Comprehensive Analysis of 497 Internet Hospitals in China: Physical Hospitals Dominate with 80% Share, Growth Slows Post-Pandemic

In 2020, internet healthcare played a positive role in epidemic prevention and control, once again becoming the focus of industry attention. VCBeat has previously released the "Internet Hospital Policy Report" to analyze industry policy trends. However, during the implementation process, the progress and intensity of promotion varied across different regions.

So, what are the actual characteristics of the current construction of internet hospitals? Taking the issuance of the Administrative Measures for Internet Hospitals (Trial) by the National Health Commission in September 2018 as the starting point, we have collected data on 497 internet hospitals from multiple public sources (data as of April 30).

By analyzing dimensions such as the establishment dates, geographic distribution, sponsoring entities, and health insurance integration status of these internet hospitals, we aim to gain a more accurate understanding of industry trends. To ensure the validity of our analysis, we strictly adhered to authoritative data sources, applying the following collection criteria:

List of Internet Hospitals: Priority shall be given to the list published by health authorities, followed by information from hospital official websites and social media accounts, as well as public reports from mainstream media. Internet hospital companies that cannot verify their acquisition of internet hospital qualifications shall not be included in the list.

Establishment Date of Internet Hospitals: Priority is given to the approval date disclosed by health authorities at all levels, followed by the approval or launch date reported by mainstream media, hospital official websites, and official social media accounts.

Basic Information of the Sponsor: Subject to the publicly available information on the official websites and official social media accounts of health commissions at all levels, hospitals, and enterprises;

Health Insurance Connectivity Status: Subject to official public reports from health commissions and healthcare security administrations at all levels, mainstream media, and the hospital’s official website and social media accounts.

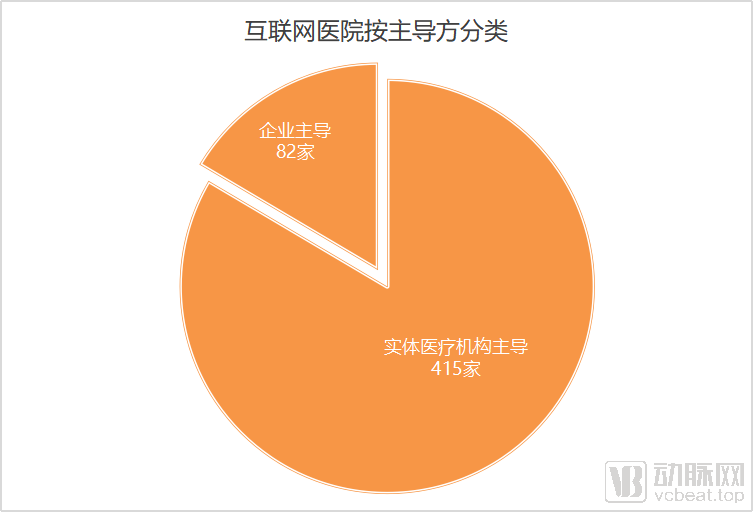

Internet hospitals are categorized into entity hospital-led and enterprise-led models based on the sponsoring entity. Among the 497 internet hospitals, 415 are led by physical hospitals, accounting for 83.5%.

Lead Parties of Internet Hospitals, Chart by VCBeat

Physicians are the most critical resource for internet hospitals. Physical hospitals naturally possess this advantage, whereas enterprises require prolonged accumulation or substantial short-term investment to build a sufficient physician base.

In the early stages of internet hospital development, few physical hospitals explored this model. As the operational framework of internet hospitals matured, and as policies provided endorsement, promotion, and standardization, an increasing number of physical hospitals began establishing their own internet hospitals. To date, the proportion of hospital-led internet hospitals has far surpassed that of enterprise-led ones.

Meanwhile, internet hospitals have just undergone a new wave of construction boom.

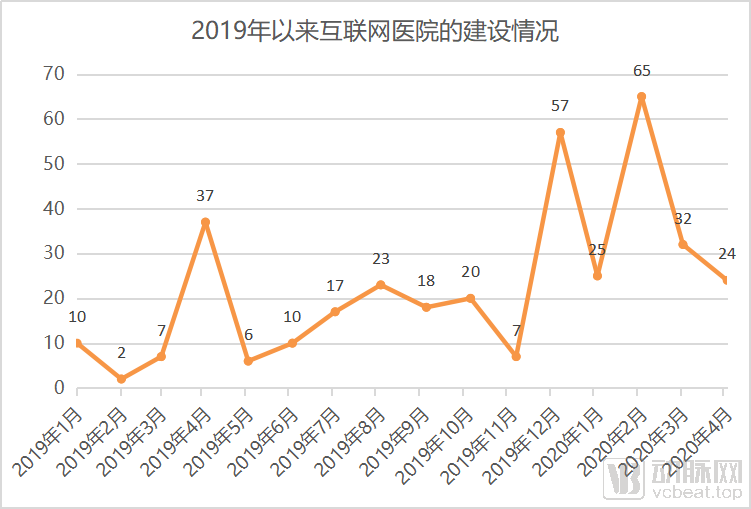

Following the issuance of the Administrative Measures for Internet Hospitals (Trial) by the National Health Commission in September 2018, internet hospitals officially entered a phase of standardized development characterized by formal approval and regulatory oversight. However, the number of internet hospitals approved during the year the new policy was introduced remained limited. Therefore, using 2019 as the starting point, we have outlined the monthly establishment of internet hospitals in the figure below (based on the date of obtaining the practice license or the launch date; cases where neither date was clear are excluded from the figure).

Establishment of Internet Hospitals Since 2019, Chart by VCBeat

As can be seen, the number of establishments showed an overall upward trend, reaching its first peak in April 2019. Following the release of the National Healthcare Security Administration’s “Guiding Opinions on Improving Price and Medical Insurance Payment Policies for ‘Internet+’ Medical Services” in August, a second peak was reached in December.

By 2020, the highest number of internet hospitals were established in February, reaching 65. This may also be the period with the largest number of internet hospitals built in a single month since their inception.

February marked the peak of the COVID-19 outbreak, and the urgent need for epidemic prevention and control accelerated the development of internet hospitals. During the pandemic, existing internet hospitals successively launched online fever clinics, follow-up consultations for chronic diseases, and pneumonia consultation services. In addition, numerous new internet hospitals received emergency approval and were rapidly deployed.

According to media reports, the internet hospital of Renmin Hospital of Wuhan University, “Wuda Cloud Medicine,” took only one day to apply for registration, becoming the first internet hospital in Hubei Province to obtain online diagnosis and treatment qualifications. Wang Gaohua, the president of Renmin Hospital of Wuhan University, introduced that they submitted an application to the Provincial Health Commission on February 3rd, and it was approved the next day.

Such rapid response was not unique to Wuhan, the epicenter of the outbreak. In Tianjin, on February 5, the Internet Hospital of Tianjin Medical University General Hospital applied to the Tianjin Municipal Health Commission to add a respiratory medicine department. The application was officially accepted at 16:14 that afternoon, and after swift review and approval, the matter was completed at 16:25, taking only 11 minutes in total.

As the pandemic stabilized, the growth rate of internet hospitals slowed down starting in March 2020, falling back to pre-pandemic levels by April.

During the pandemic, internet hospitals met the medication needs of a large number of patients with chronic diseases by providing online follow-up consultations, e-prescribing, and drug delivery services, with some expenses eligible for reimbursement through basic medical insurance. However, the development of internet hospitals should not rely solely on pandemic prevention and control measures. Although the industry effectively educated users and cultivated their habits during this period, it remains uncertain whether the appeal of online consultations to patients will be sustained in the post-pandemic era.

Therefore, the service model of internet hospitals urgently needs to be upgraded by restructuring healthcare service processes, rather than simply replicating offline workflows.

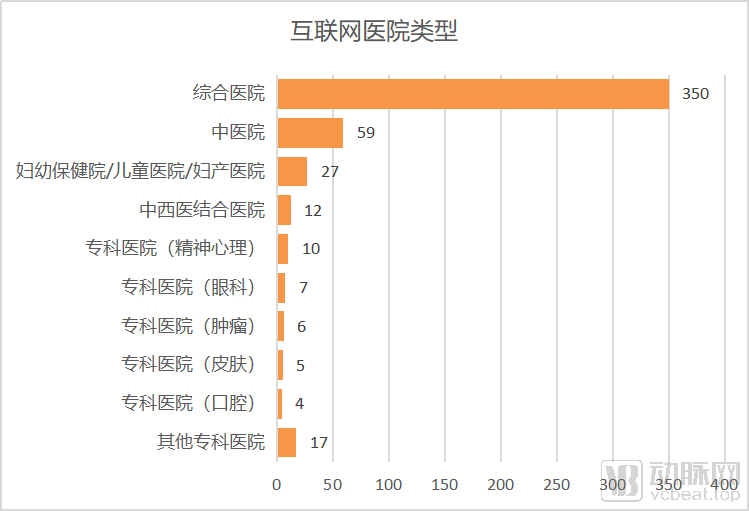

Types of 497 Internet Hospitals, Chart by VCBeat

Based on the current landscape of internet hospitals, general hospitals and traditional Chinese medicine (TCM) hospitals dominate the market, while specialized hospitals exhibit diverse models. General hospitals offer comprehensive departments, capable of meeting a wide range of patient needs. Although TCM hospitals cannot perform pulse diagnosis online, they are still authorized to issue electronic prescriptions.

On April 10, Longhua Hospital Affiliated to Shanghai University of Traditional Chinese Medicine issued a traditional Chinese medicine (TCM) prescription through its internet hospital. A patient with ankylosing spondylitis, who had been receiving treatment at the Department of Rheumatology and Immunology of Longhua Hospital, experienced significant remission after long-term stable therapy. Following a video consultation via the internet hospital, the physician prescribed a herbal formula for the patient, which can be delivered directly to their home by a logistics company in the form of TCM decoction pieces.

Maternal and child health hospitals, children’s hospitals, and obstetrics and gynecology hospitals also account for a significant proportion of hospital types. Pregnant women and children are populations with high healthcare needs yet face considerable barriers to accessing medical care. During the epidemic, the Children’s Hospital of Chongqing Medical University launched its internet hospital on February 3. In February alone, it conducted more than 12,000 online consultations and issued 397 electronic prescriptions, 54% of which were for pediatric patients from other regions. Medications were delivered to multiple locations in Sichuan, Guizhou, Yunnan provinces, as well as various areas within Chongqing Municipality, greatly facilitating patients’ access to medical care.

Among other specialized hospitals, those focusing on chronic diseases or specialties with strong consumer demand, such as dentistry and ophthalmology, predominate. These hospitals are able to meet patients’ multi-level needs for medical care, health management, and consumer-oriented services.

Due to variations in medical resources, clinical standards, and health informatics infrastructure across China, the development of internet hospitals differs significantly from region to region.

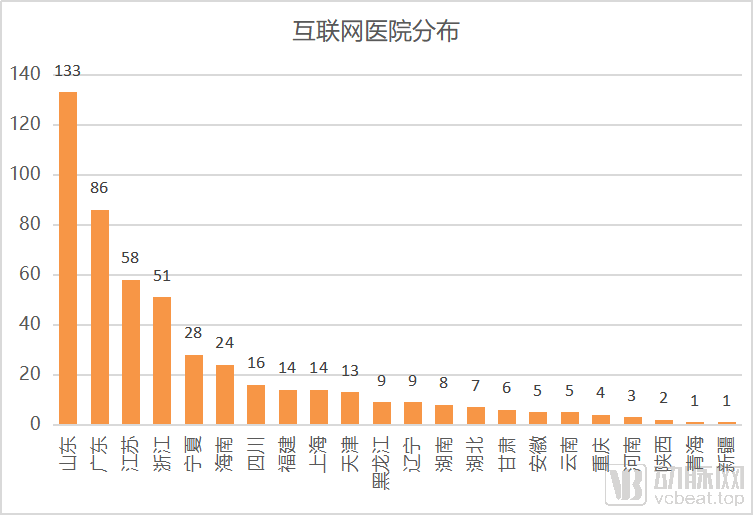

Overall Distribution of Internet Hospitals, Chart by VCBeat

As shown in the figure above, internet hospitals are currently concentrated mainly in the eastern and southern coastal provinces. These regions benefit from a high concentration of high-quality medical resources, advanced levels of healthcare informatization, and a solid foundational infrastructure. Notably, Shandong, Jiangsu, Anhui, Zhejiang, Fujian, and Guangdong have been designated by the National Health Commission as demonstration provinces for “Internet + Healthcare.”

The regions with the highest number of internet hospitals were among the earliest to explore this industry. Currently, Shandong Province has 133 internet hospitals.

Since 2019, Hainan, Shanghai, Tianjin, Heilongjiang and other regions have accelerated the development of internet hospitals. Among them, Hainan’s internet hospitals are predominantly enterprise-led, with 22 out of the current 24 internet hospitals falling into this category.

Shaanxi is also accelerating the development of internet-based medical services. Driven by pandemic prevention and control requirements, several hospitals have been approved to provide online diagnosis and treatment services, although few have been licensed as full-fledged internet hospitals. In contrast, Beijing has only approved a handful of physical hospitals to offer online diagnosis and treatment services and has not yet licensed any internet hospitals.

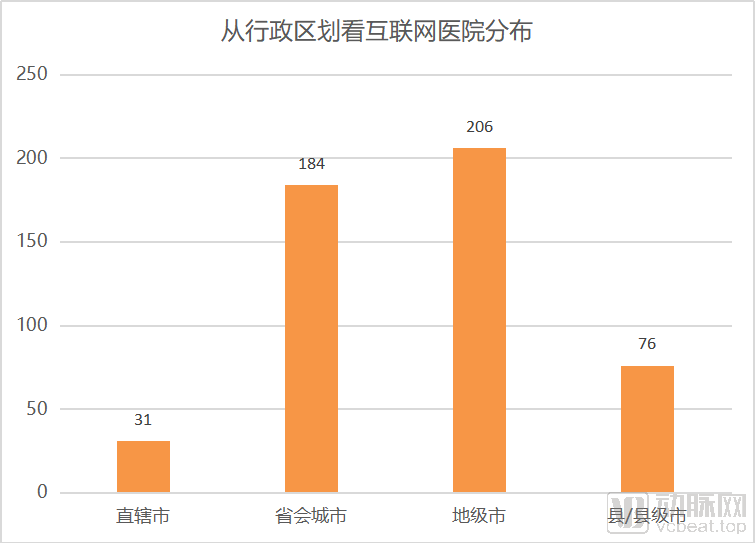

At present, internet hospitals are increasingly expanding into prefecture-level cities, counties, and county-level cities. Based on administrative divisions, we have compiled the number of internet hospitals in various types of cities:

Distribution of Internet Hospitals by Administrative Division, Chart by VCBeat

As shown in the figure above, there are more than 200 internet hospitals located in municipalities directly under the Central Government and provincial capitals, over 200 in prefecture-level cities, and 76 in county-level cities.

As of now, most provinces across China have established development goals for internet-based healthcare. Provinces such as Hebei, Hubei, and Sichuan have taken regional distribution into account, requiring cities and prefectures to simultaneously build internet hospitals or launch internet healthcare services, in addition to the large tertiary Grade A hospitals located in provincial capitals.

The distribution of internet hospitals also reflects a trend of gradually expanding coverage to lower-tier regions under policy promotion. Especially in provinces such as Zhejiang, Guangdong, Shandong, and Jiangsu, internet hospitals have already achieved relatively extensive coverage in prefecture-level and county-level cities.

What patterns emerge when analyzing the two types of applicants for internet hospital licenses: physical hospitals and enterprises?

Physical Hospitals Lead, with Public Tertiary Grade A Hospitals Dominating and Private Institutions Holding a Small Share

Let us first examine physical hospitals, which are categorized into different types based on their funding sources and hospital classifications; this, in turn, leads to distinct characteristics among internet hospitals.

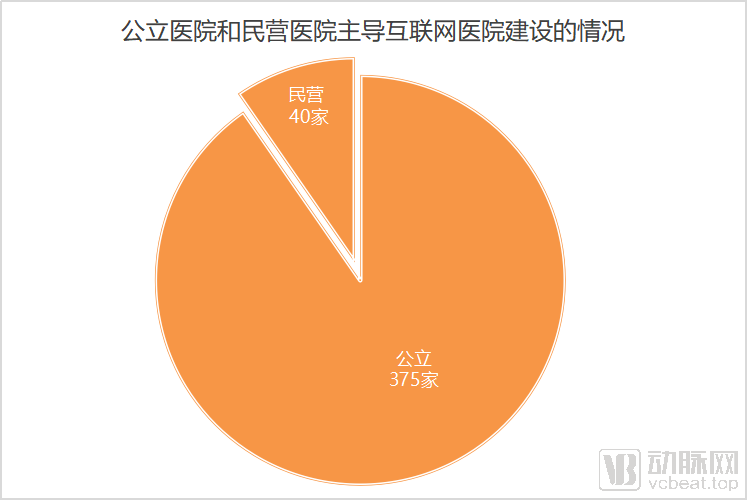

Among the 415 physical hospitals that have currently applied to establish internet hospitals, 375 are public and 40 are private, accounting for 90% and 10%, respectively, of internet hospitals led by physical hospitals. In contrast, according to the China Health Statistics Yearbook 2018, there are 12,000 public hospitals and 21,000 private hospitals nationwide, with the number of private hospitals far exceeding that of public hospitals.

That is to say, approximately 3.1% of public hospitals have established internet hospitals, whereas only 0.2% of private hospitals have done so.

Internet Hospital Development in Public and Private Hospitals | Chart by VCBeat

For public hospitals, especially large tertiary Grade A hospitals, the primary purpose of establishing internet hospitals is to triage patients with common and chronic diseases, create an integrated online-offline workflow, and improve the overall efficiency of patient care and hospital management. Meanwhile, the accelerated investment by public hospitals in internet hospital development is also partly driven by administrative initiatives from their supervisory authorities.

For private hospitals with lower outpatient volumes, shifting patients with common and chronic diseases to online platforms is not an urgent necessity. Instead, these institutions prioritize enhancing the quality of medical care and services to attract patients. If they choose to establish internet hospitals, they aim to achieve this same objective. Therefore, private hospitals—particularly for-profit ones—must carefully balance the relationship between construction and operational costs and benefits.

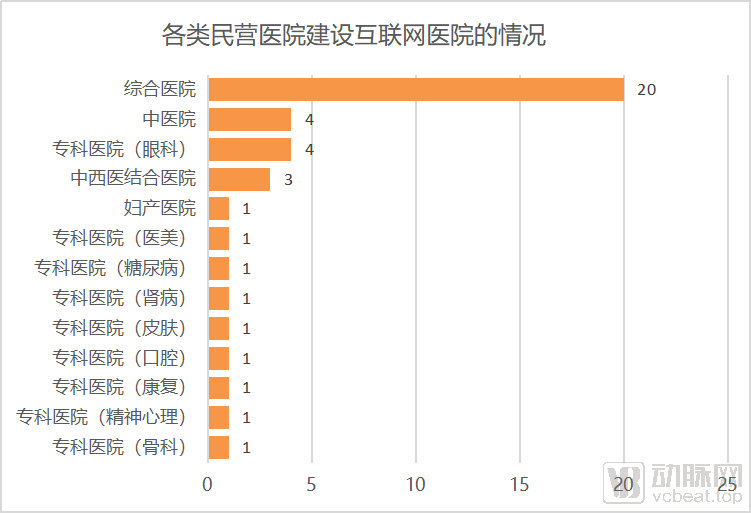

Types of Private Hospitals Applying for Internet Hospital Licenses, Chart by VCBeat

The chart above illustrates the types of private hospitals that have established internet hospitals, with general hospitals still constituting the majority. Specialized hospitals cover areas with strong consumer attributes, such as ophthalmology, obstetrics and gynecology, and dentistry. Among various specialized hospitals, the internet helps shape hospital brands and bridge the gap between doctors and patients, thereby promoting hospital operations.

However, overall, private specialized hospitals have been less active in establishing internet hospitals, and it remains uncertain whether they can sustainably expand patient acquisition channels through online platforms in the future. Nevertheless, during the pandemic, the volume of offline medical services declined across the board, particularly among private healthcare institutions. By expanding online services, these institutions were at least able to minimize the impact brought by the pandemic.

In terms of hospital classification, nearly 13% of tertiary hospitals across China have established internet hospitals. Among these, 253 Grade A tertiary hospitals have expanded their services to include internet hospitals, accounting for 17.5% of the 1,442 Grade A tertiary hospitals nationwide.

Among these Grade A tertiary hospitals, renowned institutions such as West China Hospital of Sichuan University, the Xiangya Hospital system of Central South University, Zhongshan Hospital Fudan University, and Huashan Hospital Fudan University have all launched internet hospitals.

Status of Internet Hospital Construction Across Hospitals of Different Tiers, Chart by VCBeat

As previously mentioned, from the perspective of administrative divisions, internet hospitals are expanding from municipalities directly under the Central Government and provincial capital cities to prefecture-level and county-level cities. The above chart also shows that only 0.61% of secondary hospitals have established internet hospitals.

Level II hospitals are distributed not only across various municipal districts but also widely in prefecture-level and county-level cities. Therefore, from the perspective of hospital classification, the downward expansion of internet hospitals follows the same trend.

However, hospital classification also reflects its service positioning and capabilities; therefore, it is neither necessary nor feasible for every hospital to independently establish an internet hospital.

Physical hospitals establishing internet hospitals may independently apply for an internet hospital license as a secondary name, or they may collaborate with third-party institutions to apply for an internet hospital license as a secondary name; the latter accounts for approximately 10% of internet hospitals led by physical hospitals.

For an internet hospital established through a joint partnership, the names of both the hospital and the enterprise must be reflected in the internet hospital’s name. Under this model, the enterprise is required not only to provide support for platform development but also to contribute resources and engage continuously in subsequent operations.

Internet healthcare companies and medical informatics enterprises are extensively participating in collaborative efforts to co-establish internet hospitals. Companies such as WeDoctor and Nali Health have jointly built internet hospitals with multiple physical hospitals. This model facilitates the deep integration of physicians and medical resources from physical hospitals with the platform reach and operational capabilities of enterprises, thereby creating complementary advantages for both parties.

Enterprises Establishing Internet Hospitals Aim to Build Their Own Closed-Loop Business Ecosystem

Internet hospitals have defined follow-up consultations for common and chronic diseases, which may seem to limit the scope of medical inquiries, yet various types of enterprises continue to enter this field.

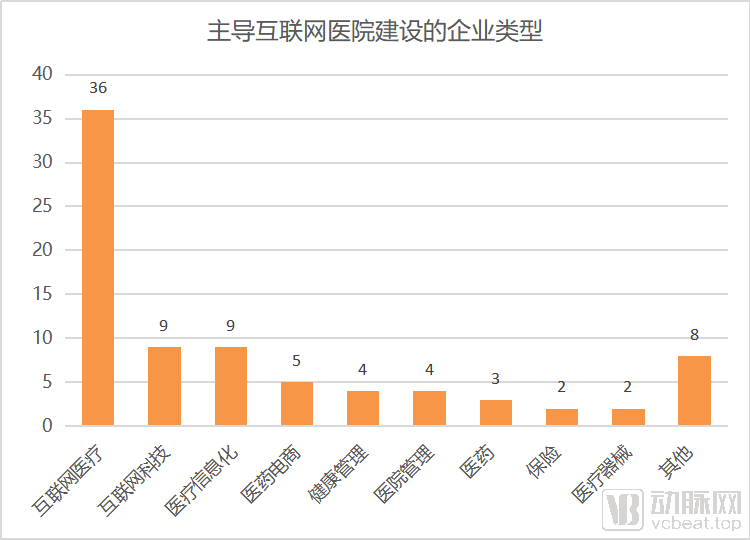

Early pioneers in the internet hospital sector were primarily companies specializing in online healthcare, healthcare informatics, and pharmaceutical e-commerce. Over time, the range of participating enterprises across various sub-sectors has become increasingly diversified, encompassing upstream pharmaceutical and medical device manufacturers as well as downstream insurance providers.

Types of Enterprises Leading Internet Hospitals, Chart by VCBeat

The above presents the number of enterprises by category among the enterprise-led internet hospitals included in our current statistics. Internet healthcare, healthcare informatization, and pharmaceutical e-commerce remain the dominant sectors, while other enterprise types are diverse.

Medical needs are not high-frequency demands, and online consultations have strictly defined scopes. Therefore, various new types of enterprises invest in building internet hospitals not for the online consultation itself, but to complete their business loops through compliant qualifications.

For example, under the influence of policies such as centralized drug procurement on the pharmaceutical distribution landscape, pharmaceutical companies can explore new sales channels and service models. Medical device manufacturers can leverage internet hospitals as an entry point to collaborate with offline medical institutions, providing diagnosis and treatment services centered around their products, thereby achieving rapid product adoption. Meanwhile, insurance companies can shift their business processes upstream through internet hospitals, enabling better health management for customers, reducing disease incidence, and thus lowering costs, or accumulating medical data to design more rational insurance products.

China has established a basic medical insurance system that covers the entire population. According to the latest data from the National Healthcare Security Administration, by the end of 2019, the coverage rate of basic medical insurance had stabilized at over 95%. For offline medical visits, patients primarily rely on medical insurance payments and out-of-pocket payments, whereas medical insurance reimbursement for online healthcare services is still in its early stages.

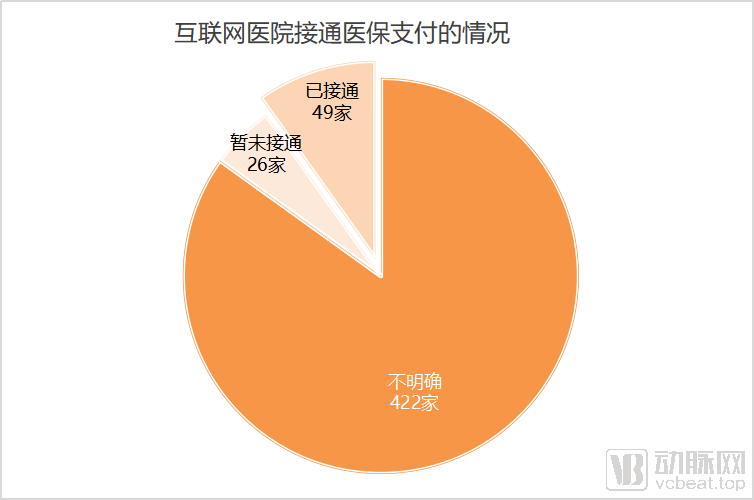

Internet Hospital Medical Insurance Integration Status, Chart by VCBeat

Among the internet hospitals included in our current statistics, only 49 have integrated with medical insurance payment systems, while 26 reported that such services are not yet available but are either underway or scheduled for implementation.

Most internet hospitals have no public information indicating whether they are connected to the medical insurance system or not, so we categorize them as “Unclear.” However, since this is a critical public service, regulatory authorities or hospitals typically disclose such status through appropriate channels. Therefore, it is highly likely that those in the “Unclear” category are not yet integrated with the national medical insurance system.

Among internet hospitals that have integrated with medical insurance payment systems, the primary settlement methods include direct online settlement, settlement via the medical insurance platform, and other payment methods.

Direct online settlement means that after patients complete follow-up consultations via internet hospitals, the system automatically calculates the out-of-pocket amount, and patients can make the payment accordingly. Examples include Ping An Good Doctor’s Hubei Internet Hospital, WeDoctor General Internet Hospital’s Wuhan Zone, and Fujian Provincial Government Hospitals.

Payment through the medical insurance platform requires integration with an internet hospital. For example, Nantong No. 6 People’s Hospital in Jiangsu Province has been integrated into the Nantong Medical Insurance APP, enabling services such as online follow-up consultations, medical insurance payments, and medication delivery.

The Shandong Provincial Internet Medical Insurance and Health Service Platform follows a similar model. By integrating internet hospital establishment, inclusion in the medical insurance designated provider network, patient identity verification, follow-up consultation confirmation, and online medical insurance settlement, the platform has established a complete closed-loop system for online payment and settlement of medical insurance services in internet hospitals, representing a new exploration of service models for internet hospitals.

Furthermore, given that the integration between internet hospitals and medical insurance information systems, as well as pharmacies, remains immature, some regions have adopted alternative approaches. These include generating QR codes for the out-of-pocket portion to enable patient scan-to-pay transactions, or requiring patients to pay upfront online at their own expense and subsequently seek reimbursement from the hospital.

The pandemic control efforts have strongly propelled the integration of medical insurance payment systems with internet hospitals, leading to the rapid launch of such services at multiple internet hospitals in Hubei, Shanghai, Jiangsu, Zhejiang, Tianjin, and other regions. In the post-pandemic era, the improvement of medical insurance payment mechanisms has become a major trend.

In the process of collecting and analyzing the aforementioned list of internet hospitals, we have identified several issues that still need to be addressed.

First, the time limits for follow-up consultations vary across regions. For instance, Shanghai’s “Administrative Measures for Internet Hospitals in Shanghai” requires patients to provide medical records from in-person hospital visits within the past two months; Tianjin First Central Hospital and Fujian Provincial People’s Hospital both require visit documentation from within the past three months; and the Children’s Hospital of Chongqing Medical University requires medical records from within the past five months.

Most physical hospitals also require that initial consultation records be from their own institution, thereby limiting the integration of follow-up care medical resources with the internet to a finite scope and specific regions.

The standardization of initial diagnosis locations and follow-up visit timeframes urgently requires improvement at the policy level.

Secondly, while an increasing number of physical hospitals have launched internet hospital platforms, online operations are not their strong suit. The greater challenge lies in ensuring these platforms deliver tangible value after implementation, rather than being treated as mere top-down mandates. Furthermore, the rational allocation of these medical resources requires a holistic, coordinated approach.

As previously mentioned, many well-known tertiary Grade A hospitals have already established internet hospitals. Although policy incentives are gradually extending the reach of internet hospitals to secondary-level institutions, patients’ trust in tertiary Grade A hospitals is likely to persist over the long term. Given that follow-up consultations can be conducted online through these top-tier hospitals, why would patients choose anything else? In other words, the “siphon effect” exerted by tertiary Grade A hospitals on patients may become even stronger. This trend appears to run counter to the broader direction of tiered diagnosis and treatment.

Therefore, how can physical hospitals enhance the operational capabilities of their internet hospital platforms? How can healthcare resources at all levels be integrated through innovations in service models? These are not only challenges faced by physical hospitals and regulatory authorities but also issues worthy of deep reflection within the industry, as the existence of these problems precisely indicates where market demand lies.

Furthermore, will the widespread launch of internet hospitals by brick-and-mortar institutions lead to a significant exodus of physicians from platform-based internet hospitals? We believe that, given the finite time and energy of physicians, a zero-sum dynamic may indeed emerge. However, must “this” and “that” necessarily be antagonistic? Is it possible to foster robust collaboration and a healthy industry ecosystem? These are also avenues worthy of exploration.

Finally, it should be noted that we have devoted substantial effort to collecting the data presented in this article. While statistical limitations may introduce certain errors, we have strived to enhance accuracy by leveraging as many authoritative sources as possible (as outlined in the introduction of this article).

On the other hand, many believe that the internet healthcare industry is once again at a pivotal growth opportunity. However, we have no intention of following the trend, nor do we aim to encourage everyone to establish internet hospitals. Instead, we hope to foster more calm and rational reflection within the industry through more comprehensive data and rigorous analysis.

Moving forward, we will continue to monitor the progress of internet hospitals from additional perspectives to provide a more comprehensive analysis.