From Storage to Therapy: A Comprehensive Report on the Mesenchymal Stem Cell Industry

By Probe Capital

Stem Cells

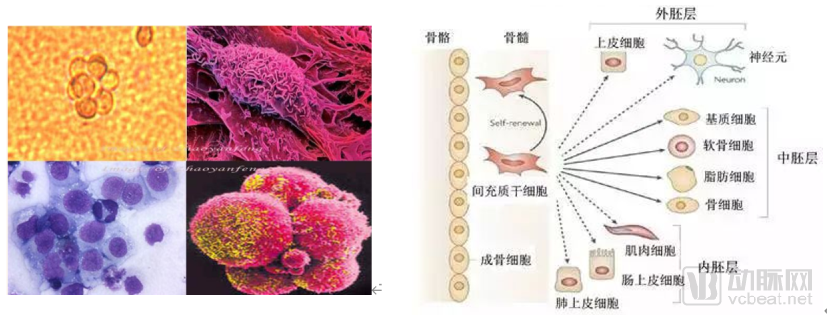

Stem cells are a population of primitive cells that are structurally and functionally undifferentiated, possessing the capacity for self-renewal, robust proliferation, and multipotent differentiation. They are widely distributed in various tissues and organs throughout the body, such as bone marrow, peripheral blood, early embryos, and adult tissues. The human body comprises more than 220 types of cells, which are organically integrated to form complex tissues and organs, each with specific functions—for example, the contractile function of cardiomyocytes and the signal transmission function of neurons. Stem cells serve as the progenitor cells for these specialized cells and are referred to by the medical community as "universal cells." Taking bone marrow mesenchymal stem cells as an example, under specific induction conditions in vivo or in vitro, they can differentiate into various tissue cells, including adipocytes, osteoblasts, chondrocytes, myocytes, tenocytes, ligament cells, neural cells, hepatocytes, cardiomyocytes, and endothelial cells.

Figure: Stem Cell Morphology and Differentiation Potential Source: Publicly available information

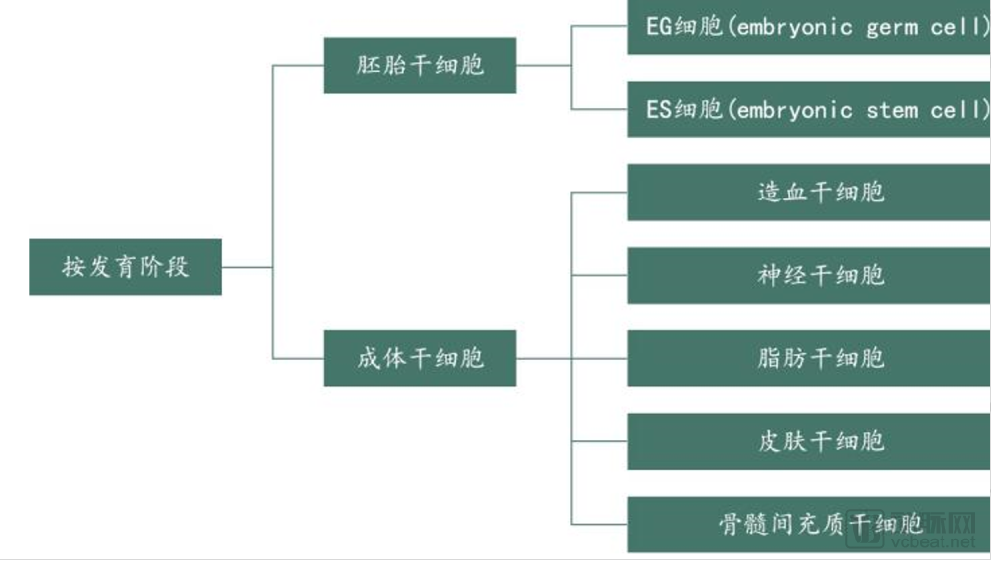

Based on cell origin and developmental stage, stem cells can be classified into embryonic stem cells (ESCs) and adult stem cells (ASCs). ESCs are cells isolated through in vitro culture and selection from the inner cell mass of embryos or primordial germ cells. They possess the characteristics of unlimited proliferation, self-renewal, and multipotent differentiation in vitro, while maintaining high telomerase activity and normal cell signaling pathways, enabling rapid proliferation. ASCs are undifferentiated cells present within differentiated tissues of mature individuals. They have the capacity for self-renewal and can differentiate into all cell types originating from their tissue of residence. Examples include hematopoietic stem cells, neural stem cells, and mesenchymal stem cells.

Studies have shown that adult stem cells (ASCs) can not only differentiate into lineage-specific cells but also into cells of other lineages that are developmentally unrelated, suggesting that ASCs possess substantial differentiation potential and can play a significant role in the treatment of various conditions, including tissue repair. It is generally believed that embryonic stem cells (ESCs) are pluripotent and capable of differentiating into various tissues and organs, whereas ASCs were thought to have only specific, lineage-restricted differentiation capacity. However, advances in research on induced pluripotent stem cells (iPS) have challenged this view, demonstrating that under certain induction conditions, ASCs can exhibit pluripotency comparable to that of ESCs.

Figure: Classification of stem cells by developmental stage Source: Public information

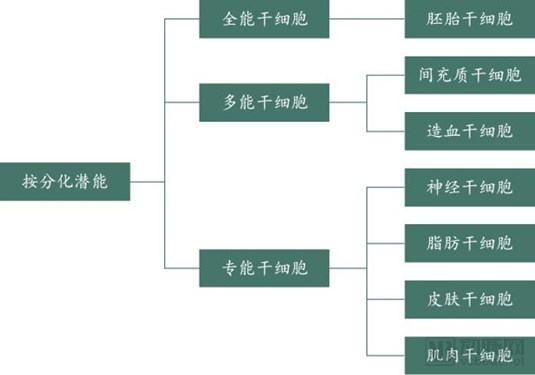

Based on differentiation potential, they can be classified into totipotent stem cells (TSCs), pluripotent stem cells (HSCs), and unipotent stem cells (USCs).

Pluripotent stem cells (such as embryonic stem cells) can differentiate into any cell type in the body. With the greatest differentiation potential, they are the optimal materials for studying histogenesis and organ function repair. However, their application faces challenges, such as the risk of teratoma formation and socio-ethical concerns.

Pluripotent stem cells possess multilineage differentiation potential and are currently a major focus of research both domestically and internationally; in particular, mesenchymal stem cells are the most extensively studied and clinically applied stem cells to date.

Unipotent Stem Cells (USCs) are stem cells with the capacity for lineage-specific differentiation, typically differentiating into only one specific cell type, such as neural stem cells (NSCs). Since tissues and organs have undergone initial differentiation by the gastrula stage of embryonic development, stem cells present after this stage are restricted to being unipotent. Additionally, certain cells found in fetal umbilical cords or adult bone marrow are also classified as unipotent stem cells; although their differentiation potential is limited, they possess self-renewal capabilities, distinguishing them from highly differentiated non-stem cells.

Figure: Classification of Stem Cells by Differentiation Potential. Source: Public Information

Mesenchymal Stem Cells

In 2006, the International Society for Cellular Therapy (ISCT) standardized the definition of mesenchymal stem cells. Only cells that simultaneously meet the following three criteria can be termed mesenchymal stem cells: ① adherence to plastic under standard culture conditions; ② expression of specific surface antigens (markers); and ③ differentiation potential into adipocytes, osteoblasts, and chondrocytes.

Mesenchymal stromal/stem cells (MSCs) originate from the mesoderm and ectoderm during early development. As multipotent stem cells, they possess the capacity for multidirectional differentiation and can differentiate into various tissue cells, including adipocytes, osteoblasts, chondrocytes, myocytes, tenocytes, ligament cells, neural cells, hepatocytes, cardiomyocytes, and endothelial cells. MSCs are primarily distributed throughout the connective tissues and organ stroma of the body, with the highest abundance found in bone marrow tissue.

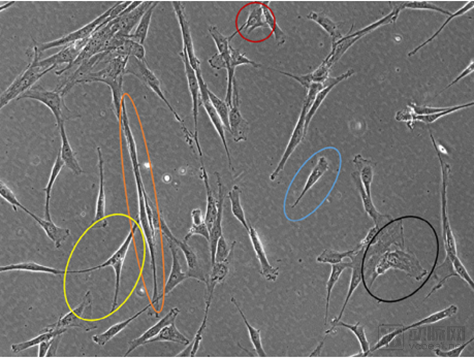

Mesenchymal stem cells retain their multipotent differentiation and self-renewal capabilities after serial passaging and cryopreservation. Studies have shown that human bone marrow-derived MSCs can maintain their stem cell characteristics for over 40 passages in vitro. Bone marrow mesenchymal stem cells exhibit heterogeneity in size and shape, including tripolar, elongated spindle-shaped, small round, short spindle-shaped, and flat morphologies.

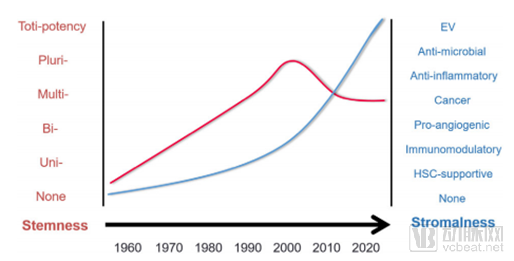

Currently, the debate over the “stemness” versus “stromality” of mesenchymal stem/stromal cells (MSCs) has diminished. Since the 1960s, accumulating data on their proliferative and differentiation capacities have supported the “stemness” of MSCs, reaching a peak around the year 2000. Since then, evidence supporting the “stromality” of MSCs has gradually increased. We define “stromality” based on tissue-supportive functions (such as support for hematopoietic stem cells), which involves various growth factors, chemokines, cytokines, and extracellular vesicles.

Figure: Morphology of MSCs. Source: Stem Cells Translational Medicine

Figure: Stemness and Stromal Properties of MSCs Source: Stem Cells Translational Medicine

Compared with other stem cells, mesenchymal stem cells (MSCs) offer advantages such as ease of acquisition, facile in vitro culture, long-term stability during passaging, low immunogenicity, and potent tissue repair capabilities. Furthermore, MSCs are derived from adult cells and can even be harvested from the patient’s own body, rather than from embryonic or fetal stem cells, thereby avoiding moral and ethical concerns.

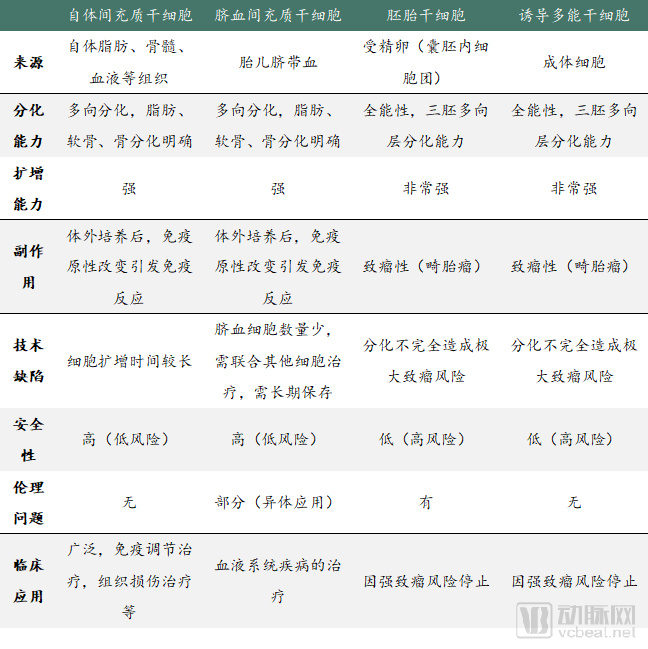

Table: Comparison of Several Types of Stem Cells Source: Compiled from Public Information

Bone marrow mesenchymal stem cells are early-stage cells of mesodermal origin. They represent a distinct population of stem cells in the bone marrow, separate from hematopoietic stem cells. These cells possess the common characteristics of stem cells, namely self-renewal and multipotent differentiation capacity. They exhibit fibroblast-like growth patterns and can differentiate into hematopoietic stromal cells, as well as numerous non-hematopoietic tissues. Specifically, they can differentiate into mesodermal lineages such as osteoblasts, chondrocytes, adipocytes, tenocytes, cardiomyocytes, endothelial cells, and hepatic and biliary epithelial cells, as well as pulmonary epithelial cells. Furthermore, they hold the potential to differentiate into ectodermal neuronal cells and endodermal hepatic oval cells.

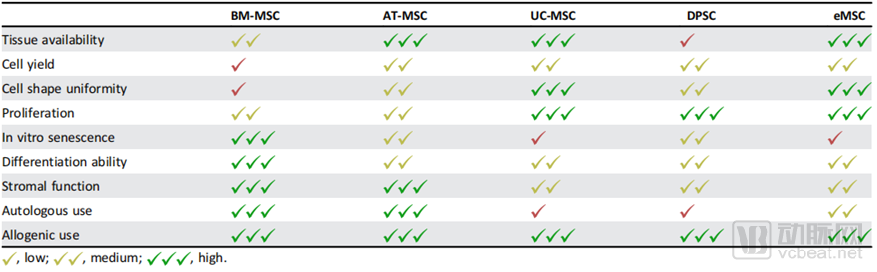

Multiple studies have demonstrated that upon in vivo transplantation, bone marrow-derived mesenchymal stem cells (MSCs) can home to various non-hematopoietic tissues, such as the lungs, bones, cartilage, and skin, and differentiate into corresponding tissue-specific cells. In vitro, bone marrow MSCs exhibit fibroblast-like colony-forming units and adhere to the culture surface for growth. Further cell cycle analysis reveals that approximately 10% of cultured MSCs are in the active replication phase (S+G2+M phases), while the vast majority remain arrested in the G0/G1 phase. Although the specific checkpoints and durations of each cell cycle phase have not yet been fully elucidated, the high proportion of cells in the G0/G1 phase indicates a strong potential for differentiation. Notably, while MSCs from different sources share core attributes, they also exhibit distinct differences.

Table: Comparison of MSCs from Different Sources Source: Stem Cells Translational Medicine

Note: BM-MSCs: bone marrow mesenchymal stem cells; AT-MSCs: adipose tissue-derived mesenchymal stem cells; UC-MSCs: umbilical cord-derived mesenchymal stem cells; DPSCs: dental pulp stem cells; eMSCs: endometrial mesenchymal stem cells

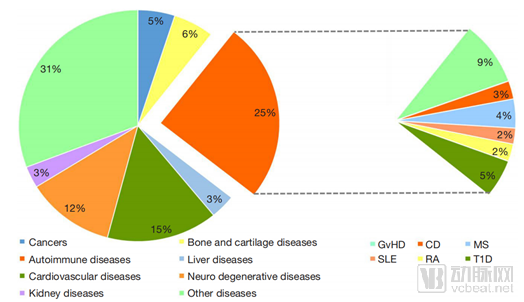

Mesenchymal stem cells (MSCs) possess diverse functions and wide-ranging applications. Their primary role is in cell transplantation therapy, while they also serve as ideal target cells for gene therapy and have applications in tissue engineering and immunotherapy. In recent years, MSCs have been extensively utilized in experimental and clinical research. A substantial body of studies has demonstrated their diagnostic and therapeutic value in diseases affecting the cardiovascular, nervous, musculoskeletal, digestive, hematopoietic, urinary, and ophthalmic systems, as well as in autoimmune disorders and orthopedic conditions.

Table: Percentage Analysis of Common Diseases in MSC-Based Cell Therapy. Source: Stem Cell Investigation

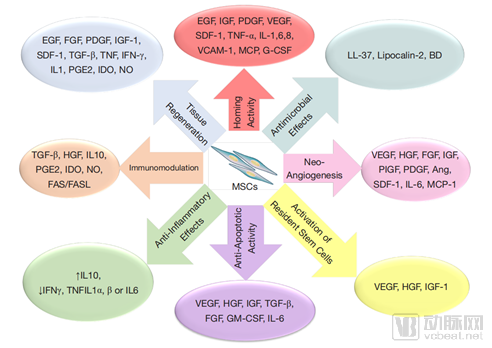

The mechanisms underlying mesenchymal stem cell (MSC) transplantation therapy are complex, involving the interplay of various processes such as homing, tissue repair and regeneration, immunomodulation, anti-inflammation, anti-apoptosis, pro-angiogenesis, immune cell activation, and antimicrobial activity. For indications including immune disorders and cardiovascular/cerebrovascular diseases, MSC therapy is generally believed to exert its therapeutic effects primarily through paracrine signaling or direct cell-to-cell interactions, thereby providing immunosuppressive effects, reducing fibrosis, and promoting vascular and tissue regeneration.

Figure: Overview of the Therapeutic Mechanisms of Bone Marrow Mesenchymal Stem Cells. Source: Stem Cell Investigation

The Hundred-Billion-Dollar Market for Stem Cell Therapy

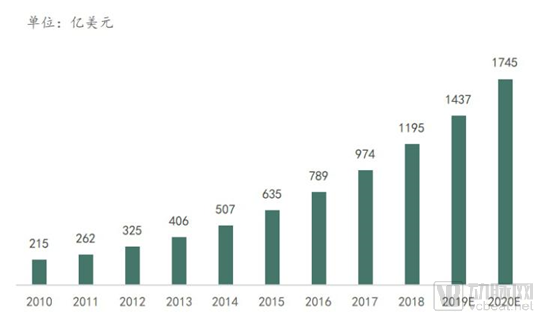

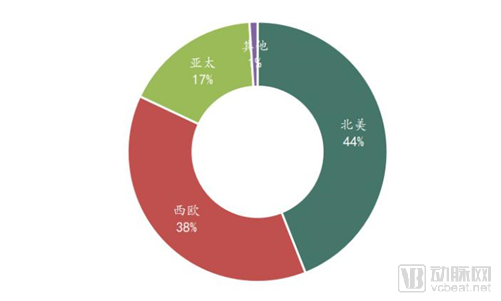

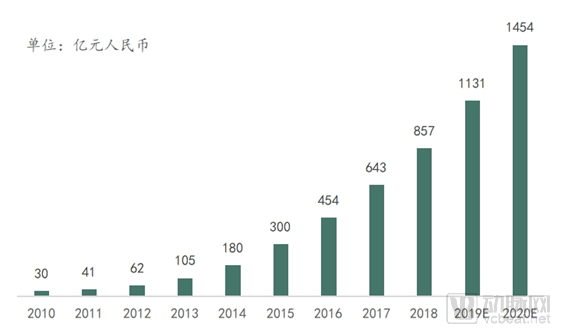

Due to their robust capabilities for self-renewal and differentiation, as well as effective regulatory mechanisms, stem cells can be directed to differentiate into one or multiple types of cellular tissues. They are widely applied in fields such as disease treatment, organ transplantation, tissue repair, and medical aesthetics. The global stem cell market is substantial in scale. According to studies by Market Research and Transparency Market Research, the global market was projected to exceed $170 billion in 2020. In terms of market distribution, North America constitutes the largest stem cell market globally, while Western Europe and the Asia-Pacific region account for 38% and 17% of the market share, respectively. Data from the Qianzhan Industry Research Institute indicates that the market size of China’s stem cell therapy industry will surpass RMB 140 billion in 2020, with a compound annual growth rate (CAGR) exceeding 30%.

Figure: Global Stem Cell Therapy Market Size, 2010-2018

Sources: Market Research, Transparency Market Research, Firestone Creation

Figure: Market Share by Region Worldwide

Source: Transparency

Figure: Market Size of Stem Cell Therapy in China, 2010–2024

Sources: Market Research, Transparency Market Research, Firestone Creation

Policy, Technology, and Demand Drive the Development of China's Stem Cell Industry

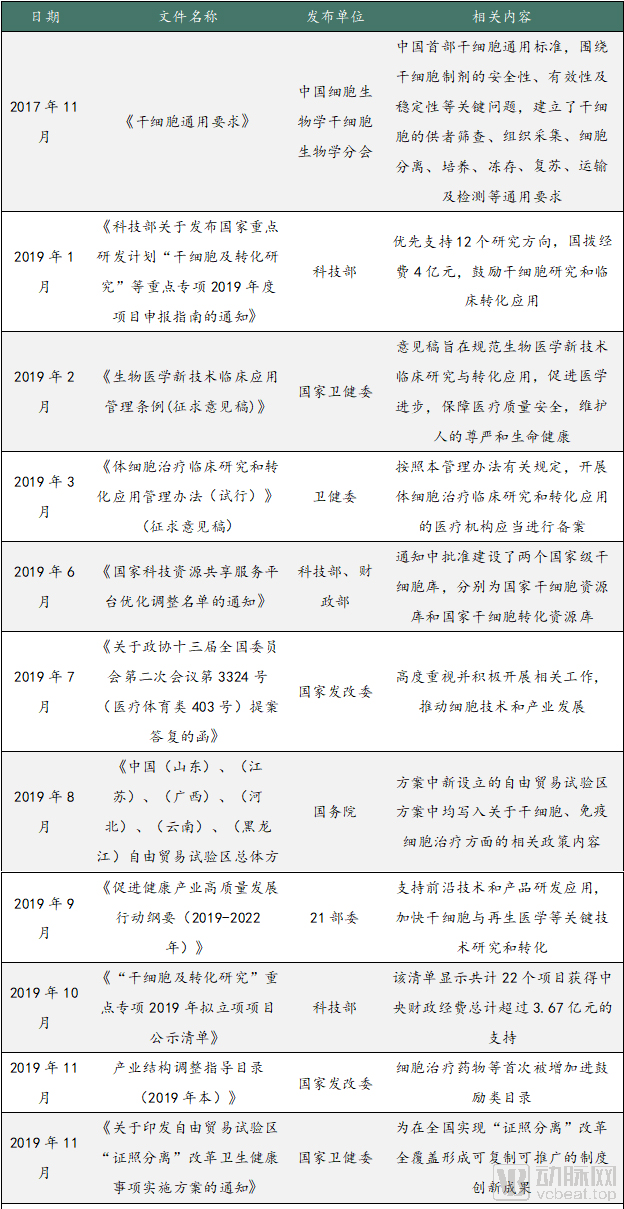

Global policies on the stem cell industry vary in stringency, with North America and Europe being particularly active. In the United States, restrictions on embryonic stem cell research were lifted just one month after President Obama took office. The FDA established a fast-track approval pathway to encourage clinical researchers to rapidly secure a leading position in clinical stem cell therapies, while multinational corporations have increased their investments to strategically position themselves across the stem cell industry chain. Since 2015, China has significantly strengthened policy support, promoting industry development through standardized regulation, technical assistance, and financial backing. Technologically, stem cells have remained a focal point of research, with continuous breakthroughs being achieved. Demand-driven growth is the fundamental force behind the development of the stem cell industry, as the clinical application of stem cells holds promise for resolving a series of medical challenges, including leukemia, AIDS, and diabetes.

In recent years, national policies supporting the stem cell industry have been continuously strengthened, and the clinical application of stem cells is entering a period of rapid and standardized development. Specific policies are listed in the table below. A “dual-track” regulatory model is adopted, whereby products are submitted for clinical trials either as “Class III Medical Technologies” or as “New Drugs,” depending on their attributes. “Class III Medical Technologies” primarily cover autologous adult stem cells and one-to-one allogeneic adult stem cells (from a single donor to a single recipient), which are regulated by the National Health Commission (NHC). “New Drugs” mainly refer to allogeneic adult stem cells derived from a single donor for use in two or more recipients, which are regulated by the National Medical Products Administration (NMPA).

Global R&D Sees Undercurrents Surge, Singularity Breakthrough Imminent; China’s Research Level Leads the World.Technological innovation is the core driver of development in the stem cell industry and the primary means to address the weakness of China’s mid- and downstream industrial chains. Globally, various approaches are being employed to develop stem cells and related products, actively translating stem cell research achievements into practical applications.

In 2016, China announced the first batch of 30 clinical research institutions for stem cells. Starting in 2019, dynamic management was implemented for the filing of stem cell clinical research institutions and projects. As of September 2019, the number of hospitals approved by the state for stem cell clinical therapeutic research increased to 106, with an additional 12 hospitals approved within the military medical system, totaling 118 institutions. The number of filed projects rose to 62, and patent applications related to literature research continued to grow. By March 2020, the number of stem cell-related clinical studies registered on ClinicalTrials.gov had reached 5,432, including 469 from China. The cities with the most active research were Guangzhou, Beijing, and Shanghai.

With the rapid advancement of stem cell technology, global pharmaceutical giants such as Bayer, Celgene, GlaxoSmithKline, and Pfizer have emerged among the applicants conducting clinical trials in China. Significant progress has also been made in China across various disease areas, including stem cell therapies for osteoarthritis, diabetic foot, acute myocardial ischemia, thalassemia, and Parkinson’s disease. However, due to regulatory constraints, the only segment of the domestic stem cell industry chain currently generating short-term cash revenue is cell storage.

Current basic research in the field of stem cells mainly focuses on the following aspects: cell reprogramming research, studies on the mechanisms of stem cell self-renewal and maintenance of pluripotency, research on novel pluripotent stem cells, and studies on directed differentiation of stem cells and their regulatory mechanisms.

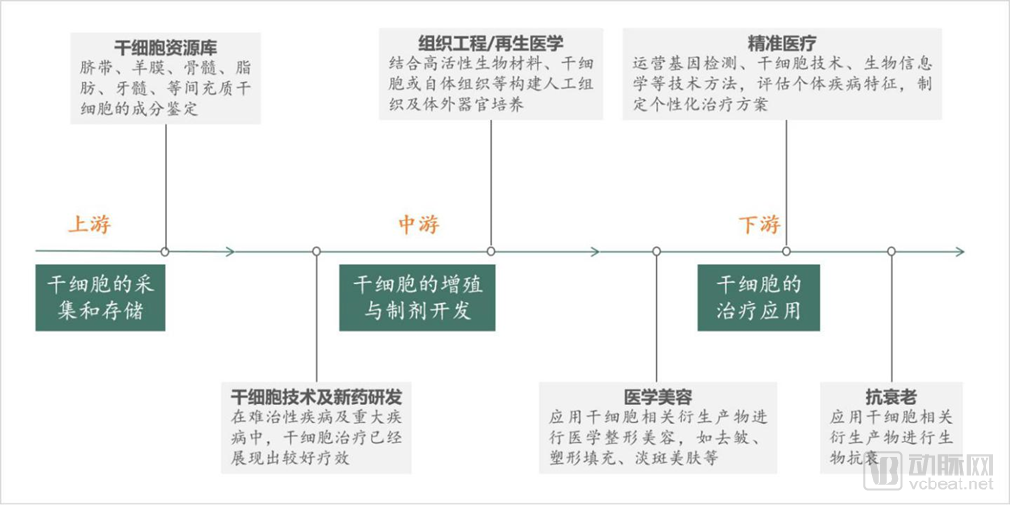

Stem Cell Industry Chain: Upstream Maturity, Mid- and Downstream Applications as Key Future Focus

The stem cell industry chain is primarily divided into three segments: upstream (stem cell collection and storage), midstream (stem cell expansion and R&D of novel stem cell drugs), and downstream (stem cell therapy).

High technological barriers have slowed the development of China’s stem cell industry. Compared with leading countries in Europe and the United States, China’s stem cell sector remains an emerging industry characterized by a fragmented competitive landscape, low industrial maturity, and the absence of dominant market leaders. While more than ten stem cell therapeutic products have been approved for marketing abroad, China lags behind. Most domestic companies are concentrated in the upstream storage segment; although research and application in the mid- and downstream sectors are accelerating, clinical translation has not yet been achieved, and the industry remains in its early stages of accumulation and development.

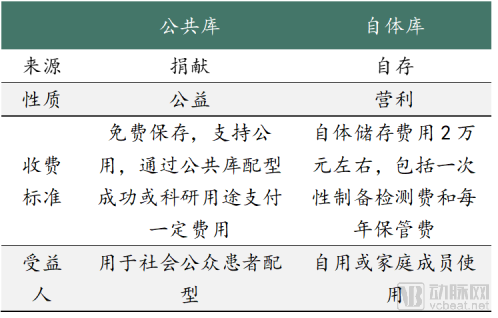

The upstream segment of the industry chain refers to stem cell collection and storage services, which currently represent the most significant and mature industrialized applications in the stem cell field. This segment primarily consists of umbilical cord blood banks, which are categorized into public and private banks. Public banks are subject to licensing restrictions (currently, only 10 provinces in China have licensed public banks), whereas private banks face no such licensing constraints.

The primary targets for collection include umbilical cord blood stem cells, umbilical cord mesenchymal stem cells, fatty liver cells, amniotic membrane, and other stem cell materials. Among these, the collection and storage of umbilical cord blood stem cells is currently the main focus (umbilical cord blood stem cells cannot proliferate, and their quantity is sufficient only for children under five years of age).

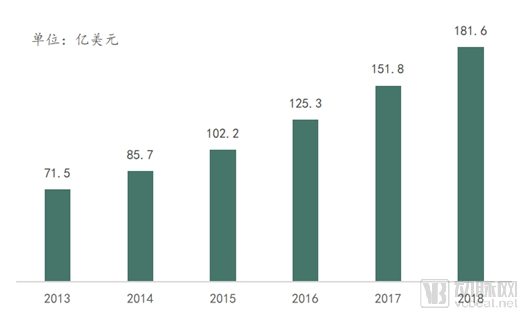

This segment of the industry chain features relatively low technical requirements, low barriers to entry, a mature development stage, and high gross profit margins. According to data from Zhiyan Consulting, the global scale of stem cell storage reached $18.16 billion in 2018. However, China’s overall stem cell storage rate is currently less than 1%, representing a significant gap compared to the 10%–15% rates observed in developed countries. This indicates substantial growth potential for the domestic storage market. Based on an annual cohort of 15 million newborns and assuming a future storage rate comparable to the minimum 10% seen in developed nations, and given that domestic umbilical cord blood banking fees are approximately RMB 20,000 per case (RMB 1,000 per year over 20 years), the corresponding market size would reach RMB 30 billion.

Figure: Global Stem Cell Storage Market Size, 2013-2018

Source: Zhiyan Consulting

Source: Public information

Currently, listed stem cell companies in China still focus primarily on storage services, with stem cell storage representing the dominant business model. The upstream stem cell storage sector is mainly dominated by enterprises such as Vcanbio, Nanjing Xinjiekou Department Store Co., Ltd., and Goldwind Medical, while the remaining market players are relatively fragmented. Future development of the upstream industry will expand upon existing stem cell banks by diversifying the types of stored cells. Meanwhile, companies relying solely on stem cell storage as their single line of business are highly likely to be acquired and integrated.

The midstream segment of the industrial chain focuses on stem cell expansion and the development of novel stem cell-based therapeutics. This generally involves the extraction and expansion of stem cells, followed by their formulation into preparations or pharmaceutical products suitable for clinical application. Characterized by high technical barriers and significant potential, this sector has seen more than ten stem cell products launched globally, with over half derived from mesenchymal stem cells (MSCs), while numerous other candidates remain in various stages of research and development. Although China’s stem cell drug development is still in its early stages, substantial research has been conducted in clinical applications such as MSCs. However, the lack of corresponding policies in the earlier phases has led to relatively lagging clinical translation, and no commercially approved products have been officially authorized to date.

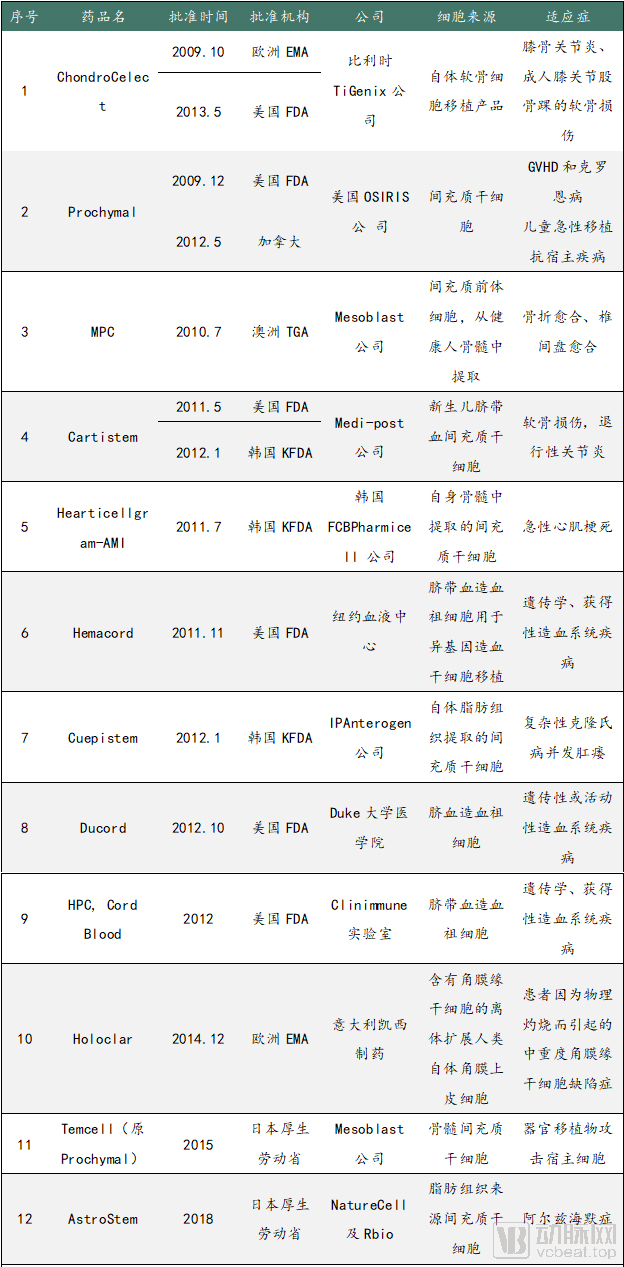

Table: Major Stem Cell Products Currently on the Market Data Source: MedPeer

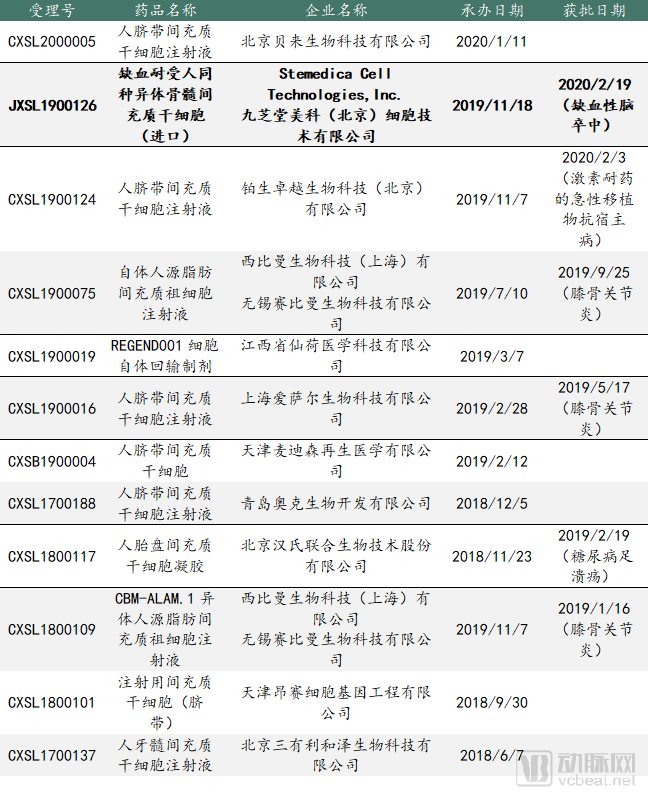

As of February 2020, the Center for Drug Evaluation (CDE) had accepted a total of 13 Investigational New Drug (IND) applications for stem cell therapies submitted by 12 companies, with six approvals granted. Among these, the IND application from Jiuzhitang Meike was approved, marking the first clinical trial authorized by the CDE that utilized imported stem cells, the first clinical trial using bone marrow-derived mesenchymal stem cells, and the first clinical trial employing stem cell therapy for a major neurological indication.

Data Source: Yimaike

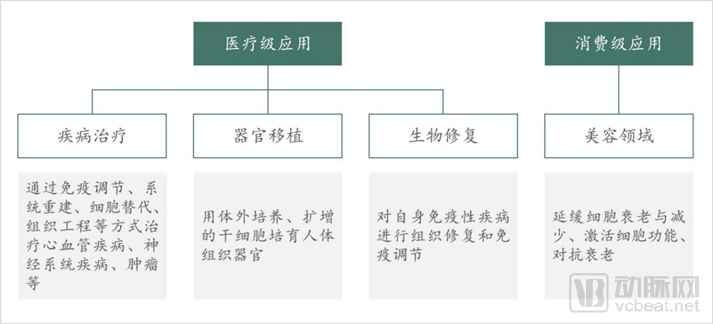

The downstream segment of the industry chain primarily comprises medical-grade and consumer-grade applications. Medical-grade applications refer to clinical uses, such as the treatment of various diseases; consumer-grade applications are mainly focused on the aesthetics sector, including anti-aging products.

Stem cells have a broad therapeutic scope for various diseases. Regenerative medicine, centered on stem cells, represents an effective treatment modality following conventional pharmacotherapy and surgical interventions, thereby driving medical reform. Hospitals serve as the primary entities for such treatments; notable examples include the Stem Cell Transplantation Center of the General Hospital of the Chinese People's Armed Police Force and Beijing Tiantan Puhua Hospital. Additionally, downstream enterprises provide stem cell therapy technologies to hospitals for profit generation. For instance, Beike Biotechnology has cumulatively treated 10,000 cases within its first five years of establishment, becoming one of the world’s five most renowned stem cell therapy centers. To date, apart from hematopoietic stem cell therapy for blood disorders, no stem cell therapies offered by any medical institution have been accepted or reviewed by regulatory authorities. Clinical applications of stem cells conducted by hospitals are classified as experimental clinical research.

Consumer-grade applications are primarily concentrated in the field of anti-aging. The decline in stem cells is one of the primary causes of human aging. Stem cell technology can be utilized to replace and renew senescent and dead cells, activate cellular functions, and delay the aging process. Consequently, stem cell-based anti-aging therapies have rapidly gained market favor due to their safety, feasibility, and efficacy, demonstrating strong potential for market development. According to research data from Global Industry Analysts, Transparency Market Research, and the Fung Business Intelligence Centre, global anti-aging market sales were projected to reach $200 billion in 2020, while China’s anti-aging market size exceeded RMB 50 billion in the same year.

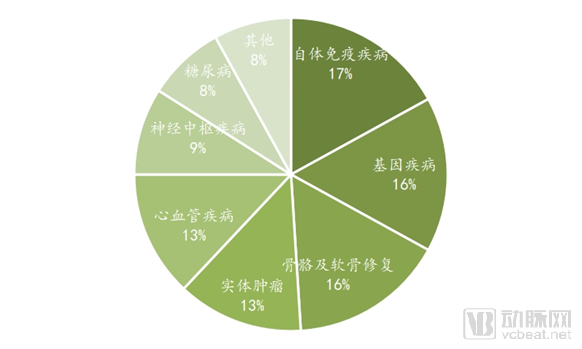

Figure: Distribution of Indications for Stem Cell Therapy. Source: Guangzheng Hengsheng

International Giants

Osiris Therapeutics

Osiris Therapeutics was founded in Maryland, USA, in 1992, listed on the NASDAQ under the ticker symbol OSIR in 2006, and delisted in April 2019. Its technology originated from stem cell research developed by a team led by Professor Arnold Caplan at Case Western Reserve University. The company’s core technology focuses on tissue regeneration and anti-inflammatory effects through stem cell therapy.

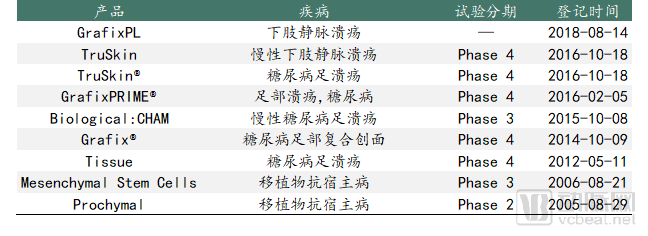

OSIR has developed two relatively mature stem cell products. Prochymal: the world’s first approved marketed allogeneic stem cell drug. Chondrogen is primarily used to treat arthritis-related conditions. In the area of stem cell biologics, the company offers five products: Grafix, Cartiform, GrafixPL, Stravix, and Bio. Grafix is one of Osiris’s key products, mainly applied in wound care. Cartiform is Osiris’s product in the field of sports medicine; it is a cryopreserved osteochondral allograft. Bio is a product for plastic surgery, primarily addressing bone injuries in the field of plastic and reconstructive surgery.

Figure: Clinical Trial Progress of Osiris’s Stem Cell Therapeutics. Source: Yaozhi Database

StemCells

StemCells Inc., founded in 1988, is a U.S.-based company engaged in the development of stem cell products, with a focus on stem cell therapies for central nervous system disorders, liver diseases, and pancreatic diseases. The company’s renowned stem cell technology, which isolates human neural stem cells from adult brain tissue, is at the forefront globally. In 2009, StemCells Inc. acquired the UK-based Stem Cell Sciences plc, thereby consolidating its leadership position in human neural stem cell technology and expanding its technological applications into cell-level research for drug development and screening. The company currently holds more than 40 U.S. patents and over 170 patents worldwide. Its most mature product, HuCNS-SC, consists of neural stem cells isolated from fetal brain tissue. Preclinical trials have demonstrated that HuCNS-SC exhibits significant efficacy in treating neurological disorders, with no observed side effects.

Figure: Clinical Trial Progress of StemCells, Inc.’s Stem Cell Therapeutics. Source: Yaozhi Database

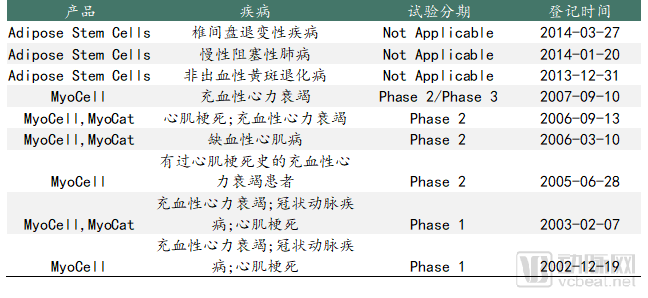

Bioheart

Bioheart was founded in 1999. The company primarily focuses on the research and development of effective cell therapies, dedicating itself to stem cell treatments for repairing cardiac injury. It also possesses smart devices capable of monitoring heart failure and other cardiovascular diseases. MyoCell, a muscle-derived stem cell product, is Bioheart’s flagship offering. It has been shown to improve cardiac function in patients months or even years after severe cardiac injury. In July 2009, it received FDA approval to conduct clinical trials for the treatment of severe chronic heart failure. AdipoCell, derived from patients’ own adipose tissue, is used to treat congestive heart failure. MyoCath is a disposable syringe developed by the company specifically for delivering the stem cell product MyoCell to myocardial tissue, and it is currently the delivery device used in most clinical trials.

Figure: Clinical Trial Progress of Bioheart’s Stem Cell Therapeutics. Source: Yaozhi Database

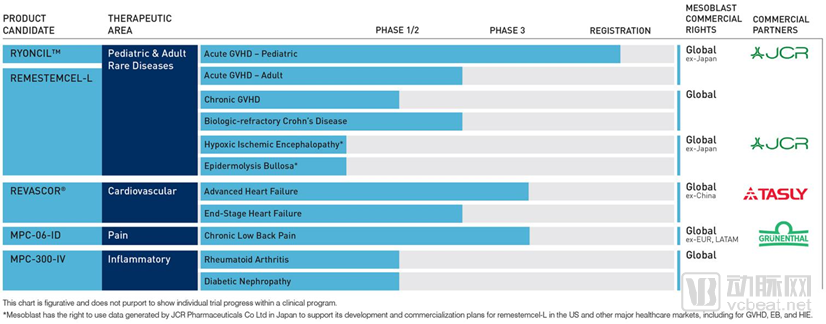

Mesoblast

Mesoblast, established in 2004 and headquartered in Melbourne, Australia, is a globally leading biotechnology company dedicated to developing cell-based regenerative therapy products. The company was listed on the Australian Securities Exchange in 2004 and subsequently listed on the NASDAQ in the United States in 2015 through the issuance of American Depositary Receipts (ADRs). In July 2018, Tasly Pharmaceutical Group (600535) announced its subscription for USD 20 million worth of Mesoblast’s ordinary shares and secured the rights to introduce two stem cell product candidates currently undergoing FDA Phase III and Phase II clinical trials, respectively: MPC-150-IM for the treatment of congestive heart failure, and MPC-25-IC for the treatment of acute myocardial infarction.

Mesoblast has developed a series of clinically convenient allogeneic stem cell therapeutic products leveraging its proprietary adult stem cell technology platforms, namely “Mesenchymal Lineage Cells (MLC)” and “Mesenchymal Precursor Cells (MPC).” These products are characterized by the absence of a need for tissue matching and no risk of rejection, enabling their ready availability to address unmet clinical needs. Such needs include cardiovascular diseases, rheumatic and autoimmune disorders, metabolic diseases, degenerative conditions such as spinal disorders, and immune-related diseases associated with the treatment of cancers and hematologic malignancies.

Figure: Clinical Trial Progress of Mesoblast’s Stem Cell Drug. Source: Company Website

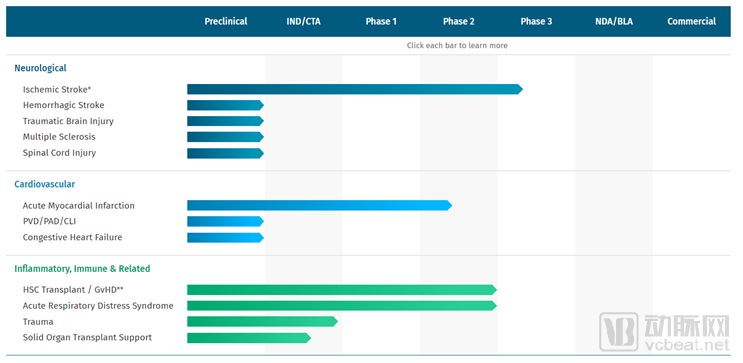

Athersys

Athersys was founded in 1995, with its headquarters in Cleveland, Ohio, USA, and went public on NASDAQ in 2007. The company specializes in stem cell and regenerative medicine, with its lead product, MultiStem, being multipotent adult progenitor cells (MAPCs) derived from allogeneic bone marrow. MultiStem received FDA approval in 2017 for the treatment of Mucopolysaccharidosis Type I (MPS-I). Other indications under development include hemorrhagic stroke, traumatic brain injury, multiple sclerosis, spinal cord injury, acute myocardial infarction, congestive heart failure, graft-versus-host disease, acute respiratory distress syndrome, and trauma. Currently, the primary indication being advanced for MultiStem is hemorrhagic stroke.

MultiStem is currently the only therapy for acute respiratory distress syndrome (ARDS) that has received Fast Track designation from the U.S. Food and Drug Administration (FDA), and is therefore considered highly relevant to the treatment of COVID-19. In 2020, the U.S. Biomedical Advanced Research and Development Authority (BARDA) identified MultiStem as a therapy with high relevance to the treatment of COVID-19.

Figure: Clinical Trial Progress of Athersys’ Stem Cell Drug. Source: Company Website

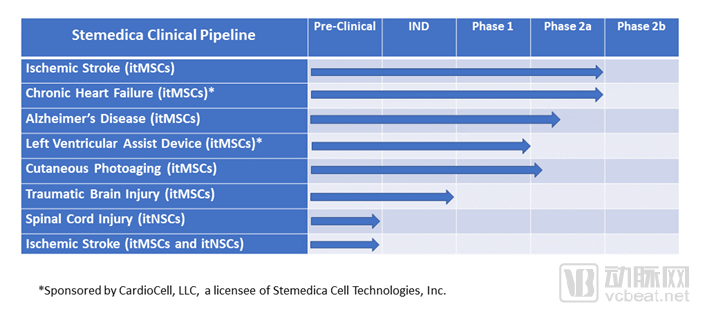

Stemedica

Stemedica, founded in 2005 and headquartered in San Diego, is one of the few biotechnology companies in the United States authorized by the FDA to conduct clinical trials on stem cell-based therapeutics. It is also among the handful of companies worldwide capable of producing both human bone marrow-derived mesenchymal stem cells (hBM-MSCs) and human neural stem cells (hNSCs). Furthermore, Stemedica was the first company in the U.S. to receive approval for initiating clinical trials for Alzheimer’s disease. To date, the company has obtained FDA approval for six clinical trials. It has established a stem cell manufacturing platform with independent intellectual property rights that complies with the U.S. FDA’s current Good Manufacturing Practice (cGMP) regulations. This platform ensures stem cell quality while achieving scalability, standardization, and traceability in the production process, resulting in unprecedented stem cell expansion efficiency. The company is developing therapies for 16 indications, six of which are being pursued in the United States and have entered Phase I or Phase II clinical stages.

Figure: Clinical Trial Progress of Stemedica’s Stem Cell Therapeutics. Source: Company Website

Domestic Companies

Supported by favorable policies, technological advancements, market demand, talent availability, and capital investment in the stem cell industry, major companies are accelerating their strategic layout in the mid- and downstream sectors of the stem cell value chain. They are dedicated to advancing stem cell technology research and promoting the application of stem cell-based products. With numerous participants across various segments, the figure below lists some representative enterprises.

Figure: Industry Chain Map of China’s Stem Cell Sector. Source: Huoshi Chuangzao, public information

Policy: Policy Tailwinds Propel Stem Cell Development into the Fast Lane

China has attached great importance to stem cell technology, issuing a series of regulatory documents in the early 1990s, such as the Key Points for Quality Control in Clinical Research on Human Somatic Cell Therapy and Gene Therapy, to promote the development of stem cell research and the clinical industry. However, in 2012, policies were tightened. To foster the scientific and orderly development of stem cell therapy technologies, standardize clinical research and application practices, and rectify stem cell treatment activities, the National Health and Family Planning Commission released the Notice on Conducting Self-Inspection and Correction in Stem Cell Clinical Research and Applications, halting ongoing unapproved stem cell clinical research and application projects. After 2015, driven by the “resonance” of multiple catalysts both domestically and internationally, the state introduced a series of supportive policies, propelling the stem cell industry onto a fast track.

Technology: Undercurrents Surge in Global R&D, Singularity Breakthrough Imminent

Technological innovation is the core driver of development in the stem cell industry. In recent years, stem cell therapy has achieved significant breakthroughs in the treatment of major diseases, including cardiovascular diseases, diabetes, degenerative diseases, and autoimmune disorders. More than ten stem cell drugs/therapies have been approved for marketing worldwide. China ranks among the global leaders in stem cell technology. As of March 2020, a total of 5,432 stem cell-related clinical studies had been registered on ClinicalTrials.gov, with 469 originating from China. China has made rapid progress in numerous disease areas, such as the use of stem cells to treat osteoarthritis, diabetic foot, acute myocardial ischemia, thalassemia, and Parkinson’s disease. With the concurrent improvement in research capabilities and the strengthening of research institutions and R&D personnel, it is foreseeable that basic stem cell research in China will continue to achieve breakthroughs, and R&D outcomes will be increasingly translated into clinical applications.

Cells: Mesenchymal Stem Cells Resolve Safety and Ethical Concerns, Driving the Development of the Stem Cell Therapy Industry

The Final Mile to Clinical Application of Stem Cell Research: Safety, Efficacy, and Ethical Concerns Have Long Hindered the Development of the Stem Cell Industry. The strong tumorigenicity and ethical issues associated with embryonic stem cells (ESCs), as well as the genetic risks and significant tumorigenic potential of induced pluripotent stem cells (iPSCs), have highlighted the broad prospects of mesenchymal stem cells (MSCs). MSCs have become the second type of adult stem cells, following hematopoietic stem cells, to enter clinical application, demonstrating outstanding safety and efficacy. Multiple studies have confirmed that MSCs exhibit no tumorigenicity in vivo. Due to their wide availability from various sources in individuals (such as adipose tissue, bone marrow, and blood), autologous MSC applications avoid immune rejection, do not introduce exogenous genes, and prevent cell-associated viral infections, thereby overcoming safety and ethical challenges. MSCs have become a focal point in clinical research, further driving the continued growth of the stem cell therapy industry.

Obtaining higher-quality cells is key to MSC therapy. The challenge in stem cell therapy lies in the complexity of stem cell products; variations in cell sources and manufacturing processes significantly impact stem cell quality and therapeutic efficacy, which is a primary reason for the suboptimal outcomes of many previous stem cell clinical trials. Post-transplantation cell survival is paramount to the success of MSC therapy. Studies have shown that hypoxic preconditioning can effectively mimic the in vivo microenvironment, helping to maintain physiological processes such as proliferation, differentiation, and metabolic balance in mesenchymal stem cells (MSCs), enabling them to enter the cell cycle faster and initiate in vitro cell division earlier than normoxic cells. Furthermore, hypoxic preconditioning significantly reduces cell damage by maintaining in vitro energy metabolism, thereby promoting MSC proliferation. Stemedica has developed BioSmart™, a clinical-grade cell production platform, at its cGMP facility in California. This platform produces ischemia-tolerant human bone marrow-derived MSCs (ithMSCs) and ischemia-tolerant human neural stem cells (ithNSCs) under hypoxic conditions (5% O2), yielding products with superior performance compared to stem cells cultured under normoxic conditions.

Industry Chain: Near-Term Focus on Memory, Long-Term Focus on Applications; Core Barriers Lie in R&D, Manufacturing, and Commercialization

A Closer Look at Storage. Within the industrial chain, upstream stem cell storage is currently the most significant and mature commercialized segment in the stem cell field, and it is a service with government-approved fee structures. This segment does not demand highly sophisticated technology nor present high barriers to entry. In the future, companies that can leverage economies of scale, standardized management practices, and technological advantages to deliver higher-quality storage services are poised for promising growth. Several publicly listed companies have already established their presence in this sector, such as Nanjing Xinbai and Zhongyuan Union Cell & Gene Engineering Corp.

Long-term Market Outlook. The primary factor in evaluating the stem cell therapy market is the potential market size of its indications. Based on global disease data and demographic trends, there is enormous potential market size for neurological disorders, cardiovascular diseases, diabetes, dermatological conditions, bone diseases, and medical aesthetics. Companies with R&D pipelines covering these indications hold greater investment value. Stemedica has 16 indications, spanning cardiovascular diseases, neurological disorders, orthopedic conditions, diabetes, autoimmune diseases, skin diseases, medical aesthetics, and anti-aging. Among these, six indications have entered Phase I and Phase II clinical trials.

Core barriers lie in R&D, manufacturing, and commercial operations. Stem cell sources are complex, with varying preparation processes and quality control indicators. Issues remain to be addressed and improved regarding the stability and safety of in vitro culture and expansion, quality standard testing technologies, and product purity. Furthermore, stem cells themselves pose challenges such as abnormal differentiation, immune rejection, and potential genetic mutations and alterations in cell function during expansion and passaging. These factors contribute to significant technical difficulties in therapeutic applications and latent medical risks stemming from biosafety concerns. Consequently, companies with advantages in R&D and manufacturing, strong cell expansion capabilities, and high cell quality are more competitive.