China's Healthcare Sector Outperforms Broader Market in Q1 2020 Amid Pandemic: Medical Index Up 7.5% vs. SSE Composite Down 8.8%

The first quarter of 2020, which has just passed, was likely the most turbulent quarter in the history of capital markets. In addition to the global pandemic, a rare event in decades, the volatility in the secondary market also caused heart rates to accelerate and blood pressure to rise. From every perspective, the first quarter of 2020 will go down in the annals of capital market history.

So, how have domestic healthcare companies performed in the secondary market? Which companies have demonstrated exceptional performance? Has the healthcare sector in the secondary market outperformed the broader market? VCBeat (WeChat ID: Vcbeat) has compiled and analyzed publicly available information.

Shanghai Composite Index Drops 8.8% in Q1, Outperforming Overseas Markets

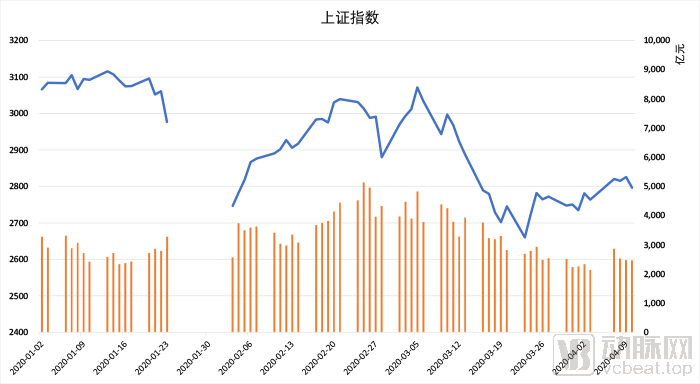

The trend of the Shanghai Composite Index in the first quarter clearly demonstrates the impact of the pandemic on the broader market. At the beginning of the year, the index hovered around 3,100 points, reaching its peak of 3,116 points on January 13. As the number of newly confirmed COVID-19 cases in Wuhan surged rapidly on January 19 and 20, the index began to decline, falling to 2,977 points before the market holiday on January 23.

Data source: Choice; Chart by VCBeat

On February 3, the epidemic situation in China had become relatively severe, significantly impacting the Shanghai Composite Index. The index fell by 369 points from its highest level at the beginning of the year to 2,747 points, representing a decline of 11.8%. Subsequently, as epidemic control measures gradually proved effective, the Shanghai Composite Index began a slow recovery. By March 5, the index closed at 3,072, nearly returning to its early-year levels.

However, the epidemic also broke out successively abroad during this period. On March 7, in view of the rapid increase in confirmed cases of novel coronavirus pneumonia in New York State in recent days, Andrew Cuomo, Governor of New York State, declared a state of emergency throughout the state. Two days later, on March 9, Italian Prime Minister Conte delivered a televised address that evening, announcing that nationwide "lockdown" measures would be implemented from March 10 to curb the spread of the COVID-19 epidemic.

The Shanghai Composite Index subsequently fell in response. On March 23, it closed at 2,660, even lower than the 2,747 recorded during the most severe phase of the domestic epidemic. Compared with the peak of 3,116, this represents a decline of 456 points, or 14.6%. As of April 10, the index had rebounded slightly to close at 2,796.631, still down 8.8% from the year’s opening level of 3,066.335.

Data source: Choice; Chart by VCBeat

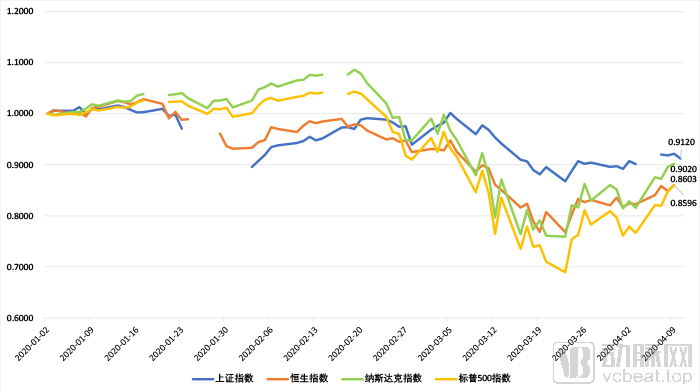

Driven by fluctuations in energy market prices, U.S. stocks began to experience volatility in late February. As the pandemic started to spread across the United States and negotiations on OPEC’s production cut agreement collapsed, the plunge in oil prices further shocked international financial markets, leading to massive swings in U.S. equities in March. On March 9, 12, 16, and 18, U.S. stocks triggered circuit breakers four times—an unprecedented occurrence in history.

Although the Chinese stock market was also affected, it has clearly proven to be more resilient in terms of price fluctuations compared to U.S. stocks. On March 23, the Nasdaq Composite Index fell to 6,861, a drop of 2,956 points, or 30.1%, from its first-quarter high of 9,817 recorded on February 19. In response to this situation, the Federal Reserve took emergency action on the same day, announcing multiple liquidity support measures and initiating unlimited quantitative easing, which led to a volatile rebound in U.S. stocks. As of April 9, the Nasdaq closed at 8,153.575, down 9.8% from its opening level of 9,039.46 at the beginning of the year.

However, unlimited quantitative easing is not a long-term solution, and its subsequent impact on the economy will soon become apparent.

Pharmaceutical Index Rises 7.5%, Outperforming the Broader Market

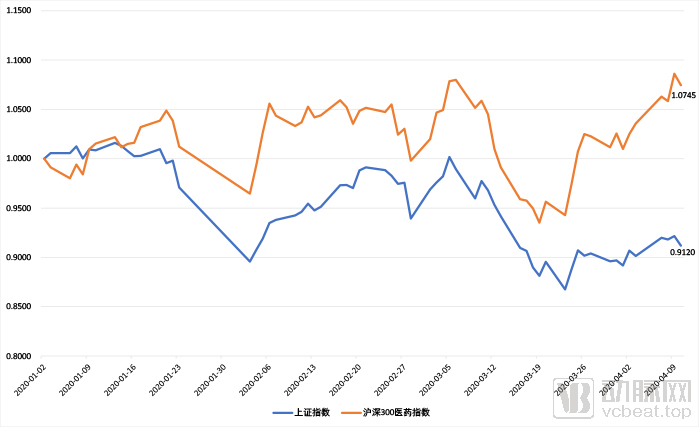

So, what changes have occurred in the broader trend between China’s healthcare sector and the overall domestic market? We compared the percentage changes of the CSI 300 Healthcare Index, which represents the healthcare sector, with those of the Shanghai Composite Index.

Data source: Choice; Chart by VCBeat

As of April 10, the CSI 300 Healthcare Index showed no significant difference in its overall trend compared to the Shanghai Composite Index, also experiencing a pattern of stability, decline, rebound, decline, and subsequent rebound. However, based on the cumulative returns chart, the CSI 300 Healthcare Index significantly outperformed the broader market. Except for the initial period when the pandemic outlook was unclear, during which its performance lagged behind the broader market, the CSI 300 Healthcare Index remained substantially higher than the broader market at all other times.

On April 9, the CSI 300 Healthcare Index closed at 11,910.7, marking the highest point within the statistical period. This represented an increase of 1,654.62 points, or 16.13%, from the low of 10,256.08 recorded on March 19. However, on April 10, the index dipped slightly to close at 11,782.99, which still constituted a 7.5% gain compared to the year-to-date starting level of 10,966.28. In contrast to the Shanghai Composite Index’s decline of 8.8%, the performance of the CSI 300 Healthcare Index was significantly stronger.

Which subsectors within the healthcare sector have demonstrated particularly outstanding performance? According to the East Money industry classification, all listed healthcare companies are categorized into six major segments: chemical pharmaceuticals, biopharmaceuticals, medical devices, traditional Chinese medicine (TCM) production, healthcare services, and pharmaceutical commerce. As there are no dedicated indices for each individual segment, we compared the average stock prices of all listed companies within each segment at the beginning of the year and on April 10. Although this approach lacks rigorous precision, it can still serve as a basic analytical reference.

Data source: Choice; Chart by VCBeat

The four sectors—chemical pharmaceuticals, biopharmaceuticals, medical devices, and healthcare services—all outperformed the CSI 300 Healthcare Index, which rose by 7.5%. Among them, medical devices performed the best, with a gain of 27.22%, while chemical pharmaceuticals (20.03%) and biopharmaceuticals (18.5%) showed similar performance.

The pharmaceutical distribution sector rose by 6.16%, slightly underperforming the CSI 300 Healthcare Index but still maintaining growth. In contrast, the traditional Chinese medicine (TCM) manufacturing segment delivered disappointing results, declining by 0.07% after the first quarter.

Next, we will analyze the stock price trends of domestically listed healthcare companies in the first quarter. By comparing the closing prices at the beginning of the year (January 2) with those on April 10, we can assess these companies’ stock performance during the first quarter.

Chemical Pharmaceuticals

There are 100 listed chemical pharmaceutical companies in China’s stock market; however, Nanxin Pharmaceutical and Zelgen Pharmaceuticals were newly listed in 2020. Therefore, these two companies were excluded from our analysis.

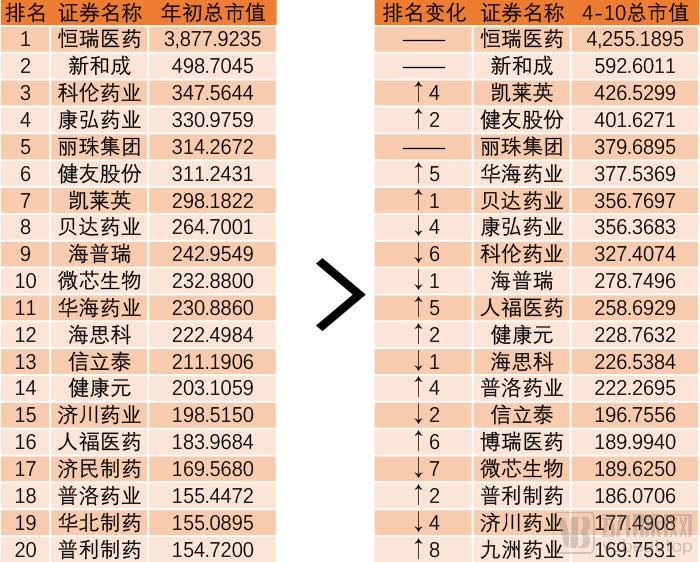

Ranked by market capitalization in early 2020, the pharmaceutical giant Hengrui Medicine (600276.SH) topped the list with a market cap of RMB 387.79 billion, firmly establishing itself as a listed industry leader. In fact, Hengrui Medicine’s market capitalization in early 2020 was equivalent to the combined total of the 14 companies ranked second through fifteenth.

The median market capitalization of these 98 listed chemical pharmaceutical companies was RMB 6.64347 billion, with 31 companies exceeding RMB 10 billion in market capitalization, accounting for 31.6%.

As of the market close on April 10, 2020, the majority of the top 20 companies by stock price gain were those with relatively mid-tier or lower market capitalizations at the beginning of the year; eight of them had market caps below the median, while only three boasted market capitalizations exceeding RMB 10 billion.

Data source: Choice; Chart by VCBeat

The top 20 companies by market capitalization saw slight changes at the close on April 10, with Borui Medicine and Jiuzhou Pharmaceutical successfully breaking into the top 20 in the chemical pharmaceutical sector, ranking 16th and 20th, respectively.

The top two positions remained unchanged, with Hengrui Medicine and NHU still leading, while Asymchem rose from seventh place into the top three. On April 10, Hengrui Medicine’s market capitalization further reached RMB 425.51895 billion, an increase of RMB 37.7266 billion since the beginning of the year—this single-quarter gain alone was equivalent to the entire market capitalization of the company ranked sixth.

Data source: Choice; Chart by VCBeat

Among the top 20 companies by market capitalization, only Huahai Pharmaceutical (600521.SH) and Asymchem (002821.SZ) made it into the top 20 gainers. Huahai Pharmaceutical saw a 63.52% increase in Q1, ranking fifth among gainers, which is quite remarkable.

Unimed Pharmaceutical (002581.SZ) was the listed chemical pharmaceutical company with the largest stock price increase in the first quarter, surging by 118.01%. Why has this company, whose core business focuses on pharmaceuticals and agricultural intermediates, experienced such a significant rise?

On April 13, the National Medical Products Administration (NMPA) approved the entry of Sinovac Biotech’s “CoronaVac” inactivated COVID-19 vaccine, developed by its affiliate Beijing Sinovac Life Sciences Co., Ltd., into clinical trials. The second-largest shareholder of Sinovac Biotech is Unimed Pharmaceuticals Inc., which holds a 26.91% stake in the company. Unimed Pharmaceuticals is a wholly-owned subsidiary of the listed company Unimedic Pharma. This likely explains why Unimedic Pharma emerged as the top gainer in the chemical pharmaceutical sector.

Porton Pharma Solutions (300363.SZ) and Tianyu Pharmaceuticals (300702.SZ) ranked second and third, with gains of 84.1% and 82.58%, respectively.

On February 7, Porton Pharma Solutions announced that it had received a confirmation letter for an order of intermediates for remdesivir, an investigational antiviral drug under development by its core client, Gilead Sciences. To date, the clinical safety and efficacy of this investigational drug have not yet been confirmed, and it remains uncertain whether it can successfully treat COVID-19. Nevertheless, this has not dampened the market’s positive outlook on Porton Pharma Solutions.

Tianyu Pharmaceuticals’ core business focuses on pharmaceutical intermediates and active pharmaceutical ingredients (APIs). As the undisputed global leader in sartan APIs, it is one of the largest suppliers of valsartan, with its production volumes of losartan and irbesartan also ranking among the highest worldwide. Due to the impact of the COVID-19 pandemic on India, another major production hub for sartan APIs, a supply shortage may arise. Consequently, Tianyu Pharmaceuticals’ stock price has continued to rise.

Biopharmaceuticals

There are 57 listed companies in the biopharmaceutical sector. After excluding three companies that went public in 2020—Bio-Thera Solutions (688177.SH), Xiamen AmoyTop Biotechnology (688278.SH), and Orient Gene Biotech (688298.SH)—there remain 54 listed companies.

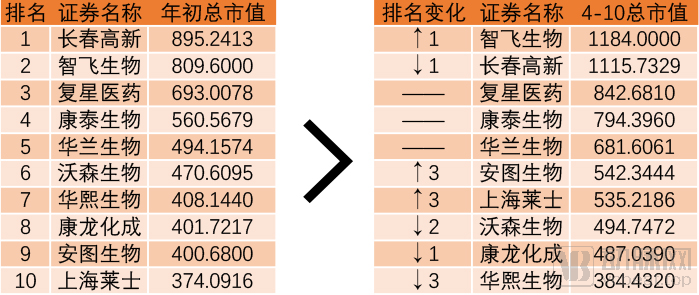

Ranked by market capitalization at the beginning of the year, Changchun High-Tech took first place with a total market cap of RMB 89.524 billion; followed closely by Zhifei Biological Products with a market cap of RMB 80.96 billion and Fosun Pharma with a market cap of RMB 69.3 billion.

The median market capitalization of these 54 companies was RMB 8.396 billion, higher than that of chemical pharmaceutical companies. Meanwhile, although the number of biopharmaceutical companies was only about half that of chemical pharmaceutical companies, as many as 21 of them had a market capitalization exceeding RMB 10 billion, accounting for 38.9%, a higher proportion than that of chemical pharmaceutical companies with a market capitalization over RMB 10 billion. This also reflects the current situation where biomedicine, as an emerging industry, is receiving greater attention from investors.

Data source: Choice; Chart by VCBeat

As of April 10, the top spot among the ten companies with the highest market capitalizations changed hands. Zhifei Biological Products, previously ranked second, surpassed Changchun High-Tech with a market cap of RMB 118.4 billion, becoming the most valuable company in the biopharmaceutical sector. Both companies are also among the few in the healthcare sector with market capitalizations exceeding RMB 100 billion.

The biopharmaceutical sector generally performed well in the first quarter, with share prices rising for as many as 37 companies and falling for only 16. The declines were generally modest, with only six companies experiencing share price drops exceeding 10%.

Data source: Choice; Chart by VCBeat

Ranked by price change, Haitai Bio ranked first with a 92.51% increase in its stock price in the first quarter. Daan Gene (56.44%) and Zhifei Biological (46.25%) ranked second and third, respectively.

Haitai Bio announced the unblinding results of the Phase III clinical trial for CPT-MM301, a novel anti-tumor drug with a new mechanism of action (DR4/DR5), in the first quarter. Preliminary analysis indicated that the trial met its pre-specified primary and key secondary endpoints, with approval for market launch expected in 2021.

However, the performance of Wuhan-based Haitai Bio was clearly impacted by the pandemic. Its first-quarter earnings forecast showed a net profit of approximately RMB 2.9855 million to RMB 8.9564 million, representing a year-on-year decline of 70%–90% compared with the RMB 29.8547 million reported in the same period last year.

Da An Gene, positioned in the field of precision medicine, has been dedicated to molecular diagnostics for over two decades and boasts one of the leading clinical molecular diagnostic product lines in China. During the reporting period, Guangzhou Clinical Laboratory Center, the largest laboratory under Da An Gene, achieved an operating revenue of RMB 365 million, representing a year-on-year increase of 30%. As early as February 2, at the initial stage of the pandemic outbreak, Da An Gene announced that its novel coronavirus nucleic acid detection kit based on fluorescent PCR technology had received approval from the National Medical Products Administration (NMPA), making it one of the earliest approved kits for COVID-19 nucleic acid testing.

On February 3, Zhifei Biological Products issued an announcement stating that its wholly-owned subsidiary, Anhui Zhifei Longcom Biopharmaceutical Co., Ltd., signed a Framework Agreement on Cooperative Intent with the Institute of Microbiology, Chinese Academy of Sciences, on January 29, 2020, to jointly develop a recombinant protein subunit vaccine for COVID-19.

In addition, Zhifei Biological’s EC reagent for tuberculosis diagnosis has completed review by the CDE (Center for Drug Evaluation of the National Medical Products Administration) and entered the approval stage. The development progress of this reagent is on par with that of the comparable product from the Statens Serum Institut in Denmark, making it one of the two most advanced novel Mycobacterium tuberculosis detection reagents worldwide.

Medical Devices

During this pandemic, shortages of protective supplies, ranging from face masks to ventilators and even extracorporeal membrane oxygenation (ECMO) machines, have repeatedly occurred in countries and regions around the world. Although China is a major manufacturing power, its medical device industry still has room for development. It is for this reason that China proposed an “import substitution” strategy for medical devices at an earlier stage. In the concrete implementation of the “New Infrastructure” initiative following the alleviation of the epidemic, medical devices have also been taken into consideration.

Among the medical device companies listed on China’s A-share market, there are a total of 48 firms, including Tailin Bioengineering (300813.SZ) and Sanyou Medical (688085.SH), which went public in 2020. Excluding these two, the remaining 46 listed companies have a median market capitalization of RMB 4.905 billion, highlighting that most listed medical device firms remain relatively small compared to pharmaceutical companies.

Mindray Medical (300760.SZ) is the undisputed giant in the medical device sector, with a market capitalization of RMB 219.22561 billion, nearly equivalent to the combined market cap of the nine companies ranked 2nd through 10th (RMB 220.20987 billion). Lepu Medical (300003.SZ) ranks second, with its market capitalization reaching RMB 59.13306 billion at the beginning of the year, representing a significant advantage over the subsequent companies. The market capitalizations of the remaining firms are relatively close to one another. In total, there are 12 companies with market capitalizations exceeding RMB 10 billion, accounting for 26% of the sector.

Data source: Choice; Chart by VCBeat

As a leading domestic ventilator supplier, Mindray Medical maintained high-intensity production throughout the pandemic. Following the global outbreak, numerous countries and regions sought to purchase ventilators from China, with orders reportedly backlogged for several months.

Data source: Choice; Chart by VCBeat

As of April 10, healthcare companies’ stock prices generally performed well. Apart from two companies that remained flat and four that experienced slight declines, a total of 40 companies saw their share prices rise, mostly by significant margins, with an average increase of 40.35%.

Ranked by percentage gain, Intco Medical (300677.SZ) posted the highest increase, with its stock price surging by 195.37%. It was followed by Edan Instruments (300206.SZ), which rose by 91.87%, and Glory Medical (002551.SZ), which gained 90.17%.

Given the substantial overall gains in the medical device sector, coupled with the relative underperformance of large-cap companies in terms of percentage growth, only Yuwell Medical (002223.SZ) and Jafron Biomedical (300529.SZ) from the top ten companies by market capitalization at the beginning of the year made it into the top ten for price appreciation. Notably, Yuwell Medical, which also benefited from the surge in demand for ventilators during the pandemic, saw its share price rise by 86.56%, ranking fourth on the gainers’ list. In fact, even industry giants such as Mindray Medical achieved a significant increase of 44.96%, underscoring the broad upward trend across the medical device industry.

Intco Medical is one of the leading manufacturers of gloves, with an annual production capacity exceeding 15 billion units. Of this, 97% of its capacity supplies markets in Europe, the United States, Japan, and other countries and regions. On the evening of April 15, Intco Medical announced its latest resolution, proposing to change the “Expansion Project for High-End Medical Gloves” previously announced in early March to the “Intco Medical Protective Equipment Industrial Park Project.” Upon completion and commissioning, the project will achieve an annual production scale of 21 billion units (21 million cases) of high-end medical gloves.

Compared with traditional latex gloves, nitrile gloves offer superior physicochemical properties, as well as enhanced hypoallergenicity and ease of donning. Global demand has been rising rapidly, even independent of the pandemic-driven surge. Their raw materials, acrylonitrile and butadiene, are conventional chemical feedstocks that are readily available in China. In contrast, the natural rubber required for the latex gloves they replace is primarily sourced from Southeast Asia, where China holds no competitive advantage. Therefore, the shift in industrial production is a logical progression.

In addition to Intco Medical, Blue Sail Medical is also one of the major suppliers of medical gloves. According to a research report by Everbright Securities, its market share was 4% in 2018, higher than Intco Medical’s 2.89% at that time. With Intco Medical’s production expansion, the market shares of both companies are projected to reach parity in 2020, each at 4.13%.

Edan Instruments’ dry blood gas analyzer is the leading brand in China, and its other products—including patient monitors, ECG devices, and POCT (blood gas) systems—are also highly aligned with the entire diagnostic and treatment workflow during the current epidemic.

According to Edan Instruments’ announcement, as of February 20, Huoshenshan Hospital, a key facility for critical care, had installed 100 patient monitors, 35 electrocardiographs (ECGs), 200 pulse oximeters, and 5 blood gas and biochemistry analyzers. Leishenshan Hospital had comparable installation figures. Across various makeshift cabin hospitals, a total of 650 patient monitors, 70 blood gas and biochemistry analyzers, and 6 portable color Doppler ultrasound systems were installed. In addition, more than 50 Edan blood gas analyzers were installed at Wuhan’s four major hospitals: Tongji Hospital, Union Hospital, Hubei Provincial People’s Hospital, and Zhongnan Hospital.

Shangrong Medical is a leading manufacturer of medical consumables in China. Its controlling subsidiary, Hefei Purell Medical Supplies Co., Ltd., is one of the largest domestic producers of disposable surgical packs and protective products, serving as a key supplier to Fortune 500 companies such as Medline, DuPont, 3M, and Kimberly-Clark. The company currently has an annual production capacity of 70 million surgical gowns and 10 million units of various types of protective clothing.

Including the production capacity of its subsidiary, Hefei Medtop Medical Hygiene Products Co., Ltd., Glory Medical was designated by relevant national authorities at the beginning of the year as one of the first batch of designated enterprises for emergency medical protective suits, ranking among the top three in the industry in terms of enterprise scale.

Traditional Chinese Medicine Production

Through continuous refinement and improvement, traditional Chinese medicine (TCM) has played a significant adjunctive role in the current epidemic. Starting from the fourth edition of the diagnosis and treatment guidelines, the National Health Commission and the National Administration of Traditional Chinese Medicine organized TCM experts to sequentially develop protocols for severe and critical cases. Lianhua Qingwen capsules, Jinhua Qinggan granules, Xuebijing injection, Qingfei Paidu decoction, Huashi Baidu formula, and Xuanfei Baidu formula have been collectively recognized as the “Three Medicines and Three Formulas” with demonstrated clinical efficacy.

In regions such as Hunan, where Traditional Chinese Medicine (TCM) was extensively applied for targeted treatment of COVID-19, the case fatality rate was lower than in other areas, demonstrating the efficacy of TCM. Data indicate that this time-honored medical system indeed held significant value during the pandemic.

A total of 66 listed traditional Chinese medicine (TCM) manufacturers are traded on domestic stock exchanges, with no new listings since the beginning of 2020. The median market capitalization of these 66 companies stands at RMB 5.1921 billion. Eighteen companies have a market capitalization exceeding RMB 10 billion, accounting for 27% of the total.

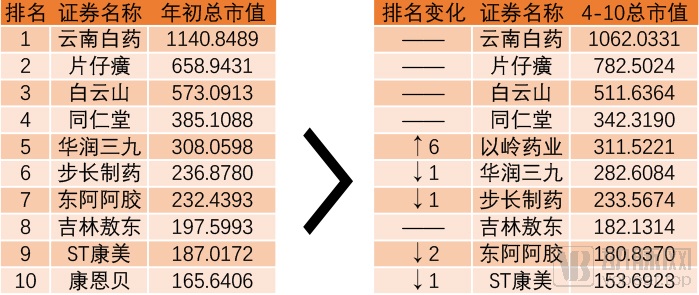

Ranked by market capitalization at the beginning of the year, Yunnan Baiyao (000538.SZ), a giant in traditional Chinese medicine production, took the top spot with a market cap of RMB 114.08489 billion. Pien Tze Huang (600436.SH) and Guangzhou Baiyunshan Pharmaceutical Holdings (600332.SH) ranked second and third, with market capitalizations of RMB 65.89431 billion and RMB 57.30913 billion, respectively.

Data source: Choice; Chart by VCBeat

As of April 10, there were slight changes in the top 10 traditional Chinese medicine (TCM) manufacturers by market capitalization. Yiling Pharmaceutical, originally ranked 11th, saw its market cap surge to RMB 31.15221 billion, driven by the popularity of Lianhua Qingwen Capsules, thereby jumping significantly to fifth place.

Data source: Choice; Chart by VCBeat

Ranked by first-quarter stock price gains, 24 traditional Chinese medicine (TCM) enterprises saw their share prices rise, making the TCM sector one of the few healthcare segments where declines outnumbered gains in the first quarter. Notably, apart from Pien Tze Huang, which posted a gain, the other nine companies among the top ten by market capitalization at the beginning of the year all experienced stock price declines in the first quarter.

Yiling Pharmaceutical ranked first with a surge of 113.71%, while Hongri Pharmaceutical (300026.SZ) and Wohua Pharmaceutical (002107.SZ) took second and third place, with increases of 38.46% and 37.03%, respectively. Among the top ten companies by market capitalization at the beginning of the year, Pien Tze Huang performed well in the first quarter, securing a spot in the top ten gainers with an 18.75% increase.

Yiling Pharmaceutical, the manufacturer of Lianhua Qingwen Capsules, has been one of the most closely watched traditional Chinese medicine companies during the current epidemic.

In Academician Zhong Nanshan’s global sharing of treatment and management protocols for COVID-19 patients, it was also mentioned that Lianhua Qingwen Capsules achieved favorable clinical outcomes (Editor’s Note: For specific insights shared by Academicians Zhong Nanshan and Li Lanjuan, please refer to〈Academicians Zhong Nanshan and Li Lanjuan Share Globally: A 20,000-Word Transcript Covering Prevention and Control, Treatment, Clinical Practice, and Medication Experience for COVID-19〉)。

On April 14, Yiling Pharmaceutical announced that its application for additional indications for Lianhua Qingwen Capsules (Granules) had been approved. This announcement marks Lianhua Qingwen as the first domestically produced drug in China to officially receive COVID-19-related indications.

Following the approval, Yiling Pharmaceutical’s market capitalization and stock price saw significant increases. As of April 17, its market cap and closing share price had surged to RMB 42.5153 billion and RMB 35.32, respectively, representing 2.91 times their levels at the beginning of the year.

Hongri Pharmaceutical’s flagship product, Xuebijing Injection, has been included in the recommended medications for both Western medical treatment measures and Traditional Chinese Medicine (TCM) clinical treatment phases for severe and critically ill cases. On April 14, Hongri Pharmaceutical announced that its application for new indications for Xuebijing Injection had been approved. The approved functions and indications now include the description: “It can be used for systemic inflammatory response syndrome (SIRS) and/or multiple organ dysfunction syndrome (MODS) in severe and critically ill patients with novel coronavirus pneumonia.”

According to Qichacha, Beijing Chaosi Electronic Technology Co., Ltd. is a wholly-owned subsidiary of Chasesun Pharmaceutical, and this company holds 100% equity in Tianjin Chaosi Medical Device Co., Ltd. Tianjin Chaosi is the global leader in finger-clip pulse oximeters, with a 60% share of the international market. Due to the impact of the global pandemic, its product sales have been very promising.

This has also pushed Hongri Pharmaceutical’s market capitalization to RMB 21.58096 billion by April 17, representing 2.05 times its value at the beginning of the year and placing it among the top ten traditional Chinese medicine (TCM) manufacturers by market cap as of that date.

Wohua Pharmaceutical primarily specializes in proprietary Chinese medicines for cardiovascular and cerebrovascular diseases. Its flagship products mainly include Fangfeng Tongsheng Pills, Juhong Pear Paste, Yuandu Ganmao Granules, and Antiviral Oral Liquid. Although its connection to the pandemic is not as direct as that of Yiling Pharmaceutical and Hongri Pharmaceutical, its first-quarter performance also saw substantial growth.

Medical Services

According to the East Money industry classification, there are 22 listed companies in the medical services sector, all of which went public before 2020. Compared with other sectors, the definition of the medical services sector is relatively broad. This sector includes not only patient-facing (B2C) medical institutions such as Aier Eye Hospital (300015.SZ) and Meinian Onehealth (002044.SZ), but also business-facing (B2B) contract research organizations (CROs) like WuXi AppTec (603259.SH) and third-party medical testing companies like KingMed Diagnostics (603882.SH), as well as healthcare IT companies such as B-Soft (300451.SZ).

The median market capitalization of these 22 companies at the beginning of the year was RMB 9.5793 billion. Ten of them, accounting for 45%, had a market capitalization exceeding RMB 10 billion, indicating that this sector has a relatively high proportion of companies with a market capitalization above RMB 10 billion.

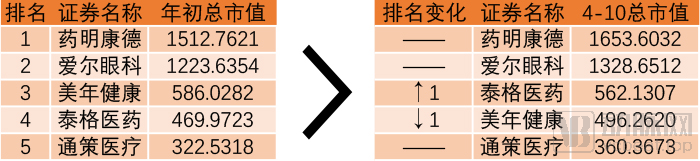

Ranked by market capitalization at the beginning of the year, WuXi AppTec was the most valuable company, with a market cap of RMB 151.27621 billion. It was followed by Aier Eye Hospital, whose market capitalization also exceeded RMB 100 billion, reaching RMB 122.36454 billion. Compared to other healthcare sectors, the medical services sector stood out relatively more, with two companies boasting beginning-of-year market caps above RMB 100 billion. Ranking third, Meinian Onehealth lagged somewhat behind the top two, with a beginning-of-year market capitalization of RMB 58.60282 billion.

Data source: Choice; Chart by VCBeat

As of the market close on April 10, the ranking of the top five companies by market capitalization saw only slight changes in the third and fourth positions. Tigermed, originally ranked fourth, surpassed Meinian Onehealth to secure the third spot with a market capitalization of RMB 56.21307 billion.

In terms of stock price gains, 12 companies saw their share prices rise, a number roughly equivalent to those that declined.

Data source: Choice; chart by VCBeat

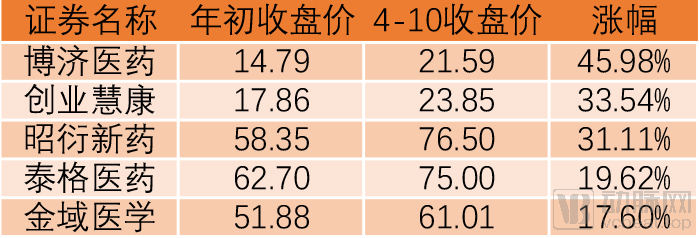

Boji Medicine (300404.SZ) ranked first with a 45.98% gain; B-Soft and Joinn Laboratories (603127.SH) ranked second and third, with gains of 33.54% and 31.11%, respectively.

Boji Medicine is one of the leading CRO companies in China and has been deeply involved in the R&D of new drugs to combat the epidemic. Boji Medicine and its subsidiary Jiutai Medical Devices, which is responsible for medical devices, have assisted in completing various tasks related to clinical research on drugs and medical devices for COVID-19, including writing clinical study documentation, coordinating with hospitals conducting clinical trials, and applying for government science and technology projects.

Currently, the R&D expenditures of listed pharmaceutical companies in China are growing at an average annual rate of over 30%, with accelerated development of innovative drugs, which is beneficial to the CRO/CDMO industry. Under the refined division of labor in modern pharmaceutical R&D, there is substantial demand for CRO services.

However, on April 10, Boji Medicine released its first-quarter earnings forecast, reporting a year-on-year decline in revenue for the quarter and an estimated net loss of RMB 4–9 million, a downturn from the net profit of RMB 1.3843 million recorded in the same period last year.

The current outbreak has exposed certain shortcomings in the level of informatization at medical institutions; meanwhile, the new model of telemedicine has gained broader recognition. Relevant authorities have also introduced the concept of “New Infrastructure,” from which healthcare informatization construction will undoubtedly benefit. This will significantly promote B-Soft’s medical and health services business.

As a leading healthcare IT enterprise in China, B-Soft’s business currently covers 400 regional public health projects. It has built over 6,000 information systems for hospitals and primary care institutions, serving more than 300,000 community-based physicians. Currently, B-Soft’s IT systems support 250 million health records and have established 100 million electronic medical records (EMRs). The year 2020 marks the deadline for secondary hospitals to complete the EMR interoperability assessment, which is expected to drive sales growth for B-Soft.

Meanwhile, B-Soft’s “Internet + Prescription Circulation” business has signed contracts with 13 hospitals. In addition, in May 2019, B-Soft won the bid for certain services of the National Healthcare Security Administration’s platform, which is expected to significantly boost its revenue from healthcare insurance-related businesses.

As another CRO company, Joinn Laboratories focused on developing overseas clients in 2018, with the proportion of revenue from overseas clients increasing significantly from 3% in 2018 to 7%. Although the pandemic had some impact on business operations, its continued spread overseas may have affected the operational efficiency of overseas safety assessment CROs. This could lead foreign pharmaceutical companies to choose Joinn Laboratories for safety assessment services, thereby accelerating the company's internationalization process.

Currently, Joinn Laboratories has acquired Biomere, a top-three preclinical CRO company in the New England region of the United States. This will strengthen its capacity to meet global pharmaceutical companies’ needs for FDA investigational new drug applications and may help attract overseas clients.

Pharmaceutical Commerce

The pharmaceutical distribution sector currently comprises 36 listed companies, all of which went public before 2020. The median market capitalization of these companies at the beginning of the year was RMB 9.42989 billion, with 17 companies having a market capitalization exceeding RMB 10 billion, accounting for 47% of the total.

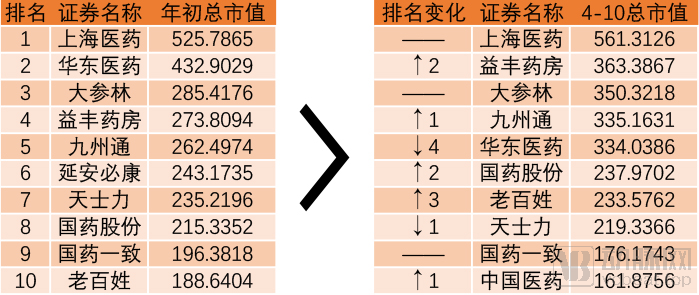

Ranked by market capitalization at the beginning of the year, Shanghai Pharmaceuticals (601607.SH) topped the list with RMB 52.57865 billion. This was also the only sector in the healthcare industry without any company reaching a market cap of RMB 100 billion. Huadong Medicine (000963.SZ) and Dashenlin Pharmaceutical Group (603233.SH) ranked second and third, with market caps of RMB 43.29029 billion and RMB 28.54176 billion, respectively.

Data source: Choice; Chart by VCBeat

As of the market capitalization rankings on April 10, there were no changes in the top three positions. China National Pharmaceutical Group (600056.SH) entered the top ten with a market cap of RMB 16.18756 billion. However, this was less due to China National Pharmaceutical’s strong performance and more attributable to the underperformance of Yan’an Bikang (002411.SZ), which had ranked sixth in market capitalization at the beginning of the year—its market value plummeted from RMB 24.31735 billion to RMB 13.13167 billion, representing a decline of 46%. This drop was particularly notable among the leading companies by market capitalization across various sectors.

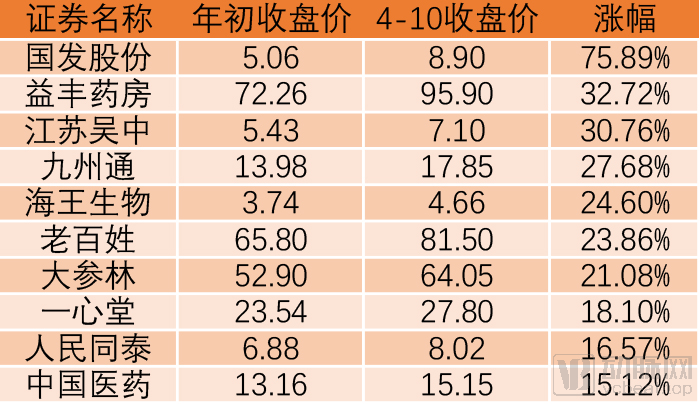

In the first quarter, the stock prices of 16 pharmaceutical commercial enterprises rose, while those of 20 others fell, remaining at a comparable level.

Guofa Shares (600538.SH) topped the gainers list, with its stock price rising 75.89% year-to-date as of the close on April 10. Yifeng Pharmacy (603939.SH) and Jiangsu Wuzhong (600200.SH) ranked second and third, with gains of 32.72% and 30.76%, respectively.

Data source: Choice; Chart by VCBeat

Beihai Guofa Marine Biological Industry Co., Ltd. Pharmaceutical Factory, a branch under Guofa Shares, is a core manufacturing enterprise in Guofa Shares’ pharmaceutical segment and one of the local suppliers of disinfection products (75% ethanol disinfectant). Sales of ethanol disinfectant surged during the pandemic, which had a significantly positive impact on Guofa Shares’ performance.

Yifeng Pharmacy is one of the pharmaceutical retail chain enterprises, primarily engaged in the chain retail of pharmaceuticals, health supplements, medical devices, and daily convenience products related to health.

On April 14, Yifeng Pharmacy released its first-quarter report for 2020, reporting a net profit attributable to shareholders of the listed company of RMB 191 million in the first quarter, a year-on-year increase of 29.68%.

One of Jiangsu Wuzhong’s products, Arbidol Hydrochloride Tablets, is an antiviral medication primarily indicated for influenza caused by influenza A and B viruses. It also exhibits potential antiviral activity against certain other respiratory viral infections, demonstrating broad-spectrum antiviral properties. During the pandemic, Arbidol was included as an antiviral agent in the sixth edition of the “Trial Protocol for the Diagnosis and Treatment of Novel Coronavirus Pneumonia.” However, the sales revenue from this product accounts for a small proportion of the listed company’s total operating income.

Stock Performance of Pandemic-Related Companies

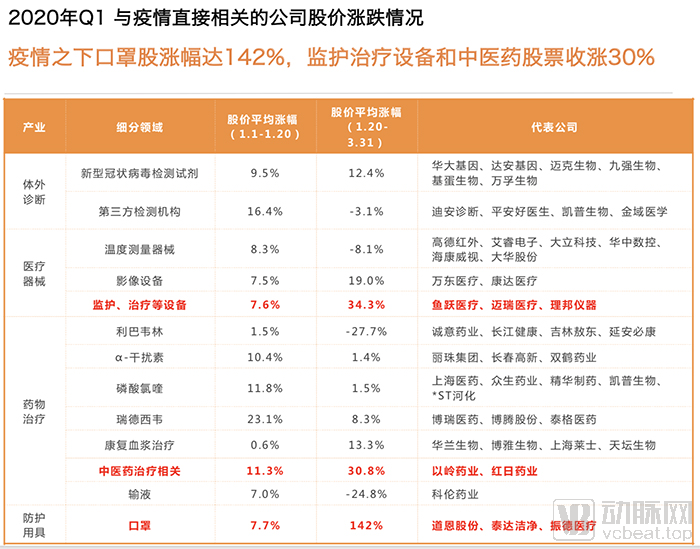

From the perspective of the entire healthcare sector, the vast majority of companies that performed well in the first quarter were directly linked to the pandemic. In addition to healthcare companies, some enterprises not classified within the healthcare sector also had direct ties to the pandemic. How did these companies perform? We have summarized their performance in the figure below.

Data source: Choice; Chart by VCBeat

It is evident from the performance of China’s secondary market healthcare indices and healthcare companies in the first quarter that the pandemic has acted as a powerful stimulant for numerous medical enterprises. Most healthcare companies whose core businesses are related to pandemic diagnosis, treatment, and protection have seen significant improvements in both their financial performance and stock prices.

Meanwhile, as the pandemic has heightened public and governmental emphasis on healthcare, even companies whose core businesses are unrelated to the pandemic will continue to benefit in the long term. The outperformance of the CSI 300 Healthcare Index against the broader market indicates that investing in healthcare is clearly one of the best hedges against inflation when the next economic downturn arrives.

Due to limitations in our expertise and the scarcity of publicly available data, this article may contain errors or omissions. We welcome readers to point them out. In subsequent issues, we will analyze the performance of healthcare companies in the global secondary market; please stay tuned.