Rock Health Q1 2020 Funding Report: Record $3.1B Raised as Telehealth Surges Amid Pandemic

In recent days, the COVID-19 pandemic has spread globally. What is the current state of the global healthcare industry’s investment and financing market amid the outbreak? Rock Health has released its investment and financing report for the first quarter of 2020, which has been translated by VCBeat (WeChat ID: vcbeat).

Venture capital investment in digital health reached a staggering $3.1 billion in the first quarter of 2020, marking the strongest start on record. However, the COVID-19 pandemic struck the United States in February of that year, directly impacting public markets. The dual crisis of the global pandemic and large-scale economic shifts is poised to rapidly affect all markets, including digital health.

Funding for digital health surged in the first quarter of 2020—before the COVID-19 pandemic disrupted the U.S. economy

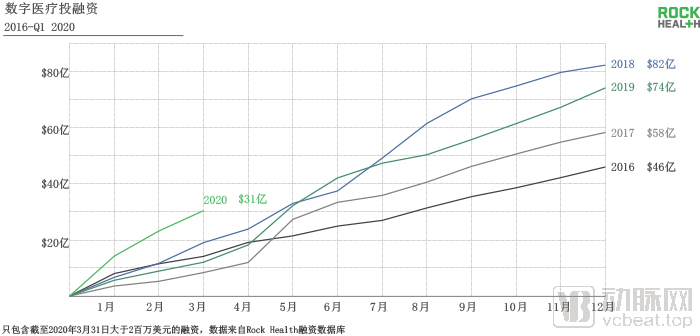

After the investment slowdown in the same period of 2018-2019, digital health investments accelerated in the first quarter of 2020. Despite a broad-based pullback in venture capital at the start of 2020, U.S. digital health companies still raised up to $3.1 billion. A total of 107 deals secured $3.1 billion in funding, representing more than 1.5 times the amount raised during the same period in previous years.

In fact, the financing volume in the first quarter of 2020 was 57% higher than the average quarterly financing volume from 2018 to 2019, making it the second-largest quarter for fundraising in history. This marked the end of the largest 12-month funding period ever recorded in the digital health sector—from the second quarter of 2019 to the first quarter of 2020—during which the digital health industry attracted a total of $9.3 billion in investment.

The strong momentum in digital health fundraising at the start of the year has been disrupted by the global COVID-19 pandemic. Although the outbreak is expected to drive up demand for related medical services and mitigate its economic impact, we anticipate that investment activity in the coming months will not sustain the high levels seen in the first quarter.

![]()

Image from Rock Health

Today, we are experiencing a historic global public health crisis. Unprecedented volatility in public markets indicates that capital markets are actively pricing in an economy expected to decline sharply due to multiple factors.

For instance, the impact of lockdowns on both supply and demand, a sharp rise in unemployment, an unrelated yet ill-timed oil price war, and new patterns of remote work, education, and social distancing. All these cultural shifts may persist even after the crisis has passed.

Due to the long-term lack of systematic and extensive epidemiological surveillance, predicting the spread and recovery trajectory of the novel coronavirus remains a mystery. Venture capital has sounded the alarm for startups—many have suffered significant blows to their revenues and are drastically cutting expenses.

To gain an initial understanding of this new reality, Rock Health surveyed more than a dozen prominent healthcare investors in late March to assess the outlook for upcoming digital health venture capital investments. Their perspectives are shared below.

The Impact of COVID-19 on Digital Health Investment

Our previous report projected that the fundraising environment in 2020 would be more challenging. However, we clearly did not anticipate the outbreak of COVID-19. The economic recession triggered by this infectious disease is underway, but its differential impacts on various sectors of the economy have yet to fully materialize.

The healthcare industry is not immune to the broader economy’s financial pressures. Although digital health startups have been at the forefront of the fight against COVID-19, they are not exempt from its impact. However, two key factors may mitigate the effects of reduced venture capital investment in digital health on the industry.

First, venture capital firms’ funding levels remain at record highs. “Defaults” are rare because limited partnership agreements make it difficult for limited partners (LPs) to exit. Moreover, venture capitalists are typically required to deploy LPs’ committed capital within a fixed timeframe. Although some investors may hesitate slightly amid valuation resets, they cannot afford to remain on the sidelines indefinitely.

Secondly, in certain circumstances, digital health startups are uniquely positioned to mitigate the direct impact of the pandemic and drive sustained positive change in the post-crisis era. While other industries (or other segments within healthcare) can often play a similar role, some digital health companies have already assumed a dominant position.

Falling is easy; getting back up is hard.

The scale and speed of the economic impact of COVID-19 are unprecedented in the United States in decades. The U.S. stock market began a rapid decline in mid-February. On March 16, 2020, the Dow Jones Industrial Average plunged nearly 3,000 points, marking its largest single-day drop since 1987. As of April 3, 2020, the S&P 500 Index had fallen more than 25% from its February peak and had not yet recovered from its fastest-ever 30% decline.

After hitting a historic low in volatility more than two years ago, public markets have entered a period of sell-offs and record-high volatility. Even if the U.S. economy has not yet entered a recession, one appears inevitable. In a recent survey by Rock Health, 10 out of the 12 investors surveyed strongly agreed that a recession had either already begun or would occur in 2020.

Governments around the world have undertaken unprecedented and necessary interventions, even if these measures were not perfect. Typical measures included creating liquidity within the financial system and providing direct support to individuals and businesses. On March 27, the U.S. federal government passed the largest economic stimulus package in history.

The U.S. government also implemented other measures, including expanding unemployment benefits, allocating $500 billion to support businesses, and issuing direct payments of $1,200 to most American taxpayers. The Federal Reserve also took unprecedented significant actions not seen since the 2008–2009 financial crisis, including unlimited purchases of U.S. Treasury securities and cutting interest rates to zero. Furthermore, for the first time in history, the Fed purchased corporate bonds and corporate bond ETFs.

Capital Access to Tighten

There is ample reason to believe that the dual shock on both supply and demand sides will be a significant event for all enterprises, and startups cannot remain unaffected. Sequoia Capital has pointed out that the novel coronavirus has undoubtedly led to supply chain disruptions, downward revisions of growth forecasts, and changes in hiring plans. Among the 12 investors surveyed by Rock Health, eight believed that fundraising for digital health startups in 2020 would be much more difficult than in 2019.

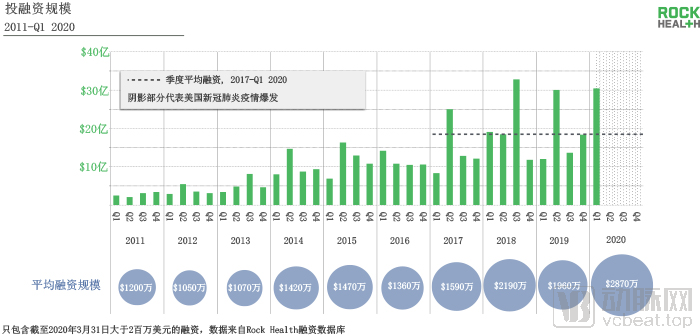

Image from Rock Health

Private capital investment will not contract as rapidly as public markets.

The scale and pace of public market sell-offs are staggering, but the private market may not experience such a severe downturn. This is because private equity (with venture capital effectively being a subset of private capital) derives from capital commitments made by limited partners (LPs). Unless these commitments are revoked, private equity and venture capital firms are obligated to continue investing the funds raised prior to the crisis. However, withdrawing such commitments is typically a considerably difficult process.

In a Rock Health survey of 12 investors, only three expressed slight concern that LPs might default on capital calls, i.e., fail to provide the funds required to meet their capital commitments.

Venture capital and private equity financing have increased for several consecutive years, leaving investors with record levels of committed capital. These undeployed funds will, to some extent, alleviate the recent difficulties companies face in raising capital from the market.

Of the 12 investors surveyed by Rock Health, only three indicated they would somewhat reduce their investment amounts in 2020, suggesting that investors largely maintained their planned investment levels for 2020.

The survey results clearly reveal a contradiction between investors’ stated intention to maintain their investment plans and their expectation that it would be significantly more difficult for startups to raise capital in 2020 than in previous years.

This divergence in conclusions may reflect the view that investors become more cautious about new investments during economic downturns, while simultaneously favoring companies in which they have already invested. In light of this, we anticipate that capital markets will shift toward demanding higher quality in investment projects, intensifying competition for the most attractive deals. Investors with deployable capital will target enterprises leading the rapidly evolving healthcare technology market.

Digital health is particularly well-suited for expanding the capacity of healthcare systems.

The global pandemic of COVID-19 and the ensuing economic recession appear bleak. However, digital health holds unique advantages in addressing many current and emerging challenges. As healthcare systems worldwide face resource strain due to a surge in hospital admissions, a range of new medical needs is emerging.

Other companies in this field are racing against time to expand their COVID-19 testing capacity and develop vaccines and treatments. Digital health companies provide technological support to deliver medical services virtually, enhance healthcare capacity, and accelerate the research and development of diagnostics and therapies.

Numerous digital health companies have been working overtime to accelerate project timelines and delivering services and technologies in novel ways—even free of charge—to respond to the COVID-19 public health crisis.

Notably, telemedicine has been deployed at the forefront of the fight against the COVID-19 pandemic. VCBeat had already identified this trend within China’s digital health sector. Moving forward, we will focus on developments in the telemedicine markets of the United Kingdom and the United States. Although some reports indicate that certain telemedicine providers encountered minor challenges in adapting to the surge in demand, telemedicine startups are rapidly responding to the escalating health crisis.

Doctor on Demand has launched an online tool to assess the risk of COVID-19. MDLIVE offers dedicated appointments for patients with COVID-19 and also provides psychological counseling services related to the pandemic. 98point6 tripled its number of internal medicine physicians within a month to cope with the surge in medical demand caused by the outbreak. PlushCare also increased its recruitment of internal medicine physicians by 50% to 100%.

The U.S. federal and state governments are also rapidly removing regulatory barriers to the adoption of telemedicine, paving the way for virtual care to become the new normal in the healthcare industry.

Medicare will temporarily cover costs for patients who benefit from telehealth services during the pandemic. The U.S. Department of Health and Human Services announced that it would waive HIPAA penalties during the outbreak, enabling providers to use tools such as FaceTime to deliver good-faith telehealth care to patients. U.S. Vice President Mike Pence also unveiled a potential plan to allow physicians to practice across state lines without obtaining licenses in other states.

This is undoubtedly a tipping point for the adoption of telemedicine, which has been steadily rising for years. The use of video-based telemedicine has grown 4.5-fold since 2015. In Rock Health’s annual Digital Health Consumer Adoption survey, the growth rate of telemedicine reached 32% in 2019.

Rock Health believes that the adoption rate of telemedicine will rise significantly this year and expresses cautious optimism that first-time consumers and providers will become long-term users. Investors surveyed by Rock Health also anticipate a substantial increase in the appeal of telemedicine; due to the COVID-19 pandemic, all respondents believe that telemedicine will achieve greater growth in 2020, exceeding even prior projections.

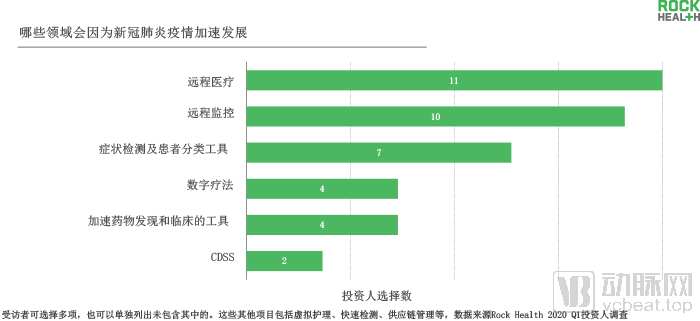

Although telemedicine has garnered significant attention in recent weeks, other digital health innovations are also providing solutions to combat the COVID-19 pandemic. In particular, investors surveyed anticipate growth in remote monitoring, symptom checking, and triage tools.

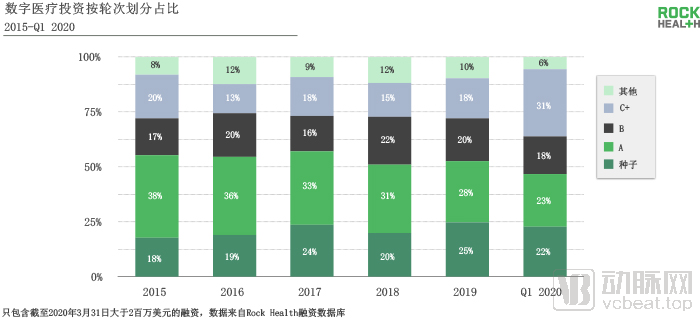

The COVID-19 pandemic masked the surge in investments during the latter part of the first quarter.

At present, the digital health investment landscape in the first quarter has served as a warning for the remainder of 2020. Nevertheless, two trends in the first quarter remain prominent:

In the first quarter of 2020, 31% of deals were Series C or later-stage transactions. This proportion was 1.8 times that of Series C or later-stage investments during the same period from 2015 to 2019. Meanwhile, 63% of the companies that completed financing were sold to investors. The proportion of investors acting as buyers far exceeded that of any other buyer group.

In the first quarter of 2020, large-scale late-stage investments accounted for a relatively high proportion.

The average deal size for financing in the first quarter of 2020 surged to $29 million. This figure was only $19.5 million in 2019, having risen to $21.5 million in 2018. As the digital health market matures, this trend is a natural consequence of the marked shift in financing toward later-stage transactions.

Image from Rock Health

The first quarter included six high-value financing rounds of $100 million or more, accounting for 33% of the total digital health financing.

Investments Face Difficult Exits in 2020 as IPO and M&A Prospects Dim

A shift in digital health investment toward Series C or later rounds typically signals that a cohort of companies is preparing for exit. Unfortunately, the impending economic downturn will dampen public investors’ interest in IPOs. Eleven out of the twelve investors surveyed by Rock Health believe that the window for digital health IPOs in 2020 has closed.

Interestingly, these same investors hold less consistent views on the M&A market. Only eight of the 12 respondents believed that market volatility would significantly curb M&A activity in the digital health sector.

Before the novel coronavirus hit the United States, investors had already focused on investing in supply chain innovation.

A significant proportion of innovative startups secured financing in the first quarter of 2020. These companies are dedicated to leveraging technology to enhance the service efficiency, capacity, and workflows of supply chains. In contrast, 68 startups providing services to suppliers raised funds in the first quarter of 2019.

Image from Rock Health

As suppliers are currently affected by the COVID-19 pandemic, are startups facing challenges in providing services to them? Or, conversely, has the sales cycle for services shortened due to the pandemic? This evolving trend warrants close attention.

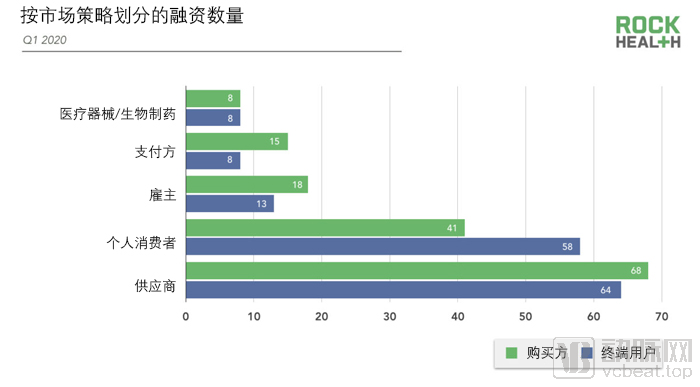

In the first quarter of 2020, investors primarily funded various solutions targeting suppliers, clinics, and healthcare systems. Among these, the largest investments focused on data collection, clinical workflows, and health system management.

Image from Rock Health

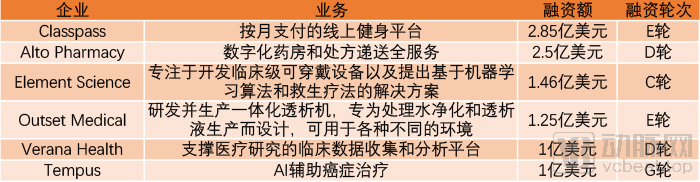

Innovaccer, a population health management platform company that offers “pay-for-performance” and SDOH management, has secured $70 million in Series C funding.

Komodo Health Secures $50 Million in Series C Funding. This leading modern healthcare intelligence platform is dedicated to leveraging real-time data to improve healthcare decision-making. Komodo Health’s Healthcare Map provides customers and partners with the essential software support needed to address complex challenges within the healthcare system.

IntelyCare secured $45 million in Series B financing in February. It provides flexible, intelligent nursing staffing solutions that optimize nursing service capacity and enable flexible employment models.

Additionally, three financing deals were directly sold to suppliers, including Begent Medical, Verana Health, and Tempus.

Final Thoughts

In addition to Rock Health, the well-known media outlet Startup also summarized the financing and investment activities for Q1 2020. Startup noted that due to the impact of the COVID-19 pandemic, some sectors showed signs of a surge in financing and investment.

Image from Startup

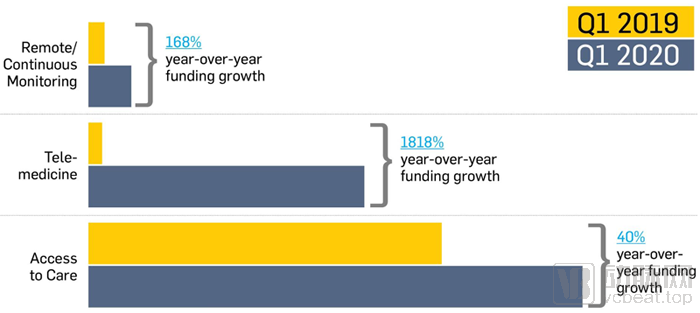

In the first quarter of 2020, telemedicine witnessed the highest year-on-year growth in investment and financing, surging by as much as 1,818% compared to the same period last year. Remote patient monitoring recorded a 168% year-on-year increase, making it the sector with the second-highest growth rate after telemedicine.

It is worth noting that the mental health sector, previously receiving little attention, has also performed well, with financing amounts increasing by 65% year-on-year. This seems to be a harbinger that the COVID-19 pandemic may have given investors time to carefully consider overlooked areas within healthcare.