Junshi Biosciences Submits Registration for STAR Market IPO with 2019 Revenue of RMB 770 Million Driven by Toripalimab

Junshi Biosciences

Innovative Drug Developer

On April 29, VCBeat learned that Junshi Biosciences has formally submitted its “Prospectus (Registration Draft)” to the STAR Market of the Shanghai Stock Exchange, bringing it one step closer to becoming the first company with a “3+H+A” listing structure.

Junshi Biosciences’ HK Stock Performance (Image from Tiger Brokers)

For this IPO application, Junshi Biosciences plans to issue no more than 87.13 million shares. With its current share price on the Hong Kong Stock Exchange at HK$37.4 per share, the company is expected to raise nearly RMB 3 billion through its listing on the STAR Market.

Junshi Biosciences is an innovation-driven biopharmaceutical company. One of its core products, JS001, has been approved for marketing and is indicated for the treatment of locally advanced or metastatic melanoma after failure of prior standard therapy. Clinical trials are currently underway to expand its indications. The New Drug Application (NDA) for UBP1211 (a biosimilar to Humira) has been submitted and accepted. JS002 (recombinant humanized anti-PCSK9 monoclonal antibody injection) is currently in Phase II clinical trials.

In 2019, Junshi Biosciences generated revenue of over RMB 770 million, driven by sales of its PD-1 monoclonal antibody, Tuoyi. The cost of sales amounted to RMB 320 million, accounting for approximately 40% of total revenue, which is broadly in line with the normal range of selling expenses for innovative drugs. However, its R&D expenditures have been growing rapidly. From 2017 to 2019, Junshi Biosciences’ R&D spending increased from RMB 275 million to RMB 946 million, representing a growth rate of nearly 100%. The overall loss remained largely flat compared with 2018, with a slight increase.

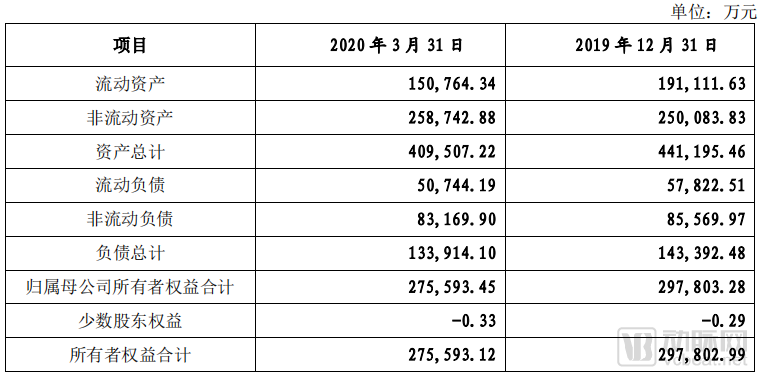

At present, Junshi Biosciences’ asset position remains relatively healthy. As of March 31, 2020, its current assets exceeded RMB 1.5 billion, and total assets surpassed RMB 4 billion. Total liabilities amounted to approximately RMB 1.3 billion, with a debt-to-asset ratio of around 32.5%.

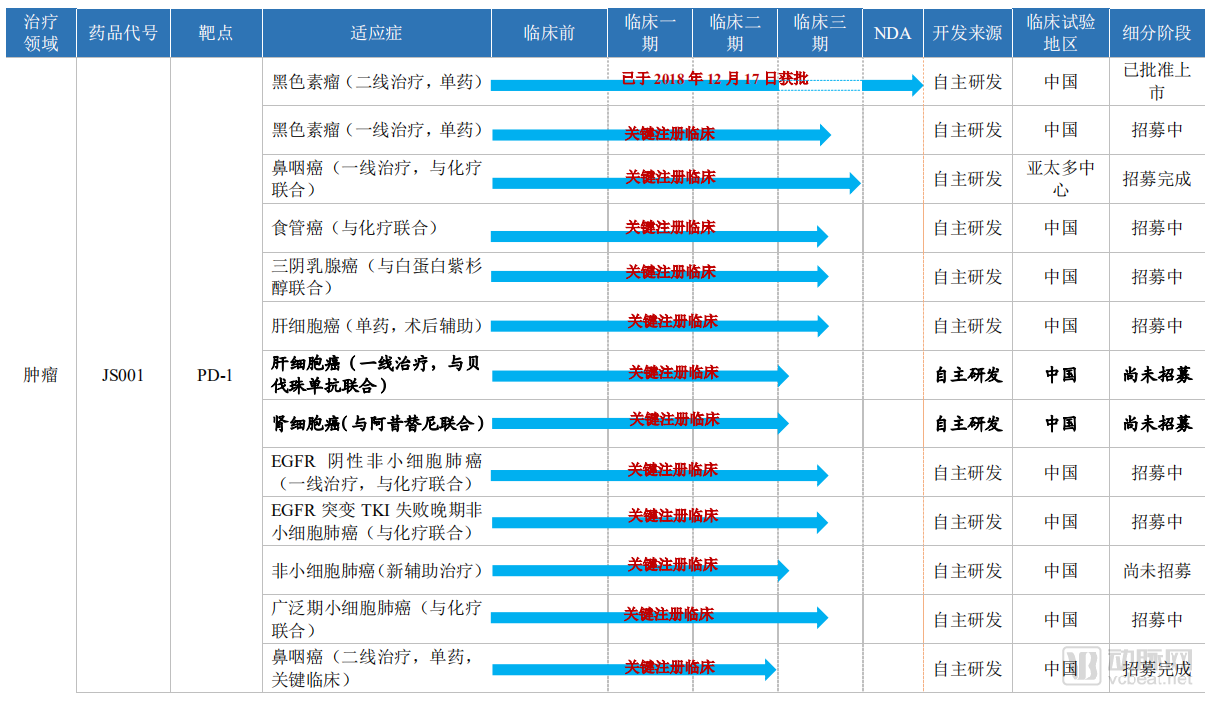

The Company’s products primarily consist of innovative biologics, most of which are original innovations developed in-house. Meanwhile, the Company has introduced products through collaborative development that synergize with its proprietary product portfolio, thereby strengthening its product pipeline. As of the date of this prospectus, one of the Company’s products has received conditional marketing approval from the National Medical Products Administration (NMPA). In addition, including research on expanded indications for this marketed product, the Company has a total of 21 products under development, comprising 19 innovative drugs and 2 biosimilars.

Junshi Biosciences’ flagship product, Tuoyi, has already launched 14 pivotal clinical trials in addition to its approved primary indication of melanoma. This signifies that Tuoyi will rapidly expand its range of indications in the coming years, thereby widening the gap with its competitors.

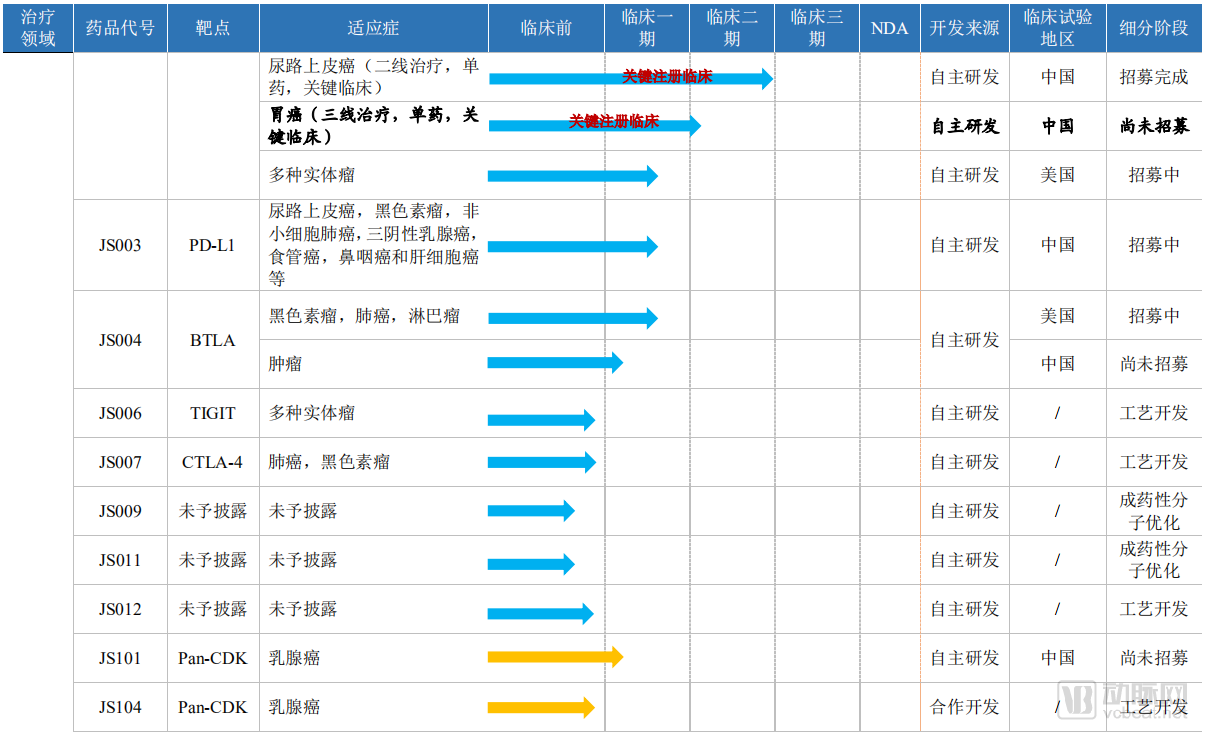

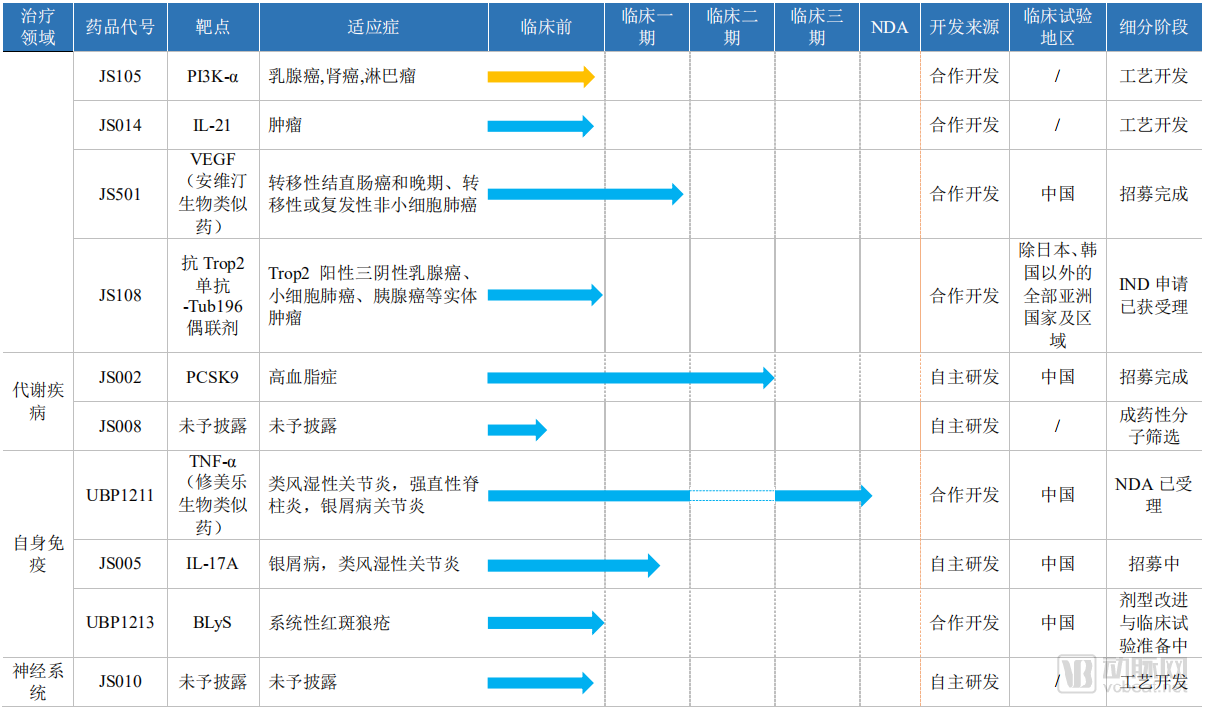

In addition to toripalimab, Junshi Biosciences has a total of eight products in clinical trials. As of March 31, 2020, the ranking of its clinical trials is as follows:

Junshi Biosciences’ UBP1211 (a biosimilar to Humira) was the fifth product in its class to submit a marketing authorization application. According to Frost & Sullivan, the market size for Humira biosimilars in China is expected to reach RMB 4.7 billion in 2023 and grow to RMB 11.5 billion by 2030. This substantial market size can accommodate competition among multiple companies.

JS002 is the first domestic product to receive clinical trial approval for a PCSK9 target and enter clinical development in China. Currently, JS002 has completed patient enrollment for its Phase II clinical trial, placing it at the forefront of the market.

JS003 (an anti-PD-L1 monoclonal antibody) lags behind its domestic competitors, but preclinical studies suggest that the drug may have a favorable safety and efficacy profile. Junshi Biosciences plans to evaluate the commercial viability of further development based on preliminary clinical safety and efficacy data upon completion of Phase I clinical trials.

Product JS004 (anti-BTLA monoclonal antibody) is the first anti-tumor drug targeting this site to receive clinical trial approval globally, and it is currently undergoing Phase I clinical trials in both China and the United States.

JS005 (anti-IL-17A monoclonal antibody) targets a key pathway in autoimmunity, with psoriasis as its primary indication. In the Chinese market, Junshi Biosciences’ product holds a leading position. Meanwhile, the company can leverage the synergistic and complementary effects of its adalimumab biosimilar and IL-17A inhibitor. Notably, competitors ahead of Junshi Biosciences have not developed adalimumab biosimilars.

JS501 (a bevacizumab biosimilar) ranks among the top ten domestic companies in this field. However, given its strong potential for combination therapy with PD-1 inhibitors as a VEGF monoclonal antibody, as well as its excellent efficacy as a monotherapy in major indications such as lung cancer and colorectal cancer, the drug still holds significant commercial value. The company will leverage its manufacturing advantages in large-molecule drugs and the synergistic benefits of combination therapy with PD-1 inhibitors to gain a competitive edge.

Overall, Junshi Biosciences’ R&D pipeline is centered on Tuoyi (toripalimab), forming a comprehensive, tiered product portfolio. The biosimilar UBS1211 has already been submitted for marketing approval and is likely to become the second product launched by Junshi Biosciences after Tuoyi. However, as all marketed products face competition from multiple similar agents, Junshi Biosciences will encounter substantial competitive pressures in its future development.