Internet + Healthcare Market Enters 4.0 Era, Projected to Surpass RMB 160 Billion in Next Three Years

Recently, IQVIA released an industry research report titled “Emerging from the Cocoon: White Paper on Internet Plus Healthcare (Part I).” Authored by IQVIA’s Consumer Health Consulting team, the full text of the report is published with authorization from VCBeat (WeChat ID: vcbeat). The report reviews the historical development and current state of the Internet Plus Healthcare market and provides an outlook on its future landscape.

Introduction

The novel pneumonia epidemic sweeping across China was officially named COVID-19 by the World Health Organization on February 12, 2020. Regions throughout China actively responded by implementing a series of necessary epidemic prevention and control measures. On March 20, 2020, the number of newly confirmed cases nationwide dropped to 41. Thanks to the joint efforts of all parties, the COVID-19 outbreak in China has been effectively contained.

According to incomplete statistics based on publicly available data, by February 2020, during the epidemic period, more than 10 internet healthcare platforms across China had launched online consultation columns, and over 200 public hospitals had provided free internet-based diagnosis and treatment or online consultations for COVID-19. Within four days of its launch, Alibaba Health’s online free clinic platform recorded 1.6 million visits. By February 11, Ping An Good Doctor’s platform had reached 1.11 billion visits, with a tenfold increase in newly registered app users and a ninefold increase in the average daily number of consultations among new users. As of 3:00 p.m. on February 10, the free clinic section dedicated to combating the novel coronavirus on WeDoctor’s Internet General Hospital had received over 97.02 million visits, mobilized 26,000 doctors for online consultations, and cumulatively provided 1.16 million medical advisory services.

On this smokeless battlefield of epidemic prevention and control, the Internet, as an enabling tool, has played a significant role in four key areas: ensuring the openness and transparency of epidemic-related information, disseminating medical knowledge on disease prevention and control while guiding public opinion, safeguarding people’s livelihoods, and coordinating and allocating healthcare resources.

Figure 1. Timeline of the COVID-19 Pandemic Development

1. Ensure the openness and transparency of epidemic information

Internet healthcare companies such as Dingxiang Doctor, Tencent Health, Ping An Good Doctor, WeDoctor, and Haodf promptly aggregated epidemic data during the outbreak, including the latest numbers of confirmed, suspected, critical, deceased, and recovered cases globally and across all regions in China, as well as the latest news related to the epidemic in each region, thereby disseminating frontline information to the public. As of February 25, Dingxiang Doctor’s real-time epidemic updates had garnered over 2.5 billion views, while Tencent’s epidemic

The topic has garnered over 1.8 billion views.

2. Disseminating Medical Knowledge on Epidemic Prevention and Control, and Guiding Public Opinion During the Outbreak

While disseminating pandemic-related information, internet-based healthcare companies have scientifically and comprehensively compiled disease-related knowledge, presenting to the general public in an accessible manner the definition, transmission routes, incubation period, and symptoms of the novel coronavirus, as well as various daily preventive measures. In light of the diverse scenarios faced by the public during the pandemic—such as “travel needs,” “households with elderly members,” “households with pregnant women or children,” and “healthcare personnel”—these companies have provided targeted protection guidelines and recommendations.

Timely scientific debunking or verification of online “rumors” should be conducted. While enhancing the public’s reserve of scientific knowledge on protective measures during the epidemic, this approach also alleviates public panic stemming from unknown viruses and unverified information sources. It facilitates better management of overall public opinion trends, guiding the public to cooperate more proactively and scientifically with local health and epidemic prevention efforts.

3. Safeguarding People's Livelihood

Alibaba, Meituan, and Ele.me, along with various e-commerce and O2O platforms, provide essential daily supplies to the public, addressing challenges in everyday life during the pandemic. Alibaba deployed its Hema Fresh team as a specialized unit to ensure the supply and delivery of goods during the Spring Festival, while also delivering food, drinking water, and other necessities to medical institutions and elderly individuals living alone across China. Meituan Waimai established a special task force for novel coronavirus pneumonia prevention and control. From Wuhan, the epicenter of the outbreak, to the rest of China, rider protective equipment, station disinfection, and temperature screening measures were aligned with standards for medical and epidemic prevention personnel. The platform provided “contactless” delivery services to consumer-end users, ensuring food safety.

Furthermore, various internet platforms for communications, education, and office productivity provide solutions that enable remote teaching and remote work, thereby ensuring the continuity of educational operations and business activities.

4. Coordination and Allocation of Medical Resources

4.1. Online Consultation

Major internet-based consultation platforms, including Ali Health, Chunyu Doctor, Tencent Healthcare, DXY, Ping An Good Doctor, WeDoctor, and Haodf, have all launched special columns on “COVID-19.” These platforms match users with physicians from departments such as respiratory medicine, internal medicine, and infectious diseases to provide online consultation services to the public. Platforms like Haodf Online, JD Health, and Ali Health also offer rapid consultation services for COVID-19, thereby alleviating pressure on physical medical institutions.

Provincial health authorities across the country have actively responded to national policies by coordinating the development of internet-based service platforms and encouraging various medical institutions to go online.

1) According to publicly available statistics, by early February 2020, more than 200 public hospitals across various regions had launched online services during the epidemic period, providing consultations for common diseases, prescription renewals for chronic conditions, and medication delivery. These hospitals also introduced innovative service models tailored to their respective departments. For instance, Shanghai Sixth People’s Hospital offered online prescriptions for common and chronic diseases, along with “zero-contact” in-hospital medication pickup and home delivery services.

2) On February 14, the Hainan Provincial Health Commission announced the official launch of the Hainan Internet Hospital Platform for COVID-19 Diagnosis and Treatment Services, which integrates 16 internet hospitals in Hainan Province to provide 24/7 services.

4.2. Online Medicine Purchase

During the pandemic, patients avoided visiting hospitals and brick-and-mortar pharmacies to purchase medications. Meanwhile, as offline pharmacies faced inventory emergencies for certain epidemic prevention supplies, a large number of consumers flocked to online channels for purchasing medicines.

B2C online pharmaceutical e-commerce platforms such as Ali Health and JD Pharmacy, as well as O2O online pharmaceutical e-commerce players like Dingdang Kuaiyao and Kuaifang, have all witnessed significant surges in traffic, active users, and purchases.

Brick-and-mortar pharmacies are also actively leveraging various online platforms by joining O2O services such as Ele.me and Meituan, or by developing their own platforms (e.g., mobile apps and WeChat mini-programs) to better provide pharmaceutical care services to both new and existing customers, thereby generating additional sales.

4.3. Online Chronic Disease Management

During the pandemic, minimizing outings was the primary preventive measure for elderly patients and those with chronic diseases, making internet-based chronic disease management and prescription renewal services an effective solution.

Public hospitals, Alibaba Health, JD Health, and other online diagnosis and treatment platforms have all launched services for online follow-up consultations and prescription renewals for chronic diseases. On February 11, Shanghai’s Jing’an District introduced a “Regional Healthcare + Internet” service on the WeChat platform “Health Jing’an.” This initiative connects residents of Jing’an District with local primary healthcare institutions via WeChat, providing services such as triage guidance, appointment scheduling, online consultations, and family doctor contract signing. On February 13, Alibaba Health announced a partnership with 50 pharmaceutical companies to launch the “Chronic Disease Welfare Program” on the Tmall platform. Covering more than ten common chronic conditions and thousands of medications, the program offers disease education, medication adherence monitoring,用药 guidance, and follow-up consultation reminders. By collaborating closely with pharmaceutical companies and logistics providers, the program ensures reasonable drug pricing and timely delivery.

4.4. Online Medical Insurance Coverage

For online chronic disease management, the healthcare security administrations in Shanghai; Chengdu, Sichuan Province; and Ningbo and Wenzhou, Zhejiang Province, have taken the lead in implementing solutions for online payments using medical insurance accounts. On February 12, the Healthcare Security Administration of Wenzhou, Zhejiang Province, announced the launch of online payment services for chronic diseases. Patients who are enrolled in medical insurance and have prior consultation records at primary healthcare institutions, or who have signed contracts with healthcare providers, can bind their personal information and request prescription renewals through the WeChat official account of the Wenzhou Medical Insurance Chronic Disease Medication Delivery Platform. After the contracted physician issues an electronic prescription, designated pharmaceutical distributors handle the delivery.

On February 23, Shanghai’s healthcare security administration introduced the “12 Healthcare Security Measures,” which include incorporating “Internet+” medical services into the scope of healthcare security reimbursement. This makes Shanghai one of the first cities to implement such a scheme since the National Healthcare Security Administration issued the Guiding Opinions on Improving Price Formation and Healthcare Security Reimbursement Policies for “Internet+” Medical Services in August 2019, proposing to support healthcare security coverage for “Internet+” medical services through reasonable pricing and dynamic price adjustments.

During the pandemic, the positive role played by internet and information technology in epidemic prevention, control, and national health care has been highly recognized by relevant government departments, society, and the public. A series of policies encouraging “Internet + Healthcare” were intensively launched in February and March, indicating that while accelerating the promotion of internet-based medical services, the state has further provided guidance for the future standardized development of the internet healthcare industry:

On February 4, 2020, the National Health Commission issued the “Notice of the General Office of the National Health Commission on Strengthening Information Technology Support for the Prevention and Control of Novel Coronavirus Pneumonia,” encouraging provinces to actively promote online consultations, guidance for home-based medical observation, and internet-based diagnosis and treatment in response to the COVID-19 epidemic.

On February 7, 2020, the National Health Commission issued an additional notice titled “Notice on Providing Internet-Based Medical Consultation Services During Epidemic Prevention and Control,” explicitly requiring provincial-level authorities to coordinate the establishment of internet healthcare service platforms or to promote and implement existing ones. The notice aimed to encourage physicians from various departments to provide online services—including diagnosis and treatment, guidance, health education, and follow-up consultations—specifically for patients with fever.

On February 28, 2020, the National Healthcare Security Administration and the National Health Commission issued the “Guiding Opinions on Promoting ‘Internet+’ Medical Insurance Services During the Prevention and Control of the COVID-19 Pandemic,” requiring that eligible fees for “Internet+” medical services be included in the scope of medical insurance reimbursement.

On March 5, 2020, the Central Committee of the Communist Party of China and the State Council issued the “Opinions on Deepening the Reform of the Medical Security System,” emphasizing the inclusion of eligible medical and pharmaceutical institutions in the scope of managed care agreements under the medical insurance program, and supporting the development of new service models such as “Internet + Healthcare.”

The IQVIA Consumer Health Consulting team continuously monitors the internet healthcare and cross-border e-commerce markets, conducting in-depth analyses of the development and evolution of domestic and international internet healthcare and pharmaceutical e-commerce sectors, thereby accumulating profound understanding and insights. As the positive role played by the “Internet Plus” model during the COVID-19 pandemic gains increasing recognition from all stakeholders, we believe that various innovative models and application scenarios will emerge around clinical drug development and the entire value chain of personal healthcare, empowering the public health and medical care systems as a whole.

As the internet healthcare and pharmaceutical e-commerce sectors undergo a transformative “metamorphosis,” the IQVIA Consumer Health Consulting team has authored a series of white papers on “Internet + Healthcare.” These papers review the historical evolution of internet healthcare and pharmaceutical e-commerce, while offering insights into the future market landscape and the value-creation pathways for various stakeholders. This white paper will be released in two parts, shared sequentially with readers interested in the “Internet + Healthcare” sector.

Abstract

Mr. Tang Zhengye, Head of IQVIA’s Consumer Health Consulting practice, believes that driven by supply-side reforms and the evolving consumer demands for upgraded, personalized, and digital healthcare services in the new era, China’s healthcare industry is entering an entirely new competitive landscape. Notably, the “Internet+”-enabled digital healthcare and pharmaceutical sectors are accelerating their development.

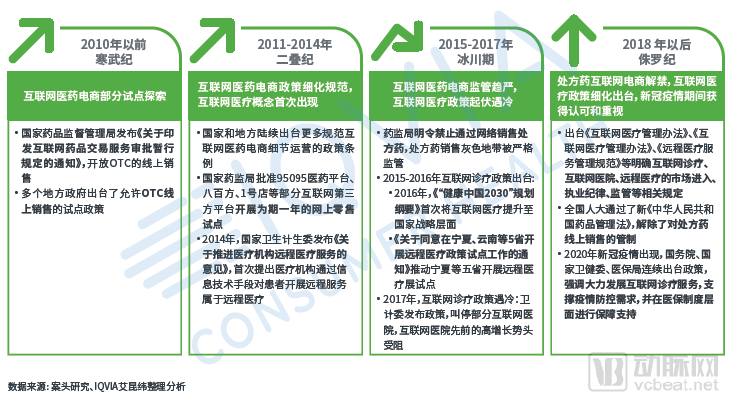

Over the past decade-plus, the evolution of China’s internet healthcare industry can be likened to the centuries-long development of Earth and life. The pre-2010 era was the “Cambrian Period,” marked by pilot programs for online sales of over-the-counter (OTC) medications. From 2011 to 2014, the “Permian Period,” saw the emergence of policy guidelines supporting third-party internet pilot platforms and telemedicine services. The years 2015–2017 constituted an “Ice Age,” during which industry growth stalled due to prohibitions on online prescription drug sales. Starting in 2018, healthcare supply-side reforms were gradually implemented, bringing greater clarity to policy direction. Then, during the COVID-19 pandemic in 2020, stakeholders across the value chain actively expanded online healthcare services at the government’s call, demonstrating to governments, enterprises, consumers, and patients alike the value delivered by the internet healthcare sector. With this validation, China’s internet healthcare industry officially entered its “Jurassic Period”—an era characterized by rapid business model fission and a flourishing diversity of market participants.

Driven by supply-side reforms in healthcare and the empowerment of the “Internet + Healthcare” industry, a healthcare system centered on “health management” is beginning to take shape, with various innovative healthcare value chains and care scenarios quietly emerging. The rise of these innovative healthcare scenarios is inseparable from the strategic positioning along the value chain by players in the internet healthcare sector.

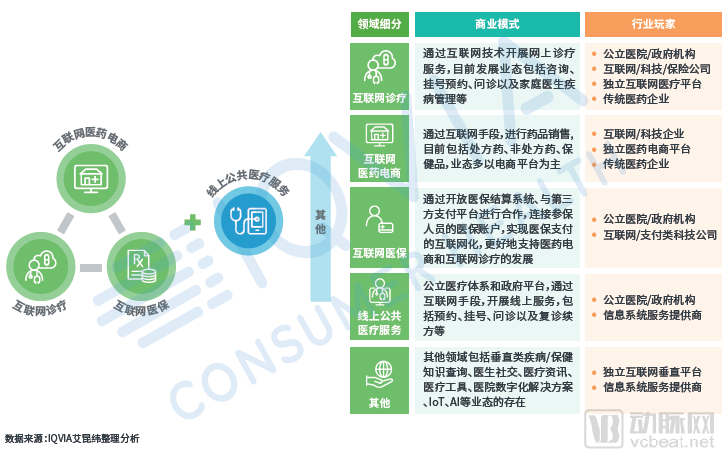

Currently, the primary business models in the internet healthcare industry include online medical consultations, online pharmaceutical e-commerce, online health insurance integration, online public health services, and other categories, along with their respective sub-segments. The five major business model categories and their sub-segments vary in terms of strategies, products, and services across the patient/consumer value chain.

Driven by technological advancements, policy support, and the entry of new market players, the internet healthcare industry will continue to create new value propositions for the broader healthcare sector. It is precisely these value propositions that will continuously refine the innovative health journey empowered by “Internet Plus,” address the various pain points of value chain participants, and enhance the overall efficiency of the healthcare industry.

1. The First Half of the “Internet + Healthcare” Market

1.1 Classification of the “Internet + Healthcare” Industry

The development of China’s internet healthcare industry has evolved to primarily comprise five key subsectors: online medical consultations, e-commerce for pharmaceuticals, internet-based health insurance, online public healthcare services, and others.

● Internet-based Medical Consultation: Providing online medical services through internet technology. Current business models include consultation, appointment scheduling, clinical consultations, and disease management by family doctors.

● Internet Pharmaceutical E-commerce: This sector leverages internet technologies to facilitate the sale of pharmaceuticals, currently encompassing prescription drugs, over-the-counter (OTC) medications, and health supplements. The business model is predominantly based on e-commerce platforms, with key industry players including traditional pharmaceutical companies, internet technology platforms, and online retailers specializing in pharmaceutical e-commerce.

● Internet-based Medical Insurance: By opening up the medical insurance settlement system and collaborating with third-party payment platforms to link insured individuals’ medical insurance accounts, this initiative enables the digitalization of medical insurance payments, thereby better supporting the development of pharmaceutical e-commerce and online healthcare services.

● Online Public Medical Services: Public healthcare systems and government platforms leverage internet technologies to deliver online services, including appointment scheduling, registration, consultations, and follow-up visits with prescription renewals.

● Others: The internet-enabled business models in the healthcare sector are not limited to the four major categories mentioned above; many other types exist, such as disease/health knowledge inquiry, physician social networking, medical news and information, medical tools, hospital digitalization solutions, IoT, and AI.

The “Breaking the Cocoon into a Butterfly” series of white papers will primarily focus on analyzing and discussing the first three types of business models.

1.2 Review of “Internet+” Healthcare Policies

The healthcare industry is vital to the national population’s health and is characterized by stringent regulation. Throughout its digital transformation, policy control has remained a significant constraint on industry development. Since 2000, with advancements in internet technology and the emergence of new business models, a series of policies governing internet-based healthcare and pharmaceutical e-commerce have been introduced, providing direction for the development of internet-enabled and digital healthcare services. However, given its dual nature as both a “medical and health” sector and an “emerging internet technology” field, the policy landscape for internet healthcare has not progressed smoothly.

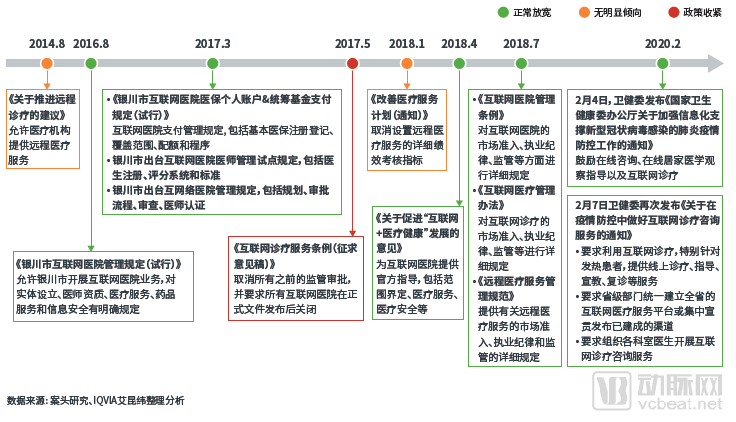

Figure 2. Segmentation of the Internet Healthcare Sector

Figure 3. Review of Internet Healthcare Policies

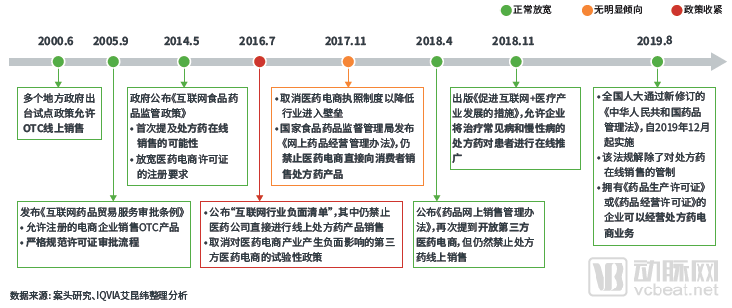

Figure 4. Review of Internet Healthcare Policies

China’s healthcare industry is supervised and regulated by various regulatory authorities through a series of policies, with its development characteristics and operational models all operating within a specific policy framework. A review of these policies reveals that, for a long time, the national policy direction for the “Internet + Healthcare” sector remained unclear. It was not until the gradual implementation of healthcare supply-side reforms, leading up to 2018, that policies became progressively more open and transparent, standardizing, encouraging, and supporting the industry’s development. We categorize the policy orientation into four phases:

● The period before 2010 was the “Cambrian Era.” Just as modern life began to emerge and develop on Earth during the Cambrian period, the internet healthcare sector saw a small number of pilot programs for the online sale of over-the-counter (OTC) medications.

● 2011–2014 was the “Permian Period.” As the final epoch of the Paleozoic Era, the Permian witnessed significant changes in the physical geographical environment, which facilitated major evolutionary developments in the biological world and heralded the advent of a new era in the history of life. During this period, we saw the first emergence of policy opinions regarding third-party internet pilot platforms and telemedicine services.

● 2015–2017 was the “glacial period,” during which the policy prohibiting the online sale of prescription drugs brought industry development to a standstill.

● The period after 2018 is the “Jurassic,” an era of fission when continents began to split apart and profound changes occurred in the history of biological evolution. Dinosaurs became the dominant terrestrial species, while reptiles and mammals began to rapidly diversify. Similarly, in the Internet-plus-healthcare sector, certain enterprises have emerged as industry leaders, and a wide variety of innovative startups have flourished.

Figure 5. Stages of Internet Healthcare Policies

1.3 Development History of the “Internet + Healthcare” Industry

With the advancement of China’s internet technology and digitalization, the “Internet+” industry is flourishing. Before tracing the development history of the “Internet+ Healthcare” sector, let us first review the evolution of its pioneer—the e-commerce industry. We believe that the development path of China’s internet healthcare industry shares certain similarities with that of e-commerce to some extent.

1.3.1 The Development History of Internet Retail

Before 2009: Internet E-commerce 1.0 – Nascent Stage

Since the introduction of internet technology to China in the 1990s, the Chinese internet industry has taken off, with emerging business models such as search engines, social networking, and e-commerce. In 1999, 8848, EachNet, and Alibaba emerged in the form of C2C (Consumer-to-Consumer), beginning to explore business models suitable for China's national conditions.

2009-2011: Internet E-commerce 2.0 – Exploration Phase

In 2009, the emergence of mobile internet further increased internet penetration. During this period, C2C remained the dominant model in the online retail market, which was relatively fragmented and lacked standardization. Most consumers remained cautious and hesitant about online shopping, harboring doubts about the reliability, authenticity, and security of online transactions. At this stage, both imported and domestically produced brands focused primarily on offline channels and had not yet considered moving online. In 2011, Alibaba announced the split of Taobao into three separate companies: Etao (a search engine), Taobao (C2C), and Tmall (B2C). Following this restructuring, Taobao focused on standardizing the C2C market while simultaneously expanding its B2C segment.

2012-2015: Internet E-commerce 3.0 – Demographic Dividend Drives Exponential Growth

Tmall Mall began proactively encouraging major offline brands to establish a presence on its platform. Starting in 2012, in addition to Taobao and Tmall, other e-commerce enterprises such as JD.com, Yihaodian, and Suning rapidly emerged and gained prominence. Some domestic and international brands with forward-looking perspectives began to recognize that online channels could drive incremental growth for their brands, and thus started to expand into online sales channels. Internet e-commerce continued to benefit significantly from the demographic dividend. Comprehensive and vertical e-commerce platforms competed fiercely to acquire and accumulate user traffic, leveraging capital, marketing efforts, product diversity, or precise positioning to continuously capture market share. They also introduced a wider range of product categories and services, thereby increasing user penetration rates and transaction volumes. From 2015 to 2016, internet retail experienced exponential, explosive growth. During this period, although major brands had varying strategic positions regarding online channels, these channels primarily served as “sales outlets,” enabling brands to reach more customers through the convenience and accessibility of online platforms.

Figure 6 China’s Internet+ Healthcare vs. Internet Retail E-commerce

Post-2016: Internet E-commerce 4.0 – Comprehensive Online-Offline Integration in New Retail

As the growth in online transactions driven by the demographic dividend gradually slowed, major e-commerce platforms and brands began to turn their attention to the offline market, leveraging internet-based thinking to capture offline traffic and consumer behavior. In 2016, Jack Ma first introduced the concept of “New Retail” at the Yunqi Conference, subsequently investing in a diverse range of physical retail entities, including department stores, supermarkets, home appliance retailers, and fresh food markets. At this point, internet retail gave rise to an entirely new business model. Evolving from the initial approach of simply moving offline goods online for sale, the industry shifted toward directing online brands, operational strategies, and traffic flows to offline channels. By utilizing digital and intelligent technologies, a consumer-centric ecosystem was constructed to provide shoppers with a seamless omnichannel experience. New Retail has also opened up new opportunities for brands and e-commerce platforms, enabling them to capture data across the entire consumer lifecycle, facilitate more precise consumer profiling, and enhance efficiency in R&D, supply chain management, and marketing.

Compared with the development trajectory of China’s internet e-commerce sector, the growth of internet healthcare exhibits certain similarities; however, its industry development remains influenced by a multitude of factors. These include macro-level healthcare policies and regulatory frameworks specific to internet healthcare, as well as the maturity of other stakeholders in the value chain—such as the supply of medical system resources and the degree of digitalization among traditional medical institutions. Due to the high professional barriers to entry in this sector, its industry maturity and market size at comparable stages tend to be lower. We believe that the development of China’s internet healthcare industry has unfolded over several decades and can be divided into four major phases.

1.3.2 The Development History of Internet + Healthcare

Figure 7 Development Stages of the Internet Healthcare Industry

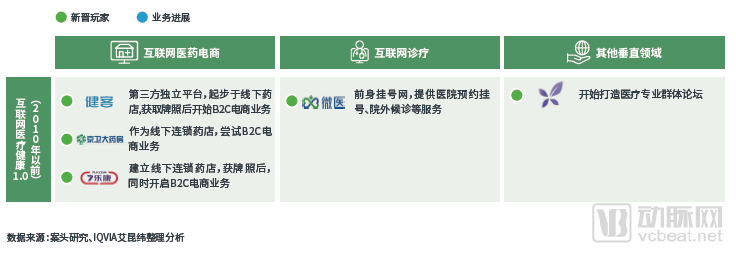

1) China's Internet Healthcare Industry 1.0 (Pre-2010) -Pharmaceutical E-commerce Ventures and Health Information Campaigns Knock on the Door of Digital Transformation in the Healthcare Industry

Prior to 2010, China’s internet industry was still in its nascent stage, and the internet healthcare sector was in its embryonic phase. During this period, the dissemination of medical and pharmaceutical information, as well as popular science education on diseases, constituted the main theme and served as the precursor to numerous pharmaceutical retail and medical service products.

During this phase, a small number of pharmaceutical e-commerce enterprises were established, displaying drug information and usage instructions to patients through online sales. However, this model was immediately halted by national policies shortly after its initial emergence in the 1990s. It was not until 2000 that policies at both the national and certain local levels were introduced to permit the online retail of over-the-counter (OTC) drugs. In September 2005, the State Food and Drug Administration promulgated the Interim Provisions on the Approval of Internet Drug Transaction Services, which clearly defined the scope of transactions, implementing entities, and regulatory standards for internet drug transaction services. These provisions required enterprises engaged in internet drug transactions to obtain corresponding qualification certificates: Certificate A, Certificate B, and Certificate C. (Note: Certificate A applies to third-party platforms conducting B2B operations; Certificate B applies to manufacturers and wholesalers conducting B2B operations; Certificate C applies to pharmaceutical retailers conducting B2C operations.) Meanwhile, retail chain enterprises were permitted to sell OTC drugs directly to consumers.

Driven by the overall development of the internet retail industry and permissive policies for pharmaceutical e-commerce, B2B and B2C pharmaceutical e-commerce began to emerge. In the B2C sector, innovative third-party internet platforms and pharmacy chain enterprises, such as Jianke and Jingwei Pharmacy, started entering the online pharmaceutical retail market, while other traditional players in the healthcare value chain remained minimally involved. Internet-based healthcare and health insurance-related services had not yet appeared. As of 2010, the market size of pharmaceutical e-commerce in China was still less than RMB 400 million.

Figure 8. Layout of Internet Healthcare 1.0 Players (Non-exhaustive)

2) China's Internet Healthcare Industry 2.0 (2011-2014) -Steady Growth of Internet E-commerce: Players Intervene in Medical Processes with Individual Products/Services

Following the liberalization of national and local policies on pharmaceutical e-commerce in 2000, and with the continuous emergence of new players in this sector, national and local authorities successively introduced more policy regulations to standardize operational details. In October 2013, the China Food and Drug Administration (CFDA) stipulated that standalone retail pharmacies were prohibited from engaging in online drug sales, while retail pharmacy chains were only permitted to sell over-the-counter (OTC) drugs online and were required to use self-operated distribution systems compliant with Good Supply Practice (GSP) certification. In May 2014, the CFDA released a draft for public comment that would allow internet platforms with appropriate qualifications to sell prescription drugs online and permit third-party logistics providers to handle the distribution of drugs or medical devices. Although these measures were not subsequently implemented, they were regarded by the industry as a positive signal for the future online sale of prescription drugs.

Meanwhile, the National Medical Products Administration began selecting certain platforms to launch online retail pilots during this phase, approving the 95095 Pharmaceutical Platform, Baibaifang, and Yihaodian in November 2013, July 2014, and July 2014, respectively, to conduct one-year pilot programs for third-party internet platforms.

At that time, traditional internet companies (BAT) and players in the healthcare industry value chain, such as distributors and chain pharmacies, began to enter the pharmaceutical e-commerce sector by obtaining e-commerce licenses through self-establishment or acquisitions. For instance, Alibaba acquired the 95095 pharmaceutical platform in 2014, thereby securing a Class A Internet Drug Transaction Service Qualification Certificate. The industry scale also started to grow rapidly with the entry of various players; by 2014, the B2C market size for online over-the-counter (OTC) pharmaceutical business had reached approximately RMB 2 billion.

Amid the booming development of pharmaceutical e-commerce, many industry players are contemplating how to engage with the new patient care pathways that have emerged as internetization dismantles information barriers. In 2014, the National Health and Family Planning Commission’s “Opinions on Promoting Remote Medical Services in Medical Institutions” formally defined remote healthcare as services provided by medical institutions to patients outside their facilities through information technology. Subsequently, single-service models in internet-based healthcare began to emerge, with internet platforms, technology companies, and health insurers leveraging resources accumulated from their traditional businesses to explore and pilot such standalone service offerings. During this phase, services were primarily concentrated on appointment registration and lightweight online consultations. The reasons for choosing these two services as entry points include:

● Appointment Registration: Prior to the advent of the internet, the healthcare industry already offered “non-offline” channels, such as appointment booking via 114 or hospital telephone lines. Patients have established a certain level of trust in these registration methods. Consequently, this demographic represents the user group most readily convertible to internet-based platforms.

● Light Consultation: On the supply side, since 2009, China has piloted multi-site practice for physicians, which was rolled out nationwide by 2014. At this point, the supply side for light consultation was adequately met. On the demand side, clinical diagnosis and treatment constitute the core component of patients’ healthcare journey. As a refined and customized approach to information gathering, light consultation serves as an effective solution to alleviate the difficulties patients face in accessing offline medical care and consultations.

At this stage, although various forms of internet-based medical service products have emerged, their essence remains focused on addressing the pain points of information asymmetry and low efficiency in information flow. Patient education and paid conversion rates continue to pose significant challenges. Consequently, market participants are primarily leveraging their own resources and targeting specific opportunities to intervene and integrate services. While testing the acceptance of digital services among internet-savvy patients, they are also engaging in continuous trial-and-error and exploration.

As of 2015, there were six internet hospitals in China. However, players offering other medical services—such as appointment registration, light consultations, health information, physician communities, and chronic disease management—began to emerge during this period. Nevertheless, business operations were still in their early stages, and the market size remained relatively small.

Figure 9. Landscape of Players in Internet Healthcare 2.0 (Non-exhaustive)

3) China’s Internet Healthcare Industry 3.0 (2015–2017) –Extend forward and backward to cover core online segments, and explore development models within the framework of policy regulations and compliance.

Following the rapid expansion of pharmaceutical e-commerce from 2010 to 2014, and although policies had not yet liberalized the online sale of prescription drugs, many such medications were sold through e-commerce channels via gray-area mechanisms such as Online-to-Offline (O2O) models. Before appropriate regulatory frameworks and sustainable development models could be established at the macro level, the state tightened restrictions and prohibited these business practices. In July 2016, the China Food and Drug Administration (CFDA) notified Hebei Province, Shanghai, and Guangdong Province to terminate the pilot programs for online retail of pharmaceuticals via third-party internet platforms. Consequently, the three approved platforms—Tmall Pharmacy, Yihaodian, and 800 Fang—were shut down. After halting the retail pilot platforms, the State Council successively abolished the Internet Drug Transaction Service Qualification Certificates (Category B, Category C, and Category A) in January and September 2017, thereby eliminating all approval requirements for enterprises providing internet drug transaction services. In November of the same year, the National Medical Products Administration drafted the “Administrative Measures for the Supervision of Online Pharmaceutical Operations (Draft for Comments),” which explicitly prohibited the online sale of prescription drugs. By 2017, the market size of China’s B2C online over-the-counter (OTC) pharmaceutical business had reached approximately RMB 7 billion.

In the realm of internet-based medical services, a number of favorable policies emerged at the policy level between 2015 and 2016. In 2015, the "Notice on Approving Pilot Programs for Telemedicine Policies in Five Provinces Including Ningxia and Yunnan" promoted pilot initiatives for telemedicine in Ningxia and four other provinces. In 2016, the "Outline of the 'Healthy China 2030' Plan" elevated internet healthcare to the level of national strategy for the first time. In the same year, Yinchuan City took the lead in issuing policy documents such as the "Yinchuan Internet Hospital Management System (Trial)," which played a pivotal role in the development of internet hospitals.

Following the introduction of this policy, more than 20 internet healthcare companies—including third-party platforms such as Haodf, WeDoctor, DXY, Chunyu Doctor, and Medlinker—were invited to participate in the Yinchuan pilot program. They successively established internet hospitals locally, extending their offerings beyond the single-product internet healthcare services characteristic of the previous phase (2.0) to cover the core diagnosis and treatment processes for patients.

However, policy direction shifted again. In 2017, acknowledging that professional medical institutions should remain the primary providers of core medical services, the government began to tighten relevant policies on internet-based healthcare. In April, the National Health and Family Planning Commission (NHFPC) released the “Administrative Measures for Internet Diagnosis and Treatment and Opinions on Promoting the Development of Internet Medical Services (Draft for Comment),” which explicitly prohibited internet hospitals from providing diagnostic and treatment services directly to the general public. Such services were restricted to interactions between tertiary hospitals and their affiliated lower-tier hospitals, and the use of terms such as “Internet Hospital,” “Cloud Hospital,” and “Online Hospital” was suspended. The previously aggressive growth momentum was curbed by this policy contraction. Meanwhile, industry players, while monitoring policy changes, continued to consolidate core user traffic through their existing business models and actively explored compliant innovative approaches. For instance, third-party internet platforms began collaborating with public hospitals across various provinces and municipalities, conducting internet-based diagnosis and treatment activities in reliance on offline hospitals, with the internet platforms primarily serving an informational role. By 2017, the number of internet hospitals nationwide had reached 48.

At this stage, the internet-based and digital development of medical insurance remained primarily focused on government-opened settlement platforms, exploring collaborations with third-party payment providers. However, application scenarios were mainly limited to facilitating payments in traditional healthcare processes. For instance, in 2016, Zhejiang Province partnered with mobile payment institutions to enable the linking of social security cards with mobile payment accounts, allowing individuals to pay their out-of-pocket expenses via mobile payments. At that time, the integration of online consultation and medication purchasing was relatively limited.

Figure 10. Strategic Landscape of Players in Internet Healthcare 3.0 (Non-exhaustive)

4) China's Internet Healthcare Industry 3.5 (2018-2019) -Policy Direction Becomes Increasingly Clear as Various Players Actively Explore New Models

After approximately a decade of development, China shifted from its previous stance of tightening regulations in 2018, with the government intensively issuing a series of policy documents to encourage and standardize internet-based pharmaceuticals and healthcare. In August 2019, the National People’s Congress passed the newly revised Drug Administration Law of the People’s Republic of China, which for the first time proposed lifting restrictions on the online sale of prescription drugs. Enterprises holding a “Drug Production License” or “Drug Operation License” are permitted to engage in e-commerce business for prescription drugs. This marked the first time since 2000 that national policy allowed the online sale of prescription drugs, representing a milestone event for internet pharmaceutical e-commerce. It signifies that China’s internet e-commerce sector can legally penetrate the offline pharmaceutical market, which includes both prescription and over-the-counter drugs and has a total size of RMB 1.4 trillion. According to IQVIA statistics, the scale of China’s B2C internet pharmaceutical market reached RMB 18 billion in 2019.

In September 2018, the National Health Commission (NHC) successively issued the Administrative Measures for Internet-based Diagnosis and Treatment (Trial), the Administrative Measures for Internet Hospitals (Trial), and the Specification for the Management of Telemedicine Services (Trial). These regulations clarified the access requirements, regulatory oversight, and operational standards for internet-based medical activities, stipulating that both the establishment of internet hospitals and the provision of internet-based diagnosis and treatment must rely on offline physical medical institutions. Meanwhile, provincial-level health commissions were required to establish regulatory bodies for internet-based diagnosis and treatment, permitting only follow-up services for common and chronic diseases in the context of internet-based diagnosis and treatment and telemedicine services.

After years of exploration, the relevant regulations have gradually become clearer, providing room for development and confidence to the internet healthcare industry. At this point, leading companies that entered the industry earlier, such as Ping An Good Doctor, JD.com, and Jianke, survived through model and strategic adjustments, as well as capital injections during the previous stage (3.0). With clear strategies in place, these companies began to focus on replicating their proven successful businesses nationwide, laying out the entire industrial chain, seeking more partners, such as collaborating with hospitals, consumer-oriented medical services, and offline medical institutions, building core moats by expanding their territories, constructing ecosystems for doctors, patients, and medical institutions, and increasing user stickiness. Meanwhile, leveraging the accumulated strategy and operational experience from earlier stages, they are realizing more profitable innovative business models.

Driven by favorable policies, more players have caught up, ramping up efforts or restarting internet healthcare business segments that were previously restricted by regulations. As of October 2019, the National Health Commission reported a total of 269 internet hospitals across China.

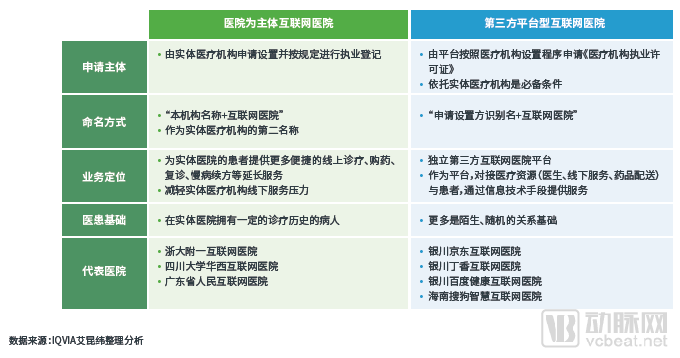

At this stage, internet hospitals have evolved into various models of establishment and market entry, primarily categorized into two major types: hospital-led internet hospitals and third-party platform-based internet hospitals.

Regarding internet-based medical insurance, in August 2019, the National Healthcare Security Administration issued the “Guiding Opinions on Improving Pricing and Medical Insurance Payment Policies for ‘Internet+’ Medical Services,” proposing for the first time that internet-based medical services be included in medical insurance coverage. If designated medical institutions provide medical services identical to those offered offline, such services shall be covered by medical insurance. Other types of internet-based diagnosis and treatment activities, as long as they meet the definition of internet-based diagnosis and treatment, are eligible to apply for inclusion in internet-based medical insurance payment.

Figure 11 Types of Internet Hospitals

Figure 12 Strategic Landscape of Players in Internet Healthcare 3.5 (Non-Exhaustive)

5) China’s Internet Healthcare Industry 4.0 (Post-2020) -Industry leaders continue to expand their ecosystem layouts, while various players across the value chain accelerate their market entry, creating new scenarios and shaping a new industry landscape.

Since 2020, we have believed that China’s internet healthcare industry would enter a phase of rapid development in its 4.0 stage. During this period, leading players will continue to build out their ecosystems, extending vertically or horizontally based on their core competencies. Various stakeholders across the value chain will also accelerate their market entry, with new tools, scenarios, and access points continually emerging to shape a new competitive landscape.

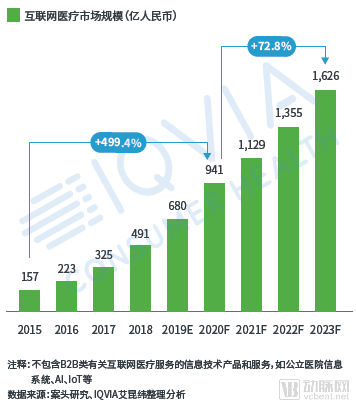

With the lifting of restrictions on online sales of prescription drugs, the penetration rate of pharmaceutical e-commerce is expected to rise further. According to IQVIA’s forecasts, the market size of China’s internet pharmaceutical B2C sector was projected to reach RMB 27.6 billion in 2020 and RMB 42.7 billion in 2023. Driven by the entry of new players, regulatory standardization, and the enabling role of internet-based medical insurance reimbursement, the internet healthcare market will maintain rapid growth. Based on comprehensive data from various sources, we believe that the internet healthcare market in China was poised to surpass RMB 94 billion in 2020.

Figure 13 Forecast of Market Size and Growth Rate of China’s Internet B2C Pharmaceutical E-commerce

Figure 14. Forecast of Market Size and Growth Rate of China's Internet Healthcare Industry

2. Outlook on the Market Landscape of “Internet+” Healthcare

For a long time, China’s healthcare service system has developed with a “treatment-centric” approach and the public healthcare system at its core, prioritizing the treatment of diseases and saving lives—that is, addressing “problems that have already occurred.” However, with socioeconomic development, rising household incomes, and shifts in demographic structure and health status, healthcare needs have evolved. There is now a growing demand for prevention, control, and improvement of overall health quality, placing new requirements on the healthcare service system. Consequently, the core value of China’s healthcare service system urgently needs to transition from problem-solving to prevention and control, shifting from a “treatment-centric” model to a “health management-centric” one.

2.1 Challenges Facing the Supply Side of Medical Resources

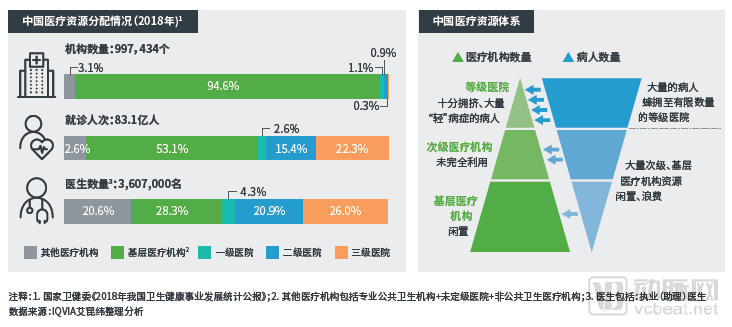

China's healthcare system is facing new challenges, most notably the pressure on medical insurance funds and structural gaps in medical resources.

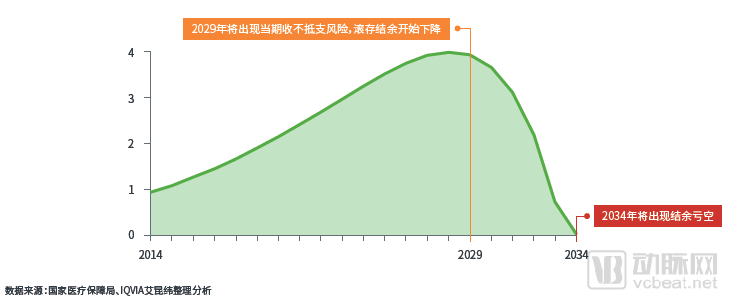

According to IQVIA’s analysis, China’s urban employee basic medical insurance fund is at risk of current expenditures exceeding revenues by 2029 and faces the risk of a deficit by 2034. Meanwhile, the allocation of medical resources suffers from structural gaps. A large number of patients flock to a limited number of tiered hospitals. For example, in 2018, tiered hospitals, which accounted for no more than 4% of all medical institutions nationwide, treated over 40% of patients, whereas primary care institutions, comprising nearly 95% of medical institutions, handled only 53% of outpatient visits.

Figure 15 Year-end cumulative balance of basic medical insurance for urban employees in China (trillion RMB)

Figure 16. China’s Healthcare Resource System and Distribution

2.2 New Changes in the Demand for Medical and Health Services

2.2.1 Population Aging Leads to Increased Frequency of Healthcare Service Demand

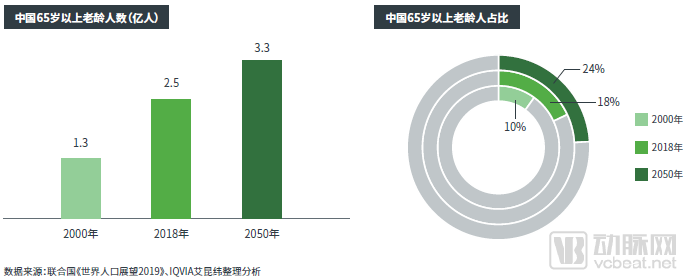

Driven by declining overall mortality and fertility rates, China’s population aging process is accelerating. From 2000 to 2018, the number of people aged 65 and above in China increased from 126 million to 249 million. During the same period, the proportion of the elderly population rose from 10.2% to 17.9%, an increase more than twice the global average for that period. By 2050, the elderly population is projected to reach 329 million, accounting for 23.6% of the total population.

The elderly population faces a higher risk of developing various acute and chronic diseases. Given the growing number of older adults, there is an increasing demand for medical resources and healthcare expenditures. Taking Shanghai’s 2015 resident population statistics as an example, although the elderly accounted for less than 20% of the total population, they represented 60% of all emergency department visits citywide, while outpatient and inpatient costs accounted for 60% and 50% of the total, respectively. Per capita medical expenses among the elderly are relatively higher than those of other age groups, thereby continuously intensifying the burden on the healthcare system.

Figure 17 Changes in China's Aging Population

2.2.2 Aging and Modern Lifestyles Drive Changes in the Disease Spectrum, Leading to Personalized Diagnosis and Treatment Needs

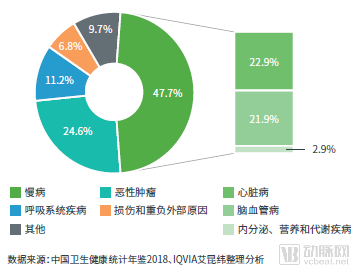

The accelerating pace of population aging, coupled with unhealthy lifestyles, has led to a persistently high prevalence of chronic diseases in China. Various chronic conditions, including obesity, cardiovascular diseases, and gastrointestinal disorders (such as gastritis and enteritis), have become the leading threats to the health of Chinese residents. (See Figure 18)

On the one hand, the prevalence of chronic diseases such as hypertension increases with age. In China, life expectancy has risen from 45 years in 1950 to 76 years in 2016, and the number of elderly patients with chronic conditions is expected to increase significantly in the future. On the other hand, with the accelerating pace of life and mounting modern-day stress, suboptimal lifestyles have become contributing factors to chronic diseases. Unhealthy dietary structures and habits, along with lifestyle stressors—such as smoking and high-salt, high-fat diets—can accelerate atherosclerosis and increase the risk of cardiovascular disease. Meanwhile, factors such as overweight and obesity are closely associated with insulin resistance and are considered key pathogenic mechanisms in type 2 diabetes.

In the treatment of chronic diseases, patients require continuous and routine health management services—such as monitoring of relevant indicators, procurement and delivery of medications for chronic conditions, and scheduling of regular medical consultations—in addition to clinical diagnosis and treatment services. Personalized medication regimens and comprehensive chronic disease management are gradually becoming the mainstream trend.

In the treatment of chronic diseases such as cardiovascular disease and diabetes, drug indications often overlap with various conditions; for instance, many medications can be used simultaneously to treat hypertension, stroke, and acute coronary syndrome. Patients with comorbid high-risk factors, such as hypertension, diabetes, and hyperlipidemia, require personalized pharmacotherapeutic regimens and differentiated management strategies, including lifestyle interventions, biomarker monitoring, and patient education.

Figure 18 Mortality Rates and Composition of Major Diseases among Chinese Residents in 2017

2.2.3 Consumer/Patient Demands for Healthcare in the New Era

1) Digitalization—The digital characteristics of the future primary consumer base are becoming increasingly prominent

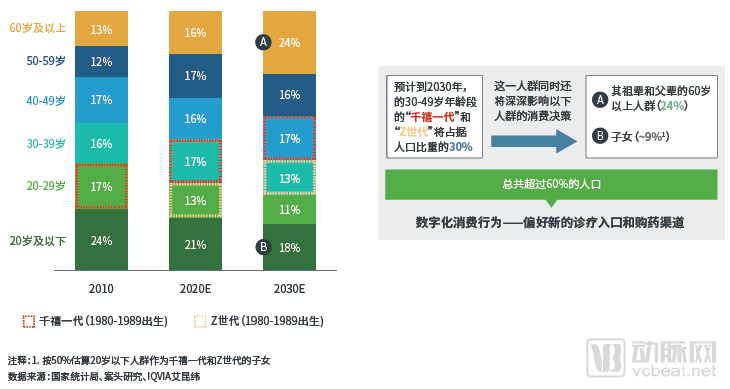

Unlike older patients, the digital DNA of Millennials and internet-native Generation Z has profoundly transformed their healthcare behaviors and pathways. The previously passive, predominantly offline, and physician-directed model of care has been replaced by a proactive approach that leverages high-tech and online tools, fostering bidirectional engagement between patients and providers. Individuals are increasingly utilizing high-tech wearable devices to monitor their health status and social media platforms for information gathering.

By 2030, Millennials and Generation Z (aged 20–40) are projected to account for 30% of the population. This demographic will also profoundly influence the consumption decisions of other age groups: their grandparents/parents (individuals aged over 60, comprising 24% of the total population) and their children (accounting for 9% of the total population). Consequently, approximately 60% of the population is expected to possess a “digital DNA.”

Consumers with a strong digital DNA will increasingly choose online consultation portals and medication purchasing channels in their medical behaviors and pathways.

2) Consumption Upgrading – Driving Demand for Whole-Life-Cycle Health Management in Preventive Care

With rapid economic development, a large number of mid-to-high-end consumer groups have emerged. The rapid growth of the middle class and the shift in their consumption concepts have laid the foundation for consumption upgrading, as traditional and homogeneous products and services can no longer meet the needs of this demographic.

Consumers have raised their expectations and standards for product efficacy and user experience, the quality of medical services, and integrated health management solutions that combine products with services.

Figure 19 Trends and Projections in Population Age Structure

Figure 20 Shifts in Healthcare Service Demand Among the Middle Class

2.3 Internet Plus is Poised to Empower the Healthcare Service Delivery System and Deepen Supply-Side Reform in Healthcare

In November 2015, President Xi Jinping first proposed the concept of “supply-side reform” at a meeting of the Central Financial and Economic Leading Group. He subsequently reiterated this theme on multiple occasions, including at State Council executive meetings, workshops for the formulation of the 13th Five-Year Plan Outline, APEC meetings, and the Central Economic Work Conference. He emphasized the necessity of advancing supply-side structural reform in China’s economic development, identifying public services such as healthcare, education, and transportation as key areas where both the total volume and quality of supply need to be enhanced.

In 2016, the Chinese government issued the “Healthy China 2030” plan and subsequently rolled out a series of policies to implement supply-side reforms in the healthcare system. These efforts aim to comprehensively improve the health status of the Chinese population and achieve coordinated development between public health and socioeconomic progress. Centered on healthcare services, pharmaceuticals, and medical insurance, the reforms advocate an integrated “three-medical” linkage approach. Key measures include optimizing the allocation of medical resources, controlling medical insurance expenditures, and advancing medical insurance reform. These initiatives seek to redistribute medical resources, enhance access to high-quality care, and ultimately achieve the goals of improving the healthcare service system, innovating service delivery models, and elevating the quality and standard of medical services.

However, despite various initiatives under the supply-side reform of healthcare services, the online, personalized, and upgraded demands of consumers in the new era have not been adequately met. During the COVID-19 pandemic, “Internet Plus” demonstrated its capacity to effectively alleviate pressure on medical resource supply and address emerging healthcare service needs in novel scenarios. Against the backdrop of contradictions between the supply and demand of medical resources, as well as shifts in both the traditional healthcare delivery system and public expectations for medical services, we believe that an Internet Plus-enabled, “health management”-centric healthcare system and related Internet Plus industries will inevitably emerge. These developments aim to resolve pain points across value chain segments and enhance overall industry efficiency.

We believe that, empowered by the "Internet Plus" initiative, China's healthcare industry as a whole will undergo three major transformations:

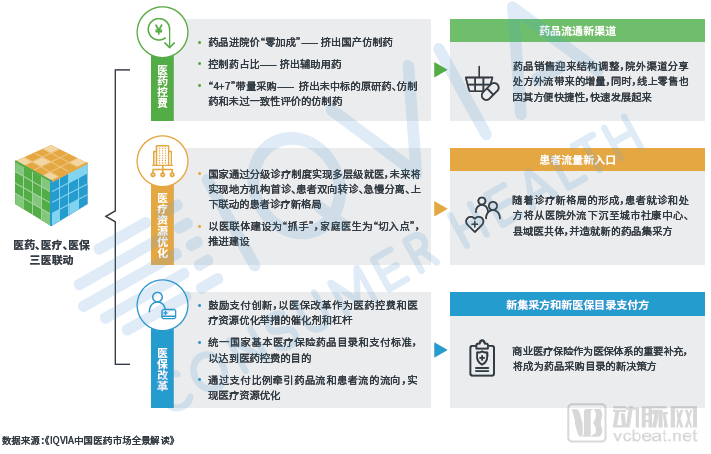

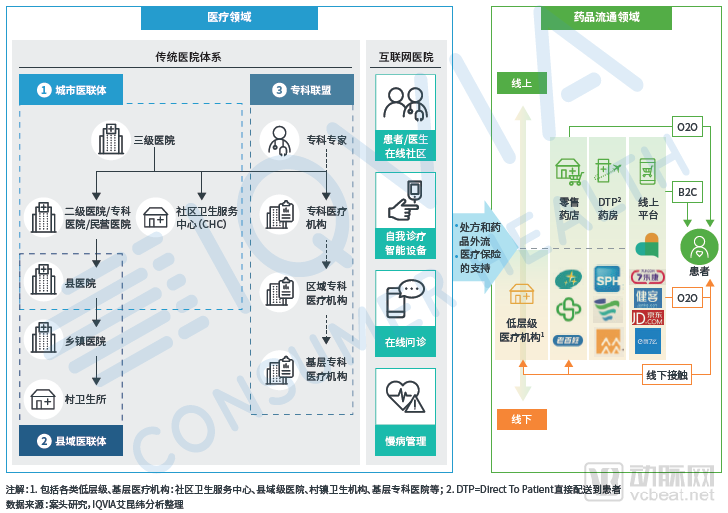

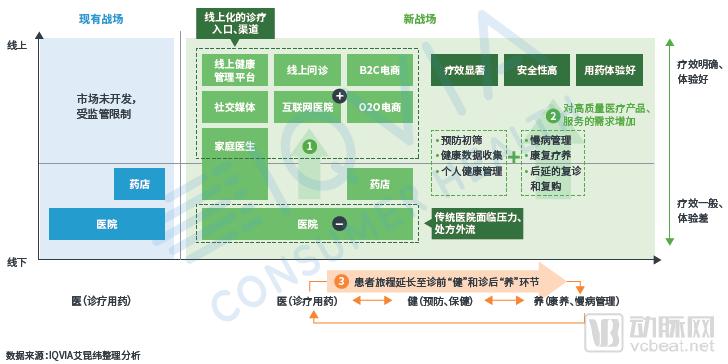

2.3.1 China’s Healthcare Service System Will Form a Two-Tier Market of “Downward Penetration” and “Upward Concentration”

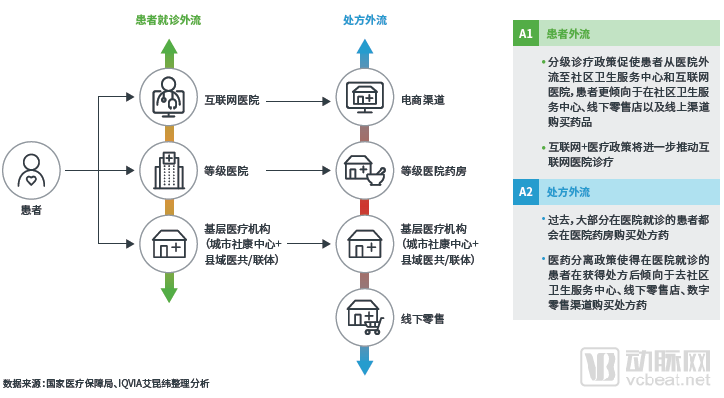

● Basic diagnostic and treatment services are being “decentralized” to community medical institutions through the “tiered diagnosis and treatment” mechanism, with pharmaceuticals also following patient flows from higher-tier medical institutions down to primary care facilities and retail channels.

● The demand for diagnosis and treatment of mild and chronic conditions will be “shifted upward” to new entry points and channels, such as internet healthcare and pharmaceutical e-commerce, to be met.

● A new integrated online-offline healthcare landscape has been established, further enhancing the rational allocation of medical resources in response to patients’ diverse healthcare needs.

Figure 21 The Reform of Tripartite Coordination among Medical Care, Health Insurance, and Pharmaceuticals

Figure 22 Two-Tier Market of the Healthcare Service System

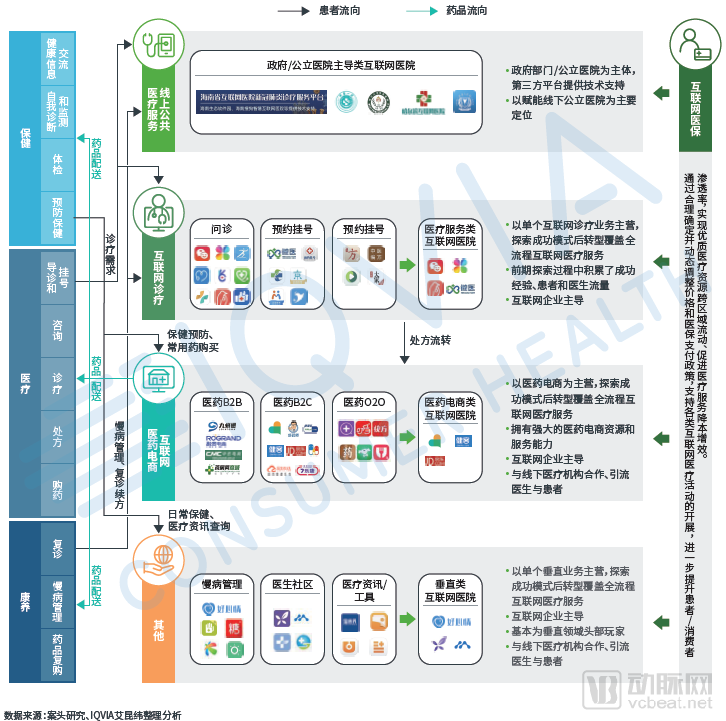

Figure 23 New Scenarios and Channels in the Internet Era

Figure 24 The New Landscape of China’s Healthcare

2.3.2 Patients/Consumers Raise Higher Quality and Standard Requirements for Medical Products and Services

● Higher demands are being placed on drug efficacy, safety, and personalized medication selection.

● Higher expectations for a positive treatment experience and the selection of treatment regimens.

● Higher requirements are proposed for the integrated experience of products and services.

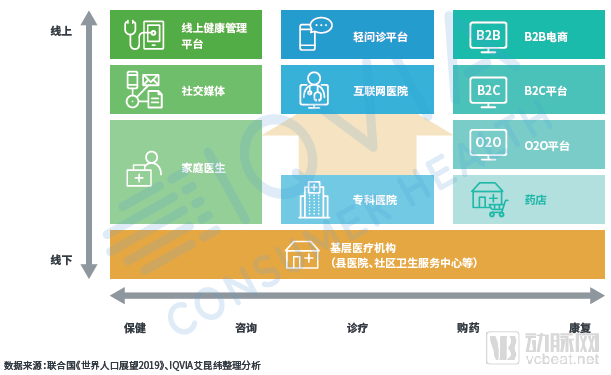

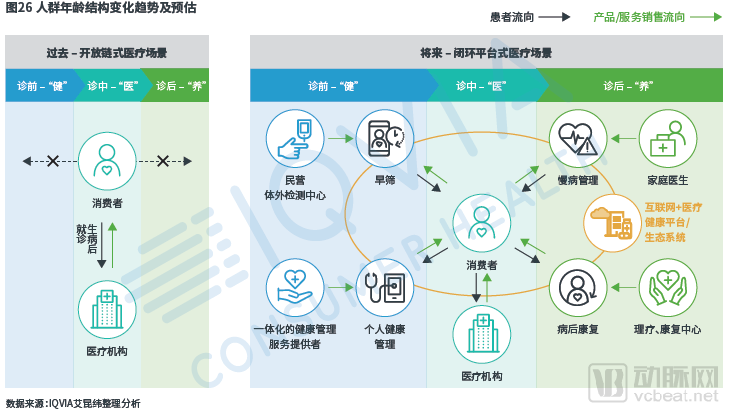

2.3.3 Patient/Consumer-Centric: The Healthcare Journey Extends Beyond Traditional Medical Treatment to Include Pre-Diagnosis “Health” and Post-Diagnosis “Wellness”

Pre-Consultation Healthcare: Growing demand for products and services related to preventive screening, health management, and data collection.

Post-Consultation Wellness: Growing Demand for Professional Chronic Disease Management Services, Rehabilitation and Convalescence, Follow-up Visits, and Repeat Purchases.

Figure 25 Changes in Medical Practice Patterns Driven by Consumption Upgrading

Figure 26 Healthcare Scenarios Enabled by Internet Medical Health

Driven by upgrades on both the supply and demand sides, policy dividends from the “Internet + Healthcare” initiative, and the accelerated entry of diverse market players, China’s healthcare market is entering a new competitive landscape. Empowered by “Internet +,” innovative healthcare value chains and medical scenarios are quietly emerging, with “digitalization,” “demand upgrading,” and “full-lifecycle coverage” becoming its three major themes.

After decades of development, the current “Internet + Healthcare” industry has evolved into major business models and segmented sectors, including online medical consultations, e-commerce for pharmaceuticals, internet-based health insurance, and online public healthcare services. Initially entering the market with “single products/services,” the industry has gradually shifted toward a development trend centered on “consumers/patients” and covering the entire lifecycle of health management, extending vertically or horizontally based on respective core competencies.

Figure 27 The New Frontier in Consumer Health

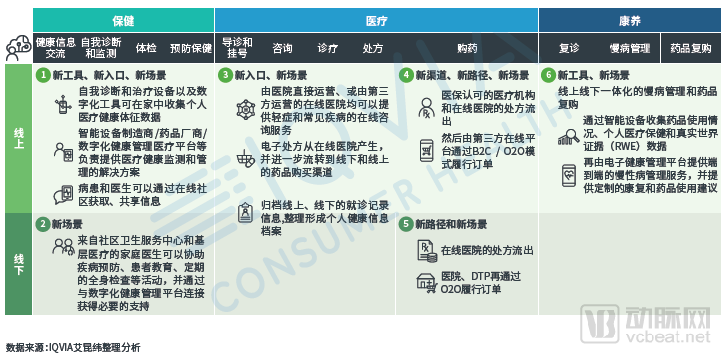

Behind the intricate and interwoven business models, numerous innovative healthcare service scenarios have already emerged, including:

1) Pre-consultation:

● Consumers/patients leverage various medical tools and social media platforms to access information on diseases and health.

● Consumers/patients leverage high-tech, smart medical devices to achieve self-diagnosis and health management by collecting health sign data, monitoring conditions, and analyzing health information.

● O2O Family Doctors Assist in Monitoring Vital Signs

● Online patient social networking

● Health Check-ups for Delayed Medication Needs

2) During Consultation:

● End-to-end online medical consultation (consultation --> triage --> registration --> diagnosis and treatment --> prescription)

● Leverage internet-based pharmaceutical e-commerce platforms and internet hospitals to conduct online consultations, purchase medications, and manage chronic diseases.

● Offline examinations, treatments, and surgeries in O2O open clinical settings

3) Post-consultation:

● Online Follow-up Consultation

● Online Chronic Disease Management

● Online repeat purchases and prescription renewals

● Seeking various end-to-end, full-lifecycle health management solutions centered on the concept of “health management”

Figure 28. Ecological Landscape of the Internet + Healthcare Industry

Figure 29 Internet+ Empowered Innovative Health Journey

We welcome readers to contact the authoring team of this article to share and exchange your insights on the “Internet + Healthcare” market, as well as your thoughts and reflections on this piece. In the upcoming *Breaking the Cocoon into a Butterfly: White Paper on Internet + Healthcare (Part II)*, the IQVIA Consumer Health Consulting team will continue to share observations on the business models, directions of value chain extension, and methods and pathways of value delivery among various players in the “Internet + Healthcare” sector. Stay tuned!

Scan the mini program code in the image to download.PDF Version of the Report

Author

Neil Tang

Head of Consumer Health Advisory Services

IQVIA China Management Consulting Division

neil.tang@iqvia.com

WeChat ID: neil_tzy

Zheng Wenxin and Gu Jianjun, consultants to the Consumer Health Advisory Team, also contributed to this article.

![]()