China's Healthcare Big Data Industry: Coexisting Challenges and Prospects

Since the release of the “Healthy China 2030” Planning Outline as the blueprint and action plan for advancing the Healthy China initiative, China’s healthcare industry has undergone profound transformations and innovations. In recent years, more robust institutional frameworks and new market rules have gradually taken shape across multiple sectors, including new drug development, social health insurance, and health management.

Meanwhile, China’s medical big data industry has also benefited from the issuance of numerous industry standards and policy guidelines. In fact, the domestic medical big data sector is in a phase of rapid development, with the market size for medical informatics expanding year by year. Project outcomes are being progressively implemented, and a significant influx of capital and corporate participants has entered the market. As the industry gradually expands and penetrates various sectors, it has significantly advanced production capabilities in areas such as pharmaceutical R&D, public health monitoring, personal health management, and medical diagnosis and treatment, marking the entry into an initial period of favorable growth. However, compared to other industries bolstered by internet technologies, the overall pace of development in China’s medical big data industry remains somewhat sluggish.

Looking back at the industry’s history, the development of medical big data in China can be traced to 2009, when the new round of healthcare reform designated the construction of health information systems, such as electronic medical records (EMRs), as a key priority. To date, the industry has accumulated ten years’ worth of massive data. In fact, the future growth potential for medical big data in China is substantial, particularly given the strong market demand driven by the rise of domestically produced innovative drugs. However, due to numerous challenges in data circulation, sharing, and other areas, the sector continues to face persistent “information silos,” despite a decade of foundational work in health informatization, thereby hindering industry development.

From a process perspective, big data in healthcare encompasses multiple stages, including data generation, collection, storage, processing, analysis, and application. Each stage features a complete supply-and-demand scenario, with market participants collectively building a smooth industrial value chain. Notably, due to the simultaneous involvement of healthcare and internet information security issues, multiple regulatory bodies exercise overlapping jurisdiction over this industry.

From the data'sSource and Output StagesFrom this perspective, healthcare institutions such as hospitals and clinics generate massive volumes of medical data daily, making them the primary sources of raw data. However, due to entrenched traditional mindsets, the long-standing absence of regulatory frameworks, and a lack of market-based incentives, a significant amount of this data remains siloed within these institutions, hindering its consolidation into centralized repositories. First, healthcare institutions operate complex medical information systems. Historically, the development costs of health IT systems in China have been high, with each hospital maintaining independent systems featuring disparate interfaces and standards. The term “honeycomb coal” has been used within the industry to describe the characteristics of poor interoperability and difficult data sharing among healthcare institutions.

Although the Ministry of Health explicitly outlined the basic requirements that commercial hospital information systems must meet in the Basic Functional Specifications for Hospital Information Systems as early as 2002, few hospitals have been able to comply with these requirements in practice due to the substantial operational costs involved.

Secondly, data gaps and errors caused by various factors—such as discrepancies in data standards, operational issues during data entry, and loss of stored data—have also made it difficult for medical big data companies to effectively process and develop healthcare data that varies widely in quality, granularity, and other dimensions.

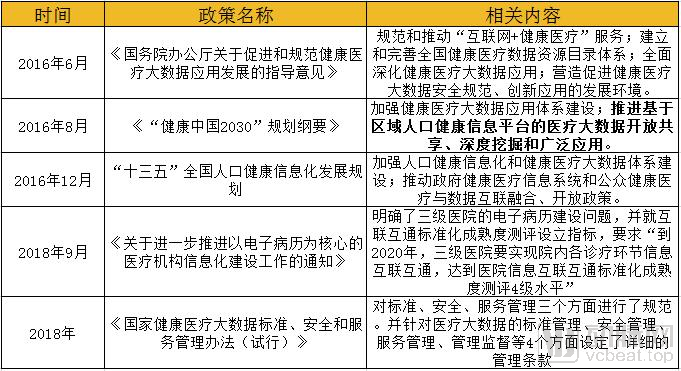

It is reassuring that both national regulators and major healthcare institutions have come to deeply recognize this issue and are gradually taking steps to improve the situation within their respective scopes. The state has successively introduced multiple policies to support the development of medical big data:

Meanwhile, an increasing number of healthcare institutions have not only recognized the immense value of data but have also begun to internally establish standardized protocols and processes for data ingress and egress, or proactively seek collaborations with third-party enterprises to upgrade and transform their existing systems. Currently, many healthcare institutions in China have taken a leading step in this regard and achieved tangible results, with some even having passed the Level 5 assessment of the National Healthcare Information Interconnectivity Standardization.

ThroughoutData CollectionIn the process, enterprises are playing an increasingly important role.Domestic enterprises are mainly concentrated in the areas of data acquisition, storage, processing, and analysis.Based on current development trends, the data acquisition market is more mature compared to other sectors. Key participants are predominantly hardware and software vendors, medical device manufacturers, or wearable device companies. These enterprises tend to be larger in scale, with several being publicly listed. However, even at the stage of raw data collection, these companies face three major challenges:

1. Significant challenges in data collection

The healthcare sector is inherently highly specialized and sensitive. It has long been subject to stringent government regulation, resulting in high barriers to entry and intricate stakeholder interests, which place exceptionally high demands on a company’s industry resources. Furthermore, the lack of unified standards and specifications for data output formats and collection tools makes it difficult to ensure data quality. Consequently, enterprises often incur higher costs to acquire high-quality medical data.

2. High compliance risks in data collection

Medical data is highly specialized and sensitive, particularly because user data privacy is subject to dual protection under both ethical principles and regulatory frameworks. Even hospitals are uncertain about which data can be shared and what risks are associated with external data sharing. Furthermore, due to the long-standing lag in the development of industry-specific laws and regulations, issues such as unclear data ownership and usage rights, inadequate management of data sharing, and the absence of access and exit mechanisms for data applications have led to compliance concerns with certain datasets.

3. Constantly Facing Data Security Challenges

The widespread adoption of the internet has also introduced significant risks of public privacy data breaches. Currently, the global landscape of cybersecurity is severe, with a continuous rise in the number of data breach incidents and increasingly serious consequences. In particular, big data has become a prime target for cyberattacks due to its immense value and centralized storage and management models. Therefore, enterprises must not only ensure the security of their underlying infrastructure components but also provide security guarantees for the data and applications running on them, as well as implement protective measures for data flows within business applications. This places extremely high demands on enterprise data security protection technologies.

In a sense,Market incentive mechanisms may be one of the most significant driving forces encouraging participants across the upstream and downstream of the industrial chain to establish data interaction standards.On the supply side, healthcare institutions also seek to convert the “dormant” data accumulated over many years into value and generate greater operational profits. On the demand side, enterprises such as pharmaceutical companies and insurance providers urgently need big data to be integrated into practical applications to reduce their R&D or operational costs. Even physicians and experts hope to obtain post-treatment follow-up data from patients to support their academic research.

Therefore, companies have abundant market collaboration opportunities. For instance, in countries with relatively mature industries such as the United States and Japan, the business model of many startups is:On one hand, it provides more affordable services to medical institutions, thereby continuously collecting and accumulating data; on the other hand, it sells the data to startups focused on technology application or, after processing and analysis, supplies it to other enterprises with data application scenario needs. Within this chain, the largest demand comes from major pharmaceutical companies.

In China, a significant number of enterprises have already accumulated vast amounts of data by establishing robust product back-end systems. Some companies are also working to convert redundant unstructured data into usable formats. Recently, industry discussions have shifted from how to accumulate and consolidate data to topics such as the practical industrial application and implementation of data. This trend indicates that corporate efforts in data collection are becoming increasingly streamlined and efficient.

As forComplianceIn any industry, the development of laws and regulations inevitably lags behind its growth trajectory. The Administrative Measures for Standards, Security, and Services of National Health and Medical Big Data (Trial) provides detailed provisions. However, the current Measures remain largely guideline-oriented, lacking specific operational specifications and procedural guidance—the critical “final step” needed for practical implementation.

Consequently, both hospitals and enterprises currently harbor concerns. Even regarding ownership, some companies have introduced the concept of “data barriers,” considering these medical big data assets as their core competitive advantages. Therefore, thoroughly resolving this issue requires continuous balancing and negotiation between “privacy protection” and “industry development.” Judging from the current practical situation in the industry, private-sector enterprises obtain data through scientific research collaborations with medical institutions.

“National Team” enterprises obtain medical data for a specific region through government-led cooperative authorizations. For instance, China Electronics Data (CEData) is authorized and led by the government to aggregate and govern hospital data within a designated area. From this perspective, “National Team” entities like CEData offer greater reliability in terms of data compliance and security.

Currently, the development of China’s medical big data industry remains in its early stages. Fortunately, driven by concerted efforts from both the government and enterprises, the sector is experiencing steady and rapid growth.

In the first half of 2017, within a three-month period, the “national team” of the medical big data industry—China Health and Medical Big Data Industry Development Group Co., Ltd., China Health and Medical Big Data Technology Development Group Co., Ltd., and China Health and Medical Big Data Co., Ltd.—successively announced their establishment, rapidly solidifying the landscape dominated by these three major groups.

The three major groups were established under the unified leadership and organization of the former National Health and Family Planning Commission, with state-owned capital playing a dominant role. Backed by state-owned enterprises such as the three major telecommunications carriers and several large state-owned banks, this signifies that central state-owned enterprises are entering the health and medical big data industry as a consortium.

Meanwhile, the five major regional centers for healthcare big data in Shandong, Jiangsu, Guizhou, Fujian, and Anhui have been established successively. These centers are tasked with national pilot projects, including the development of the National Health and Medical Big Data Center, regional centers, application development centers, and industrial parks. Furthermore, they are deepening their responsibilities to promote overall industry construction and cultivate the industrial ecosystem by actively fostering market collaborations or introducing private enterprises to establish joint ventures.

Jin Xiaotao, former Deputy Director of the National Health and Family Planning Commission and President of the Chinese Society for Health Information Technology and Healthcare Big Data, once emphasized that the operational principle of the “national team” in medical data is “government-led, market-operated.” Under the supervision of the Big Data Office, the “national team” will assume responsibility for investing in and operating national healthcare big data centers and industrial parks. With the goal of ensuring the security of healthcare big data, it will invest in leading enterprises within the industry to break through core technologies; leverage financial instruments to promote the incubation and cultivation of the health industry; build an ecosystem for the healthcare big data industry; and advance the development of foundational national healthcare big data infrastructure.

The establishment of the “Three Major Groups and Five Regional Centers” signifies that, at the national level, efforts have begun to tap into the “gold mine” of medical data.

How can the “gold mine” be processed into products after being unearthed? This requires the participation of enterprises and capital to provide support for the development of medical companies.

Amid the raging pandemic, Inspur Health recently announced the completion of a RMB 100 million Series A financing round to strengthen its data value-added services and internet-based product offerings. The company aims to collaborate with more regional and large-scale medical institutions to accelerate the development of a platform-based service for personal full-lifecycle health management. This achievement is no small feat and underscores investor confidence in the medical big data industry. The tangible impact of data- and technology-driven empowerment is evident: recently, XtalPi partnered with Zensun Pharmaceuticals to announce significant progress, suggesting that chloroquine could become a breakthrough treatment for COVID-19. This serves as empirical evidence of how big data and artificial intelligence are accelerating new drug development.

Another example is the collaboration between China Electronics Data (CEC Data) with WeDoctor, Senyi Intelligence, and WuXi AppTec. As a “national team” member in the development of the health and medical big data industry, CEC Data’s top priority is to leverage the strengths of its shareholders and cultivate the core “security + intelligence” capabilities of the national health and medical big data industry development group.

In 2018, China Electronics Data participated in Medlinker’s Series D financing round, which totaled RMB 1 billion. At that time, Medlinker had already established a deep presence among physicians, but its potential for expansion to either the patient side or the pharmaceutical manufacturer side was limited. With strategic investment from and collaboration with China Electronics Data, Medlinker could achieve horizontal expansion, thereby significantly broadening its market landscape.

Similarly, the core business of Senyi Intelligent, founded in April 2016, is to address the pain points of medical big data. It transforms low-value data into high-quality data through data governance, promoting data-driven artificial intelligence applications oriented toward medical research, clinical management, and patient services. As a technology company, Senyi Intelligent originally specialized in developing research platforms and performing natural language processing (NLP) tasks such as word segmentation and data structuring. Following its collaboration with China Electronics Data, it transformed into a data service provider. By entering hospitals through its research platforms and leveraging China Electronics Data’s resources, it can directly conduct drug activity analysis for pharmaceutical companies. Thus, it has successfully transitioned from a technology-focused enterprise to an operations-oriented company.

Furthermore, it is worth noting that the strategic alliance between China Electronics Data (CEC Data) and WuXi AppTec has given rise to CEC WuXi. Leveraging the National Health and Medical Big Data Service Platform and the National Health and Medical Big Data Security Platform established by CEC Data, and integrating WuXi AppTec’s professional expertise and extensive experience in new drug development and the broader health industry, CEC WuXi provides partners with full-industry-chain, integrated big data analytics products and solutions for healthcare. These solutions span the entire lifecycle, from drug research and development and post-marketing efficacy evaluation to distribution and sales.

In the healthcare industry, companies such as LinkDoc Technology, Yidu Cloud, and Taimei Medical have long been leveraging medical big data to deliver services. For instance, LinkDoc Technology, a provider of artificial intelligence and medical big data solutions, was founded in 2014. By virtue of its core technologies and capabilities in the integration, processing, and analysis of medical big data, the company offers comprehensive medical big data solutions to society, various industries, government agencies, healthcare institutions at all levels, domestic and international medical device manufacturers, and pharmaceutical companies. It also provides integrated services including AI-assisted decision-making systems, end-to-end patient management, hospital public opinion monitoring and brand building, drug and medical device R&D, and insurance cost control. The company’s Series D financing round in 2018 reached RMB 1 billion.

Overall, although China’s health and medical big data industry currently faces numerous challenges and development barriers stemming from its inherent characteristics, it holds immense potential for growth in the long run. Against the backdrop of the “Healthy China” initiative being elevated to a national strategy, there are broad application prospects across various related fields. In the future, as industry-related services deepen, humanity may be able to predict outbreak trends of epidemic diseases and reduce healthcare costs. Patients will also enjoy more convenient services, and traditional public health management and healthcare models are bound to undergo disruptive transformations.