels from an optically denser medium to an optically less dense medium.

As shown in the figure below, the optical path system is located beneath the metal surface, while the immobilized ligand proteins and the analyte are situated above the surface. The analyte flows over the metal surface in solution and interacts with the ligand proteins.

Figure 2: Schematic diagram of the SPR principle

Source: ACROBiosystems, VCBeat

A single-wavelength laser beam emitted from the light source below enters the prism (light green semicircle), resulting in multi-angle incidence of light onto the metal surface. Nearly all incident light is reflected, with one exception: when the angle of incidence reaches a specific value, the photon energy is absorbed by the metal and converted into surface plasmon waves, while an evanescent wave with exponentially decaying amplitude propagates within the metal medium.When surface plasmon waves on a metal surface resonate with evanescent waves, light at this angle will not be reflected out; this angle is referred to asResonance Angle。

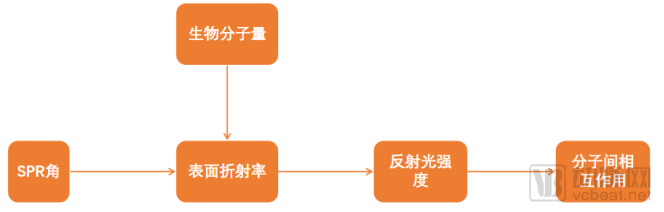

Surface Plasmon Resonance (SPR) is highly sensitive to the refractive index of the dielectric medium attached to the surface of a metal thin film. When the properties of the surface medium change or the amount of adsorbed material varies, the resonance angle shifts accordingly. Therefore, SPR spectra (changes in resonance angle vs. time) can reflect changes in substances interacting with the metal film surface.

Figure 3: Schematic diagram of the SPR conduction process

Source: VCBeat

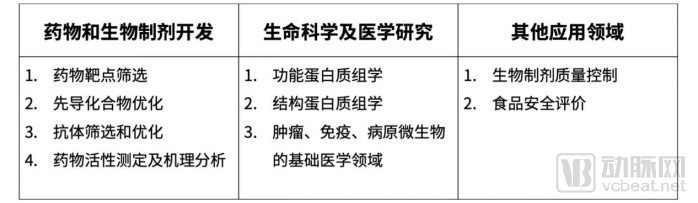

Molecular interaction analyzers based on traditional SPR technology are mainly used forAnalysis of Affinity, Binding Specificity, and Kinetics of Interactions Between Two Biomolecules, such as between small-molecule drugs and proteins or between antigens and antibodies, enabling real-time monitoring of the entire process of dynamic molecular interactions.

Figure 5: Primary Functions of the Molecular Interaction Analyzer

Source: VCBeat

R&D-focused pharmaceutical companies, CROs, universities, and research institutes are the primary users of this type of instrument.Widely used in the drug development phase, especially for drug screening and functional proteomics analysis.。

Table 1: Application Areas of Molecular Interaction Analyzers

Source: VCBeat

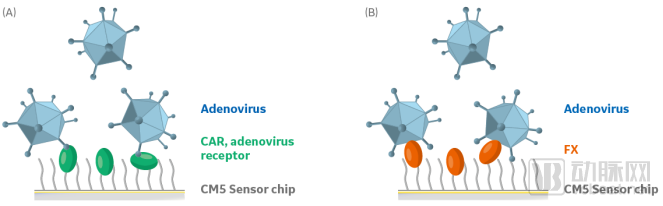

Furthermore,SPR technology can also be used for the quantitative detection of viral antigens.. There are two main technical principles: one involves the binding of viral particles to CAR receptors via viral fiber proteins; the other involves the binding of viral hexon proteins to Factor X (FX) protein. In this setup, either the CAR receptor or the FX protein is immobilized on a sensor chip, and detection is performed using a molecular interaction analysis system.

Figure 6: Schematic diagram of SPR quantitative detection of viral antigens

Source: GE Healthcare, VCBeat

During the global outbreak of the novel coronavirus (COVID-19), Biacore vigorously promoted its surface plasmon resonance (SPR) instruments for quantitative analysis of viral concentration, establishing them as an alternative to nucleic acid testing. With higher sensitivity, these instruments can effectively reduce the incidence of false-negative results associated with nucleic acid tests.

Molecular interaction analyzers based on traditional surface plasmon resonance (SPR) technology are widely used, but they have certain limitations. As they employ two-dimensional planar chips, signal data can only be collected in two dimensions. This necessitates complex and precise optical systems to capture weak signals, resulting in high instrument costs (over RMB 2 million per unit), making them affordable only for large enterprises or institutions.

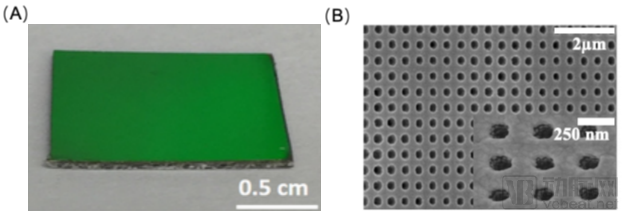

The greatest breakthrough of Liangzhun Xlement is transforming the optical chip from a two-dimensional base film to a three-dimensional base film, building upon the original SPR technology.

Figure 7: Two-dimensional chip for conventional SPR technology

Source: GE, VCBeat

The 3D-based membrane chip amplifies signals by more than a thousand-fold, delivering higher detection sensitivity and a lower limit of detection for molecular concentrations.. At the same time, there is no longer a need for traditional, complex optical path systems to capture weak signals; instead, simple LED light sources and photodiodes are used, which greatly simplifies the manufacturing process and thereby reduces costs.

Figure 8: Appearance and SEM structural images of the 3D nano-SPR chip

Source: Xlement, VCBeat

Furthermore, by leveraging 3D nanoscale surface plasmon resonance (SPR) technology, with a particular emphasis on its quantitative concentration analysis capabilities, it is possible to develop various types of ultra-sensitive biochips, thereby enabling the application of this technology in miniaturized, portable rapid-detection instruments.

II. In addition to molecular interaction analyzers, new technologies have also opened up consumer-facing application scenarios

3D Nano-SPR technology, as a universal detection technology platform, is widely applicable to various scenarios for detecting biomolecules. From the perspective of target users, it is divided into B2B applications and B2C applications. B2B applications are primarily based on the function of measuring intermolecular interactions, with end-users and application scenarios identical to those of traditional SPR technology, achieving import substitution with certain advantages.

Figure 9: Two Application Directions of 3D Nano-SPR Technology

Source: VCBeat

In terms of technical approach, traditional SPR technology employs two-dimensional planar chips, which can only collect signal data in two dimensions. This necessitates complex and precise optical systems to capture weak signals, making it impossible to develop miniaturized, lightweight home-use detection instruments, and it also lacks advantages in terms of detection cost.

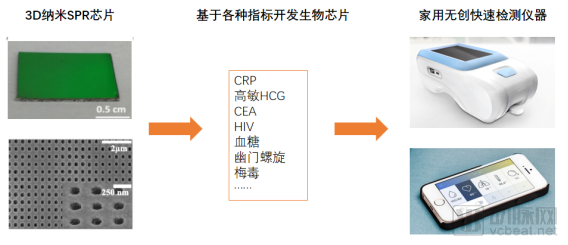

Compared with traditional SPR technology, the new generation of 3D nano-SPR technology significantly enhances signal acquisition capabilities. It eliminates the need for complex optical coupling devices to receive signals and enables spectral quantitative analysis using only conventional equipment, such as optical microscopes. This allows for the ultra-sensitive detection of various sample concentrations, thereby facilitating the development of miniaturized, lightweight, non-invasive, rapid home-testing devices targeted at consumer end-users.

Traditional SPR-based molecular interaction analyzers are prohibitively expensive (RMB 2–5 million per unit), limiting their adoption to large pharmaceutical companies, CROs, and select universities and research institutes. Consequently, numerous small and medium-sized pharmaceutical enterprises that require measurements of molecular interactions cannot afford to purchase these instruments directly.

A new generation of molecular interaction analyzers based on 3D nano-SPR technology, offering superior cost-effectiveness (<500,000 RMB/unit),It not only offers a degree of substitutability for existing products but also increases the likelihood of procurement by small and medium-sized pharmaceutical enterprises.

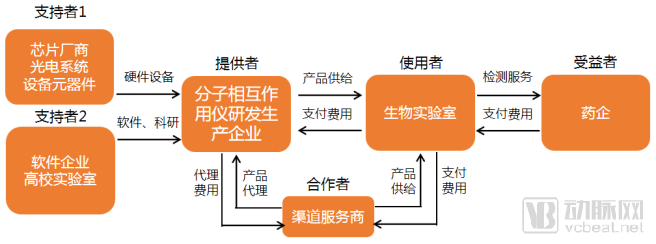

Figure 10: Market Stakeholder Relationship Map for Molecular Interaction Analyzers

Source: VCBeat

Users of Molecular Interaction Analyzers:R&D-focused pharmaceutical companies, CROs, and various laboratories in universities and research institutes, primarily used for detecting intermolecular interaction forces, conducting drug screening and scientific research, etc.

Beneficiaries of Molecular Interaction Analyzers:Pharmaceutical Companies, once the development of an innovative drug is successful, it may bring a new therapy for related diseases, or reduce the price of similar imported drugs, thereby capturing a larger market share.

Provider of Molecular Interaction Analyzers:R&D and Manufacturing Enterprise for Molecular Interaction Analyzers, providing users with instrument consumables and after-sales maintenance services.

Proponents of Molecular Interaction Analyzers:Hardware Service Providers and Software Developers, hardware service providers mainly offer hardware support such as chips, optoelectronic systems, and equipment components. Software developers primarily include software development companies and university laboratories, which provide operating systems and research support for instruments.

Collaborators of the Molecular Interaction Analyzer:Channel Service Provider, channel service providers offer channel agency services to manufacturers and developers of molecular interaction analyzers, helping products reach end users. Providers primarily distribute products through two channels: first, by selling directly to end users and collecting fees (direct sales); second, by distributing through channel service providers, leveraging their market resources for product expansion (distribution).

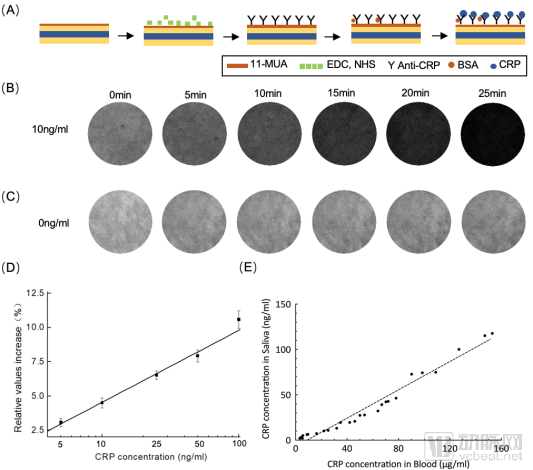

In addition to measuring intermolecular interactions, 3D nano-SPR technology can also achieve label-free quantitative protein detection.. Due to the fact that the sensitivity of new technology is three orders of magnitude higher than traditional SPR technology, it is easier to achieve ultra-low concentration protein quantitative analysis.

Figure 11: Quantitative Detection of Salivary CRP Concentration Using 3D Nano-SPR

(A) Schematic diagram of CRP antibody modification and quantitative CRP analysis; (B) Chip response changes when the CRP concentration in the saliva sample to be tested is 10 ng/mL; (C) Chip response changes for the negative control; (D) Correlation between chip signal intensity and CRP protein concentration in saliva samples; (E) Correlation between CRP protein concentrations in clinical blood and saliva samples.

Leveraging its label-free protein quantification capability, the 3D nanoscale SPR biosensor can be applied to the detection of various clinical samples in the biomedical field, such as plasma, urine, saliva, and cell tissues. Compared with classical methods including immunoturbidimetry, fluorescence immunoassay, and ELISA, the quantitative analysis method based on the 3D nanoscale SPR biosensor offers the advantages of rapidity, accuracy, and label-free operation, while simplifying sample pretreatment processes.

Miniaturization and lightweight design of instruments are one of the development trends in in vitro diagnostics, gradually extending from large hospitals to primary care facilities and then to home settings.The home-use non-invasive rapid detection device has realized part of the function of transferring diagnosis outside hospitals.The diagnostic market in large hospitals has become relatively mature, while primary healthcare institutions are experiencing rapid growth. Home-based non-invasive rapid testing may emerge as the next key direction for development.

Figure 12: Comparison between home-use non-invasive rapid testing devices and in-hospital diagnostic instruments

Source: VCBeat

Large-scale in vitro diagnostic instruments used within hospitals are suitable for high-volume, long-term operation and cover nearly all testing parameters. While they deliver accurate results, their accessibility is limited, requiring patients to make regular hospital visits. The high cost of testing makes them suitable for precise disease diagnosis.

In recent years, with the decentralization of medical resources and technological advancements such as microfluidics and single-test chemiluminescence, an increasing number of primary healthcare institutions have been equipped with mid-sized in vitro diagnostic (IVD) instruments. These facilities now provide initial and follow-up consultations for patients with common diseases at the primary care level, thereby gradually establishing a tiered diagnosis and treatment system.

Miniaturized, portable, non-invasive rapid home testing devices are suitable for prognostic management of diseases, particularly common and chronic conditions (such as the common cold, cancer, and cardiovascular and cerebrovascular diseases) that require regular monitoring and assessment. These tests can be completed at home or in community pharmacies at a low cost.

Figure 13: Various home-use, non-invasive, rapid diagnostic devices can be developed based on 3D nano-SPR technology

Source: Xlement, VCBeat

Taking the home-use saliva CRP detector developed by Xlement as an example, the concentration signal of high-sensitivity C-reactive protein (hs-CRP) in saliva is acquired via 3D nano-surface plasmon resonance (SPR) technology. Images are then captured by a digital camera attached to a conventional microscope, and machine learning-based image analysis software quantifies hs-CRP levels in saliva by analyzing transmittance changes in the red channel. This approach enables differentiation between viral and bacterial influenza and, in theory, can assist in identifying asymptomatic carriers of the novel coronavirus (COVID-19).

CRP: C-reactive protein (CRP) is an inflammatory marker, primarily used for the diagnosis and differential diagnosis of infections. Plasma CRP levels rise sharply when the body is subjected to infection or tissue injury.

hs-CRP: High-sensitivity C-reactive protein (hs-CRP) refers to the ultra-low concentrations ranging from 0.005 to 0.1 mg/L that can be detected, in contrast to conventional C-reactive protein assays (for example, hs-CRP levels in saliva are only one-tenth of those in blood, with a normal range of 1–5 ng/mL).

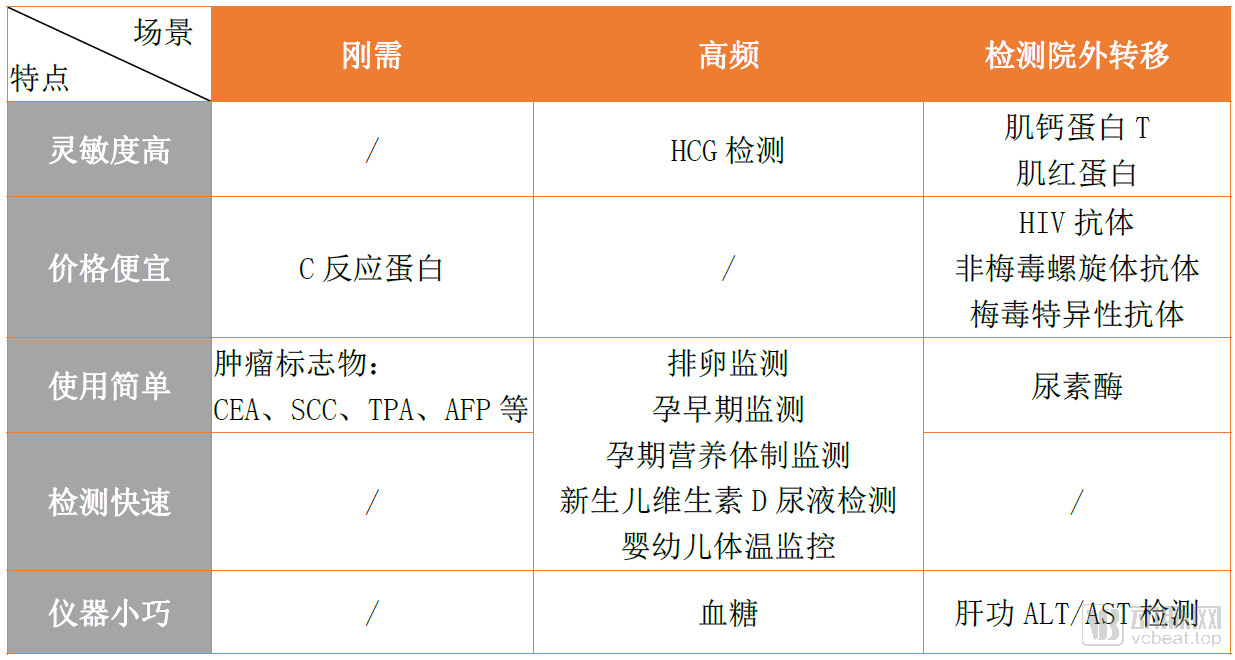

As a universal technology platform, 3D nano-SPR technology can be used to develop various other non-invasive rapid home-testing devices (based on different biochips) capable of detecting a wide range of biochemical markers, in addition to CRP.Integrating the five key features of 3D nanoscale SPR technology with the three major application scenarios—high necessity, high frequency, and detection of extra-hospital metastasis—the following commonly used testing indicators are all suitable for consumer-end applications.

Table 2: C-End Application Detection Metrics Matrix

Source: VCBeat

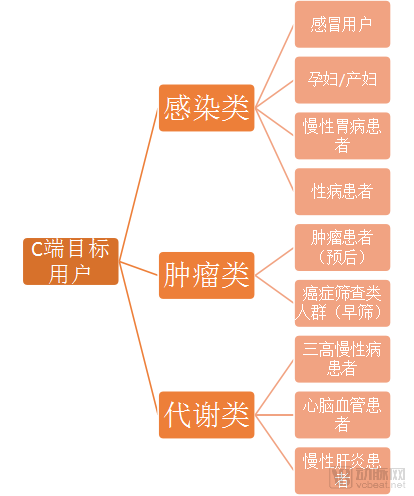

Based on the aforementioned diagnostic indicators, the disease spectrum is categorized into three major groups: infections, tumors, and metabolic disorders, encompassing patients with 12 specific diseases. These individuals constitute the target users for home-use non-invasive rapid diagnostic devices.

Figure 14: Target Users of Consumer-Facing Products

Source: VCBeat

Infectious Diseases: First, non-invasive testing for household-acquired infections (such as colds and fever caused by bacteria or viruses); second, HCG testing for pregnancy, including quantitative determination of pregnancy status and monitoring during miscarriage; third, testing for chronic gastric diseases; fourth, testing for sexually transmitted diseases such as HIV/AIDS.

Tumor Category: The primary focus is on postoperative management and prognosis for cancer patients, including regular follow-up visits to assess recurrence; the secondary focus is on early cancer screening, organized at the community or pharmacy level.

Metabolic: Early monitoring of cardiovascular and cerebrovascular diseases, such as myocardial infarction and cerebral infarction, based on existing biomarkers; additionally, chronic disease management for individuals with the "three highs" (hypertension, hyperglycemia, and hyperlipidemia) through monitoring of blood glucose and lipid levels.

The various compact diagnostic devices developed based on this technology fill a global market gap for home-use, non-invasive, rapid SPR detection instruments. As a versatile platform technology, it offers strong scalability and broad consumer-facing application scenarios. Furthermore, the new generation of molecular interaction analyzers for business clients provide exceptional cost-effectiveness and are poised to replace existing similar products, thereby increasing adoption rates.

Although the application scenarios for 3D nano-SPR technology are extensive at the qualitative level, the specific market size at the quantitative level and user acceptance remain to be determined. To address this, VCBeat Research conducted extensive surveys among B-end and C-end target users to gain insights into their actual needs, estimate market size, and gather feedback on new products.

To estimate the market size of next-generation 3D nano-SPR instruments, we first calculate the existing market capacity of traditional molecular interaction analyzers, and then assume the replacement rate and penetration rate of the new-generation instruments to assess the development prospects of 3D nano-SPR technology.

Existing Market Size of Traditional Molecular Interaction Analyzers

The existing market size refers to the total scale of instruments such as Biacore and ForteBio that have already been sold, calculated using the following formula:

Market Size = Total Number of Instruments × (Unit Price per Instrument + Annual Maintenance Unit Price + Chip Consumable Usage × Unit Price per Chip Consumable)

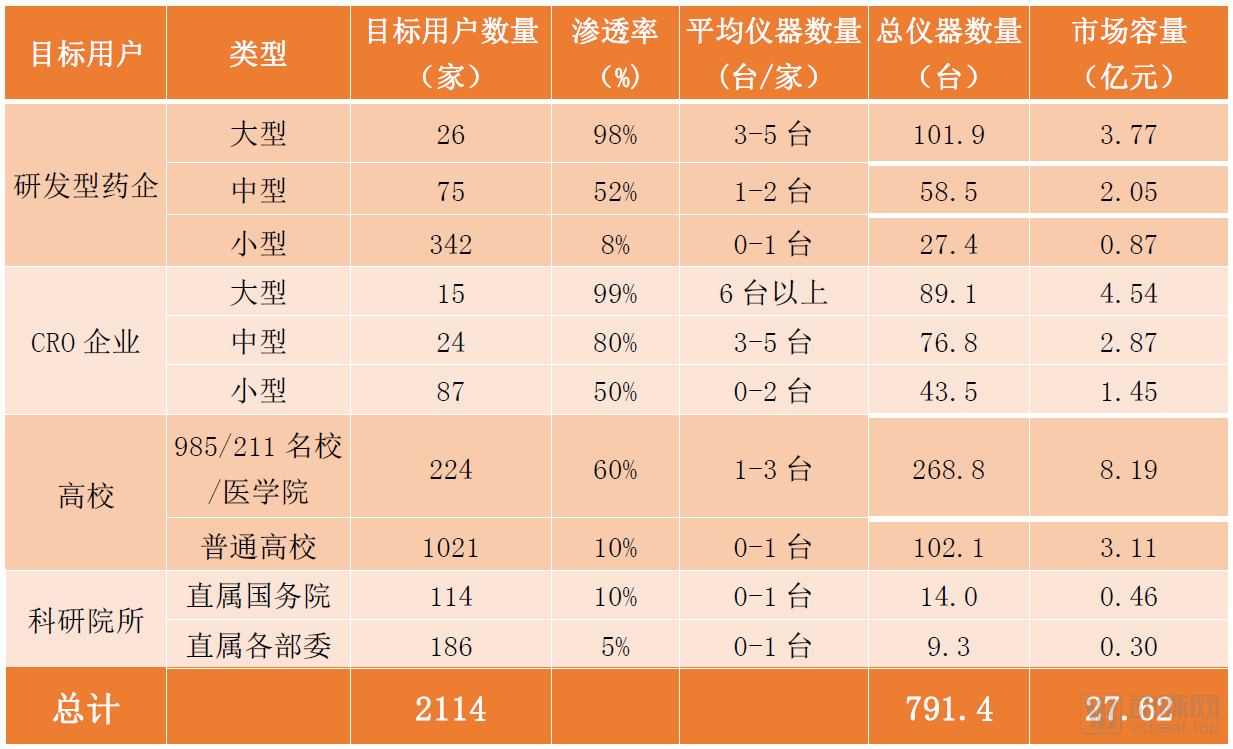

Total Number of Instruments= Number of Target Users × Penetration Rate × Average Number of Instruments; the penetration rate and average number of instruments for each type of target user were obtained through interview-based research, as detailed in the table below;

Unit Price of Instrument: The unit prices of mainstream instruments such as Biacore and ForteBio range from RMB 2 million to RMB 4 million;

Annual Maintenance Unit Price: The warranty period for instruments is generally 1–2 years, with annual maintenance and repair costs ranging from RMB 100,000 to 200,000 thereafter;

Chip and Consumable Usage: The consumption of chip-based consumables is primarily driven by experimental volume. Large pharmaceutical companies and CROs, which have high experimental throughput, require hundreds of chips per instrument annually. For instruments with lower utilization rates, annual chip consumption is typically less than 100 units.

Unit Price of Chip Consumables: The unit price of chips ranges from 2,000 to 6,000 yuan. The CM5 chip costs approximately 2,000 yuan per sensor chip, while the SA chip and biotin cap cost approximately 4,000 yuan per sensor chip.

Table 4: Market Size of Molecular Interaction Analyzers in China, 2020

Source: Corporate research, VCBeat

In 2020, the market size of molecular interaction analyzers in China was approximately RMB 2.76 billion, with an installed base of around 791 units. The two major brands, Biacore and ForteBio, accounted for more than 90% of the market share.

Potential Market Size of 3D Nano-SPR Instruments

As described in Chapter 2, Liangzhun Xlement has developed a new molecular interaction analyzer (Xlement SPR 100) based on 3D nano-SPR technology. This instrument offers exceptional cost-effectiveness and is designed to achieve two objectives: first, to partially replace mainstream instruments currently available on the market, such as Biacore and ForteBio; second, to increase penetration among small and medium-sized pharmaceutical companies, universities, and research institutes that previously lacked such instrumentation.

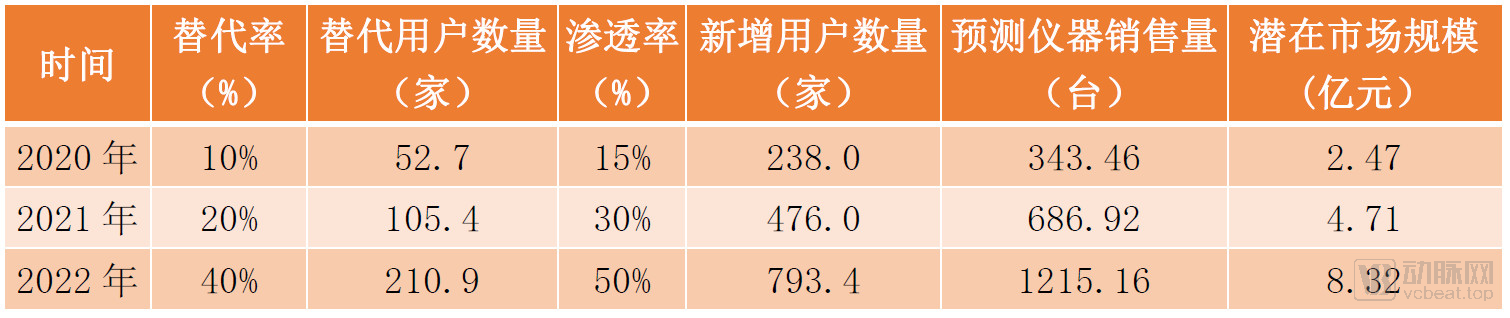

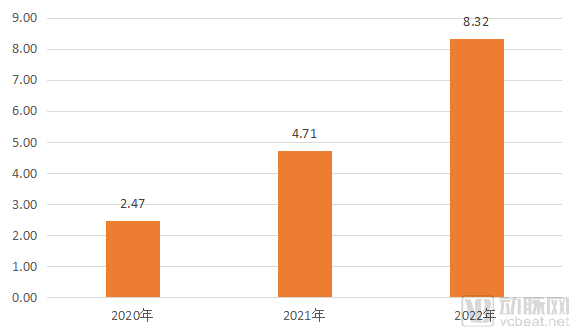

How large is the potential market size for 3D nano-SPR molecular interaction analyzers? According to Xlement’s strategic plan, VCBeat predictsBased on the replacement rate and penetration rate of new instruments over the next three years, the potential market size for Xlement SPR 100 is estimated to be RMB 250 million, RMB 470 million, and RMB 830 million, respectively.

Table 5: Estimated Potential Market Size for Liangzhun Xlement SPR 100 (CNY 100 million)

Source: Liangzhun XlemVCBeat

Potential Market Size = (Number of Existing Instruments × Replacement Rate + Number of Target Users Without Instruments × Penetration Rate) × (Unit Price of Instrument + Annual Maintenance Unit Price + Chip Consumable Usage × Unit Price of Chip Consumables)

Replacement Rate: Refers to the replacement of existing instruments by Xlement SPR 100;

Penetration Rate: Development of new users, including small and medium-sized pharmaceutical companies and universities that previously lacked molecular interaction analyzers;

Unit Price of Instrument: Specifically refers to the unit price of Xlement SPR 100, which is RMB 200,000–300,000 per unit;

Unit Price for Maintenance and Repair: CNY 10,000–20,000/year;

Chip Consumable Usage: Refer to the usage volume of existing instruments;

Unit Price of Chip Consumables: 3,000-4,000/sheet;

Figure 16: Estimated Potential Market Size of Xlement SPR 100 for the Next Three Years (RMB 100 million)

Source: Corporate Research, VCBeat

If Liangzhun Xlement officially launched the promotion of Xlement SPR 100 in 2020, the market size is projected to reach RMB 250 million in the first year, RMB 470 million in 2021, and RMB 830 million in 2022, representing a compound annual growth rate (CAGR) of 83%.

The estimation of the C-end market size follows the same core formula as that for the B-end: Market Size = Number of Target Users × Penetration Rate × Frequency × Average Transaction Value. The difference lies in the fact that C-end products have not yet been launched; therefore, data such as penetration rate and frequency can only be hypothesized based on research, ultimately yielding an estimate of the potential market size.

Number of C-end Target Users

Among target users for infection-related products, patients with the common cold represent the largest group. With an average of 1–2 colds per person annually across China’s population of 1.4 billion, there is a substantial user base. However, purchases of such home-use diagnostic devices are made at a minimum on a household basis, with one device per household. According to the China Statistical Yearbook 2019, the urban population in China reached 830 million by the end of 2018, and the average household size was three persons per household, implying approximately 280 million urban households.

In 2019, China had 14.65 million newborns, a figure roughly equivalent to the number of pregnant women or parturients. Additionally, there were 36 million patients with chronic gastric diseases and 958,000 people living with HIV/AIDS.

Table 6: Number of Target Users in the C-end Market (in ten thousands, as of December 2019)

In April 2019, a report released by the National Cancer Center revealed that in 2015, there were 3.929 million new cases of malignant tumors in China, with approximately 2.338 million deaths. On average, more than 10,000 people were diagnosed with cancer each day, equivalent to 7.5 people per minute. Source: VCBeat

There is a larger population of patients with metabolic diseases. The number of patients with cardiovascular and cerebrovascular diseases (including stroke and coronary heart disease, but excluding hypertension) has reached 45 million. This is followed by patients with chronic hepatitis, primarily chronic hepatitis B and chronic hepatitis C, totaling approximately 32.56 million.

Consumer Market Potential Size

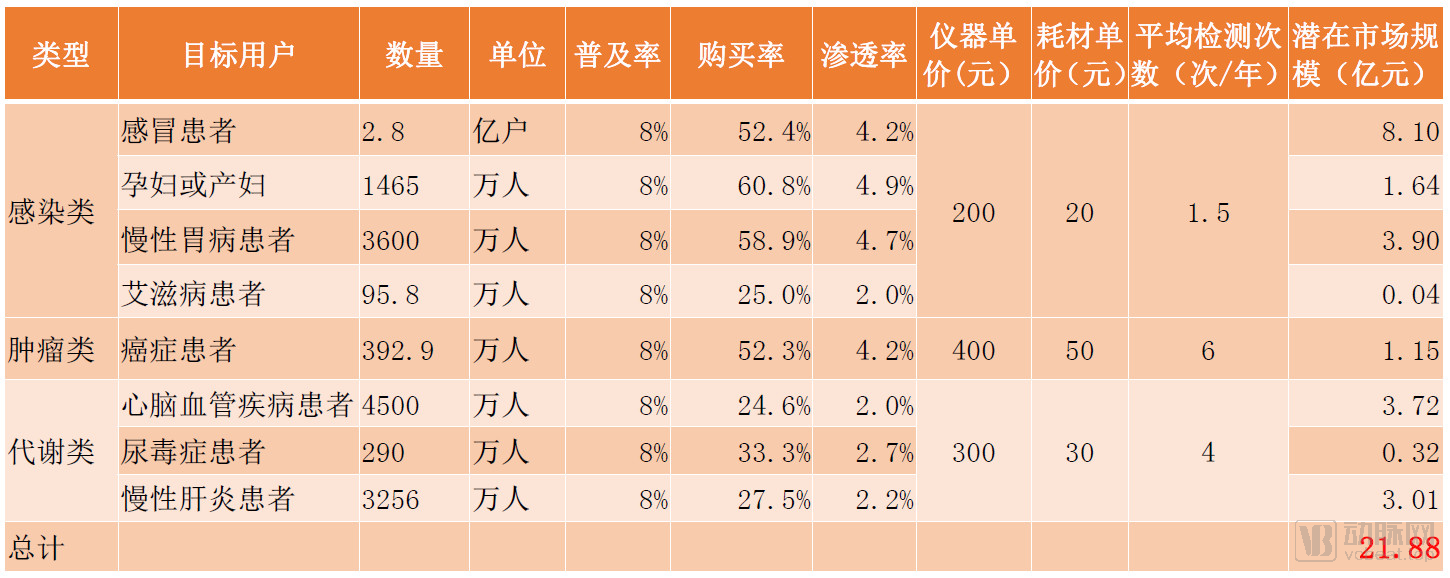

The first step in product sales is to make target users aware of the product's existence (Prevalence Rate), which is also one of the functions of marketing and promotion. VCBeat assumes that the penetration rate of new products will be around 8% in the next 2-3 years.

The second step is to understand how many users of this product are willing to purchase (Purchase Rate). Through questionnaire surveys, the purchase intentions of different user groups were obtained, with an overall purchase rate of approximately 50%. Pregnant or postpartum women exhibited the highest purchase rate (60.8%).

The unit prices of instruments and consumables, as well as the testing frequency, were all determined based on survey feedback, selecting the average price with the highest acceptance rate. Instruments and consumables for infectious diseases have the lowest prices, followed by those for metabolic disorders, while oncology-related products are the most expensive. Moreover, oncology tests also have the highest frequency (averaging six times per year), resulting in a higher revenue per customer.

Consumer Market Potential = Target User Base × Penetration Rate × Purchase Rate × (Unit Price of Device + Unit Price of Consumables × Number of Tests)

Table 7: The potential market size for the consumer segment is approximately RMB 2.2 billion

Source: VCBeat

Based on calculations,The potential market size for the consumer segment is approximately RMB 2.2 billion, comprising RMB 1.37 billion for infectious diseases, RMB 710 million for metabolic disorders, and RMB 120 million for oncology.. The most important segments are the markets for patients with common colds and those with cardiovascular and cerebrovascular diseases. The core reason is that these markets have a very large patient base.

Consumer Willingness to Purchase Home-Use Non-Invasive Rapid Diagnostic Tests

To assess target users’ willingness to purchase the detector product, VCBeat designed seven relevant questions in its questionnaire. The following is a detailed analysis of each question:

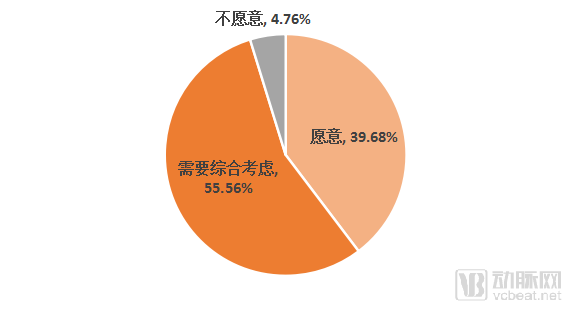

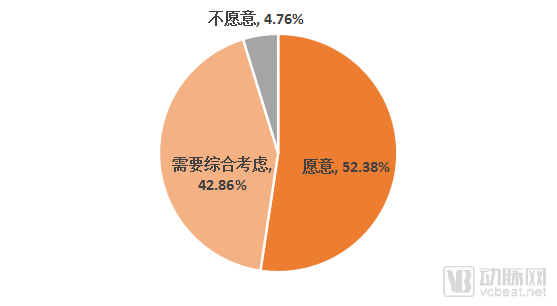

(1) If there were a testing device that could measure CRP levels using saliva at home, helping to determine whether one is an asymptomatic carrier of the novel coronavirus, would you be willing to purchase one for your household? (Assuming the device costs approximately 200 yuan, and the consumable cost per test is 30 yuan.)

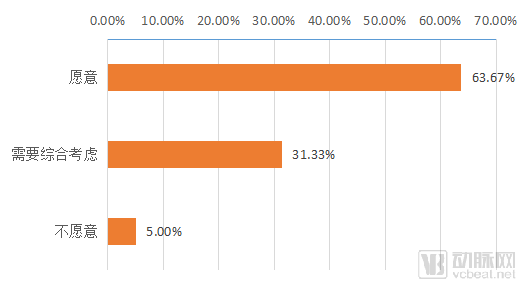

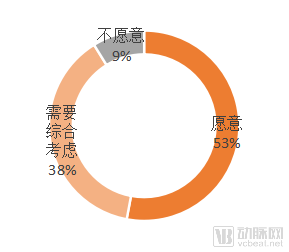

Approximately 40% of users indicated a willingness to purchase., 60% indicated that they needed to consider various factors comprehensively or were unwilling. Their main concerns included the belief that the pandemic would end soon and difficulties in operating instruments.

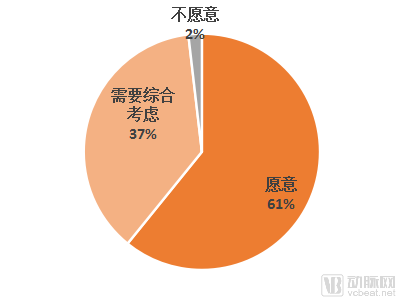

(2) After the pandemic ends, if you develop cold-like symptoms and have the aforementioned devices at home (which can distinguish between viral and bacterial colds and detect latent SARS-CoV-2 infection), would you use them for home testing?

After the end of the pandemic,52% of users expressed willingness to continue using the device for home testing and to recommend it to friends and family.. 43% of users believe that the performance indicators of this instrument are still under comprehensive consideration.

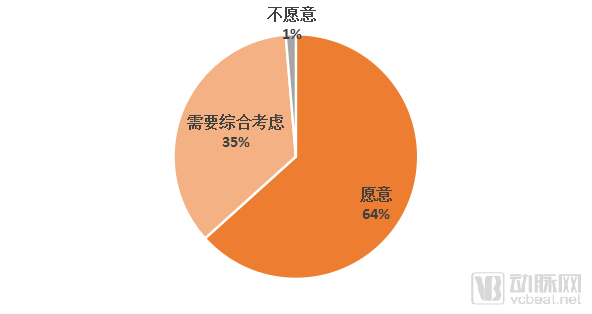

(3) Pregnant women in the early stages of pregnancy are required to visit the hospital weekly for venipuncture to measure HCG levels and assess whether the fertilized egg is developing normally. If there were a product that could complement hospital-based HCG testing by allowing daily self-monitoring of HCG growth trends via saliva at home, would you consider purchasing it?

Pregnant women exhibit a strong core drive toward fetal health,This item demonstrates a very high purchase intent (61%), with only 2% of users explicitly stating their unwillingness to purchase.

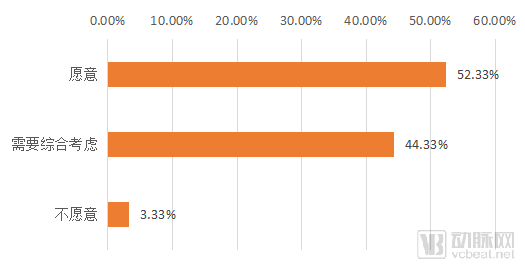

(4) If a pharmacy near your residence offers a device capable of self-testing via fingerstick blood samples and provides test results equivalent to those of hospital-based complete blood count (CBC) analyses (which can be directly used by physicians for prescribing, eliminating the need for a hospital visit), would you be willing to accept remote medical consultation for common colds and fever, with prescriptions issued based on the CBC results from the pharmacy?

This question is similar to Question 2, except that the testing is conducted at nearby pharmacies, and the results issued are consistent with those from hospitals, allowing them to be used directly for physicians to write prescriptions. The proportion of users willing to purchase has increased significantly, reaching 64%.Whether diagnostic results are recognized by medical institutions is one of the key factors influencing purchase intention.

(5) Post-operative follow-up for cancer is a necessary management strategy. If there were a home-use device that allowed patients to self-monitor the trend (declining, stable, or rising) of cancer-specific biomarkers using fingerstick blood samples once a week, thereby enabling early detection of recurrence risk, would you consider purchasing it? (Assuming the cost is within your financial means.)

(6) If a self-service testing device were available at community health service centers or residential property management offices, enabling you or your family members to self-test for cancer biomarkers using a finger-prick blood sample (with results recognized by hospitals), would you be willing to use this product? (Assuming the cost is within your financial means.)

(7) If there were a portable testing device that allowed you to perform such metabolic tests at home (for chronic disease management monitoring and disease risk assessment), would you be willing to purchase this product/service? (Assuming the cost is within your financial means)

Overall, Questions 1–4 pertain to infectious disease products, Questions 5–6 to oncology products, and Question 7 to metabolic disease products.Product promotion strategies are categorized into two models: D2C and B2B2C.D2C refers to products used at home, while B2B2C involves placing products in nearby pharmacies, community health service centers, and residential property management offices, where patients gather to use them.

Based on the feedback regarding purchase intent, users demonstrate a higher acceptance of the B2B2C model compared to the D2C model.

Key Considerations for Product Purchasing

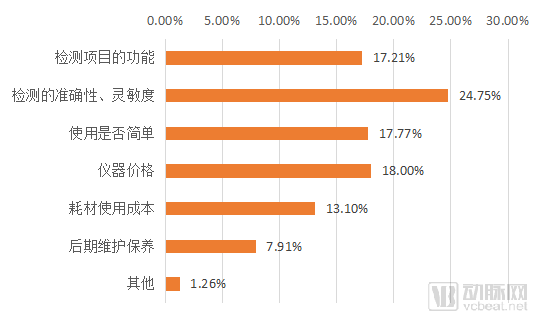

To investigate the primary factors users consider when evaluating instruments, a multiple-choice question was included in the questionnaire: “If you were to purchase this type of instrument, what factors would you primarily consider? (Select all that apply)”

The options primarily focus on instrument performance, instrument price, ease of operation, cost of use, and maintenance. Among the 1,000 valid questionnaires, there were a total of 3,022 responses (multiple-choice questions).

Figure 26: Factors Considered by C-End Consumers When Purchasing Products

Source: VCBeat

Users’ primary consideration is the accuracy of the device, accounting for 25%; this is followed by the price and testing capabilities of the device; the third consideration is the ease of operation (17.7%), as ordinary users may lack professional medical knowledge; finally, other factors such as consumable costs and maintenance are also taken into account.

Chapter 3 provided a detailed discussion of the demand side; this chapter will examine the supply side, analyzing existing solutions for both B-end and C-end application scenarios. It will conduct a comparative analysis of competing products across three dimensions: product performance, technological advantages, and market strategy.

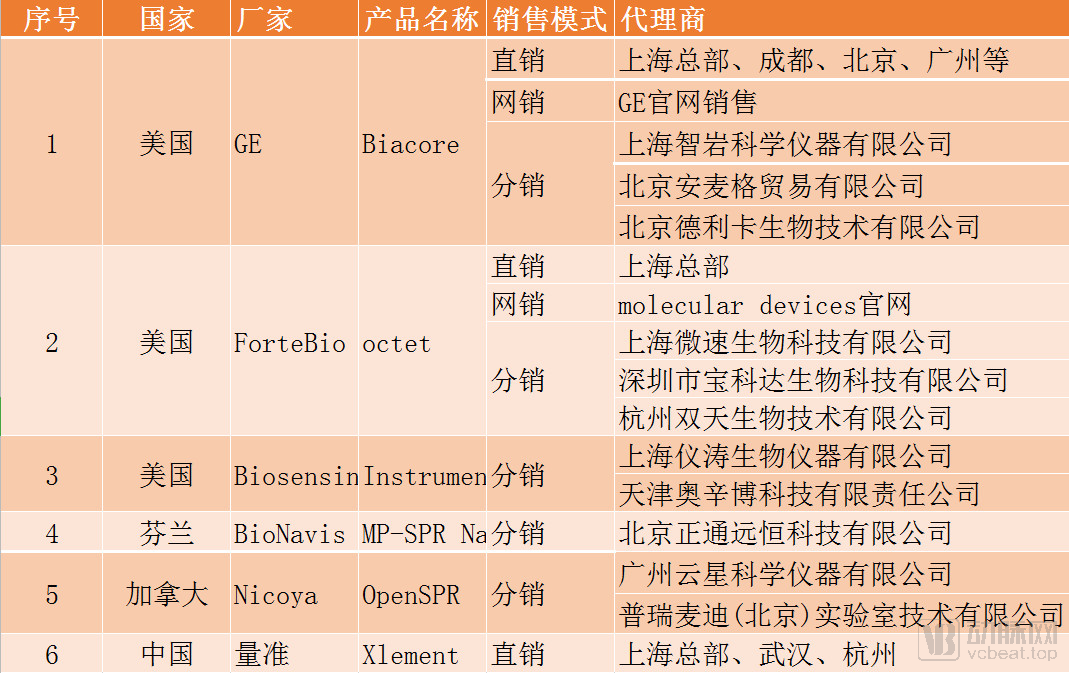

There are nearly 10 brands of molecular interaction analyzers for the B2B market worldwide, such as GE Healthcare’s Biacore (USA), ForteBio’s Octet, and Nicoya’s OpenSPR (Canada). Although these instruments offer similar functionalities, they employ different technological principles, leading to variations in performance and application scenarios.

Product Performance Comparison

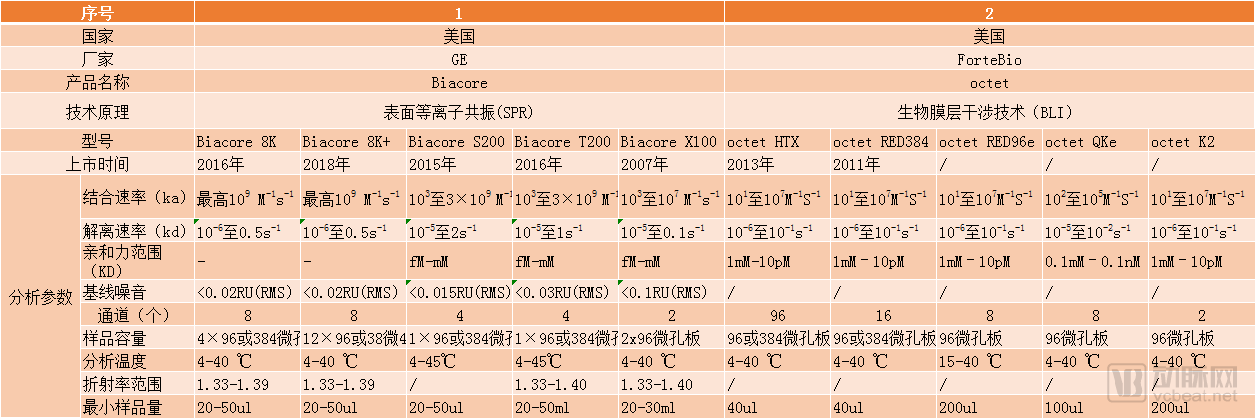

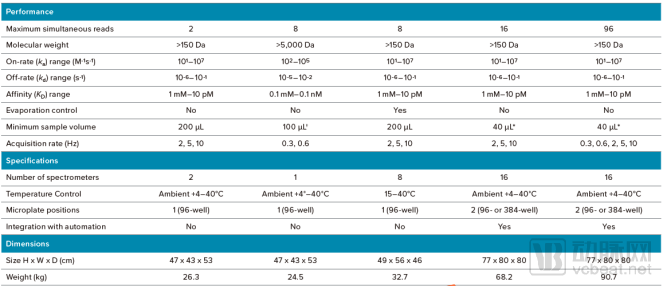

Currently, the domestic market for molecular interaction analyzers is still dominated by imported products. Here, we list the six most representative product lines, comprising a total of 20 models: three from the United States (Biacore, ForteBio, and Biosensing), one from Finland (BioNavis), one from Canada (Nicoya), and one from China (Liangzhun Xlement).

Table 8: Performance Comparison of Six Molecular Interaction Analyzers

Source: Product manuals of respective instruments, VCBeat.

Biacore: The Gold Standard for Molecular Interaction Analysis

In 1990, Biacore AB of Sweden developed the first commercial instrument based on SPR technology—the Biacore—which was later acquired by GE.

Figure 27: Five Biacore Products Currently on the Market

Source: GE Official Website, VCBeat

After 30 years of development, Biacore has become the gold standard for label-free molecular interaction analysis. It offers a diverse range of models, including five products: Biacore 8K/8K+, Biacore S200, Biacore T200, and Biacore X100. The lower limit of detection for molecular weight ranges from 100 Da to unlimited, enabling broad applications in pharmacology, antibody and vaccine screening, and protein research. However, due to the relatively complex optical system, the instruments are very expensive, with high subsequent maintenance costs. Currently, purchases are predominantly made by leading institutions such as multinational pharmaceutical companies, contract research organizations (CROs), and university biological laboratories.

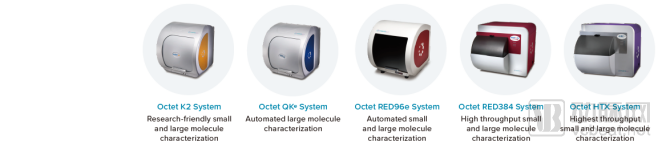

ForteBio: High-Throughput Screening

ForteBio’s Octet platform is based on the principle of Bio-Layer Interferometry (BLI), detecting molecular interactions through phase shifts in interference wavelengths on the biosensor surface. Current models include the Octet series: HTX, RED384, RED96e, QKe, and K2. The detectable molecular weight range spans from 2 kDa to 100 kDa.

Figure 28: Five ForteBio Products Currently on the Market

Source: Fortebio Official Website, VCBeat

Fortebio's core advantage lies in its high throughput., enabling rapid primary screening of 96 or 384 samples simultaneously. The latest product, Octet HTX, features 96 channels, far surpassing the 4- or 8-channel capacity of competing products. However, ForteBio has limitations in molecular weight detection and cannot effectively detect interactions involving small molecules.Suitable for screening macromolecular antibody vaccines, but less suitable for screening small-molecule drugs or peptide drugs.

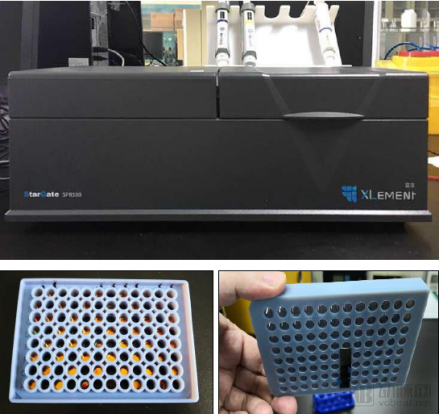

Liangzhun Xlement SPR 100: A New Generation of Breakthrough Technology

In 2019, Xlement launched the Xlement SPR100, a biomolecular interaction analyzer equipped with novel nanoplasmonic optical sensors, achieving a breakthrough in import substitution for products of its kind.

Figure 29: Liangzhun Xlement SPR10 Instrument

Source: Xlement, VCBeat

Compared with similar products,Xlement SPR100 Features Three Distinct AdvantagesFirst,Unbeatable Value for Money, at only one-tenth of the market price of Biacore systems, with lower costs for chip consumables and maintenance compared to similar products; secondly,Rich Instrument Functions, capable of performing 80% of the detection functions of Biacore and covering all functionalities of the Tecon microplate reader; thirdly,Unlimited Optimization Potential, its integrated NanoSPR chip, as a universal platform technology, enables the development of various ultra-sensitive biochips for application in diverse scenarios.

Other Representative Products

In addition to the three instruments mentioned above, Nicoya’s OpenSPR from Canada employs a novel Localized Surface Plasmon Resonance (LSPR) technology. Its key advantages include ease of operation, rapid result generation, and straightforward instrument maintenance. The detection is unaffected by temperature or buffer refractive index, enabling the analysis of molecules with molecular weights above 90 Da. It allows for the rapid completion of real-time Co-IP assays within 2–3 hours.

Figure 30: Three Other Molecular Interaction Analyzers

Source: VCBeat

Finland-based BioNavis has launched four models in its Navi series, based on the Multi-Parameter Surface Plasmon Resonance (MP-SPR) principle. MP-SPR expands the range of substrates from traditional gold, dextran, and other polymer films to include cellulose, PS, PET, PMMA, SiO2, and more. Furthermore, while conventional SPR is limited to measuring sample layer thicknesses of less than 150 nm, MP-SPR breaks through this limitation, enabling the measurement of sample layers with thicknesses up to several micrometers.Enables the measurement of living cell monolayers。

U.S.-based Biosensing has ingeniously integrated SPR technology with optical microscopy to launch the MP-SPR Navi series of biosensing detectors. This instrument canSimultaneously obtain in situ bright-field imaging of cells, SPR imaging, and quantitative data from SPR kinetic curves, including affinity constants and association/dissociation rate constants.

Comparison of Technical Principles

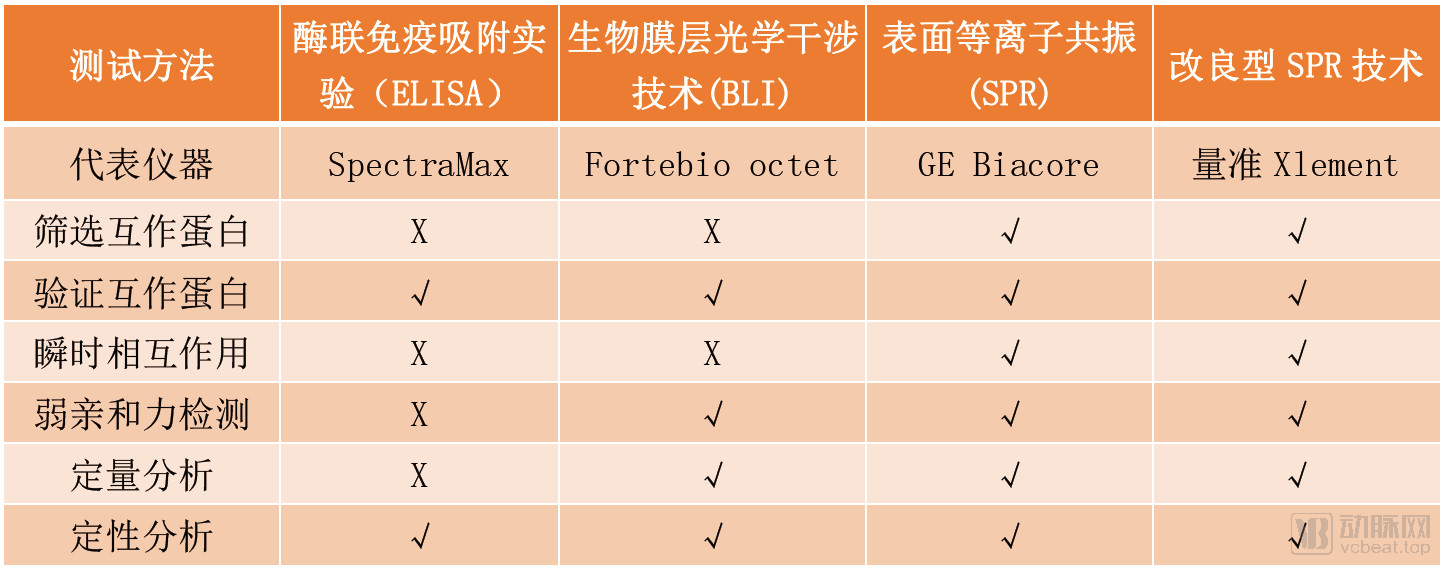

In terms of technical principles, the mainstream methods for measuring intermolecular interaction forces are currently divided into four categories:Enzyme-Linked Immunosorbent Assay (ELISA), Bio-Layer Interferometry (BLI), Surface Plasmon Resonance (SPR), and modified SPR technologies (e.g., NanoSPR).

Among the six products mentioned above, except for ForteBio, which employs Bio-Layer Interferometry (BLI) technology, the other five products all utilize Surface Plasmon Resonance (SPR) technology. Specifically, Biacore adopts conventional SPR technology, while the remaining four products feature improved SPR technologies.

Table 9: Comparison of Representative Instruments and Performance of Four Technologies

Source: VCBeat

SPR technology has been analyzed in detail in Chapter 1; here, we briefly introduce the principles of Enzyme-Linked Immunosorbent Assay (ELISA) and Bio-Layer Interferometry (BLI).

Enzyme-Linked Immunosorbent Assay (ELISA): ELISA is a commonly used immunoenzymatic technique. The primary method involves adsorbing known antigens or antibodies onto the surface of a solid-phase carrier, followed by incubation with enzyme-labeled (conjugated) antibodies or antigens. A chromogenic substrate is then added to produce a color reaction. The difference in color intensity between the test sample and the standard is measured using a microplate reader, and an enzyme activity curve is plotted to determine the concentration of the analyte.

Bio-Layer Interferometry (BLI): BLI detects biomolecular interactions based on wavelength shifts in interferometric spectra. When a beam of visible light is emitted from the spectrometer, two reflected beams are generated at the two interfaces of the optical film layer at the sensor tip, producing an interference spectrum. Any changes in the thickness and density of the film layer resulting from molecular binding are reflected by the shift value of the interference spectrum.

Figure 31: Schematic diagram of the principle of Bio-Layer Interferometry (BLI)

Source: Shuangtian Bio, VCBeat

Compared with the first two technologies, SPR technology offers numerous advantages. It enables real-time, label-free monitoring of the dynamic process of reactions, yields cleaner and more accurate experimental data, and provides better reproducibility and stability. Furthermore, SPR technology boasts higher sensitivity and can detect a broader range of affinities; the Biacore S200 system, for instance, is capable of detecting samples at levels as low as 0.015 RU (resonance units).

Market Strategy Comparison

In addition to strong product performance, market strategy is also a key determinant of a product’s success. Product pricing defines its market positioning, while distribution channels determine the sales network. We will conduct a comparative analysis of the six representative products mentioned above from the perspectives of pricing strategy and channel strategy.

Pricing Strategy: A Tripartite Division into High, Mid, and Low Tiers

Prices of Six Representative Products Are Divided into Three Tiers: The first tier includes Biacore and ForteBio, which have the highest unit prices, reaching2–5 million yuan; The second tier includes Nicoya, Biosensing, and BioNavis, whose prices are 50% lower than those of the first tier,Approximately RMB 1–2 million; the third tier is Xlement with precise dosing, priced at only one-tenth of the first tier,Approximately 200,000–300,000 yuan。

As the gold standard for molecular interaction analysis instruments, Biacore commands the highest price. The S200 and T200 models are priced between RMB 2 million and 3 million. The latest-generation 8K/8K+ systems offer higher throughput and superior performance, with unit prices ranging from RMB 3 million to 5 million. Chip consumables vary by type: CM5 chips (commonly used) cost approximately RMB 2,000 per chip, SA chips around RMB 4,000 per chip, and Biotin CAP chips about RMB 4,000 per chip, with more expensive chips exceeding RMB 6,000.

Table 10: Price Comparison of Six Representative Products (CNY 10,000/unit)

Source: Yiqi.com, VCBeat

ForteBio and Biacore are priced in the same order of magnitude; however, ForteBio’s average unit price is 20% lower than that of Biacore. The Octet 96e model costs approximately RMB 2.8 million per unit, the Octet RED384 model exceeds RMB 3 million per unit, and the highest-throughput Octet HTX model approaches RMB 4 million per unit.

In addition, the three products from Nicoya, Biosensing, and BioNavis are similarly priced, ranging between RMB 1 million and 2 million. Older models from Biosensing, such as the BI-2500 and BI-4500, can be priced lower, at RMB 500,000 to 1 million.

Finally, the most affordable option is Liangzhun’s Xlement SPR100, priced at only one-tenth that of Biacore, approximately RMB 200,000–300,000 per unit. The unit price for chip consumables ranges from RMB 3,000 to 4,000, slightly lower than that of Biacore’s consumables.

Channel Strategy: Distribution as the Primary Channel, Direct Sales as the Secondary Channel

The sales models of the six representative products remain predominantly distribution-based, supplemented by direct sales. Biacore, ForteBio, and Liangzhun Xlement have all established their headquarters in Shanghai and set up branches in major cities across China to provide direct sales services. Biacore and ForteBio even allow customers to request quotes directly through their official websites, with nearby branches providing door-to-door delivery as well as maintenance and repair services.

Furthermore, regarding the distribution model, with the exception of Finland’s BioNavis (which has only one exclusive distributor: Beijing Zhengtong Yuanheng Technology Co., Ltd.), other manufacturers have partnered with multiple distributors, establishing a three-tier channel structure comprising headquarters, provincial-level distributors, and prefecture-level distributors.

Table 11: Sales Models and Distributors of Six Representative Products

Sources: Yiqi.com, VCBeat

Overall, the B2B market for molecular interaction analyzers features a diverse range of products; however, surface plasmon resonance (SPR) technology, represented by Biacore, continues to dominate due to its superior performance and early market entry. With breakthroughs in 3D nano-SPR technology, next-generation molecular interaction analyzers are gradually catching up with traditional SPR instruments, thanks to their higher cost-effectiveness, and are poised to surpass them.

The above is an excerpt of the key highlights from the report. Please scan the QR code below for the full report.Free access.