2019 Global Diagnostics and Genetic Testing Industry Report: Intensifying Market Concentration and the Rise of Molecular Diagnostics

Amid the escalating global pandemic, the healthcare and life sciences sector has once again become the focal point of market attention. As a key area of long-term focus and deep cultivation, the HuaXing Healthcare team has continued its tradition in this early spring, when warmth still contends with lingering chill. Starting from five major sectors—biopharmaceuticals, IVD and genetic testing, medical devices, healthcare services, and smart healthcare—as well as the funding side, the team strives to comprehensively map out the development trends in the global healthcare industry over the past year.

In 2019, the financing environment for China’s diagnostics and genetic testing industry tightened further, with a pronounced “winner-takes-all” effect in private equity financing; genetic testing companies led the pack in both deal count and capital raised. In the six months since the launch of the STAR Market, in vitro diagnostics (IVD) emerged as a hot subsector within the biopharmaceutical segment. The M&A market saw two major transactions exceeding RMB 1 billion each over the course of the year. More than half of overseas financing deals were completed by genetic testing firms, while molecular diagnostics companies remained highly sought-after, commanding a substantial share of industry resources.

This report will focus on both the domestic and international markets, providing a comprehensive review of capital activities in various sub-sectors of the diagnostics and genetic testing industries in 2019.

Full Report:

In 2019, the financing environment for China’s diagnostics and genetic testing industry tightened further. Over the past year, the protracted Sino-U.S. trade dispute and U.S. restrictions on technology transfers to China have strengthened the national commitment to bolstering the high-end medical device sector. Policies at all levels of government have increasingly encouraged greater independent innovation within the industry.

Currently, many local governments have issued lists permitting the procurement of imported medical equipment, reagents, and consumables. We anticipate that in the post-pandemic era, high-end domestically produced equipment in the field of biosafety will garner greater attention, further advancing China’s medical equipment industry along the path of self-reliance and controllability.

However, the potential impact of healthcare insurance cost-containment measures on the diagnostics industry cannot be overlooked: certain provinces and municipalities have begun implementing the “Two-Invoice System” and volume-based procurement for in vitro diagnostic (IVD) reagents; it is becoming a trend for end-user medical institutions to adopt a “volume-for-price” model; both IVD manufacturers and distributors will face significant challenges.

In 2019, the financing environment for China’s diagnostic and genetic testing industry tightened further. Over the past year, the protracted Sino-U.S. trade dispute and U.S. restrictions on technology transfers to China have strengthened the national commitment to bolstering the high-end medical device sector. Policies at all levels of government have increasingly encouraged greater independent innovation within the industry.

Currently, many local governments have issued lists permitting the procurement of imported medical devices, reagents, and consumables. We anticipate that in the post-pandemic era, high-end domestically produced equipment in the field of biosafety will garner greater attention, further advancing China’s progress toward self-reliance and controllability in its medical equipment sector.

However, the potential impact of healthcare cost-containment measures on the diagnostics industry cannot be overlooked: certain provinces and municipalities have begun implementing the “two-invoice system” and volume-based procurement for in vitro diagnostic (IVD) reagents; it is becoming a trend for end-user medical institutions to adopt a “volume-for-price” model; both IVD manufacturers and distributors will face significant challenges.

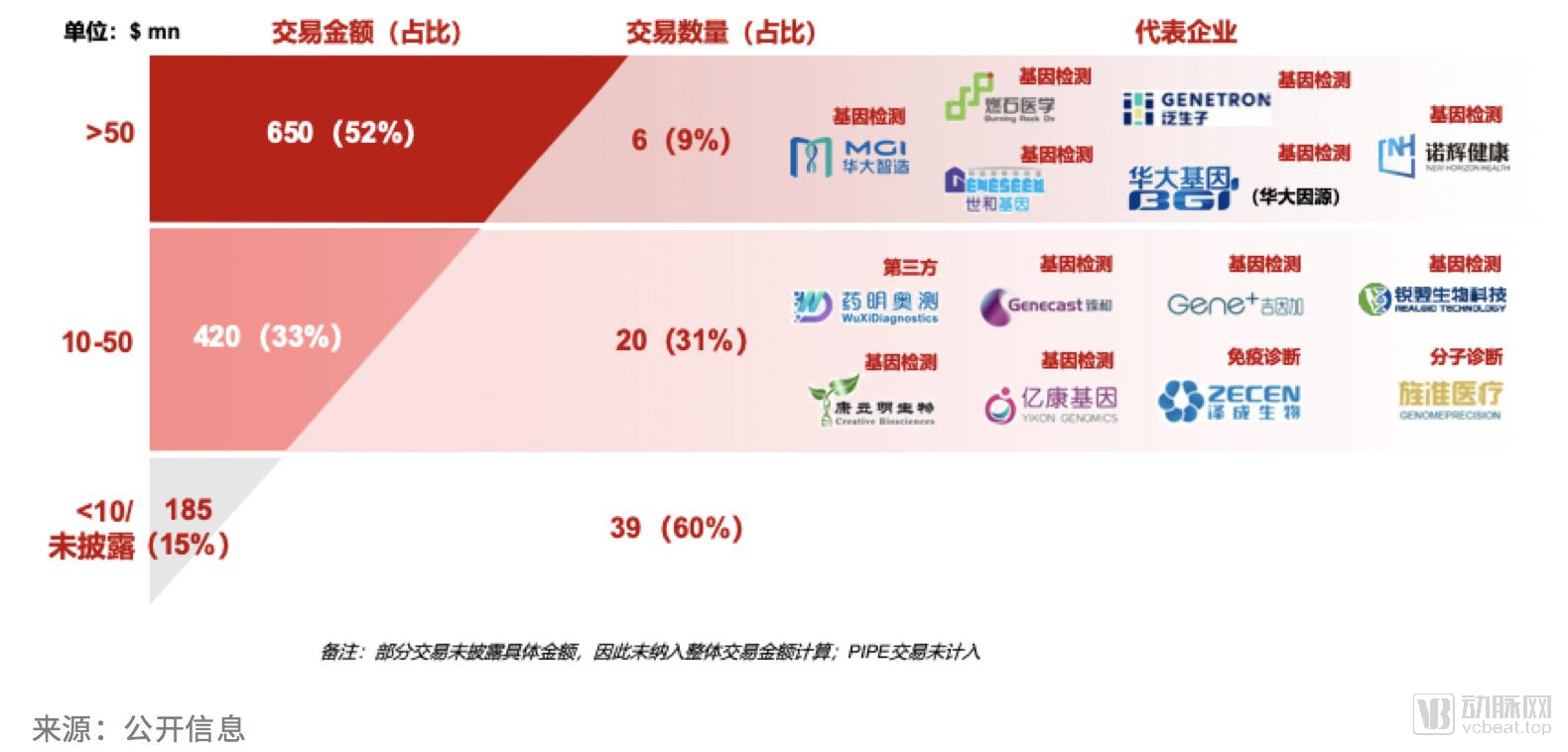

According to statistics, there were 65 private equity financing transactions in China's diagnostics and genetic testing industry in 2019, a year-on-year decrease of approximately 18% compared with 2018. However, the total financing amount declined only slightly from that of 2018, reaching approximately USD 1.25 billion.

Over the past year, the "winner-takes-all" effect in private equity financing within the industry has been particularly pronounced. The aggregate value of just three deals, each exceeding $100 million, accounted for one-third of the total annual transaction volume. These three leading transactions were MGI Tech’s $200 million Series A round, Burning Rock Biotech’s $130 million Series C round, and Genetron Health’s $110 million Series D round.

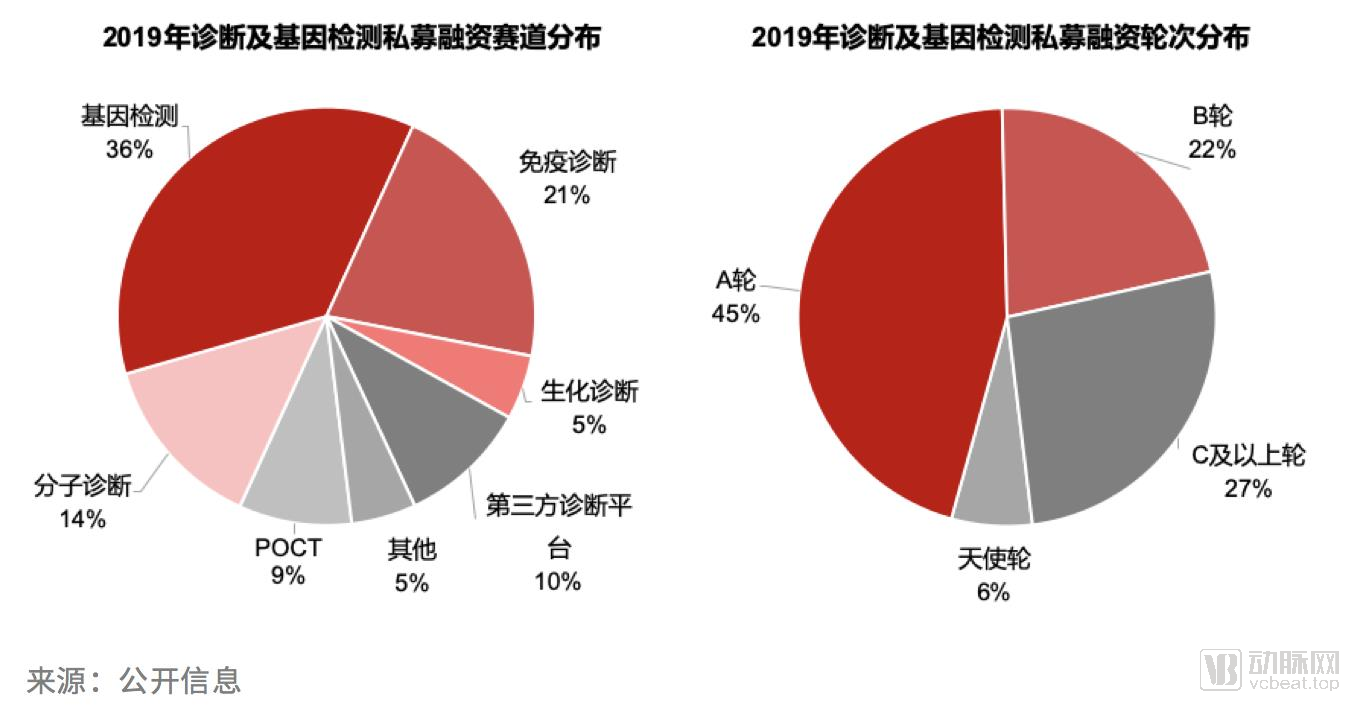

Among the specialized subsectors, genetic testing companies are paramount, accounting for 36% of the total number of transactions and 70% of the total financing amount in the industry, while other subsectors show a relatively even distribution. Focusing specifically on genetic testing companies, the three most active application areas are tumor companion diagnostics, early cancer screening and diagnosis, and novel microbial testing.

1. Tumor Companion Diagnostics

Leading companies in the first and second tiers of this sector completed substantial private equity financing rounds in 2019, with some, such as Burning Rock and Genetron Health, already pursuing fundraising in public markets. It is anticipated that once these industry leaders complete their initial public offerings, they will widen the funding gap with competitors, further clarifying the competitive landscape.

We believe that ensuring compliance in products and sales, increasing the population penetration rate of diagnostic products, and empowering hospitals to enhance their on-site testing capabilities remain the key areas of focus for the industry’s future development. However, given the substantial investments required for new product R&D, market development and education, and clinical trials, coupled with the difficulty of bringing clinical sales expenses under control in the short term, it will take some time before the industry achieves stable overall profitability.

Currently, some companies are beginning to explore new models such as bundling diagnostic product design with insurance sales, thereby providing pharmaceutical companies with integrated R&D and commercialization services. Whether these new business models can generate more diversified revenue streams for enterprises and inject fresh momentum into industry development remains to be seen over time.

2. Early Screening and Diagnosis of Tumors

In 2019, Kangliming and New Horizon Health each completed significant private equity financing rounds. While advancing the commercialization of their existing products, they also actively expanded their product pipelines for early screening and diagnosis of multiple single-cancer types. Additionally, Burning Rock Biotech partnered with Illumina to jointly develop products for cancer screening, diagnosis, and monitoring.

The rapid development in this field has been driven by national policy incentives. In September 2019, ten government agencies, including the National Health Commission, jointly formulated the “Healthy China Action—Implementation Plan for Cancer Prevention and Control (2019–2022),” which explicitly calls for accelerating early cancer screening, early diagnosis, and early treatment; expanding the coverage of such services; encouraging high-risk populations to undergo regular cancer-preventive health examinations; and ultimately improving cancer survival rates.

The field of early cancer screening and diagnosis holds broad prospects, but it is still in its early stages, and maturity will take time to develop. It is not only necessary to further improve the performance metrics of products through new technological means, but also imperative to subject them to rigorous clinical validation trials to ensure safety and efficacy. Regulatory compliance and certification are indispensable steps and key to the long-term, healthy development of this sector.

3. Novel Microbial Detection

Multiple companies utilizing novel molecular diagnostic techniques (including mNGS) for pathogen diagnosis, including industry leader BGI PathoGenesis, completed private equity financing successively in the second half of 2019. Meanwhile, some enterprises primarily engaged in other areas of genetic testing also established microbiology testing subsidiaries or business divisions in 2019.

Infection is one of the leading causes of death among clinical patients. However, current clinical diagnostic methods still face urgent challenges, including low detection accuracy, prolonged turnaround times, and an inability to identify unknown pathogens. The outbreak of the novel coronavirus has further intensified the demand for new technologies in clinical microbiology testing, while also providing emerging microbial diagnostics companies with an opportunity to demonstrate their capabilities. During this pandemic, we were pleased to find that some companies were among the first institutions to detect viral nucleic acid sequences in patients, thereby providing robust technical support for subsequent epidemic prevention and control efforts.

Overall, the industry outlook is positive, with further market expansion enabled by a broad target population, scalable application scenarios, and standardized product compliance.

4. Third-Party Laboratory Testing

WuXi NextCODE Completes $50 Million Series A Financing. The company specializes in high-end specialized diagnostic tests, establishing a multi-platform, multi-omics, and clinical big data integration platform to empower assisted diagnostic decision-making and clinical research.

The nationwide implementation of DRG will play a positive role in the business development of enterprises in the third-party testing sector, and the proportion of hospital laboratory outsourcing in regions implementing DRG will increase significantly.

Furthermore, as policies further relax the qualification requirements for nucleic acid testing for third-party clinical laboratories, the proportion of specialized testing services and the overall profit margin of enterprises are expected to increase accordingly.

5. Digital PCR and Single-Cell Analysis

The technologies employed in these two fields hold significant potential for mutual借鉴. As microdroplet and microfluidic technology platforms mature, companies in related application areas have begun to emerge in rapid succession. In 2019, multiple enterprises, including Singleron and BioBrain, completed financing rounds to support their expansion.

These companies are still in their early stages of development, exploring technological platforms and application scenarios. However, with established overseas players such as Bio-Rad and 10x Genomics paving the way, the field holds promising prospects for growth.

6. Mass Spectrometry

Mass spectrometry is regarded as the next “gene sequencing” in the diagnostics industry, a platform technology with substantial market potential. As the technology matures, it is gradually transitioning from scientific research to clinical applications, with imminent market expansion. In 2019, several companies, including Rongzhi Biology, Yingsheng Biology, Baichen Diagnostics, and Baiqu Biology, completed financing rounds, with Rongzhi and Yingsheng each raising nearly RMB 100 million.

Upstream instrument market is dominated by an oligopoly, with the vast majority of equipment reliant on imports. Most domestic companies develop assay kits through OEM arrangements or procure mass spectrometers, expanding their businesses via service-based models. Biocytogen has taken the lead in completing its upstream layout. Its independently developed wide-range quantitative time-of-flight mass spectrometer, QuanTOF, and microfluidic chip-based rapid nucleic acid analysis system, QuanPLEX, have broad applications, including rapid microbial identification, SNP genotyping, and protein quantification.

In the United States, clinical mass spectrometry accounts for 15% of the medical testing market, whereas in China it represents only 1–2%, indicating substantial growth potential. Currently, relatively mature clinical applications of mass spectrometry in China are primarily focused on microbial identification and newborn screening for genetic disorders. Applications such as vitamin analysis, therapeutic drug monitoring, and small-molecule biomarker detection are still in their early stages of development but are poised to become highly prominent areas in the future of clinical mass spectrometry in China.

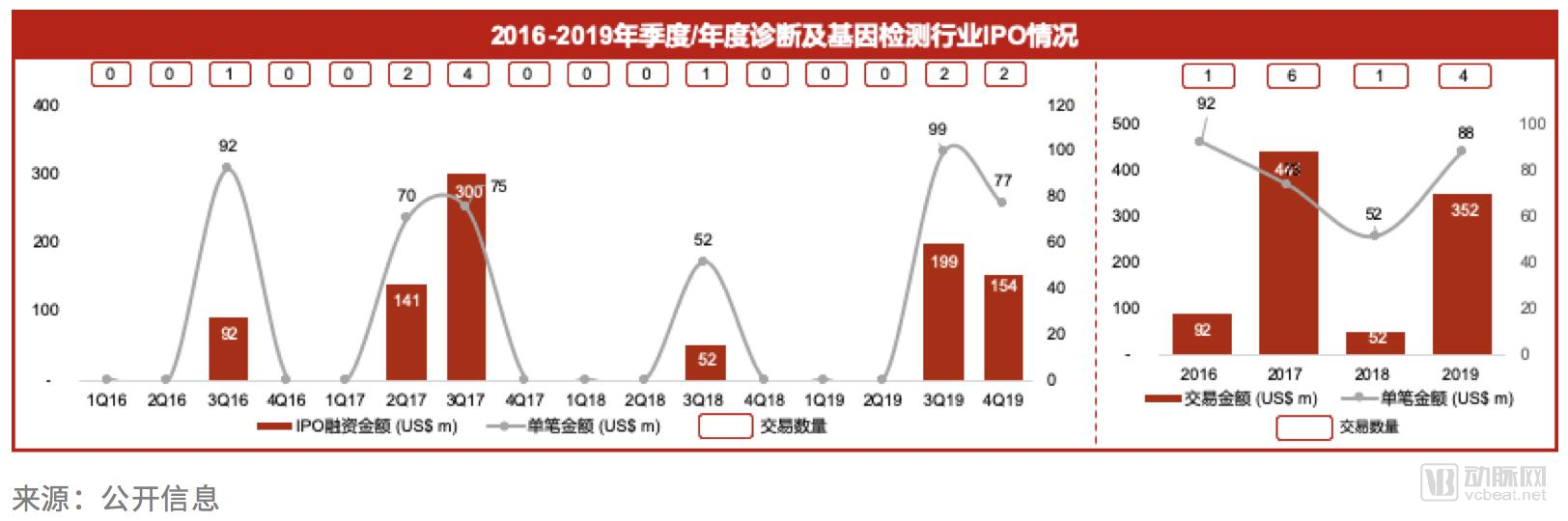

Since the launch of the STAR Market six months ago, a total of 16 pharmaceutical and biotechnology companies have held their listing ceremonies. Among them, three in vitro diagnostics (IVD) companies—Hotgen Biotech, Pumen Technology, and Shuoshi Biotech—have raised an average of RMB 520 million each, making IVD one of the most sought-after subsectors within the biopharmaceutical segment.

IVD companies listed on the STAR Market have seen an average gain of nearly 102.97% and a median gain of 99.25% to date, outperforming the STAR Market Index’s 3.8% rise. The average price-to-earnings (P/E) ratio of IVD enterprises stands at 87.42, ranking third among major market segments. Their product portfolios primarily cover cardiovascular and cerebrovascular diseases, inflammatory infections, pathogens, female reproductive health, and early cancer screening. The main drivers of future revenue growth for these companies are the import substitution of domestically produced products and the expansion of the primary care market spurred by tiered diagnosis and treatment.

In addition, two companies, Orient Gene and Sansure Biotech, submitted listing applications, with Orient Gene officially listed for trading in early February 2020.

Overall, the STAR Market’s preference for IVD companies has been concentrated in fields such as POCT, chemiluminescence immunoassay, and PCR-based molecular diagnostics. Applicant companies are typically large-scale enterprises with average annual revenues exceeding RMB 200 million and net profits surpassing RMB 40 million. In the early stage of the STAR Market’s launch, healthcare sector applicants were predominantly profitable medical device companies, among which IVD firms benefited most, accounting for nearly 25%. The STAR Market has provided unlisted IVD companies with a more convenient and efficient IPO pathway and higher market valuations.

In 2019, Huajian Medical successfully listed on the Hong Kong Stock Exchange, raising a total of HK$1 billion. As a distributor of in vitro diagnostic (IVD) products, Huajian Medical specializes in providing IVD instruments, reagents, and consumables, as well as centralized procurement solutions for clinical laboratories, to suppliers and distributors serving various medical institutions.

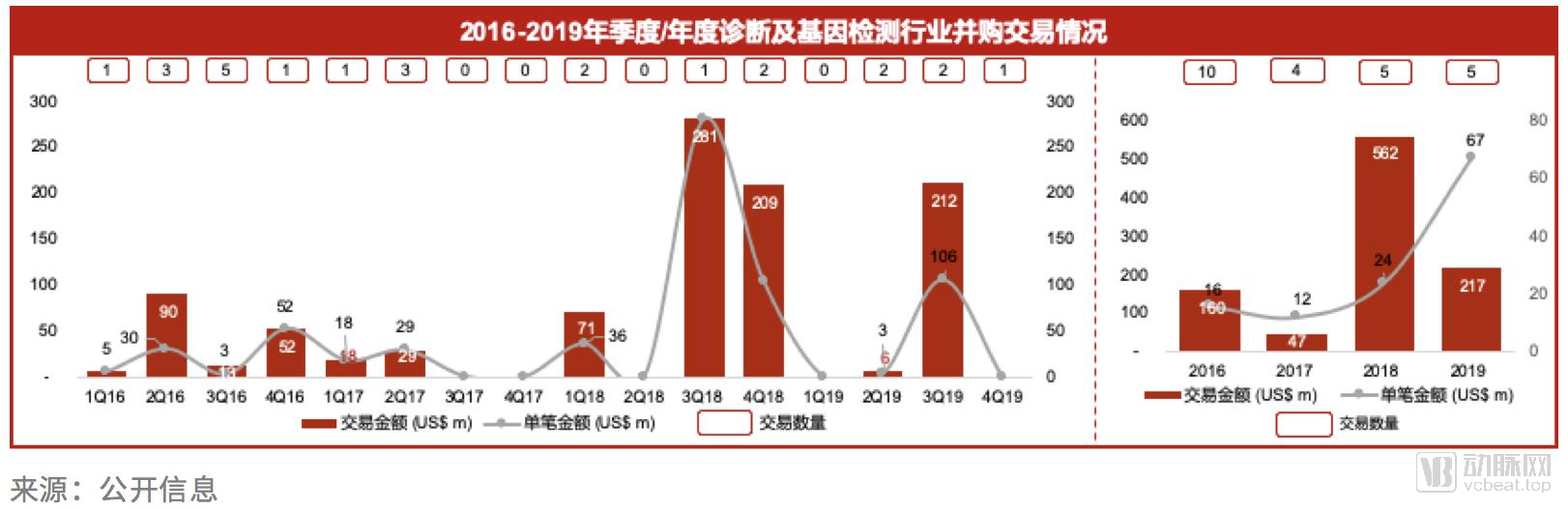

Over the past year, the diagnostics industry witnessed two major M&A transactions exceeding RMB 1 billion each. Hangzhou Xiacheng State-owned Capital Investment acquired a 20.02% stake in Runda Medical for RMB 1.5 billion, becoming its controlling shareholder. In addition to helping the company diversify its financing channels and alleviate financial pressure, the entry of state-owned strategic investors also facilitates access to public hospital channels, ensuring the company’s sustained and rapid business growth.

Another M&A transaction involved Jiuyuan Biology and Sinopharm Investment jointly acquiring Maixin Biology. Through this acquisition, Jiuyuan’s diagnostics business line will extend into the field of pathological diagnostic reagents and instruments. By partnering with Sinopharm in this joint acquisition, Jiuyuan has also achieved a tighter strategic alignment with Sinopharm, leveraging its extensive distribution network to achieve better nationwide coverage across China.

In 2019, more than half of overseas financing transactions were completed by companies involved in genetic testing, with multiple large-scale deals exceeding $30 million. Molecular diagnostics companies remained highly sought-after, capturing the majority of industry resources, which reflects the sustained interest from overseas markets in the molecular diagnostics sector.

1. Sequencing Instruments

Overseas gene sequencers remained under intense scrutiny in 2019, yet the industry pioneers experienced divergent fortunes.

2019 was not a banner year for Illumina. Although Illumina entered into a deep product partnership with Qiagen, effectively prompting the latter’s complete exit from the sequencer competition, Illumina did not launch any new instruments throughout the year. Coupled with a decline in its microarray business and delays in the initiation of national genomics projects, Illumina’s global performance slowed, dampening market enthusiasm for the company.

Furthermore, Illumina’s proposal to acquire PacBio encountered significant resistance over the past year, including inquiries from regulatory authorities in the United Kingdom and the United States, as well as strong opposition from competitor Oxford Nanopore. Although Illumina offered to waive certain PacBio sequencing patents as part of the deal to facilitate the acquisition, the transaction ultimately failed to materialize. In the end, Illumina terminated the acquisition by paying a $98 million breakup fee.

In 2019, Thermo Fisher Scientific launched a new sequencing system centered on ease of use. Although its throughput metrics still lag behind those of competitors, the system emphasizes automation of the “sample-to-result” workflow and offers small- to medium-sized panel testing tailored for primary healthcare institutions that lack specialized personnel and dedicated facilities.

In the field of single-molecule long-read sequencing instruments, PacBio and Oxford Nanopore Technologies (ONT) have upgraded their existing platforms, increasing data output, reducing usage costs, and expanding application scenarios. In 2019, ONT successfully secured a new round of financing amounting to approximately $140 million. In addition to continuing to improve performance in detecting genomic structural variants, ONT has extended its applications to clinical detection of pathogens causing infectious diseases, food safety, and certain genetic disorders that are difficult to detect using PCR and next-generation sequencing (NGS). Meanwhile, leveraging the advantages of compact, portable instruments and simplified operation, ONT continues to focus on point-of-care testing (POCT) and on-site microbial detection, differentiating itself from short-read sequencing platforms. Furthermore, jointly winning the UAE population sequencing project with BGI has added significant weight to ONT’s future bids for national-level population cohort sequencing projects.

While making significant progress in private financing, other companies in the industry are also innovating in product development, striving to break Illumina’s dominance in the sequencer market. Genapsys, a next-generation sequencing company, announced the completion of $90 million in Series C financing and launched a small-to-medium throughput sequencer in the U.S. based on microfluidics and CMOS chip detection technology. Targeting the low-cost sequencer market, its primary customers are small and medium-sized laboratories. Two other companies employing novel DNA sequencing technology platforms—Omniome and Element Biosciences—have both secured substantial private funding from top-tier venture capital firms. Interestingly, founding team members at both companies have prior ties to Illumina. Although neither company has yet released a prototype sequencer, both have prioritized improving ease of use, increasing data output, and reducing costs as their core R&D objectives.

2. Early Diagnosis and Screening

Early diagnosis and screening emerged as another major hotspot in the overseas genetic testing sector in 2019. Over the past year, several companies secured substantial private equity financing. In addition to the “veteran” player Grail, which raised $125 million, emerging companies such as Thrive, Freenome, and Seer Bio completed financings of $110 million, $160 million, and $72.5 million (comprising $17.5 million in Series C and $55 million in Series D), respectively, in 2019.

From a technical roadmap perspective, early screening technologies are showing an increasingly diversified trend. To enhance detection metrics while keeping overall costs under control, companies are more inclined to adopt multi-marker combined testing (including DNA variants, methylation, fragmentomics, and plasma protein biomarkers). The methodological approach has also shifted from being dominated by genetic testing to a combined gene-plus-protein strategy (as seen with Thrive and Freenome), utilizing multi-target assays to improve the detection rate of early-stage tumors. Notably, Seer Bio has adopted a completely different approach from its competitors, pioneering the use of novel mass spectrometry technology to detect early tumor signals in blood through plasma protein biomarkers.

Oncimmune stands out by employing a multi-autoantibody panel for early cancer screening. In the published EarlyCDT-Lung clinical trial for lung cancer screening, patients randomly assigned to undergo the EarlyCDT test demonstrated a higher detection rate of early-stage lung cancer during the follow-up period.

For Grail, a super unicorn in the industry, 2019 was a pivotal year in its effort to turn the tide and shake off negative publicity surrounding its rapid cash burn in the early stages of development, management turbulence, and slow progress in clinical product development. Grail’s multi-cancer liquid biopsy test can highly specifically detect tumor signals in the blood of patients with 12 types of cancer, earning it the FDA’s Breakthrough Device Designation. Subsequently, the company published favorable results from an independent validation study of the test across 20 cancer types. Having successfully completed a financing round at the end of last year, Grail is now continuing to advance its various clinical trials with strong momentum.

Some leading oncology genetic testing companies that entered the capital markets early have also actively embraced the wave of early cancer screening. Guardant Health, which entered the oncology companion diagnostics market through liquid biopsy, has intensively invested resources in the early screening field. In early 2019, it acquired Bellwether Bio, integrating Bellwether’s cfDNA fragmentomics analysis technology into its existing ctDNA detection platform to form a combined early screening technology portfolio featuring DNA variants plus epigenetic markers (DNA methylation + fragmentomics). In the LUNAR-2 clinical validation trial for colorectal cancer, Guardant’s colorectal cancer early screening technology demonstrated favorable performance metrics. Subsequently, in mid-2019, the company launched the ECLIPSE large-scale prospective clinical trial for colorectal cancer screening, planning to enroll 10,000 average-risk volunteers to evaluate the clinical performance of its colorectal cancer early screening product through testing and follow-up.

Guardant’s flagship companion diagnostics business has also made significant progress. Following the prospective NILE clinical trial in lung cancer, which supported the adoption of ctDNA testing as a first-line diagnostic tool for lung cancer companion diagnostics, its core product, Guardant360, has secured coverage under the U.S. national health insurance program for diagnosing most solid tumors.

Exact Sciences, which built its foundation on early colorectal cancer screening, has seen continued strong sales momentum for its flagship product, Cologuard, benefiting from the expanded indication to include individuals aged 45–49. Last year, the company initiated a strategy of mergers, acquisitions, and investment expansion, acquiring genomic oncology testing company Genomic Health for a total consideration of $2.8 billion. In addition to gaining Genomic Health’s commercialized product portfolio (primarily comprising breast cancer adjuvant therapy products), Exact Sciences leveraged this opportunity to enhance its sample testing capacity and expand its regulatory affairs and sales teams, thereby laying a more solid foundation for the regulatory approval and commercialization of its upcoming early-screening new products.

Exact Sciences participated in the investment of Thrive Earlier Detection, an emerging early-screening company, to lay out new methodologies for early detection. In terms of clinical progress, the upgraded version of Cologuard is advancing smoothly, and the company has also made positive strides in the field of early liver cancer screening. Its early-stage liver cancer screening product, which combines DNA methylation markers with plasma protein testing, has demonstrated superior performance compared to traditional alpha-fetoprotein (AFP) testing, thereby earning Breakthrough Device Designation from the FDA.

3. Large-Scale Population Cohort Sequencing

In 2019, large-scale population cohort sequencing projects also achieved new breakthroughs. The UK Biobank and the Wellcome Trust charitable foundation formed a strategic partnership with four pharmaceutical companies (Amgen, AstraZeneca, GSK, and J&J): they will jointly invest £200 million to perform whole-genome sequencing on samples from 500,000 participants in the UK Biobank, aiming to identify methods for the prevention, diagnosis, and treatment of diseases such as Alzheimer’s disease and cancer. The UK Biobank has collected blood, urine, and saliva samples, along with comprehensive electronic health records, from volunteers. These phenotypic and genotypic data will be made openly accessible worldwide, providing robust support from medical big data for fields including genetics, medicine, public health research, and new drug development.

4. Single-Cell Sequencing

Companies in the single-cell sequencing sector achieved significant progress in 2019. In terms of private financing, Isoplexis, a single-cell proteomics company, secured nearly $50 million to accelerate the application of its single-cell immune biomarker detection platform in the discovery of novel therapies for cancer and other diseases.

10x Genomics is undoubtedly a leader in the field. After completing a $35 million Series D financing round in January, the company listed on NASDAQ in August, raising $390 million and achieving a market capitalization that briefly surpassed $10 billion. Subsequently, at the end of the year, the company launched its new spatial gene expression profiling product, elevating single-cell research tools to new heights.

The applications of single-cell sequencing continue to expand. Celsius Therapeutics, a company focused on leveraging single-cell omics analysis to guide new drug development, has entered into a collaboration with Janssen to help identify biomarkers that predict treatment outcomes in inflammatory bowel disease.

5. Consumer-Grade Genomic Testing

In 2019, overseas direct-to-consumer (DTC) genomic testing companies faced significant challenges. 23andMe, Ancestry, and Helix all announced layoff plans, while Veritas terminated all its U.S. operations due to funding issues. The decline in the total consumption of reagents and consumables (such as gene chips) for DTC testing also directly dragged down Illumina’s revenue.

There are three potential reasons for the overall market downturn: 1) Market saturation: 20–30 million people across the United States have already undergone direct-to-consumer (DTC) genetic testing, and the early-adopter segment in the U.S. that was curious about DTC testing is approaching saturation; 2) Limited utility: Ancestry information provided in test reports holds limited significance for users, and the clinical guidance value of individual genetic variant data for user health and medical decision-making remains immature; 3) Privacy and security risks: The use of DTC genetic data by U.S. law enforcement agencies to assist in apprehending suspects has heightened public awareness and concern regarding genetic privacy and security.

The future development of the overseas DTC sector requires a shift in target audiences and an enhancement of product offerings: 1) Transition from consumer-grade to medical-grade services: This includes registering and obtaining regulatory approval for genetic risk testing panels, providing genotyping services for population-based health cohort studies, and collaborating closely with pharmaceutical companies to explore new therapeutic targets and mechanisms of drug action; 2) Provide comprehensive solutions: Beyond delivering test reports, offer targeted products and services to patients, thereby creating a closed-loop ecosystem of testing followed by tailored products/services; 3) Strengthen health management information: Incorporate polygenic risk score (PRS) analysis algorithms and microbiome profiling into DTC testing to provide users with rich, long-term health insights.

6. Novel Detection Technologies

In the field of novel detection technologies, Adaptive Biotechnologies also listed on NASDAQ in 2019, raising $300 million. The company employs high-throughput sequencing methods to analyze T-cell and B-cell receptor sequences. Its minimal residual disease (MRD) detection product for acute lymphoblastic leukemia has been approved for market launch, with sensitivity far exceeding that of existing detection technologies. The company has also partnered with Microsoft to leverage sequencing analysis of immune cells in blood combined with machine learning to elucidate the relationship between the immune system and various diseases.

Mammoth Biosciences and Sherlock Biosciences are the two most representative companies in the field of disease diagnostic platforms based on CRISPR-Cas gene-editing systems. They were founded in 2017 and 2019, respectively, by Jennifer Doudna and Feng Zhang, the two leading figures in the gene-editing arena. Shortly after its establishment, Sherlock secured $35 million in Series A financing, while Mammoth recently closed a $45 million Series B round. The core focus of both companies’ product development is rapid CRISPR-based nucleic acid diagnostics. During the COVID-19 pandemic, Sherlock also released a corresponding rapid viral RNA detection solution, significantly streamlining sample processing and analysis workflows.

The emergence of Cradle Genomics in the field of reproductive genetics has reignited enthusiasm for the further development of non-invasive prenatal testing (NIPT). The approach of performing non-invasive fetal genetic testing using trophoblast cells collected from the cervix holds promise for enabling more comprehensive detection of genetic disorders at an earlier stage of pregnancy and at a lower cost.

ArcherDx is dedicated to leveraging Anchored Multiplex PCR (AMP) library preparation technology for the detection of gene fusions and mutations. The company completed two rounds of financing in 2019, raising a total of $115 million. ArcherDx’s proprietary PCR-based library preparation technology enables the simultaneous detection of novel gene fusions and mutations. Subsequently, the company entered into a collaboration with Illumina on the development of in vitro diagnostic (IVD) products.

7. Other Notable Product Registration Updates

NantHealth’s Whole Exome Sequencing (WES) Oncology Product Receives FDA Approval. The approval was based on results from concordance validation of mutation detection against the FDA-approved MSK-IMPACT 468-gene panel. In addition to reporting somatic mutations in these 468 genes (with a mutation frequency as low as 2%), the product can also detect tumor mutational burden (TMB) in cancer tissues. This is the first WES diagnostic product approved by the FDA for detecting tumor mutational burden (TMB) in solid tumors.

Tumor mutational burden (TMB) was once considered an important biomarker for predicting the efficacy of immune checkpoint inhibitors. However, its predictive value was repeatedly challenged in multiple clinical trials conducted in 2019. In several clinical trials carried out by Bristol-Myers Squibb (BMS) and Merck & Co. (MSD), the outcomes of immunotherapy combination regimens (immunotherapy plus immunotherapy or immunotherapy plus chemotherapy) were highly similar regardless of TMB levels. The negative results may be attributed to the combination therapy itself or to the lack of standardization in TMB detection methods. Therefore, although whole-exome sequencing (WES)-based TMB testing products have received regulatory approval, their practical clinical utility remains to be confirmed through further clinical trials.

Vela Diagnostics’ NGS-based assay for detecting HIV-1 drug-resistance mutations received FDA marketing approval in 2019. Cleared through the FDA’s De Novo pathway, this test kit is the first innovative product to employ next-generation sequencing (NGS) methodology for HIV genotyping and drug-resistance testing.

Bio-Techne’s exosome-based prostate cancer diagnostic product has received FDA Breakthrough Device Designation, becoming the first exosome liquid biopsy product to earn this distinction, and is recommended by the NCCN Clinical Practice Guidelines in Oncology for Prostate Cancer.

LAM’s early screening product for liver cancer has received the FDA Breakthrough Device Designation. This product enables non-invasive detection of early-stage liver cancer based on ctDNA methylation signals, achieving high accuracy.

Prescient Metabiomics’ colorectal cancer screening product, LifeKit Prevent, has received FDA Breakthrough Device designation. Unlike current fecal DNA-based colorectal cancer screening products on the market, this product detects adenomas and early-stage colorectal cancer by analyzing DNA and RNA markers in fecal microbiota, rather than human-derived DNA.