Rapid Growth of the Orthokeratology Lens Market in China, Projected to Reach RMB 20 Billion, Faces Three Major Challenges

Autek China

Rigid Gas-Permeable Contact Lens Manufacturer

Recently, schools and universities across China have adopted online remote teaching due to the impact of the pandemic. How to protect eyesight amid frequent use of electronic devices has become one of the top concerns for parents lately.

In fact, not only during the pandemic but also with the widespread adoption of electronic devices in recent years, vision protection for children and adolescents has become increasingly challenging. On one hand, it is necessary to improve daily eye-use habits to prevent myopia; on the other hand, scientific correction methods should be employed to slow its progression.

Rigid Gas Permeable Contact Lenses for Orthokeratology (hereinafter referred to as “Orthokeratology Lenses,” commonly known as OK lenses, i.e., Orthokeratology Lenses) are one of the myopia correction devices currently available on the market. They not only correct vision but also help control the progression of myopia. Primarily worn at night, they do not interfere with normal daily activities during the day. As a non-surgical approach, they offer high reversibility and safety, with their primary user base being children and adolescents.

However, despite its numerous advantages, this corrective “miracle device” has a low market penetration rate in China. So, what is the current state of the domestic orthokeratology lens market? What is the future growth potential? This article will provide an overview and analysis from multiple dimensions, including key enterprises, products and technologies, policies and scientific research, as well as issues and challenges.

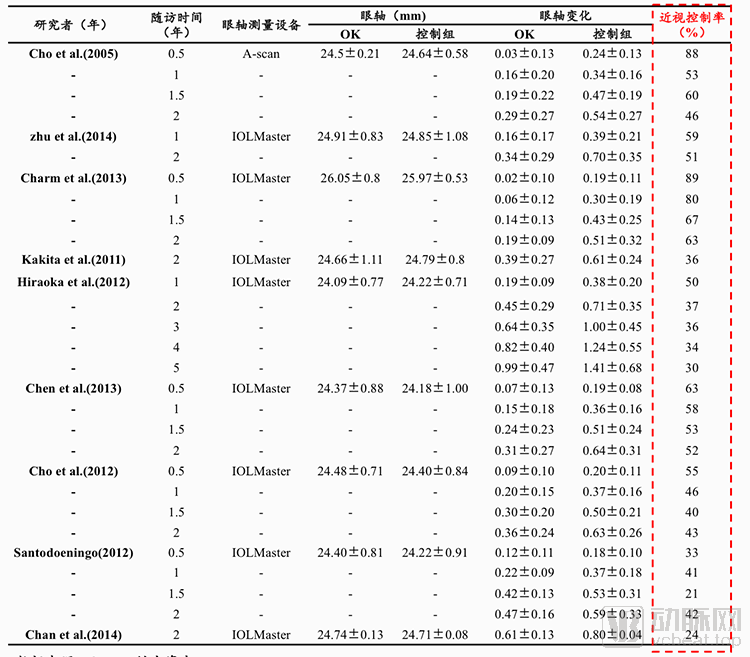

Orthokeratology lenses originated in the United States and have undergone decades of development. According to statistics from Mingfeng Capital, orthokeratology lenses have accumulated extensive clinical trial data to date. Numerous clinical studies both domestically and internationally have demonstrated that orthokeratology lenses can effectively control axial elongation, reducing the rate of myopia progression by 40%–60%. They are currently the most effective optical intervention for slowing myopia progression.

According to clinical data, the average annual increase in myopia for patients wearing conventional spectacle lenses is generally between 100 and 125 degrees, whereas for those wearing orthokeratology lenses, the average annual increase is less than 25 degrees.

Summary of Key Research Data on Orthokeratology Lenses, Sources: CNKI, Mingfeng Capital

As shown by the prominent research data in the figure above, orthokeratology lenses achieve significant myopia control effects within the first six months of wear. Over the subsequent two years, although the control rate declines somewhat, it remains above 30%–40%, with some cases reaching as high as 50%–60%.

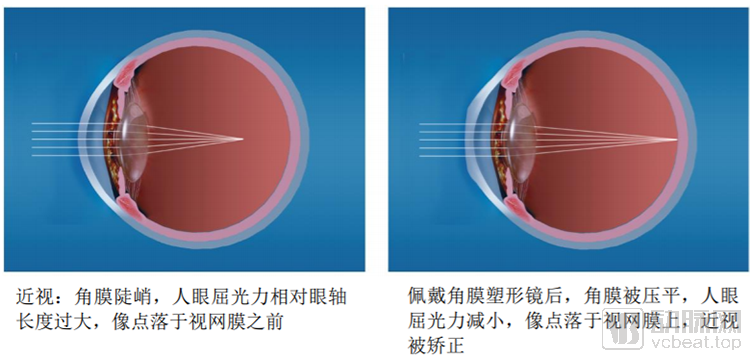

In China, orthokeratology lenses are regulated as Class III medical devices and have been included in the Guidelines for Myopia Prevention and Control issued by the National Health Commission, becoming one of the officially recognized corrective measures. According to the definition in these Guidelines, orthokeratology lenses are reverse-geometry rigid gas permeable contact lenses that flatten the curvature of the central cornea within a certain range through wear, thereby temporarily reducing myopia by a certain amount. They represent a reversible, non-surgical physical reshaping method.

“The Guidelines” also point out that clinical trials have found that long-term wear of orthokeratology lenses can delay the progression of axial length in adolescents by approximately 0.19 mm/year.

Mechanism of Action of Orthokeratology Lenses, Image Source: Autek China Prospectus

Since surgical correction is primarily indicated for myopic patients aged 18 and older with stable refractive error, children and adolescents are largely limited to non-surgical correction methods. A comparison of several non-surgical approaches for myopia correction reveals the following characteristics:

Comparison of Several Non-Surgical Myopia Correction Methods. Data Source: National Health Commission’s “Guidelines for Myopia Prevention and Control” and Other Publicly Available Materials

Orthokeratology lenses are a corrective method with numerous advantages but also requiring significant precautions.

Prior to prescribing orthokeratology lenses, ophthalmologists conduct over ten examinations—including visual acuity testing, keratometry, corneal topography, slit-lamp microscopy, fundus examination, and intraocular pressure measurement—to determine patient suitability. For eligible patients, appropriate trial lenses are selected, and all necessary customization parameters are collected and submitted to the manufacturer. After dispensing, patients must undergo regular follow-up visits and strictly adhere to lens hygiene protocols to prevent infections.

Orthokeratology lenses are primarily used by children and adolescents. Throughout the process of lens adaptation, consistent wear, and maintenance with follow-up visits, parents need to provide ongoing encouragement and supervision.

Furthermore, among the various corrective options, orthokeratology lenses command the highest price in the end-user market, which serves as one of the factors influencing consumer choice. However, as parents’ spending power and willingness to invest in their children’s growth and health have increased in recent years, the impact of this factor is gradually diminishing.

Having undergone four stages of development, it is now used in more than 30 countries and regions.

Orthokeratology lenses are mostly worn at night. Since the corneal tissue is avascular, the oxygen required to maintain its physiological functions is almost entirely supplied by the tear film on the corneal surface. When orthokeratology lenses are worn, oxygen must first permeate through the lens to reach the tear film. Furthermore, during nighttime with eyes closed, the oxygen level available to the tear film is significantly lower than when the eyes are open. Orthokeratology lenses exhibit high oxygen permeability. The material determines this oxygen permeability, which is directly related to the safety of use.

Orthokeratology lenses achieve their reshaping effect due to their specialized design. The design approach determines the range of refractive errors that can be corrected, the efficacy of correction, and wearing comfort, thereby influencing the overall effectiveness of use.

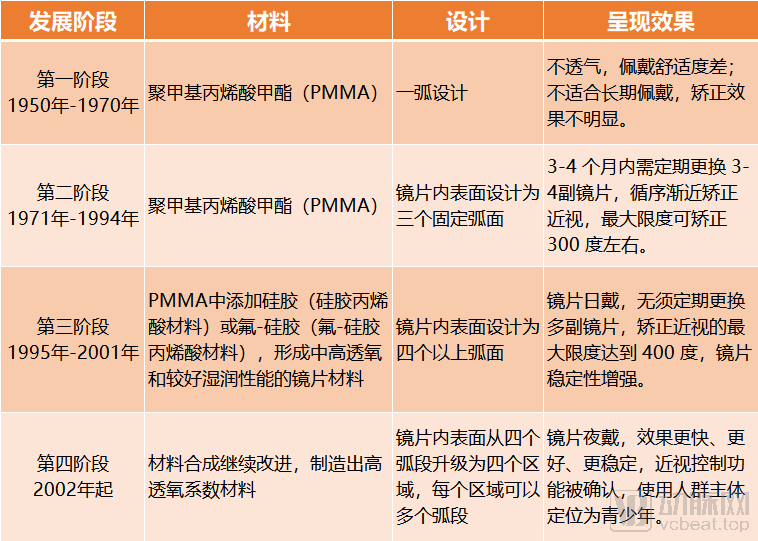

Reviewing the Development History of Orthokeratology Lenses from Two Key Elements: Materials and Design, Comprising Four Stages with Corresponding Four Generations of Product Iterations.

Four Stages of the Development of Orthokeratology Lenses. Source: Public Information; Chart by VCBeat

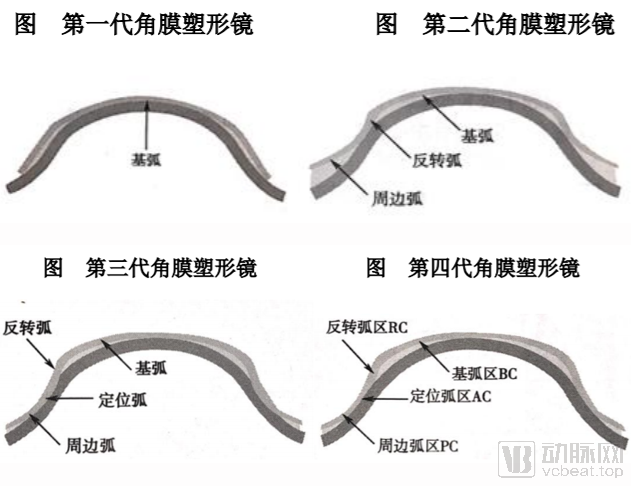

Evolution of Orthokeratology Lens Design, Source: "Fitting Techniques for Orthokeratology Lenses - Basic Level Study Guide"

Orthokeratology emerged and developed alongside the application and promotion of rigid gas-permeable contact lenses in the 1960s. During the early use of poly(methyl methacrylate) (PMMA), the material for contact lenses, many clinical patients observed that rigid contact lenses altered corneal curvature, reduced refractive error, and improved uncorrected visual acuity. The first generation of orthokeratology was initiated based on these clinical observations. At that time, PMMA lenses with a single-curve design were commonly used; however, due to their poor oxygen permeability and inability to be worn for extended periods, the therapeutic effects were not significant.

In 1971, the second generation of orthokeratology lenses emerged. The inner surface of the lens was designed with three fixed arcs. Wearers needed to regularly replace 3-4 pairs of lenses within 3-4 months to gradually correct myopia, with a maximum correction of around 300 degrees. Its feature is the reverse geometry three-arc design, which improved positioning compared to the first-generation products.

Around 1995, the third generation of products emerged, characterized by designing the inner surface of the lens with more than four arcs, including the base curve, reverse curve, alignment curve, and peripheral curve. These lenses utilized materials with moderate to high oxygen permeability and improved wettability, achieving a maximum myopia correction of 4.00 diopters and enhanced lens stability. In 1998, a corneal reshaping lens named Contex was introduced, featuring better breathability, more refined curvature design, and more precise corneal topography mapping technology. At that time, Contex received the first certification for daytime wear of corneal reshaping lenses.

In 2002, the U.S. FDA first approved the clinical use of overnight orthokeratology lenses made from high-oxygen-permeability materials, marking the beginning of the fourth generation of orthokeratology lenses. These lenses are divided into the base curve zone (also known as the central optical zone or treatment zone), the reverse curve zone, the alignment curve zone (also known as the fitting curve zone), and the peripheral curve zone (also known as the peripheral arc zone or edge curve zone). Among these, the alignment curve and reverse curve adopt a multi-arc design.

At this stage, the lenses demonstrated strong stability and comfortable wear, with adolescents becoming the primary user group. Since then, the orthokeratology lens market has been fully activated.

Currently, orthokeratology has gained widespread recognition and adoption. At present, more than 30 countries and regions worldwide are utilizing orthokeratology for myopia correction.

Orthokeratology lenses have a relatively short history of development in China. They were introduced from the United States in 1997, and a nationwide surge in their popularity began in 1998.

Currently, most of the world’s major manufacturers of orthokeratology lenses have established a presence in the Chinese market. U.S.-based E&E Optics Inc. previously sold its products in China but did not renew its registration after the certificate expired in 2013. At present, there are nine companies whose product registration certificates remain valid.

Some companies have a 50-year history, while others are still in their early stages.

Companies Related to Orthokeratology Lenses, Source: Center for Medical Device Evaluation, National Medical Products Administration,Official Websites of Various CompaniesBased on publicly available information; chart by VCBeat

Among the nine companies, Hengtai Optical, Alpha Corporation, Procornea Nederland B.V., and Paragon Vision Sciences were all established in the 1970s, with two of them boasting a 50-year history. Each has evolved from distributing or manufacturing rigid gas permeable contact lenses to independently developing and producing orthokeratology lenses.

Among them, Hengtai Optics initially focused on the manufacturing of contact lenses and acted as an agent for the sales of contact lenses, care solutions, and related products. In 1998, Hengtai Optics established a manufacturing plant for orthokeratology lenses and set up a professional optometry center to promote orthokeratology lenses. In 2013, it launched toric orthokeratology lenses for astigmatism correction.

Alpha Corporation primarily manufactured rigid gas permeable contact lenses in its early years and served as a distributor for major contact lens manufacturers, such as Bausch + Lomb, in the Chubu region of Japan. In 2002, the company began developing orthokeratology lenses and initiated clinical trials in 2005. Its orthokeratology product received approval from the Ministry of Health, Labour and Welfare in 2009 and was subsequently launched on the market, with registration and sales in China commencing in 2011.

Although Euclid Systems Corporation and Lucid Korea, both established in the 1990s, started 20 years later than the aforementioned companies, they have developed very rapidly.

Euclid Systems Corporation’s orthokeratology lenses received FDA approval for production in 2004, and were subsequently approved in South Korea, Russia, Japan, Europe, and other countries and regions in the following years. In 2007, Euclid Systems Corporation’s orthokeratology lenses were approved for entry into the Chinese market. To better expand its market presence, the company established a wholly-owned subsidiary, Euclid Trading (Shanghai) Co., Ltd., as its general agent in China. In 2013, it further established the Euclid Beijing Branch to oversee marketing and sales across the Chinese market.

Currently, Euclid Systems Corporation’s products are distributed across Europe, the United States, and Asia, with ongoing expansion into global markets, establishing it as one of the world’s leading manufacturing bases for orthokeratology lenses.

Lucid Korea initiated a large-scale clinical study project on “Orthokeratology Lenses Suitable for Asians” in 2005, and launched the CH3 design featuring a “large optical zone, ultra-wide reverse curve, ultra-narrow alignment curve, and linked peripheral curve” in 2007. Currently, Lucid Korea’s orthokeratology lenses and RGP lenses hold over 45% of the market share in South Korea, and have been sold in China since 2011.

Autek China and Eyebright Medical are currently the only two companies in mainland China that hold registration certificates for orthokeratology lenses. Autek China, established in 2000, first registered and launched its orthokeratology lenses in 2005. In 2017, Autek China was listed on the ChiNext board.

Since its establishment, Aierbo Nuode has started with the R&D and production of independently innovated intraocular lenses for cataracts, aiming to develop a full range of ophthalmic medical products. In 2019, Aierbo Nuode’s self-developed Proview orthokeratology lens was approved for market launch, and in the same year, the company submitted an IPO application to the STAR Market.

Based on the establishment date, as well as the research and development and market launch of orthokeratology lenses, AutekKangshiAierbo Nuode is still in its early stages. However, both companies have established extensive product portfolios and possess their respective competitive advantages.

In addition to orthokeratology lenses, Autek China’s core products include rigid gas permeable contact lenses and care products, covering the entire lifecycle of orthokeratology lens use.

Although Aierbode was founded most recently and launched its orthokeratology lenses later than its peers, it has rapidly established a product portfolio covering two major sectors—ophthalmic surgery and optometry—within just ten years.

Surgical products include various intraocular lenses (IOLs), capsular tension rings, IOL implantation systems, ophthalmic viscosurgical devices (OVDs), various ophthalmic microsurgical instruments, and ophthalmic surgical knives. Optometric products, in addition to orthokeratology lenses, also include rigid gas permeable contact lenses and tear fluid test strips. The diverse product portfolio leverages commonalities in materials, optical design, and manufacturing processes, enabling shared sales channels to increase revenue and reduce overall costs.

Centralized Raw Material Supply, with Design and Manufacturing Processes Reflecting Product Differentiation

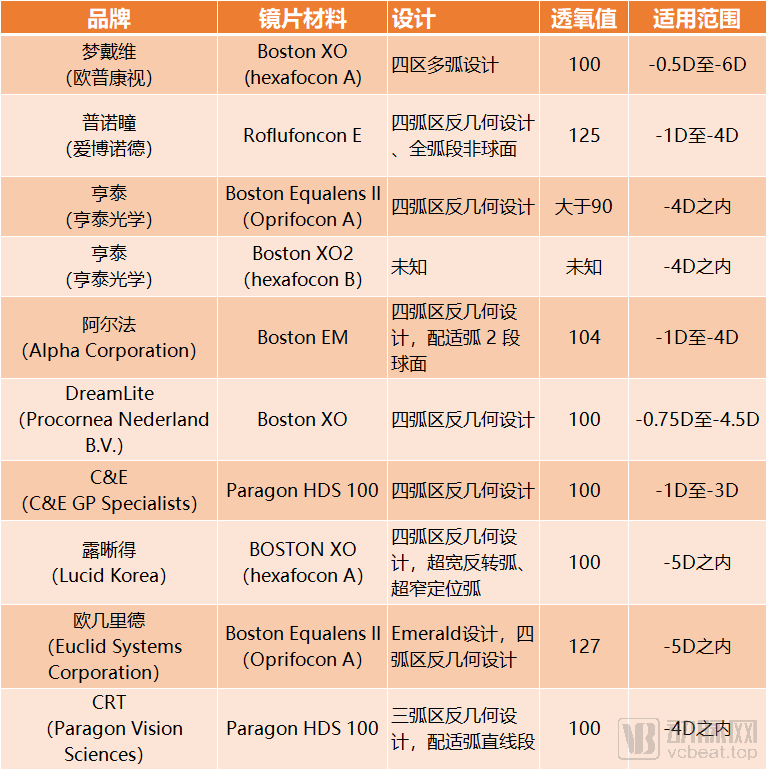

As previously mentioned, material and design are the most critical factors for orthokeratology lenses. What are the main differences among domestic orthokeratology lens products in these two aspects? We have compiled the key parameters of 10 products from 9 companies:

Key Technical Parameters of Domestic Orthokeratology Lens Products, Source: Publicly Available Data

In the figure above, the materials of the 10 products are mainly from the Boston series, Paragon HDS 100, and Roflufilcon E. These three materials originate from Bausch & Lomb (USA), Contamac (UK), and Paragon (USA), respectively. If the same material from the same manufacturer is used, the differences in oxygen permeability coefficients are not significant.

This indicates that the material supply for both domestically produced and imported orthokeratology lenses is relatively concentrated, highlighting significant room for growth in the research, development, and manufacturing of raw materials by domestic enterprises.

Orthokeratology Lens Industry Landscape, Chart by VCBeat

In recent years, domestic enterprises have gradually expanded their layouts into the materials sector. According to the STAR Market application materials submitted by Aierbode to the Shanghai Stock Exchange, the company previously sourced most of its orthokeratology lens materials from Contamac. However, it initiated in-house material research and development in 2017, conducting comparative tests with externally purchased materials that met consistency evaluation standards. Currently, the company has obtained approval from drug regulatory authorities to use self-developed raw materials for the production of orthokeratology lenses.

In addition, Haohai Biological Technology, which focuses on the research and development, production, and sales of medical biomaterials, acquired Contamac in 2017, planning to enter the research, development, and manufacturing of orthokeratology lenses by starting with upstream raw materials. Contamac’s optometric materials are sold to nearly 70 countries and regions worldwide, making it one of the largest independent producers of optometric materials globally. In 2019, Contamac’s independently developed next-generation high-oxygen-permeable contact lens material, Optimum Infinite, received approval from the U.S. FDA for market launch. With an oxygen permeability exceeding 180, it is currently one of the optometric materials with the highest oxygen permeability worldwide.

In terms of design, nearly all products have adopted the fourth-generation reverse geometry design with four arc zones. Different brands vary in their detailed handling of each arc zone to achieve varying degrees of alignment with corneal topography, which ultimately determines the range of corrective power and the wearing experience.

The base curve zone of the Procornea (a product of Aibonode) contact lenses adopts an aspheric design consistent with the corneal surface expression formula, achieving a better match with corneal topography, improving lens positioning accuracy, and ensuring a comfortable wearing experience. The reverse curve features a non-concentric design to guarantee tear reservoir space and provide stable reshaping effects. The alignment zone also employs an aspheric design, developed based on large-sample survey data of Chinese eyes, thereby accommodating a broader population and reducing the complexity of lens selection during fitting. The company has filed a series of core patents to protect its specialized designs.

The alignment arc zone of Alpha (a product of Alpha Corporation) is divided into two segments, primarily to achieve better centration of the lens. In addition, the special design of DreamVision (a product of Autek China) enables it to correct myopia of up to 6.00 diopters.

In addition to materials and design, manufacturing processes are also a critical factor influencing the efficacy of orthokeratology lenses. Euclid (a product of Euclid Systems Corporation) employs microcomputer-controlled aerodynamic magnetic levigation lathes for cutting and fabrication. This approach minimizes electrical resonance interference in the lathe, enhances machining precision, improves lens surface smoothness, and eliminates the need for polishing, thereby yielding better corrective outcomes and wearing comfort.

The market is growing rapidly, with an expected value of over RMB 20 billion in 2023.

Currently, China’s orthokeratology lens industry is in its early stages of development, characterized by low market penetration but rapid growth.

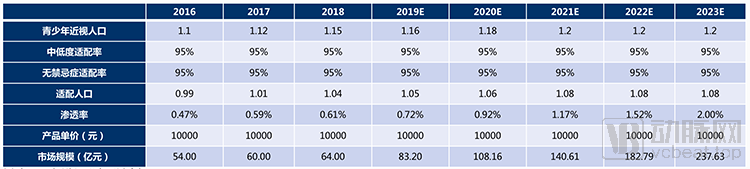

According to data from the Ophthalmology and Optometry Branch of the China Association of Medical Device Industry, the usage volume of orthokeratology lenses in China reached 640,000 pairs in 2018, with an industry penetration rate of only about 1%. Among the school-age adolescent population in China, the penetration rate was merely 0.61%. In contrast, developed countries and regions, particularly East Asia—which shares similar physiological structures with China—have average penetration rates exceeding 5%, showing a rapid upward trend.

According to estimates by Mingfeng Capital, the penetration rate of orthokeratology lenses in China is expected to reach approximately 2% by 2023, with a compound annual growth rate (CAGR) of 30%. Taking into account the uneven development between urban and rural areas in China, the industry penetration rate in first- and second-tier cities with higher consumption levels is projected to reach 5%–10%. Overall, the domestic terminal market size for orthokeratology lenses is expected to reach RMB 23.7 billion by 2023.

Market Size Estimation of Orthokeratology Lenses in China, Source: China Medical Device Industry Association, Mingfeng Capital

Meanwhile, publicly available corporate data also reveals the growth trend of the orthokeratology lens market in recent years.

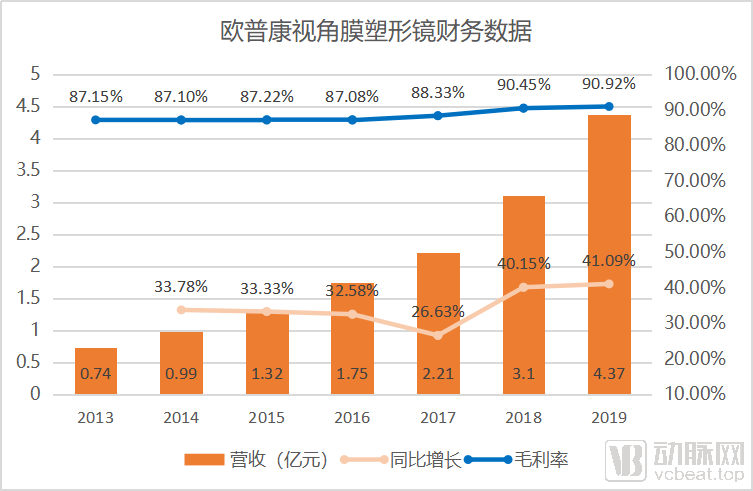

Data source: Autek China’s prospectus and annual reports; chart by VCBeat.

Autek China’s annual revenue from orthokeratology lenses grew from RMB 74 million in 2013 to RMB 437 million in 2019, maintaining an annual growth rate of approximately 30%–40%.

Its gross profit margin has also maintained year-on-year growth, reaching nearly 91% in 2019. This indicates that, over time, the expansion of sales channels for orthokeratology lenses and the increase in lens sales volume have led to economies of scale, thereby reducing the per-unit cost and driving the growth in gross profit margin.

Furthermore, since the launch of Aibonode’s orthokeratology lenses in April 2019, the sales volume and revenue of custom-made lenses (i.e., lenses sold to end users) have steadily increased. The company is currently accelerating its efforts to expand market channels.

Orthokeratology lenses are predominantly marketed through a B2B2C sales model. Although nine companies, including multinational corporations in the field of optometry, are currently competing in the Chinese market, the industry as a whole remains in a phase of collective market expansion rather than mere competition for existing market share. As latecomers, domestic enterprises can still leverage their respective advantages to expand their market presence.

In the initial years following the introduction of orthokeratology lenses into the Chinese market in 1997, the industry witnessed various irregular practices. These included exaggerated claims regarding efficacy, fitting institutions lacking standardized protocols and qualified professionals, inadequate timely follow-up examinations and after-sales services, and even the presence of counterfeit and substandard products in the market. Such issues led to corneal infections among wearers, adversely impacting the entire industry.

These issues have drawn the attention of relevant authorities, leading to strict regulatory oversight of orthokeratology lenses since 2001. The National Medical Products Administration and the former Ministry of Health have successively issued administrative measures, clarifying management requirements across all stages—from manufacturing and distribution to fitting institutions and regulatory bodies.

According to regulations, hospitals authorized to fit orthokeratology lenses must be medical institutions at Level II or above. Ophthalmologists must hold an intermediate or higher professional title and have successfully completed relevant knowledge training organized by provincial health administrative departments or professional academic societies entrusted by such departments, passing the required assessments.

Opticians must hold a professional title at the intermediate level or above, participate in the aforementioned training, and pass the assessment. Furthermore, opticians must perform the fitting of orthokeratology lenses in collaboration with ophthalmologists.

Since then, the industry has entered a stage of standardized development and has ushered in a new round of opportunities amid the intensive rollout of national policies and measures for the prevention and control of myopia among adolescents in recent years.

Policies on Orthokeratology Lenses. Data sources: official websites of the National Health Commission, the National Medical Products Administration, the Ministry of Education, and other relevant departments. Graphic by VCBeat.

In June 2018, the National Health Commission issued the Guidelines for the Prevention and Control of Myopia, officially including orthokeratology lenses as a myopia correction measure. This signifies that orthokeratology lenses have received full official recognition.

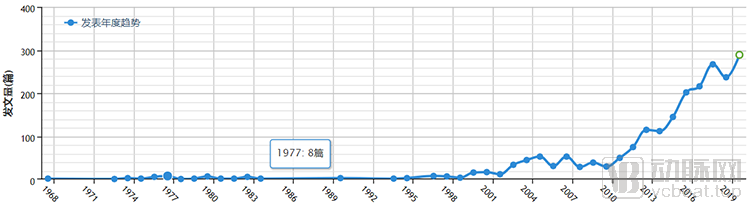

As an emerging technology, continuous research serves as a critical foundation for industrial development. A keyword search for “orthokeratology lenses” on CNKI yields nearly 2,000 relevant papers. The majority of these publications appeared after 2010, with a rapid year-on-year increase; since 2016, the annual number of publications has consistently exceeded 200. This trend aligns with the standardized development trajectory of China’s orthokeratology lens industry.

Annual Number of Published Papers on Orthokeratology Lenses. Data Source: CNKI

The authors of this paper are primarily ophthalmologists from various regions across China, with participation from industry enterprises. The study focuses on monitoring relevant physiological indicators in adolescents following orthokeratology lens wear, aiming to continuously track the safety and efficacy of orthokeratology lenses and identify areas for improvement.

The growing body of research has created favorable conditions for industry development. On one hand, it promotes the advancement and maturation of product technologies; on the other, safety and efficacy are the primary concerns of users, and scientific data, when translated into accessible popular science knowledge, provides valuable reference information for them.

In summary, given the current landscape, orthokeratology lenses have a promising market outlook. With the advancement of the information age, visual strain has reached unprecedented levels, significantly increasing the incidence of refractive errors. Consequently, the demand for vision correction of refractive errors is growing rapidly, with end-user demographics trending toward younger ages and greater personalization.

Meanwhile, with the continuous accumulation of clinical fitting and service experience in recent years and the strengthening of national regulatory oversight, companies in the industry will inevitably become more specialized and standardized, ultimately driving the orthokeratology lens sector toward greater safety and efficacy. However, it is also important to recognize that the industry still faces numerous challenges.

First, a shortage of qualified fitting professionals has limited the market penetration of orthokeratology lenses at the consumer end.Wang Zhen, a partner at Mingfeng Capital, noted that few universities currently offer optometry programs, resulting in a tight talent supply, while existing curricula place heavy emphasis on specialized education. Therefore, he recommended increasing the number of universities offering optometry majors and appropriately incorporating practical courses such as operations and marketing into the optometry curriculum.

In the realm of degree-based education for talent development, Aier Eye Hospital Group jointly established the Aier School of Ophthalmology at Central South University in 2013, dedicated to training master’s and doctoral students. As a downstream enterprise in the ophthalmology sector, Aier Eye Hospital enables close integration of scientific research, teaching, and clinical practice. Competent orthokeratology lens manufacturers may also consider participating in such talent development initiatives.

In the field of vocational education, enterprises and investment institutions have also made strategic moves. For example, Mingfeng Capital invested in Zhongke Xingmei Hospital Investment Co., Ltd. and signed a cooperation agreement with the School of Continuing Education of Peking Union Medical College to conduct vocational training in fields such as plastic surgery and ophthalmology in Chengdu.

Aierbode is also a portfolio company of Mingfeng Capital. Mingfeng Capital’s strategic investments in upstream talent development can further empower Aierbode’s growth.

Secondly, user education remains a long and arduous task.As previously mentioned, orthokeratology lenses underwent a period of unregulated development in China, and their adverse effects have not yet been fully eliminated. Numerous rumors persist online claiming that wearing orthokeratology lenses is harmful to the eyes. Even when educational content about orthokeratology is available, it often lacks authoritative professional sources, making it difficult to gain users’ full trust.

User education is a long-term process that involves multiple stakeholders across the industry chain, including upstream raw material manufacturing, midstream product research and development and manufacturing, and downstream fitting and sales. Science popularization content should not only highlight authoritative sources but also deeply penetrate the daily life scenarios of target audiences through more accessible formats aligned with current communication trends, such as short videos and live streaming.

Finally, the industrial ecosystem needs to be further improved.Although Aibonode has achieved the capability to independently synthesize raw materials for orthokeratology lenses, and Haohai Biological Technology has also entered the raw material R&D and manufacturing sector through acquisitions, domestic companies have not yet extended deeply enough into the upstream supply chain. Raw materials are a critical factor determining the oxygen permeability coefficient, a key product indicator. If China’s industrial chain can achieve further breakthroughs in the R&D and manufacturing of raw materials, the market will see significantly greater growth potential.

References: Prospectuses of Autek China and Eyebright Medical, as well as their annual financial reports;

We also extend our gratitude to Mingfeng Capital for its support with industry data in this article.