U.S. Telehealth Payment Reforms Accelerate Amid Surge in Online Visits as COVID-19 Cases Nearing 800,000

In early April 2020, leading U.S. telehealth providers such as Teladoc and AmWell unprecedentedly took the initiative to publicly disclose their telehealth service utilization data.

Teladoc released data for the second week of March this year: daily access requests reached 15,000, representing a more than 50% increase in traffic compared to the previous week; AmWell compared data from the same period, showing a 250% month-on-month increase in overall visits, with telehealth visits surging by as much as 600% in New York State, the epicenter of the pandemic.

Although the U.S. telemedicine industry has developed relatively mature business models, its overall growth has remained lukewarm. Lacking the massive demand for medical resource allocation seen in China, and without sufficient incentives for insurance companies to drive adoption, telemedicine has faced significant headwinds. Additionally, widely varying policies across different states have restricted physicians’ scope of practice. In short, the advancement of telemedicine in the United States has not been the rapid surge many envisioned; rather, it has remained marginalized outside the mainstream.

Until the outbreak of COVID-19.

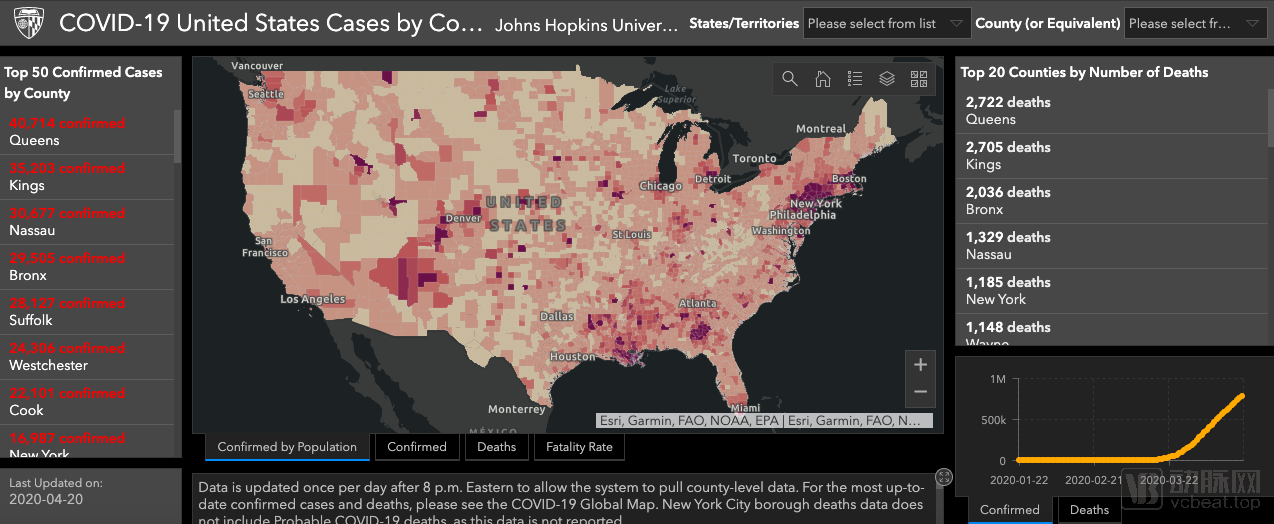

As of 18:00 on April 21, 2020, the cumulative number of confirmed COVID-19 cases in the United States had risen to 787,960. On the East Coast, the number of confirmed cases in New York, Miami, and their surrounding cities exceeded 250,000. The situation on the West Coast was somewhat better, but the total number of confirmed cases in Los Angeles and its surrounding cities still surpassed 50,000.

Geographic Distribution of the U.S. Epidemic Through the Hopkins Epidemic Map

Prior to the COVID-19 pandemic, the varying stringency of state-level laws and regulations governing telemedicine resulted in inconsistencies across states in terms of the categories, quality, and accessibility of services available to patients. Telemedicine providers were required to tailor their offerings to comply with disparate state legal frameworks, which imposed significant constraints on the widespread adoption and standardization of telemedicine.

The U.S. government has clearly recognized this situation as well. Since March, the Center for Connected Health Policy (CCHP) has issued documents on telehealth licensure waivers and telehealth service coverage under COVID-19, keeping them updated in real time in an effort to reduce contact between patients and providers and to widely adopt telehealth as a substitute.

Under the guidance of official documents, various regions rapidly exempted or relaxed telemedicine-related regulations based on their local circumstances. However, this has not seemed to clarify the legal and regulatory framework for telemedicine.

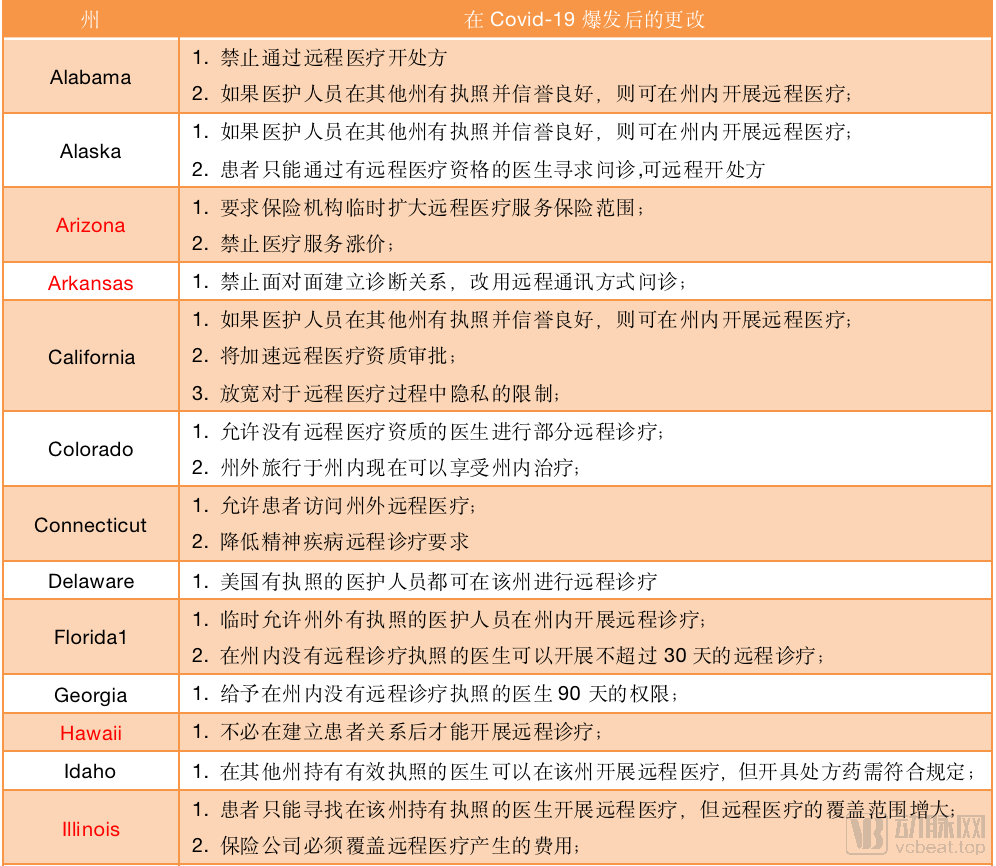

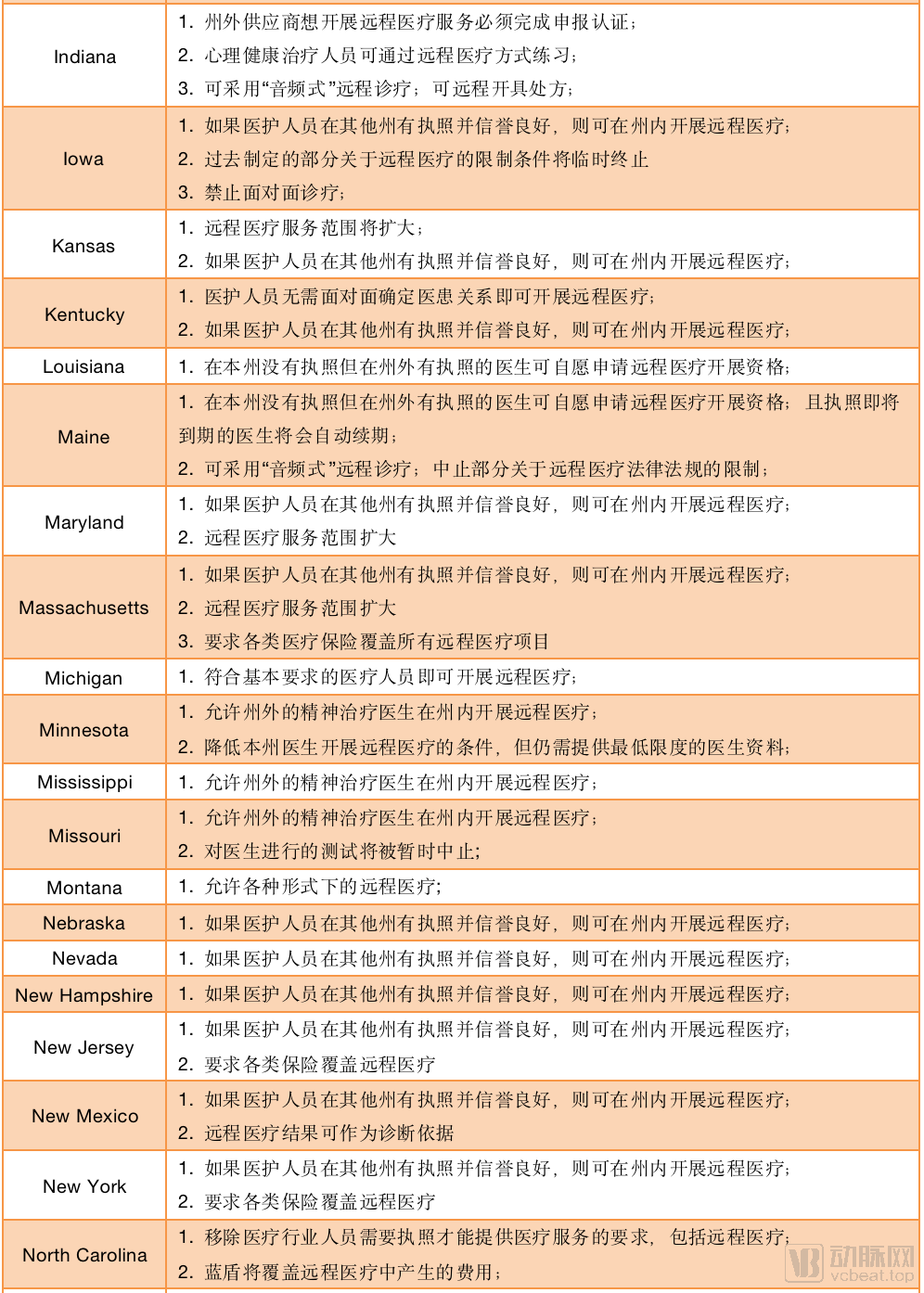

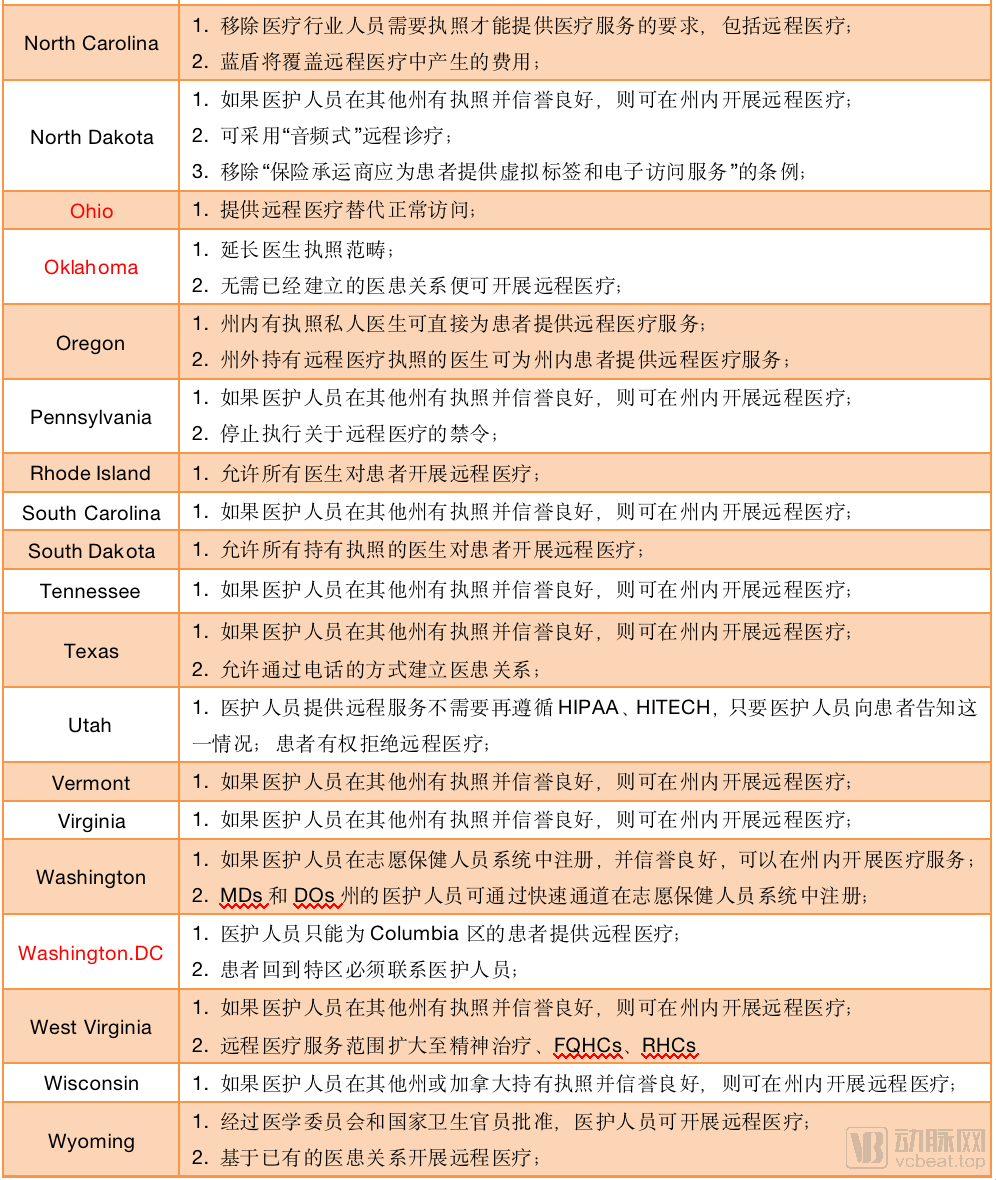

Policy Changes in Telemedicine Across the 50 U.S. States and the District of Columbia During the Pandemic; States Marked in Red Did Not Achieve Policy Breakthroughs

Based on the policy changes in the aforementioned 51 regions, it is evident that 44 of them heeded official recommendations and implemented policy exemptions related to telemedicine; however, seven regions have yet to relax restrictions on telemedicine services. These policy adjustments are closely correlated with the severity of COVID-19 infections in each state.

Among these exemption policies, the most significant and widespread measure was the temporary lifting of restrictions on the scope of telemedicine services provided by healthcare professionals. This meant that New York State, which was hit hardest by the pandemic, could accept telemedicine services from across China, thereby avoiding a scramble for the state’s existing resources.

Most states have announced the elimination of “face-to-face consultations” between patients and healthcare providers, with the exception of patients with special medical needs, such as those requiring hemodialysis or suffering from end-stage renal disease. For these patients, policies still mandate monthly “face-to-face consultations” with healthcare providers to ensure the safety of patients with other conditions during the COVID-19 pandemic.

Some states have also adopted indirect measures to promote telemedicine, such as automatically extending expiring medical licenses to enable physicians to provide telemedicine services under legal protection, establishing expedited channels for license applications, and permitting audio-only consultations to improve the efficiency of telemedicine.

Insurance is a critical component of the U.S. healthcare system. Official documents explicitly require insurers to expand coverage for telemedicine services and provide corresponding guidelines. However, a review of policy summaries reveals that only six states have codified these coverage adjustments into law, with varying scopes of coverage across states. Nevertheless, for patients with COVID-19, there is a program that waives treatment costs upon enrollment in Medicare, which supersedes the benefits previously available to patients enrolled in Medicare or Medicaid.

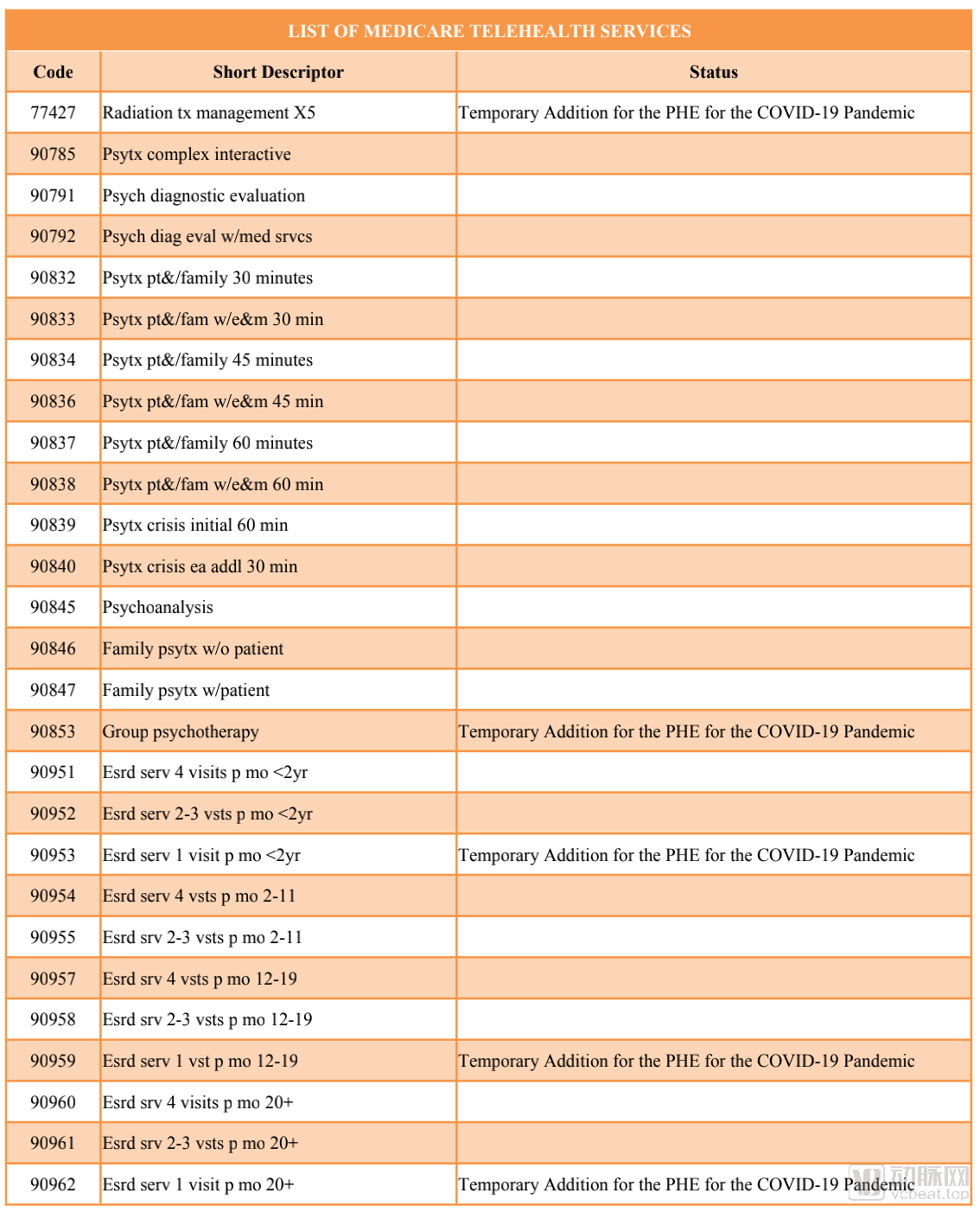

Items Covered by Insurance (Partial), Totaling 191 Entries, with 85 Temporarily Added

This document assigns a unique code to each disease based on age and frequency of medical visits, aligning with the corresponding insurance reimbursement policies. In this revision, items such as Group Psychotherapy have been included, and new frequency coverage has been added for diseases such as end-stage renal disease.

Overall, most regions in the United States remain positive about the promotion of telemedicine services and have significantly relaxed relevant regulations, yet the policy issues facing telemedicine remain unresolved.

“In the absence of unified telemedicine laws and regulations to serve as a definitive regulatory framework, these fragmented jurisdictions have woven an intricate web of policies. CNBC has described the current conduct of telemedicine service providers as ‘an attempt to figure out what they are allowed to do.’”

This is merely a matter of state regulations; the situation could become even more complex when insurance is taken into account—patients are uncertain about which medical expenses will be covered by the federal government and when commercial insurers will include certain services in their reimbursement coverage, resulting in severe information asymmetry.

For example, in a statement released by American Well, the company indicated that it has partnered with numerous insurers, with varying coverage under each partnership. However, it is important to note that its insurance coverage excludes certain plans, such as Academic Health Plan, iCare, APWU, and Blue Shield of Kansas, Massachusetts, Michigan, North Dakota, Nebraska, Rhode Island, and Vermont, among others.

However, none of these factors can curb the public’s rigid demand for telemedicine during the pandemic.

In brief, the role of telemedicine during the COVID-19 pandemic can be summarized into four aspects, which is very similar to but slightly different from the role played by internet-based healthcare in China during the epidemic.

Screen patients via telemedicine and provide status updates to mildly ill patients isolating at home

In the early stages of the COVID-19 outbreak, the U.S. public did not adopt strict quarantine measures for prevention, meaning that individuals could still seek in-person consultations with physicians during the pandemic. However, for patients who were infected with the virus and unable to visit hospitals, or those with mild symptoms who were reluctant to seek hospital-based treatment, telemedicine served as a critical means to ensure the safety of both healthcare providers and patients while facilitating timely communication of patients’ health status. Furthermore, if individuals suspected they might be infected with the novel coronavirus, this approach enabled them to undergo preliminary medical consultations with minimal contact with others.

This function is analogous to the health codes we use, conveying users’ basic health information, and can therefore be regarded as the most fundamental function of telemedicine on the patient side.

Enhancing Clinical Efficiency with AI

This is also a feature widely adopted across various countries: companies such as Yitu Healthcare, Shukun Technology, and Dashu Yida in China, as well as Lunit in South Korea, have all developed AI-powered chatbots to help residents assess their likelihood of having COVID-19 from home.

With the surge in demand for services from providers such as Teladoc and AmWell, it is no longer practical to handle such a high volume of consultation requests solely through manual labor. In this context, we need a tool to triage patients based on their specific conditions, which represents one of the key roles of AI-enabled telemedicine during the pandemic.

In this way, telehealth service providers can alleviate the load on front-end servers to a certain extent, allowing patients to receive treatments tailored to their needs without prolonged waiting times. Therefore, even telehealth, which aims to promote the redistribution of medical resources, requires the assistance of technologies such as artificial intelligence to optimize resource allocation.

Addressing the Uneven Geographic Distribution of Medical Resources

As the pandemic continued to evolve, people’s mobility became increasingly restricted. Coupled with the inherent uneven distribution of medical resources under commercial agglomeration, residents in remote areas or overly densely populated regions struggled to access adequate healthcare services. Physicians faced similar disparities: some were overwhelmed with work, while others had no patients to serve. Telemedicine helps break down these geographical barriers.

Moreover, the distribution of COVID-19 infections among patients is also uneven. As can be seen from the epidemic map provided by Johns Hopkins University in the preceding text, infection rates in coastal cities are significantly higher than those in inland regions. Many cities may have only dozens to hundreds of confirmed COVID-19 cases, which implies that their medical resources can be reallocated through telemedicine.

This is the core of the CCHP policy. If restrictions on telemedicine were fully lifted, Teladoc in Texas would be able to provide more specialized COVID-19 consultation services to patients in New York State, and even issue certain prescriptions. However, as of April 14, Washington, D.C. still does not welcome out-of-state physicians providing remote care to local patients, particularly in the absence of an established doctor-patient relationship.

This policy has another positive aspect: previously, telemedicine providers competed only within their respective states, with just over 100 telemedicine startups across the United States, making the competition far from intense. However, following regulatory liberalization—particularly the elimination of specific licensure requirements for telemedicine in certain regions—these companies now face competition not only from telemedicine firms in other states but also from non-telemedicine physicians participating in federal healthcare programs. In this new landscape, every physician effectively becomes a telemedicine provider.

Based on existing policies, this competition may last only three months—many states have suspended regional restriction schemes merely as part of their emergency pandemic measures and plan to reinstate them within 60–90 days. So, after several months of trial, will the United States maintain its open telemedicine policy, having tasted the benefits of market competition? This is entirely possible.

During the COVID-19 Pandemic, People Feared More Than Just the Virus

Although we should indeed prioritize the prevention and control of COVID-19, there are many other people whose lives are threatened not only by the coronavirus.

Patients with chronic diseases constitute one such group. When telemedicine first emerged, many startups focused on providing tracking and reminder services for conditions such as diabetes and heart disease. During the pandemic, these patients still required ongoing medication management. Policy changes in states such as Indiana have emphasized the right of patients with non-COVID-19 conditions to obtain prescriptions from telemedicine providers, which may represent a significant direction for the future development of telemedicine in the United States.

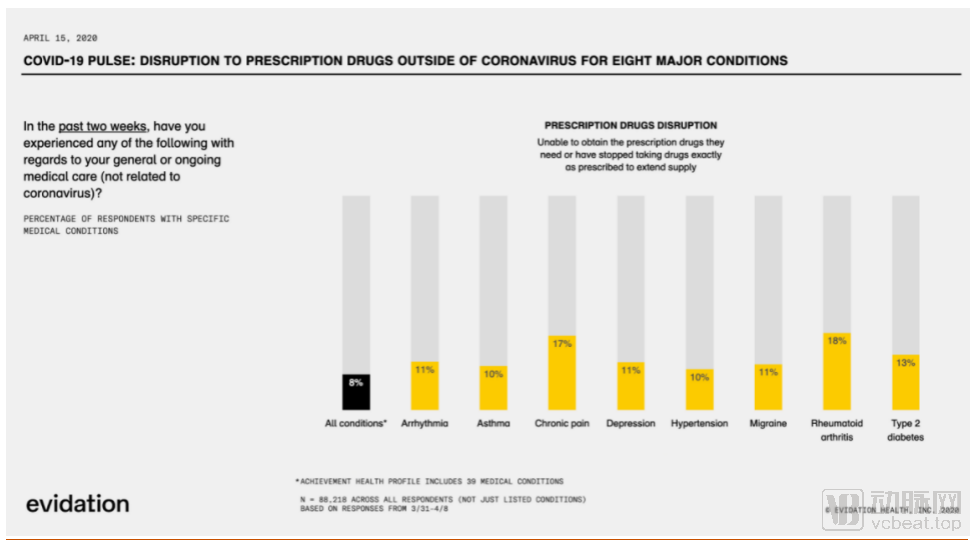

A survey conducted by Evidation from March 31 to April 8 found that nearly 33% of patients missed or canceled doctor appointments, and 7% had difficulty obtaining prescription medications.

Next is psychiatric counseling. In the face of sudden and seemingly endless disasters, individuals experiencing significant disruptions to their lives and work are highly susceptible to developing mental health issues. States such as Connecticut and Minnesota have specifically emphasized the potential for delivering psychotherapy through telehealth services. For telehealth, audio-only psychiatric treatment may be one of its most effective modalities.

CCHP also highlighted two critical groups: hemodialysis patients and those with end-stage renal disease. Relying solely on telemedicine would put the lives of these patients at grave risk. Therefore, for telemedicine to achieve substantial growth in the post-pandemic era, it must be supported by complementary offline measures.

Although major healthcare providers such as UnitedHealth Group Inc. and Humana Inc. have all announced their entry into the telemedicine sector, Teladoc remains the only publicly traded telemedicine company in the United States at this stage. It offers transparent data for reference by new market entrants and, to some extent, reflects the state of telemedicine development in the U.S.

On January 12, 2020, Teladoc Health, a leader in the U.S. telehealth sector, announced its acquisition of InTouch Health for $600 million. InTouch Health is a leading provider of telehealth solutions for acute care, collaborating with more than 450 hospitals and healthcare systems worldwide and serving over 14,500 physician users. Furthermore, InTouch Health partners with more than 130 health systems and operates across 2,135 care sites, supporting over 40 clinical use cases. It was ranked by KLAS Research as the world’s top virtual care platform for two consecutive years.

Upon completion of this acquisition, Teladoc Health will become the world’s only telehealth company covering all care domains. Its services will span from critical care and chronic disease management to routine care, extending across diverse settings including home care, pharmacies, retail clinics, physician offices, and ambulances. This means that during the pandemic, patients with any care needs could find corresponding services on the Teladoc platform.

Teladoc’s Stock Price Trend Over the Past 18 Months

As mentioned above, Teladoc’s visit volume doubled within a week, and with the worsening pandemic in April, traffic is expected to peak this month. Given the current state of the outbreak in the United States, the country may continue to experience the epidemic for another 2–3 months, which means that Teladoc will sustain high traffic volumes for an extended period.

The implied value increase from the surge in visit volume may have already been reflected in the stock price. When Teladoc announced its results for the previous quarter in February, its stock price had already doubled compared to the same period last year; after weathering the storm from February to April, its share price doubled once again.

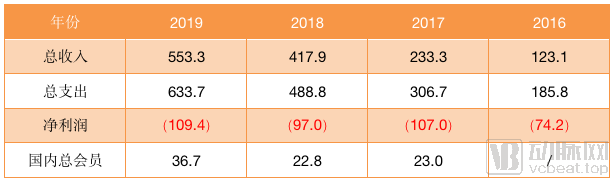

Looking at the annual reports, Teladoc’s revenue has grown continuously since the fourth quarter of 2017: its revenue in Q4 2017 was $77.1 million, and by Q3 2019, quarterly revenue had reached $137.9 million. However, it still maintained an annual loss of $100 million. Nevertheless, bolstered by the dual tailwinds of the current environment and policy support, Teladoc is highly likely to turn a profit this year.

Teladoc Operational Performance (in millions of U.S. dollars and millions of people)

However, Teladoc’s business model has not undergone significant changes, continuing to rely primarily on a hybrid approach combining per-visit purchases and membership subscriptions. On its official website, we can see pricing such as $55 for routine care, $90 for mental health services, and $85 for dermatology consultations per visit. However, by purchasing a Teladoc membership, users can access a limited number of these services throughout the year for just $30. Its business model is clear: leverage the membership system to attract more customers for online diagnostics, and then drive referrals to offline healthcare providers and pharmacies.

During the pandemic, the partnership between Teladoc and Blue Shield took a significant step forward. Blue Shield announced that its members would have access to telemedicine services provided by Teladoc’s nationally board-certified physicians at any time, with these services fully covered under their insurance plans.

Meanwhile, Teladoc has also entered into an in-depth collaboration with the University of Virginia (UVA), recruiting patients for free Q&A sessions on COVID-19-related issues and providing complimentary telehealth services to participants in the UVA Health Plan through June 4.

Globally, companies such as Teladoc, AmWell, and Doctor on Demand in the United States; Babylon in the United Kingdom; and Ping An Good Doctor and WeDoctor in China have all experienced explosive growth recently. However, fundamentally, the pandemic, as a systemic factor, has been the primary driver propelling the industry’s rapid development.

This surge will undoubtedly lead more patients to learn about and utilize telemedicine. However, it is equally certain that as the pandemic stabilizes, telemedicine visit volumes will decline. Therefore, how to mitigate this drop-off and sustain the engagement of existing users is undoubtedly a key challenge facing telemedicine providers in the near future.

Objectively speaking, China has capitalized on this wave of development more effectively than the United States. In areas such as online consultations, prescription outflow, health insurance coverage, and pandemic tracking, China has advanced with greater decisiveness and speed. Notably, the feedback effect of pharmaceutical e-commerce on internet healthcare has significantly enhanced consumer recognition of these two sub-sectors. In contrast, the U.S. has been overly conservative.

However, both China and the United States still face three common issues that need to be addressed.

First, the issue of informatization in telemedicine. How to integrate EHR with software and ensure interoperability?

Second, data privacy and security concerns. Many states have been hesitant to promote telemedicine services, partly due to considerations of data security.

Third, there is the issue of business model. Although investors recognize the value of healthcare companies both domestically and internationally, all of these companies are currently operating at a loss. How to achieve profitability? This is a question that telemedicine service providers must address.

Compared to two years ago, China’s telemedicine, or internet-based healthcare, has developed its own distinct model and no longer needs to learn from overseas business models. However, there are still lessons to be drawn in the area of commercial health insurance; internet healthcare must accelerate its coverage under national medical insurance and integration with commercial insurance plans. Furthermore, regarding privacy and data security, as the industry advances rapidly, data-related issues are most likely to arise.