2019 Healthcare IT Tender Data Analysis: Highest Winning Bid Nearly RMB 120 Million, Tier-3 Hospitals Account for 60% of Demand

Since the 1990s, relevant authorities in China have gradually recognized the significant improvements that informatization brings to hospital management and clinical capabilities, and have formulated strategic frameworks for hospital informatization. Since then, Chinese hospitals have substantially enhanced their level of informatization to optimize the allocation of medical resources, thereby fully unleashing the potential of existing healthcare resources.

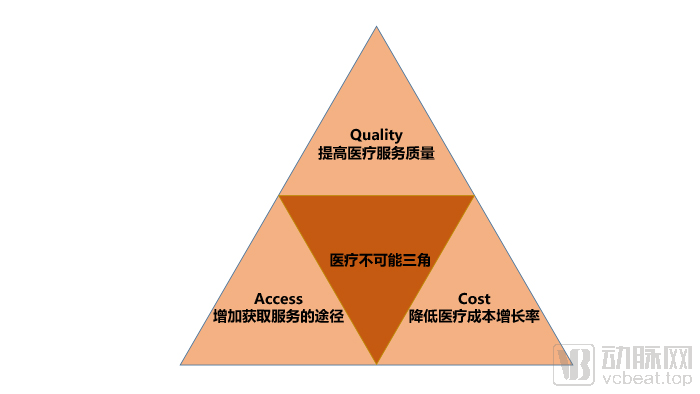

In most healthcare scenarios, it is impossible to simultaneously improve the quality of care, increase the accessibility of medical services, and reduce the cost of healthcare without breaking existing rules. VCBeat’s VBInsight refers to this as the “Impossible Trinity of Healthcare.” The only solution to this triangular dilemma is to introduce new technological increments. Only by changing modes of activity, industrial structures, and social norms can new technologies drive all variables within the triangle model to develop in the same direction.

Information technology, through the introduction of technological increments, first reduces the workload of administrative staff within hospitals and improves work efficiency; second, it supports the clinical activities of medical personnel by collecting and processing patients' clinical medical information, providing assisted diagnosis and treatment as well as clinical decision support, thereby enhancing the quality of care delivered by healthcare professionals; third, it expands the coverage of medical services through informatization, enabling more patients to access high-quality healthcare; and fourth, it assists hospital leadership in management and decision-making, thereby helping hospitals improve efficiency, reduce costs, and elevate service standards.

The past two decades have witnessed the most rapid development in information technology (IT) and communication technologies, marking China’s transition from a laggard to a follower, and gradually achieving overtaking on the bend in the IT sector. Correspondingly, there has been a significant improvement in the awareness and level of IT application in hospitals across China. With the support of IT, the efficiency of medical resource utilization has also seen a marked increase. In 1995, at the early stage of IT infrastructure development, the average number of daily patient visits per physician in general hospitals in China was only 4.4. By 2018, this figure had risen to 7.0. The adoption of IT in hospitals has significantly enhanced patient reception efficiency, improving hospital infrastructure and service capabilities through scientific means.

Nevertheless, there remains significant room for improvement in the level of informatization in hospitals across China. First, awareness and understanding of informatization among hospitals still need to be enhanced. Many hospitals hold numerous misconceptions or misunderstandings regarding their informatization initiatives. Taking Electronic Medical Records (EMR) as an example, hospital perceptions of EMR have evolved through several stages—from simply digitizing paper-based medical records to encompassing all information related to clinical diagnosis and treatment around the medical record. It is only recently that we have gradually come to recognize that EMRs should also include comprehensive records pertaining to lifelong health management. Only by incorporating information from all processes and links related to diagnosis and treatment, and leveraging big data platforms, can effective decision support be provided for clinical care and health management, thereby maximizing the efficacy of EMRs.

Secondly, with the continuous development of informatization in recent decades, hospital informatization in China has rapidly progressed through several stages. Although the pace of development has been unprecedented, it has also led to rapid updates in construction concepts; information systems built just a few years ago may already be obsolete for current needs. This has resulted in an inability to achieve unified planning and management at the data level across information subsystems from different eras and with varying business types, creating numerous “information silos.” How to integrate existing systems to enable centralized data management has become one of the most significant challenges facing hospital information management departments.

With the advancement of big data, artificial intelligence, 5G, and the Internet of Things (IoT), the collection, transmission, and analysis of medical data have become increasingly convenient compared to the past. Consequently, the development of healthcare informatization is placing greater emphasis on the management and application of medical data. Therefore, future healthcare informatization will prioritize the integration and application of medical big data more than ever before.

So, what was the actual state of hospital informatization construction in 2019? This report aggregates data on informatization procurement by medical institutions published through multiple third-party public channels, such as government procurement websites and institutional official websites, and performs secondary structured processing of the data to examine the implementation pathways of informatization procurement in public hospitals.

Development and Structural Analysis of Healthcare Informatics

Since its inception in the early 1970s, China’s healthcare informatization has shifted its focus from internal hospital management to patient diagnosis and treatment, and further to regional information interoperability. This evolution has transitioned from individual institutions to holistic systems, and from localized applications to wide-area networks, thereby strengthening its connotations and functions while continuously expanding its service scope. VCBeat Institute categorizes healthcare informatization into four stages (1.0–4.0): Stage 1.0, centered on billing and addressing non-clinical operations; Stage 2.0, core-business oriented with departmental subsystem applications; Stage 3.0, focused on interoperability and building integrated data platforms; and Stage 4.0, characterized by regional interoperability, big data analytics, and AI-enabled assisted diagnosis and treatment.

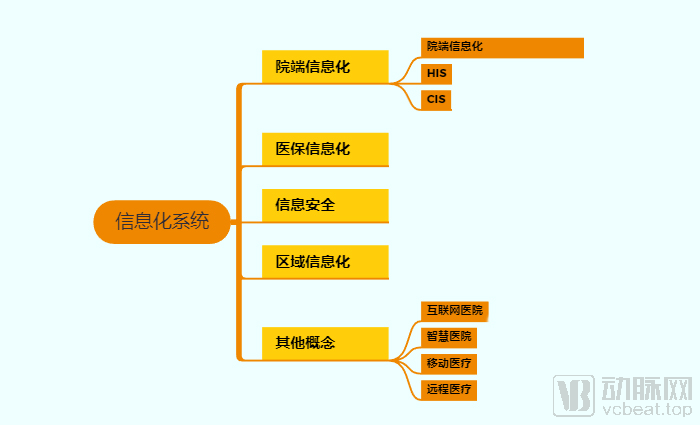

Since the 1980s, with the introduction of minicomputers into China, some forward-thinking hospitals began adopting them for management purposes, marking the inception of healthcare informatization in the country. The Hospital Information System (HIS), which focuses on financial management and cost accounting and leverages information network technologies to allocate hospital resources—including personnel, finances, and materials—was the first information system to be introduced.

By the end of the 20th century, China’s economic and technological capabilities had improved significantly. The deepening of healthcare reform and the growing demand for medical services placed increasingly higher requirements on hospital informatization. The focus of informatization shifted from the management level to the operational level, leading to the introduction of Clinical Information Systems (CIS) in hospitals. CIS facilitates full-process informatization of patient diagnosis and treatment workflows, as well as informatization across various clinical and technical departments.

However, there is no industry-wide unified standard for the interfaces of subservient application systems under CIS, making it difficult to integrate systems from different vendors and often requiring licensing fees. This has directly led to the emergence of “information silos” within hospitals, giving rise to integrated systems in the 3.0 stage. Healthcare IT companies have developed integration platforms to connect disparate medical subsystems, consolidate data across different systems, and establish a Clinical Data Repository (CDR). It is only at this stage that the hospital’s overall informatization system can be considered fully established.

In the past one to two years, with the rise of big data platforms and artificial intelligence in recent years and the huge potential demonstrated by their systems in applications in other fields. Since 2010, the focus of hospital information construction in China has gradually begun to shift to GMIS (Globe Medical Information Service).

This phase is primarily government-led, with regional residents’ electronic health records (EHRs) at its core. It connects internal hospital systems with external platforms via the internet to establish information systems serving patients, hospitals, and health administrative authorities. Big data and advanced clinical decision support systems (CDSS) are also integrated to enable refined management of the healthcare system and assist physicians in clinical diagnosis and treatment.

In addition to the aforementioned hospital information systems, healthcare informatics in a broader sense also encompasses medical insurance informatization. Originating in October 2002, the social security “Golden Insurance Project” integrated medical insurance with pension, work-related injury, maternity, and unemployment insurance into a single system, establishing an information network covering the entire country, which has served as the primary driver for the development of medical insurance informatization in China.

Currently, the vast majority of hospitals in China are at Stage 2.0 and are advancing toward Stages 3.0 and 4.0. Since Stages 3.0 and 4.0 are not mutually exclusive, their implementation is proceeding largely in parallel. Overall, China’s healthcare informatization remains at a relatively low level, with a long road ahead for future development. However, driven by the impact of the COVID-19 pandemic, the deployment of advanced information applications has accelerated significantly, yielding remarkable results. Consequently, hospital informatization is poised for a major surge in development, offering broad and promising prospects.

The Role of Policy in Driving Healthcare Informatics

Policy has played a major behind-the-scenes driving role in the process of hospital informatization. From the inception of healthcare informatization to the differentiation of key focuses at various stages, the role of policy is undeniable. We have compiled the most important laws and regulations in China’s healthcare informatization sector over the past two years, along with the primary informatization systems involved and their core content.

The rapid adoption of EMRs over the past two years particularly illustrates the role of policy in advancing healthcare informatization. Currently, the most authoritative standard for hospital informatization is the HIMSS Electronic Medical Record Adoption Model (EMRAM) certification launched by the Healthcare Information and Management Systems Society, which reflects the recognition by medical institutions of the role of informatization in hospital management. In anotherThe authoritative accreditation of the Joint Commission International (JCI), i.e.,During the JCI accreditation process, it is also necessary to improve information systems and leverage them to support clinical workflow management, thereby meeting JCI requirements.

In the process of building the GMIS, relevant departments have gained a profound understanding of the core role of Electronic Medical Records (EMR). To promote the greater efficacy of information systems in hospitals across China, the National Health Commission has implemented mandatory evaluation standards for hospital information systems in recent years, with key assessment indicators including the level of EMR functional application and the standardized maturity of interoperability. Policies related to healthcare informatization issued since 2019 clearly demonstrate the state’s strengthened assessment of medical institutions’ informatization capabilities, mandating the advancement of hospital information system construction and application by incorporating informatization-related metrics into performance evaluations.

On August 28, 2018, the National Health Commission’s Bureau of Medical Administration and Hospital Management issued the “Notice on Further Promoting the Construction of Information Systems in Healthcare Institutions with Electronic Medical Records (EMR) at the Core.” The notice strengthened efforts to advance EMR informatization and set forth clear benchmarks: by 2019, all tertiary hospitals within their respective jurisdictions were required to achieve Level 3 or above in the EMR Application Level Grading Evaluation, enabling data exchange among different departments within the hospital; by 2020, they were required to reach Level 4 or above, achieving institution-wide information sharing and incorporating clinical decision support capabilities.

Driven by policy initiatives, healthcare institutions have actively promoted the development of Electronic Medical Records (EMR) and continuously enhanced their in-hospital application levels, achieving favorable outcomes in a short period. Regardless of the specific certification scheme, the core objective remains to compel hospitals to improve EMR adoption by evaluating the role EMRs play in clinical workflows, thereby ensuring that standardized data entered can be utilized by the Government Medical Information System (GMIS) in the future.

The promotion of the Government-led Medical Information System (GMIS) further underscores the pivotal role of policy in driving healthcare informatization in China. The 2003 SARS crisis brought GMIS into the spotlight in China. Given the need to coordinate connectivity among healthcare institutions within regions, government policy intervention was virtually the only viable approach. Driven by government initiatives, China invested heavily in establishing a five-tiered network-based direct reporting system covering central, provincial, municipal, county, and township levels, while also strengthening the emergency command and decision-making systems for public health emergencies at both the central and provincial levels. This constituted the initial application of GMIS in China. In subsequent epidemics after 2003, this system has played a crucial role.

Recognizing the immense potential of the Government-led Medical Information System (GMIS), the Chinese government began incorporating GMIS into its development agenda for the next phase. Starting in 2006, the state successively issued relevant laws and regulations to promote the construction and adoption of GMIS. In 2016, the “Guiding Opinions on Promoting and Regulating the Application and Development of Health and Medical Big Data” were released, setting a goal to establish a national tiered open-application platform for healthcare information by 2020, thereby achieving cross-departmental and cross-regional sharing of foundational data resources. Subsequently, public health big data platforms began to be established across various regions. In 2018, the “Administrative Measures for Standards, Security, and Services of National Health and Medical Big Data (Trial)” were promulgated, emphasizing strengthened management of health and medical big data services and fully leveraging such data as a critical foundational strategic resource for the nation. During the recent COVID-19 pandemic, the existing GMIS played a significant role, which will further accelerate the development and implementation of GMIS in China.

Analysis and Deconstruction of Bidding Data for Informatics in Public Hospitals in 2019

Data Sample Sources and Descriptions:

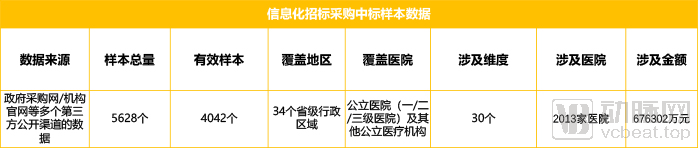

VCBeat’s data team monitored publicly available bid award samples for medical informatization procurement and tendering published on the China Government Procurement Network in 2019, collecting a total of 5,628 bid award records. Through secondary structuring of the data, we extracted 4,042 valid samples, with a total value of RMB 6.76 billion. The amount represented by these samples accounts for more than 10% of the estimated market size of China’s medical informatization sector in 2019 (RMB 60 billion).

Meanwhile, public medical institutions in China are classified as public service entities. Under the Government Procurement Law of the People’s Republic of China, government agencies may conduct procurement through open tendering, invited tendering, competitive negotiations, single-source procurement, request for quotations, and other procurement methods recognized by the State Council’s department responsible for supervising and administering government procurement; however, open tendering shall serve as the primary method of government procurement. Therefore, the data sample collected in this study is sufficiently large to reflect the basic conditions of the healthcare informatization market and is fairly representative, although VCBeat does not guarantee its comprehensiveness.VCBeat will incorporate the cleaned and organized procurement bid-winning data for these healthcare informatics products into its VCBeat Data π column, making it available for review by VIP members.

The entire dataset encompasses 30 dimensions, including bidding type, release date, province and city, administrative procurement, project name, procuring entity, winning bidder, winning bid amount, and informatization classification. We will conduct basic data analysis and cross-tabulation analysis on the sample of winning bids for informatization procurement based on these dimensions to examine the procurement pathways for informatization in medical institutions.

Basic Dimension Analysis:

Let us first examine the macro-level statistics.

Data Source: Artery Orange Database

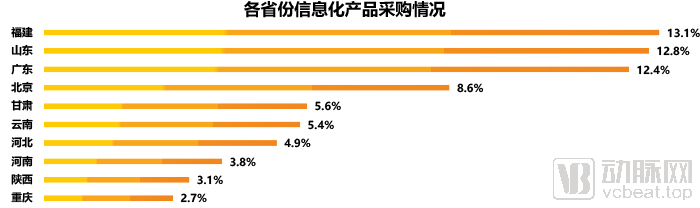

Based on the location of the projects, Fujian Province, Shandong Province, and Guangdong Province rank as the top three, with their share of informatization projects significantly leading the pack, accounting for 38.3% of the total—nearly 40%. Preliminary observations suggest a certain correlation between the procurement of informatization systems in each province and its economic level; a detailed analysis of this correlation will be conducted later. As the data for this report is sourced from the China Government Procurement Network, we have noted discrepancies between the procurement data and actual conditions in certain provinces and municipalities, such as Zhejiang and Hunan. We infer that this may be because major procurement data in some provinces are published on other procurement announcement platforms. Therefore, this dataset does not fully represent the actual procurement status of medical informatization products across all provinces. Moving forward, VCBeat will further refine and supplement this information through additional channels.

Data Source: Artery Orange Database

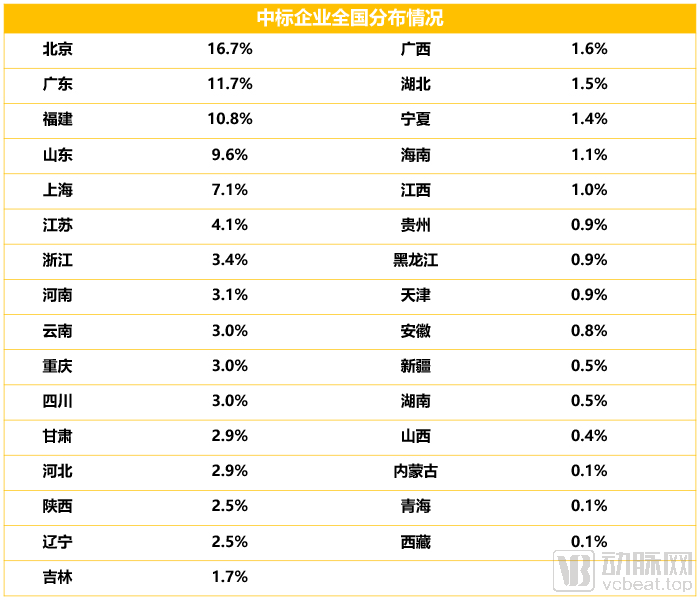

Among the winning bidders nationwide, 16.7% were from Beijing, taking the lead by a significant margin over other provinces. This highlights Beijing’s dual advantages as China’s internet hub and its economic and political center. Guangdong, Fujian, and Shandong ranked second to fourth, coinciding with the top three provinces in terms of the proportion of informatization procurement, indicating that each province still shows some preference for local enterprises. A detailed analysis will be provided later.

It is worth noting that Shanghai, Jiangsu, and Zhejiang rank fifth to seventh. The proportion of winning bidders from these three regions significantly exceeds their respective shares of healthcare IT project procurement within the overall sample, underscoring the robust foundation of the healthcare informatics industry in the Yangtze River Delta region.

Data Source: VCBeat Orange Database

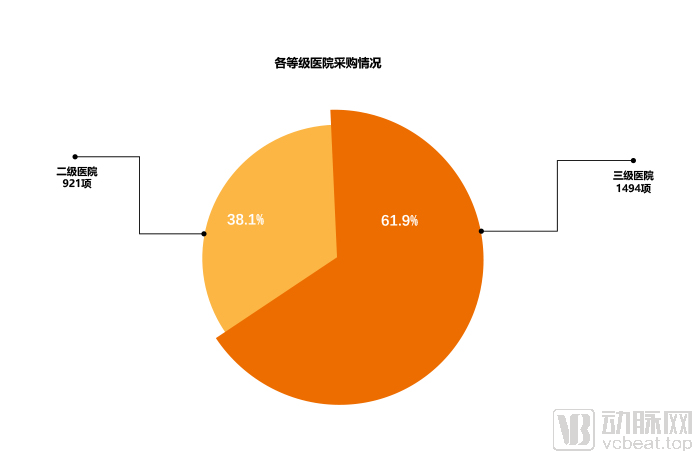

In hospital procurement, tertiary hospitals accounted for 61.9% of the total number of procurement projects. Although there are far more secondary hospitals than tertiary ones, their financial resources and level of attention received are currently significantly lower than those of tertiary hospitals. Due to heavy medical workloads, complex clinical and hospital management, and a high acceptance rate of new technologies, tertiary hospitals have an extremely strong demand for informatization. Meanwhile, having invested in informatization earlier, tertiary hospitals are now gradually phasing out and upgrading their early-stage informatization projects.

However, with the nationwide launch of performance assessments for secondary hospitals in 2020 and the strain on medical resources exposed during the COVID-19 pandemic, the informatization process of secondary hospitals may have accelerated in 2020.

Data source: Arterial Orange Database

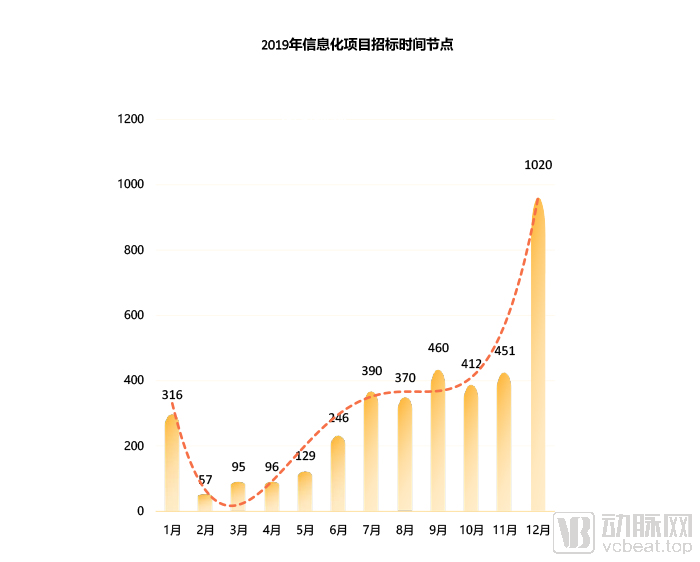

The procurement timeline for healthcare institutions’ information systems mirrors that of government procurement: some long-duration projects commence at the beginning of the year, followed by a pronounced trough until activity ramps up rapidly after the summer. The need to exhaust all budget allocations before year-end makes December the annual peak. Although the “year-end spending spree” model has many drawbacks, this situation is unlikely to change unless the national fiscal budget system is reformed.

Which types of information technology systems are most common in the annual procurement activities of public medical institutions? What proportion do these IT systems account for in the total procurement expenditure? These are the facts we aim to clarify next.

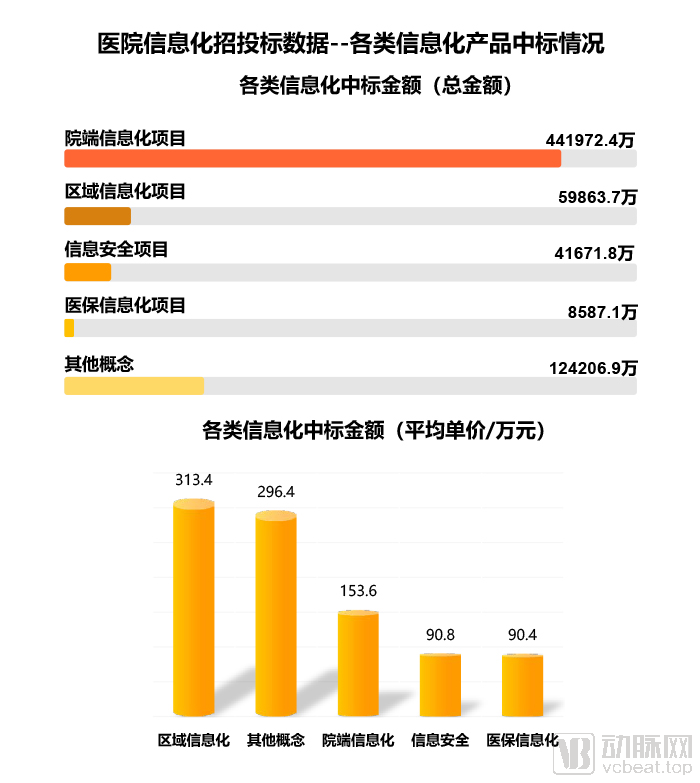

Data source: Artery Orange Database

Data Source: Arterial Orange Database

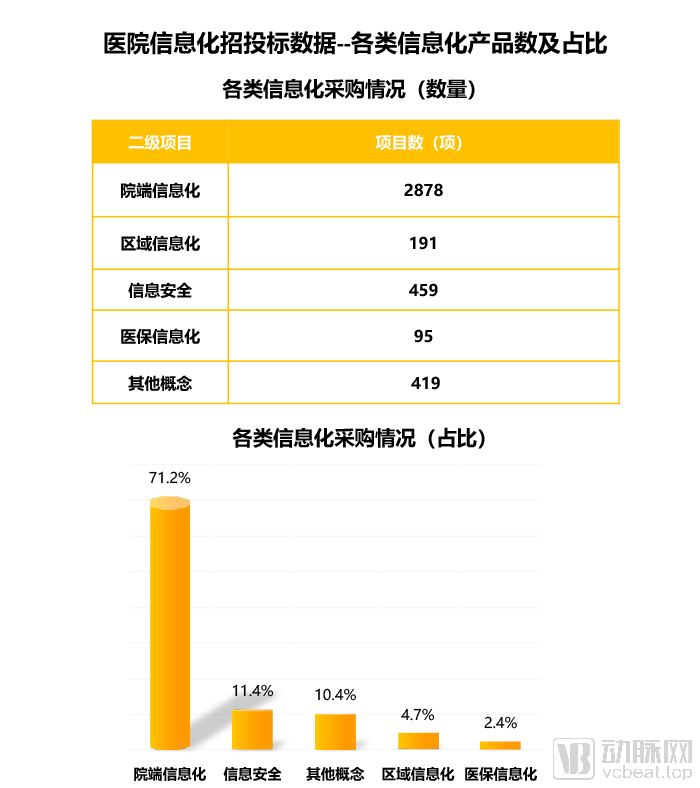

From a statistical perspective, hospital-side informatization projects, represented by Hospital Information Systems (HIS) and Clinical Information Systems (CIS), hold an absolute advantage. There are a total of 2,878 such projects, accounting for 71.2%—nearly three-quarters—of all informatization projects. However, their share of the total winning bid amount is slightly lower, at 65.4%. As hospital-side informatization involves relatively mature systems with modest unit prices, the average unit price for these 2,878 projects in this analysis is RMB 1.536 million, which is not high and aligns with our understanding of the market.

Among the samples in this statistical analysis, the project with the highest winning bid amount was also a hospital-side informatization initiative. The “Software Integration and Implementation Services (Phase I) for the Fujian County-Level Healthcare Informatization Project under the World Bank Loan-funded Health Reform Promotion Project,” procured by the Fujian Provincial Health Commission, had a winning bid of RMB 119.87 million.

Notably, information security projects ranked second in the number of informatization procurement projects, with a total of 459 projects, accounting for 11.4%. However, due to the relatively low cost of such projects, their share of total procurement expenditure was modest, at only 6.2%. In recent years, the Chinese government has successively introduced laws and policies related to information security, such as the Cybersecurity Law and the Regulations on the Security Protection of Computer Information Systems. In May 2019, the state issued the Classified Protection of Cybersecurity 2.0 Standard, which came into effect on December 1, 2019. This standard sets forth new security requirements for emerging technologies, including cloud computing, the Internet of Things (IoT), mobile internet, industrial control systems, and big data. Furthermore, it elevates the legal basis from State Council Decree No. 147 under the previous version 1.0 to the Cybersecurity Law. Driven by these robust policy measures, demand for information security projects among healthcare institutions that had not yet met the new standards has naturally surged.

Although the GMIS regional informatization sector comprised only 191 projects, accounting for just 4.7% of the total number, its total annual value approached RMB 599 million, representing 8.9% of the total amount. In terms of average implementation cost per project, GMIS stood out significantly at RMB 3.134 million, far exceeding the average for other information systems.

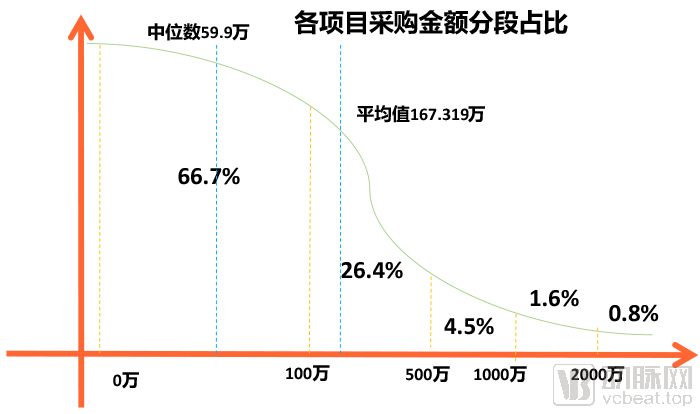

In addition to the mean, we also analyzed the percentage distribution of procurement amounts by segment for each item.

Data Source: Artery Orange Database

Data shows that medical informatics systems priced under RMB 1 million account for the largest share, at exactly 60%; projects priced between RMB 1 million and RMB 5 million constitute 26.4%; and those priced above RMB 5 million make up only 6.1%. Among all 4,042 projects, the average unit price is RMB 1.67319 million, with a median of RMB 599,000.

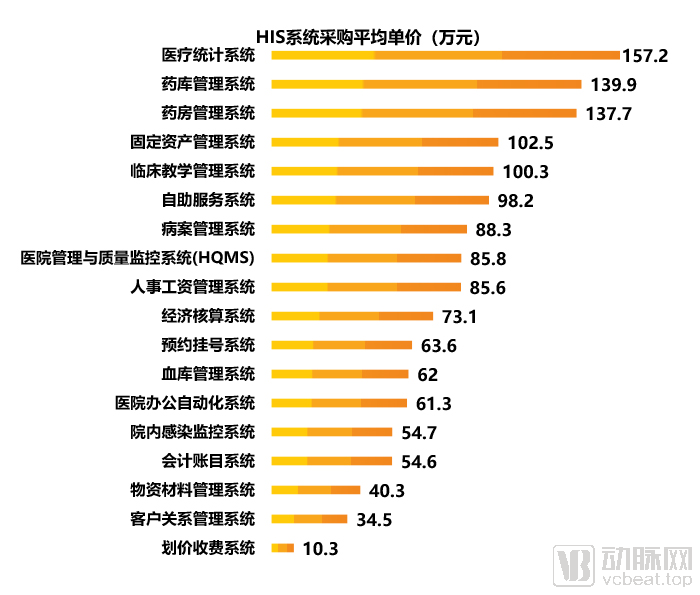

Based on the aforementioned statistics, it is evident that hospital-side information systems, primarily Hospital Information Systems (HIS) and Clinical Information Systems (CIS), account for the majority in terms of both quantity and monetary value. So, what is the price composition when delving into the specific sub-segments of hospital-side information systems? We have structured and statistically analyzed the data, revealing the following average unit prices for subsystem procurement. It should be noted that a small number of projects in the data sample were bundled as turnkey solutions without detailed breakdowns, making it impossible to disaggregate them. Consequently, these data points were excluded from the statistical analysis of the subsystems.

Data Source: Arterial Orange Database

Among the 18 sub-applications under the Hospital Information System (HIS), the top three in terms of average unit price are the Medical Statistics System (RMB 1.572 million), the Pharmacy Warehouse Management System (RMB 1.399 million), and the Pharmacy Dispensary Management System (RMB 1.377 million), which are approximately 30% higher than other modules. The least expensive is the Pricing and Billing System, with an average unit price of only RMB 103,000. Overall, the average price of HIS systems is RMB 805,500.

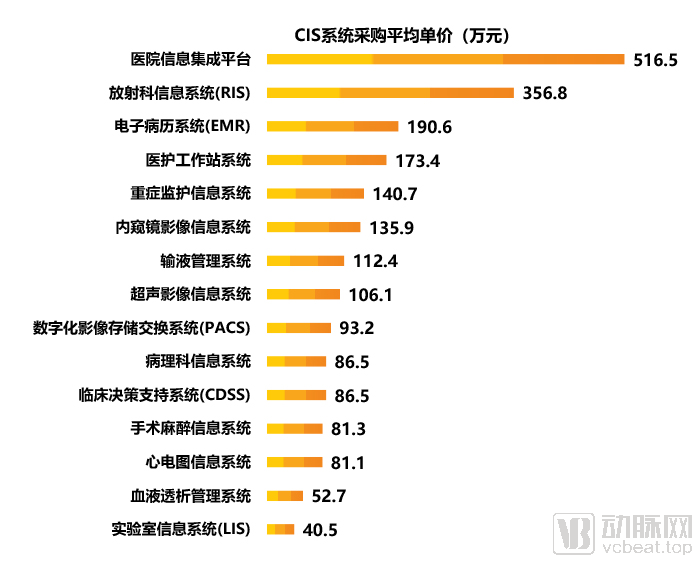

Data Source: Arterial Orange Database

Among the subsystems of the Clinical Information System (CIS), the Hospital Information Integration Platform has an average unit price of RMB 5.165 million, significantly higher than other subsystems. As a comprehensive information system, this higher price is understandable. Ranking second is the Radiology Information System (RIS), with an average unit price of RMB 3.568 million. However, after re-verifying the sample data, we found that the number of RIS samples was notably small, lacking generalizability. Similarly, the endoscopy system and ultrasound system also suffered from limited sample sizes, rendering their results non-representative. According to industry experts, the unit prices for RIS, endoscopy systems, and ultrasound systems are generally around 30% of those for PACS systems of the same tier. Ranking third is the currently highly popular Electronic Medical Record (EMR) system, though its average unit price of RMB 1.906 million is not substantially higher than the subsequent entries. Ranking fourth is the Nurse and Physician Workstation System, with an average unit price of RMB 1.734 million.

Final Thoughts

Medical informatization in China has evolved over the past two decades, progressing through four distinct stages driven by technological advancements. These stages have enabled the transition from hospital management and clinical IT applications to data integration and Clinical Decision Support Systems (CDSS). With the deepening deployment of Internet-based Global Medical Information Systems (GMIS), emerging technologies such as mobile health, the Internet of Things (IoT), big data, cloud computing, and artificial intelligence will unlock greater potential for medical informatization. In the future, medical informatization will trend toward intelligence, mobility, integration, and regionalization.

Next, VCBeat will conduct further cross-dimensional analysis by segmenting the sample data of winning bids for these healthcare informatics products. Stay tuned.