Health Insurance Sector Booms in 2020: Major Policies Launched, VCs Invest Heavily Amid Pandemic

In recent years, health insurance has been one of the most notable segments within the healthcare industry. Regulators, enterprises, and investment institutions have all recognizedThe Innovative Role of Commercial Health Insurance in Medical Payments and the Emerging Industry Landscape It May Create。

In 2019, three companies in the industry announced financing on the same day, one company secured funding three times within a single year, the largest single financing round exceeded RMB 1 billion, and nearly 30 financing events occurred throughout the year.Sequoia China, Alibaba, Tencentsuch industry giants frequently appear on investors' lists.

In the first quarter of 2020, despite the impact of external factors such as the black swan event of the COVID-19 pandemic and a precipitous decline in primary market financing, the health insurance industry continued to maintain its robust momentum.

On the capital side,In the first quarter of this year, nearly 10 investment and financing transactions took place. As funding rounds have progressed to later stages, single-round investments exceeding RMB 100 million have become the norm.; on the policy front, regulators have also intensified their efforts, as evidenced by the measures issued by the Central Committee of the Communist Party of China and the State Council on March 5"Opinions on Deepening the Reform of the Medical Security System"policies, among others, more clearly define the development direction of commercial health insurance; on the market side, an increasing number of players are entering the field.

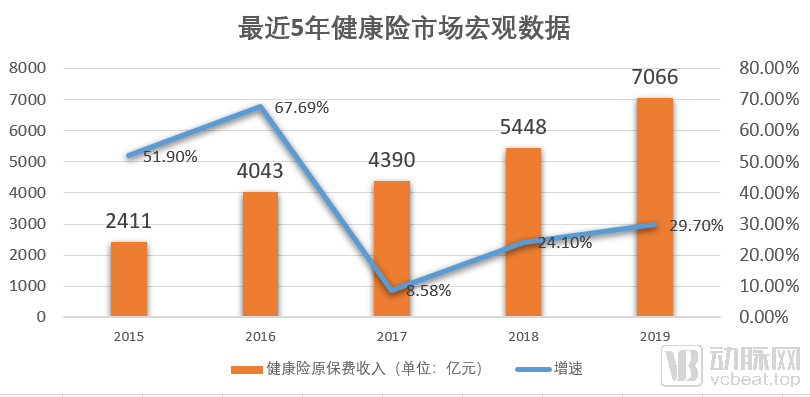

According to data from the China Banking and Insurance Regulatory Commission,In 2019, the original premium income of health insurance reached RMB 706.6 billion, with a year-on-year growth rate of 29.70%., with a compound annual growth rate (CAGR) exceeding 30% over the past five years. Such rapid expansion is remarkable, outpacing industry averages whether viewed within the niche segments of the insurance sector or the specialized fields of the healthcare industry.

In recent years, improving the efficiency of medical insurance fund expenditures and implementing cost containment measures have been the direction of the government’s healthcare reforms. During the major State Council institutional reform in 2018, the National Healthcare Security Administration (NHSA) was established, with its mission centered on “medical insurance cost containment” and the “coordinated development of medical care, health insurance, and pharmaceuticals.” Against this backdrop, the continuous emphasis on developing commercial medical and health insurance to serve as a supplement to basic medical security has seemingly emerged as an effective solution to address the current dilemmas in payment systems.

Moreover, in addition to alleviating pressure on the social medical security system, health insurance can also resolve supply-side contradictions. With rising personal health expenditures, an aging population, accelerated urbanization, a growing middle-income group, and an expanding population with chronic diseases, the current supply capacity of social security falls far short of meeting the rapidly growing demand for health protection among the public.

Driven by multiple factors, residents have become increasingly conscious of controlling their medical expenses, leading to surging market demand for health insurance. From the perspectives of the external macroeconomic environment, regulatory guidance within the industry, and the strategic development goals of leading life insurers, the demand for protection-oriented insurance products, represented by health insurance, has been consistently and effectively stimulated. This is the key reason why health insurance premiums have continued to grow at a rate exceeding the industry average.

Policyholders eliminate economic uncertainty by prepaying premiums in exchange for compensation for losses should risks materialize in the future; insurers aggregate the needs of the insured, transforming dispersed risks into approximate certainty and thereby realizing commercial value. This is the essence of insurance.

Health insurance is no exception. For users, its greatest value lies in enabling them to cover uncertain medical expenses with low and predictable upfront costs. Currently, although national basic medical insurance provides a safety net and drug prices have declined due to centralized procurement, individuals still bear a substantial out-of-pocket burden. According to data from the National Health Commission,In 2018, China's total health expenditure amounted to approximately RMB 5.8 trillion, of which individual out-of-pocket health spending reached RMB 1,666.29 billion, accounting for 28.7% of the total.With such a high proportion of out-of-pocket expenses, health insurance has a clear role to play.

“Undoubtedly, China’s healthcare payment system will evolve toward diversification.” This view was echoed by several prominent investors and entrepreneurs in interviews with VCBeat. They believe that the market demand for health insurance, as well as the industry’s own need for insurtech, are both clearly defined, ensuring that the sector will maintain a trajectory of rapid growth in the future.

The traditional health insurance market is a red ocean, characterized by severe product homogenization, with price competition being a common marketing strategy among companies. Moreover, the market maintains a high level of concentration, with 80% of revenue concentrated in the top 8% of enterprises. The main participants are primarily life and property insurance companies, while specialized health insurance companies remain small in both scale and number.

However, in recent years, with the emergence of numerous innovative health insurance companies, the industry’s market landscape is shifting toward diversification, evolving from a model dominated by single insurers to one involving internet platforms, healthcare institutions, pharmaceutical groups, health management organizations, medical big data companies, and entities from the real economy. The industry is on the eve of profound transformation.

To some extent,The health insurance market is just getting started.

An examination of the development trajectory of China’s health insurance industry reveals that national policies have determined every inflection point and developmental stage.

From the restoration of commercial insurance in 1980 to the promulgation of China’s first Insurance Law in 1995 and the subsequent launch of the basic medical insurance system reform for urban employees in 1996, marked the initial stage of health insurance development in China. During this period, reforms to the public-funded medical care system created opportunities for the growth of health insurance. In 2003, amendments to the Insurance Law permitted property insurance companies to underwrite short-term health insurance products. Two years later, PICC Health, the first specialized health insurance company, was established. By 2009, with the commencement of the new healthcare reform, the supplementary role of commercial insurance was explicitly affirmed. This phase represented a period of expanded promotion, characterized by the accelerated introduction of health insurance products and regulatory frameworks.

Since 2012, health insurance has entered its third phase, ushering in a period of explosive growth. In the following years, the annual premium growth rate for health insurance remained above 40%. Health insurance appeared to be caught up in a frenzy; amidst this rapid development, many problems began to emerge. The prevalence of short-to-medium duration products, the frequent emergence of dark horses, significant adjustments in market structure, and capital giants sweeping through the secondary market... Insurance seemed to be drifting further and further away from its essential purpose of providing protection.

The turning point came in 2017, when regulatory authorities began to tighten controls. The issuance of “Document No. 134” by the China Insurance Regulatory Commission (CIRC) promptly cooled the previously aggressive expansion of the insurance industry. The document emphasized that insurance should “return to its fundamental roots” and signaled a strict regulatory stance, including severe penalties for companies or individuals violating regulations. That year, the growth rate of health insurance premiums dropped to 8.58%.

Since 2018, policy conditions have improved, and the industry has once again embarked on a steep upward growth trajectory. Particularly inOver the past six months, regulators have intensively rolled out a series of landmark policies, clearly delineating the boundaries and outlining the blueprint for the health insurance industry.

Major Health Insurance-Related Policies in the Past Six Months

On November 12, 2019, the China Banking and Insurance Regulatory Commission (CBIRC) released the newly revised"Measures for the Administration of Health Insurance"(commonly known as the “New Health Insurance Regulations”), which triggered significant repercussions in the industry. Many industry veterans with years of experience vaguely recall that the previous revision of the Administrative Measures for Health Insurance was made more than a decade ago.

The Measures highlight the protective nature of health insurance, implementing comprehensive revisions across areas such as the definition and classification of health insurance, product regulation, and sales operations. These revisions aim to standardize the design, sales, and claims settlement practices of health insurance products, while encouraging health insurers to fully assume social responsibilities. In terms of conceptual positioning, health insurance is established as a vital component of the national multi-tiered medical security system; the definition and business classification of health insurance are refined, with medical accident insurance incorporated into the scope of health insurance. Regarding product regulation and operational sales, the Measures specify the conditions required for operating health insurance businesses and promote the enhancement of specialized operational capabilities. They uphold the protective essence of health insurance by clarifying the characteristics and requirements of various health insurance products. Furthermore, insurance companies are encouraged to apply information technology, big data, and other advanced tools to health insurance product development, risk management, and claims processing, thereby improving overall management standards.

In terms of consumer rights protection, prohibitive regulations have been imposed on insurance companies selling health insurance products, including a ban on forced bundling with other products and a prohibition on inducing consumers to repeatedly purchase expense-reimbursement medical insurance products with identical or similar coverage. It is explicitly stipulated that insurance companies shall not require policyholders to provide, nor illegally collect or obtain, the insured’s genetic information or genetic testing data, except for family medical history. Furthermore, recent healthcare reform policies have been incorporated and adopted, such as providing preferential support to impoverished populations.

On January 23 this year, 13 departments, including the China Banking and Insurance Regulatory Commission (CBIRC) and the National Healthcare Security Administration (NHSA), jointly issued the “Opinions on the Development of Commercial Insurance in the Social Services Sector.” This policy document once again clearly defined the direction for the development of health insurance and proposed striving to achieve byBy 2025, the market size of commercial health insurance is to reach RMB 2 trillion.planning.

Furthermore, the document explicitly outlines five key areas of focus for future work:Improve health insurance products and services, strengthen the protection function of commercial pension insurance, vigorously develop commercial insurance in fields such as education, childcare, domestic services, culture, tourism, and sports, support insurance funds to invest in social service sectors including healthcare and elderly care, and improve the insurance market system.

On March 5 this year, the Central Committee of the Communist Party of China and the State Council issued"Opinions on Deepening the Reform of the Medical Security System", this document may directly impact the development of China’s healthcare payment system and shape the trajectory of the entire medical and health industry. Although it begins with deepening medical insurance reform, it thoroughly addresses the broader “three-medical linkage” reform (integrating healthcare services, medical insurance, and pharmaceuticals). It is widely regarded across sectors as a foundational policy document that will set the tone for China’s healthcare reforms over the next decade.

The “Opinions” consist of 28 articles, with an overall framework that can be summarized as “1+4+2.”

“1” refers to the overall objective: “Strive to fully establish by 2030 a multi-tiered medical security system in which basic medical insurance serves as the mainstay, medical assistance provides a safety net, and supplementary medical insurance, commercial health insurance, charitable donations, and mutual medical aid develop in concert.”

“4” refers to the four mechanisms of sound benefit guarantees, fundraising and operations, medical insurance payment, and fund supervision. “2” refers to the improvement of two supports: pharmaceutical service supply and medical security services.

From the overall objectives outlined in this document, it is evident that not only commercial health insurance but also online mutual aid schemes have been incorporated into the strategic goals. In the future, they will work alongside basic medical insurance to jointly fulfill a multi-tiered healthcare security role.

Over the past two years, innovative payment models—including health insurance and online mutual aid—have emerged as one of the hottest sectors in the industry, even becoming a major trend.Prominent first- and second-tier internet companies in the market, such as Tencent, Alibaba, Meituan, JD.com, 360, and Suning, as well as leading first- and second-tier venture capital firms, including Sequoia China, Qiming Venture Partners, Yunfeng Capital, and BlueRun Ventures, have all made their presence felt in the field of innovative payment solutions, either prominently or discreetly.

In 2019, the industry recorded nearly 30 financing and investment events. Notable deals that drew significant industry attention included Waterdrop’s RMB 1 billion Series C funding round backed by Tencent and Boyu Capital, as well as Nuanwa Technology’s RMB 100 million angel round led by Sequoia China.

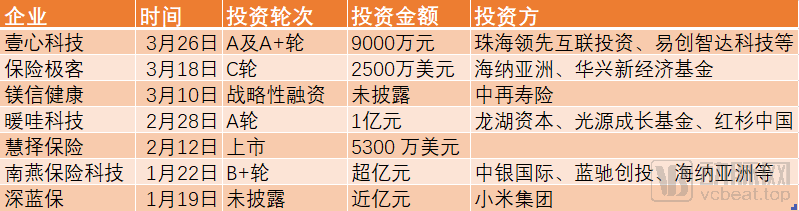

In the first quarter of 2020, the industry remained highly active. According to incomplete statistics from VCBeat, a total of seven financing and investment transactions occurred in the sector. As financing stages have shifted toward later rounds, single-round funding amounts exceeding RMB 100 million have seemingly become the norm. The industry may witness a window period for startups going public over the next three to five years.

Statistics on Health Insurance Industry Financing Events in Q1 2020; Data Source: VCBeat Database

On February 12 of this year, Huize Insurance rang the opening bell and listed on NASDAQ, hailed as the “first stock in insurance e-commerce.” Its business model primarily relies on commission income generated from traffic via third-party channels, accompanied by substantial channel expenses. According to its prospectus, Huize turned profitable in 2018, reporting a net profit of RMB 2.9 million and an adjusted profit of RMB 30.1 million for that year. In the first nine months of 2019, Huize achieved a net profit of RMB 22.5 million, representing a significant year-on-year increase of 216%; its adjusted profit reached RMB 103 million, surging nearly 400% year-on-year.

Baoxian Jike, a health insurance group insurance specialist, has secured $25 million in Series C funding, setting a new record for the largest single financing round in China’s health insurance group insurance sector. According to Ren Bin, founder of Baoxian Jike, the company’s core business metrics have grown by over 200% in the past three years, and it is now nearing break-even.

Judging from the list of investment firms, Susquehanna International Group (SIG) and China Renaissance’s New Economy Fund are entering this sector. Meanwhile, institutions such as Sequoia China, which entered the field several years ago, are increasing their positions against the trend amid a sharp decline in primary market investments, continuing to bet on the future of health insurance.

Furthermore, among publicly listed healthcare companies, most attach great importance to health insurance. For instance, Meinian Onehealth and Aier Eye Hospital have announced plans to initiate the establishment of health insurance companies, which are currently in the preparatory and regulatory approval stages. According to media reports, senior executives at China Resources Medical have called for deep collaboration with health insurers across business models, products, and capital. Meinian Onehealth currently operates an insurance brokerage subsidiary, while Topchoice Medical has disclosed in its annual report its implementation of the “HMO” model...

A huge wave of players is coming!

As the first quarter of this year comes to a close, China’s “battle against the epidemic” is nearing its end. This outbreak has undoubtedly placed the healthcare industry in the spotlight, broadly amplifying anxieties and concerns across all sectors regarding the scarcity of medical resources. Accompanying this trend has been a heightened awareness of personal health and risk protection.

According to data disclosed in the “2018 China Commercial Health Insurance Development Index Report,” the current coverage rate of commercial health insurance is less than 10%. This indicates that commercial health insurance will remain a vast market with significant growth potential in the future, with new concepts, products, models, and technologies continually emerging within the industry.

Based on projected market growth rates, the health insurance sector is expected to reach its ultimate trillion-yuan blue ocean in 2020.