2019 China Healthcare Services Capital Market Report: A Weak Cycle, A New Starting Point

Introduction

Amid the escalating global pandemic, the healthcare and life sciences sector has once again become a focal point of market attention. As a key area of long-standing interest and deep expertise, the Huaxing Healthcare team has continued its established practice in this early spring, when warmth still contends with lingering chill. By examining five major sectors—biopharmaceuticals, IVD and genetic testing, medical devices, healthcare services, and smart healthcare—as well as capital markets, the team strives to provide a comprehensive overview of the development trends in the global healthcare industry over the past year.

The 5P framework is commonly used to describe the comprehensive U.S. healthcare system: patient, physician, payor, provider, and policy maker. As providers, hospitals, clinics, and the numerous third-party or new-model service providers that have emerged in recent years bear multiple responsibilities. They serve as the venues for realizing the value of pharmaceuticals and medical devices, facilitate interactions between physicians and patients, act as the recipients of healthcare payments, and constitute the primary entities responsible for implementing healthcare policies. The social value of healthcare services, the stability of growth, and the certainty of assets have also made such investment targets highly attractive to large private equity firms and strategic investors.

In 2019, China’s domestic private equity market for healthcare services experienced a significant downturn, with substantial declines in both the number and value of transactions. Ophthalmology, assisted reproduction, pediatrics, high-end chain clinics, and third-party services remained the hottest investment sectors. M&A activity focused on similar sectors as private equity, with frequent interactions between the primary and secondary markets. The only industry IPO over the past year was Jinxin Fertility, which performed exceptionally well on the Hong Kong Stock Exchange.

This issue will analyze the capital market performance of China’s healthcare services sector over the past year from three perspectives: private equity financing, mergers and acquisitions, and initial public offerings (IPOs).

Full Report

In 2019, the key tasks of healthcare reform were to improve government funding policies for public hospitals and further encourage the flow of social capital into grassroots medical services. Smart healthcare and telemedicine have gradually been incorporated into the medical insurance system, becoming part of the new normal.

Key policies released in 2019 included: In January, the General Office of the State Council launched performance assessments for tertiary public hospitals to evaluate the effectiveness of healthcare reforms. As the new round of healthcare reform entered a more critical phase, the coordination among medical services, health insurance, and pharmaceuticals (the “Three-Medical Linkage”) became more closely integrated in 2019. The assessment framework comprised four dimensions and 55 specific indicators. Assessment results were directly linked to hospital fiscal subsidies, performance-based wages, and medical insurance policies.

In March, the General Office of the National Health Commission issued the “Graded Evaluation Standard System for Smart Hospital Services (Trial).”

In June, the National Health Commission released 22 new policies to vigorously promote the development of private hospitals, emphasizing that the government will increase support for socially operated medical institutions. From 2019 to 2020, pilot programs for clinic filing management were launched in 10 cities, including Beijing, Shanghai, Shenyang, Nanjing, Hangzhou, Wuhan, Guangzhou, Shenzhen, Chengdu, and Xi’an. This initiative will streamline the process and lower the thresholds for chain outpatient clinics to obtain qualifications. The policies will also support socially operated medical institutions in joining telemedicine collaboration networks to enhance their diagnostic and treatment service capabilities.

In December, the General Office of the National Health Commission and the General Office of the National Administration of Traditional Chinese Medicine launched the performance assessment for secondary hospitals.

“Primary Care,” “Telemedicine,” and “Operations-First” emerged as the key policy terms for the healthcare services industry in 2019, and the outbreak in early 2020 further amplified the significance of these three concepts. Companies that had proactively secured qualifications for internet hospitals navigated the first quarter of 2020 smoothly, with some even achieving steady growth. In contrast, the traditional offline healthcare sector, already grappling with rising costs and tighter cost-containment measures in recent years, faced further adversity.

Private Equity Financing: Capital sentiment is becoming increasingly conservative,2020Challenging

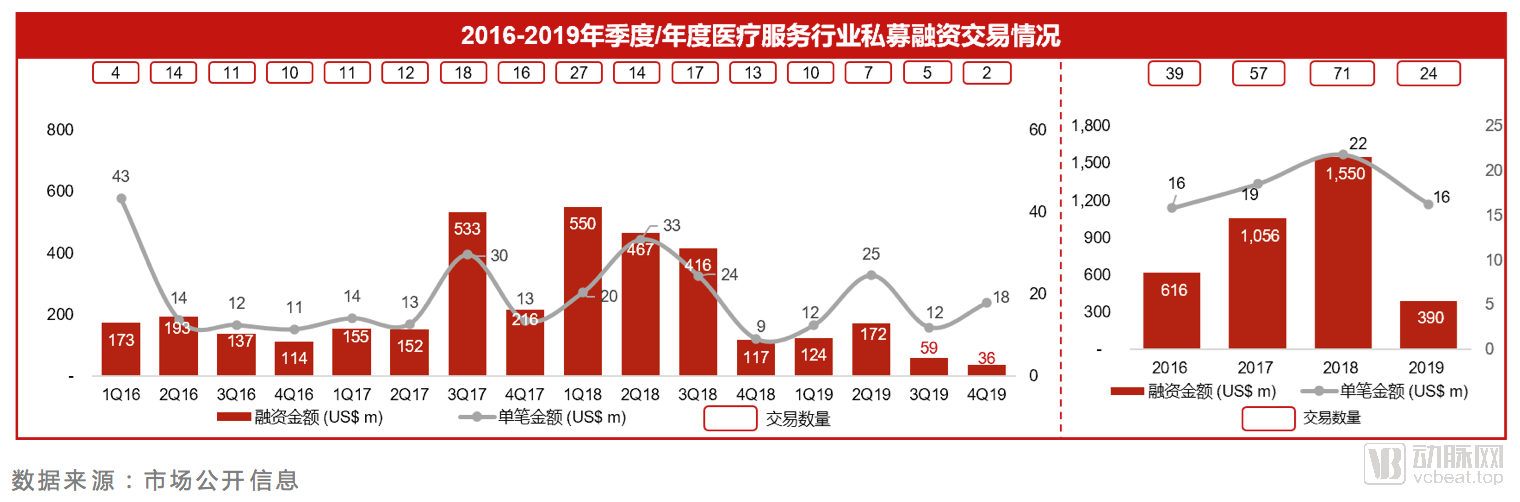

In 2019, the disclosed financing amount in the healthcare services sector was approximately $390 million, representing a 75% decline from 2018. The total number of transactions stood at 24, a 66% decrease compared to 2018. On a quarterly basis, financing in Q2 2019 reached $172 million, the highest for the year, marking a 39% quarter-on-quarter increase, while the number of transactions surged by 108% quarter-on-quarter.

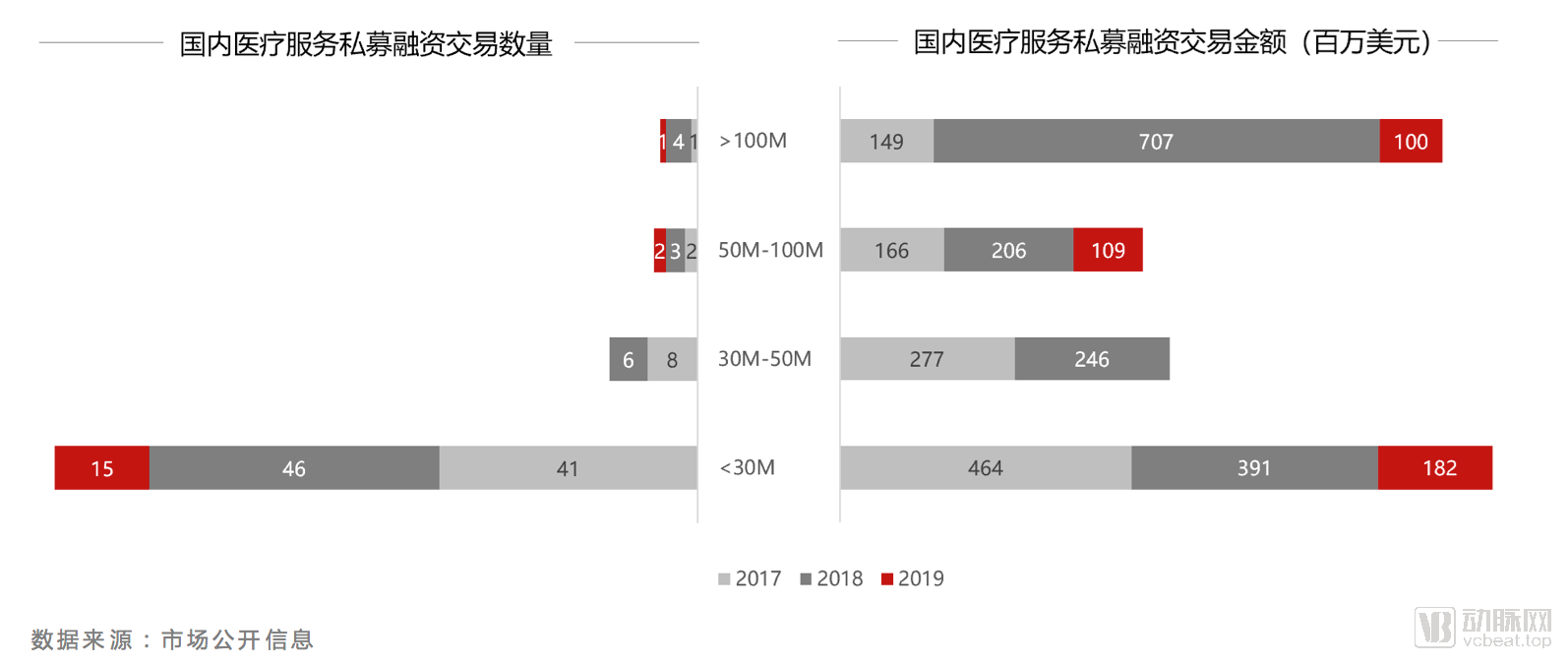

Among these, the only deal exceeding $100 million was Weier Nuo’s $100 million Series C financing round. The majority of projects raised less than $30 million, accounting for 15 deals in total. There were no transactions in the $30–50 million range, and only two financing deals fell within the $50–100 million bracket. A total of 24 transactions with disclosed financing amounts were recorded, with an average raise of $16.25 million, representing a 25.6% decline compared to 2018.

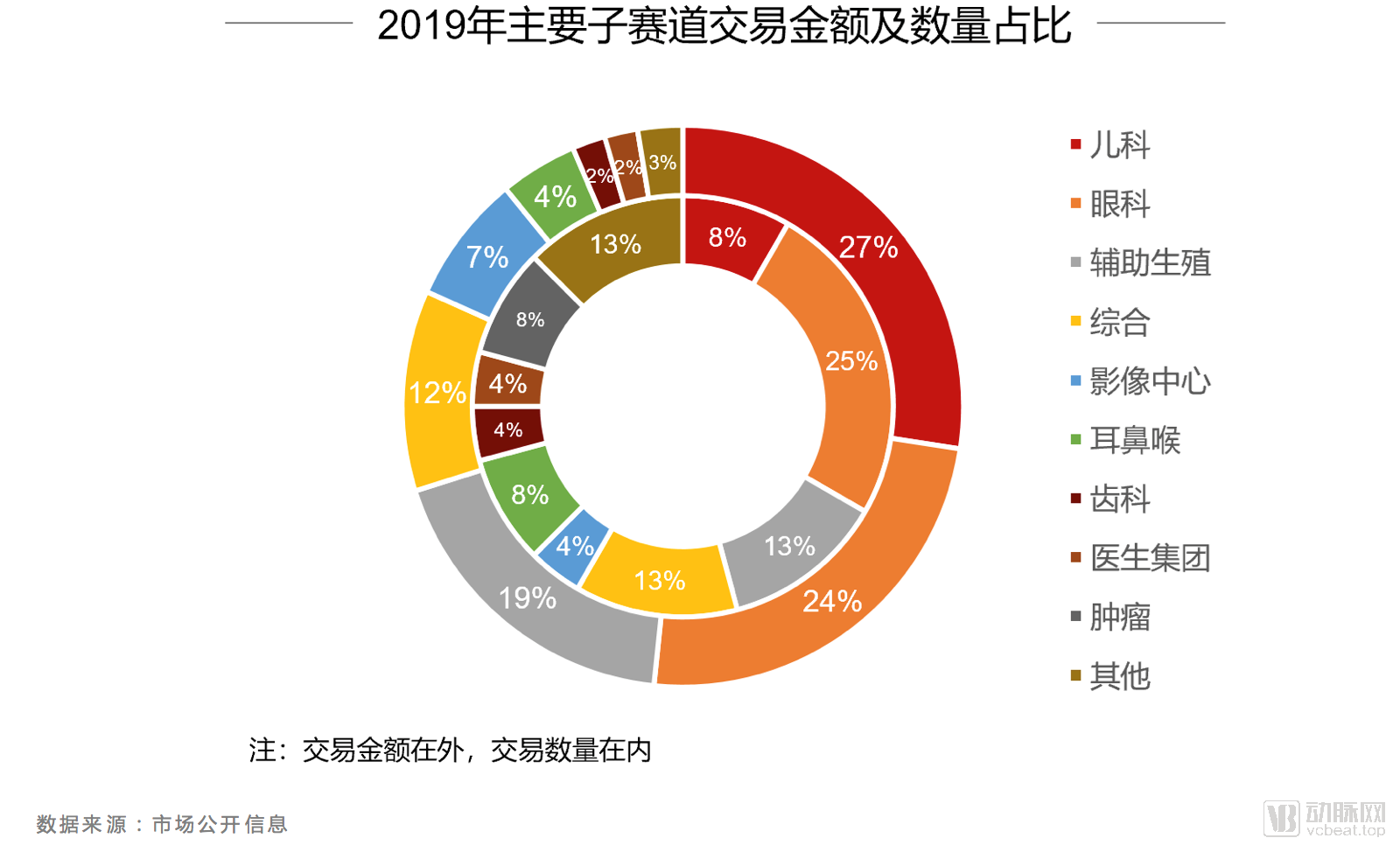

From the perspective of specific sub-sectors, the following private equity financing transactions have raised RMB 100 million or more:

Private financing in healthcare services hit a new low in 2019, following the decline in the second half of 2018, with both the number of deals and transaction amounts contracting.

2014–2017 marked the golden age of financing in the healthcare services industry, as capital markets enthusiastically embraced the emergence of new business formats and models, injecting substantial funds to facilitate their nationwide replication and expansion. By 2019, investment sentiment in the healthcare services sector had grown increasingly conservative, focusing exclusively on three sub-sectors: ophthalmology, pediatrics, and assisted reproductive technology (ART). Aier Eye Hospital’s outstanding performance in the secondary market, coupled with rigid demand for fertility services and strong willingness to pay among pediatric care consumers, alleviated investors’ concerns regarding payment mechanisms and profitability models.

Even for specialized hospitals that are profitable, revenue-generating, large-scale, and possess strong brands, market valuations remain conservative, with secondary-market stock price fluctuations serving as a strict barometer.

2020 is expected to be another challenging year for consumer healthcare. After the epidemic ends, public hospitals will need time to recover, while most private hospitals, which primarily offer scheduled surgeries or consumer healthcare services, will also find it difficult to achieve their original performance targets for 2020.

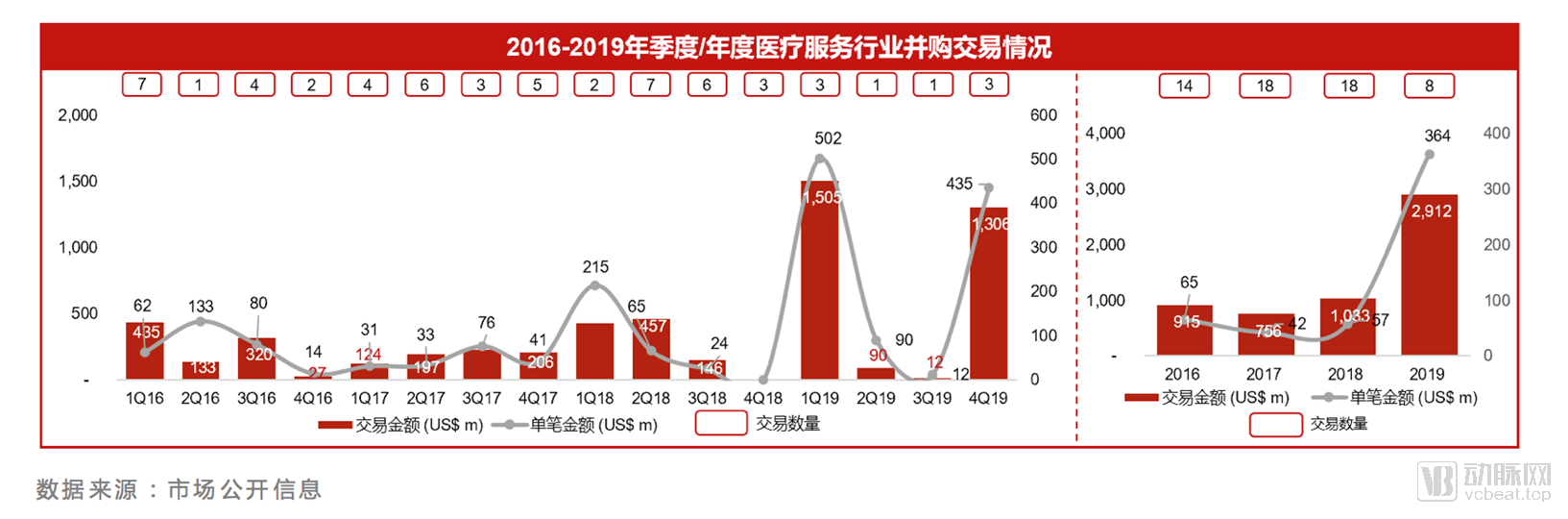

In 2019, the total value of M&A transactions in China’s healthcare services industry amounted to approximately USD 2.9 billion, representing a year-on-year increase of about 182% compared with 2018, primarily driven by New Frontier Health’s acquisition of United Family Healthcare.

Top 3 Domestic M&A Cases in the Healthcare Services Sector in 2019:

1. United Family Healthcare

On July 30, New Frontier Health Corporation (NYSE: NFC), the publicly listed investment vehicle established by New Frontier Group (hereinafter referred to as “New Frontier Health”), and United Family Healthcare (hereinafter referred to as “UFH”) announced that they had entered into a definitive agreement under which New Frontier Health will acquire UFH from its existing shareholders, including TPG and Fosun Pharma, through a combination of cash and stock. Upon completion of the transaction, the combined company is expected to have an initial fully diluted enterprise value of $1.44 billion.

2. iKang Guobin

On March 11, iKang Healthcare Group completed its merger and acquisition financing, with investors including Alibaba, Suning.com, Yunfeng Capital, and Boyu Capital. The traditional hallmark of iKang lies in its extended services before and after health check-ups. Through collaboration with Alibaba, the company will have opportunities to generate synergies in areas such as pharmaceutical e-commerce and health management, while also focusing on vertical expansion based on its existing network of health examination centers in first- and second-tier cities.

3. Renxing Health (600530)

On March 14, Jiaoda Onlly issued an announcement proposing to acquire 100% equity interest in Shanghai Renxing Health Management Co., Ltd., a subsidiary of Bairen Health, for RMB 600 million in cash. This move represents a significant step for Jiaoda Onlly to improve its asset quality and optimize the existing business structure of the listed company, while also serving as an innovative attempt by Bairen Health to bring its elderly care business to the capital markets.

Domestic M&A buyers can be categorized into three types: funds, industrial investors, and pharmaceutical companies. Among these, acquisitions in the ophthalmic hospital sector are particularly active.

1. Aier Eye Hospital

In August 2019, Aier Eye Hospital’s wholly-owned subsidiary in Singapore acquired a 35% stake in the Singapore-listed company ISEC Healthcare Ltd. and launched a voluntary general offer on the open market, aiming to increase its holding to a maximum of 78.22%. ISEC operates 11 ophthalmology and general practice clinics located in Singapore (6), Malaysia (4), and Myanmar (1). The transaction consideration was S$67.0759 million in cash, with the total acquisition cost reaching up to approximately S$150 million.

In October 2019, Aier Eye Hospital Group issued an announcement stating that the company planned to acquire 100% equity interest in Tianjin Zhongshixin Enterprise Management Co., Ltd., 100% equity interest in Zhanjiang Aolide Optometry Center Co., Ltd., and 80% equity interest in Xuancheng Eye Hospital Co., Ltd., involving a total of 28 assets.

2. C-MER Eye Care

Acquisition of Kunming Eye Hospital: In March 2019, C-MER Eye Care completed the acquisition of an 80% equity stake in Kunming Eye Hospital. With a capacity of 80 beds, Kunming Eye Hospital provides inpatient ophthalmic treatment services and has been recognized by the Ministry of Health as one of the leading private eye hospitals attractive to foreign investment. This acquisition marks C-MER Eye Care’s expansion of its ophthalmic medical service network into Western China (Yunnan Province).

Acquisition of Shanghai Lushide Medical: In September 2019, all conditions precedent for C-MER Eye Care’s acquisition of 100% equity interest in Shanghai Lushide Medical were satisfied, and the closing was completed. Upon completion of the closing, Shanghai Lushide Medical became an indirect wholly-owned subsidiary. Shanghai Lushide Medical operates one eye hospital located in Huangpu District and three clinics located in Pudong New Area, Yangpu District, and Putuo District, respectively. It employs over 80 staff members (including 14 physicians) and has a capacity of 30 beds. It provides patients with specialized diagnostic and treatment services for ophthalmic conditions, including cataract and refractive surgeries, as well as optometry services.

Kunming Eye Hospital: On March 28, 2019, C-MER Eye Care completed the acquisition of an 80% equity stake in Kunming Eye Hospital. With a capacity of 80 beds, the hospital provides inpatient ophthalmic treatment and has been recognized by the Ministry of Health as one of the leading private eye hospitals attracting foreign investment. This acquisition marks C-MER Eye Care’s expansion of its ophthalmic medical service network into Western China (Yunnan Province).

Meanwhile, hospital mergers and acquisitions (M&A) overseas, particularly in the United States, have maintained a stable and active trend. The number of M&A deals rose slightly from 90 in 2018 to 92 in 2019, with an average transaction value of $278 million. Notably, acquirers are gradually shifting their focus from financial considerations to strategic objectives, moving beyond mere consolidation of similar entities toward strategic asset allocation. This approach aims to complement different business segments to better meet consumer demands.

In Asia’s M&A landscape, the moves of giant IHH have drawn significant attention. In September 2019, IHH Healthcare Bhd acquired Prince Court Medical Centre Sdn Bhd, a private healthcare facility with 277 beds, from its major shareholder Khazanah Nasional Bhd for RM1.02 billion in cash (approximately US$230 million). The acquisition aims to consolidate IHH’s position in Malaysia’s private healthcare sector and expand its service offerings.

In 2019, the new Chapter 18A regulations and the STAR Market did not propel healthcare service companies to the same rapid growth seen in innovative drug or medical device firms. However, a review of the year’s performance reveals that leading enterprises still achieved respectable results, with “stability” emerging as the keyword for 2019.

Over the past year, no healthcare service companies have listed on the A-share market, and only one enterprise successfully completed an IPO on the Hong Kong stock exchange. Jinxin Fertility, leveraging its unicorn status in the assisted reproductive technology (ART) sector, stood out with a valuation of HK$24 billion and a fundraising amount of HK$3.05 billion. The offering was oversubscribed by 99 times, drawing strong investor demand. Following the listing, the company delivered impressive post-IPO performance, revitalizing investor confidence in healthcare service firms pursuing IPOs in Hong Kong.

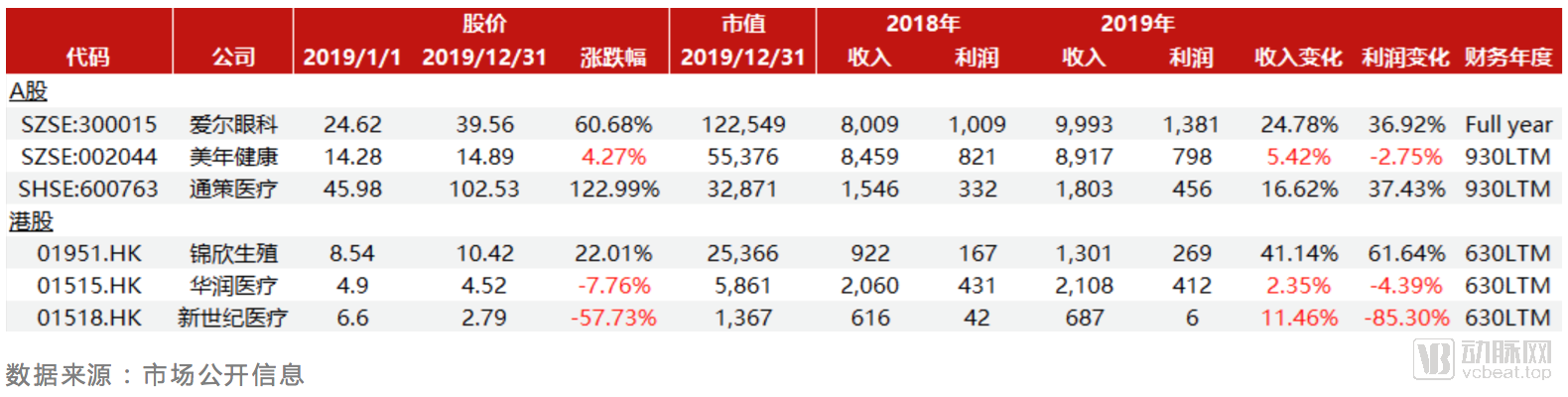

An analysis of the 2019 performance of healthcare service companies listed on the A-share and Hong Kong stock markets reveals that stable growth in revenue and profit has become a key criterion for evaluating market capitalization in the secondary market. We selected three companies from each segment for summary. As full-year 2019 financial data have not yet been disclosed for some enterprises, an examination of the published quarterly reports alone shows that any company experiencing a decline in revenue or profit failed to achieve strong results in 2019. Notably, Aier Eye Hospital, which has been operating in the secondary market for ten years, saw its market capitalization surpass the RMB 100 billion mark, driven by robust organic and inorganic growth, thereby establishing itself as a benchmark enterprise in China’s healthcare services sector.

Outlook

1. 2020 is expected to be a preparatory period for initial public offerings (IPOs) by a batch of healthcare service enterprises.

2. A cohort of healthcare service companies specializing in ophthalmology, traditional Chinese medicine, and women’s and children’s health is approaching a pivotal moment in the capital markets, warranting close attention.

3. Both the market and enterprises are gradually recognizing that a successful IPO is merely the first step; the key issue healthcare service companies need to delve deeper into is how to ensure sustained business expansion or seek breakthroughs through integration from an industry chain perspective.