After the Billion-Dollar EMR Market, Are Internet Hospitals the Next Target for HIT?

From being overlooked to growing wildly, the medical IT industry has gradually taken shape.

Reflecting on the Evolution of Healthcare Experiences Over the Past Decade. In the past, every medical visit required family members to rummage through drawers and cabinets to locate previous medical records, prescriptions, medication boxes, and even receipts. Today, many hospitals have digitized patient cards, migrated medical data to the cloud, and enabled remote appointment scheduling and payment via WeChat official accounts and hospital apps.

Today’s convenience is inseparable from foundational healthcare IT infrastructure. Since the launch of China’s new healthcare reforms, the healthcare informatization market has evolved from a niche segment with few participants and a lack of unified standards into a fiercely competitive “red ocean” characterized by clearly defined regional business divisions and numerous industry players. As market segmentation becomes increasingly pronounced, it is easy to identify the leading contenders.

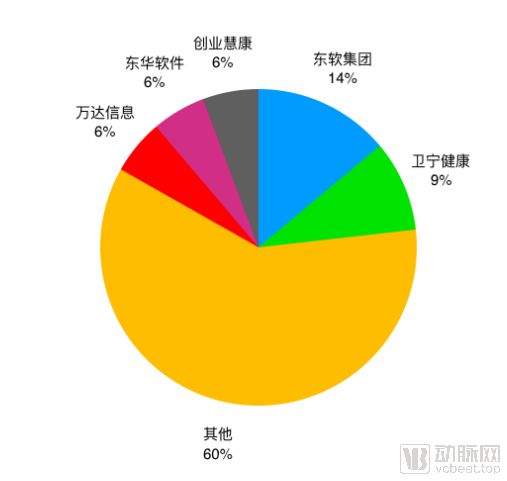

Market Share of Medical IT Solutions in China

IDC, “China Healthcare IT Solutions Market Forecast, 2018–2022,” Guojin Securities Research Institute

Change is gradually unfolding beneath the surface. Today’s industry leaders are no longer confined to selling health IT software to hospitals; although this segment remains the primary revenue source for most companies, new business lines are emerging.

Annual reports from the informatics sector have, to some extent, reflected these changes. In 2019, more than ten companies delivered starkly contrasting results, with some celebrating success while others faced setbacks.

VCBeat conducted a line-by-line analysis of the annual reports of publicly listed medical IT companies, examining aspects such as annual report data, foundational IT development, and the extended development of informatization, in an effort to outline the key priorities for healthcare informatization in the coming year.

As of April 23, 2020, due to the impact of COVID-19, among publicly listed medical IT companies, only Winning Health and B-Soft had released their full annual reports, while other enterprises disclosed the basic operational performance for 2019 in the form of preliminary earnings announcements. Nevertheless, we can still glean insights from the available data.

Summary of 2019 Annual Reports of Information Technology Enterprises (Unit: RMB 100 million)

Note: Data for Winning Health and Ectron Medical are sourced from annual reports, while the remaining data are derived from preliminary annual report announcements.

Operating Revenue and Operating Costs

As indicated by the table data, most companies have achieved positive operating revenues. This revenue growth is driven by two factors. On one hand, the Graded Evaluation of Electronic Medical Record (EMR) System Application Levels, introduced at the end of 2018, has spurred hospitals to proactively seek upgrades to their EMR systems and interoperability infrastructure. Based on current market pricing, comprehensive EMR solutions compliant with Level 4 or above of the graded evaluation exceed RMB 10 million, while those meeting Level 3 or above are priced at approximately RMB 10 million. Consequently, medical IT companies have seen a substantial increase in operating revenues.

On the other hand, hospitals are deepening their understanding of informatization. Directors of Information Departments are steering their work toward standardization and measurability, while also striving to reduce associated costs.

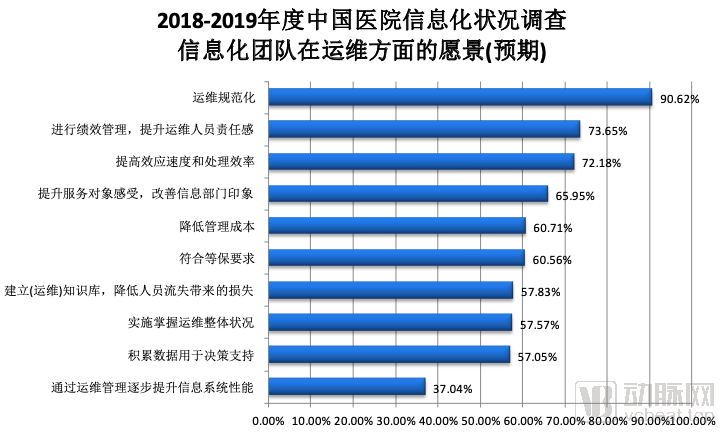

The data are sourced from the "Survey Report on the Status of Hospital Informatization in China (2018–2019)" released by CHIMA.

Net Profit

Among the 11 companies included in this analysis, seven reported net profit growth exceeding 20%. Notably, Rongke Technology’s net profit surged by 103.23%, and Yinjiang Co., Ltd.’s net profit rose by 284.63%. Only Wanda Information and Das Intellitech incurred losses.

First, let’s examine the growth trends. In addition to expanding their business operations, some companies are also attempting to reduce costs in the revenue-generation process.

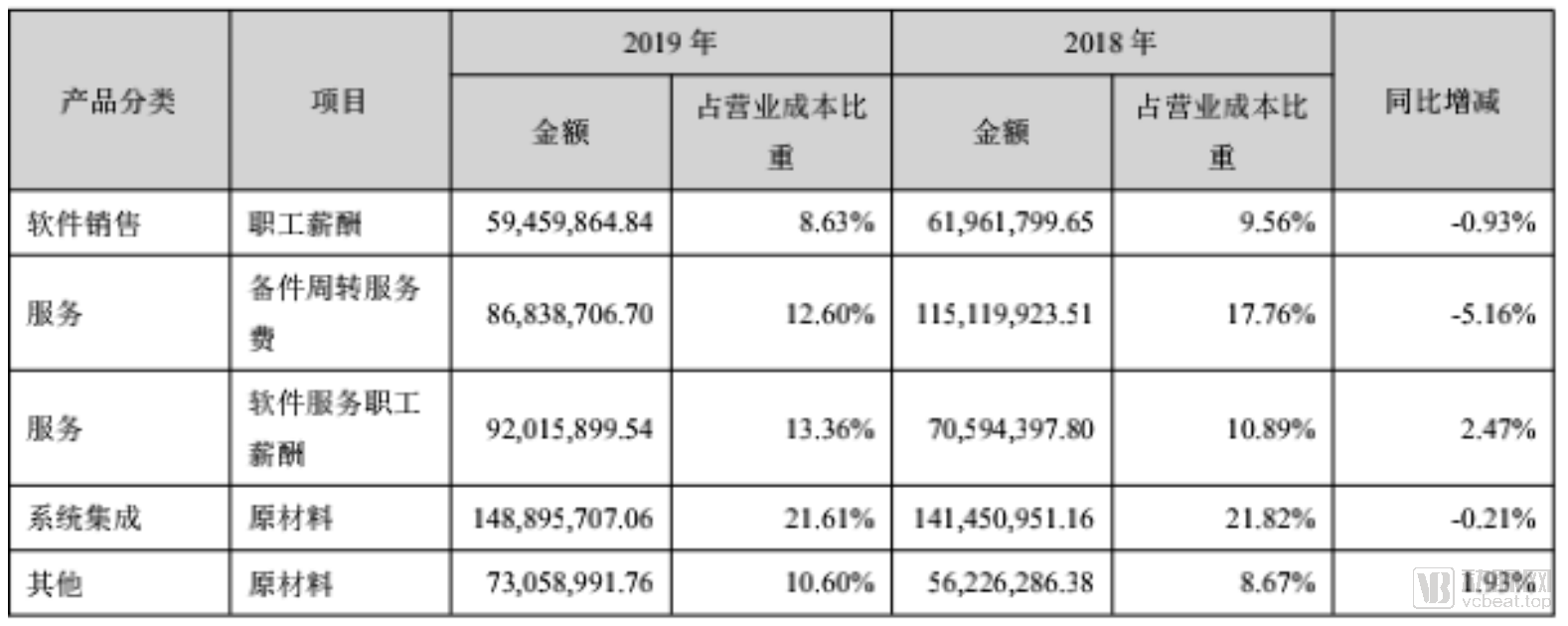

Taking B-Soft as an example, the company achieved a 47.67% profit growth in 2019. The addition of 19 new orders worth tens of millions each contributed significantly to its revenue, while cost reductions also helped boost profits to some extent. These cost cuts mainly stemmed from decreased spare parts turnover service fees and reduced employee compensation for software sales staff.

B-Soft Operating Costs (Data Source: B-Soft 2019 Annual Report)

Das Intellisense and Wonders Information have underperformed in the “Internet + Healthcare” wave over the past two years, with Wonders Information in particular experiencing a significant decline in profits. According to the announcement, the sharp drop in profits was attributed to increased expenditures due to the company’s inability to meet customer demands; product transformation results falling short of expectations; prolonged cash flow turnover cycles caused by fund misappropriation by the former controlling shareholder; and management instability.

Around 2015, both Thinkive Medical and Wonders Information entered the healthcare informatics sector through mergers and acquisitions leading to public listings, achieving rapid performance growth and emerging as leaders in the medical IT field. However, the current turbulence may well become a watershed moment that widens the gap between the two companies.

In contrast, Das Intellitech’s losses are likely to improve as operations gradually recover in 2020, with the deferred orders from 2019 being delivered one by one, and as the newly built “Das Building” begins to generate property-related income.

Return on Equity (ROE)

Since the annual report and the preliminary earnings announcement differ in their calculation basis for net profit, only ROE is estimated here for analysis.

Among the aforementioned companies, B-Soft ranked first with an ROE of 0.8, and its stock price increase further corroborated the company’s strength. Winning Health followed with an ROE of 0.6, a figure on par with that of 2018. The ROEs of other profitable enterprises ranged from 0.1 to 0.4.

As listed IT companies primarily provide informatization solutions, with hospitals as their main clients, a significant proportion of their revenue comes from high-value projects with long cycles. This results in a low accounts receivable turnover ratio, causing the return on equity (ROE) in the medical IT industry to be lower than that of other industries. From this perspective, the aforementioned companies have delivered a satisfactory performance.

In addition to annual reports, some companies have also released preliminary quarterly data. Through these figures, we may be able to roughly estimate the impact of the novel coronavirus on the full-year economy.

Q1 Earnings Forecasts for Listed Companies

For healthcare IT companies, hospitals typically finalize their informatization budgets in the first quarter. Consequently, this data does not accurately reflect the performance of listed companies’ informatization solution businesses; rather, it primarily reflects revenue from SaaS-based services and payment collections from the previous year. This explains the significant variations observed among different companies in the table.

As the epidemic gradually came under control in China, it did not significantly affect the overall level of hospital informatization for the year (although hospital fiscal appropriations may be reduced). Factors such as the expansion of internet hospitals and new infrastructure initiatives at major hospitals in the first quarter are likely to drive an increase in hospital informatization spending in the second half of the year.

Overall, judging solely from the data, the healthcare IT industry continues to show an upward trend, with no signs of stagnation whatsoever. However, there is ultimately a limit to hospitals’ informatization upgrades. According to IDC forecasts, the overall compound annual growth rate (CAGR) of China’s healthcare informatization market from 2017 to 2021 will reach 15.9%. Yet, when broken down by specific segments, Hospital Information Systems (HIS) have lagged behind, with a CAGR of only 8.8%. In contrast, the CAGRs for core healthcare management systems, electronic medical records (EMR), integration platforms and clinical data warehouses, and tiered diagnosis and treatment systems have reached as high as 19.8%, 19.7%, 20.7%, and 25.1%, respectively, all exceeding the industry’s overall growth rate.

Information technology spending at tertiary hospitals accounts for nearly 82.0% of their total expenditures. As this large cohort completes its foundational IT infrastructure, a greater share of spending is shifting toward operations and maintenance, database management, and the development of emerging smart hospital initiatives. New business models are taking shape within these areas.

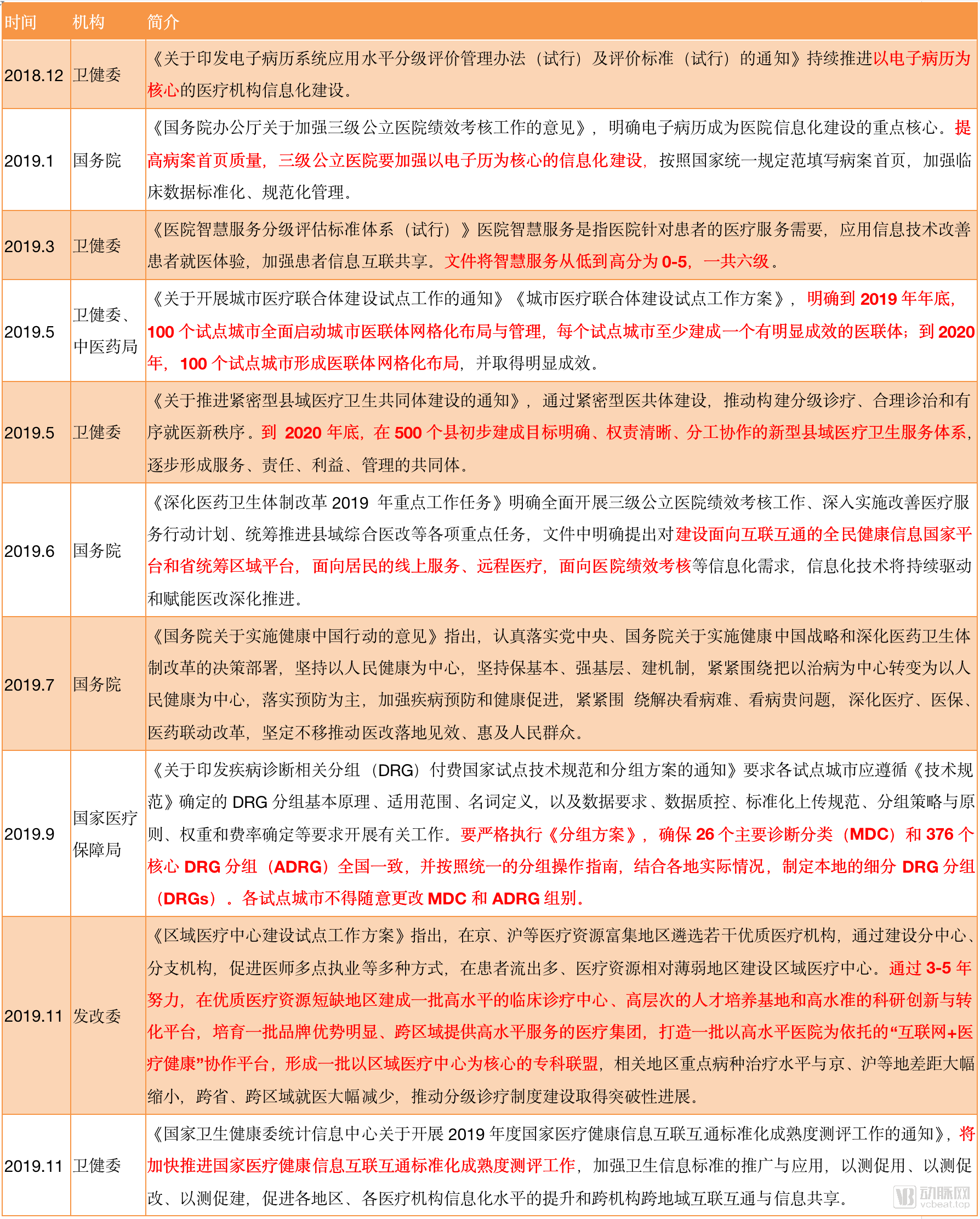

A review of policies reveals that, since December 2018, the Chinese government has progressively heightened its emphasis on hospital informatization. This focus is evident not only in the development of in-hospital information systems—such as electronic medical records (EMR), smart hospitals, and Diagnosis-Related Groups (DRG)—but also in the promotion of models like medical consortia and the new county-level healthcare service system.

2019 Policy Summary

In 2019, more than 7,000 hospitals across China applied for electronic medical record (EMR) system grading. The China Government Procurement Network recorded 227 procurement entries related to EMR systems and health information interoperability, with the publicly disclosed amount reaching RMB 721 million. The market size, measured in billions of yuan, has continued to grow year by year. Based on this trend, the EMR market is expected to maintain several more years of growth potential.

A Closer Look at Smart Hospital Service Ratings and DRGIn March 2019, the State Council issued the Notice on the “Smart Hospital Service Grading and Evaluation Standard System (Trial)”, followed by detailed grading and scoring criteria in July, marking the formal transition of the rating work from planning to implementation. In October 2019, the National Healthcare Security Administration released the technical standard titled “National Healthcare Security DRG (CHS-DRG) Grouping Scheme.” This introduced an official template for DRG (Diagnosis-Related Groups, a payment-by-service-unit model), which had previously seen a proliferation of diverse approaches, and mandated that the 30 cities included in the pilot plan conduct simulated operations in 2020.

But for listed companies, this market is somewhat of a “chicken rib.”

There are not many listed companies engaged in the pre-diagnosis, intra-diagnosis, and post-diagnosis processes; rather, startups are more actively involved in this space. Of course, this path is far from smooth.

“Few hospitals are shifting their focus toward ‘smart transformation’; most are still upgrading their electronic medical record (EMR) systems. This requires substantial investment and effort, so despite policy support, widespread adoption will take time. Moreover, the fact that this rating system is not linked to performance evaluations is also a significant influencing factor,” explained a vendor providing smart healthcare service solutions to VCBeat, noting that demand from hospitals remains unclear.

The supply side also faces challenges. Taking “signage and navigation” within the “in-consultation services” segment as an example, this technology is already highly mature. In Grade A tertiary hospitals such as Shenzhen Nanshan Hospital, users can leverage WeChat mini-programs to navigate precisely to a specific department on a particular floor—a highly practical application. However, achieving such precision demands substantial investment in equipment. To ensure high accuracy and comprehensive coverage, a Bluetooth beacon must be installed approximately every five meters, with each unit costing around RMB 200. These relatively high costs make it difficult for health IT companies to generate profits from this solution.

VCBeat has compiled incomplete statistics on the smart healthcare businesses (covering services involved in Smart Hospital 1.0) of listed companies. The majority of these enterprises still focus their solutions on foundational data management systems, such as Hospital Information Systems (HIS) and Picture Archiving and Communication Systems (PACS), with relatively fewer software developments at the application level.

DRGs are frequently mentioned in the annual reports of major companies, but currently, only three enterprises—Neusoft Wanghai, Ping An Insurance, and Guoxin Health—are capable of providing solutions to regional health commissions. With Neusoft Wanghai now under Ping An’s ownership, none of the traditional healthcare IT listed companies previously analyzed can yet offer a mature solution. Will they miss out on the DRG boom? We may have to wait another six months for the answer.

As mentioned above, the current medical IT industry can be viewed as a superposition of two states. On one hand, supported by policies, hospital information departments are advocating for in-depth informatization reforms, which hospitals also endorse. On the other hand, this demand has been partially met, and a growth ceiling has become apparent; therefore, medical IT companies need to identify new avenues for development.

This superposition manifests specifically in two trends. The first trend is an increase in the number of large-scale informatization orders, which are beginning to be delivered in phases, leading to a consolidation of the fragmented informatization market toward top-tier players.

According to the data released in 2019, B-Soft added 19 new orders worth over RMB 10 million each, while Winning Health added 41 such orders. These EMR-related businesses contributed a significant number of multi-million-yuan orders to both companies.

Furthermore, subsidized by governments at all levels, hospitals are incentivized to purchase more hardware products, including traditional IT equipment and 5G and IoT infrastructure required for new digital infrastructure. These informatization add-ons will generate greater revenue for leading enterprises.

Second, medical IT companies are attempting to enter the internet healthcare sector. As Smart Hospital 1.0 has largely taken shape in terms of technology, more publicly listed companies are turning their attention to Smart Hospital 2.0, which is primarily driven by 5G, cloud computing, and artificial intelligence, with internet hospitals serving as its core platform.

This trend does not mean that these health IT companies will go all out to build internet hospitals. On the contrary, they may stay out of direct-to-consumer (To C) businesses and instead leverage their connections with hospitals to secure early-mover advantages. By building technical middle platforms for hospitals and enterprises that need to develop internet hospitals, they can ultimately establish long-term relationships centered on SaaS services.

Under the SaaS model, listed companies will be better positioned to leverage their traffic advantages on the hospital side, provide operational support, and maintain strong connections with hospitals. This enables them to offer more value-added services while achieving a smoother balance sheet.

Judging from the current situation, listed companies have not progressed at a uniform pace in building their internet healthcare capabilities, and their business models vary. Among them, Winning Health has made a notable and successful attempt.

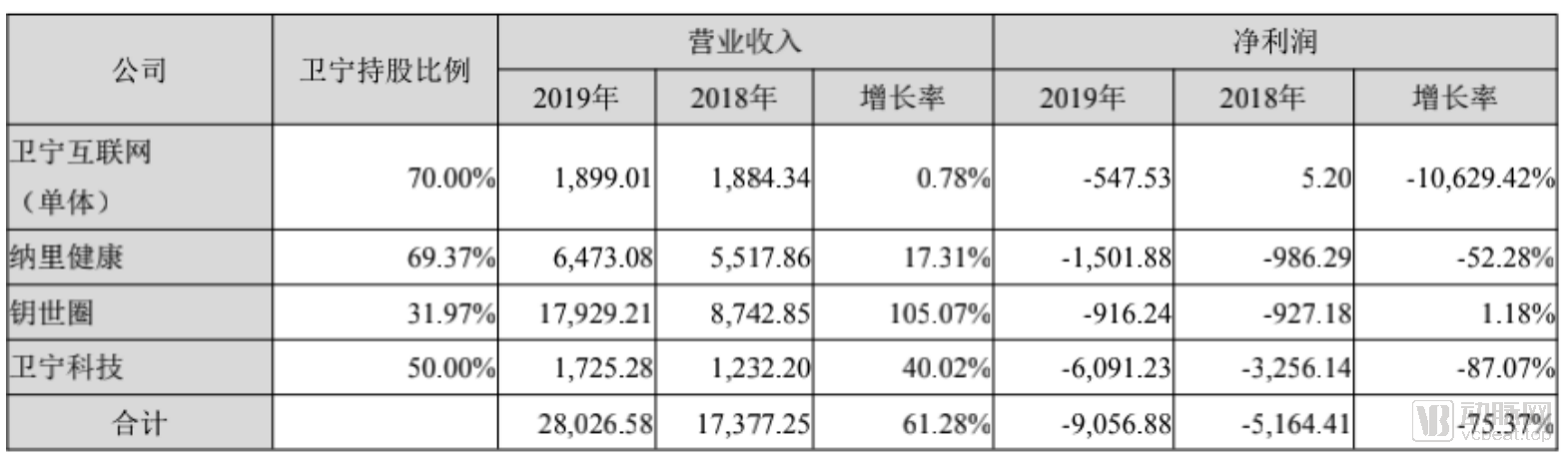

According to the annual report, KeyShiQuan, a “pharmaceutical consortium” centered on “Cloud Pharmacy” and integrating “prescription circulation, insurance-pharmacy linkage, B2B empowerment, and health services,” has experienced rapid growth, with its revenue accounting for nearly one-tenth of Winning Health’s total revenue.

In contrast, although Nali Health’s new “Internet + Healthcare Services” model has cumulatively signed contracts for 462 medical projects, connected with more than 4,000 domestic medical institutions (including 89 internet hospitals that have obtained medical institution practice licenses through cooperative co-construction models), and served over 200 million patient visits, it continues to incur losses.

The rapid growth of Yaoshiquan is closely tied to Winning Health’s own pharmaceutical sales. Relevant sources indicated that Winning Health obtained the qualification to sell drugs to small and medium-sized pharmacies. Taking Shanghai Yaoshiquan Cloud Health Technology Development Co., Ltd. as an example, it acquired the drug wholesale and retail license through its indirect controlling stake in Chongqing Nuodazhi Pharmaceutical Co., Ltd. Coupled with its inherent advantage in driving patient flow from hospital informatization systems, Yaoshiquan’s B2B model has become a core contributor to its revenue.

Of course, Cloud Healthcare and Cloud Insurance have also made significant contributions to connectivity. During the reporting period, Cloud Insurance expanded its coverage to hundreds of additional medical institutions, with new transaction volume exceeding RMB 21 billion (cumulative transaction volume has surpassed RMB 30 billion) and more than 97 million new transactions.

In December 2019, China Life Health Industry Fund injected an additional RMB 200 million in capital into the company, laying a solid foundation for its subsequent accelerated development.

Overall, SaaS services are still in the development phase, so current financial reports mostly show losses. However, as this segment of the business matures, its marginal costs will continue to decline. Therefore, this model is highly likely to become the core business for future healthcare IT companies.

Synthesizing annual report data, policy trends, and industry trends, VCBeat has compiled the following insights:

1. The epidemic will, to a certain extent, hinder product sales for health IT companies, primarily manifested in delayed delivery of existing orders and reduced hospital fiscal spending; however, as the outbreak is contained, the financial statements of medical IT enterprises will gradually return to normal;

2. Hospitals’ emphasis on informatization will attract more talent to their information technology departments. In this context, hospitals will put forward more precise and personalized demands for medical IT enterprises, which must enhance their business capabilities to cope with the rapidly developing market;

3. The upgrading of electronic medical records (EMR) and interoperability systems will persist for an extended period, leading to further consolidation of market share in the healthcare IT sector, with leading enterprises securing more mega-contracts valued at hundreds of billions. Meanwhile, primary care institutions will also embark on their informatization initiatives, creating opportunities for startups to carve out their own niche.

4. Smart hospital-related businesses are fragmented and niche, and are not currently a primary focus of hospital investment. Although policies promoting smart hospital service ratings are being advanced, it will take some time before the sector reaches maturity;

5. Over the next few years, the proportion of revenue from SaaS-based services will gradually increase. The “Internet+” businesses of healthcare IT companies will extend to a broader range of B-side medical clients, such as by building internet hospital platforms, e-commerce platforms, and commercial insurance platforms. In particular, with hospitals increasingly developing their own internet hospitals, providing SaaS technical support to these institutions can strengthen ties with them and facilitate the rollout of additional services in the future.

In summary, policy remains the “source” that healthcare IT must focus on. However, due to the proliferation of diverse policy offshoots in recent years, enterprises should not follow policies blindly. Instead, they must identify the points where hospital needs and policy directives align most closely to avoid unnecessary detours.

The impediments to informatization caused by the pandemic can hardly be considered a challenge; clarifying how to interpret policies and understand hospital needs, thereby formulating future development paths for enterprises, is perhaps the most critical step for medical IT companies at this stage.