How UnitedHealth Group Achieved $240 Billion in Annual Revenue: Building a Health Insurance and Services Powerhouse

UnitedHealth Group

Health Insurance and Health Information Technology Service Provider

Recently, UnitedHealth Group, the largest commercial health insurer in the United States, released its 2019 annual report, reporting full-year revenue of $240 billion and net profit of $14 billion.Based on annual revenue or estimated data for the same period, UnitedHealth Group is roughly equivalent to one Apple, two Microsofts, 4.5 Alibaba Groups, and 168 Kweichow Moutais.。

In 1974, UnitedHealth Group was founded in Minnesota, USA. Over its more than 40-year history, how did UnitedHealth transform from a startup into a business giant with both market capitalization and annual revenue exceeding one trillion yuan? Under what policy and market opportunities did it emerge, and how did it build a closed-loop business model combining health insurance and medical services to disrupt and reshape the healthcare ecosystem? Most importantly, what insights can UnitedHealth offer to innovators in China?

In the industry, many companies have publicly or semi-publicly declared, “We aim to become China’s UnitedHealth,” or “We intend to build a closed-loop commercial ecosystem following the UnitedHealth model.” Inspired by this vision, what are the potential development and evolutionary pathways for a “Chinese UnitedHealth”?

To this end, VCBeat has conducted an in-depth analysis of the UnitedHealth Group case to provide some insights for the industry.

The United States is one of the countries with the most developed commercial health insurance systems in the world. Since 1840, it underwent an initial development and exploration phase lasting nearly 80 years. During this period, the health insurance market experienced the emergence and decline of fragmented health insurance products and workers’ compensation insurance funds. It was not until 1966, with the rise of managed care, that commercial health insurance officially entered a period of rapid growth.

In 1973, the U.S. Congress passed the “Health Maintenance Organization Act,” shifting from a model in which only non-profit medical institutions such as hospitals provided health management services (on a fee-for-service reimbursement basis) to one in which commercial insurance companies could enter into agreements with independent physicians to deliver healthcare services to enrollees (managed care, which integrates the provision of medical services with the insurance funding required to support them).

With the introduction of legislation, Health Maintenance Organization (HMO) services have gradually been integrated into health insurance, becoming the primary form of early managed care. Compared to traditional indemnity insurance products, which face issues such as over-treatment, over-prescription, and high loss ratios, HMOs contract with physicians, paying them an annual capitation fee while requiring patients to seek care from designated doctors and hospitals, thereby effectively controlling medical costs.

In addition to managing claims and costs, managed care organizations must professionally oversee the content, format, timing, providers, and settings of medical services. This imposes stringent requirements on professional expertise, medical resources, system infrastructure, and specialized pharmaceutical services. Building an integrated healthcare service platform demands long-term accumulation and deep engagement within the healthcare industry.

Against this backdrop, UnitedHealth Group was founded.

In 1974, a group of physicians and healthcare professionals seeking to expand consumer health coverage established an organization called Charter Med Incorporated. In 1977, Dr. Paul Ellwood, a health policy researcher who had first coined the term “HMO,” and entrepreneur Richard Burke jointly founded UnitedHealth, which became the parent company of Charter Med Incorporated.

UnitedHealth Group was founded with the original mission of improving patients’ health while enhancing the overall healthcare system.

As a startup, how did UnitedHealth Group overcome the typical bottlenecks faced by startups and secure its first pot of gold?

The U.S. healthcare insurance system is divided into public and private insurance. Public insurance includes Medicare, which provides health coverage for individuals aged 65 and older, and Medicaid, which covers low-income individuals, people with disabilities, children, and other eligible groups. Individuals outside these categories must purchase health insurance privately, falling under commercial insurance. Employer-sponsored plans are typically purchased by companies for their employees, while small business owners, informal workers, and others must obtain coverage independently.

In 1979, UnitedHealth pioneered innovations in this system by launching the “Senior Health Plan,” piloting market-based alternatives to Medicare, and formulating a series of policies tailored to older adults. This established UnitedHealth as a leading provider of health services for the elderly.Throughout its subsequent development, the customer acquisition pathway through collaboration with government agencies and industry associations has been woven into the entire developmental trajectory of UnitedHealth Group.

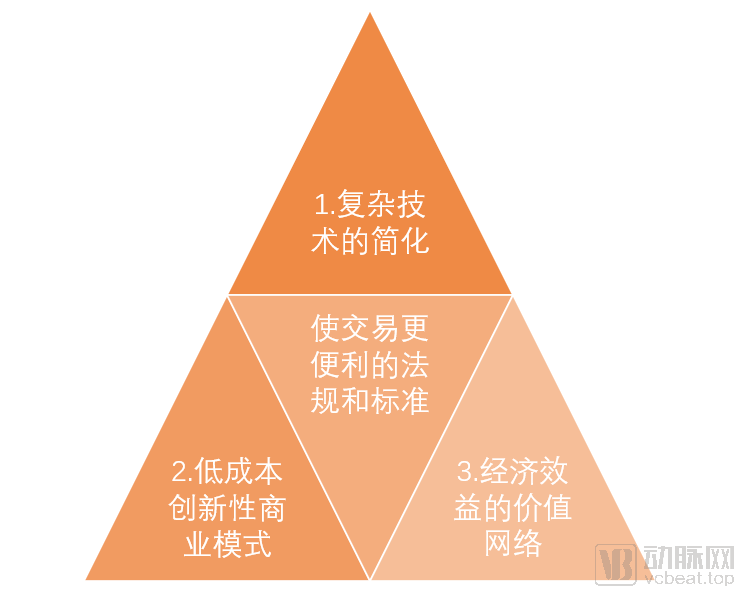

Beyond business model innovation, technological innovation is also taking shape at UnitedHealth Group. In its early stages, the company focused its operations on technology and service systems within the healthcare industry. When it went public in 1984, UnitedHealth even defined itself as a technology platform for the healthcare sector.

With business model innovation and technological innovation, coupled with the subsequent establishment of a new value network, this perfectly constitutes the triangular model of disruptive innovation. Through a series of practices and experiments, UnitedHealth Group has embarked on the path toward disruptive innovation in the healthcare industry.

(Image source: The Innovator’s Prescription)

With a DNA of disruptive innovation, UnitedHealth Group began its legendary journey.

In 1988, UnitedHealth Group pioneered the modern Pharmacy Benefits Management (PBM) business, linking benefit design with retail pharmacy networks and providing mail-order pharmacy services. The core concept behind this innovative business model was to leverage economies of scale in price negotiations with pharmaceutical companies and pharmacies, thereby helping consumers better control prescription drug costs.

The essence of the PBM model lies in aggregating demand to leverage volume for lower prices, which is fundamentally identical to the models of “national reimbursement drug price negotiations” and “volume-based procurement” that have prevailed in China’s healthcare industry in recent years.

In 1995, UnitedHealth Group acquired MetraHealth for $1.65 billion. MetraHealth was formed by integrating the group health businesses of Travelers Insurance Company and Metropolitan Life Insurance Company. This transaction was of significant importance to UnitedHealth Group, marking a critical step in its evolution into a leading player in the U.S. health insurance industry. Additionally, around that time, UnitedHealth Group also acquired four health management companies.

The growth in UnitedHealth’s business data driven by acquisitions was evident. By the end of 1996, UnitedHealth’s premiums reached $8.5 billion, representing a 151% increase compared to the end of 1994; service revenue reached $1.4 billion, marking a 408% increase over the same period.

In the same year, UnitedHealth Group also intensified its efforts in the health insurance TPA sector by launching AdjudiPro, a system capable of automating the complaint review and adjudication process. Leveraging artificial intelligence, this system helps control and reduce the time and costs associated with processing complaints submitted by physicians on behalf of patients across China.

In 1998, United HealthCare Corporation was renamed UnitedHealth Group, and its existing businesses were restructured into five independent operating units: UnitedHealthcare, Ovations, Uniprise, Specialized Care Services, and Ingenix. Each subsidiary closely aligned with the group’s mission, began to specialize in a specific segment of the health insurance industry, and quickly distinguished itself.

With the company’s group-based operations as a key milestone, the above can be regarded as the first stage of UnitedHealth’s development. During this phase, UnitedHealth rapidly overcame the bottlenecks typical of a startup by leveraging innovative business models, mergers and acquisitions, and negotiations with the government. It successfully validated its model in the journey from 0 to 1 and achieved notable accomplishments in many areas of health insurance, gradually strengthening its market position.

Following its transition to a group-based operational model, UnitedHealth achieved a leap from 1 to 10 by deepening cooperative negotiations and expanding through mergers and acquisitions, ultimately becoming an aircraft carrier-like presence in the U.S. and even global health insurance industry.

In 2007, UnitedHealth Group expanded its insurance products beyond inpatient medical coverage to include prescription drug benefits, as it became a provider for the Medicare Part D prescription drug plan. Its partnerships with Medicare and AARP have significantly aided customer acquisition for UnitedHealth Group. To date, the elderly population, which constitutes its largest revenue-contributing customer segment, continues to be primarily sourced through Medicare and AARP.

In 2009, UnitedHealthcare launched a pioneering Patient-Centered Medical Home (PCMH) initiative in Arizona, Colorado, Ohio, New York, and Rhode Island, encompassing primary care practices. This program was developed in collaboration with national professional societies for primary care. Under the PCMH model, patients receive coordinated care from their primary care physician or “medical home,” rather than fragmented and episodic care from various healthcare providers or institutions.

That same year, UnitedHealth Group partnered with Cisco to establish the nation’s first telehealth network, enabling patients to connect with physicians and specialists when in-person visits were not feasible. The “Connected Care” initiative leverages state-of-the-art videoconferencing and electronic health record technologies to expand physicians’ service reach to underserved areas in both rural and urban communities.

Between 2009 and 2010, Ingenix successively acquired a data mining company and a hospital systems R&D company, integrating them with its existing operations to form OptumInsight.

In 2015, UnitedHealth Group acquired pharmacy benefit manager Catamaran Corp. for approximately $12.8 billion, doubling its pharmacy benefit management membership to 65 million.

In 2017, UnitedHealth Group acquired the physician group of DaVita Inc., a U.S. kidney care company, for $4.9 billion.

In the same year, UnitedHealth Group’s Optum Health Services division acquired Surgical Care Affiliates, the largest ambulatory surgery center operator in the United States, for approximately $2.3 billion, adding a major surgical services company to its growing network of physician groups and clinic members. Surgical Care Affiliates operates 205 surgical facilities, employs more than 7,500 physicians, and provides care to 1 million patients annually. Its service specialties include ophthalmology, orthopedics, gastrointestinal surgery, and pain management.

In 2019, UnitedHealth Group acquired Equian LLC, a healthcare payment company, for $3.2 billion.

In terms of acquisition frequency, UnitedHealth Group has increased its pace of acquisitions in recent years. Regarding its acquisition trajectory, domestically in the United States, UnitedHealth Group primarily targets specialized healthcare services companies, leveraging Optum as its platform; internationally, it focuses on acquiring health insurance companies.

(The image shows the UnitedHealth Group building)

During the second phase of its development, as UnitedHealth Group consolidated into a conglomerate and grew into a health insurance giant, mergers and acquisitions remained its primary growth strategy. Nevertheless, the company’s achievements in other areas should not be overlooked. These include the independent or joint launch of electronic medical records (EMR) systems, telemedicine services, Accountable Care Organization (ACO) models, cancer care payment models, health management incentive programs, and medication safety support programs.

According to UnitedHealth Group’s 2019 annual report, the company reported a net profit attributable to common shareholders of $13.839 billion (approximately RMB 100 billion) for the full fiscal year 2019, representing a year-on-year increase of 15.46%. Operating revenue amounted to $242.155 billion (approximately RMB 1.7 trillion), up 7.03% year on year.

Looking back at UnitedHealth Group’s development over the past four decades, we can distill its growth trajectory into the following logic:After evolving into a major underwriter of health insurance, UnitedHealth Group leveraged its advantageous position as a healthcare payer to become the architect and leader of new medical service networks, ultimately establishing a closed-loop business model integrating health insurance with healthcare services.

This is merely a preliminary observation by the author; for an industry giant like UnitedHealth Group, with over four decades of development history, any simplistic generalization would be incomplete or inaccurate.

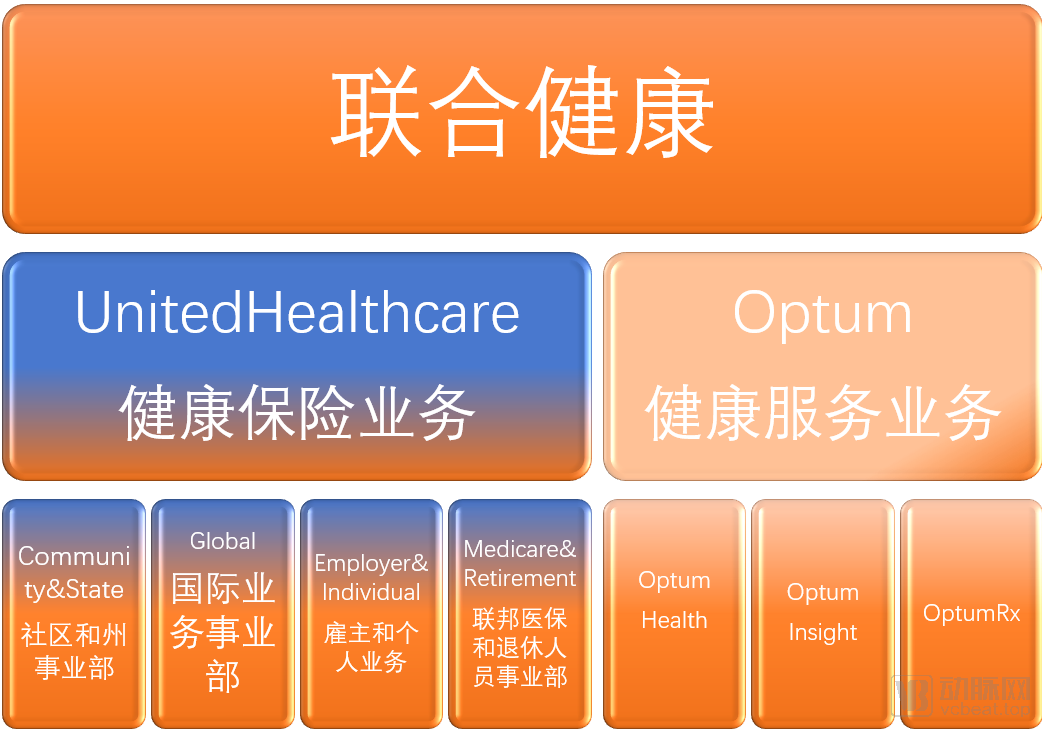

1. Organizational Structure

Today, UnitedHealth Group has formed two major business architecture systems centered around its business model, namelyThe UnitedHealthcare platform, centered on health insurance, and the Optum platform, focused on health services.

(UnitedHealth Group Organizational and Business Architecture Diagram)

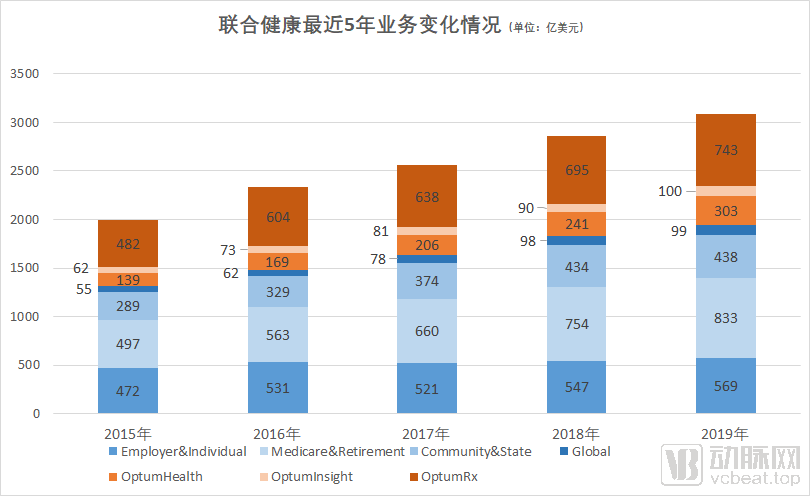

UnitedHealthcare’s Employer & Individual segment offers a consumer-oriented suite of health benefit plans and services to large employers, the public sector, small and mid-sized employers, and individuals across the United States. This segment facilitates access to healthcare services for more than 27 million people on behalf of its clients and partners. It serves 230,000 employer clients in all 50 U.S. states, with underlying business platforms including insurance companies, health maintenance organizations (HMOs), and third-party administrators (TPAs). Large employers often maintain their own health insurance management systems, for which UnitedHealth provides professional support and charges service fees. In contrast, small and mid-sized employers and individuals, due to preference or capacity constraints, are more inclined to purchase UnitedHealth’s health insurance products.

The Medicare & Retiree Division primarily serves individuals aged 50 and older, providing services tailored to this demographic’s common needs, including preventive and acute care, chronic disease management, and other specialized requirements.

UnitedHealthcare’s Community & State division is dedicated to serving state-sponsored programs that assist individuals who are low-income, have poor health status, or lack employer-sponsored health benefits. These state programs pay UnitedHealth a per-member-per-month premium. Such state-sponsored programs include Medicaid Plans, the Children’s Health Insurance Program (CHIP), Special Needs Plans (SNPs), and Integrated Medicare-Medicaid Plans, among others.

The Global Business segment primarily operates in Brazil, where it leverages the local platform Amil to provide medical insurance plans to over 4 million individuals and dental insurance coverage to 2 million. The segment owns and operates 150 hospitals, specialty centers, and various clinics across Brazil and Portugal. Additionally, it maintains a healthcare provider network in Brazil that connects 21,000 physicians, 1,800 hospitals, and 7,000 laboratories or diagnostic centers.

On the Optum platform, OptumHealth serves as UnitedHealth Group’s diversified health services platform, supporting the physical, mental, and financial health needs of 91 million people. Its MedExpress network comprises 240 community-based clinics that provide medical care for emergency and walk-in patients in a welcoming environment. Additionally, its Surgical Care Affiliates platform operates 200 ambulatory surgery centers and surgical hospitals, offering low-cost, high-value surgical services compared to traditional hospitals.

Optum Insight’s core competencies focus on data and analytics, information technology, and other areas, helping to improve healthcare quality and enhance the efficiency of healthcare systems. Optum Insight’s primary clients and markets include healthcare providers (including physicians and hospitals), health insurers, government entities, and life sciences companies. Optum Insight provides services and support to more than four-fifths of U.S. hospitals, 100,000 physicians, and approximately 300 health insurers.

OptumRx provides comprehensive pharmacy care services to 56 million people in the United States through its network of more than 67,000 retail pharmacies, multiple home-delivery, specialty, and community health pharmacies, as well as infusion services. In 2019, OptumRx managed $96 billion in pharmaceutical expenditures, including $40 billion in specialty pharmaceutical expenditures.

2. Revenue Analysis

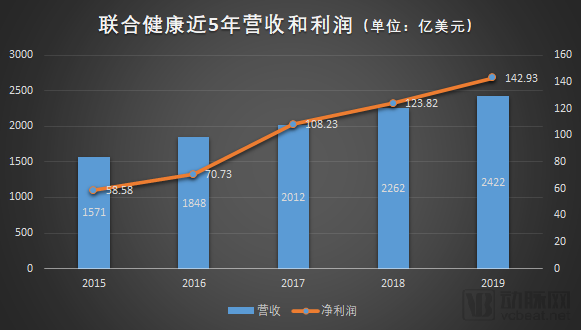

In terms of revenue, UnitedHealth Group has maintained steady growth in recent years.

The above data indicate that UnitedHealth Group’s revenue and profits have maintained a steady growth trend, without experiencing significant surges or declines. This reflects the unique characteristics of the healthcare industry, which is counter-cyclical and follows a trajectory of stable growth.

In terms of UnitedHealth Group’s operating profit margin, although the company generated $242.2 billion in revenue in 2019, its net profit accounted for only 6% of that revenue. Over the past five years, its profit margin has remained within the range of 3% to 7%. According to UnitedHealth Group’s annual report, the company typically uses approximately 80% to 85% of its premium income to cover the costs of medical services provided to customers.Thus, it is evident that UnitedHealth Group’s profitability largely depends on its ability to forecast, price, and effectively manage healthcare costs.

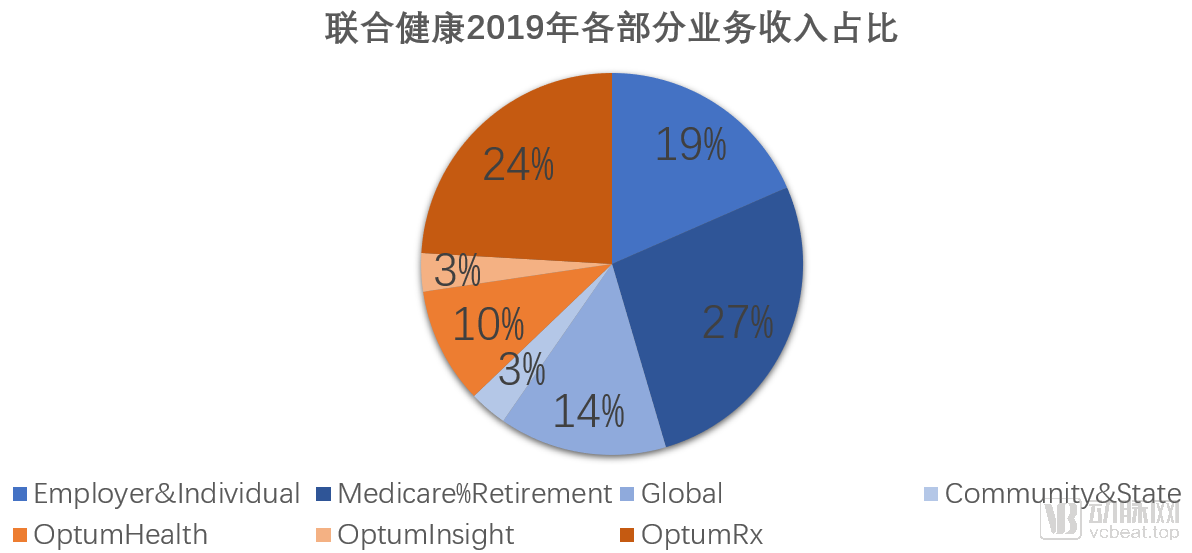

Such characteristics are more clearly reflected in its revenue structure.

As shown in the chart above, the blue segment represents revenue from the health insurance business (UnitedHealthcare), accounting for 63% of total revenue, while the orange segment represents revenue from the health services business (Optum), accounting for 37% of total revenue.

The health insurance business segment generated total annual revenues of $193.8 billion, a 5.6% increase from the previous year. The primary drivers of this growth were an increase in enrollment and savings in operational expenses. Among the four divisions within this segment, the Employer & Individual division and the Medicare & Retirees division were the main revenue contributors, generating $56.9 billion and $83.3 billion, respectively.

The Health Services business segment generated $113 billion in revenue for the full year, a year-over-year increase of 11.5%, driven by growth in both revenue and operating margin. Every division within the Health Services business segment achieved double-digit growth in operating revenue.

From the reasons for revenue growth in the two business systems, we can see that:Forecasting, pricing, and effectively managing healthcare costs are critically important to UnitedHealth Group.。

3. Analysis of Development Trends

![]()

As shown in the above charts, UnitedHealth Group’s health insurance business has experienced a significant slowdown in growth, while its international insurance operations have remained sluggish. Growth is primarily driven by two domestic U.S. segments: the Employer & Individual segment and the Medicare & Retiree segment. Leveraging technology to enhance health management and control health insurance premiums will continue to be the consistent strategic direction for the health insurance business.

In contrast, the health services segment has demonstrated a significantly higher overall growth rate than the health insurance business. In particular, OptumHealth and OptumRx are poised to become the primary engines driving UnitedHealth Group’s future growth. The digitalization and informatization of healthcare services also represent the future direction of development for the entire healthcare services industry.

History always repeats itself with striking similarity.

In today’s China, the healthcare industry, at its current stage—with crises, transformations, regulations, structural shifts, and evolving processes—appears to be on the eve of birthing a “UnitedHealth.”

In terms of policy, over the past six months,The joint issuance of the “Opinions on the Development of Commercial Insurance in the Social Services Sector” by 13 ministries and commissions, the release of the “Opinions on Deepening the Reform of the Medical Security System” by the CPC Central Committee and the State Council, and the newly revised “Measures for the Administration of Health Insurance” by the China Banking and Insurance Regulatory Commission have garnered significant policy support and robust promotion for the health insurance sector.。

“By 2025, the market size of commercial health insurance is to reach RMB 2 trillion.” Regulators have established a top-level design for the development of health insurance, outlining a clear blueprint.

On the market side, the compound annual growth rate (CAGR) of health insurance over the past five years has exceeded 30%, and the market size is expected to reach the trillion-yuan level this year. Such rapid industry growth has attracted a large influx of players and capital. Prominent first- and second-tier internet companies in China, such as Tencent, Alibaba, Meituan, JD.com, 360, and Suning, as well as leading first- and second-tier venture capital firms, such as Sequoia China, Qiming Venture Partners, Yunfeng Capital, and BlueRun Ventures, have all entered this sector.

On the demand side, driven by factors such as heightened insurance awareness in the wake of the COVID-19 pandemic, population aging, and consumption upgrading, purchasing commercial medical insurance will become a basic necessity akin to “water, electricity, and gas” for people in the future.

Moreover, the development of commercial health insurance presents the industry with even greater opportunities, in thatAs new healthcare payment methods gain widespread adoption across the industry, a novel healthcare service model tailored to these mechanisms will also be established.

This implies that the development of health insurance in China will inevitably follow the path of UnitedHealth Group, namely by establishing a “health insurance + healthcare services” network. Insurance is a unique product; consumers purchase it not with the expectation of filing claims, but to secure more comprehensive health coverage and access to superior medical services.

Despite favorable policies and market trends, the industry still faces significant pain points, such as severe product homogenization, a monolithic product structure, inadequate medical services, and low levels of technological integration. To some extent, China’s health insurance industry is still in its infancy.

Although the industry is crowded with numerous players, they often operate in silos, achieving only modest success in specific niches of health insurance. Most players lack the capability to provide medical services.No player with absolute strength has yet emerged in the current market that truly spans both health insurance and medical services.

Under such circumstances, only by truly calming one’s mind, deeply cultivating the industry, and strengthening both internal capabilities and external presence can genuine growth be achieved. If one is coerced by capital and blindly pursues performance metrics and valuations,“Salvation once received shall also be lost”。

China’s healthcare ecosystem differs significantly from that of the United States and other countries, making it impossible to fully replicate UnitedHealth Group. The growth trajectory of Chinese health insurance companies will inevitably possess distinct Chinese characteristics, and at most, they can evolve into a “UnitedHealth with Chinese characteristics” in the future. “When orange trees grow south of the Huai River, they bear oranges; when they grow north of the Huai River, they bear trifoliate oranges. Their leaves look similar, but their fruits taste different.”

The greatest lesson UnitedHealth Group has imparted to the industry is this: amid profound changes and the fleeting nature of worldly affairs, 46 years on, its mission remains remarkably similar to that at its founding.

“we are working to help people live healthier lives and help make the health system work better for everyone.”

We are committed to helping people lead healthier lives and strive to make the healthcare system work better for everyone.

Source

1. “UnitedHealth: A Giant in the U.S. Health Insurance Industry,” Wang Guangying, https://mp.weixin.qq.com/s?src=11×tamp=1586309274&ver=2265&signature=eRPIFmhr3iZQI0tHpx5v37krvRGNrAFWvkkclKlPkB1oSN2BLRQ9q7VYEAnl0ZiwzZhMrUjCMeU1E5QszBrPvZ5UTF7ifaLfvUo0P1fxWdpQFcOwu*EHorsaLjPSV3l5&new=1

2. “UnitedHealth’s Market Cap Approaches $200 Billion: How Can Chinese Health Insurers Learn from It?”, iFenxi, https://36kr.com/p/5098785

3. UnitedHealth Group 2019 Annual Report

4.https://www.businesswire.com/news/home/20200115005257/en/