Global Healthcare Investment Dynamics Report Q1 2020: 420 Deals and $12 Billion in Funding Amid Pandemic

HongShan

Business Consulting, Enterprise Management Consulting Investment Institutions

Khosla Ventures

Venture Capital Firms

I. Changes in Healthcare Capital Amid the COVID-19 Pandemic

Global healthcare financing remains active: total global healthcare funding in Q1 2020 increased by 13% year-on-year;

The domestic healthcare industry maintains a robust financing landscape: while total funding amounts have declined and the number of deals has dropped sharply, large-ticket transactions remain frequent;

Since the outbreak of the pandemic in 2020, the A-share pharmaceutical and biotechnology index has risen against the trend, demonstrating robust performance with an 8% gain in Q1. Among these, stocks directly related to the pandemic, such as mask manufacturers, saw an average increase of 142%, while stocks in the monitoring and treatment equipment and traditional Chinese medicine sectors both recorded average gains exceeding 30%.

The pandemic has accelerated financing progress in China’s IVD sector and the global digital health field, which will benefit the long-term development of the healthcare industry.

II. Global Healthcare Financing Trends in Q1 2020

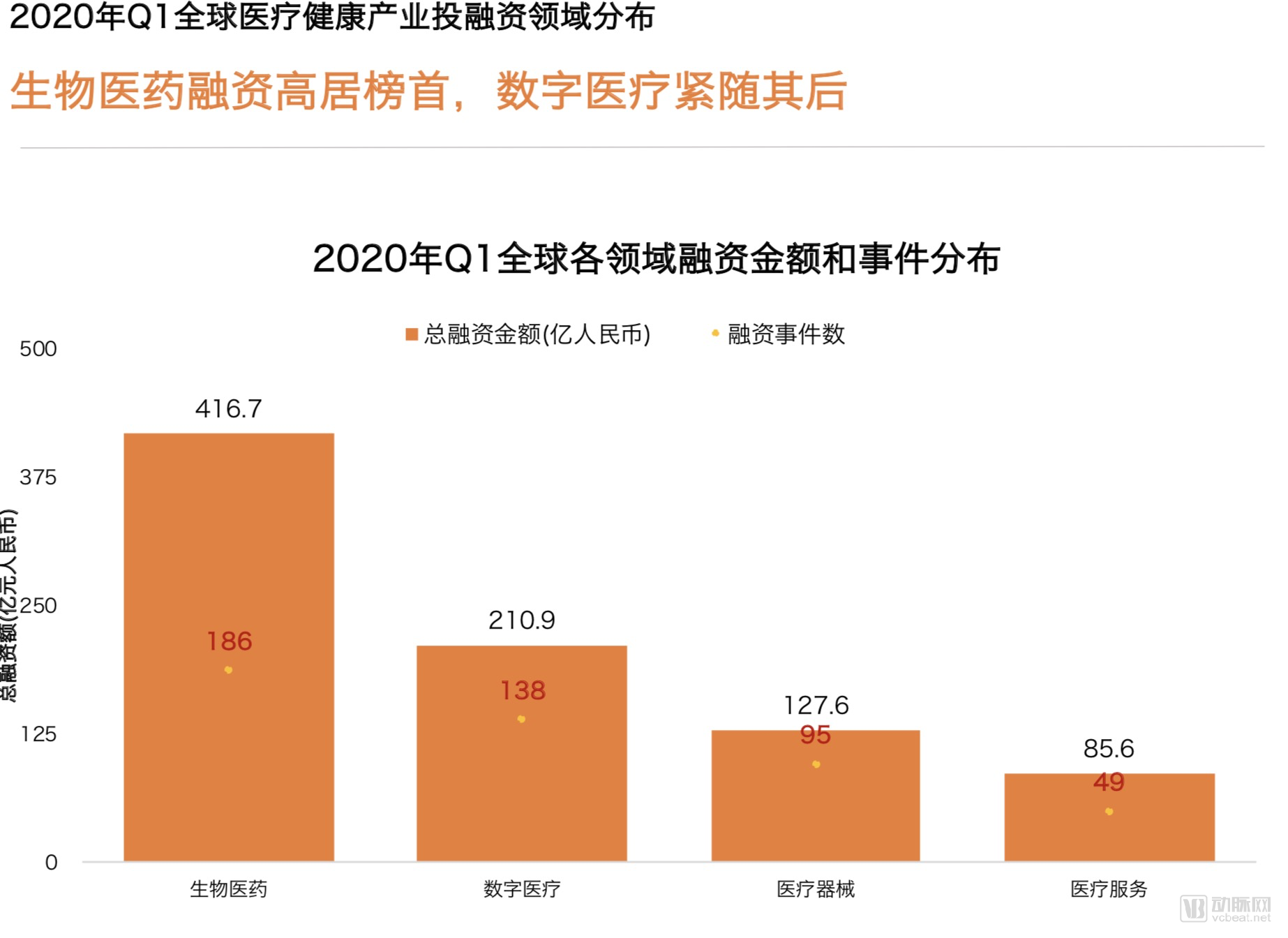

Global Distribution of Financing by Sector: Biopharmaceuticals Lead, Followed Closely by Digital Health;

In Q1 2020, a total of 14 investment firms made more than five investments, with Khosla Ventures being the most active at eight deals;

China, U.S., and Hong Kong Stock Markets Welcome 20 Healthcare IPOs; Average Share Price on the STAR Market Surges by 171%

In Q1 2020, Shanghai surpassed Beijing in both the number and total amount of financing deals, becoming the top destination for startups in China during that quarter;

Digital Pharmacy Alto Raises $250 Million in Series D Funding, Becoming the Top-Funded Deal Globally for the Quarter; China’s Top 10 Financing Deals Dominated by Biopharmaceutical Companies.

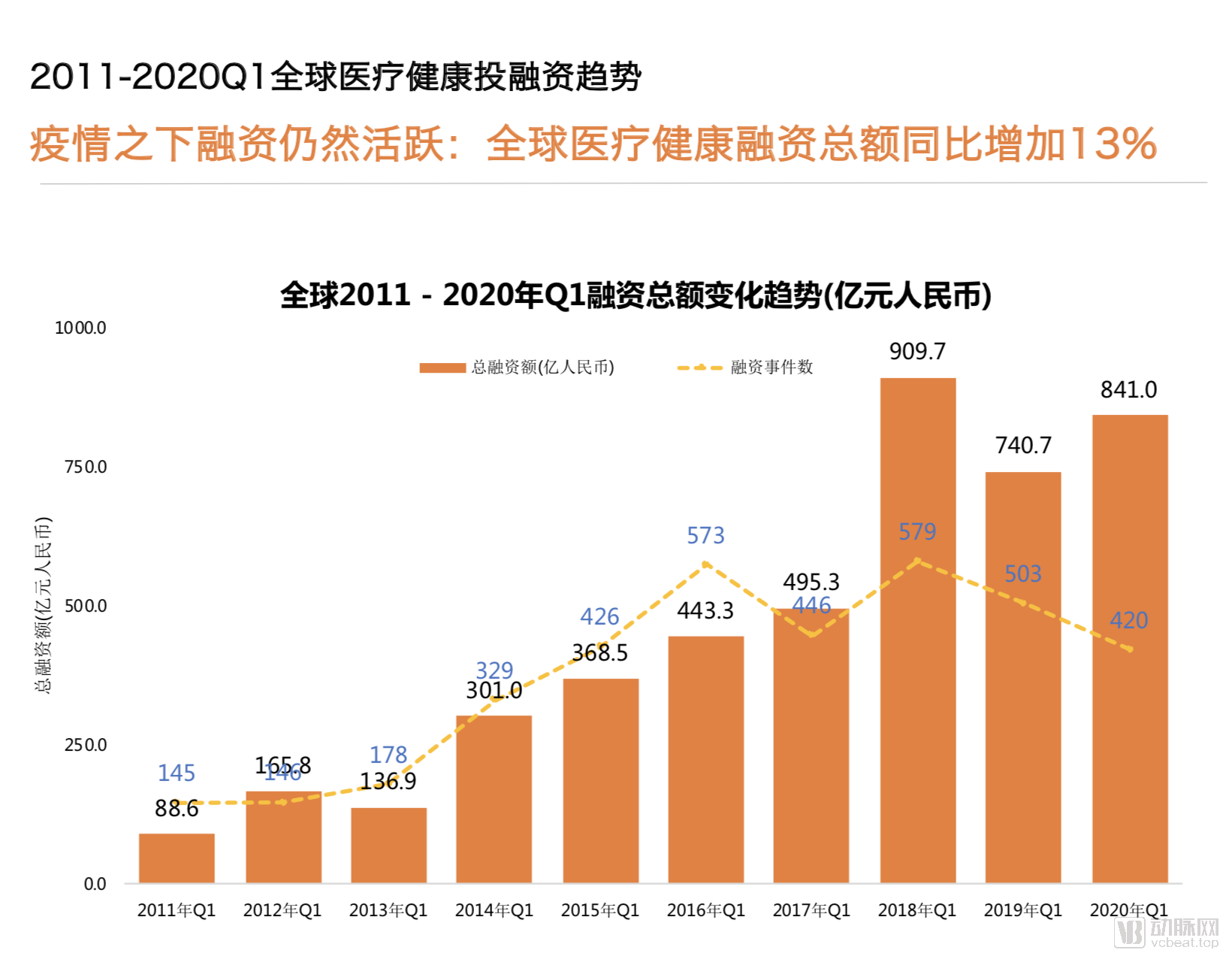

(1) Financing Remains Active Amid the Pandemic: Global Healthcare and Medical Financing in Q1 2020 Increased by 13% Year-on-Year

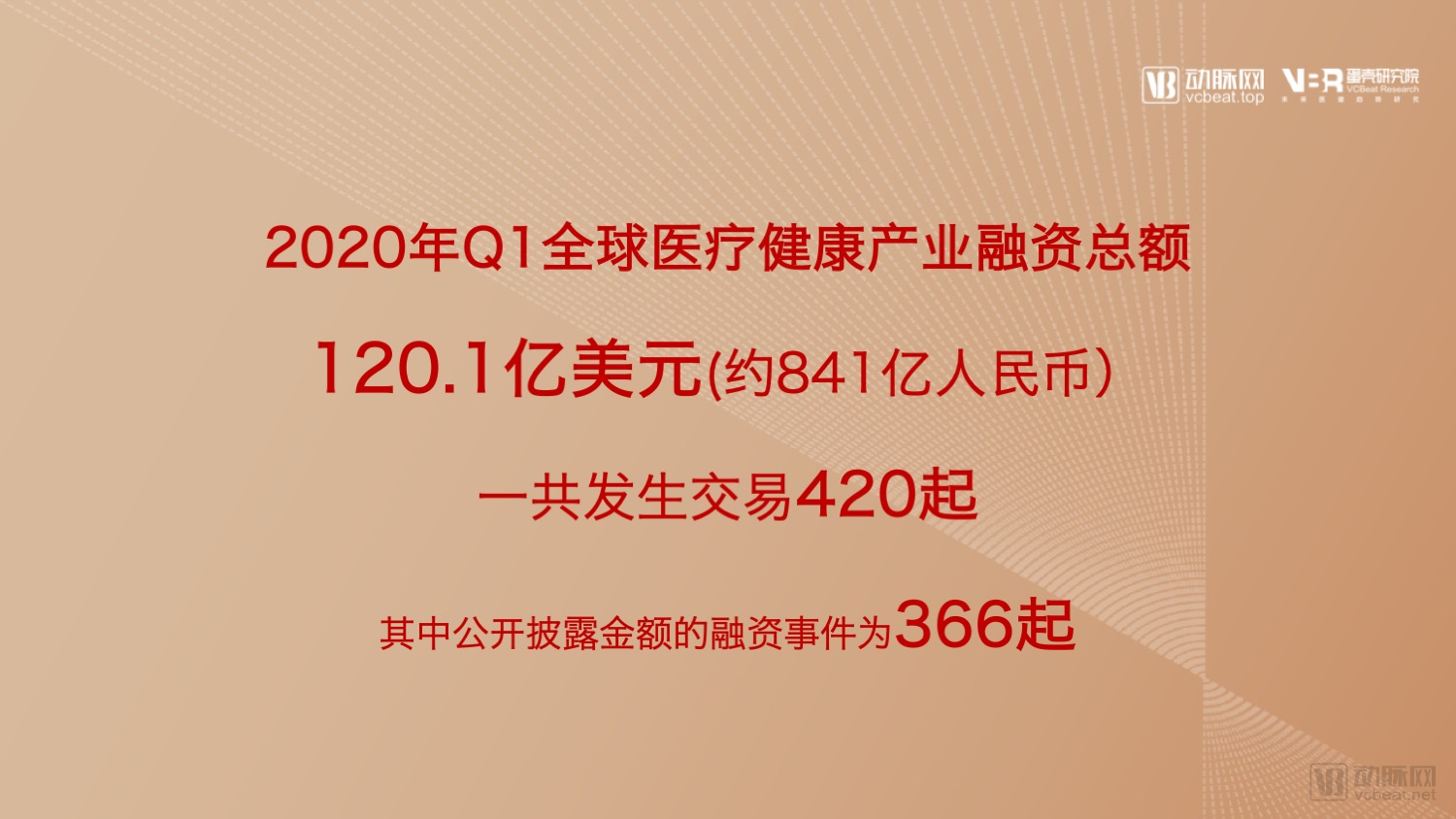

In the first quarter of 2020, a total of420 Financing Events(including 54 undisclosed financing events), with total funding reaching$12.01 billion(approximately RMB 84.1 billion), representing a 13% year-on-year increase in financing amount.

Although the total amount of global healthcare financing remains high, the number of financing events has declined compared with previous years, mainly due toBased on the decline in financing events in China (a year-on-year drop of nearly 50%).The epidemic has slowed the resumption of work for a large number of startups and investment institutions in China, thereby affecting the progress and disclosure of financing projects.

We found that despite the global shadow cast by the COVID-19 pandemic and intensified instability in the global economy, financing activities in the healthcare sector remained highly active in the first quarter of 2020. However,Given the inherent lag in investment and financing data as an indicator of capital market sentiment, the impact of the pandemic on primary market fundraising may become more pronounced in subsequent quarters.

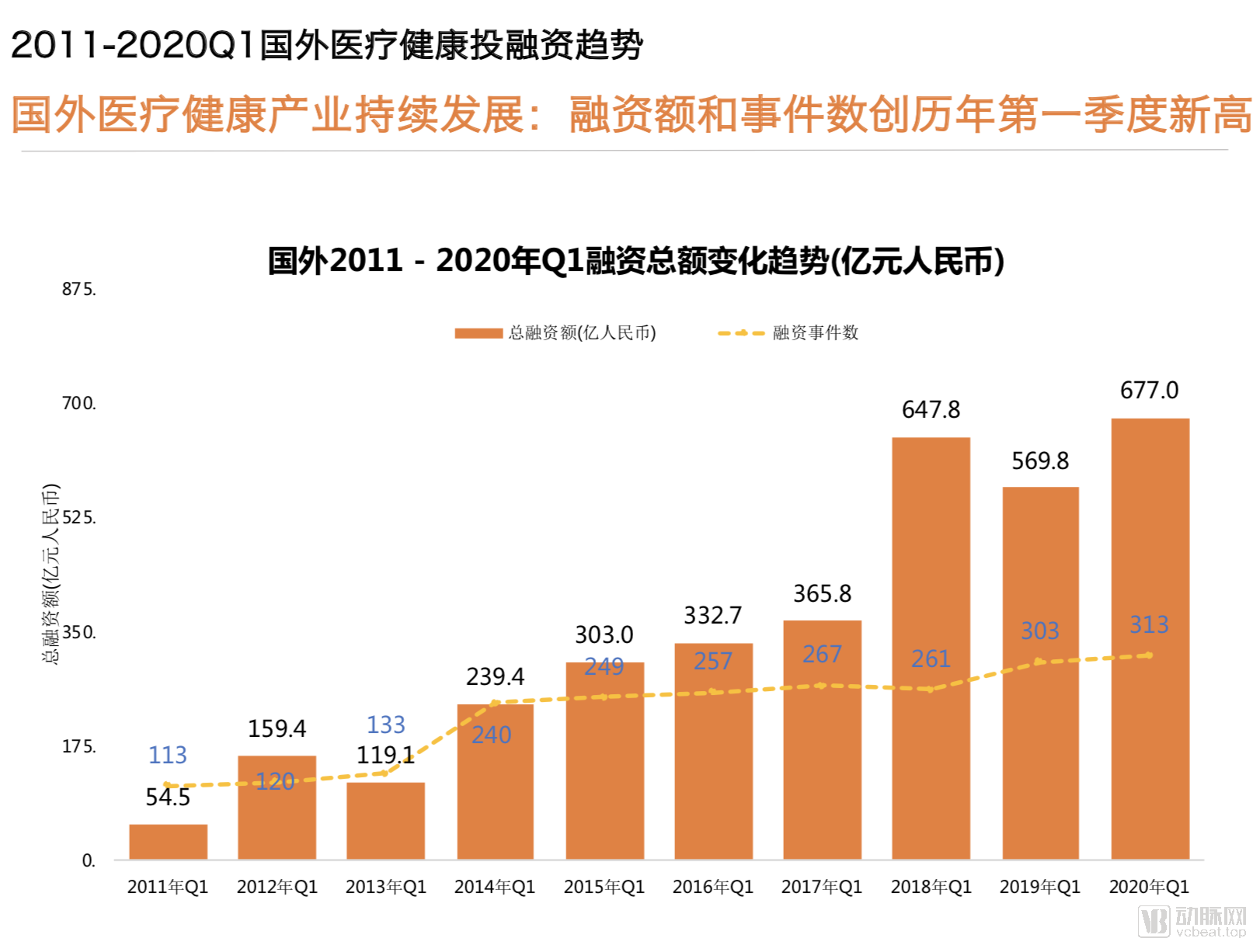

(2) Continuous Development of the Overseas Healthcare Industry: Financing Amount and Number of Financing Events Hit Record Highs for the First Quarter

In the first quarter of 2020, the overseas healthcare and medical industry continued to thrive, with total financing reaching a historical Q1 high of $9.67 billion (approximately RMB 67.7 billion). The number of financing deals also hit a record high of 313 (including 33 deals with undisclosed amounts).

Amidst the severe turbulence in international capital markets, with industries such as tourism and entertainment consumption falling into distress, primary market financing for the overseas healthcare industry has continued to demonstrate robust growth.However, it is important to note that after the severe turbulence in global capital markets, even as the pandemic subsides, the potential economic recession will likely cool and rationalize overseas capital markets, potentially slowing down subsequent financing growth.However, forDigital HealthIf the pandemic benefits specific sectors, it may trigger a new wave of financing.

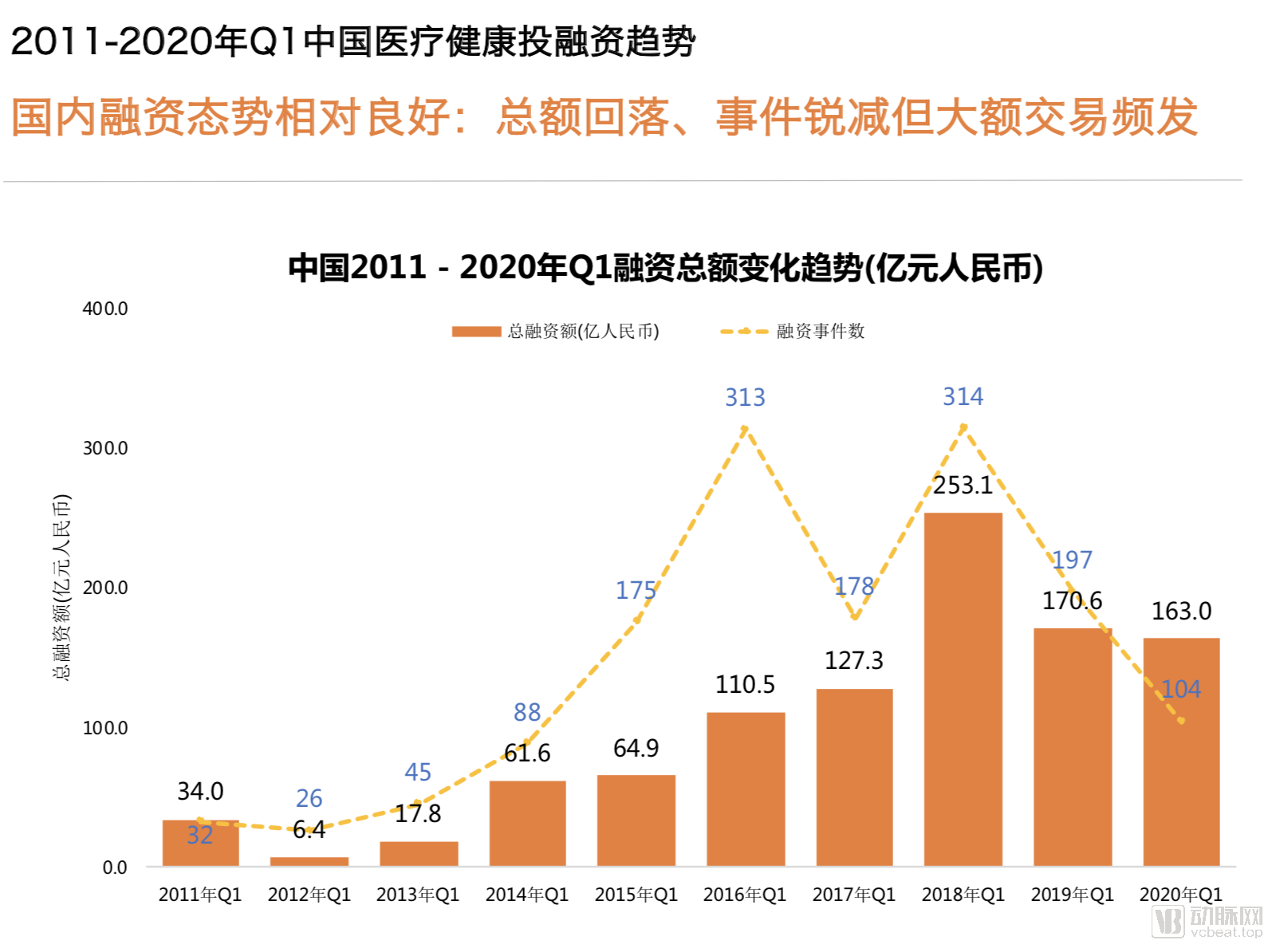

(3) The financing landscape for China’s healthcare industry remains robust: while total funding amounts have declined and the number of financing deals has dropped sharply, large-scale transactions are occurring frequently.

Q1 2020,A total of 104 financing deals occurred in China’s healthcare industry, hitting the lowest point since Q1 2015 and nearly halving compared to the same period last year.

Affected by the dual impact of the novel coronavirus and China’s overall capital environment, the number of healthcare financing deals in the first quarter of 2020 declined sharply. Notably, however, despite the steep drop in the total number of financing transactions, the total amount raised remained nearly on par with the same period in 2019. This was primarily driven by a significant number of large-scale financing rounds during the quarter, with 47 individual deals exceeding RMB 100 million each.

Furthermore, according to data from IT Juzi, there were 634 investment deals in the new economy sector across all industries in Q1 2020, a year-on-year decrease of 44.5%; the total transaction amount reached RMB 119.1 billion, a year-on-year decline of 31.3%. We have observed that the healthcare industry remains resilient, accounting for nearly one-sixth of all financing events across industries. In addition, the pandemic is expected to accelerate the development of more specialized segments, such as in vitro diagnostics (IVD) and internet healthcare. Therefore, we believe that China’s healthcare industry will continue to exhibit strong growth prospects in the future.

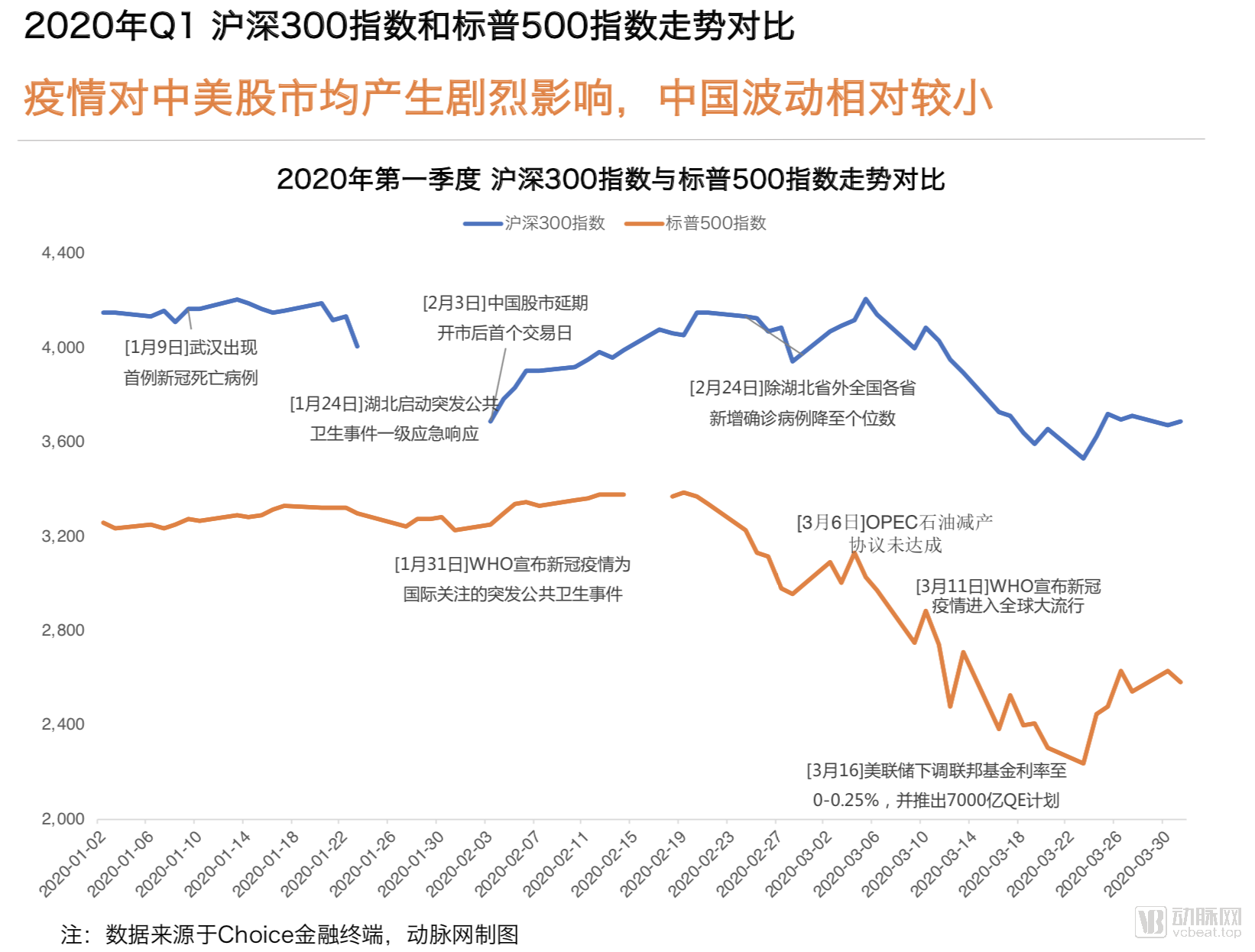

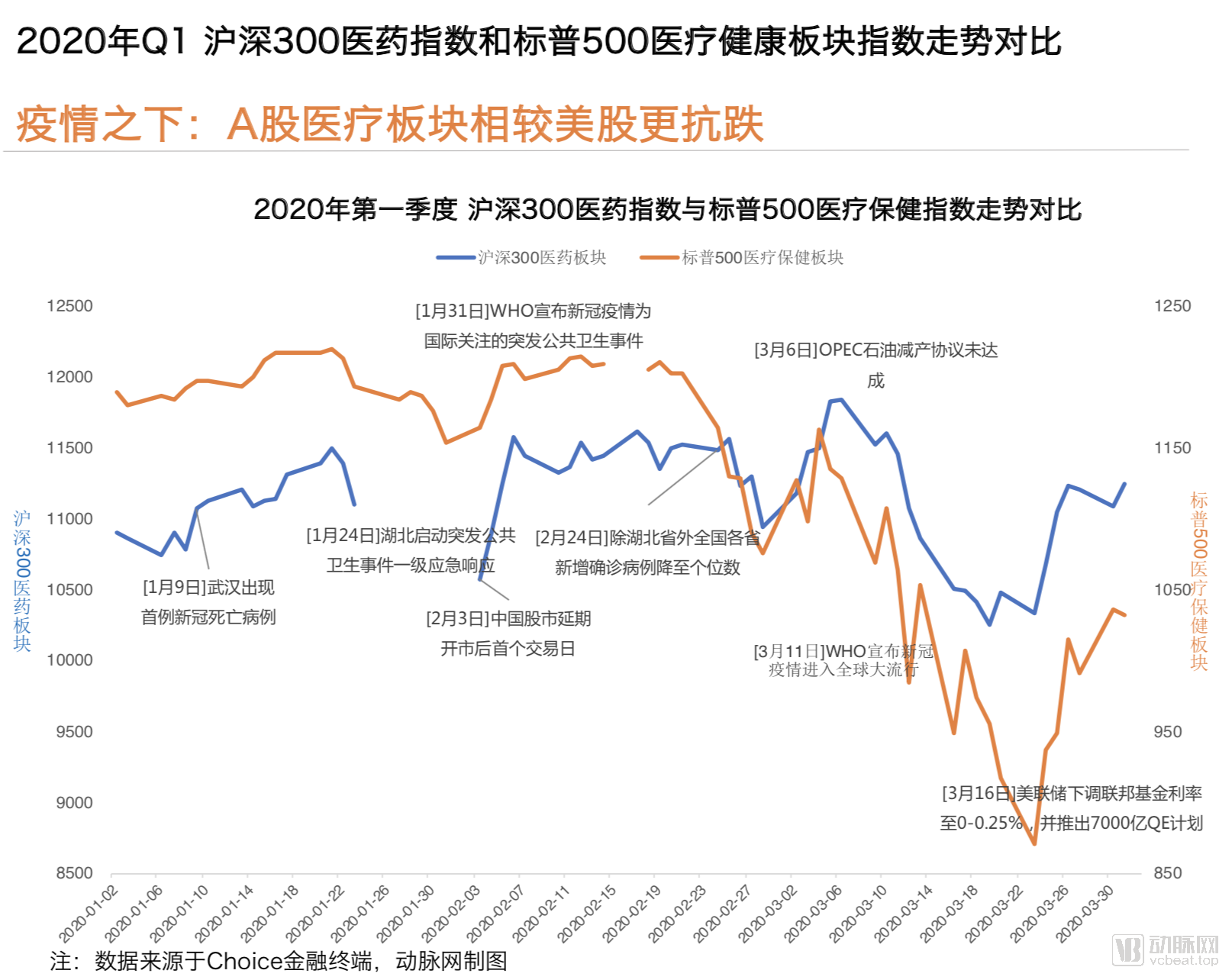

(1)Amid the Pandemic: The Outbreak Has Severely Impacted Both Chinese and U.S. Stock Markets, with Relatively Lower Volatility in China

Comparing the two curves,It is evident that the stock market movements in both countries are correlated. Although the epidemic in China was effectively contained by March, its global spread still caused the CSI 300 Index to decline in tandem with the plunge in U.S. stocks.However,China has seen relatively less fluctuation.

At the beginning of the year, China was the first to be affected by the COVID-19 pandemic, briefly plunging into a situation of production halts and a sharp decline in consumption. On the first trading day after the 2020 Spring Festival holiday, the A-share market experienced a significant drop. However, as China implemented effective epidemic control measures, the CSI 300 Index began to recover.

Compared with the S&P 500 Index, the decline in U.S. stocks in February was mainly driven by developments in energy markets. As the pandemic spread globally and OPEC’s production-cut negotiations collapsed, oil prices plummeted, further rattling international financial markets.

On March 9, 12, 16, and 18, U.S. stocks experienced four circuit-breaker halts within a mere two weeks. Dragged down by this turmoil, China’s A-share market also began a sustained decline.

On March 23, the Federal Reserve announced a series of measures to support U.S. dollar liquidity, initiating an unlimited quantitative easing (“money-printing”) mode. Since then, U.S. stocks have begun to rebound amid volatility...

(2) Amid the Pandemic: A-Share Healthcare Stocks Show Greater Resilience Than Their U.S. Counterparts

A comparison of the Q1 trends in the healthcare sector indices of China and the United States in 2020 reveals that,The impact of the pandemic on China’s healthcare sector was far less severe than on that of the United States.

The CSI 300 Healthcare Index declined only in line with the broader market after the Spring Festival holiday trading resumed; even on the day when the Shanghai Composite Index fell by more than 7%, the healthcare sector dropped by just 3%. Subsequently, as demand for medical resources surged explosively, the pharmaceutical and biotechnology sector continued to rise.

Until late February, under the dual impact of the crude oil price war and the global stock market plunge, the trend of China’s pharmaceutical and biological index gradually paralleled that of the U.S. healthcare sector, but with significantly lower volatility than its U.S. counterpart during the same period.

Compared with the maximum amplitude of stock indices in the first quarter, the S&P 500 Healthcare Sector fell by nearly 30%, while the A-share pharmaceutical sector proved more resilient, with a decline of only 13%.

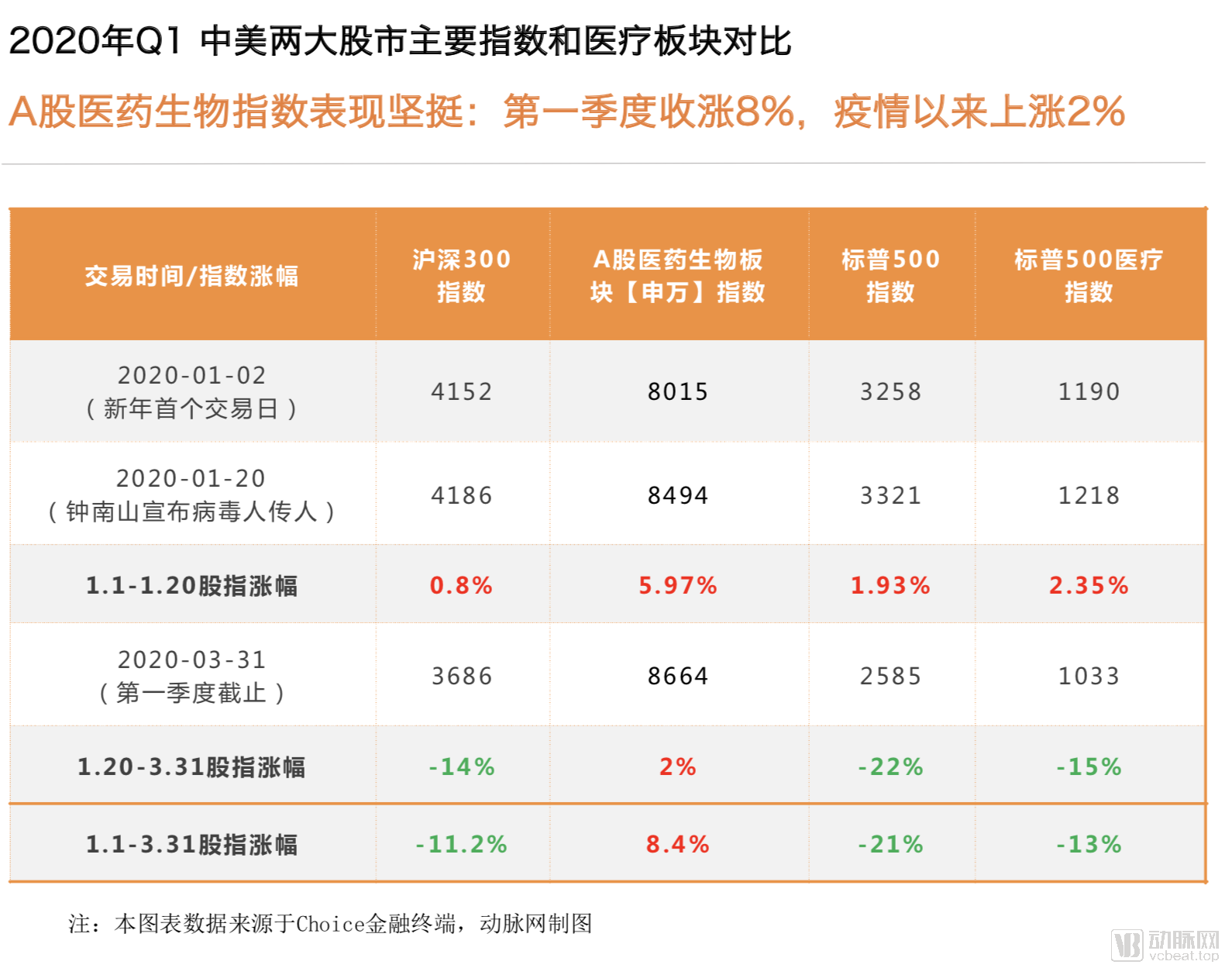

(3) The A-share pharmaceutical and biotechnology index remained resilient: it closed 8% higher in the first quarter, marking a 2% gain since the onset of the pandemic.

In the first quarter of 2020, amid the impact of the pandemic, the secondary market experienced panic-driven volatility and a downward trend.China’s healthcare sector index bucked the trend, rising 8.4% in the first quarter, while the broader Shanghai Composite Index fell more than 11% over the same period;Moreover, following the outbreak of the COVID-19 pandemic in China and globally, the pharmaceutical and biotechnology sector has maintained a 2% growth rate.

A comparison with the United States during the same period reveals that the S&P 500 Healthcare Index fell by 13% in the first quarter of 2020, a decline slightly smaller than that of the broader S&P 500 Index. Clearly, the U.S. healthcare sector was more significantly impacted by the pandemic.

A comparison of the four major indices in the table provides a more intuitive view ofShock Resistance and Risk Resilience of the A-Share Healthcare Sector During the Pandemic。

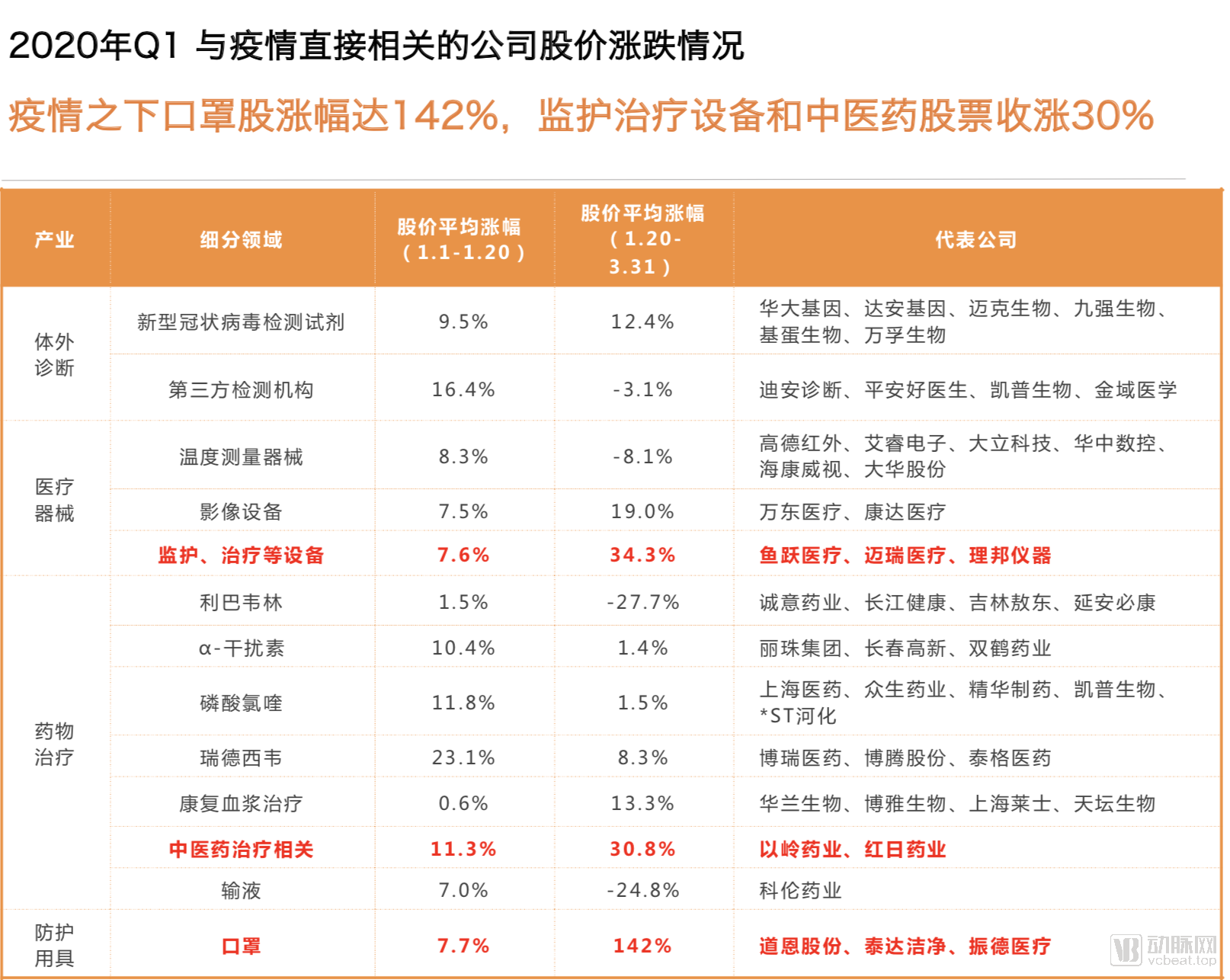

(4) Growth in A-share subsectors: Mask stocks surged 142%; monitoring and treatment equipment and traditional Chinese medicine stocks closed up over 30%

VCBeat tracked the stock price trends of selected companies in the fields of in vitro diagnostics, medical devices, and pharmaceutical treatments that are directly related to the epidemic. By designating January 20, when Academician Zhong Nanshan announced human-to-human transmission of the virus, as the key inflection point marking the onset of the epidemic’s impact, we assessed how the epidemic affected secondary market performance across different sub-sectors (as of the end of the first quarter).

Data shows that, across nearly 10 sub-sectors,Mask-related stocks saw the highest average price increase during the pandemic, reaching 142%.

Secondly,Average Gain of 34.3% for Monitoring and Treatment Equipment Stocks, representative companies include Yuwell Medical, Mindray Medical, and Edan Instruments, which manufacture ventilators or patient monitors.

Traditional Chinese Medicine (TCM) treatment stocks followed closely with a 30.8% increase, representing Yiling Pharmaceutical, the manufacturer of Lianhua Qingwen Capsules, and Chireh Pharma, the producer of Xuebijing.

(1)Frequent Financing in China's IVD Sector: 15 Deals, Cumulative Funding of RMB 760 Million

Q1 2020, ChinaIn Vitro DiagnosticsA total of 13 financing events occurred in the sector, with cumulative funding reaching RMB 760 million. These companies focus on diverse subfields and were mostly established relatively recently; consequently, their financing rounds are generally at early stages, with funding amounts typically in the tens of millions of yuan.

Since the outbreak of the COVID-19 pandemic, the in vitro diagnostics (IVD) industry has garnered increased attention, and the Chinese government has introduced multiple policies to accelerate the approval of diagnostic reagents. The rapid response—launching six test kits within 15 days after the viral genome was published—demonstrates the progress made in China’s public health system and IVD R&D capabilities since the SARS epidemic. Currently, China’s IVD industry has transformed from merely replicating foreign products to independently developing rapid molecular diagnostic solutions. In the future, there is significant potential for domestic substitution in advanced methodological areas such as chemiluminescence and molecular diagnostics.

Jinshi Medicine focuses on the development of diagnostic products for infectious diseases and the provision of medical testing services. It completed its Series B+ financing round in January, just two months after its Series B round. The rapid growth of the pathogen detection industry and a series of recent industry changes were among the reasons for the company’s additional Series B+ fundraising. The company has also launched the “2019-nCoV Novel Coronavirus Nucleic Acid Test Kit.”

(2) Transaction activity in the overseas digital health sector remains robust, with the pandemic potentially further stimulating its development

After March, the COVID-19 epidemic accelerated its spread in Europe and the United States. As a result, both the number and amount of financing events abroad declined in March. However, this decline had little overall impact on quarterly financing.

In the first quarter of 2020, the digital health sector abroad remained highly active, with a total of 115 financing events and cumulative funding amounting to USD 2.71 billion (approximately RMB 19 billion).

Amid the heightened threat of the pandemic in March, nearly 30 digital health companies successfully secured financing, including online consultation and appointment platforms and telemedicine service providers. As their role in combating the epidemic becomes increasingly prominent, financing for the digital health sector is likely to receive further stimulus.

(3) Long-term positive outlook for healthcare: The COVID-19 pandemic has provided certain long-term benefits to all four major subsectors.

Medical diagnosis, research and development of new drugs and vaccines, online consultation services, and medical robots have emerged as prominent applications in the fight against the epidemic, drawing widespread public attention. This trend will facilitate the further development of the healthcare industry in the medium to long term.

In short, the fundamental long-term bullish logic of the healthcare industry should remain unchanged, whether driven by the stimulus from this pandemic, supported by national strategies and policies, sustained by its consistent high-speed growth in recent years, or shaped by China’s increasingly severe aging population.

(1) Global Distribution of Financing by Sector: Biopharmaceuticals leads the pack, with digital health following closely behind;

In the first quarter of 2020, the global biopharmaceutical sector led all subsectors with 186 transactions and a total financing amount of RMB 41.67 billion.

In addition to the perennially hot sector of biopharmaceuticals, digital health funding remained highly active this quarter. Furthermore, we believe that the application of AI, big data, and telemedicine on the front lines of the pandemic response will likely further drive innovation and financing in the digital health sector, sparking a new wave of investment.

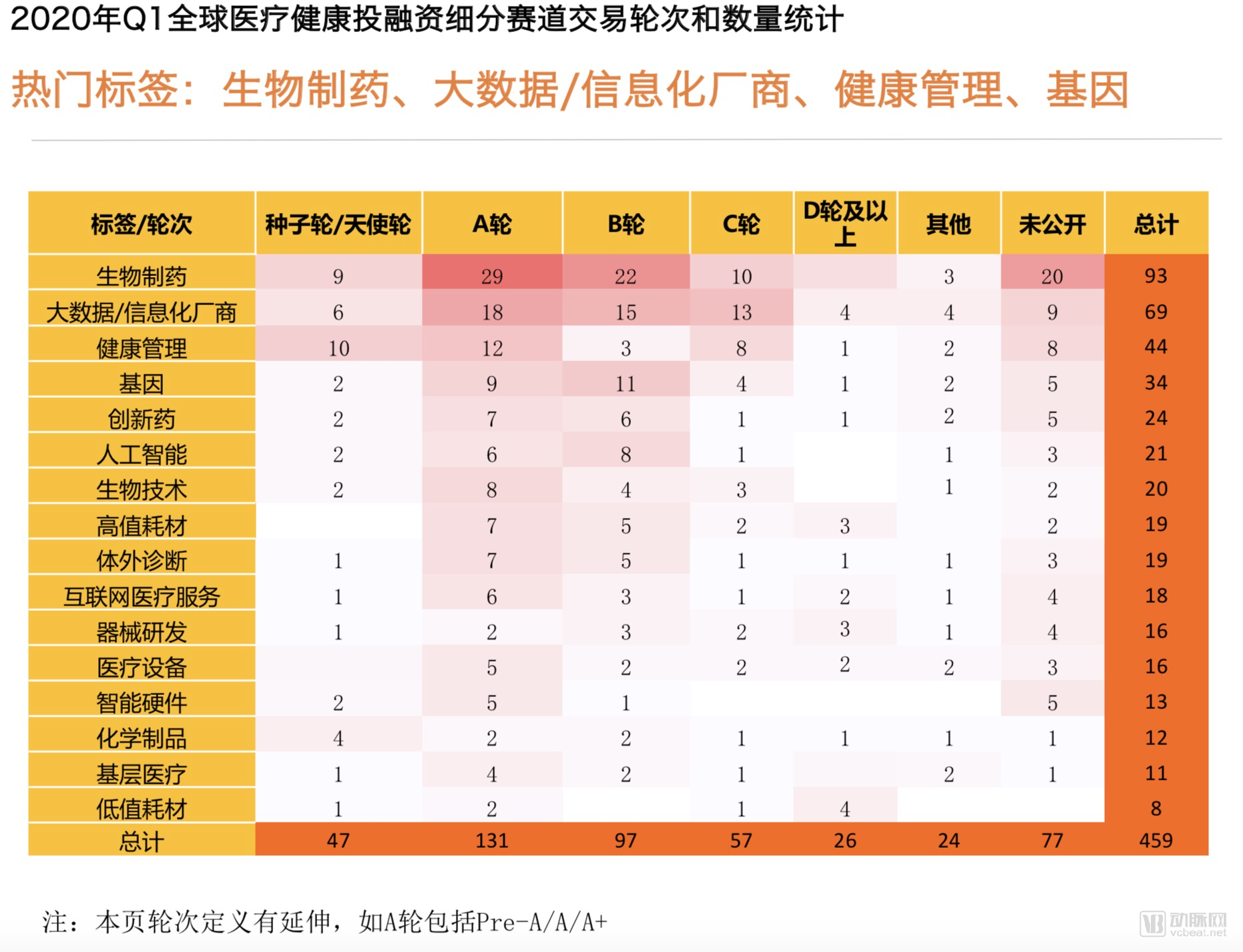

(2) Global Hot Financing Tags: Biopharmaceuticals, Big Data/IT Vendors, Health Management, Genomics;

(3) Digital health is booming abroad, while the domestic medical service landscape is favorable.

In the first quarter of 2020, tags such as global biopharmaceuticals, big data/informatics vendors, health management, and genomics garnered significant attention.

In addition to the perennially hot biopharmaceutical sector, digital health companies have received substantial financing support amid the pandemic.

From the distribution of financing rounds,Q1 2020 Saw the Highest Frequency of Series A Financing Events, reaching 131 cases; among them, there were 29 Series A financing events in the biopharmaceutical sector.

A comparison of the distribution of financing across various healthcare sectors in China and abroad during the first quarter of 2020 reveals that biopharmaceuticals remained the most heavily favored sector both domestically and internationally. However, there were differences in financing focus across other sectors. Abroad, digital health experienced robust growth, with 115 financing deals completed in a single quarter, accumulating a total of RMB 19.24 billion. In contrast, financing activities and amounts in other sectors in China were more evenly distributed, with medical services demonstrating a relatively stronger financing trend.

(1) Khosla Ventures was the most active investor in the first quarter, backing eight healthcare startups;

In Q1 2020, Khosla Ventures was the most active global investor in healthcare, making eight investments during the quarter. Its frequent investment areas included digital health, genetic testing, and in vitro diagnostics. Among the companies receiving co-investments from active institutional investors, those in the biopharmaceutical sector predominated, such as China’s innovative drug companies Legend Biotech and Abbisko Therapeutics.

(2) New Drug Development and Digital Healthcare Draw Attention, with 9 Institutions Making Five Investments in a Single Quarter

In the first quarter of 2020, a total of 14 institutions made five or more investments. Active investment firms invested more frequently in Series C companies.

Khosla Ventures made eight investments in a single quarter, with most portfolio companies at Series A stage; the firm favors digital health and biotechnology. Five Chinese institutions—Qiming Venture Partners, HongShan, Yifeng Capital, Lilly Asia Ventures, and Vivo Capital—entered the list of active investors this quarter.

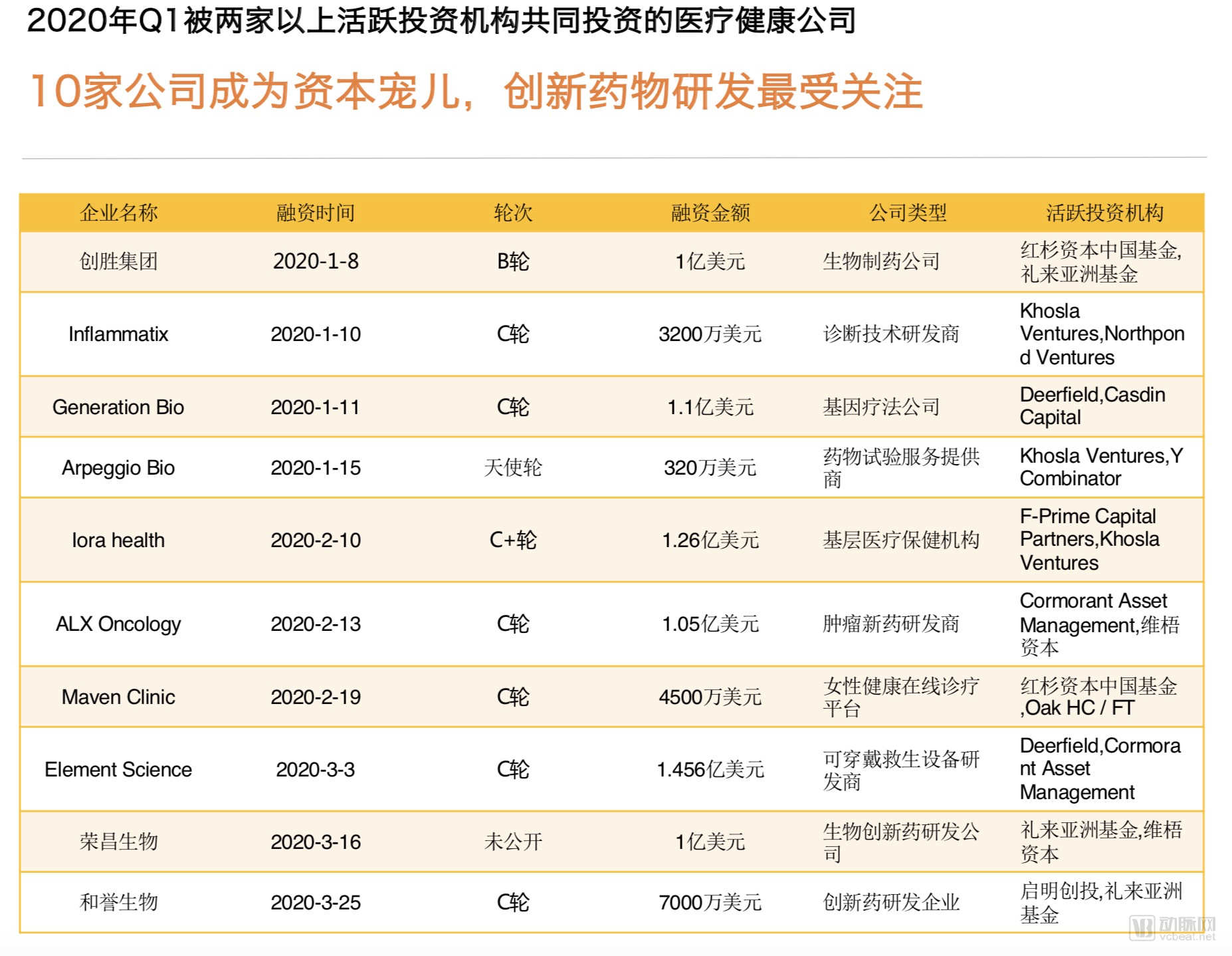

(3) Ten companies have become investor favorites, with innovative drug R&D drawing the most attention.

Among the top 10 healthcare investment institutions by number of investments in Q1 2020, 10 portfolio companies received backing from two or more of these investors, reflecting the potential and strength of these startups.

From the perspective of round distribution,The likelihood of receiving simultaneous investments from two active top-tier firms is higher around the Series C round, which also indicates that companies at this stage have more mature business models or R&D progress. FromIn terms of company types, the ten companies represent a more diversified range of sectors. Beyond conventional hotspots in recent years such as oncology therapeutics and gene technology, digital health has continued to develop. Health service provider Iora Health and Maven Clinic, an online telemedicine platform for women’s health, have both received cross-investments from active institutional investors.

Among the 10 companies are three Chinese firms: Transcenta Holding, RemeGen, and Abbisko Therapeutics, all of which have received investment from Lilly Asia Ventures.

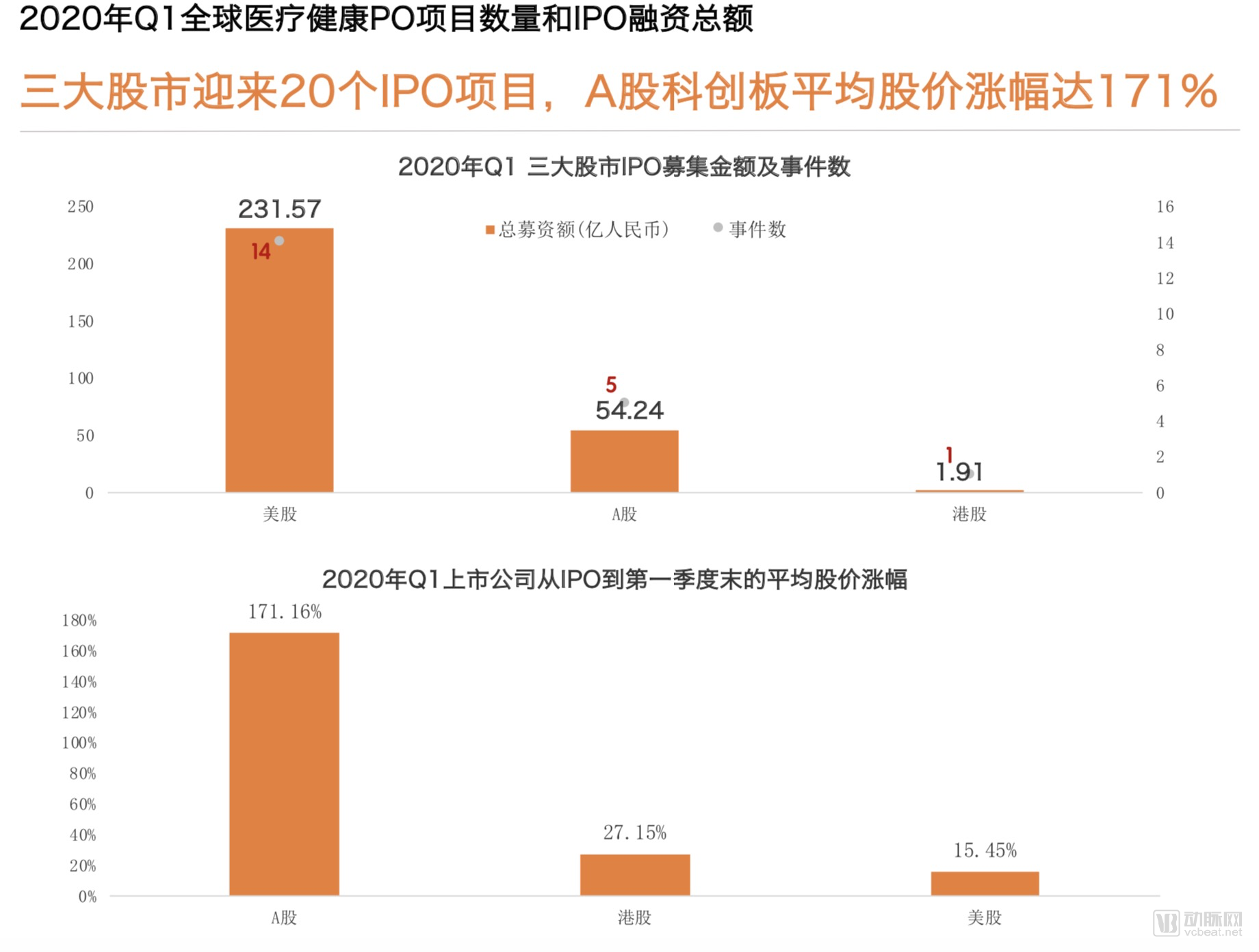

(1) The A-share, Hong Kong stock, and US stock markets welcomed 20 IPO projects, with the average share price increase on the STAR Market reaching 171%;

In the first quarter of 2020, 20 healthcare companies went public across the U.S., A-share, and Hong Kong stock markets. Among them, 14 listed in the U.S., securing an absolute majority of the total capital raised across the three markets; additionally, 5 companies listed on the A-share market, and 1 on the Hong Kong stock market.

However,A potential global economic recession in the future will likely dampen investor interest in IPOs, casting a somewhat dim outlook on capital exit prospects for 2020.

Despite the poor performance of the secondary market amid the pandemic, the IPO prices of this batch of newly listed healthcare stocks have mostly continued to rise, especially inSix companies listed on the STAR Market of China's A-shares,As of March 31, 2020,Its average stock price increase since listing reached 171%.

(2) In the first quarter, eight Chinese healthcare and medical companies completed their initial public offerings (IPOs), with all A-share listings on the STAR Market;

In the first quarter of 2020, affected by the pandemic, the IPO processes of Chinese healthcare companies were delayed. As of March 31, 2020, a total of eight Chinese healthcare companies were listed on the A-share, Hong Kong Stock Exchange, or U.S. stock markets.

All five companies listed on the A-share market went public via the STAR Market. Since MicroCore Biopharma became the first biopharmaceutical company to list on the STAR Market in June 2019, the pace of IPOs for domestic biopharmaceutical enterprises has accelerated. Amid the broader economic downturn, the STAR Market has provided more options for capital exit for biopharmaceutical companies.

(3) Five companies went public within five years of their establishment, with Passage BIO taking only 2 years and 7 months from founding to its IPO.

Among the 140 healthcare companies that went public in 2019, the average time from establishment to IPO was approximately 117 months (9 years and 8 months). Using this as a benchmark for comparison with companies that had their IPOs in Q1 2020, half of them took less time to go public than the 2019 average.

Passage Bio and Beam Therapeutics, the two companies with the most rapid financing progress, both belong to the gene therapy sector., especially Passage BIO, which successfully listed on the U.S. stock market after only 2 years and 7 months of establishment, achieving a rapid capital exit.

Beam Therapeutics focuses on single-base editing technology, while Passage Bio is dedicated to applying adeno-associated virus (AAV) gene therapies to treat rare central nervous system (CNS) disorders caused by monogenic defects. The rapid public listings of both companies further underscore the sustained momentum in the gene therapy sector, as gene technologies offer expanded possibilities for treating refractory conditions such as rare and genetic diseases.

(1) Global: The United States remains dominant, with China and the U.S. together accounting for 90% of global financing totals;

In the first quarter of 2020, the five countries with the highest number of global healthcare and medical financing deals were the United States, China, the United Kingdom, Canada, and Israel. The United States led the world with 208 financing deals totaling $7.49 billion (RMB 52.87 billion), followed closely by China. Together, China and the United States accounted for 90% of the total financing amount and 89% of the total number of financing deals among all countries.

Israel is one of the countries with the highest medical efficiency worldwide, boasting nearly 30 years of accumulated data from its healthcare system, 98% of which has been digitized. Although Israel’s financing volume was modest in the first quarter of 2020, six of its innovative projects ranked fifth globally. In terms of investment hotspots, digital health and biotechnology were areas of shared global focus in the first quarter of 2020.

(2) United States: California dominates, with Massachusetts and New York forming secondary hubs;

In the first quarter of 2020, California, USA, recorded a cumulative total of 67 healthcare financing and investment deals, raising $2.78 billion (approximately RMB 19.66 billion), making it the region with the highest frequency of global healthcare venture capital activity.

Massachusetts has surpassed the more economically developed New York to become the second-largest U.S. state for healthcare investment and financing, thanks to its renowned biotechnology industry cluster and abundant medical resources; however, it still lags far behind California in terms of overall scale.

(3) China: Shanghai surpassed Beijing in both the number of financing events and the total amount raised, becoming the top choice for startups this quarter.

In terms of the scale of healthcare investment and financing in individual provinces and municipalities, the five regions with the highest concentration of healthcare investment and financing deals in China during the first quarter of 2020 were, in order, Shanghai, Beijing, Guangdong, Jiangsu, and Zhejiang.

Shanghai recorded 31 financing deals, raising RMB 4.64 billion, making it the city with the highest number of financing events in the first quarter. This marks the first time that Shanghai has surpassed Beijing in both the number and total value of financing deals within a single quarter.

In terms of regional cluster development, while Beijing continues to demonstrate robust growth momentum, the Jiangsu-Zhejiang-Shanghai region has been expanding its influence in the healthcare industry in recent years and is expected to emerge as China’s largest healthcare industry cluster by investment and financing scale.

(1) Digital pharmacy Alto ranks first globally in quarterly funding, with three Chinese companies making the list;

Among the top 10 companies by financing amount in the first quarter of 2020, there were six U.S. companies, three Chinese companies, and one Israeli company. The financing amounts for all ten companies exceeded RMB 1 billion. Three Chinese companies—Da An Gene, Nanjing Legend Biotech, and Zhiyun Health—made the list.

The highest amount of financing in the global healthcare sector in the first quarter of 2020 wasAlto Pharmacy. Alto, founded in 2015 and formerly known as ScriptDash, is headquartered in the United States. The company is dedicated to building a patient-centric pharmacy with free same-day medication delivery services.

(2) Top 10 Financing Amounts in China: Biopharmaceutical Companies Occupy Eight Spots, with Two Digital Health Companies on the List.

Among the top 10 companies in China by financing amount in Q1 2020,Biopharmaceutical companies continue to hold a dominant position.

In addition to biopharmaceutical companies with consistently high financing amounts, two digital health companies—Zhiyun Health and Panoview Medical Imaging—made the list.

This quarter witnessed a significant number of large-scale financing transactions in China’s healthcare industry, with 47 deals exceeding RMB 100 million each. Even Yushu Biopharma, ranked tenth on the list, secured approximately RMB 500 million in funding.

As a digital health company focused on chronic disease management, Zhiyun Health’s completion of a RMB 1 billion financing round has attracted significant attention. Initially, the company positioned itself as a platform offering diabetes management services to consumers (patients) and patient management tools to doctors. It later expanded into serious medical care by providing SaaS platforms to hospitals and establishing an e-commerce trading platform for pharmaceuticals. In its subsequent development, the company upgraded from single-disease diabetes management to comprehensive chronic disease management and built an internet hospital.