China's Medical Informatization Market Reaches Approximately RMB 58.2 Billion: Insights from 2019 Bidding Data

In“Analysis of Winning Bid Data for Medical Informatics in 2019: Highest Bid Amount Approaches RMB 120 Million, with Tertiary Hospitals Accounting for 60% of Demand”In the analytical report, we conducted a statistical analysis of the basic dimensions of the healthcare informatization procurement data sample. Next, we will perform cross-comparisons on the granular dimensions of the data, aiming to derive more in-depth analytical insights.

These granular dimensions are highly intriguing. For instance, what are the differences in IT product requirements between tertiary and secondary hospitals? How do needs differ between coastal provinces and municipalities versus less developed inland regions? Which companies have secured the highest number of bids and the largest contract values? Let’s take a closer look.

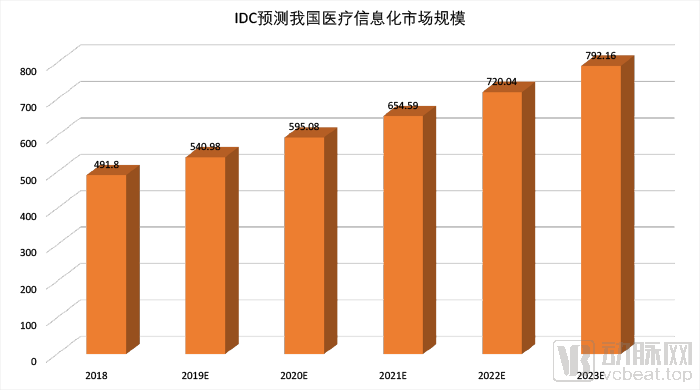

Estimated Market Size of China's Healthcare Informatics Industry

In recent years, the growth rate of healthcare informatization in China has been remarkably rapid, to the extent that major consulting firms have had to continuously update their data. The report “IDC: China Healthcare IT Market Forecast, 2017–2021,” released by IDC in 2016, stated that the total market size for healthcare informatization in China was RMB 8.746 billion in 2009 and grew to RMB 26.879 billion in 2015. The report also projected that the total market size would reach RMB 36 billion in 2018 and RMB 39.356 billion in 2019.

In May 2019, IDC revised its forecasts in the newly released report, “China Healthcare IT Market Forecast, 2019–2023.” Actual IT spending in China’s healthcare industry reached RMB 49.18 billion in 2018, which was 36.6% higher than the previous forecast. Consequently, IDC updated its projection, estimating that the healthcare informatization market will achieve a compound annual growth rate (CAGR) of 10% from 2018 to 2023. Based on this forecast, the size of China’s healthcare informatization market is expected to be approximately RMB 54 billion in 2019 and reach RMB 79.16 billion by 2023.

However, we believe that the market size of healthcare informatization may be more optimistic than this forecast. There are two reasons: first, policy promotion has increased the existing market; second, the increase in medical institutions has provided incremental market growth.

China’s healthcare industry is currently experiencing comprehensive and robust growth. The state continues to advance the implementation of the “Healthy China” national strategy, while simultaneously promoting policy-driven reforms in the pharmaceutical and healthcare systems. Specific directions for development and innovative implementation in healthcare informatization—such as smart hospitals, medical consortia, and “Internet + Healthcare”—are being actively propelled forward.

In early 2019, the state further clarified the definition and connotation of "smart hospitals," which primarily encompass three major areas: electronic medical records (EMR) for medical staff, smart services for patients, and smart management for administrators. This signifies that the state has established clear standard requirements for smart hospital construction across three critical dimensions—medical personnel, patients, and management—which will serve as a key driver for the high-quality development of healthcare services and the enhancement of patient service experiences in China. Currently, the state has officially issued tiered evaluation requirements for EMR systems and smart services, with evaluation standards for smart management to be released subsequently.

Meanwhile, the state will also promote the formation of a tiered diagnosis and treatment pattern, focusing on pilot construction of urban medical consortia and closely-knit county-level medical communities: In early 2019, the National Health Commission explicitly stated that it would vigorously advance pilot programs for medical consortium construction, establishing 100 urban medical groups and 500 county-level medical communities nationwide.

In May 2019, the national government issued the “Notice on Launching Pilot Programs for the Construction of Urban Medical Consortia” and the “Notice on Advancing the Construction of Close-knit County-level Healthcare Communities.” The documents explicitly stated that by the end of 2019, 100 pilot cities would fully implement grid-based layout and management for urban medical consortia; by the end of 2020, these 100 pilot cities would establish a grid-based layout for medical consortia with significant results achieved, and a new type of county-level healthcare service system would be initially established in 500 counties (including county-level cities and municipal districts). The construction of medical consortia will further promote the development of the regional health informatics product market.

In June 2019, the Chinese government released the "Key Tasks for Deepening the Reform of the Medical and Healthcare System in 2019," which explicitly outlined comprehensive performance assessments for all tertiary public hospitals, in-depth implementation of the Action Plan for Improving Medical Services, and coordinated advancement of comprehensive medical reforms at the county level. The document clearly stated that information technology would continue to drive and empower the deepening of healthcare reform by addressing informatization needs such as the construction of a national platform and provincially coordinated regional platforms for interconnected universal health information, online services and telemedicine for residents, and hospital performance evaluations.

Meanwhile, following the 2018 issuance at the national level of policy documents including the “Opinions on Promoting the Development of ‘Internet + Healthcare’,” as well as regulatory standards for internet-based diagnosis and treatment, internet hospital management, and remote medical services, nearly 20 provinces (municipalities directly under the Central Government and autonomous regions)—including Guangdong, Gansu, Jilin, Anhui, Shanxi, and Tianjin—intensively rolled out implementation opinions on “Internet + Healthcare” in 2019. These provincial-level initiatives defined specific construction objectives and implementation pathways to advance the development of “Internet + Healthcare.”

Meanwhile, in 2019, the National Health Commission will continue to implement the requirements set forth in the “Notice on Issuing the Work Plan for Comprehensively Enhancing the Comprehensive Capabilities of County-Level Hospitals (2018–2020),” namely that by 2020, 500 county hospitals (including some in impoverished counties) and county traditional Chinese medicine (TCM) hospitals shall meet the service capability standards for “Grade III General Hospitals” and “Grade III TCM Hospitals,” respectively. This aims to ensure that 90% of county general hospitals and county TCM hospitals across China meet the basic standards for medical service capabilities. Such capacity building includes improvements driven by informatization initiatives.

Beyond this, China’s healthcare system has also exposed certain urgent issues during the COVID-19 pandemic. In the fight against the epidemic, emerging medical information technologies have played a significant role. Telemedicine, remote diagnosis and treatment data sharing, biopharmaceuticals, and medical devices are considered important components of the currently popular “new infrastructure” concept. All of these will drive substantial development in China’s healthcare informatization and hospital informatization construction.

The above outlines the impact of policy-driven initiatives on the healthcare informatics market. On another front, according to the latest data from the “2018 Statistical Bulletin on the Development of China’s Health and Family Planning Services,” the total number of hospitals in China reached 33,009 by the end of 2018, an increase of 1,953 compared with 2017. These newly added hospitals will also need to invest from scratch in their informatization construction.

According to the "Survey Report on the Informatization Status of Chinese Hospitals (2018-2019)" released by CHIMA, which surveyed 1,909 hospitals and estimated figures using the interval median replacement method, the average planned investment in informatization construction over the next two years is RMB 16.6769 million for tertiary hospitals and RMB 4.9669 million for hospitals below the tertiary level. By multiplying these figures by the total number of secondary and tertiary hospitals in China (9,017 secondary hospitals and 2,548 tertiary hospitals), the total amount reaches RMB 87.28 billion.

Of course, it is unlikely that all hospitals will simultaneously carry out information technology construction every year. The survey report by CHIMA also indicates that 66.53% of hospitals establish a fixed annual budget for information technology construction.Based on this ratio, we can simply estimate that the market size of medical informatics in 2019 is projected to reach RMB 58.067 billion, approaching RMB 60 billion.

Analysis and Deconstruction of Sub-Dimensions in the 2019 Bidding Data for Informatics in Public Hospitals

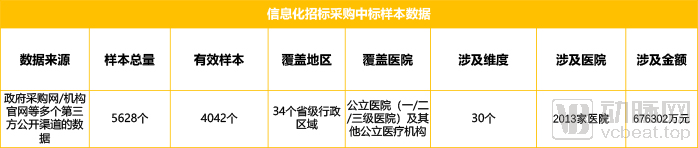

Data Sample Sources and Description:

The VCBeat Data Team monitored publicly available winning bid samples for medical informatics procurement tenders on the China Government Procurement Network in 2019, collecting a total of 5,628 records. Through secondary structural processing of the data, we extracted 4,042 valid samples, involving a total amount of RMB 6.76 billion.

Public healthcare institutions in China are classified as public service entities. In accordance with the Government Procurement Law of the People’s Republic of China, government agencies may conduct procurement through open tendering, invited tendering, competitive negotiations, single-source procurement, request for quotations, and other methods recognized by the State Council’s department responsible for supervising and administering government procurement; however, open tendering shall serve as the primary method of government procurement. Meanwhile, the estimated value covered by the sample accounts for more than 10% of the market size of China’s healthcare informatization sector in 2019 (RMB 58.067 billion). The data sample is sufficiently large to reflect the basic conditions of the healthcare informatization market and is quite representative, although VCBeat does not guarantee its comprehensiveness.

The entire data sample encompasses 30 dimensions, including bidding type, release date, province and city, government procurement, procurement project name, procuring entity, winning bidder, winning bid amount, and informatization classification. In“Analysis of Winning Bid Data for Medical Informatics in 2019: Highest Bid Amount Approaches RMB 120 Million, with Tertiary Hospitals Accounting for 60% of Demand”In this section, we conducted a basic data analysis of the winning bid samples for informatization tendering and procurement based on the aforementioned dimensions. Next, we will focus on the analysis of cross-dimensional data.

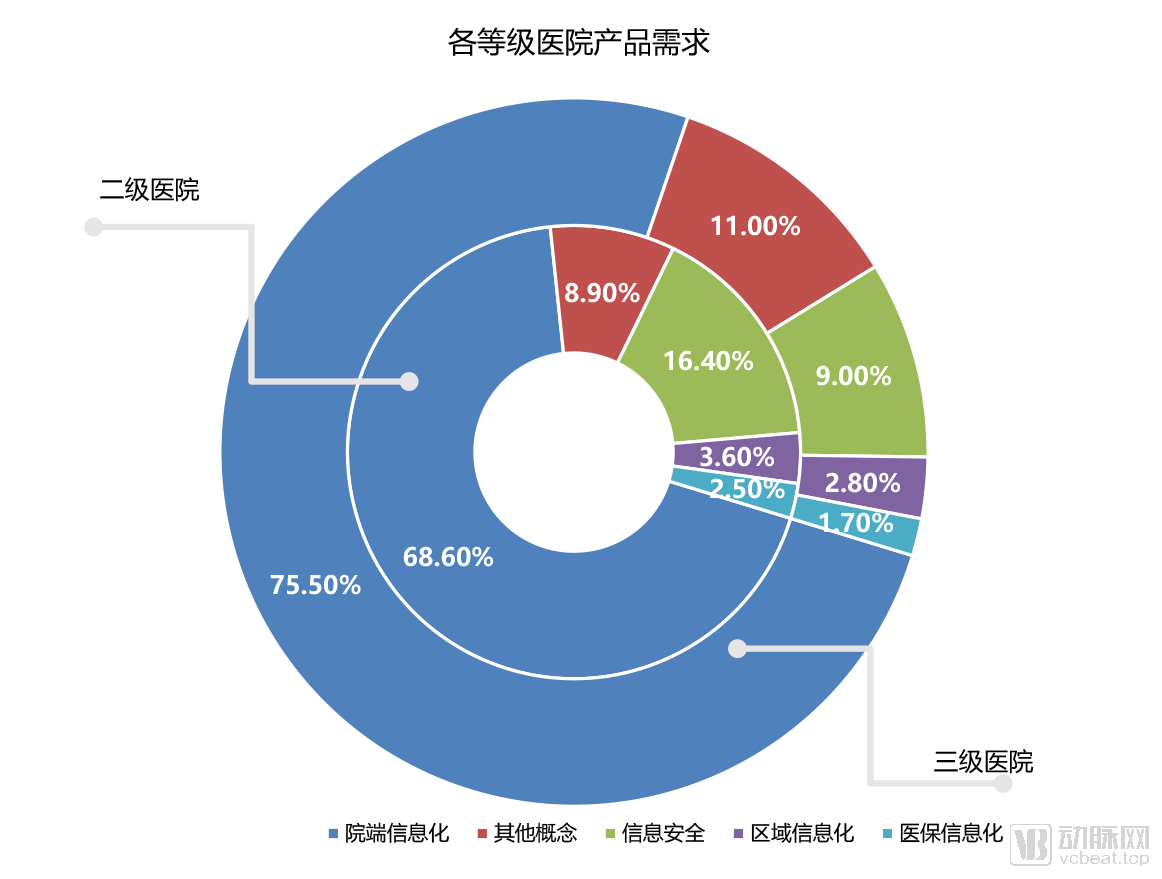

Overview of Procurement by Hospital Tier

Data Source: VBInsight Database

Based on our cross-tabulated analysis of hospitals at different tiers and their procurement of IT products, it is evident that there are significant differences between secondary and tertiary hospitals in certain areas. The most pronounced distinction lies in the differing proportions allocated to information security projects.

The proportion of secondary hospitals procuring information security solutions reached 16.4%, nearly double that of tertiary hospitals. We believe this does not necessarily indicate that secondary hospitals place greater emphasis on information security than tertiary hospitals. In fact, the “2017–2018 Survey Report on the Status of Hospital Informatics in China,” released by the Information Professional Committee of the Chinese Hospital Association, noted that tertiary hospitals significantly outperformed hospitals below the tertiary level in implementing classified protection assessments. Furthermore, the adoption rate of such assessments was higher in economically developed regions than in moderately developed and less developed regions. Relatively speaking, tertiary hospitals began their informatics construction earlier and achieved a higher level of informatization, having already completed their information security infrastructure during the course of their digital transformation.

As early as 2011, the National Health Commission issued the “Guiding Opinions on Information Security Classified Protection in the Health Industry,” which stipulated that critical business systems of tertiary hospitals must pass Level 3 classified protection assessment, while those of secondary hospitals must pass Level 2 assessment.

In 2016, the National Health Commission issued the "2016 Evaluation Methods for the Accreditation Standards of Tertiary General Hospitals (Complete Version)," which re-emphasized that core business systems of tertiary hospitals must achieve Level 3 certification under the Classified Protection of Cybersecurity Multi-Level Protection Scheme (MLPS) to meet the cybersecurity requirements stipulated in the tertiary hospital accreditation standards. This marked the first time that mandatory information security requirements were imposed on tertiary hospitals.

By 2018, the National Health Commission’s “Administrative Measures for Standards, Security, and Services of National Health and Medical Big Data (Trial)” stipulated that platforms hosting health and medical big data must comply with the Classified Protection of Cybersecurity. Since hospitals adopting big data technologies are typically Grade A tertiary hospitals, their cybersecurity classified protection assessments are primarily conducted at Level 3. Meanwhile, the “Administrative Measures for Internet Hospitals (Trial)” also requires that platforms supporting internet hospitals pass the Level 3 assessment of the cybersecurity classified protection evaluation.

It is evident that prior to the release of the Multi-Level Protection Scheme (MLPS) 2.0 standards, tertiary hospitals had already become key targets for MLPS assessments and had largely completed their information security infrastructure development. Current projects primarily serve to address remaining gaps or facilitate system upgrades.

In May 2019, the state released the "Standard for Classified Protection of Cybersecurity 2.0," which was scheduled to take effect on December 1, 2019. This standard adheres to the Cybersecurity Law. As a mandatory regulation, failure to pass the MLPS 2.0 assessment constitutes a legal violation. Consequently, many Tier II hospitals that had not yet undergone assessment procured information security projects within the year to meet the requirements of the new MLPS evaluation.

We believe that changes in the procurement proportion of information security projects across hospitals of different tiers have led to corresponding shifts in the share of other project types, such as hospital-side informatization, within the procurement portfolios of secondary and tertiary hospitals. In the areas of regional informatization and medical insurance informatization, the proportions for secondary and tertiary hospitals show little disparity, remaining at comparable levels.

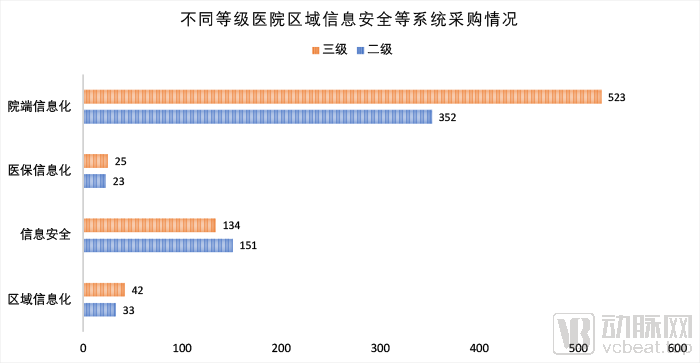

We conducted a detailed multi-dimensional comparative analysis of 2,199 health information system projects tendered by hospitals (with the remaining projects tendered by institutions such as the National Health Commission) to examine the differences in information system procurement among hospitals of different tiers.

Since a significant portion of the sample data could not be disaggregated by specific hospital classifications, such as Grade III Class A or Grade III Class B, we decided to use “Grade III” and “Grade II” as unified categories after several attempts. Additionally, many hospital-side informatization projects did not specify their types and thus could not be further detailed; moreover, their data volumes differed significantly from those that could be disaggregated, making it inappropriate to present them in the same chart. For these data points, we uniformly labeled them as “Hospital-Side Informatization” and grouped them together with other categories such as Medical Insurance Informatization, Information Security, and Regional Informatization.

Data Source: VBInsight Database

In terms of the number of procurements for medical insurance information systems, there is little difference between tertiary and secondary hospitals, indicating that demand for such essential systems is not sensitive to hospital classification. Since tertiary hospitals are required to assume greater responsibility within regional information systems, they also have a higher number of tenders for regional informatization compared to secondary hospitals. Regarding hospital-side informatization, tertiary hospitals clearly lead in procurement volume, which aligns with their greater emphasis on IT infrastructure and larger resource allocations for digital transformation. As previously mentioned, due to requirements for Multi-Level Protection Scheme (MLPS) assessments, secondary hospitals procure more information security systems; this represents one of the few areas where secondary hospitals surpass tertiary hospitals in procurement volume for information systems.

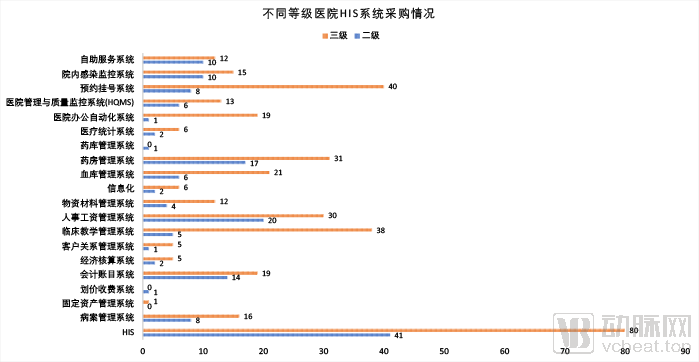

Data source: Artery Orange Database

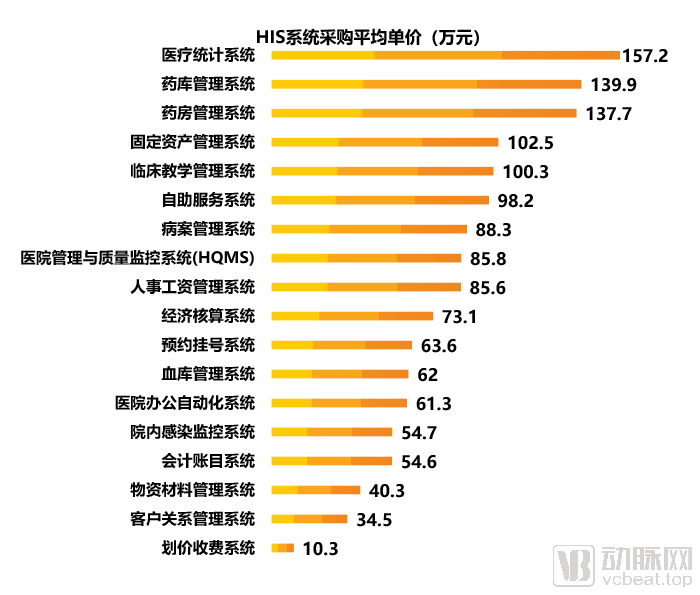

Significant disparities are evident in the adoption of Hospital Information Systems (HIS) across hospitals of different tiers. Except for a limited number of systems, such as self-service kiosks and accounting software, where procurement volumes at Tier-2 hospitals approach those of Tier-3 hospitals, Tier-2 hospitals lag significantly behind in most other areas. The procurement volumes for appointment scheduling systems, hospital office automation systems, clinical teaching management systems, and customer relationship management systems at Tier-3 hospitals are 5 times, 19 times, 7.6 times, and 5 times those at Tier-2 hospitals, respectively. Taking the appointment scheduling system as an example, Tier-3 hospitals generally offer online appointment registration via platforms like WeChat, greatly alleviating the difficulty of securing appointments. This highlights the substantial gap in informatization levels between Tier-2 and Tier-3 hospitals and underscores the significant market potential for IT infrastructure development in Tier-2 hospitals.

It should be noted that some tender projects are presented in the form of general contracting, or it is impossible to determine which specific part they belong to. For this portion of data, we uniformly categorize them under the “HIS” label.

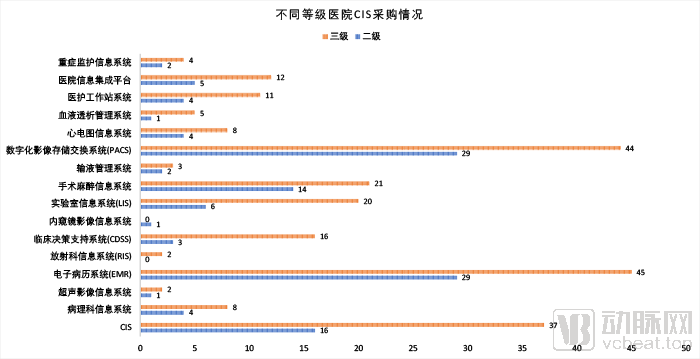

Data Source: VCBeat Orange Database

Among CIS subsystems that are closely relevant to clinical practice, a significant gap remains between tertiary and secondary hospitals. However, this disparity is relatively smaller than that observed in HIS systems. The largest gap is seen in Clinical Decision Support Systems (CDSS), with the number of tenders in tertiary hospitals being 5.33 times that of secondary hospitals. Due to their substantial contribution to clinical care, the value of CDSS in clinical applications has been validated by practice. Nevertheless, this does not necessarily indicate that secondary hospitals place insufficient emphasis on these systems; limited budgets may also be a major contributing factor. Among projects with considerable disparities between tertiary and secondary hospitals, hemodialysis management systems rank second, with a ratio of 5:1. Given the trend of shifting chronic disease management to primary care institutions, secondary hospitals clearly have significant room for growth in this area.

Consistent with the situation in HIS, some tender projects appear in the form of general contracting, or it is impossible to determine which specific part they belong to. For this part of the data, we uniformly classify them under the "CIS" label.

Data Source: VBBeat Orange Database

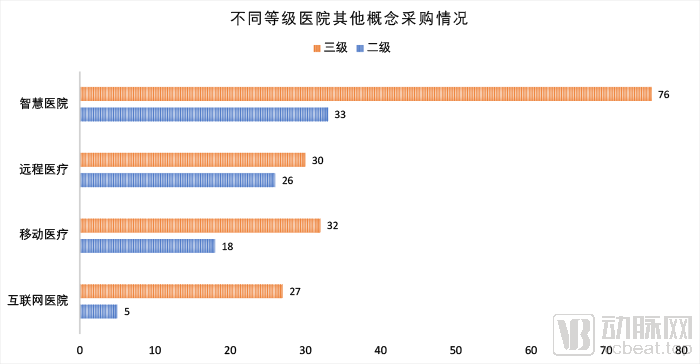

In tendering and procurement across other categories, a significant gap remains between tertiary and secondary hospitals. The largest disparity is seen in internet hospitals, where the number of tenders issued by tertiary hospitals is 5.4 times that of secondary hospitals. The only category in which the number of tender projects is relatively close between the two tiers is telemedicine, with secondary hospitals issuing just four fewer tenders than tertiary hospitals.

Data Source: Artery Orange Database

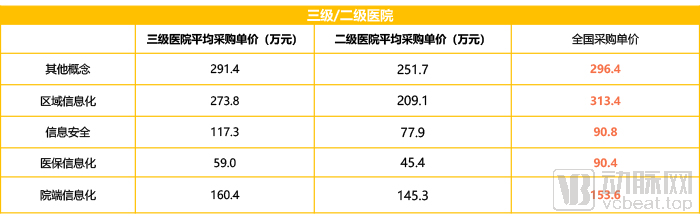

Differences are also evident in the unit procurement prices of informatization projects across different hospital tiers. Among all five major categories of informatization projects, the average unit procurement price at tertiary hospitals is higher than that at secondary hospitals. Notably, the average unit prices for regional informatization projects and information security projects at tertiary hospitals are 31% and 50.6% higher, respectively, than those at secondary hospitals, highlighting significant disparities.

On the one hand, tertiary hospitals receive greater emphasis and have more ample budgets compared to secondary hospitals. The CHIMA survey report indicates that the average planned investment in informatization construction over the next two years for tertiary hospitals is RMB 16.6769 million, which is more than three times the average for hospitals below the tertiary level (RMB 4.9669 million). Consequently, they are often able to select solutions with superior performance and more comprehensive functionality during procurement, naturally resulting in differences in unit prices. On the other hand, as previously mentioned, it is typically tertiary hospitals that introduce big data into regional informatization systems, leading to relatively higher requirements for information security. Therefore, this also results in significant differences in unit prices between secondary and tertiary hospitals for these two projects.

Demand for Informatics Products in Medical Institutions by Province

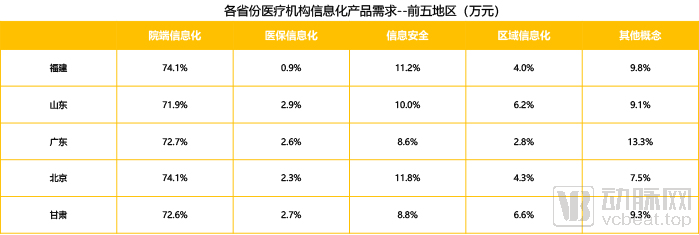

Based on our previous statistics, the top five provinces in terms of the number of healthcare informatization procurement projects are Fujian, Shandong, Guangdong, Beijing, and Gansu. So, what is the distribution pattern in the selection of informatization products by hospitals in these leading provinces?

Data Source: Arterial Orange Database

While the top five provinces differ in the specific breakdown of project types, the macro-level variations are not significant. Hospital-side informatization remains the largest category across all provinces, generally hovering around the median of 71.2%. Since public hospital procurement is heavily dependent on government funding, each province’s distinct focus reflects its local conditions and serves as an indicator of its informatization progress. For instance, the notably higher proportion of regional informatization projects in Shandong and Gansu suggests that both provinces were in a critical phase of regional infrastructure development in 2019.

Guangdong’s relatively low share in information security and regional informatization should not be interpreted as a lack of emphasis on these areas. In fact, Guangdong is undoubtedly among the leading tier in China in terms of healthcare informatization, having been an early adopter in both information security and regional informatization initiatives. We believe that its lower proportion is partly because construction in regional informatization and information security started earlier and has reached a mature stage, moving past the period of intensive investment. On the other hand, Guangdong accounts for a significantly higher share in other categories, which compresses the proportional representation of other types of projects.

Notably, the “other concepts” category includes internet hospitals, smart hospitals, mobile health, and telemedicine. Guangdong’s disproportionately high share in this area further demonstrates that the province, which ranks among the top tier in informatization, has significantly increased its investments in these emerging fields.

Data Source: VCBeat Orange Database

Data Source: VCBeat Orange Database

As open tendering has been implemented for an extended period, pricing for healthcare informatization projects has become relatively transparent. Coupled with competitive market forces, it is unlikely that there will be significant price disparities among comparable products from different vendors. In light of the previously observed differences in average prices for sub-projects within the most popular Hospital Information System (HIS) and Clinical Information System (CIS) categories across basic dimensions, it can be inferred that such variations primarily stem from differing provincial procurement preferences for various subsystems. A higher average project unit price indicates a greater proportion of locally procured, higher-priced informatization systems.

Among the top five provinces by procurement volume of informatization systems, there are significant disparities in the average unit price for similar projects across different regions. Guangdong and Beijing rank highest in terms of unit prices for hospital-side informatization, with a substantial lead, reflecting their strong commitment to the development of hospital information systems.

In other concepts representing the development direction of internet healthcare, Beijing and Fujian rank in the top two, indicating their investment in emerging medical informatization. In particular, the unit price level in Beijing is more than double that of the regions ranked third and fourth, demonstrating the standard expected of a leading hub for internet healthcare.

Gansu has surprisingly entered the top two in terms of unit prices for medical insurance informatization, information security, and regional informatization, matching Beijing with three such categories. This is quite unexpected. Particularly in medical insurance informatization and regional informatization, its project unit prices are significantly higher than those of the other top five provinces. Although Gansu lags behind in both medical resources and medical informatization construction, the relatively high unit price for medical insurance informatization—a rigid demand—may indicate that the region is working to address previous shortcomings. Meanwhile, the characteristic of vast territory with a sparse population means that experiences from developed regions may not be directly applicable to Gansu, which is likely one of the reasons why the local government places greater emphasis on regional informatization construction.

As a major province in terms of both economy and population, Shandong did not rank in the top two for unit prices across various systems. In fact, it ranked relatively low in most categories. Although its total procurement volume ranked fourth nationwide, this was primarily driven by a high number of projects rather than higher individual values. This suggests that local investment is distributed rather evenly, while also reflecting to some extent that the region’s healthcare informatization is “large in scale but not strong in capability.” Given Shandong’s economic standing, we believe there is still significant room for future growth.

Correlation Between Provincial Economic Levels and IT Procurement

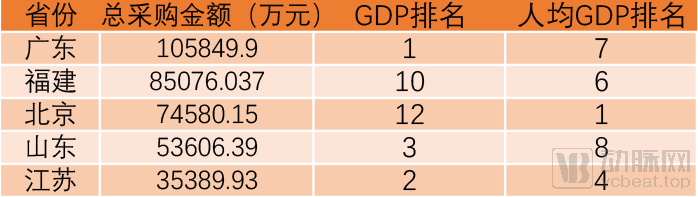

# How Strong Is the Correlation Between Provincial Economic Development and Healthcare Informatics Maturity? We retrieved publicly available 2018 GDP data for each province from the National Bureau of Statistics, ranked them, and performed a cross-comparison with procurement amounts in the statistical sample.

Data Source: VCBeat Orange Database and National Bureau of Statistics

In our statistical sample, the top five regions by procurement amount are Guangdong, Fujian, Beijing, Shandong, and Jiangsu. This ranking significantly overlaps with the top five regions by GDP—Guangdong, Jiangsu, and Shandong also rank among the top three in GDP (followed by Zhejiang and Henan). Although Fujian and Beijing do not rank highest in absolute GDP terms (10th and 12th, respectively), their per capita GDP figures are exceptionally high, ranking 1st (Beijing) and 6th (Fujian), underscoring their considerable affluence. There is a strong correlation between regional economic development and the adoption of healthcare informatics.

Data Source: VCBeat Orange Database and China Health Yearbook

Local government health expenditures are closely linked to the potential market size for healthcare informatization in each region. According to statistics from the 2019 China Health Statistics Yearbook, nearly half of the top ten regions in terms of government health spending in 2018 did not rank among the top ten in total procurement amount. This indicates that the market space for healthcare informatization in these regions is far from saturated and still holds significant room for growth.

It is worth noting that our data samples were sourced from the Government Procurement Network, where significant data gaps exist for certain provinces. For instance, the total tender amounts for Zhejiang and Hunan show noticeable discrepancies compared to actual conditions. We infer that this may be because major procurement data for some provinces are published on other procurement announcement platforms. In future reports, we will further expand the sources of our data collection to ensure a more comprehensive dataset.

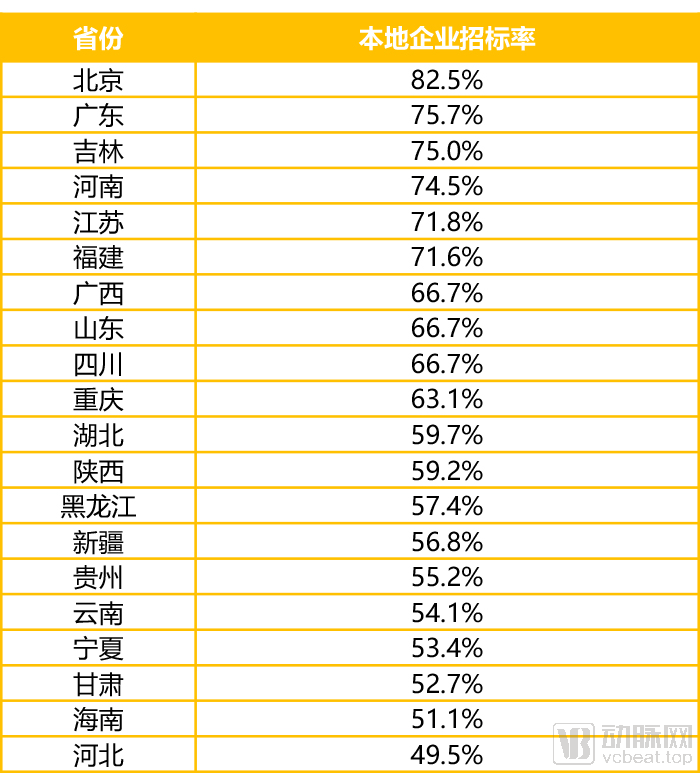

Data Source: Artery Orange Database

The local enterprise bid-winning rate refers to the proportion of bids won by enterprises within their home province, which can, to some extent, indicate the degree of preference for local enterprises in procurement activities. To mitigate the impact of missing data on the analysis, we selected the top 20 provinces in China by total tender amount for examination. Furthermore, the procurement expenditure in each of these provinces exceeded RMB 100 million, ensuring sufficient statistical robustness. According to the statistics, the top five provinces with the highest local enterprise bid-winning rates are Beijing, Guangdong, Jilin, Henan, and Jiangsu, in that order. Notably, Beijing, Guangdong, and Jiangsu are widely recognized as regions with a high concentration and advanced development of medical informatics companies in China, and they also rank among the leading areas in terms of the distribution of successful bidders.

In addition, Zhejiang is a region in China with a relatively high concentration of healthcare IT enterprises, ranking among the top in terms of the distribution of winning bidders. In fact, among the sample data, local enterprises in Zhejiang had the highest bidding rate; however, due to their low ranking in terms of winning bid amounts, we considered the sample data to contain significant errors and thus excluded it from our analysis.

Although IT enterprises in Henan Province have relatively low visibility, they rank eighth in the distribution of winning bidders. It is therefore reasonable that companies from these regions exhibit a high bid-winning rate. However, Jilin Province ranks only 16th with a 1.7% share in the distribution of winning bidders, yet its local companies’ bid-winning rate ranks third at 75%. This may indicate a significant level of local protectionism.

Companies have also recognized this objective reality and taken a series of measures to circumvent it. The most typical approach is establishing local subsidiaries in an effort to secure relatively fair treatment in bidding processes.

Driven by the consideration of supporting local enterprises, provinces tend to prioritize procurement from businesses within their own jurisdictions. This is a normal phenomenon and not unique to China; even in Western countries that champion free-market economies, numerous trade barriers remain in place to protect domestic industries. The key issue lies in ensuring that support for local enterprises is reasonable and moderate, rather than unrestrained.

Which companies have the highest number of successful bids?

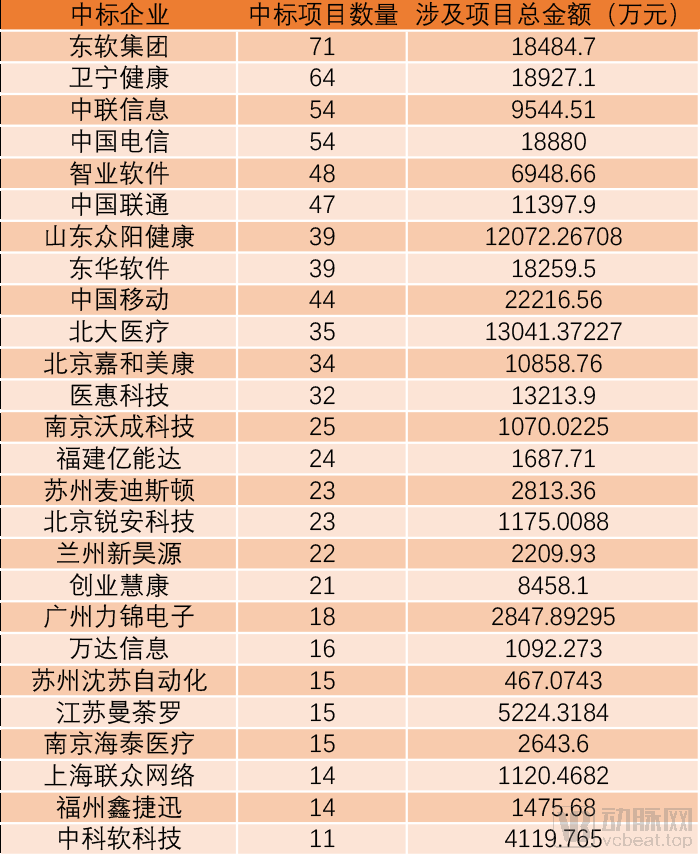

So, which IT companies rank at the top in tenders? We have compiled statistics and listed the top 20 based on the number of winning bids and the total winning bid amount. It should be noted that since there is a large amount of winning bid data from branch offices and subsidiaries in the tender data, we used the enterprise association graph from Qichacha to confirm whether they are affiliated companies. The data for these affiliated companies is all attributed to the parent company. Taking Neusoft as an example, we include its affiliated companies such as Dongruan Wanghai, XIKANG, and various local branches under the Neusoft Group.

It should be noted that our analysis is based solely on the statistical data from the current sample, which is representative but not comprehensive, and therefore does not reflect the full status of the winning bidders. For comprehensive official corporate data, please refer to official documents such as annual reports published by each enterprise. In case of any discrepancy between the sample data and the actual situation of the enterprise, the official corporate data shall prevail.

Data Source: VCBeat Orange Database

Among the top 20 companies ranked by the number of won bids, Neusoft ranked highest, with its affiliated companies securing a total of 71 projects, involving an amount of RMB 184.847 million. Following closely was Winning Health Technology Group Co., Ltd., which won 64 projects. However, in terms of contract value, Winning Health’s 64 projects totaled RMB 189.271 million, surpassing that of Neusoft, thereby demonstrating higher project value. Chongqing Zhonglian and China Telecommunications Group Co., Ltd. tied for third place, each winning 54 projects. Nevertheless, there was a significant disparity in their contract values: China Telecom’s total contract amount reached RMB 188.8 million, far exceeding Chongqing Zhonglian’s RMB 95.4451 million. This difference is reasonable, considering that China Telecom’s projects primarily involved communication system hardware integration, which typically commands higher contract values.

The top 20 companies won a total of 817 bids, accounting for 20.2% of the 4,042 projects awarded to more than 200 companies.

Data Source: Artery Orange Database

Among the top 20 companies by contract value, China Mobile Communications Group Co.,Ltd. ranked highest, with 44 projects totaling RMB 222.1656 million. China Telecommunications Group Co.,ltd. showed a similar pattern, with 54 projects amounting to RMB 188.8 million. However, the winning bids for these two telecommunications operators were predominantly high-value, highly concentrated communications system integration projects, representing a special case. Winning Health Technology Group Co.,Ltd. ranked second, with a total contract value of RMB 189.271 million. Whether measured by the number of projects or total contract value, Winning Health secured a top-two position, demonstrating the strong foundation of this established healthcare IT enterprise.

Excluding the two telecommunications carriers, China Mobile and China Telecom, Winning Health Technology Group Co.,Ltd. ranks first in terms of total contract value, followed by Neusoft (RMB 184.847 million) and DHC Software Co.,Ltd. (RMB 182.595 million). Notably, DHC Software Co.,Ltd. achieved a total value of RMB 182.595 million with only 39 projects, resulting in an average project value of RMB 4.8619 million. This high per-project figure, comparable to that of telecommunications carriers, underscores the substantial value and quality of its projects.

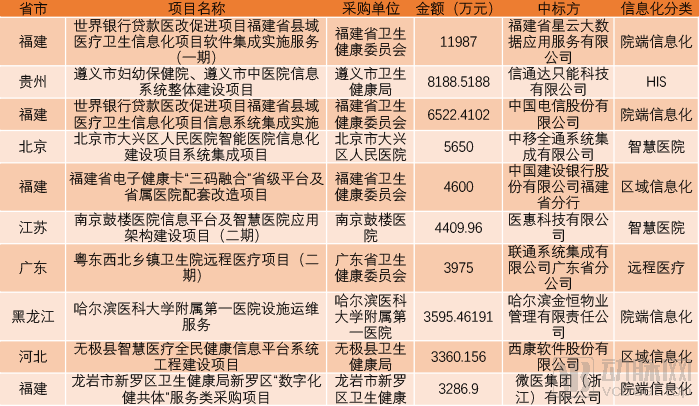

Among the top ten projects by winning bid amount, the top three are all hospital-side informatization projects, which account for half of the top ten. The next category comprises other concepts, with three projects; the remaining two spots are taken by regional informatization projects.

Data Source: VCBeat Orange Database

Among the top ten projects, most are bundled packages commissioned by local Health Commissions, resulting in relatively high prices. For instance, the top-ranked project is the “Software Integration and Implementation Services for the Fujian County-Level Healthcare Informatics Project under the World Bank Loan Healthcare Reform Promotion Project,” tendered by the Fujian Provincial Health Commission, with a contract value reaching RMB 119.87 million. Judging from the project title, it is clearly an informatics initiative implemented across county-level medical institutions throughout Fujian Province. Overall, such projects account for seven of the top ten spots.

Among the top ten projects ranked by total bid amount, three were implemented by hospitals. Notably, the Smart Hospital Information Construction Integration Project of Beijing Daxing District People's Hospital ranked fourth among all projects, with a bid amount of RMB 56.5 million. In addition, the Smart Hospital Project of Nanjing Drum Tower Hospital and the Hospital-Side Informationization Project of the First Affiliated Hospital of Harbin Medical University ranked sixth and eighth, respectively.

When viewed by region, Fujian Province accounted for four of the top ten projects by total amount, with the first- and third-ranked projects both located in Fujian. Given that Fujian also ranked among the leaders in both the number of procurement projects and the total procurement amount, it is evident that the province made substantial investments in healthcare informatization in 2019. In addition to Fujian’s four entries, Guizhou, Beijing, Jiangsu, Guangdong, Heilongjiang, and Hebei each had one project selected.

Final Remarks

Through analysis of basic and segmented dimensions, we have gained a certain understanding of the procurement of information systems in medical institutions in 2019. Sample statistics reveal significant disparities in informatization construction among hospitals of different tiers.

Tertiary hospitals hold an absolute advantage over secondary hospitals across all dimensions. However, from another perspective, there is significant room for growth in the informatization of secondary hospitals. According to relevant policies and regulations, the end of 2020 marked the deadline for the EMR assessment of secondary hospitals, requiring all such institutions to achieve a rating of Level 3 or higher in the graded evaluation system, mirroring the requirements imposed on tertiary hospitals in 2019.

Given the constrained financial resources of secondary hospitals, high-value projects often require applications for fiscal subsidies. The approval process for budgets is frequently subject to delays. Coupled with the large number of secondary hospitals, we believe that 2020 may witness a surge in IT infrastructure development within this sector.

Meanwhile, based on currently published data, at least 2,300 tertiary hospitals still need to participate in and pass the Hospital Information Interconnectivity Assessment before 2021, achieving a minimum standard of Level 4—an upgrade from the previous Level 3 requirement. This segment of the market driven by such upgrades is also noteworthy.

In the corporate sector, we also observe that China’s healthcare IT market remains relatively fragmented. Compared with other countries and regions with more advanced healthcare IT infrastructure, there is still considerable room for leading Chinese healthcare IT companies to increase their market share. The adoption of emerging IT systems—such as microservices, artificial intelligence, and cloud computing—places high demands on enterprises’ technical capabilities, which will benefit leading players. As a result, market concentration is expected to further increase in the future.

Given the limitations of our expertise and statistical sample, we welcome readers’ corrections and suggestions regarding any errors or omissions in this report. Please also feel free to share any data statistics topics of interest.