From Internet Healthcare to Medical Digitalization: Legend Capital's Strategic Investment Journey Across 37 Portfolio Companies

Legend Capital

Early-stage venture capital and growth-stage private equity investment institutions

Author: Qi Fei, Investment Director at Legend Capital

The sudden onset of the COVID-19 pandemic has brought internet healthcare back into the public spotlight. Services such as remote medical consultations while staying at home, online prescription and delivery of medications without leaving the house, and real-time updates on epidemic analysis and popular science articles have allowed people to experience the convenience and reassurance offered by internet healthcare. This resurgence has also attracted significant attention from society and users alike. At this point, five years have passed since the previous wave of fervor in internet healthcare, and nearly two decades have elapsed since the industry’s inception.

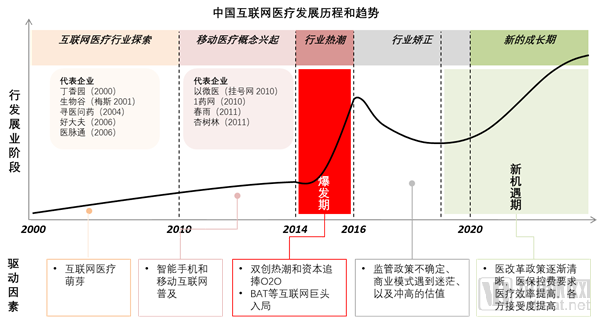

I. Flowers Fall, Try as We Might: Internet Healthcare in Those Years

Since 2000, the first wave of internet-based physician communities and online consultation companies has emerged, paving the way for the development of the internet healthcare industry. Companies such as DXY, MedSci (Bioon), Xunyi Wenyao, Haodf, and Medlive have been established successively, initiating early explorations in the industry.

Around 2010, smartphones and the mobile internet sparked a new wave, giving rise to the concept of mobile health. A cohort of companies with strong mobile internet DNA emerged, and younger firms such as WeDoctor (Guahao.com), 1 Drug Store, Chunyu Doctor, and Xingshulin gradually grew in prominence.

2014, widely regarded as Year One of Internet Healthcare, saw the sector—traditionally conservative and resistant to disruption yet brimming with vast potential as a sunrise industry—garner significant attention from entrepreneurs and investors amid the surge in mass entrepreneurship and innovation and the capital frenzy surrounding O2O models. Internet giants such as BAT also entered the fray. Overnight, industry enthusiasm reached unprecedented levels, with large-scale financing rounds sweeping through the market. During this period, we interviewed numerous industry veterans and emerging innovators, witnessed a series of landmark financing events, and participated in some of them.

This industry enthusiasm did not last long. Capital interest peaked in late 2015 and early 2016, but the difficulties in policy implementation, uncertainty around business models, and inflated valuations pushed the sector into a period of adjustment. Leading companies that had secured large-scale financing embarked on more arduous exploration, while many other enterprises faced challenging transformations and fundraising hurdles, with some players quietly exiting the market. Although there were several minor upswings between 2017 and 2018 centered on medical big data and medical artificial intelligence, the industry as a whole remained mired in uncertainty.

Yet opportunities were also brewing during this period. The policy direction of healthcare reform became increasingly clear, and acceptance of the internet among healthcare stakeholders—including patients, hospitals, physicians, and pharmaceutical companies—gradually increased. A cohort of entrepreneurs with backgrounds in the medical and pharmaceutical industries began to identify entry points and validate certain business models. The industry was quietly undergoing a series of changes, until the outbreak of the pandemic.

Image source: Legend Capital

II. A Dazzling Array: The Landscape of the Internet Healthcare Industry

Regarding internet healthcare or digital health, it may be difficult to provide a precise definition, as internet or digital technological upgrades can permeate nearly every细分 scenario in healthcare. PerhapsIn the years to come, the concept of "standalone" will cease to exist, as the healthcare industry will ultimately achieve comprehensive digitalization.

It is precisely for this reason that, during the boom period of the internet/digital healthcare industry, the sheer number of niche sectors and projects, coupled with their diverse and complex business models, has made them difficult to comprehend. Internet healthcare companies can be positioned within a three-dimensional framework based on three dimensions: target users, core technologies, and specific disease categories or medical departments. If target users serve as the primary classification criterion, these companies can be broadly categorized into the following five types, all of which have been invested in and strategically covered by Legend Capital in the past:

Patient/Customer:Targeting patients or consumers as the primary users, this model connects with hospitals, doctors/medical professionals, and pharmaceutical companies on the other end to provide corresponding services. It can be further subdivided into categories such as doctor-patient communication (which is divided into platform-based and vertical-specific types and is gradually evolving into internet hospitals), pharmaceutical e-commerce, appointment registration, and health-related consumption. This sector represents the main battlefield with the largest number of internet healthcare companies and the most intense competition.

Taking the Gengmei app, which focuses on the vertical sector of medical aesthetics, as an example, the company is committed to bridging the connection between patients and physicians. Through community operations and e-commerce platforms for aesthetic products, it has aggregated tens of millions of medical aesthetics users on one end, and thousands of certified medical aesthetics institutions and 20,000 licensed physicians on the other. This approach breaks down the industry’s longstanding information asymmetry, creating value for both sides. Another enterprise, Tongxin Yilian, positions itself as a technology-driven healthcare platform. By integrating imaging technology with artificial intelligence, it has developed intelligent imaging diagnostic products. These products are promoted through online internet hospitals and offline physical imaging centers, providing chronic disease patients with a closed-loop service encompassing consultation, examination, and treatment.

Doctor:With physicians as the core user base, and given their role as the primary providers of medical care, a significant number of their needs—such as continuing education, examination and promotion, and scientific research and innovation—have not been effectively met. Over the past two decades, numerous established companies in the industry have accompanied physicians in their gradual learning and professional growth, while simultaneously achieving their own expansion and development.

Taking Oncology News as an example, its user base focuses on oncologists—the physician group most sensitive to the iteration of clinical data and knowledge. By starting with oncology-specific content and training for physicians, it specializes in services for oncologists and their patients, covering more than 160,000 mid-to-high-end oncologists. It has become China’s largest provider of precision digital marketing services for pharmaceutical companies in the oncology vertical.

Healthcare Institutions:Targeting healthcare institutions at all levels as core clients, we provide products and solutions tailored to the informatization, digitalization, and intelligent upgrade needs across different tiers and scenarios. These offerings are further segmented to include traditional health IT vendors, next-generation health IT companies, AI systems, and smart medical devices.

Taking Baiyang Intelligent Technology as an example, the company is dedicated to optimizing healthcare scenarios through smart medical technologies. Centered on the healthcare ecosystem, it serves medical institutions and patients throughout the entire diagnosis and treatment process, thereby achieving optimization of healthcare settings. Leveraging a deep understanding of hospital management workflows and clinical practices, and utilizing cloud-based architecture, the company integrates specialized intelligent products for specific departments and diseases into real-world clinical settings, ensuring practical applicability and reimbursability.

Another enterprise, Aiyisheng, deeply explores the real-world needs of primary care hospitals and community health service centers for chronic disease management. It has developed an intelligent chronic disease management system based on clinical guidelines, providing general practice and specialty-specific chronic disease management solutions to benchmark communities, medical consortia, and cloud hospitals such as Fangzhuang, Luohu, and Xuhui. Additionally, it offers urban population chronic disease management operational services to commercial insurance companies like Ping An and Taikang, which administer basic medical insurance programs.

Gairui Technology has penetrated deeper into the grassroots township and village doctor systems, emerging as a leading provider of “all-in-one” devices and comprehensive solutions for primary healthcare in China. Its all-in-one devices serve over 50,000 township and village doctors, contributing to the upgrading of China’s primary healthcare infrastructure. In addition, companies such as Deepwise (Shenrui Bolian), Lunit, and Deyingjia are exploring AI-powered medical imaging; Zhiyinowis is pioneering intelligent bioinformatics analysis services within hospitals; Kailite is advancing intelligent continuous glucose monitoring, while Kailian is developing smart insulin pumps and closed-loop patient management models; and Hongfeng Zhikong is driving automation in hospital pharmacies. Each of these companies is delivering products and solutions to healthcare institutions in their respective scenarios and through their unique approaches.

Pharmaceuticals:Targeting pharmaceutical companies and pharmacies as core clients, services are provided across key segments of the pharmaceutical value chain, including R&D, distribution, and retail. These services can be further categorized into specialized areas such as pharmaceutical R&D support, pharmaceutical circulation, and pharmacy empowerment. For instance, Yi Fuzhen, a third-party platform provider for prescription circulation, facilitates the interconnectivity and real-time sharing of prescription data from medical institutions, medical insurance settlement information, and retail drug consumption records. This integration strengthens regulatory oversight by relevant government authorities, enhances prescription appropriateness, and enables deeper mining of prescription big data. The platform has already been implemented in Gansu Province and Wuzhou City, Guangxi Zhuang Autonomous Region, establishing a presence across one province, six cities, and two districts, with projects deployed in over 300 hospitals. These initiatives collectively serve a population of nearly 100 million.

Payer:Targeting insurance payers as its primary clients, the company covers services such as social health insurance administration, commercial insurance TPA (Third-Party Administration), and internet-based insurance. As a leader in China’s commercial insurance TPA sector and a pioneer in the domestic PBM (Pharmacy Benefit Management) industry, Jianbao Technology leverages its digital platform to provide direct billing claims processing and health management services for commercial insurance clients. The platform connects over 110,000 healthcare providers, including pharmacies, dental clinics, medical examination centers, and hospitals, serving more than 300,000 families, with an annual premium administration volume exceeding RMB 6 billion.

Internet/Digital Healthcare Industry Landscape, Image Source: Legend Capital

III. Do Not Laugh at Me for Lying Drunk on the Battlefield: Pioneers of Healthcare Reform

Looking back at the boom of the internet healthcare industry in 2014–2015 and its slump in 2017–2018, many people have questions: What exactly did the industry go through? To answer this question, we need to analyze it from two dimensions: the internet and healthcare.

From the perspective of the internet, its essence lies in transforming the methods and efficiency of information dissemination, including how information is acquired (media), how goods are traded (e-commerce), and how people communicate (telecommunications). Consequently, classic profit models that have emerged include advertising, e-commerce, gaming, and data. The service industry itself will not be fundamentally disrupted by the advent of the internet; however, its marketing strategies, service processes, and customer experiences will undergo changes, thereby driving transformations in organizational structures.

Healthcare is inherently part of the service sector, and it stands out as the most complex, knowledge-intensive, and least standardized industry within that sector. Consequently, conflicts arise when the highly market-driven internet ecosystem intersects with the decidedly non-market-oriented healthcare system—when rapid iteration meets meticulous deliberation, and when a traffic-centric mindset encounters specialized, low-frequency demand. Compounding these challenges is the significant incompatibility in communication frameworks between teams with internet backgrounds and those with healthcare expertise, necessitating deep mutual learning and adaptation through a often difficult process of integration.

This conflict is essentially a clash between “Internet + Healthcare” and “Healthcare + Internet,” or, put differently, a judgment on whether the sector should be approached as a fast-moving industry or a slow-moving one.

The answer to this question seems to be becoming increasingly clear today.

Due to historical factors and objective realities, China’s healthcare system has evolved into a complex web of relationships, akin to a tangled ball of yarn. It is difficult to straighten the entire thread by untying just one or two knots. The primary contradiction in China’s healthcare sector lies in the insufficiency of supply-side resources, particularly high-quality care. The efficiency and convenience offered by the internet are not the most pressing issues facing the current healthcare landscape. Especially when healthcare providers are less than cooperative, many challenges cannot be resolved through isolated interventions. Consequently, after making considerable efforts, internet healthcare companies have found themselves lingering on the periphery of core medical resources. Alternatively, they face such a multitude of stakeholders to align and prerequisites to meet in order to validate a business model that the probability of success remains exceedingly low.

This was also the most awkward topic in internet healthcare during those years: business models or profitability models.

Homogenized business models, limited access to core medical resources, and an inability to break through existing commercial paradigms have become the three major obstacles facing internet healthcare. As aspirations meet reality, it has gradually become apparent that the internet is not a panacea for disrupting all industries; rather, the industrial logic of “healthcare + internet” more closely aligns with the current state of the sector.

We will not simply dismiss the industry of those years as a bubble. After engaging with numerous entrepreneurs driven by vision and ambition, we regard that period as a milestone era. Although not all enterprises survived, talent remained, experience accumulated, and mindsets evolved. Years from now, when we look back, we may find that the efforts made by those companies and entrepreneurs had a profound impact on the transformation of the entire healthcare industry. Their influence likely holds significant importance in reshaping the perspectives of various stakeholders in today’s healthcare sector and even in informing the approaches to healthcare reform.

Whether by choice or by circumstance, that cohort of internet healthcare companies has shouldered the mission of stirring the waters and serving as pioneers in healthcare reform.

IV. Familiar Swallows Return: The Black Swan Arrives

From an industry perspective, the “black swan” event of the COVID-19 pandemic has indeed significantly propelled the development of the internet healthcare sector. The outbreak led to a rapid surge in traffic to internet-based applications, while also driving widespread public awareness and adoption of online medical platforms. This resulted in a substantial increase in both industry penetration and public recognition, with attention to and usage frequency of various online healthcare products reaching record highs. Meanwhile, hospitals have recognized the shortcomings of their previous informatization efforts and will accelerate the development of information systems and internet hospitals. The government is also expected to expedite the introduction of relevant policies, fast-tracking initiatives that might otherwise have taken considerably longer to implement. Specific impacts include:

Patient Side:During the pandemic control period, internet healthcare providers have successively launched online free clinic services. Online consultations can reduce the risk of cross-infection among patients. Meanwhile, during the special period when medical resources are prioritized for epidemic areas and fever clinics, these services can effectively improve hospitals’ service coverage and efficiency. Pandemic control efforts have accelerated public acceptance of online medical services, leading to an explosive growth in user inquiries. Additionally, users can purchase common medications through online healthcare platforms, significantly enhancing overall usage habits. After the pandemic subsides in phases, a certain proportion of users are expected to convert into long-term users.

Doctor's Side:Constrained by the pandemic, doctors have increasingly adopted online consultations for many common conditions outside of fever clinics, including in fields such as stomatology and maternal and child health, thereby further enhancing their proficiency with digital platforms.

Healthcare Institution Side:The pandemic has acted as a catalyst for the digitalization of hospital diagnosis and treatment. An increasing number of hospitals are accelerating the launch of online consultation services, including virtual fever clinic services, which facilitate initial diagnosis and patient triage, thereby effectively alleviating pressure on offline facilities. In the post-pandemic era, demand for advanced hospital information system upgrades and the development of internet hospitals is expected to rise significantly. This will enhance both service efficiency and patient experience. Furthermore, the construction of medical consortia and the implementation of tiered diagnosis and treatment systems are likely to gain momentum under these favorable conditions.

Pharmaceutical Sector:Due to the impact of the pandemic, pharmaceutical companies were unable to carry out R&D, market access, and marketing activities. Coupled with the pressure of healthcare insurance cost containment, many R&D and marketing efforts will gradually shift toward more efficient digital health enterprises in the future, thereby driving industry development.

Payment Terminal:Supporting policies for online settlement via internet hospitals have already been introduced by the national medical insurance system, with expectations of earlier-than-anticipated implementation. This development will significantly promote online diagnosis and treatment services in hospitals in the future, while also benefiting internet hospital platforms and health information technology enterprises. Meanwhile, the recent epidemic has served as a wake-up call to enhance public health awareness. Health insurance is poised for further growth, with more innovative health insurance products expected to emerge. Third-party service providers offering refined management and operational support for the insurance industry will also experience rapid expansion.

The understanding and cooperation from various industry stakeholders, along with policy easing, which had been elusive for many years, have quietly shifted in the aftermath of the pandemic. Previous expectations for the industry are gradually being realized, marking the entry of sector development into a new phase. This positive trend will, on one hand, concentrate benefits among leading companies in specialized sub-sectors; on the other hand, and more importantly, it signals that public healthcare institutions—the mainstay of the medical system—will comprehensively embark on digital transformation, propelling industry development into an entirely new stage.

V. Searching for It Amidst the Crowd: The Digitalization of Healthcare

Unlike traditional internet healthcare, which primarily served as a connector among industry stakeholders to enhance the efficiency of information transmission and communication, our understanding of medical digitalization is broader. It encompasses not only narrow-sense internet healthcare but also the wider scope of digital health, including traditional and next-generation healthcare informatization (informatization), medical big data and blockchain technologies and applications (datafication), and medical artificial intelligence and smart hardware (intelligentization). Furthermore, it includes the digital transformation and reengineering driven by various stakeholders in the healthcare industry, such as the digitalization of R&D, marketing, and distribution processes for pharmaceutical and medical device companies, innovative digital diagnostic and therapeutic products and solutions, and the upgrading of digital management and service systems in healthcare institutions.

Over a relatively long horizon, we are confident in the trend toward comprehensive digitalization across all sectors and scenarios of healthcare. There is significant room for digital technologies to enhance efficiency in doctor-patient communication, diagnosis, treatment, and healthcare services. The granularity of medical data and the precision of clinical diagnosis and treatment will continue to improve, which in turn will drive advancements in diagnostic and therapeutic methods and technologies.

However, precisely due to the complexity of medical specialties, as well as the intricacies of healthcare system policies, regulatory oversight, and commercial logic, this transformation is inevitably a gradual process. The current pandemic may serve as a new starting point, initiating a wave of digital adoption among professional medical institutions and pharmaceutical and medical device manufacturers. Nevertheless, the path to realization is extremely arduous and challenging. Medical institutions, primarily public hospitals, have recognized the value of digital online healthcare. Yet, this transformation cannot be achieved merely by shifting doctors or clinical practices onto the internet for the purpose of information transmission and transfer. Instead, it requires a fundamental reengineering of healthcare management and clinical pathways to substantially improve the efficiency of healthcare service delivery. Such reengineering demands close collaboration between enterprises and medical institutions, abandoning entrenched mindsets to pursue genuine model innovation. Achieving this goal will not suffice with efforts from existing internet/digital health companies or tech giants with internet backgrounds alone; it requires the joint promotion of all relevant stakeholders across the healthcare industry, including traditional players such as pharmaceutical and medical device companies and healthcare institutions.

On one hand, companies with an Internet/digital health background need to gradually penetrate into healthcare scenarios, understand the underlying medical logic and stakeholder relationships, leverage technology to reconstruct business models in specific niches, improve the efficiency of healthcare delivery, pharmaceuticals, and health insurance, progressively validate their business models, and strengthen competitive barriers. Over the past two years, we have been encouraged to observe that a number of Internet/digital health companies, including those mentioned earlier, have gradually identified their value propositions, strengthened their core capabilities, and become key players in their respective niche scenarios.

On the other hand, stakeholders in the traditional healthcare system are also carrying out digital exploration and upgrades based on their respective backgrounds to varying degrees. The specific types include:

Digital Diagnosis and Treatment Based on BioinformaticsWith the continuous advancement of gene testing and multi-omics technologies, an increasing amount of biological data related to human diseases and health is being acquired. Companies leveraging these tests and bioinformatics analyses are accumulating significant data assets. Representative genetic testing and diagnostic enterprises—such as Berry Genomics, HuiRui Gene, New Horizon Health, and Jinshi Gene—have each amassed population-level datasets exceeding one million samples. Further research and analysis centered on these data hold the potential to drive breakthroughs in novel diagnostic methods and products, while also providing greater guidance for future new drug development.

Medical device companies with deep expertise in specialized disease treatment areas, leveraging new digital equipment and materials, are also exploring innovative products in the fields of devices and consumables. They aim to address more complex medical challenges through more precise digital equipment. Taking the upstream dental industry as an example, Legend Capital has invested in Born Dental and Aidite, both suppliers of upstream equipment, consumables, and materials. These two companies have established competitive advantages in their respective niche markets while also focusing on the future trend of dental digitalization. They are actively engaged in the research, development, and strategic deployment of product and technology platforms such as CBCT, intraoral scanning, digital orthodontics, and 3D printing.

Digital Transformation of Healthcare InstitutionsHealthcare institutions are the core providers of medical services. Institutions, including public hospitals, are actively pursuing digitalization efforts. The future trend centers on comprehensive digitalization across all stages of diagnosis and treatment, as well as leveraging digital information to optimize clinical decision-making, thereby enhancing efficiency and precision. In the private consumer healthcare sector—such as dentistry and medical aesthetics—which features a higher degree of marketization and fewer restrictions from medical insurance schemes, such explorations have already taken the lead.

As a leading domestic dental chain service brand, Happy Dental began systematically studying the U.S. DSO model more than two years ago. Through over two years of self-driven innovation and breakthroughs, it developed an online SaaS system to innovatively transform its management and operational models. The company has initially achieved digital management upgrades for dozens of its self-operated clinics nationwide, established a full-course cycle management system based on patient records, and implemented centralized remote diagnostic and treatment guidance by experts. Furthermore, this management model has been exported and empowered to dozens of partner member clinics. In the future, Happy Dental aims to achieve comprehensive digital standardized operational management for both its self-operated and member dental clinics, with the goal of becoming China’s largest dental healthcare group.

Digital third-party professional services—platform-based service companies covering multiple stages such as R&D, marketing, and distribution for pharmaceutical and medical device enterprises, including CROs and distributors—are leveraging their existing scale advantages to pursue digital transformation and efficiency improvements. Taking Guoke Hengtai as an example, this rapidly growing medical device commercial enterprise is a domestic leader in third-party specialized logistics and comprehensive services for high-value medical consumables. Its goal is to significantly increase investment in information systems, build an integrated information platform spanning both in-hospital and out-of-hospital settings, and establish a data-driven logistics distribution system and services. Ultimately, it aims to become a comprehensive digital supply chain service provider for the high-value medical consumables industry.

Legend Capital Portfolio Companies’ Explorations Across Various Dimensions of Healthcare Digitalization

Finally, whether for internet/digital health companies in the conventional sense or for traditional stakeholders in the healthcare industry, the trend of digitalization in the healthcare sector is already emerging. A new chapter has begun, and industry enthusiasm will continue to grow. An increasing number of professionals with backgrounds in healthcare or IT will join this major trend. We also look forward to seeing greater collaboration between internet/digital health companies and various healthcare entities—including medical institutions, pharmaceutical and medical device companies, and insurers—to drive digitalization into more deep-seated scenarios across the healthcare industry.

At the same time, we must never underestimate the challenges facing industry development; this exploratory process may prove more protracted than anticipated. Aligning with the trends of healthcare reform, adhering to business logic, and preparing to support the industry’s long-term growth are essential competencies for us as industry practitioners.

Fortunately, in the healthcare industry, time is our friend.

Epilogue

Do you remember the 768 Creative Park in Beijing in early summer 2015? On a rooftop filled with drifting locust blossoms, Li Datao, founder of VCBeat, then embarking on his first entrepreneurial venture and fundraising round, shared with us his vision for the future of digital healthcare.

“Why establish a professional media outlet focused on healthcare digitalization? How long will this trend last?”

“It may take ten to twenty years for an industry media outlet to truly demonstrate its value. We aim to be observers of the industry and the earliest companions to entrepreneurs!”

“Well, let us go and witness this chapter of history together!”

About Legend Capital

Legend Capital is an independent professional venture capital firm under Legend Holdings, established in April 2001. Its core business focuses on early-stage venture capital and growth-stage expansion investment. Currently, the total assets under management of its USD and RMB funds exceed RMB 50 billion. As of 2019, Legend Capital had invested in nearly 450 companies, among which more than 70 have successfully gone public or been listed on domestic or overseas stock exchanges.

Since 2007, Legend Capital has been strategically investing in the healthcare sector, accumulating over 100 investments with a total capital commitment exceeding $1.3 billion. Its portfolio spans multiple sub-sectors, including biopharmaceuticals, medical devices and diagnostics, professional services, gene technology, and digital health, with deep strategic positioning in therapeutic areas such as cardiac medicine and surgery, neurosurgery, diabetes, and oncology.